Revenue, 2025

$536.1Bn

Forecast, 2035

$1,025.5Bn

CAGR, 2025-2035

6.7%

Report Coverage

Global

Market Size and Forecast

2025

$536.1Bn

2035

$1,025.5Bn

CAGR

6.7%

The global Food Packaging Market reached USD 536.1 billion in 2025 and is expected to grow to USD 1,025.5 billion by 2035, registering a CAGR of 6.7% from 2025 to 2035. The growth of the market can be attributed to rising demand for packaged food, ready-to-eat meals, frozen food, dairy products, bakery items, snacks, and beverage packaging. Food packaging is also becoming more important in reducing spoilage, improving shelf life, supporting safe transport, and protecting food quality across retail and online delivery channels. Public food system data show that 13.2% of food is lost in the supply chain after harvest and before retail, while 19% is wasted at retail, food service, and household levels, which increases the need for better protective and sustainable packaging.

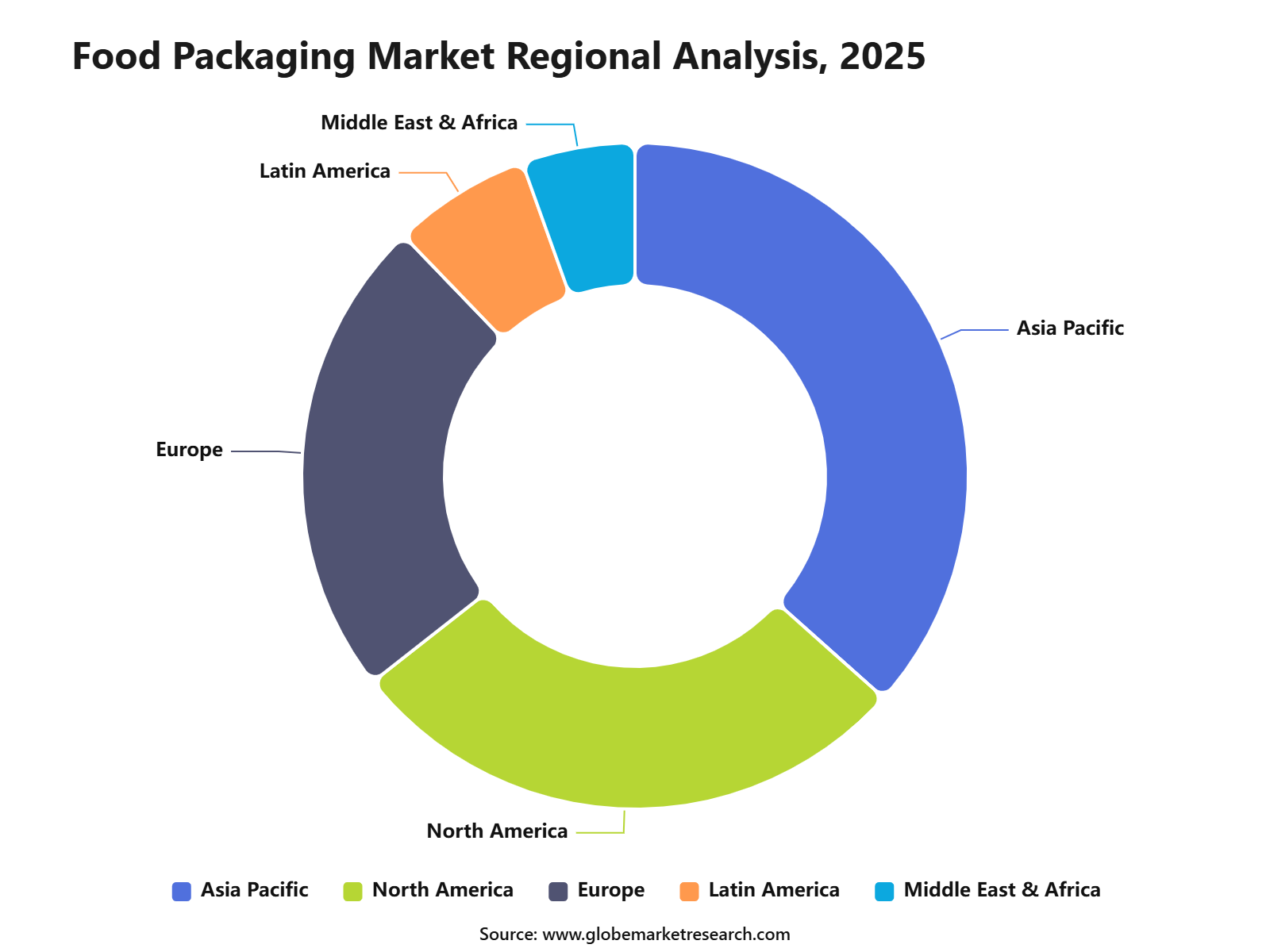

Asia Pacific held the largest regional share of 35.6% in 2025, supported by strong food production, rising urban population, higher packaged food consumption, and expanding modern retail across China, India, Japan, South Korea, and Southeast Asia. The region has more than 2.2 billion urban residents, and its urban population is projected to rise by 50% by 2050, which is expected to increase demand for convenient, portion-controlled, and transport-safe packaged food products. Growth is also supported by the expansion of food delivery platforms, supermarket chains, cold chain logistics, and e-commerce grocery channels.

Key Market Insights

Plastics led the material segment with 47.8% share, supported by low cost, durability, lightweight properties, and wide use across packaged food products.

Flexible packaging accounted for 54.3% share by product type, driven by rising demand for convenient, lightweight, and shelf-stable packaging formats.

Bags and pouches captured 30.1% share by packaging type, supported by easy handling, lower material use, resealability, and strong adoption in snacks, frozen food, and ready-to-eat products.

Bakery and confectionery held 40.8% share by application, driven by high consumption of packaged bakery items, chocolates, sweets, and snack products.

Frozen food accounted for 32.1% share by food type, supported by rising demand for convenient meals, longer shelf life, and cold-chain retail expansion.

