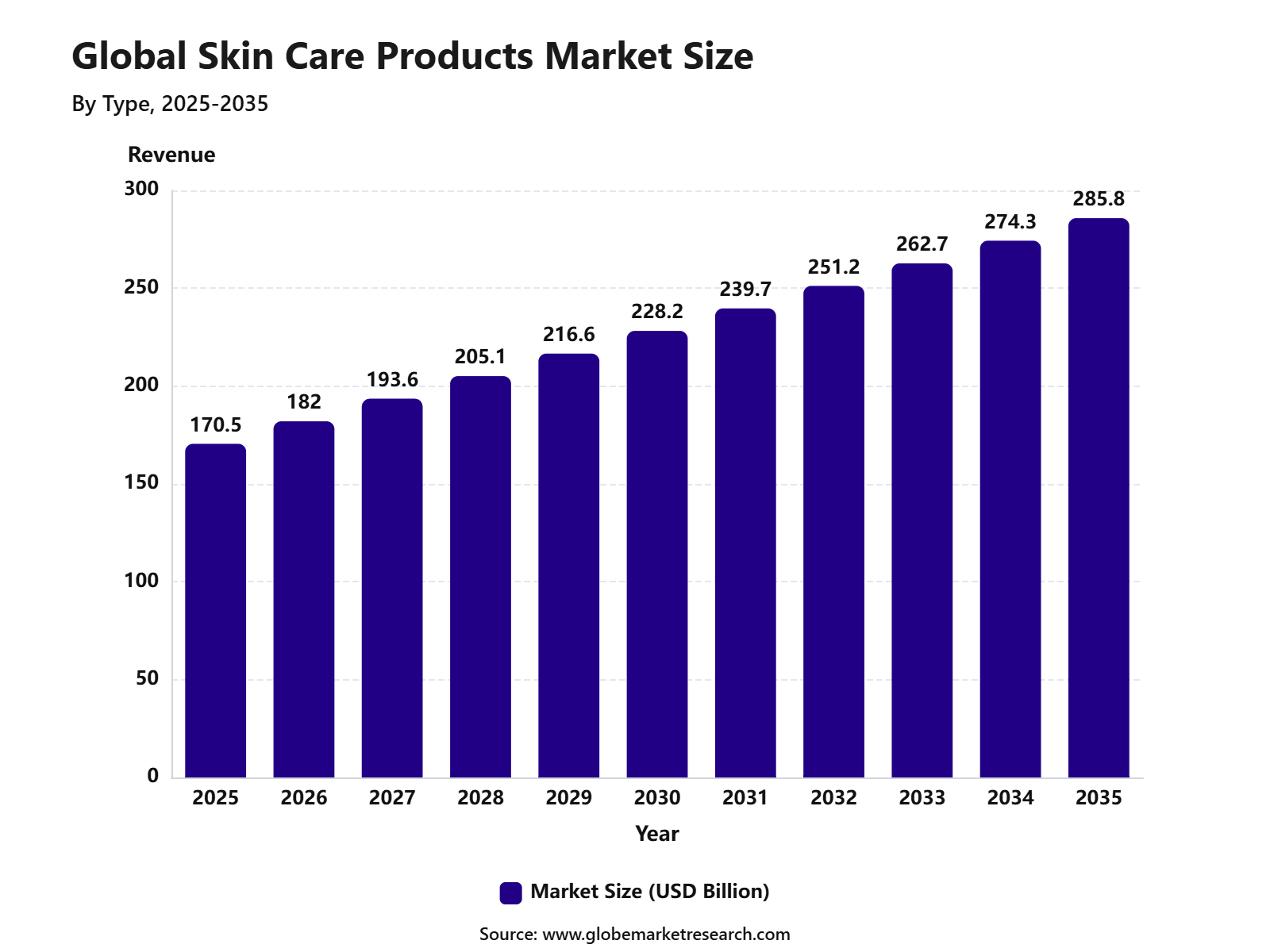

Revenue, 2025

$170.5Bn

Forecast, 2035

$285.8Bn

CAGR, 2025-2035

5.3%

Report Coverage

Global

Market Size and Forecast

The global skin care products market was valued at USD 170.5 billion in 2025 and is projected to reach USD 285.8 billion by 2035, growing at a CAGR of 5.3% during the forecast period. The growth of the market can be attributed to rising consumer focus on daily skin health, increasing use of moisturizers, cleansers, sunscreens, serums, anti-aging products, and growing demand for natural and dermatologist-tested formulations. The market is also being supported by higher beauty spending, expanding e-commerce access, social media-led product discovery, and rising awareness of preventive skin care among younger and working consumers.

