Introduction

According to Globe Market Research, the growth of the market can be attributed to rising concerns over indoor air pollution, increasing cases of respiratory discomfort, higher consumer awareness about clean indoor environments, and growing adoption of smart home appliances. Residential air purifiers are increasingly being used to reduce dust, smoke, pollen, pet dander, allergens, odor, and fine particulate matter inside homes. Demand is being supported by the rising exposure of households to outdoor pollution that enters indoor spaces, along with indoor sources such as cooking emissions, cleaning products, building materials, furniture, and poor ventilation.

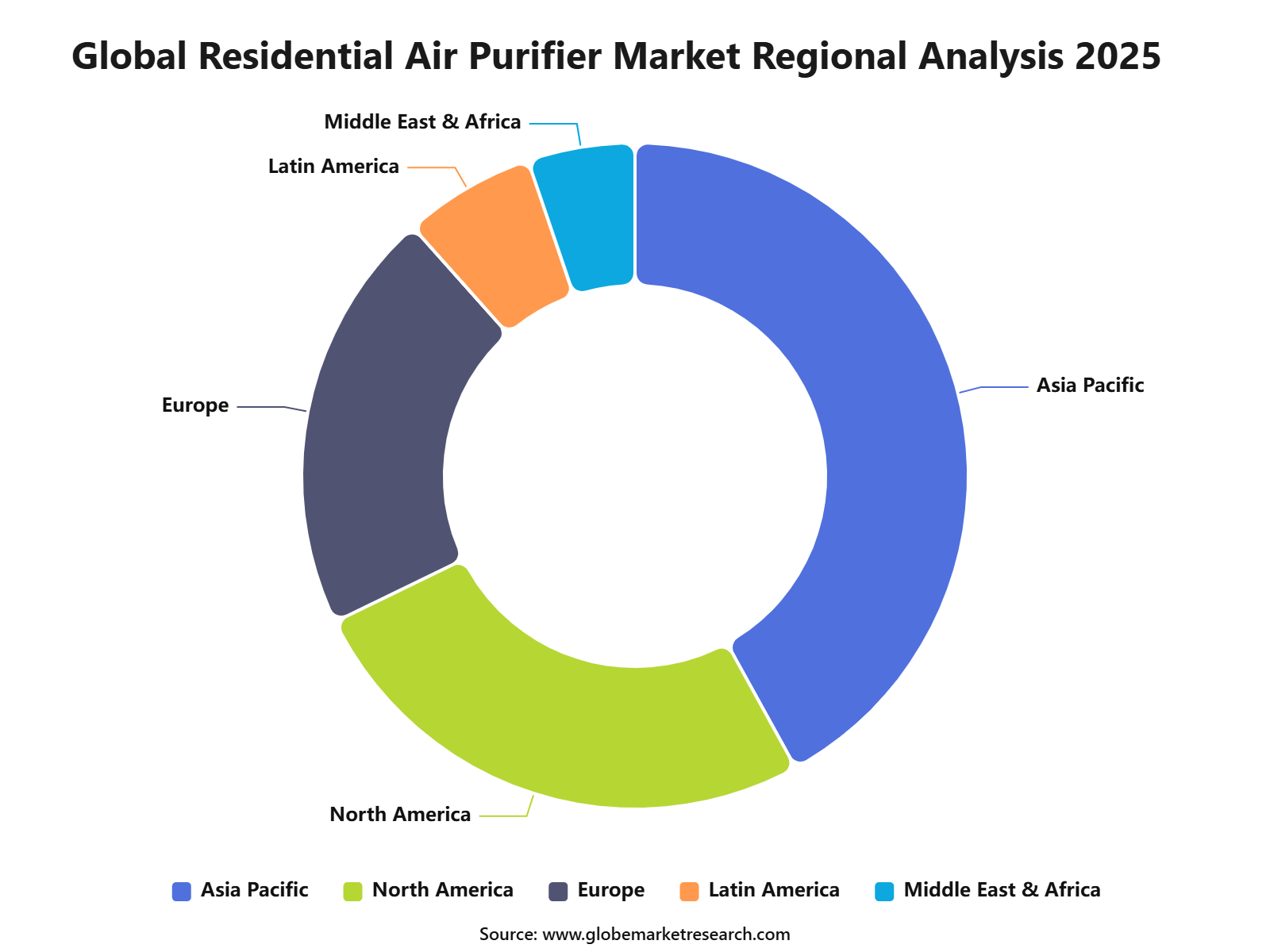

Consumers are becoming more aware that indoor air quality directly affects sleep quality, respiratory health, child health, and overall household wellness. As a result, air purifiers are shifting from seasonal purchases to regular home health appliances, especially in urban areas. Asia Pacific held the largest market share of 42.0% in 2025, driven by high pollution levels, rapid urbanization, increasing disposable income, and strong demand for home-based air quality solutions

