Revenue, 2025

$4.9Bn

Forecast, 2035

$16.5Bn

CAGR, 2025-2035

12.9%

Report Coverage

Global

Market Size and Forecast

2025

$4.9Bn

2035

$16.5Bn

CAGR

12.9%

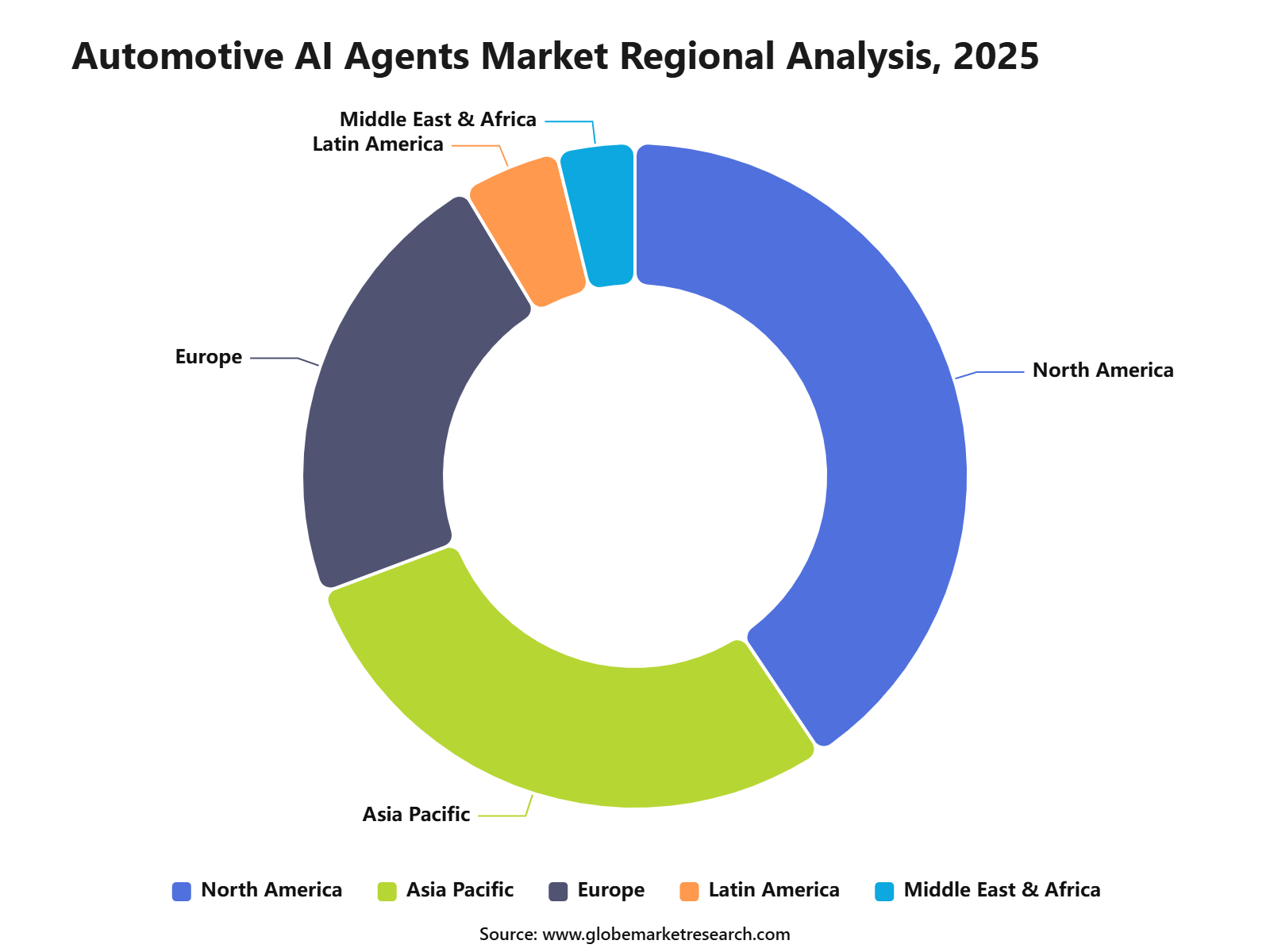

The Global Automotive AI Agents Market reached USD 4.9 bn in 2025 and is expected to grow to USD 16.5 bn by 2035, registering a CAGR of 12.9% from 2025 to 2035. The growth of the market can be attributed to the rising integration of AI in connected vehicles, electric vehicles, autonomous driving systems, driver assistance technologies, and in-vehicle virtual assistants. North America held the largest regional share of 40.6% in 2025, valued at USD 1.9 billion, supported by strong adoption of advanced driver assistance systems, high investment in autonomous vehicle technologies, presence of leading automotive technology companies, and mature connected vehicle infrastructure.

Automotive AI agents are increasingly being used to improve vehicle safety, support predictive maintenance, enhance fleet operations, personalize infotainment, and enable real-time decision-making through edge and cloud-based deployment models. The strongest growth driver is the rising adoption of electric and connected vehicles across global markets. IEA expects electric car sales to reach 23 million units in 2026, representing 28% of total car sales. Electric vehicles require advanced software for battery health, charging optimization, energy management, and predictive diagnostics. This creates a strong base for AI agents that can manage vehicle performance and improve the ownership experience.

Key Market Insights - 2025 Share

Autonomous driving AI agents accounted for 40.2% share in 2025, making them the leading agent type. Growth was supported by rising use of AI for route planning, object detection, lane assistance, decision-making, and semi-autonomous driving functions.

Passenger vehicles held 67.8% share in 2025, reflecting strong adoption of AI-enabled safety, infotainment, navigation, and in-cabin assistance systems. The segment benefited from growing consumer demand for safer, smarter, and more connected driving experiences.

