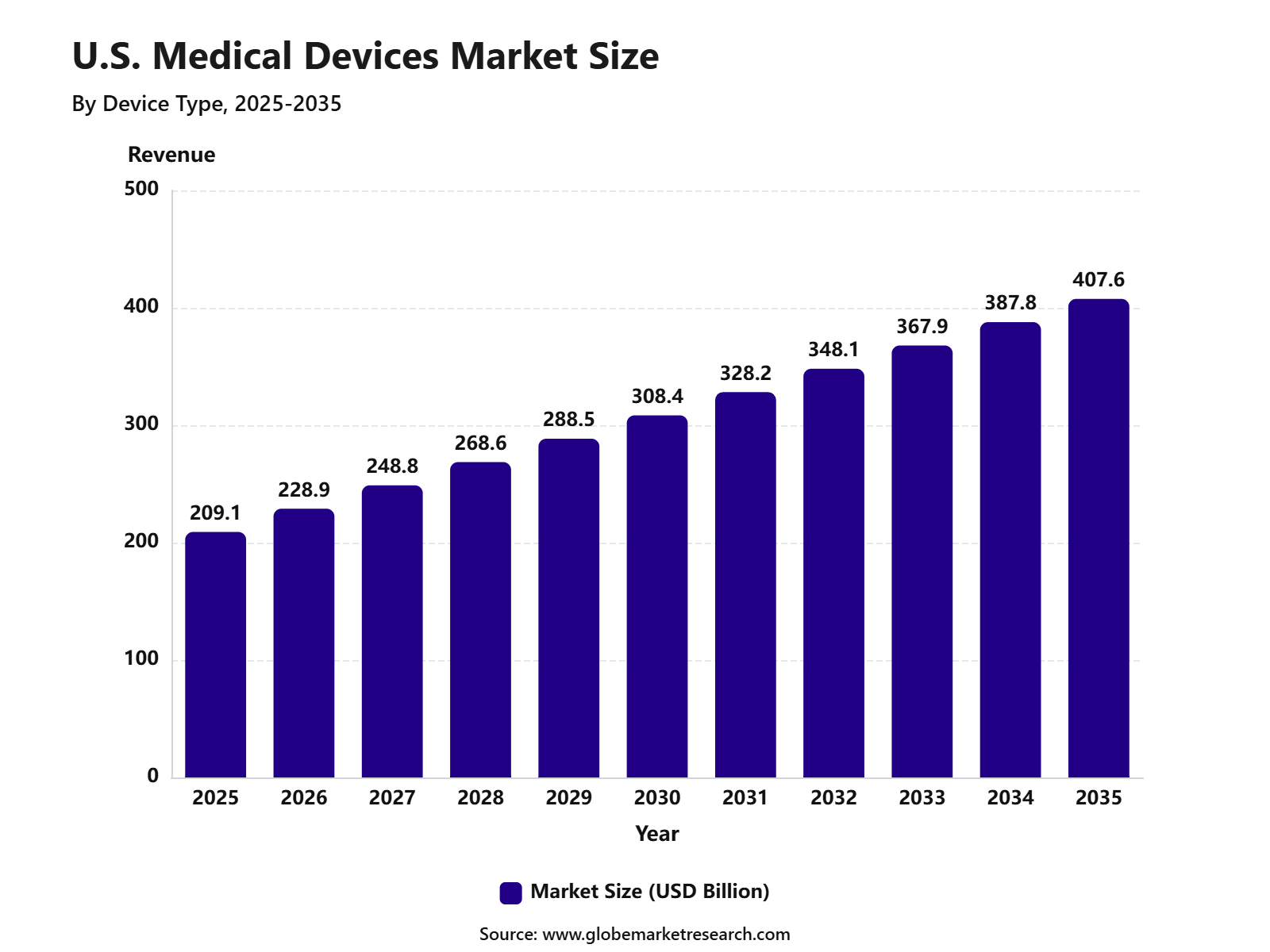

Revenue, 2025

$209.1Bn

Forecast, 2035

$407.6Bn

CAGR, 2025-2035

6.9%

Report Coverage

US

Market Size and Forecast

The U.S. Medical Devices Market was valued at USD 209.1 billion in 2025 and is projected to reach USD 407.6 billion by 2035, growing at a CAGR of 6.9% from 2025 to 2035. Growth in the market is supported by advanced healthcare infrastructure, high medical spending, strong adoption of minimally invasive procedures, and continuous innovation in diagnostic, surgical, cardiovascular, orthopedic, and patient monitoring devices.

Medical devices include instruments, equipment, implants, software, and digital health tools used for diagnosis, treatment, monitoring, and disease management. The growth of the U.S. medical devices market can be attributed to the rising burden of chronic diseases, increasing elderly population, growing demand for home healthcare, and wider use of connected medical technologies. Hospitals, ambulatory surgical centers, diagnostic laboratories, and specialty clinics are increasing the use of advanced devices to improve clinical outcomes and operational efficiency.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market outlook remains strong as manufacturers focus on AI-enabled diagnostics, wearable medical devices, robotic surgery systems, remote patient monitoring, and next-generation implantable devices. Demand is expected to rise for products that support faster diagnosis, improved patient safety, lower hospital stays, and personalized care. The U.S. is expected to remain a major medical device market due to strong research activity, established reimbursement systems, high technology adoption, and the presence of leading global medical device companies.

Key Market Insights

In vitro diagnostics led the device type segment with 19.9% share, supported by strong demand for laboratory testing, disease screening, point-of-care diagnostics, and routine clinical decision-making.