Key Market Insights - 2025 Share

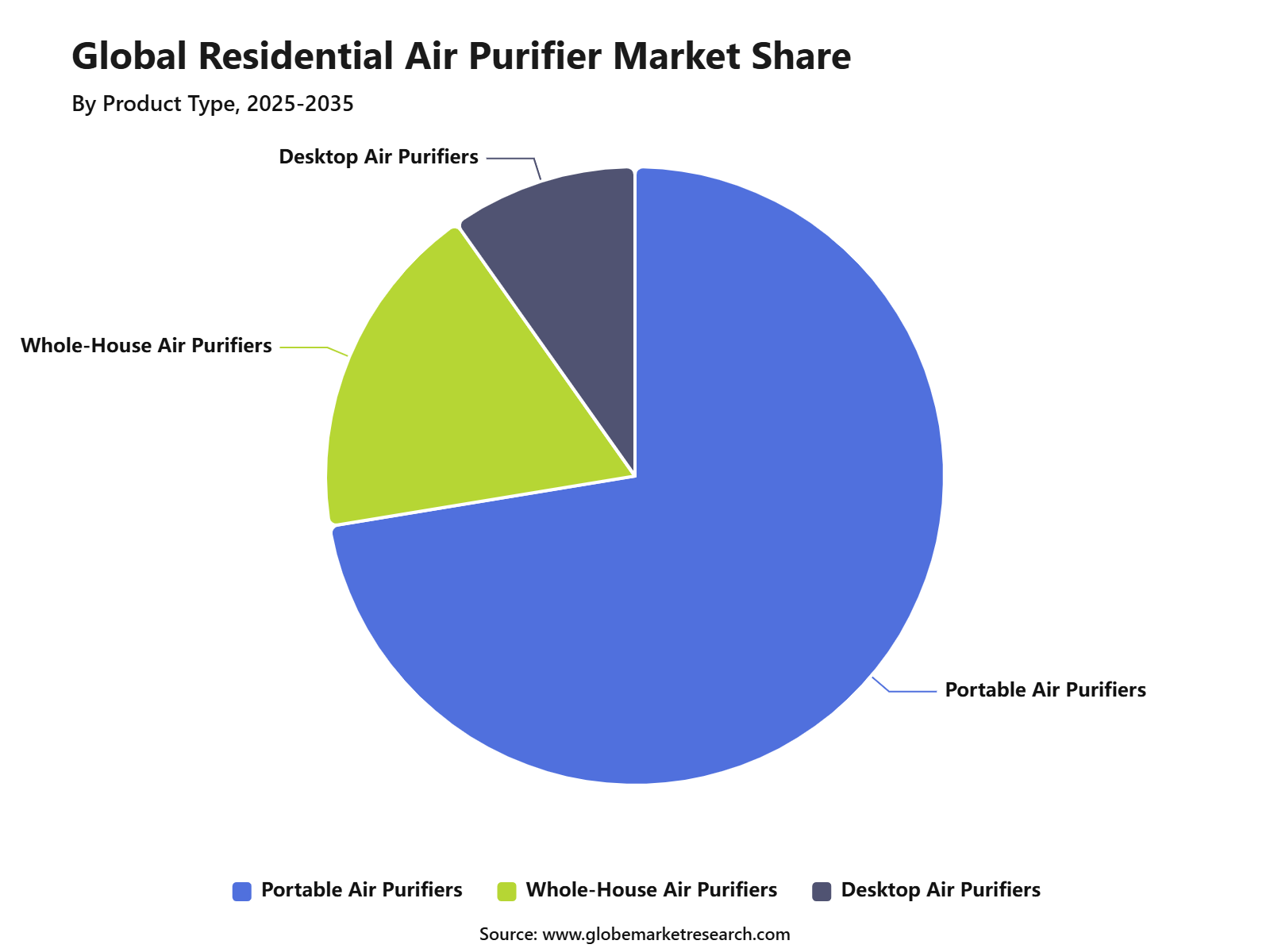

Portable air purifiers led the product type segment with 72.4% share, supported by easy installation, flexible room-to-room use, lower upfront cost, and strong demand for compact indoor air cleaning devices.

HEPA filtration accounted for 53.4% share by technology, driven by its strong ability to capture fine particles, dust, pollen, pet dander, and other airborne allergens in homes.

Dust and allergen removal held 41.8% share by application, supported by rising allergy concerns, increasing indoor pollution awareness, and higher use in homes with children, elderly people, and pets.

Asia Pacific accounted for the largest regional share with 42.0% in 2025, supported by high urban pollution levels, rising health awareness, and growing demand for residential indoor air quality solutions.

Go-to-Market and Sales Economics

The go-to-market strategy for residential air purifiers should be built around health protection, room-level performance, and long-term ownership cost. According to EPA, Demand is being supported by high indoor exposure, as people spend about 90% of their time indoors, and indoor air can contain PM2.5, PM10, formaldehyde, mold, pollen, and volatile organic compounds from cooking, cleaning, furniture, and outdoor pollution entering the home. EPA guidance also states that portable air cleaners can improve indoor air quality, although filtration should support, not replace, source control and clean ventilation.

The strongest sales messaging should focus on verified CADR, HEPA filtration, activated carbon for gases and odors, low-noise operation, and energy efficiency. In 2026, buyers are comparing products more carefully because performance claims are easy to overstate. AHAM recommends that CADR should be at least two-thirds of the room area, while wildfire smoke applications may require smoke CADR equal to the room size in square feet. This makes room-size education an important conversion tool and helps reduce returns caused by undersized products.