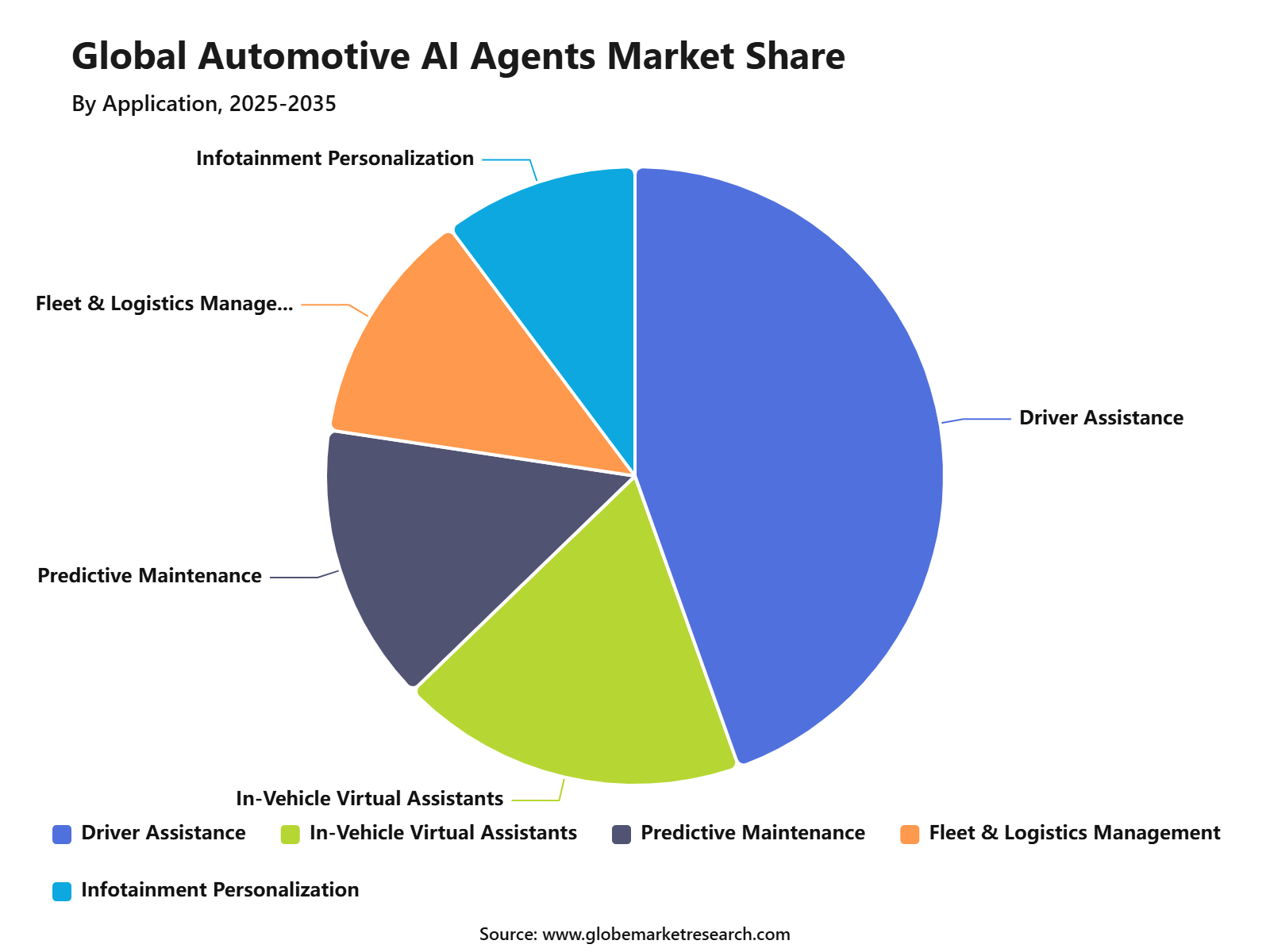

Driver assistance and safety led the application segment with 44.5% share in 2025. Adoption was driven by increasing use of AI agents in collision warning, adaptive cruise control, driver monitoring, emergency braking, and real-time road condition analysis.

Edge and on-board AI agents captured 47.7% share in 2025, supported by the need for faster decision-making, lower latency, and real-time vehicle data processing. This deployment type is important for safety-critical automotive applications where instant response is required.

North America held 40.6% share of the automotive AI agents market in 2025. The regional market was valued at USD 1.9 billion, supported by strong automotive technology adoption, advanced vehicle safety standards, and investment in connected and autonomous vehicle systems.

In-Vehicle Virtual Assistants accounted for 18.2% share, driven by growing use of voice assistants, natural language interaction, navigation support, climate control, infotainment commands, and personalized cabin experiences.

Predictive Maintenance held 14.6% share, supported by AI-based fault detection, vehicle health monitoring, battery diagnostics, powertrain analysis, and service scheduling. This segment is gaining importance across connected vehicles and commercial fleets.

Fleet & Logistics Management represented 12.4% share, driven by route optimization, driver behavior tracking, fuel efficiency monitoring, delivery planning, and real-time fleet visibility. Infotainment Personalization accounted for 10.3% share, supported by customized content, user profiles, media recommendations, and connected entertainment systems.