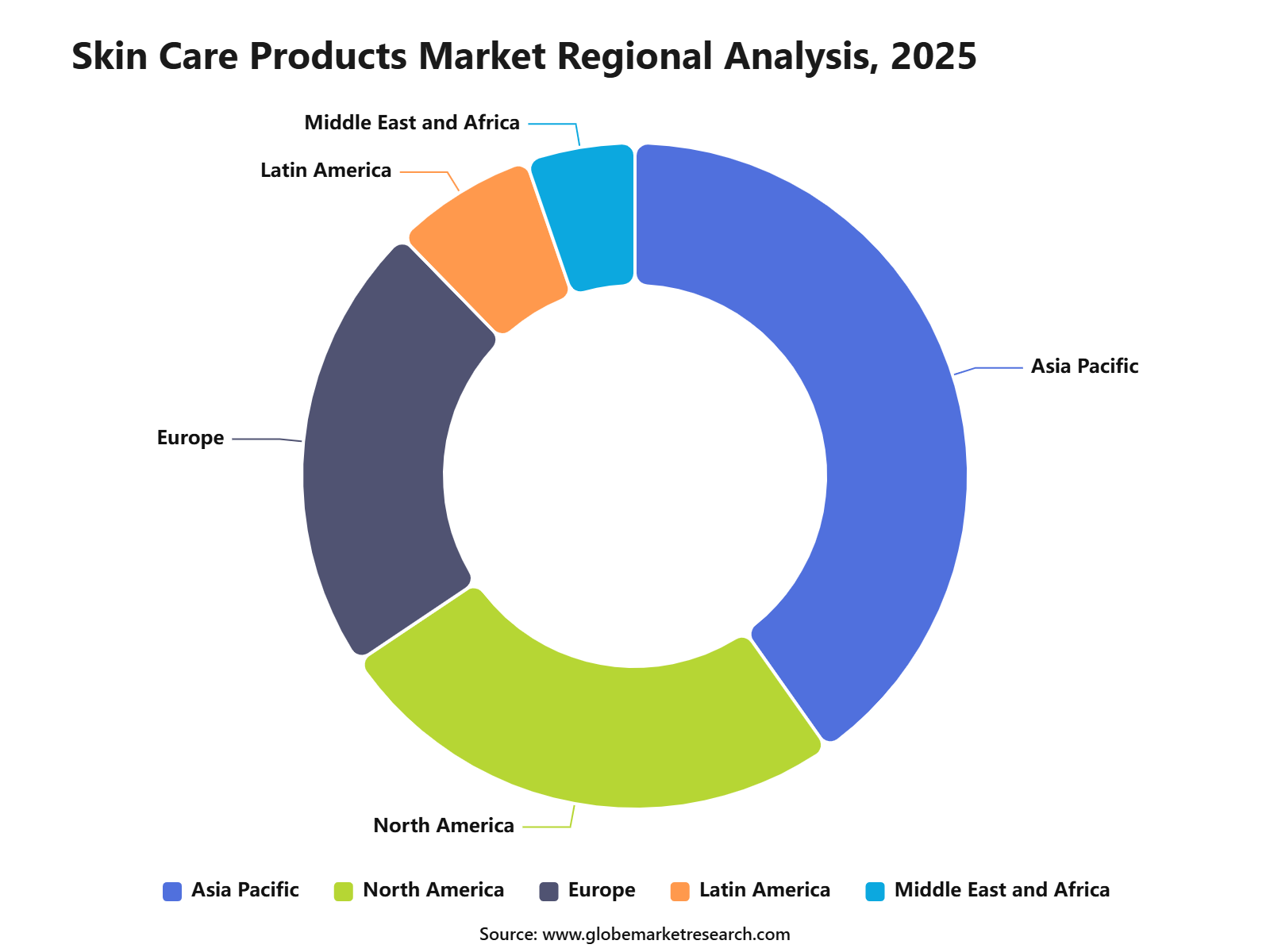

Asia Pacific held the leading regional share of 40.2% in 2025, valued at around USD 68.5 billion, supported by large consumer populations, strong beauty routines, rising disposable income, and high demand from countries such as China, India, Japan, and South Korea. The region is also benefiting from the popularity of K-beauty, clean-label products, sunscreen adoption, and online beauty platforms. Global beauty demand remains resilient, with the wider beauty market estimated at more than EUR 290 billion in 2024 and expanding by 4.5%, supported by innovation, personalized products, and emerging market growth.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Facial care led the market by type with 84.7% share, supported by daily use of cleansers, moisturizers, serums, toners, sunscreens, and anti-aging products.

Tubes accounted for 37.8% share by packaging, driven by ease of use, portability, controlled dispensing, and suitability for creams, gels, and lotions.

Face creams and moisturizers held 42.3% share by product, supported by strong demand for hydration, skin barrier repair, anti-aging care, and daily facial nourishment.

Supermarkets and hypermarkets captured 45.3% share by distribution channel, supported by wide product availability, competitive pricing, and strong consumer footfall.