Based on data from energy star, Sales economics are increasingly shaped by recurring filter replacement, energy use, and multi-room adoption. A standard room air cleaner running continuously can use around 394 kWh per year, while ENERGY STAR certified models are more than 50% more energy efficient and can save about 211 kWh per year, equal to roughly USD 18 to USD 40 in annual electricity savings depending on unit size. This supports premium pricing for efficient models, especially when the value is explained through total cost of ownership rather than only upfront price.

Risk Factors & Market Barriers

Regulatory & Compliance Risks

Regulatory compliance is becoming a direct market-entry risk for residential air purifier brands. In the U.S., the Department of Energy has adopted air cleaner energy conservation standards based on PM2.5 CADR per watt, with Tier 2 compliance applying to products manufactured in or imported into the U.S. starting December 31, 2025. The Tier 2 thresholds are 1.9, 2.4, and 2.9 PM2.5 CADR/W across product classes, which means weaker designs may require motor, fan, airflow, and filtration redesign before they can compete in 2026 and beyond.

By California Air Resources Board, Ozone-related regulation is another major risk, particularly for electronic, ionizer, plasma, UV, and electrostatic air-cleaning products. California requires all portable indoor air cleaning devices sold to consumers or businesses in the state to be CARB certified, and electronic air cleaners must meet an ozone emission limit of 0.050 parts per million, or 50 ppb. Products that cannot prove low ozone emissions may face listing delays, channel rejection, product returns, or reputational damage.

Based on data from dpiit, India is also moving toward stronger quality control for portable electric indoor air purifiers. A Government of India quality control order document identifies IS 17531:2021 as the standard for portable electric indoor air purifiers and proposes mandatory use of the Standard Mark within 6 months for general enterprises, 9 months for small enterprises, and 12 months for micro enterprises after notification. This creates a compliance cost for importers and private-label sellers, but it may also improve buyer trust by reducing low-quality products in the market.