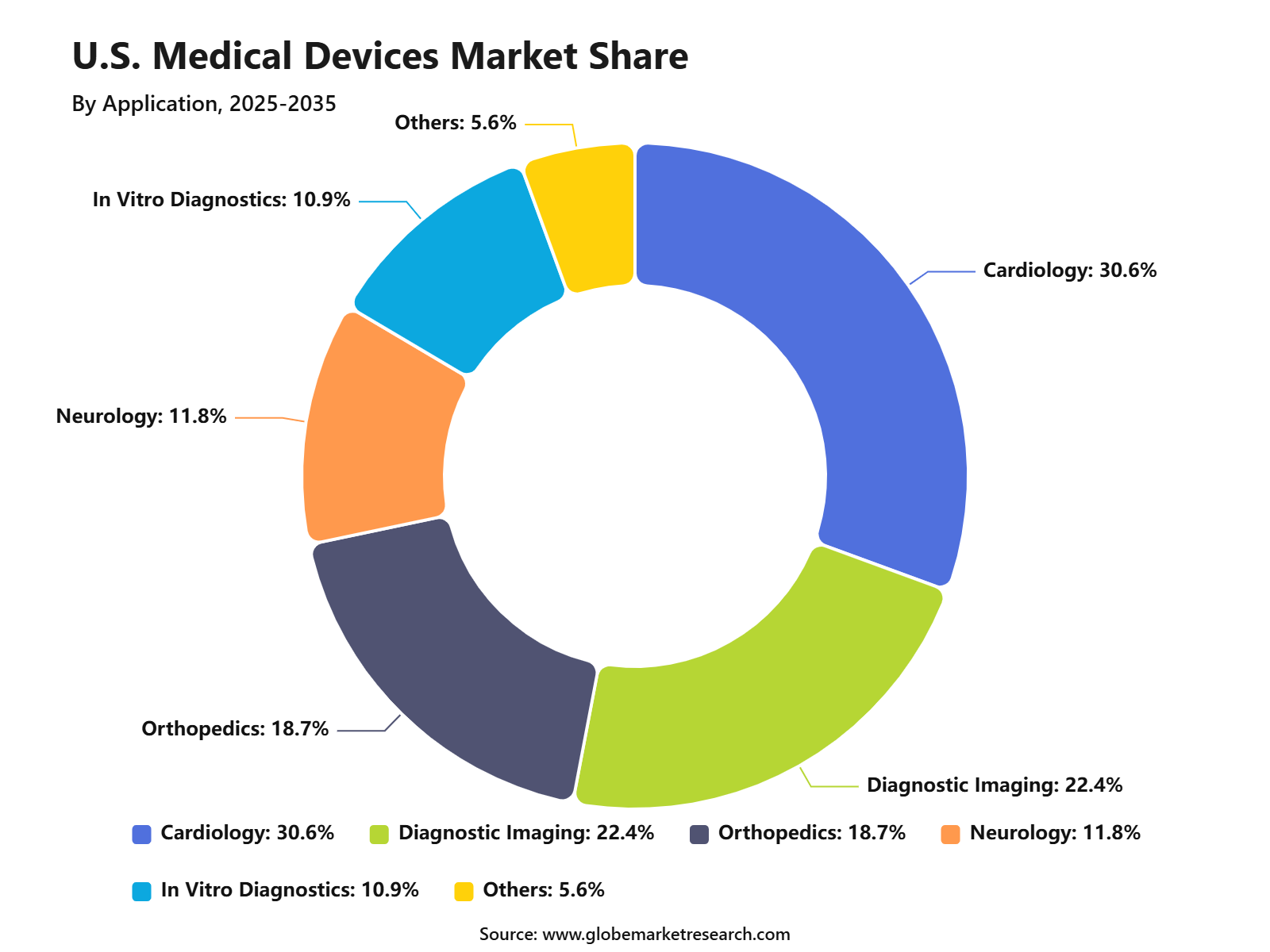

Cardiology accounted for 30.6% share by application, driven by high prevalence of heart-related conditions, rising diagnostic procedures, and continued use of monitoring and treatment devices.

Hospitals and clinics held 56.4% share by end user, supported by high patient volume, advanced medical infrastructure, and wide use of diagnostic, surgical, and therapeutic devices.

Conventional devices dominated the technology segment with 68.8% share, driven by broad clinical acceptance, established regulatory pathways, lower implementation complexity, and reliable use across healthcare settings.

Go-to-Market and Sales Strategy

The U.S. Medical Devices Market needs a care-pathway-led go-to-market strategy because hospitals, clinics, ambulatory surgery centers, diagnostic laboratories, home healthcare providers, and payers buy devices based on clinical value, workflow fit, safety, reimbursement, and total cost of care. Suppliers should position products around measurable outcomes such as faster diagnosis, shorter procedure time, lower readmissions, better patient monitoring, improved surgical precision, and reduced staff burden.

U.S. health care spending reached USD 5.3 trillion in 2024, or USD 15,474 per person, and accounted for 18.0% of GDP, showing the scale of the healthcare system in which medical devices are used. Sales economics are strongest when device companies combine hardware with software, service, training, consumables, data integration, and clinical support.

The commercial model is shifting from one-time capital equipment sales toward installed-base revenue, service contracts, disposable accessories, remote monitoring, AI-enabled workflow tools, and value-based purchasing support. FDA’s CDRH authorized 124 novel medical devices in 2025, including the first blood test to diagnose Alzheimer’s disease, while 44 breakthrough devices received marketing authorization in the same year.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFDevice Type Analysis

In vitro diagnostics led the U.S. Medical Devices Market by device type with 19.9% share, supported by their wide use in disease detection, patient screening, treatment monitoring, and clinical decision-making. IVD products include diagnostic tests, reagents, instruments, and systems used to examine blood, tissue, urine, and other human samples outside the body. The growth of this segment can be attributed to rising demand for early diagnosis, chronic disease monitoring, infectious disease testing, cancer screening, and routine laboratory testing.