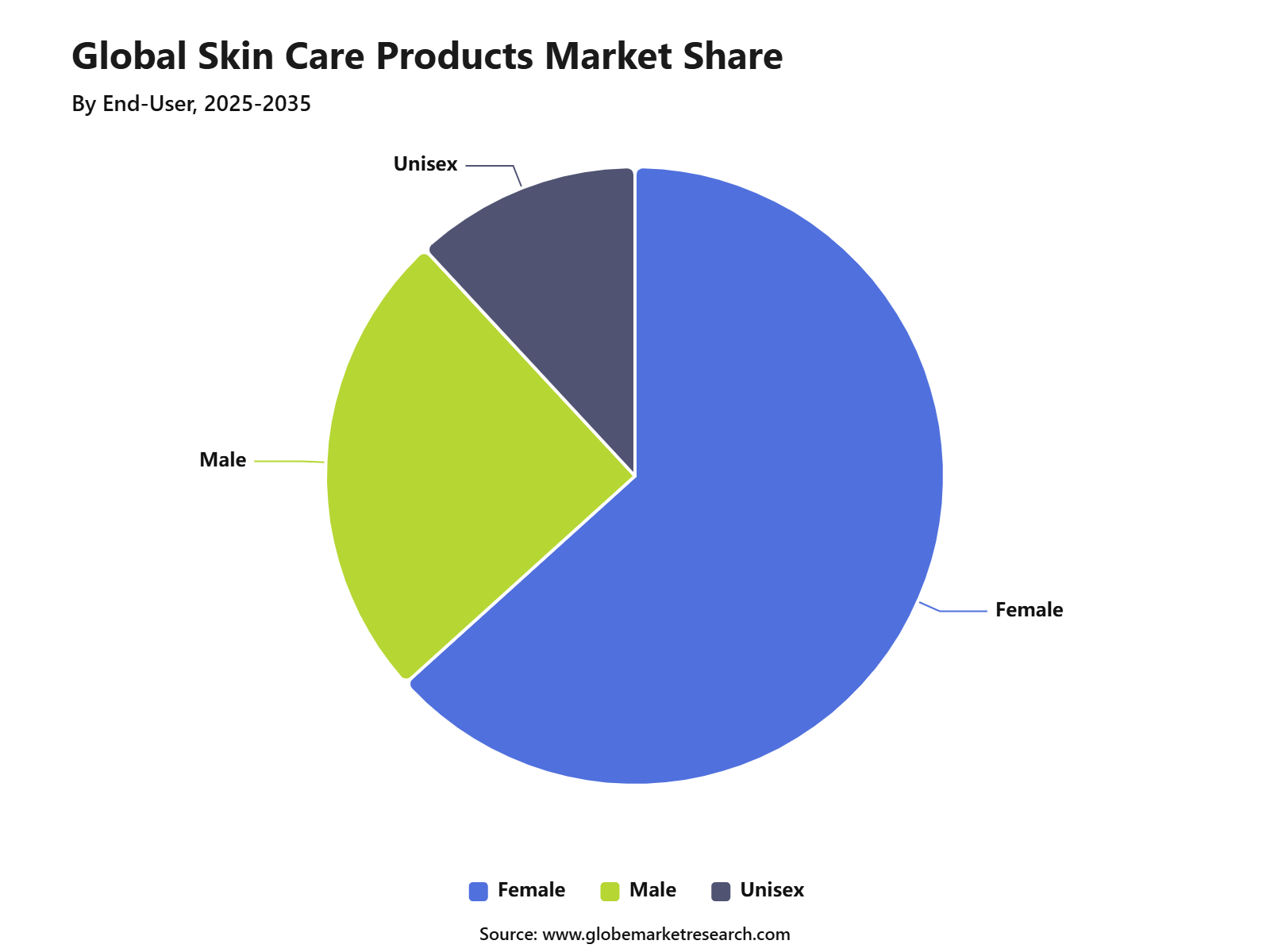

Female consumers represented 63.3% share, driven by higher usage across daily skincare routines, beauty care, sun protection, and premium product categories.

Mass skincare products held 69.6% share, supported by affordability, broad retail availability, and high demand from price-sensitive consumers.

Chemical-based ingredients accounted for 62.5% share, supported by their strong use in active formulations, preservatives, exfoliants, anti-aging products, and dermatology-tested skincare solutions.

Asia Pacific led the skin care products market with 40.2% share, supported by high beauty product consumption, rising disposable income, strong retail growth, and increasing awareness of daily skincare.

Market Overview

The growth of the Skin Care Products Market is being driven by rising consumer awareness about skin protection, aging signs, pollution exposure, and daily skin damage. Sunscreen, moisturizer, cleanser, and serum use is becoming more common as consumers understand the role of prevention in skin health. Demand is also increasing due to higher interest in acne care, pigmentation control, skin brightening, wrinkle reduction, and hydration support. This has created strong market potential for products that combine cosmetic benefits with visible skin care performance.

Demand in the Skin Care Products Market remains strong because skin care is a repeat-purchase category used across all age groups. Daily-use products such as cleansers, moisturizers, sunscreens, and body lotions generate steady volume demand, while serums, anti-aging creams, masks, and treatment products support premium growth. Consumers are also building multi-step routines that include cleansing, toning, treatment, hydration, and sun protection. This routine-based use pattern supports stable demand across both offline and online channels.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFType Analysis

Facial care led the type segment with 84.7% share in 2025, supported by daily use of cleansers, toners, serums, sunscreens, face masks, and moisturizers. The segment remains strong because facial skin concerns such as dryness, acne, dullness, pigmentation, sensitivity, and aging are common across different age groups. Consumers also tend to buy face care products more frequently because these items are part of regular morning and evening routines.

