Revenue, 2025

$7.8Bn

Forecast, 2035

$13.1Bn

CAGR, 2026-2035

5.3%

Report Coverage

Global

Market Size and Forecast

2026

$7.8Bn

2035

$13.1Bn

CAGR

5.3%

The global inboard electric motors market was valued at USD 7.8 billion in 2025 and is projected to reach USD 13.1 billion by 2035, growing at a CAGR of 5.3% from 2025 to 2035. The market growth is supported by rising demand for low-emission marine propulsion systems, increasing adoption of electric boats, and stricter regulations on fuel-based marine engines. Inboard electric motors are gaining traction due to their quiet operation, lower maintenance needs, and better energy efficiency compared to conventional propulsion systems.

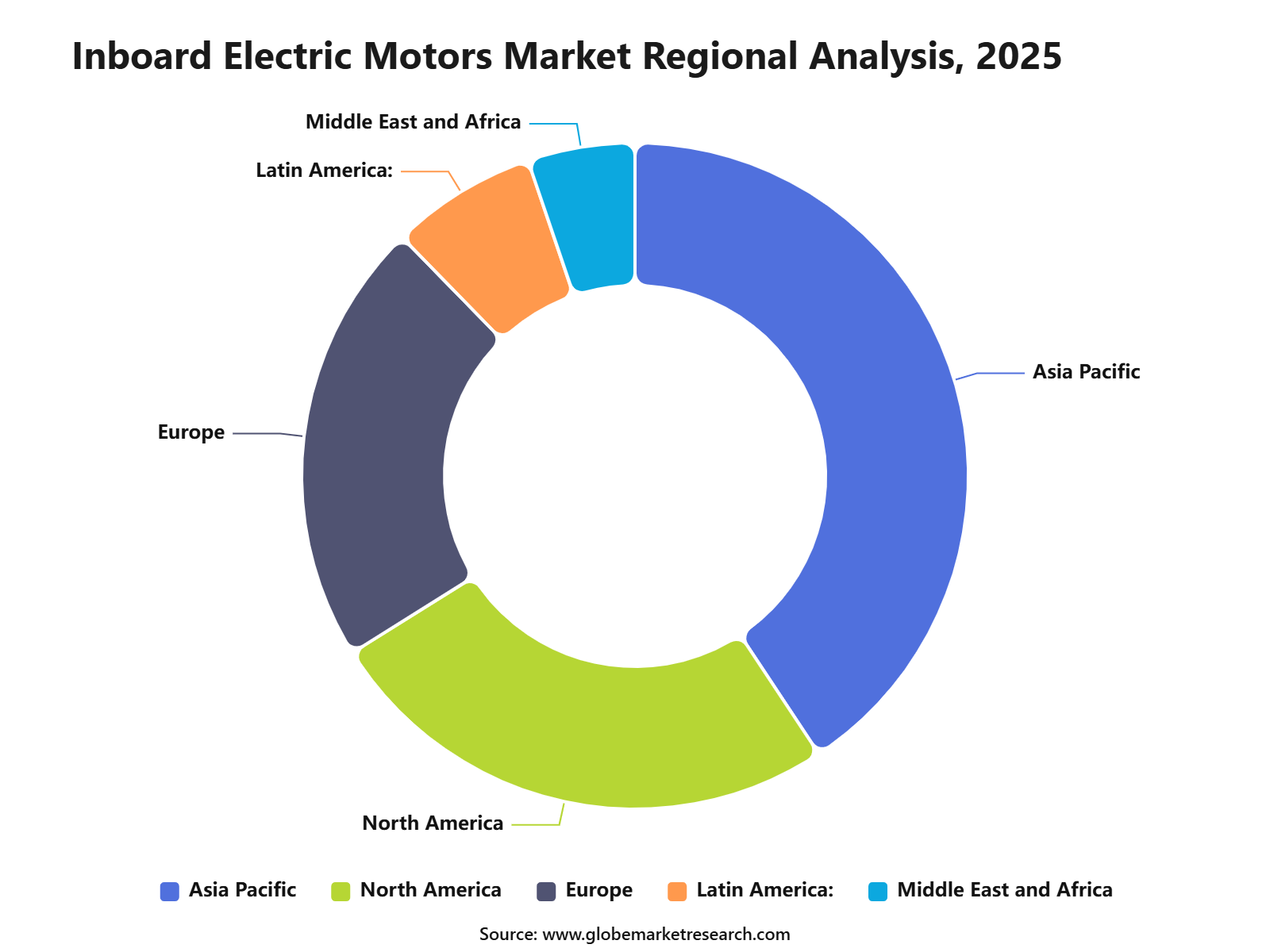

Asia Pacific held the largest regional share of 40.7% in 2025, driven by expanding recreational boating, rising marine tourism, and growing investment in electric mobility across coastal economies. Countries in the region are also supporting cleaner transport technologies, which is encouraging boat manufacturers and fleet operators to adopt electric propulsion systems. The demand is expected to increase further as commercial vessels, passenger boats, and leisure marine operators shift toward sustainable and cost-efficient power solutions.

Key Market Insights

Low power inboard electric motors below 10 HP led the market with 50.6% share, supported by strong use in small boats, recreational vessels, and low-speed marine applications.

Civil entertainment accounted for 45.3% share by application, driven by rising demand for electric boating in leisure, tourism, and personal watercraft activities.

Recreational boats held around 57.3% share by boat type, supported by growing consumer preference for quiet, low-emission, and easy-to-maintain marine propulsion systems.

Lithium-ion batteries represented around 56.0% share by battery type, driven by higher energy density, longer battery life, faster charging, and better performance compared with traditional battery options.

OEM sales channels accounted for around 62.3% share, supported by increasing integration of electric propulsion systems in newly manufactured boats and vessels.