Market Adoption Barriers

The main adoption barrier is consumer confusion around performance claims. Many buyers still compare air purifiers by price, coverage area, filter label, or brand name, while actual performance depends on CADR, room size, fan speed, filter quality, airflow design, and operating time. EPA guidance states that no portable air cleaner can remove all pollutants from a home, and mold issues cannot be solved by an air purifier unless the moisture source is addressed. This creates a need for careful, evidence-based messaging rather than exaggerated health claims.

Upfront cost and ongoing ownership cost also limit wider household penetration. Since air purifiers are often required in bedrooms, living rooms, and workspaces, one household may need more than one unit for effective coverage. Energy cost can become a concern when devices run continuously, although ENERGY STAR certified models reduce this barrier by saving about 211 kWh per year versus standard models. Filter replacement cost, noise at higher speeds, and uncertainty about genuine HEPA or activated carbon performance can slow repeat purchases if post-sale education is weak.

A further barrier is trust. Consumer Reports noted in 2026 that its ratings covered more than 180 air purifiers and that weaker models may struggle even at high speed while producing noticeable noise. This shows that product testing, verified CADR, low-noise performance, clear warranty terms, and transparent filter replacement schedules are critical for conversion. Brands that rely only on "large room", "medical-grade", or "99.97% filtration" claims without verified performance data may face lower buyer confidence and higher return rates.

Product Type Insights

Portable air purifiers led the product type segment with 72.4% share in 2025. The segment’s leadership can be attributed to easy installation, room-to-room flexibility, lower upfront cost, and strong suitability for apartments, bedrooms, living rooms, and small home offices. Consumers prefer portable units because they do not require major structural changes and can be used immediately after purchase.

The demand for portable air purifiers is also supported by rising awareness of indoor dust, smoke, pet dander, pollen, and fine particles. These devices are practical for households that need targeted air cleaning in specific rooms rather than whole-home systems. Their compact design, simple controls, and wider availability across retail and online channels keep them highly preferred among residential buyers.

Technology Insights

HEPA filtration accounted for 53.4% share by technology in 2025. The segment remained dominant because HEPA filters are widely used to capture fine particles, dust, pollen, pet dander, and other airborne allergens in residential spaces. This makes the technology highly relevant for homes with allergy-sensitive individuals, children, elderly people, and pets.

The segment also benefits from strong consumer trust and clear product understanding. Many buyers look for HEPA-based purifiers because the technology is associated with particle removal and cleaner indoor air. As indoor air quality concerns increase, HEPA filtration continues to remain one of the most preferred technologies in residential air purifier products.

Application Insights

Dust and allergen removal held 41.8% share by application in 2025. Growth in this segment is driven by rising allergy concerns, increasing indoor pollution awareness, and higher use of air purifiers in homes affected by dust, pollen, pet hair, and household particles. Consumers are increasingly using air purifiers as part of daily home care, especially in bedrooms and living areas.

The segment is also supported by lifestyle and health-related needs. Homes with pets, carpets, soft furnishings, and poor ventilation often face higher particle buildup. Air purifiers used for dust and allergen removal help improve comfort and reduce exposure to common indoor triggers. This keeps the segment important across both urban and suburban households.

Regional Insights

Asia Pacific accounted for the largest regional share of 42.0% in 2025. The region’s leadership is supported by high urban pollution levels, dense populations, rising household income, and growing consumer focus on indoor air quality. Countries across the region face strong exposure to outdoor fine particles, which often increases concern about air quality inside homes.

The regional demand is also supported by expanding urban housing, wider availability of compact appliances, and stronger awareness of health-related air quality risks. Consumers in major cities are increasingly using residential air purifiers to manage dust, smoke, allergens, and pollution entering indoor spaces. This makes Asia Pacific the leading region for residential air purifier adoption.

Key Player Analysis

The residential air purifier market is moderately consolidated, with strong participation from global appliance, HVAC, electronics, and specialist filtration companies. Key players such as Daikin Industries, Honeywell International, Sharp, Panasonic, LG Electronics, Samsung Electronics, Philips, Dyson, Blueair, IQAir, Midea Group, Xiaomi, Whirlpool, Winix, Austin Air Systems, and Camfil AB are competing through filtration efficiency, smart monitoring, product design, room coverage, noise control, and energy performance. Demand is being supported by rising concerns over PM2.5 pollution, allergens, pet dander, indoor dust, smoke, volatile organic compounds, and household health protection.