Modified atmosphere packaging held 37.6% share by technology, driven by its ability to extend product freshness, reduce spoilage, and maintain food quality.

Food manufacturers led the distribution channel with 53.0% share, supported by large-scale packaging demand from processed food producers and packaged food brands.

Asia Pacific held 36.6% share of the food packaging market, supported by rising food consumption, urbanization, packaged food demand, and strong manufacturing capacity.

Market Overview

The food packaging market covers materials, formats, and systems used to protect food products from damage, contamination, spoilage, and quality loss during storage, transport, retail display, and consumption. It includes plastic, paper and paperboard, metal, glass, flexible films, trays, cartons, pouches, cans, bottles, wraps, and advanced packaging formats. The market is closely linked with food safety, shelf-life extension, branding, logistics efficiency, and consumer convenience. Its growth is supported by packaged food consumption, online grocery expansion, food delivery, frozen food demand, and stricter packaging safety rules.

The main growth driver for the food packaging market is the rising consumption of packaged, ready-to-eat, frozen, bakery, dairy, meat, seafood, and convenience food products. Urban consumers are demanding food that is safe, portable, easy to store, and suitable for quick preparation. Packaging helps food brands maintain hygiene, reduce handling risk, and improve product visibility across retail and e-commerce channels. This demand is especially strong in Asia Pacific, where population growth, urbanization, rising income, and modern retail expansion are increasing packaged food consumption.

The adoption of advanced food packaging technologies is increasing due to the need for longer shelf life, better product safety, reduced waste, and stronger supply chain visibility. Modified atmosphere packaging is being used to control oxygen and carbon dioxide levels inside packs, helping fresh food stay stable for longer periods. Smart labels, QR codes, freshness indicators, tamper-evident seals, and track-and-trace features are also gaining attention in premium packaged food and export-oriented supply chains. These technologies support both consumer trust and operational efficiency.