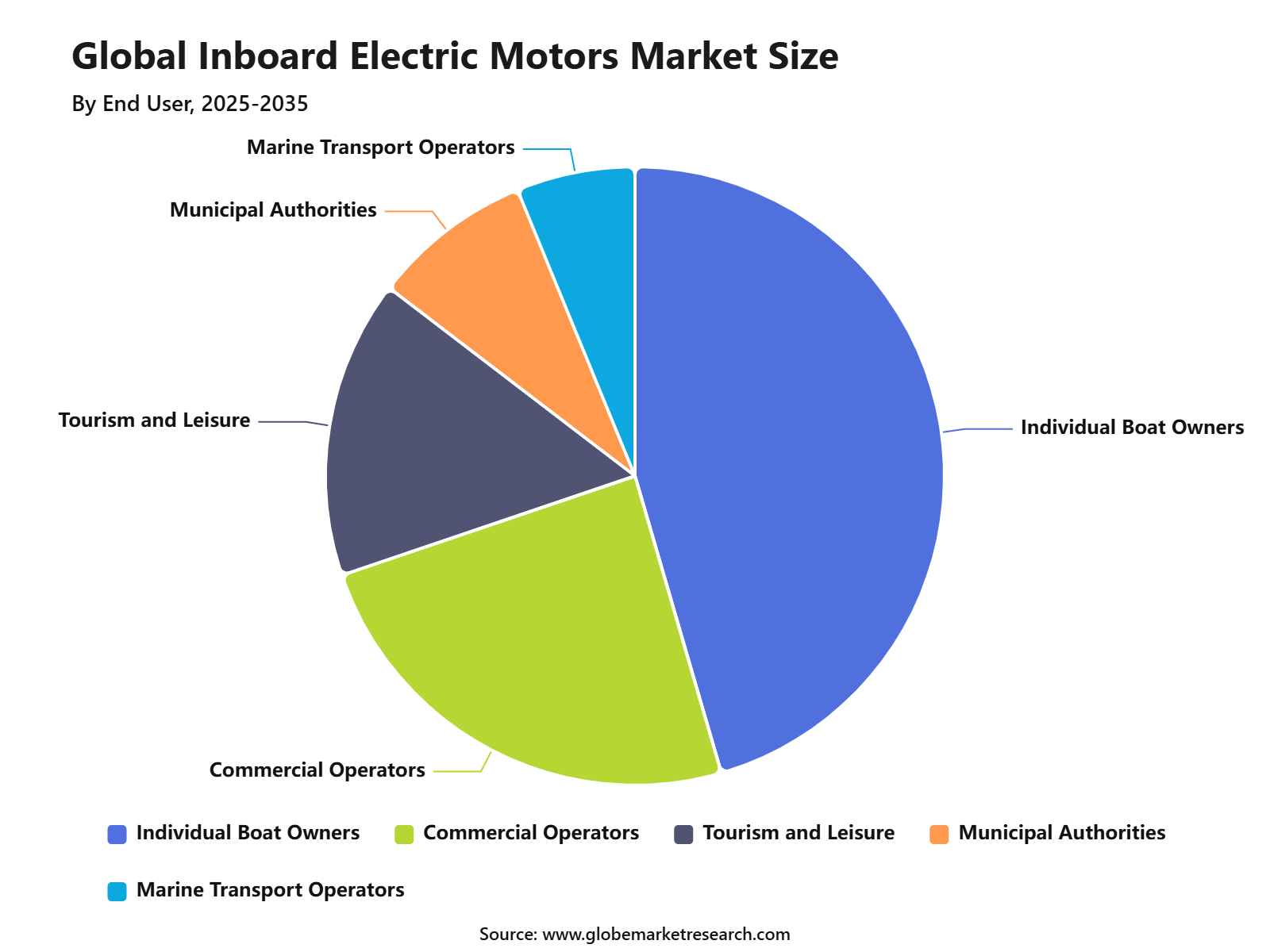

Individual boat owners held an estimated 45.5% share by end user, driven by rising interest in sustainable boating, lower operating costs, and improved user experience.

Asia Pacific captured 40.7% share of the inboard electric motors market, supported by growing marine tourism, rising boat production, and increasing adoption of electric mobility across coastal economies.

Type Insights

Low power inboard electric motors below 10 HP led the type segment with 50.6% share in 2025. The segment’s leadership can be attributed to strong use in small boats, dinghies, tenders, lake boats, fishing boats, and leisure craft where quiet operation, easy handling, and lower running cost are important. These motors are suitable for short-distance movement and light-duty boating, where high propulsion output is not always required.

The segment also benefits from growing preference for clean and low-noise boating in lakes, inland waterways, marinas, and eco-sensitive water bodies. Low power systems are easier to install, require less battery capacity, and are more practical for individual boat owners. This makes below 10 HP motors a preferred entry point for electric propulsion adoption.

Application Insights

Civil entertainment held the leading application share of 45.3% in 2025, supported by rising use of electric boats for leisure rides, lake cruising, tourism, fishing, private recreation, and short-distance water activities. This segment benefits from consumer interest in quieter and more comfortable boating experiences. Electric inboard motors are especially useful in recreational settings where smooth operation and low vibration improve the user experience.

The growth of this segment is also supported by marina-based leisure activity and water tourism. Many users prefer electric propulsion because it reduces fuel handling, lowers engine noise, and supports cleaner operation during short trips. As recreational boating becomes more experience-focused, civil entertainment continues to remain a major demand area for inboard electric motors.

Boat / Vessel Type Insights

Recreational boats led the boat and vessel type segment with around 57.3% share in 2025. The segment’s dominance is supported by strong demand from private boat owners, leisure users, fishing enthusiasts, lake operators, and small tourism businesses. Electric inboard motors are well suited for recreational boats because they offer quiet operation, smoother acceleration, and lower routine maintenance compared with traditional fuel-based systems.

The segment also gains from rising interest in sustainable and low-emission boating. Recreational users often operate boats in lakes, rivers, coastal areas, and protected water zones where noise and emissions are becoming more important concerns. This is increasing demand for electric propulsion systems that can support clean leisure boating without reducing comfort.

Battery Type Insights

Lithium-ion batteries held the leading battery type share of around 56.0% in 2025. Their leadership is supported by higher energy density, faster charging potential, lighter weight, and better cycle life compared with many older battery technologies. In electric boats, these factors are important because weight, space, range, and power delivery directly affect performance.