Hospitals, diagnostic laboratories, clinics, and point-of-care settings continue to rely on IVD products to support faster and more accurate patient care. IVD demand is expected to remain strong as healthcare providers focus on preventive care and precision medicine. The segment is also being supported by advances in molecular diagnostics, immunoassays, companion diagnostics, point-of-care testing, and automated laboratory systems.

Application Analysis

Cardiology accounted for 30.6% share of the U.S. Medical Devices Market, supported by the high burden of heart disease and the need for continuous diagnosis, monitoring, treatment, and intervention. Cardiology devices include ECG systems, pacemakers, stents, defibrillators, heart valves, cardiac monitors, catheters, and imaging-support systems. The dominance of this segment can be linked to the high prevalence of cardiovascular conditions such as coronary artery disease, heart failure, arrhythmia, hypertension, and stroke-related risks.

Strong demand is also supported by aging population, lifestyle-related disease burden, and growing use of minimally invasive cardiac procedures. Cardiology is expected to remain a major application area as hospitals and clinics invest in advanced cardiac care. Demand is likely to remain strong for remote cardiac monitoring, implantable devices, interventional cardiology products, electrophysiology systems, and AI-supported cardiac diagnostics.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFEnd User Analysis

Hospitals and clinics led the end-user segment with 56.4% share, supported by high patient volumes, broad treatment capacity, and strong use of diagnostic, surgical, monitoring, and therapeutic devices. These facilities remain the primary users of medical devices because they handle emergency care, inpatient treatment, outpatient procedures, diagnostic testing, and specialty care.

The growth of this segment can be attributed to rising procedure volumes, hospital infrastructure upgrades, and increasing demand for connected healthcare systems. Hospitals and clinics require medical devices for imaging, diagnostics, cardiology, orthopedics, respiratory care, surgery, critical care, and patient monitoring.

Hospitals and clinics are expected to remain the leading end-user group due to their central role in U.S. healthcare delivery. Future demand will be supported by digital health integration, minimally invasive procedures, advanced diagnostics, remote monitoring, and higher investment in patient safety and workflow efficiency.

Technology Analysis

Conventional devices held 68.8% share of the U.S. Medical Devices Market, supported by their established clinical use, broad availability, proven reliability, and strong adoption across hospitals and clinics. These devices include standard diagnostic tools, surgical instruments, monitoring systems, implants, consumables, and therapy equipment used in routine care. The segment remains dominant because many healthcare procedures still depend on trusted and widely adopted device technologies.

Conventional devices are preferred where clinical familiarity, regulatory acceptance, cost efficiency, and consistent performance are important for daily medical practice. Conventional devices are expected to maintain a strong position, even as digital, robotic, connected, and AI-enabled devices continue to expand. Demand will remain steady because hospitals and clinics need reliable core equipment for diagnostics, surgery, patient monitoring, emergency care, and chronic disease management.

Risk Factors & Market Barriers

The main risk factor is supply-chain dependence. The American Hospital Association stated that the U.S. imported more than USD 75 billion in medical devices and supplies in 2024, while FDA estimates cited by AHA indicate that about 62% of medical devices used in the U.S. are imported. This creates exposure to tariffs, shipping disruption, overseas manufacturing delays, quality issues, and country-specific trade restrictions.

Another barrier is product quality and recall risk. Medical devices are used in high-risk clinical settings, So any defect can affect patient safety, hospital operations, and brand trust. FDA continues to maintain an up-to-date medical device shortage list, and its latest update extended the shortage of stereotactic breast biopsy needles to Q1 2027 while also adding discontinuances reported since March 2026. This shows that supply continuity remains a real market barrier, especially for specialized and procedure-critical devices.

Regulatory & Compliance Risks

Regulatory compliance is a major cost and timing factor in the U.S. Medical Devices Market. Device makers must manage FDA classification, premarket submissions, quality systems, labeling, clinical evidence, post-market surveillance, adverse event reporting, recalls, cybersecurity, and manufacturing controls. FDA’s current medical device user fee schedule lists standard fees of USD 26,067 for a 510(k), USD 173,782 for a De Novo request, and USD 579,272 for a PMA, PDP, PMR, or BLA submission. These fees show why regulatory planning is an important part of product economics, especially for smaller companies.