Sustainability & Environmental Impact

Sustainability has become a major priority in the food packaging market because packaging is one of the largest sources of plastic waste. Around 36% of all plastics produced are used in packaging, including single-use food and beverage containers, and nearly 85% of these containers end up in landfills or as mismanaged waste, according to UNEP. This has increased pressure on food brands, retailers, and packaging manufacturers to reduce virgin plastic use, improve recyclability, and shift toward paper-based, compostable, recyclable, and reusable packaging formats.

The environmental impact of food packaging is mainly linked to plastic waste, landfill pressure, marine pollution, carbon emissions, and low recycling rates. In the European Union, packaging accounts for 40% of plastics use, while half of marine litter comes from packaging, showing why stricter packaging rules are being introduced. The EU’s Packaging and Packaging Waste Regulation aims to make all packaging placed on the EU market recyclable in an economically viable way by 2030, while reducing the use of virgin materials and supporting a circular packaging system.

Consumer demand is also supporting the shift toward sustainable packaging. Despite weak recycling and reuse rates, consumers are showing a clear willingness to pay a small premium for packaging that is recyclable, compostable, or lower-impact. Nearly 50% of U.S. consumers and more than 70% of UK consumers have been reported as willing to pay an additional 1% to 3% for sustainable or compostable packaging. This willingness is important for food manufacturers because sustainable packaging often carries higher material, certification, compliance, and supply chain costs.

Go-to-Market and Sales Economics

The food packaging market is driven by a B2B sales model, where suppliers serve food manufacturers, beverage companies, frozen food brands, bakeries, dairy processors, quick-service restaurants, supermarkets, private-label retailers, and food delivery operators. Sales are mainly supported by direct contracts, distributor networks, customized packaging development, food-grade certifications, and long-term supply agreements. Buyers usually select suppliers based on cost per unit, material quality, safety compliance, printing capability, delivery reliability, and the ability to support large-volume production.

The sales economics of food packaging are shaped by raw material prices, resin and paperboard costs, energy expenses, labor, freight, printing, tooling, and packaging design complexity. Higher order volumes reduce per-unit cost, while advanced formats such as high-barrier films, modified atmosphere packaging, recyclable mono-material pouches, compostable trays, and tamper-evident containers often carry premium pricing. Demand remains strong because U.S. food spending reached USD 2.51 trillion in 2025, with food-away-from-home accounting for 56.3% of total food expenditure.

Packaging suppliers are also using sustainability and food-loss reduction as key sales arguments. Globally, 13.2% of food is lost after harvest and before retail, while another 19% is wasted at retail, food service, and household levels, making shelf-life protection an important value proposition. The EU Packaging and Packaging Waste Regulation will generally apply from August 2026, increasing pressure on food brands to adopt recyclable, reusable, and lower-waste packaging formats. As a result, suppliers with strong compliance support, sustainable materials, shorter lead times, and scalable production capacity are expected to gain stronger preference from food companies and retail buyers.

Material Analysis

Plastics led the material segment with 47.8% share, supported by their wide use in films, trays, containers, wraps, bottles, and pouches. The material is preferred in food packaging because it offers strong barrier protection, light weight, low cost, and easy shaping for different food formats. The growth of plastics in food packaging can be attributed to rising demand for packaged snacks, frozen meals, dairy products, bakery items, sauces, beverages, and ready-to-eat foods.

Plastic packaging also helps reduce breakage, improve transport efficiency, and protect food from moisture, oxygen, and contamination during storage and distribution. Sustainability has become a major factor in this segment, as packaging uses a large share of global plastic production. Food brands and packaging producers are increasing the use of recyclable plastics, mono-material films, post-consumer recycled content, and lighter packaging structures to meet retailer and regulatory expectations.