The growth of facial care can also be linked to higher awareness of skin health and prevention-based routines. Consumers are paying closer attention to hydration, sun protection, barrier repair, and ingredient suitability. Social media education and dermatologist-led content have also increased product knowledge. As a result, facial care remains the most active and highest-priority category in the Skin Care Products Market.

Packaging Analysis

Tubes held the leading packaging share of 37.8% in 2025, driven by convenience, hygiene, portability, and controlled product dispensing. Tube packaging is widely used for face creams, moisturizers, sunscreen, cleansers, gels, and lotions because it is easy to carry and simple to use. It also helps reduce direct hand contact with the remaining product, which supports better product handling than open jars.

The segment’s strength is also supported by its suitability for both mass and premium skincare products. Tubes are lightweight, cost-effective, shelf-friendly, and suitable for daily-use formulations. Brands also prefer tubes because they allow clear labeling, attractive design, and easy size variation. This makes tube packaging practical for consumers and efficient for manufacturers.

Products Analysis

Face creams and moisturizers led the product segment with 42.3% share in 2025, supported by their role in daily hydration, skin barrier care, and dryness prevention. These products are used across all age groups and skin types, including dry, oily, sensitive, combination, and normal skin. Their broad application makes them one of the most essential products in skincare routines.

Demand is also being supported by rising interest in barrier repair, lightweight hydration, anti-aging care, and multi-functional formulas. Consumers are increasingly choosing moisturizers with ingredients such as hyaluronic acid, ceramides, niacinamide, peptides, and SPF support. This has made face creams and moisturizers a repeat-purchase category with strong household penetration.

Distribution Channel Analysis

Supermarkets and hypermarkets led the distribution channel segment with 45.3% share in 2025, supported by easy product access, wide brand availability, and frequent household shopping visits. These outlets allow consumers to compare prices, pack sizes, ingredients, and product claims before purchase. The channel is especially strong for mass skincare products, daily-use moisturizers, cleansers, sunscreens, and body care items.

The segment also benefits from promotional offers, bundle packs, seasonal discounts, and strong shelf visibility. Many consumers still prefer buying skincare from physical stores because they can check labels, textures, packaging, and product suitability more confidently. While online beauty sales are growing, supermarkets and hypermarkets remain important for high-volume and affordable skincare purchases.

End-User Analysis

Female consumers held the leading end-user share of 63.3% in 2025, supported by higher usage frequency and broader product adoption across skincare routines. Women generally use a wider mix of products, including cleansers, moisturizers, sunscreens, serums, exfoliators, masks, eye creams, and anti-aging products. This creates stronger demand across both basic and advanced skincare categories.

The segment is also supported by beauty education, social media influence, professional skincare advice, and higher awareness of preventive skin care. Female consumers are more likely to follow structured routines and compare products based on ingredients, skin type, reviews, and visible results. This keeps women as the largest end-user group in the market.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFCategory Analysis

Mass skincare products dominated the category segment with 69.6% share in 2025, driven by affordability, wide availability, and daily-use demand. These products serve a broad consumer base because they offer basic skincare needs such as cleansing, moisturizing, sun protection, and body care at accessible price points. The segment is especially strong in supermarkets, pharmacies, hypermarkets, and general retail stores.

The growth of mass skincare is also supported by improved product quality and better ingredient communication. Many affordable brands now offer formulas focused on hydration, acne care, barrier repair, brightening, and sensitive skin. This has helped mass skincare move beyond basic products and reach consumers who want effective care without premium pricing.

Ingredient Analysis

Chemical-based skincare products held the leading ingredient share of 62.5% in 2025, supported by their wide use in moisturizers, sunscreens, acne products, exfoliants, anti-aging creams, and brightening formulas. Ingredients such as niacinamide, retinol, salicylic acid, glycolic acid, hyaluronic acid, peptides, and chemical UV filters are widely used because they can target specific skin concerns. This makes chemical formulations important for performance-focused skincare.