Market Overview

Demand is being supported by the large global vehicle base and the steady recovery of vehicle production and sales. OICA reported that global vehicle sales reached 99.8 million units in 2025, while production increased to 96.4 million units. As these vehicles become more digital, automakers are adding AI-based functions to improve safety, comfort, maintenance, and aftersales engagement. This trend is expected to continue in 2026 as buyers place higher value on connected features and intelligent assistance.

Investment opportunities are strong in autonomous driving AI agents, driver assistance systems, edge AI chips, in-cabin intelligence, and predictive maintenance platforms. Suppliers that can combine software, sensors, computing hardware, and safety validation are expected to benefit from rising vehicle intelligence. Demand is especially attractive in passenger vehicles because this category has the largest production scale and faster adoption of comfort and safety features. Commercial vehicles also offer high potential because fleet owners are willing to invest in tools that reduce repair costs and improve asset use.

Automotive AI Agents Statistics

Automotive AI leaders are scaling faster than laggards. Around 38.6% of AI-leading automotive companies are already rebuilding applications with embedded AI capabilities, compared with only 12% of laggards.

Based on data from Reuters, Robotaxi deployment is becoming a major proof point for automotive AI agents. Waymo reported 200 million fully autonomous miles on public roads and around 400,000 weekly rides across cities such as Phoenix, San Francisco Bay Area, Los Angeles, Austin, Atlanta, and Miami.