Large appliance and electronics companies are strengthening their position by combining air purification with smart home systems, mobile app controls, real-time air quality indicators, and connected device ecosystems. LG, Samsung, Philips, Panasonic, Sharp, Xiaomi, Midea, Whirlpool, and Daikin benefit from wide distribution networks, strong consumer trust, and established after-sales service. These companies are also focusing on compact designs, affordable replacement filters, and multi-stage filtration technologies to serve urban homes, apartments, and family households.

Specialist brands such as Dyson, Blueair, IQAir, Winix, Austin Air Systems, Honeywell, and Camfil AB are gaining attention through premium filtration, high CADR performance, HEPA-based systems, activated carbon filters, and solutions for allergy-sensitive consumers. Dyson and Blueair are positioned strongly in the premium and design-focused category, while IQAir, Austin Air, and Camfil focus more on high-efficiency filtration and health-driven performance. Overall, competition is expected to increase as consumers compare products based on verified filtration quality, filter replacement cost, smart features, energy use, and long-term reliability.

List of Top Companies

Daikin Industries, Ltd.

Honeywell International Inc.

Sharp Corporation

Panasonic Corporation

LG Electronics Inc.

Samsung Electronics Co., Ltd.

Koninklijke Philips N.V.

Dyson Limited

Blueair

IQAir

Midea Group

Xiaomi Corporation

Whirlpool Corporation

Winix Inc.

Austin Air Systems

Camfil AB

Others

Recent Developments

March 2026 - Sharp India launched the Ryohu window AC range with active air purification. The lineup includes six models across 1.5-ton and 2-ton capacities and uses patented Plasmacluster technology.

December 2025 - Blueair was ranked the Best Air Purifier Brand of 2025 by Consumer Reports. The ranking was based on performance, reliability, and customer satisfaction.