Product Type Analysis

Flexible packaging dominated the product type segment with 54.3% share, driven by strong demand from food manufacturers and retail brands. Flexible formats are widely used because they require less material than rigid packaging and can be designed for sealing, printing, portion control, and product protection. The segment is strongly supported by snacks, bakery products, frozen foods, dry foods, confectionery, sauces, pet food, and ready meals.

Its adoption is rising because flexible packaging improves shelf visibility, lowers transport weight, and supports convenient packaging features such as resealable closures and easy-tear openings. Flexible packaging also supports modern food distribution needs, especially where products move across long supply chains. The segment is benefiting from demand for lightweight packs, high-barrier films, recyclable structures, and packaging that can protect freshness while reducing storage and logistics costs.

Packaging Type Analysis

Bags and pouches accounted for 30.1% share, making them the leading packaging type in the food packaging market. Their use is high across snacks, frozen foods, bakery products, confectionery, dry mixes, coffee, grains, sauces, and ready-to-cook products. The growth of bags and pouches can be linked to their low material use, strong shelf appeal, easy storage, and suitability for both single-serve and family-size formats.

Stand-up pouches, flat pouches, zipper pouches, and vacuum bags are increasingly used by food companies to improve convenience and extend product shelf life. Demand is also rising because bags and pouches support online grocery, modern retail, and convenience-led consumption. Their lightweight structure helps reduce shipping weight, while improved barrier films help protect food from moisture, odor transfer, freezer burn, and oxygen exposure.

Application Analysis

Bakery and confectionery led the application segment with 40.8% share, supported by high consumption of bread, biscuits, cakes, cookies, chocolates, candies, and sweet snacks. These products require packaging that protects taste, texture, freshness, shape, and visual appeal during handling and retail display. The segment benefits from strong demand for packaged bakery and confectionery products across supermarkets, convenience stores, online grocery platforms, cafes, and foodservice channels.

Packaging plays an important role in portion packs, gift packs, resealable packs, and premium formats used for chocolates, cookies, cakes, and biscuits. The need for freshness protection remains high in bakery and confectionery packaging because many products are sensitive to moisture, oxygen, and temperature changes. As a result, producers are using barrier films, paper-based packs, cartons, flow wraps, and laminated structures to improve shelf life and reduce product damage.

Food Type Analysis

Frozen food held 32.1% share, supported by rising consumer demand for convenient meals, longer shelf life, and reduced food preparation time. Frozen vegetables, meat, seafood, snacks, desserts, ready meals, and bakery items require packaging that can perform well under low-temperature storage. Packaging demand in this segment is shaped by the need to prevent freezer burn, moisture loss, seal failure, and product contamination.

Films, trays, cartons, bags, and pouches used for frozen food must protect product quality during freezing, storage, transport, and retail display. The segment is also supported by the growth of cold-chain logistics and modern grocery retail. As frozen food consumption increases, food manufacturers are investing in durable, printable, and high-barrier packaging formats that can maintain product safety and support clear cooking, storage, and nutrition information.