Advanced driver assistance remains a key adoption area for automotive AI agents. The U.S. will require nearly all new passenger cars and trucks to include automatic emergency braking by September 2029, and the rule is expected to save at least 360 lives and prevent more than 24,000 injuries each year.

Safety performance is improving as AI-based perception systems advance. IIHS reported that pedestrian-recognition automatic braking systems reduced pedestrian crashes by 27%, showing the practical safety value of AI-enabled vehicle sensing and response.

By Agent Type Analysis

Autonomous driving AI agents led the agent type segment with 40.2% share in 2025, supported by rising use of AI in perception, route planning, decision-making, object detection, lane control, and driver monitoring. These agents are important because modern vehicles need to understand the road environment in real time and respond to changing traffic conditions. Their adoption is being supported by the growth of automated driving systems, advanced sensors, connected vehicle platforms, and software-defined vehicle architectures.

The segment is also gaining strength as automakers move from basic driver assistance toward more advanced automated functions. Autonomous driving AI agents help vehicles process data from cameras, radar, lidar, ultrasonic sensors, maps, and vehicle control systems. Their value is higher in safety-critical functions where fast judgement and low delay are required. This makes autonomous driving AI agents the most influential category in the Automotive AI Agents Market.

Agent Type | 2025 Share |

|---|---|

Autonomous Driving AI Agents | 40.2% |

Conversational AI Agents | 21.8% |

Predictive Maintenance AI Agents | 16.4% |

Fleet Management AI Agents | 12.7% |

Others | 8.9% |

Vehicle Type Analysis

Passenger vehicles accounted for the leading vehicle type share of 67.8% in 2025, driven by high production volumes, wider consumer adoption of connected features, and growing demand for safer personal mobility. AI agents are increasingly being added to passenger cars through driver assistance, in-car voice support, predictive maintenance, navigation, infotainment, and vehicle personalization. The segment benefits from strong consumer interest in comfort, safety, convenience, and intelligent in-vehicle experiences.

The growth of AI agents in passenger vehicles is also supported by electric vehicle adoption and software-defined vehicle development. New passenger cars are being designed with more sensors, computing hardware, connectivity, and over-the-air update capability. This creates a stronger base for deploying AI agents across vehicle control, cabin experience, safety alerts, and maintenance support. As passenger cars become more digital, this segment is expected to remain the main adoption area for automotive AI agents.

Vehicle Type | 2025 Share |

|---|---|

Passenger Vehicles | 67.8% |

Commercial Vehicles | 16.5% |

Electric Vehicles (EVs) | 10.7% |

Autonomous Vehicles | 5.0% |

Application Analysis

Driver assistance and safety led the application segment with 44.5% share in 2025, supported by increasing use of automatic emergency braking, adaptive cruise control, lane keeping assistance, blind spot detection, pedestrian detection, and driver monitoring systems. AI agents are important in this area because they can help analyze road conditions, identify risks, and support faster safety responses. Demand is being driven by consumer safety expectations, regulatory pressure, and the need to reduce crash severity.

Application Segment | 2025 Share |

|---|---|

Driver Assistance & Safety | 44.5% |

In-Vehicle Virtual Assistants | 18.2% |

Predictive Maintenance | 14.6% |

Fleet & Logistics Management | 12.4% |

Infotainment Personalization | 10.3% |

The segment is also supported by the wider shift toward active safety systems in passenger cars and light vehicles. AI agents can help improve how vehicles detect hazards, prioritize alerts, and support driver decisions during complex road situations. These systems are especially valuable in urban traffic, highway driving, night driving, and pedestrian-heavy zones. As safety features become more common in new vehicles, driver assistance and safety will remain a core application area for automotive AI agents.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFDeployment Type Analysis

Edge and on-board AI agents dominated the deployment type segment with 47.7% share in 2025, driven by the need for low-latency processing, local decision-making, data privacy, and reliable vehicle operation. Vehicles cannot depend only on cloud systems for safety-critical functions because driving decisions often need to be made within milliseconds. On-board AI agents allow vehicles to process sensor data directly inside the vehicle, which improves response time and reduces dependence on network connectivity.