Market Coverage

Report Highlights | Details |

|---|---|

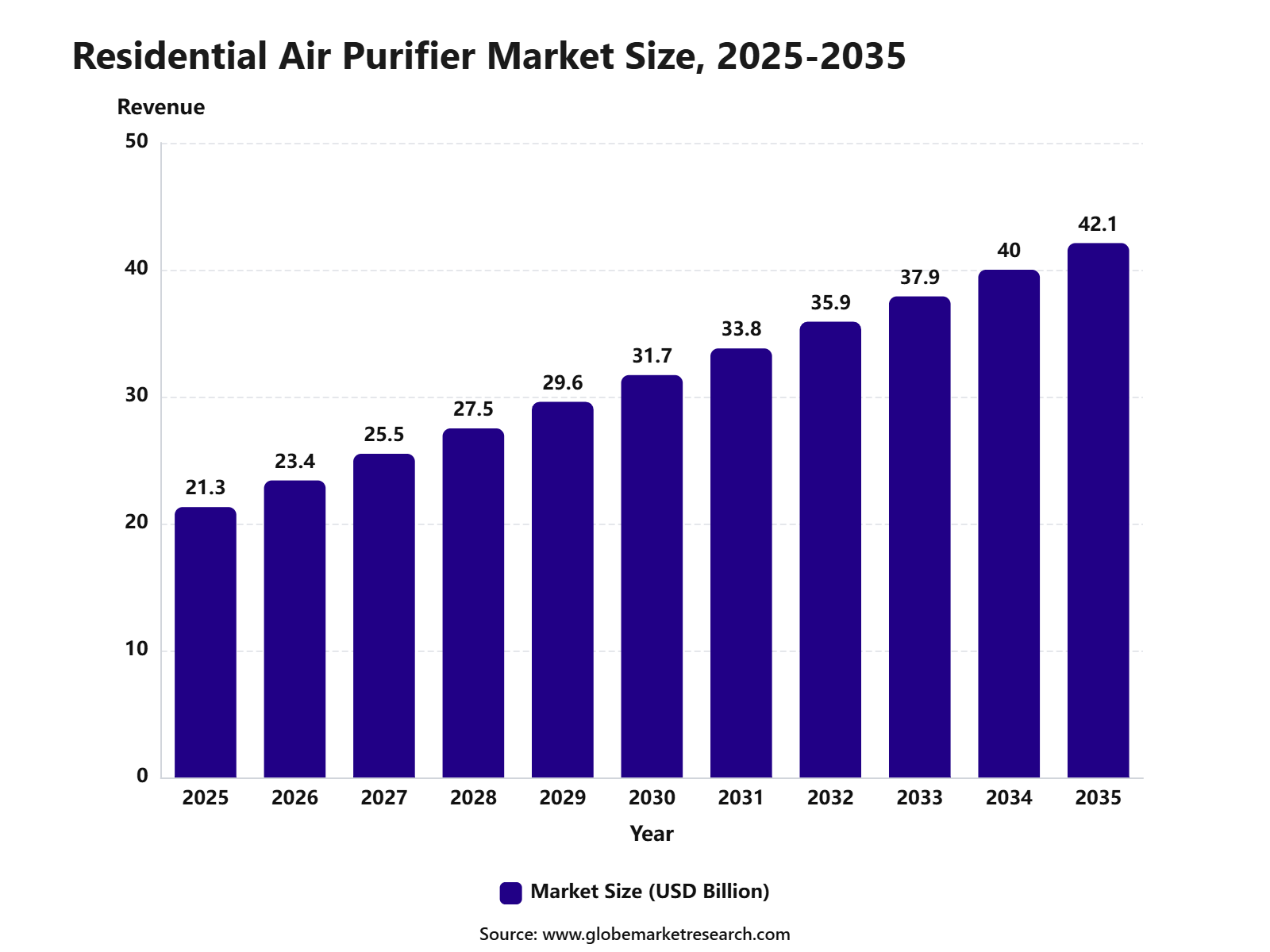

Market Revenue (2025) | USD 21.32 Bn |

Forecast Revenue (2035) | USD 42.15 Bn |

CAGR (2025-2035) | 9.5% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI impact analysis, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends |

Segments Covered | By Product Type (Portable Air Purifiers, Whole-House Air Purifiers, Desktop Air Purifiers), By Technology (HEPA Filtration, Activated Carbon Filtration, UV-C Purification, Ionic Filtration, Hybrid Filtration), By Application (Dust and Allergen Removal, Smoke and Odor Control, Pet Dander Removal, Mold and Bacteria Reduction) |

Key companies profiled | Daikin Industries, Ltd., Honeywell International Inc., Sharp Corporation, Panasonic Corporation, LG Electronics Inc., Samsung Electronics Co., Ltd., Koninklijke Philips N.V., Dyson Limited, Blueair, IQAir, Midea Group, Xiaomi Corporation, Whirlpool Corporation, Winix Inc., Austin Air Systems, Camfil AB, Others |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Segments Covered in This Report

By Product Type

Portable Air Purifiers

Whole-House Air Purifiers

Desktop Air Purifiers

By Technology

HEPA Filtration

Activated Carbon Filtration

UV-C Purification

Ionic Filtration

Hybrid Filtration

By Application

Dust and Allergen Removal

Smoke and Odor Control

Pet Dander Removal

Mold and Bacteria Reduction

Key Regions and Countries

Asia Pacific

China

India

Japan

South Korea

Australia

Indonesia

Thailand

Vietnam

Malaysia

North America

United States

Canada

Mexico

Europe

Germany

United Kingdom

France

Italy

Spain

Netherlands

Sweden

Switzerland

Latin America

Brazil

Argentina

Chile

Colombia

Middle East and Africa

Saudi Arabia

United Arab Emirates

South Africa

Egypt

Qatar

Kuwait

Explore the full Residential Air Purifier Market report to gain detailed insights into global market size, revenue share, CAGR, emerging trends, segmental performance, regional outlook, and competitive landscape.

Read the report here: https://www.globemarketresearch.com/reports/residential-air-purifier-market

To place an order or request more information, please contact our sales team at [email protected]. Our team will be happy to assist you with report details, customization options, and purchase support.