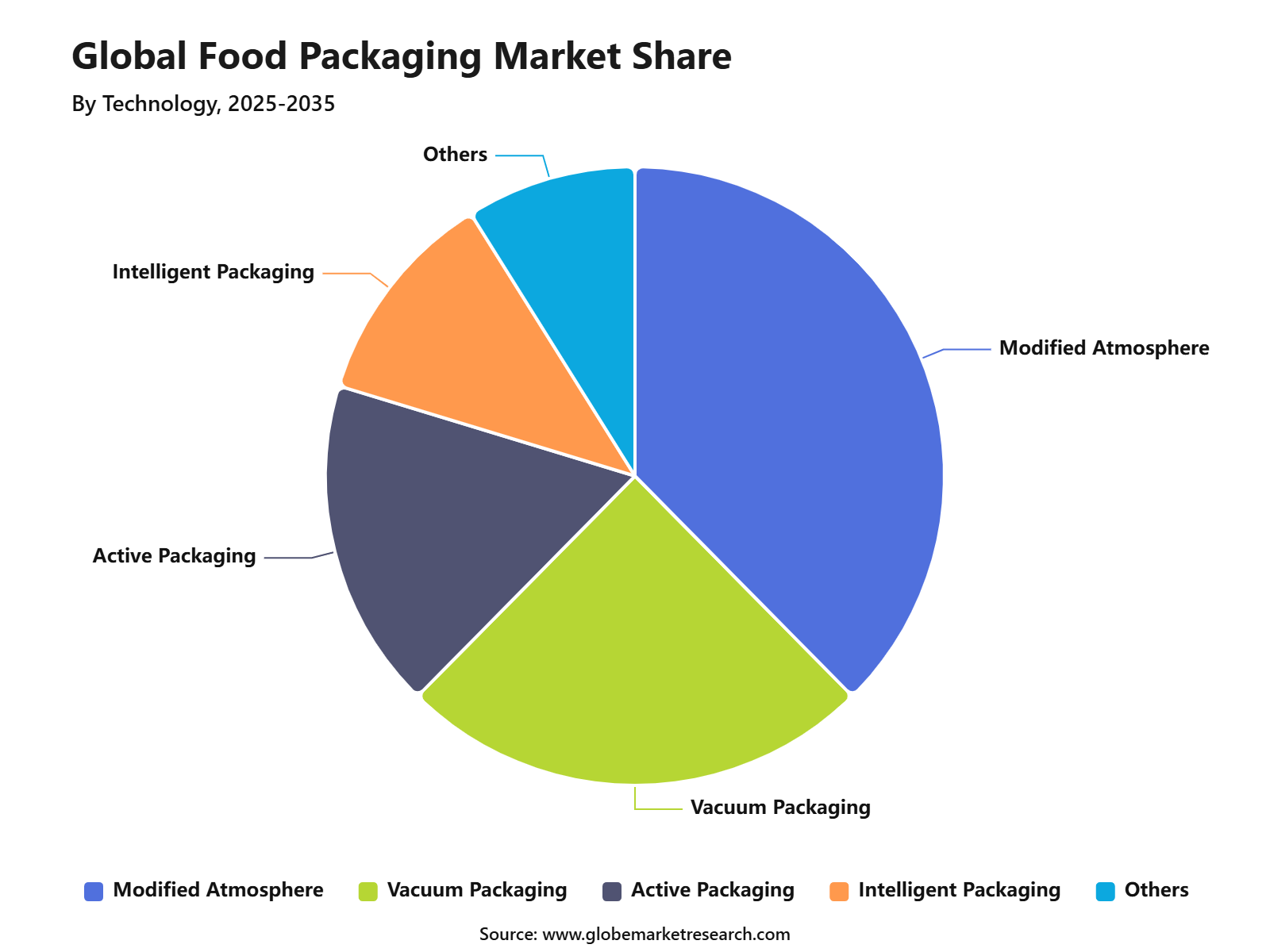

Technology Analysis

Modified atmosphere packaging led the technology segment with 37.6% share, supported by its strong use in fresh produce, meat, seafood, bakery, dairy, and ready-to-eat meals. The technology works by changing the gas mix inside the package to slow spoilage and preserve freshness. The demand for modified atmosphere packaging is rising because food producers are under pressure to reduce waste, extend shelf life, and improve product quality during distribution.

It is especially useful for products that are sensitive to oxygen, microbial growth, color changes, and texture loss. This technology also supports retailers by reducing product returns and improving inventory handling. As consumers look for fresher and safer packaged foods, modified atmosphere packaging is expected to remain important across chilled, fresh, and premium food categories.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFDistribution Channel Analysis

Food manufacturers led the distribution channel segment with 53.0% share, as packaging is mainly selected and purchased during the food production and processing stage. Manufacturers require packaging for filling, sealing, labeling, coding, storage, transport, and retail-ready presentation.