This deployment model is becoming more important as vehicles use larger volumes of camera, radar, lidar, and cabin data. Edge AI helps manage real-time functions such as obstacle detection, lane tracking, driver monitoring, parking assistance, voice interaction, and predictive alerts. Hybrid edge-to-cloud models are also gaining attention because they allow critical tasks to run inside the vehicle while cloud systems support updates, learning, and broader service integration. This makes edge and on-board AI agents a key foundation for intelligent vehicle systems.

Deployment Type | 2025 Share |

|---|---|

Edge / On-Board AI Agents | 47.7% |

Cloud-Based AI Agents | 31.4% |

Hybrid Deployment | 20.9% |

Regional Analyst View

North America held 40.6% share of the Automotive AI Agents Market in 2025 and was valued at USD 1.9 Bn, supported by strong automotive technology adoption, advanced vehicle safety regulation, and high demand for connected vehicles. The region has a mature base of automakers, technology providers, cloud platforms, semiconductor suppliers, and mobility software companies. This supports faster development of AI-enabled driver assistance, in-car assistants, predictive maintenance tools, and autonomous driving systems.

Region | 2025 Share |

|---|---|

North America | 40.6% |

Asia Pacific | 28.7% |

Europe | 22.1% |

Latin America | 4.8% |

Middle East & Africa | 3.8% |

The region’s leadership is also supported by rising investment in software-defined vehicles, EV platforms, and advanced safety systems. The U.S. has been active in vehicle safety regulation, including the move to make automatic emergency braking standard on new passenger cars and light trucks. North America also has strong consumer awareness of digital vehicle features, such as connected navigation, hands-free assistance, driver monitoring, and over-the-air updates. These factors make the region a leading market for automotive AI agent deployment.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFSegments Covered in the Report

By Agent Type

Autonomous Driving AI Agents

Conversational AI Agents

Predictive Maintenance AI Agents

Fleet Management AI Agents

Others

By Vehicle Type

Passenger Vehicles

Commercial Vehicles

Electric Vehicles (EVs)

Autonomous Vehicles

By Application

Driver Assistance & Safety

In-Vehicle Virtual Assistants

Predictive Maintenance

Fleet & Logistics Management

Infotainment Personalization

By Deployment Type

Edge / On-Board AI Agents

Cloud-Based AI Agents

Hybrid Deployment

By Region

North America

Asia Pacific

Europe

Latin America

Middle East & Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising adoption of autonomous driving technologies | +3.4% | North America, Europe, China, Japan | Drives AI agent deployment. |

Growth in advanced driver assistance systems | +3.0% | U.S., Germany, Japan, South Korea | Supports safety automation. |

Increasing demand for connected vehicles | +2.7% | North America, Europe, Asia Pacific | Expands in-vehicle AI use. |

Growth in electric and software-defined vehicles | +2.5% | China, U.S., Europe, South Korea | Supports intelligent mobility. |

Rising use of predictive maintenance | +2.2% | Global automotive fleets | Reduces vehicle downtime. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High development and integration cost | -1.8% | Global OEMs and suppliers | Limits faster adoption. |

Data privacy and cybersecurity concerns | -1.5% | North America, Europe, developed Asia | Raises trust issues. |

Regulatory uncertainty for autonomous systems | -1.4% | U.S., Europe, China, India | Slows deployment. |

Limited AI readiness in low-cost vehicles | -1.1% | Emerging markets | Restricts mass adoption. |

Dependence on high-quality vehicle data | -1.0% | Global | Affects model accuracy. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Expansion of autonomous mobility services | +3.2% | U.S., China, Europe, UAE | Creates new revenue. |

Growth in AI-based driver assistance | +3.0% | North America, Europe, Asia Pacific | Improves vehicle safety. |

AI agents for fleet management | +2.6% | U.S., Europe, India, China | Optimizes fleet operations. |

In-vehicle virtual assistants | +2.4% | Global passenger vehicle market | Improves user experience. |

AI-enabled infotainment personalization | +2.1% | U.S., China, Europe, Japan | Supports premium features. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Safety validation complexity | -1.6% | Autonomous and ADAS markets | Extends testing cycles. |

AI decision reliability issues | -1.4% | Global | Affects user confidence. |

Legacy vehicle platform integration | -1.2% | Traditional OEMs | Delays adoption. |

Shortage of automotive AI talent | -1.0% | U.S., Europe, Asia Pacific | Slows development. |

Liability concerns in AI-driven decisions | -0.9% | Regulated markets | Raises legal risk. |

Recent Developments

June 2026 - NVIDIA introduced new physical AI agent skills for autonomous vehicles, robotics, and vision AI systems at CVPR 2026. These tools are designed to speed data generation, simulation, policy training, and evaluation for autonomous system development.