Cybersecurity compliance is becoming more important as devices become connected to hospital networks, cloud systems, mobile apps, and other devices. FDA issued final cybersecurity guidance on June 27, 2025, covering quality system considerations and the content expected in premarket submissions for devices with cybersecurity risk. FDA states that connected medical devices can improve care, but the same connectivity can increase cybersecurity risks that may affect device safety and effectiveness.

Market Adoption Barriers

Market adoption barriers are mainly linked to hospital budgets, reimbursement uncertainty, physician training, clinical evidence, workflow disruption, and purchasing committee approval. Hospitals do not adopt new devices only because they are innovative. They require proof that the device improves outcomes, reduces cost, fits existing workflows, and can be supported by trained staff. This is especially important for surgical robots, AI-enabled diagnostics, remote monitoring tools, connected implants, and advanced imaging systems.

AI-enabled devices face a special adoption barrier because buyers need confidence in safety, accuracy, bias control, cybersecurity, and clinical responsibility. FDA maintains an AI-enabled medical device list to identify devices authorized for marketing in the U.S., and it states that the list is intended to improve transparency for innovators, providers, and patients. Reuters reported in February 2026 that at least 1,357 FDA-authorized medical devices used AI, but also highlighted safety concerns around adverse events and recalls, showing that adoption will depend on strong validation and post-market monitoring.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape is spread across in vitro diagnostics, diagnostic imaging, cardiovascular devices, orthopedic implants, surgical instruments, patient monitoring, diabetes care, wound care, neurology devices, respiratory care, dialysis products, dental devices, home healthcare equipment, and digital health tools. Hospitals and health systems remain core buyers, but outpatient centers, diagnostic laboratories, physician offices, and home healthcare channels are becoming more important as care shifts outside traditional inpatient settings. This supports demand for portable, connected, easy-to-use, and lower-maintenance devices.

Advanced technology categories are expanding the revenue landscape. AI-enabled imaging, remote patient monitoring, robotic-assisted surgery, connected wearables, point-of-care diagnostics, and software as a medical device can create recurring revenue through subscriptions, upgrades, data services, and service contracts. FDA’s 2025 CDRH annual report also highlights digital health actions, including AI lifecycle management guidance work, the Regulatory Accelerator, and the TEMPO pilot for digital health devices, which shows that regulatory infrastructure is evolving alongside technology adoption.

Financial Impact

The financial impact can be positive for companies that combine clinical differentiation with strong reimbursement, service revenue, consumables, and installed-base expansion. Device companies with recurring sales from catheters, sensors, test cartridges, implants, surgical tools, monitoring accessories, software subscriptions, and maintenance contracts can create more stable revenue than companies relying only on capital equipment purchases. A strong financial model should include regulatory cost, clinical evidence cost, hospital sales cycle length, training cost, and post-market support.

Financial risk remains linked to tariffs, recalls, cybersecurity, reimbursement pressure, hospital budget constraints, and imported-supply dependence. Tariff exposure can raise input costs, while quality issues can trigger warning letters, recalls, customer loss, and legal claims. The strongest financial resilience is expected from companies with diversified manufacturing, FDA-ready quality systems, strong cybersecurity documentation, differentiated clinical evidence, and contracts that protect margins when tariff or component costs rise.