The segment remains strong because consumers are looking for visible results, tested claims, and targeted solutions. Chemical ingredients are commonly used to support hydration, texture improvement, oil control, wrinkle care, pigmentation reduction, and sun protection. However, demand is also becoming more selective as consumers pay closer attention to safety, skin sensitivity, and ingredient transparency.

Region Analysis

Asia Pacific held the leading regional share of 40.2% in 2025, supported by a large consumer base, strong beauty culture, rising income levels, and high interest in skincare routines. Countries such as China, India, Japan, South Korea, Indonesia, Vietnam, and Thailand have strong demand for facial care, sunscreen, moisturizers, brightening products, and anti-aging solutions. Skincare is also strongly influenced by local beauty traditions, K-beauty, J-beauty, and ingredient-led product innovation.

The region’s leadership is further supported by rapid digital adoption and social media-driven product discovery. Consumers across Asia Pacific are increasingly learning about skincare through short videos, influencers, e-commerce platforms, dermatology content, and product reviews. This has increased awareness of ingredients, skin types, and routine-based care. As a result, Asia Pacific remains the most dynamic regional market for skin care products.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFCustomer Acquisition Economics

According to NIQ, Customer acquisition in the skin care products market is driven by trust, proof of results, ingredient transparency, and repeat-purchase behavior. Skin care buyers usually compare products based on skin type, visible results, dermatologist support, reviews, price, safety claims, and before-and-after content. This makes acquisition more education-led than impulse-led, especially for serums, acne care, anti-aging products, sunscreen, sensitive-skin products, and barrier-repair creams.

Public retail data shows that beauty sales continued to grow in 2025, while online beauty sales expanded faster than store-based channels, indicating that digital discovery has become a major acquisition route for skin care brands. Digital acquisition economics are strongly supported by e-commerce and social commerce. Public industry data reported that 41% of U.S. beauty and personal care sales were driven by e-commerce, while social commerce influenced 68% of global beauty purchases. This means brands must invest in product education, creator content, reviews, video demonstrations, search visibility, and marketplace optimization.

Investment Opportunity Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Dermatology-backed skin care brands | +1.2% | North America, Europe, Asia Pacific | Builds premium trust. |

Natural and clean-label products | +1.1% | U.S., Europe, urban Asia | Supports brand differentiation. |

Personalized skin care platforms | +1.0% | Developed markets | Offers targeted growth. |

Men’s skin care products | +0.8% | U.S., China, India, Europe | Opens new demand. |

Online and D2C beauty channels | +0.9% | Global | Improves market reach. |

Risk Factors & Market Barriers

Regulatory & Compliance Risks

Regulatory risk is becoming a major operating barrier in the skin care products market because products can be classified differently based on claims, ingredients, and intended use. The FDA states that whether a product is a cosmetic or a drug is determined by intended use, and different regulations apply to each category. A moisturizer may be treated as a cosmetic when it is used to improve appearance, but sunscreen, acne treatment, skin protectants, skin bleaches, eczema products, and rosacea treatments may be regulated as drugs in the United States.

MoCRA has also increased compliance obligations for cosmetic companies operating in the U.S. market. Manufacturers and processors are required to register cosmetic product facilities with the FDA and renew registration every two years, while responsible persons must list cosmetic products, report serious adverse events, and maintain safety substantiation records. These requirements increase the cost of documentation, supplier control, adverse event tracking, and product launch planning. Smaller brands may face higher barriers because compliance systems, legal review, testing, and technical records require specialized support.

Claims management is another key risk area. The FTC requires companies to have proper substantiation for health-related product claims, and FDA has expressed concern about anti-aging and anti-wrinkle products marketed as cosmetics when claims suggest effects on the structure or function of the skin. This is important for products using terms such as repair, restore, regenerate, collagen boosting, anti-aging, acne clearing, scar reducing, or clinically proven. Brands that use strong performance language without adequate testing may face warning letters, legal action, product relabeling costs, and consumer trust loss.