The segment is also supported by wider use of lithium-based batteries in electric mobility and marine energy storage systems. For inboard electric motors, lithium-ion batteries help improve acceleration, operating time, and system efficiency. Although battery safety, cost, and thermal management remain important issues, lithium-ion systems continue to be the preferred battery choice for modern electric boating applications.

Sales Channel Insights

OEMs led the sales channel segment with around 62.3% share in 2025. This dominance is supported by the growing integration of electric propulsion systems directly into newly built boats. Boat manufacturers prefer OEM integration because it allows better alignment between the motor, battery, hull design, control system, charging setup, and onboard electronics.

The OEM channel also benefits from rising demand for factory-fitted electric boats. Buyers increasingly prefer complete propulsion packages that are tested, certified, and supported by the manufacturer. This reduces installation complexity and improves confidence in performance, safety, and warranty coverage. As electric boat designs become more standardized, OEMs are expected to remain the main sales channel.

End User Insights

Individual boat owners held the leading end-user share at an estimated 45.5% in 2025. The segment is supported by private users who operate boats for leisure, fishing, family trips, lake cruising, and short-distance recreation. Electric inboard motors are attractive to this group because they offer quiet operation, lower maintenance needs, and easier day-to-day use.

The segment also benefits from the growing preference for personal recreational experiences. Many boat owners are looking for propulsion systems that are simple, clean, and suitable for regular weekend use. Electric inboard motors meet these needs, especially for users who operate on inland waters or in areas where fuel engine restrictions and noise limits are becoming more common.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Insights

Asia Pacific held the leading regional share of 40.7% in 2025, supported by strong coastal tourism, expanding marine leisure activity, rising disposable income, and growing interest in cleaner mobility technologies. Countries with large coastlines, island tourism, lake destinations, and inland waterways provide a strong base for electric boat adoption. The region also benefits from growing manufacturing capacity across batteries, motors, and electric mobility components.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe region’s leadership is further supported by increasing focus on sustainable tourism and low-emission transport. Electric propulsion is gaining attention across recreational boating, water tourism, ferries, and short-distance marine mobility. As charging infrastructure, battery supply, and marina development improve, Asia Pacific is expected to remain an important market for inboard electric motors.

Regional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +1.6% | China, Japan, South Korea, Australia | Drives volume growth. |

Europe emission-led adoption | +1.3% | Norway, Netherlands, Germany, France | Supports clean boating. |

North America recreational boating demand | +1.2% | U.S. and Canada | Strengthens premium sales. |

Middle East luxury marine adoption | +0.6% | UAE, Saudi Arabia, Qatar | Supports yacht demand. |

Latin America emerging opportunity | +0.5% | Brazil, Mexico, Chile | Builds gradual adoption. |

Go-to-Market and Sales Economics

The Inboard Electric Motors Market is positioned around clean propulsion, lower operating noise, reduced fuel dependence, and improved vessel efficiency. The main go-to-market focus is expected to remain on boat builders, yacht manufacturers, retrofit service providers, marina operators, tourism fleets, passenger boat operators, and commercial vessel owners. Sales economics are strongly linked to battery cost, charging access, vessel range, installation complexity, and fuel savings.

In 2026, maritime electrification is being supported by broader battery industry progress, with global electric car sales expected to reach about 23 million units and electric cars expected to represent nearly 28 out of every 100 new cars sold worldwide. This matters for inboard electric motors because higher battery production can improve supplier scale, component availability, battery management systems, and power electronics quality across transport markets.

Customer acquisition in this market depends on proving practical value rather than only promoting sustainability. Buyers usually want evidence of lower maintenance, fewer moving parts, smoother acceleration, quieter operation, and predictable service support. As of mid-May 2026, about 1,900 electrified vessels were registered globally as operational or on order, showing that marine electrification is no longer limited to pilot projects. This supports the sales case for electric inboard motor suppliers, especially in ferries, inland vessels, tourism boats, yachts, and short-distance commercial routes.