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for advanced healthcare devices | +1.8% | U.S. hospitals and specialty clinics | Drives device adoption. |

Growth in chronic disease management | +1.5% | U.S. healthcare system | Supports monitoring devices. |

Increasing use of minimally invasive procedures | +1.3% | Surgical centers and hospitals | Expands procedural device use. |

Aging population and higher care needs | +1.1% | Nationwide | Raises diagnostic demand. |

Strong healthcare technology innovation | +1.0% | U.S. medtech hubs | Supports premium devices. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High device development cost | -0.9% | U.S. manufacturers | Raises pricing pressure. |

Strict regulatory approval process | -0.8% | FDA-regulated market | Delays product launches. |

Reimbursement uncertainty | -0.7% | Hospitals and outpatient centers | Affects purchasing decisions. |

Cybersecurity risks in connected devices | -0.6% | Digital health and hospital systems | Raises compliance burden. |

Supply chain pressure for components | -0.5% | U.S. and global suppliers | Impacts device availability. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in wearable medical devices | +1.6% | U.S. consumer and clinical markets | Supports remote care. |

Expansion of home healthcare devices | +1.4% | Aging and chronic care population | Reduces hospital visits. |

Rising demand for robotic surgery systems | +1.2% | Large hospitals and surgical centers | Improves procedure precision. |

AI-enabled diagnostics and imaging | +1.1% | U.S. hospitals and imaging centers | Enhances clinical decisions. |

Remote patient monitoring adoption | +1.0% | Chronic disease care programs | Builds recurring demand. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Managing product safety and recalls | -0.8% | U.S. medical device companies | Affects brand trust. |

Integration with hospital IT systems | -0.7% | Hospitals and health networks | Slows digital adoption. |

Pricing pressure from buyers | -0.6% | Hospitals, payers, group purchasing organizations | Limits margin strength. |

Shortage of skilled device operators | -0.5% | Advanced surgical and imaging settings | Affects utilization. |

Data privacy compliance complexity | -0.5% | Connected and wearable devices | Increases operating risk. |

Segment Covered in the Report

By Device Type

In Vitro Diagnostics (IVD)

Diagnostic Imaging

Cardiovascular Devices

Orthopedic Devices

Surgical Devices

Patient Monitoring Devices

Others

By Application

Cardiology

Diagnostic Imaging

Orthopedics

Neurology

In Vitro Diagnostics

Others

By End User

Hospitals and Clinics

Ambulatory Surgical Centers

Diagnostic Laboratories

Home Healthcare

Others

By Technology

Conventional Devices

Connected Medical Devices

AI-Enabled Medical Devices

Robotic-Assisted Devices

Recent Developments

January 2026, Boston Scientific agreed to acquire Penumbra in a USD 14.5 billion transaction. The deal is expected to expand Boston Scientific’s cardiovascular and neurovascular device portfolio, including products used in stroke, pulmonary embolism, heart attack, and aneurysm treatment. Penumbra was expected to generate about USD 1.4 billion in 2025 sales, and the transaction is expected to close in 2026.

January 2026, Intuitive received FDA 510(k) clearance for selected thoracoscopically assisted cardiac procedures using the da Vinci 5 robotic surgical system. The indicated procedures include mitral valve repair, atrial septal defect repair, left atrial appendage closure, tricuspid valve repair, and other selected cardiac procedures. A limited number of U.S. sites are expected to work with Intuitive through 2026 to establish da Vinci 5 cardiac programs.

February 2026, The FDA’s Quality Management System Regulation became effective on February 2, 2026. The rule incorporates ISO 13485:2016 into U.S. medical device current good manufacturing practice requirements under 21 CFR Part 820. FDA also moved away from its older inspection approach and began using a new inspection process aligned with the updated compliance program.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 209.1 Billion |

Forecast Revenue (2035) | USD 407.6 Billion |

CAGR (2025-2035) | 6.9% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Device Type (In Vitro Diagnostics (IVD), Diagnostic Imaging, Cardiovascular Devices, Orthopedic Devices, Surgical Devices, Patient Monitoring Devices, Others), By Application (Cardiology, Diagnostic Imaging, Orthopedics, Neurology, In Vitro Diagnostics, Others), By End User (Hospitals and Clinics, Ambulatory Surgical Centers, Diagnostic Laboratories, Home Healthcare, Others), By Technology (Conventional Devices, Connected Medical Devices, AI-Enabled Medical Devices, Robotic-Assisted Devices) |

Competitive Environment Analysis

The U.S. Medical Devices Market is highly competitive, innovation-driven, and strongly regulated. Competition is led by companies with broad portfolios across diagnostic imaging, cardiovascular devices, orthopaedic implants, surgical instruments, patient monitoring, in vitro diagnostics, diabetes care, robotic-assisted surgery, and connected medical devices. The market is supported by advanced hospital infrastructure, high procedure volumes, strong reimbursement systems, and continuous demand for safer, faster, and more accurate care delivery.