The segment is supported by the large-scale production of snacks, bakery products, dairy items, beverages, frozen meals, sauces, confectionery, and processed foods. Packaging is closely linked with production efficiency because it affects line speed, product safety, shelf life, branding, and compliance with food labeling rules.

Food manufacturers are also investing in packaging that supports automation, waste reduction, traceability, and supply chain performance. Demand is moving toward lightweight materials, recyclable formats, stronger seals, and packaging designs that reduce product loss during storage and transportation.

Regional Analysis

Asia Pacific led the food packaging market with 36.6% share, supported by strong food production, large consumer populations, urbanization, and rising demand for packaged and convenience foods. China, India, Japan, South Korea, Indonesia, Vietnam, and Thailand are key contributors to regional packaging demand.

The region benefits from the expansion of modern retail, online grocery, food delivery, quick-service restaurants, and organized food manufacturing. Packaged snacks, frozen foods, ready meals, bakery products, dairy products, sauces, and beverages are creating steady demand for flexible packaging, plastic containers, cartons, trays, and pouches.

Asia Pacific is also seeing stronger investment in sustainable packaging, recycling systems, paper-based formats, and high-barrier flexible packaging. As income levels improve and urban households spend more on packaged foods, the region is expected to remain a major growth center for food packaging.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFMarket Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Shift toward flexible packaging | +1.5% | Asia Pacific, North America, Europe | Supports lightweight formats. |

Growth of bags and pouches | +1.2% | Global | Improves convenience. |

Modified atmosphere packaging adoption | +1.1% | Meat, bakery, frozen food sectors | Extends shelf life. |

Paper-based packaging growth | +1.0% | Europe, North America, India | Supports plastic reduction. |

Premium and branded food packaging | +0.9% | U.S., Europe, China, Japan | Improves shelf appeal. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Packaging Manufacturers | +1.6% | Global | Expands production capacity. |

Food and Beverage Companies | +1.3% | Global | Drives packaging innovation. |

Private Equity Firms | +1.0% | North America, Europe, Asia Pacific | Supports business scaling. |

Sustainable Material Investors | +1.2% | Europe, U.S., Asia Pacific | Supports eco-friendly formats. |

Automation and Machinery Investors | +0.9% | Global | Improves packaging efficiency. |

Segments Covered in the Report

By Material

Plastic

Paper & Paperboard

Metal

Glass

Bioplastics

Others

By Product Type

Flexible Packaging

Rigid Packaging

Semi-Rigid Packaging

By Packaging Type

Bottles

Cans

Pouches

Boxes & Cartons

Trays

Cups & Tubs

Films & Wraps

Bags & Sachets

Others

By Application

Bakery & Confectionery

Dairy Products

Meat, Poultry & Seafood

Fruits & Vegetables

Ready-to-Eat Meals

Snacks

Sauces & Dressings

Beverages

Frozen Food

Others

By Food Type

Fresh Food

Frozen Food

Processed Food

Ready-to-Eat Food

Convenience Food

Baby Food

Pet Food

Others

By Technology

Modified Atmosphere Packaging

Vacuum Packaging

Active Packaging

Intelligent Packaging

Aseptic Packaging

Retort Packaging

Others

By Distribution Channel

Food Manufacturers

Retail Packaging

Foodservice Packaging

E-commerce Packaging

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for packaged food | +1.8% | Asia Pacific, North America, Europe | Drives packaging consumption. |

Growth in ready-to-eat meals | +1.5% | U.S., China, India, Japan, Europe | Supports convenience packaging. |

Expansion of food delivery and e-commerce | +1.3% | Global urban markets | Increases protective packaging use. |

Rising focus on food safety and shelf life | +1.2% | Global | Supports barrier packaging demand. |