Market Adoption Barriers

High upfront cost remains the leading adoption barrier in the Inboard Electric Motors Market. Buyers must consider the cost of the electric motor, battery pack, inverter, control system, cooling system, charging connection, installation labor, marine certification, and after-sales service. Battery price uncertainty can affect purchase planning because lithium prices at the beginning of 2026 were more than double the same period in 2025, although they remained around 70% lower than the 2022 peak. This creates a mixed cost environment, where long-term battery progress supports adoption but short-term raw material movement can affect pricing.

Charging infrastructure is another major barrier. Electric inboard motors are most practical when boats follow predictable routes and can return to reliable charging points. A 2026 clean maritime funding scope in the U.K. specifically includes 100% battery electric vessels, port-based charging systems, localized energy generation, load management, and energy storage for passenger, freight, pleasure, and commercial vessels. This shows that infrastructure is now being treated as a necessary part of electric vessel deployment, not only as an optional add-on.

Range anxiety and buyer confidence can also slow adoption. Boat owners and fleet operators may hesitate if they are unsure about cruising range, charging time, battery life, saltwater durability, service access, or resale value. This is especially important for larger recreational boats and commercial vessels that need higher power output and longer operating hours. Adoption is expected to be stronger where routes are short, charging access is fixed, maintenance savings are clear, and the operating profile matches battery capacity.

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Shift toward low-emission boating | +1.4% | Europe, North America, Asia Pacific | Supports electric demand. |

Lithium-ion battery adoption | +1.2% | Global | Improves motor performance. |

Growth of OEM-fitted electric propulsion | +1.0% | U.S., Europe, Japan, China | Strengthens new boat sales. |

Hybrid-electric marine systems | +0.9% | Commercial and leisure vessels | Expands use cases. |

Smart propulsion monitoring | +0.7% | Developed boating markets | Improves system control. |

Investment Opportunity Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Recreational electric boat propulsion | +1.3% | North America, Europe, Asia Pacific | Offers steady growth. |

Lithium-ion battery integration | +1.1% | Global | Supports performance gains. |

OEM electric motor supply contracts | +1.0% | Europe, U.S., China, Japan | Builds long-term revenue. |

Marina charging infrastructure | +0.8% | Developed boating markets | Enables adoption growth. |

Electric retrofit kits | +0.7% | Aftermarket and small boat users | Opens replacement demand. |

Segments Covered in the Report

By Type

Low Power Below 10 HP

Medium Power 10 to 35 HP

Large Power Above 35 HP

By Application

Civil Entertainment

Municipal

Commercial

Other Applications

By Boat / Vessel Type

Recreational Boats

Yachts

Fishing Boats

Workboats

Passenger Boats

Commercial Vessels

By Battery Type

Lithium-ion Batteries

Lead-acid Batteries

Nickel-based Batteries

Other Battery Types

By Sales Channel

OEM

Aftermarket

By End User

Individual Boat Owners

Commercial Operators

Tourism and Leisure Operators

Municipal Authorities

Marine Transport Operators

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for electric propulsion in boats | +1.5% | Europe, North America, Asia Pacific | Drives clean marine adoption. |

Growing recreational boating activity | +1.2% | U.S., Europe, Australia, Japan | Supports motor demand. |

Stricter emission rules for marine engines | +1.0% | Europe, North America, developed Asia | Encourages electric conversion. |

Lower operating noise and vibration | +0.9% | Recreational and tourism boating markets | Improves user experience. |

Rising fuel cost and maintenance savings | +0.8% | Global | Supports electric shift. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in recreational electric boats | +1.4% | North America, Europe, Asia Pacific | Expands core demand. |

Expansion of electric yachts and leisure vessels | +1.1% | Europe, U.S., GCC, Australia | Supports premium adoption. |

Battery technology improvement | +1.0% | Global | Extends vessel range. |

OEM partnerships with boat manufacturers | +0.9% | Europe, North America, Asia Pacific | Improves market access. |

Growth in eco-tourism boating | +0.8% | Europe, Asia Pacific, island markets | Supports sustainable fleets. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Battery weight and space constraints | -0.8% | Small and medium vessels | Affects boat design. |

Slow marina electrification | -0.7% | Global coastal and inland markets | Limits charging access. |

Performance concerns versus diesel engines | -0.6% | Commercial and heavy-duty users | Slows adoption. |

Supply chain pressure for batteries | -0.5% | Global | Raises production risk. |

Safety and certification requirements | -0.5% | U.S., Europe, Asia Pacific | Increases compliance needs. |

Recent Developments

January 2026 - VETUS launched the E-LINE 22 kW electric inboard motor. The system delivers 22 KW output and 130 Nm torque. It is designed for vessels up to 15 m or 20 tons. The product supports both new builds and diesel engine replacement projects.