The competitive landscape is shaped by regulatory strength, clinical evidence, product reliability, physician trust, and long-term service support. Large companies have an advantage because they can support hospitals with full product ecosystems, training, maintenance, software updates, and compliance documentation. Smaller and specialized companies compete through focused innovation in areas such as minimally invasive surgery, digital health, neurotechnology, structural heart, imaging software, and AI-enabled diagnostics.

Technology adoption is increasing across connected devices, remote monitoring, AI-enabled imaging, robotic surgery, digital therapeutics, and smart hospital equipment. These products support faster clinical decisions, better workflow control, and improved patient monitoring. However, adoption also requires stronger cybersecurity controls, clinical validation, data governance, and integration with hospital IT systems.

Implementation Complexity & Technology Readiness

Medical Device Technology | Implementation Complexity | Technology Readiness | Market Position |

|---|---|---|---|

Conventional medical devices | Low to Moderate | High | Widely used across care settings. |

In vitro diagnostics | Moderate | High | Strong use in labs, hospitals, and POC testing. |

Diagnostic imaging systems | High | High | Essential but capital-intensive. |

Cardiovascular devices | High | High | Strong demand in cardiac care. |

Orthopaedic implants | High | High | Established use in surgical procedures. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Medtronic plc

Abbott Laboratories

Johnson & Johnson MedTech

Boston Scientific Corporation

Stryker Corporation

Becton Dickinson and Company

GE HealthCare Technologies Inc.

Zimmer Biomet Holdings, Inc.

Edwards Lifesciences Corporation

Intuitive Surgical, Inc.

Danaher

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Healthcare and Pharmaceuticals

Skin Care Products Market to Cross USD 285.8 Bn by 2035

Global Skin Care Products Market By Type (Facial Care, Body Care, Lip Care), By Packaging (Tubes, Bottles, Jars, Others), By Products (Face Creams & Moisturizers, Cleansers & Face Wash, Sunscreen, Body Creams & Moisturizers, and Others), By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, and Others), By End-User (Female, Male, Unisex), By Category (Premium Skincare Products, Mass Skincare Products), By Ingredient (Chemical, Natural), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Biohacking Market to Exceed USD 231.3 Billion by 2035

Global Biohacking Market Size, Share Analysis Report By Product Type (Wearable Devices, Smart Implants, Gene-Editing Kits, Nootropics & Supplements, Sensors & Biomonitoring Patches, Others), By Biohacking Type (Nutrigenomics, DIY Biology, Grinder, and Others), By End User (Consumers, Healthcare Facilities, and Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Telemedicine Market to Exceed USD 981.6 Billion by 2035

Global Telemedicine Market Size, Share Analysis Report By Modality (Synchronous, Asynchronous, Remote Patient Monitoring), By Component (Software Platforms, Hardware & Peripherals, Services), By End User (Healthcare Providers, Payers & Employers, Patients / Home Users, Government Agencies & NGOs), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Helicobacter Pylori Diagnostics Market to hit 4.6 Bn by 2035

Global Helicobacter Pylori Diagnostics Market Size and Trade Analysis Report By Product Type (Instruments, Services, and Reagents), By Application (Immunoassays, Molecular Diagnostics, and Point-of-Care (POC)), By End User (Hospitals, Diagnostic Laboratories, and Clinics), By Regional Insights, Leading Companies and Growth Forecasts by 2025-2035