Increasing demand for flexible packaging | +1.0% | Asia Pacific, Europe, North America | Improves cost efficiency. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Plastic waste regulations | -1.1% | Europe, North America, Asia Pacific | Pressures material choices. |

High cost of sustainable packaging | -0.9% | Global | Limits fast adoption. |

Volatility in raw material prices | -0.8% | Global | Affects production margins. |

Recycling infrastructure gaps | -0.7% | Emerging markets | Slows circular packaging growth. |

Strict food-contact compliance needs | -0.6% | U.S., Europe, Japan, China | Raises testing cost. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Sustainable and recyclable packaging | +1.6% | Europe, North America, Asia Pacific | Creates long-term growth. |

Growth in biodegradable materials | +1.3% | Europe, U.S., Japan, India | Supports eco-friendly demand. |

Expansion of frozen food packaging | +1.2% | North America, Europe, Asia Pacific | Drives cold-chain packaging. |

Smart and active packaging adoption | +1.0% | Developed markets | Improves freshness tracking. |

Demand from food manufacturers | +1.4% | Global | Supports bulk packaging use. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Balancing cost and sustainability | -0.9% | Global | Affects packaging decisions. |

Maintaining product freshness | -0.8% | Global | Requires advanced materials. |

Complex recycling of multi-layer packaging | -0.7% | Europe, North America, Asia Pacific | Limits circular use. |

Supply chain disruption risk | -0.6% | Global | Impacts packaging availability. |

Consumer concern over plastic use | -0.6% | Europe, North America, urban Asia | Reduces plastic preference. |

Recent Developments

May 2026 - Amcor launched recycle-ready polypropylene dip cups for dressings, condiments, and sauces. The solution is available in 10 sizes, ranging from 0.5 oz to 2.0 oz. It supports food brands shifting from traditional materials to recyclable packaging formats.

March 2026 - Just Eat Takeaway, Huhtamaki, and Xampla expanded plastic-free takeaway boxes across 10 European markets. The packaging uses Xampla’s plant-based Morro Coating and targets food delivery packaging. The rollout covers Austria, Belgium, Bulgaria, Switzerland, Germany, Italy, the Netherlands, Poland, Slovakia, and Spain.

February 2026 - Tetra Pak expanded its paper-based barrier packaging to high-speed A3/Speed filling lines in Asia. Maeil Dairies became the first producer to use the solution for soy milk. The line can produce up to 24,000 packages per hour, supporting scale-up of renewable beverage packaging.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 536.1 Bn |

Forecast Revenue (2035) | USD 1,025.5 Bn |

CAGR (2025-2035) | 6.7% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Material (Plastic, Paper & Paperboard, Metal, Glass, Bioplastics, Others), By Product Type (Flexible Packaging, Rigid Packaging, Semi-Rigid Packaging), By Packaging Type (Bottles, Cans, Pouches, Boxes & Cartons, Trays, and Others), By Application (Bakery & Confectionery, Dairy Products, Meat, Poultry & Seafood, Fruits & Vegetables, and Others), By Food Type (Fresh Food, Frozen Food, Processed Food, and Others), By Technology (Modified Atmosphere Packaging, Vacuum Packaging, Active Packaging, Intelligent Packaging and Others), By Distribution Channel (Food Manufacturers, Retail Packaging, Foodservice Packaging, E-commerce Packaging, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Amcor plc, Sealed Air Corporation, Mondi plc, Tetra Pak International S.A., Huhtamaki Oyj, Berry Global Group Inc., Sonoco Products Company, Smurfit Westrock plc, DS Smith plc, Crown Holdings Inc., Graphic Packaging Holding Company, Constantia Flexibles Group GmbH, Coveris Group, Silgan Holdings Inc., Winpak Ltd., ProAmpac Holdings Inc., UFlex Limited, WestRock Company, Ball Corporation, International Paper Company. |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali K. brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Packaging