April 2026 - Volkswagen Group announced plans to equip new China-specific vehicles with onboard AI agents from the second half of 2026. These agents are expected to support human-like interaction, restaurant booking, parking support, and complex in-car decision-making. Volkswagen also plans more than 20 new electrified vehicles.

March 2026 - Qualcomm and Wayve partnered to develop an integrated AI driving system for advanced driver assistance and self-driving vehicles. The system combines Wayve’s AI Driver software with Qualcomm’s Snapdragon Ride chips and active safety software. Wayve had recently raised USD 1.2 billion and reached an USD 8.6 billion valuation.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 4.9 Bn |

Forecast Revenue (2035) | USD 16.5 Bn |

CAGR (2025-2035) | 12.9% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Agent Type (Conversational AI Agents, Autonomous Driving AI Agents, Predictive Maintenance AI Agents, Fleet Management AI Agents and Others), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles (EVs), Autonomous Vehicles), By Application (Driver Assistance & Safety, In-Vehicle Virtual Assistants, Predictive Maintenance, Fleet & Logistics Management, Infotainment Personalization), By Deployment Type (Cloud-Based AI Agents Edge/On-Board AI Agents, Hybrid Deployment) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | NVIDIA Corporation, Alphabet Inc. (Waymo), Tesla Inc., Intel Corporation (Mobileye), Qualcomm Technologies, Microsoft Corporation, Amazon Web Services (AWS), IBM Corporation, Bosch, Continental AG |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

NVIDIA Corporation

Alphabet Inc. (Waymo)

Tesla Inc.

Intel Corporation (Mobileye)

Qualcomm Technologies

Microsoft Corporation

Amazon Web Services (AWS)

IBM Corporation

Bosch

Continental AG

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Suraj is a Senior Management Consultant with over 7 years of experience in market research, business strategy, and consulting. He has worked with Fortune 500 companies and growing startups, helping them with market entry, cross-border expansion, demand analysis, competitive assessment, and growth planning. His analytical thinking and strong industry knowledge help clients make clear, confident, and informed business decisions.

Frequently Asked Questions

Related Reports

More in Automotive and Transportation

Inboard Electric Motors Market to hit 13.1 Bn by 2035

Global Inboard Electric Motors Market Size By Type(Low Power Below 10 HP, Medium Power 10 to 35 HP, Large Power Above 35 HP), By Application (Civil Entertainment, Municipal, Commercial, Other Applications), By Boat / Vessel Type (Recreational Boats, Yachts, Fishing Boats, Workboats, Passenger Boats, Commercial Vessels), By Battery Type (Lithium-ion Batteries, Lead-acid Batteries, Nickel-based Batteries, Other Battery Types), By Sales Channel (OEM, Aftermarket), By End User (Individual Boat Owners, Commercial Operators, Tourism and Leisure Operators, Municipal Authorities, Marine Transport Operators), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Chauffeur Car Market to Exceed USD 403.8 Billion by 2035

By Service Type (Business Travel Services, Leisure Travel Services, Airport Transfers, Event-specific Services), By Vehicle Type (Luxury Cars, Executive Cars, SUVs, Vans, Limousines), By Customer Type (Corporate Clients, Individual Customers, Tourist and Leisure Travelers), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Automotive Alternator & Starter Motor Market to Hit USD 62.8 Bn by 2035

Global Automotive Alternator & Starter Motor Market Size, Share and AI Impact Analysis By Product (Alternator, Starter Motor), By Vehicle Type (Passenger vehicle, Commercial Vehicle, Off-road Vehicle), By Sales Channel (OEM, Aftermarket), By Regional Insights, Leading Companies and Growth Forecasts By 2025-2035