Market Adoption Barriers

Market adoption barriers are high because skin care is closely linked to trust, visible results, irritation risk, and long-term routine behavior. Consumers often hesitate before trying a new product because skin reactions, acne flare-ups, dryness, redness, or sensitivity can damage confidence in the brand. Dermatology guidance shows that skin care choices must be adjusted by skin type, age, product order, and specific concerns, which makes consumer education important. Products with unclear usage steps or complex ingredient claims may face slower conversion.

Price sensitivity is another barrier because many consumers now compare premium and mass products more carefully before buying. Skin care routines often require several items, including cleanser, toner, serum, moisturizer, sunscreen, eye cream, acne care, exfoliant, and night treatment. When a brand asks consumers to buy a full routine at once, the first purchase cost can become high. Trial sizes, starter kits, refill packs, bundles, and sample-led discovery can reduce this barrier.

Trust barriers are especially strong in sensitive-skin, acne care, anti-aging, sunscreen, and hyperpigmentation products. Consumers are more likely to seek dermatologist-backed information, clinical testing, transparent ingredient lists, fragrance disclosure, non-comedogenic positioning, and safety support before switching. Products that overpromise fast results may attract first-time attention but can face weak repeat purchase if claims are not matched by visible performance. Long-term adoption is stronger when products are easy to use, safe for daily routines, and supported by credible evidence.

Segments Covered in the Report

By Type

Facial Care

Body Care

Lip Care

By Packaging

Tubes

Bottles

Jars

Others

By Products

Face Creams & Moisturizers

Cleansers & Face Wash

Sunscreen

Body Creams & Moisturizers

Shaving Lotions & Creams

Face Masks

Others

By Distribution Channel

Supermarkets & Hypermarkets

Convenience Stores

Pharmacy & Drugstore

Online

Others

By End-User

Female

Male

Unisex

By Category

Premium Skincare Products

Mass Skincare Products

By Ingredient

Chemical

Natural

By Region

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa (MEA)

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising consumer focus on skin health | +1.5% | North America, Europe, Asia Pacific | Drives daily product use. |

Growth in anti-aging product demand | +1.2% | U.S., Europe, Japan, South Korea | Supports premium sales. |

Increasing adoption of sun protection products | +1.0% | Global | Expands preventive care. |

Rising demand for natural and clean-label products | +0.9% | North America, Europe, urban Asia | Builds premium growth. |

Expansion of online beauty retail | +0.8% | Global | Improves product access. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High price of premium products | -0.8% | Emerging markets and mass consumers | Limits premium adoption. |

Skin sensitivity and allergy concerns | -0.7% | Global | Affects product trust. |

Strong competition among brands | -0.6% | Global | Pressures margins. |

Regulatory checks on ingredients | -0.5% | U.S., Europe, Asia Pacific | Raises compliance cost. |

Counterfeit beauty products | -0.4% | Asia Pacific, Latin America, online channels | Reduces brand confidence. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in personalized skin care | +1.3% | North America, Europe, developed Asia | Supports targeted products. |

Expansion of men’s skin care | +1.1% | U.S., Europe, China, India | Creates new demand. |

Demand for dermatology-backed products | +1.0% | Global | Builds consumer trust. |

Growth in premium and luxury skin care | +0.9% | U.S., Europe, China, GCC | Improves revenue value. |

Rising demand in emerging economies | +0.8% | India, Brazil, Indonesia, Africa | Expands volume growth. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Fast-changing beauty trends | -0.7% | Global | Requires frequent innovation. |

Product claims and efficacy concerns | -0.6% | Global | Affects repeat purchases. |

Supply chain pressure for natural ingredients | -0.5% | Global | Increases sourcing risk. |

Sustainability pressure on packaging | -0.5% | Europe, North America | Raises reformulation needs. |

Price competition in mass retail | -0.4% | Global | Reduces margin strength. |

Recent Developments

May 2026 - Olay, owned by Procter & Gamble, expanded its skin longevity positioning through its "Skinsurance" campaign. The brand promoted its Super Collection as a long-term skin care investment focused on wrinkles, dryness, dullness, elasticity, and uneven tone. Olay also highlighted its position as the No. 1 anti-aging skincare brand.