May 2025 - Volvo Penta unveiled its electric IPS marine propulsion range. The rollout is planned from Q4 2025, starting with the IPS900E with power up to 515 KW. The wider electric IPS range covers 220 kW to 1.1 MW per driveline, scalable up to 4.5 MW in quad setups.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 7.8 Bn |

Forecast Revenue (2035) | USD 13.1 Bn |

CAGR (2025-2035) | 5.3% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Type(Low Power Below 10 HP, Medium Power 10 to 35 HP, Large Power Above 35 HP), By Application (Civil Entertainment, Municipal, Commercial, Other Applications), By Boat / Vessel Type (Recreational Boats, Yachts, Fishing Boats, Workboats, Passenger Boats, Commercial Vessels), By Battery Type (Lithium-ion Batteries, Lead-acid Batteries, Nickel-based Batteries, Other Battery Types), By Sales Channel (OEM, Aftermarket), By End User (Individual Boat Owners, Commercial Operators, Tourism and Leisure Operators, Municipal Authorities, Marine Transport Operators), By Regional Insights |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Torqeedo GmbH, ePropulsion Technology Limited, Elco Motor Yachts, Vision Marine Technologies Inc., Evoy AS, Bellmarine, Oceanvolt, RAD Propulsion, Combi Outboards, Yamaha Motor Co., Ltd., Mercury Marine, Volvo Penta, Siemens AG, ABB Ltd., WEG S.A., Lynch Motors, Kräutler Elektromaschinen GmbH, Pure Watercraft, Aquamot GmbH, Other Key Players. |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Torqeedo GmbH

ePropulsion Technology Limited

Elco Motor Yachts

Vision Marine Technologies Inc.

Evoy AS

Bellmarine

Oceanvolt

RAD Propulsion

Combi Outboards

Yamaha Motor Co., Ltd.

Mercury Marine

Volvo Penta

Siemens AG

ABB Ltd.

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Suraj is a Senior Management Consultant with over 7 years of experience in market research, business strategy, and consulting. He has worked with Fortune 500 companies and growing startups, helping them with market entry, cross-border expansion, demand analysis, competitive assessment, and growth planning. His analytical thinking and strong industry knowledge help clients make clear, confident, and informed business decisions.

Frequently Asked Questions

Related Reports

More in Automotive and Transportation

Automotive AI Agents Market to hit 16.5 Bn by 2035

Global Automotive AI Agents Market By Agent Type (Conversational AI Agents, Autonomous Driving AI Agents, Predictive Maintenance AI Agents, Fleet Management AI Agents and Others), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles (EVs), Autonomous Vehicles), By Application (Driver Assistance & Safety, In-Vehicle Virtual Assistants, Predictive Maintenance, Fleet & Logistics Management, Infotainment Personalization), By Deployment Type (Cloud-Based AI Agents, Edge/On-Board AI Agents, Hybrid Deployment), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Chauffeur Car Market to Exceed USD 403.8 Billion by 2035

By Service Type (Business Travel Services, Leisure Travel Services, Airport Transfers, Event-specific Services), By Vehicle Type (Luxury Cars, Executive Cars, SUVs, Vans, Limousines), By Customer Type (Corporate Clients, Individual Customers, Tourist and Leisure Travelers), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Automotive Alternator & Starter Motor Market to Hit USD 62.8 Bn by 2035

Global Automotive Alternator & Starter Motor Market Size, Share and AI Impact Analysis By Product (Alternator, Starter Motor), By Vehicle Type (Passenger vehicle, Commercial Vehicle, Off-road Vehicle), By Sales Channel (OEM, Aftermarket), By Regional Insights, Leading Companies and Growth Forecasts By 2025-2035