March 2026 - Estée Lauder Companies agreed to acquire full ownership of Forest Essentials, an Indian luxury Ayurvedic skincare brand. The company had first invested in the brand in 2008 and increased its stake to 49% in 2020. Financial terms were not disclosed, and the deal is expected to close in the second half of 2026.

March 2026 - Beiersdorf committed EUR 100 million to its second-generation Skin Care Innovation Fund. The fund will support investments and strategic partnerships in life sciences, sustainability, AI, and digital health linked to skin care innovation.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 170.5 Bn |

Forecast Revenue (2035) | USD 285.8 Bn |

CAGR (2025-2035) | 5.3% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Type (Facial Care, Body Care, Lip Care), By Packaging (Tubes, Bottles, Jars, Others), By Products (Face Creams & Moisturizers, Cleansers & Face Wash, Sunscreen, Body Creams & Moisturizers, and Others), By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, and Others), By End-User (Female, Male, Unisex), By Category (Premium Skincare Products, Mass Skincare Products), By Ingredient (Chemical, Natural) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Colgate-Palmolive Company, L'Oreal S.A., Procter & Gamble, Unilever, Coty Inc., Shiseido Co. Ltd, Avon Products Inc., Revlon, Beiersdorf AG, Johnson & Johnson Inc. |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

L'Oreal S.A.

Colgate-Palmolive Company

Procter & Gamble

Unilever

Coty Inc.

Shiseido Co. Ltd

Avon Products Inc.

Revlon

Beiersdorf AG

Johnson & Johnson Inc.

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Healthcare and Pharmaceuticals

US Medical Devices Market to hit USD 407.6 billion by 2035

US Medical Devices Market Size, Go-to-Market Strategy Analysis By Device Type (In Vitro Diagnostics (IVD), Diagnostic Imaging, Cardiovascular Devices, Orthopedic Devices, Surgical Devices, Patient Monitoring Devices, Others), By Application (Cardiology, Diagnostic Imaging, Orthopedics, Neurology, In Vitro Diagnostics, Others), By End User (Hospitals and Clinics, Ambulatory Surgical Centers, Diagnostic Laboratories, Home Healthcare, Others), By Technology (Conventional Devices, Connected Medical Devices, AI-Enabled Medical Devices, Robotic-Assisted Devices), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Biohacking Market to Exceed USD 231.3 Billion by 2035

Global Biohacking Market Size, Share Analysis Report By Product Type (Wearable Devices, Smart Implants, Gene-Editing Kits, Nootropics & Supplements, Sensors & Biomonitoring Patches, Others), By Biohacking Type (Nutrigenomics, DIY Biology, Grinder, and Others), By End User (Consumers, Healthcare Facilities, and Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Telemedicine Market to Exceed USD 981.6 Billion by 2035

Global Telemedicine Market Size, Share Analysis Report By Modality (Synchronous, Asynchronous, Remote Patient Monitoring), By Component (Software Platforms, Hardware & Peripherals, Services), By End User (Healthcare Providers, Payers & Employers, Patients / Home Users, Government Agencies & NGOs), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Helicobacter Pylori Diagnostics Market to hit 4.6 Bn by 2035

Global Helicobacter Pylori Diagnostics Market Size and Trade Analysis Report By Product Type (Instruments, Services, and Reagents), By Application (Immunoassays, Molecular Diagnostics, and Point-of-Care (POC)), By End User (Hospitals, Diagnostic Laboratories, and Clinics), By Regional Insights, Leading Companies and Growth Forecasts by 2025-2035