Revenue, 2025

$4,640.0 Bn

Forecast, 2035

$8,602.5 Bn

CAGR, 2025-2035

7.3%

Report Coverage

Global

Market Size and Forecast

The Real Estate Market was valued at USD 4,640.0 billion in 2025 and is projected to reach USD 8,602.5 billion by 2035, reflecting steady long-term expansion across residential, commercial, and income-generating property assets. The market growth can be attributed to rising urban housing demand, strong commercial leasing activity, infrastructure-led development, and increasing investment in rental and institutional real estate assets.

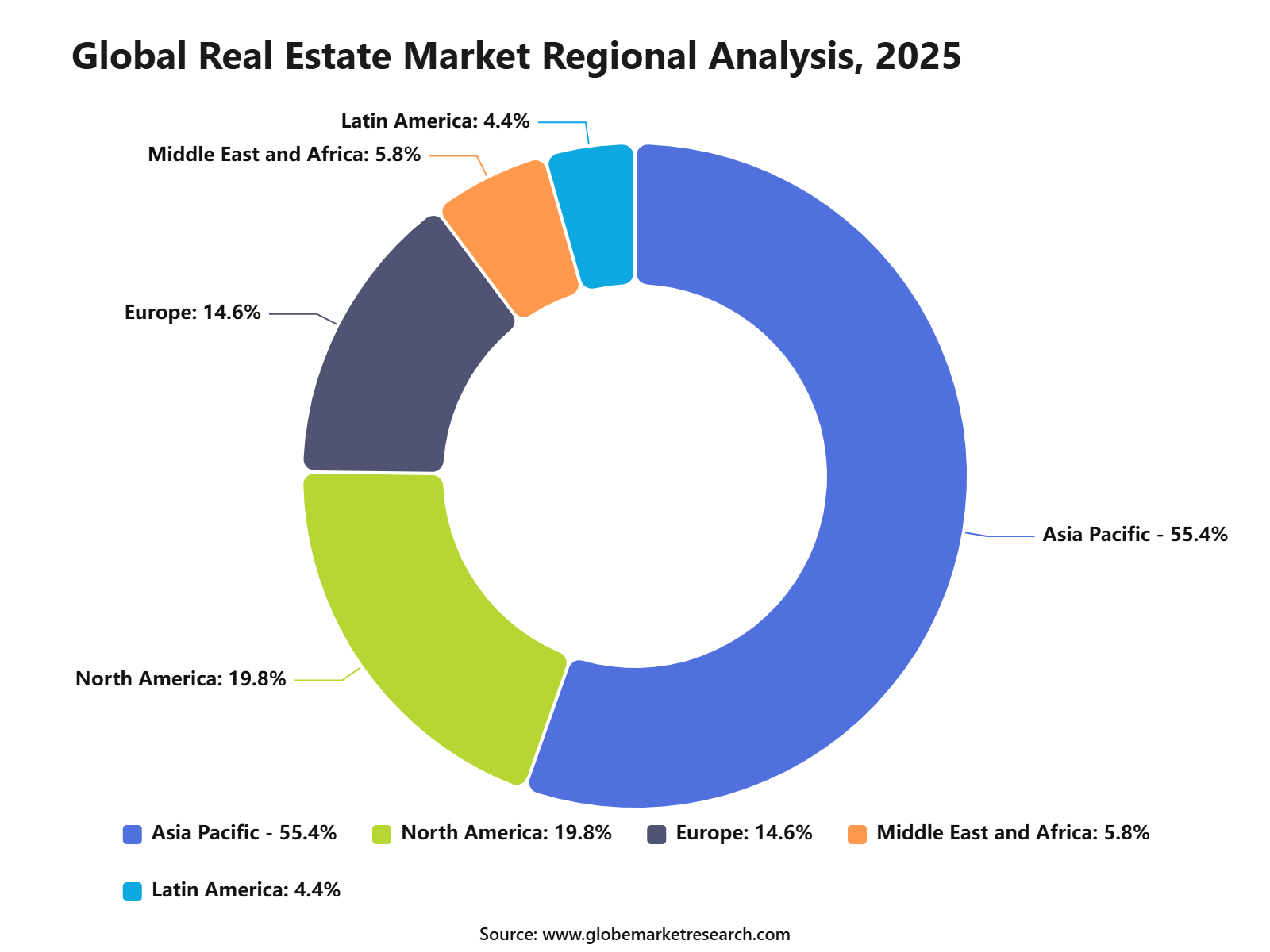

Asia Pacific led the market with a 54.6% share in 2025, representing approximately USD 2,533.4 billion. The region’s dominance was supported by large urban populations, rapid construction activity, expanding middle-income housing demand, and strong real estate investment across China, India, Japan, South Korea, and Southeast Asia. The market is expected to maintain stable growth as urbanization, industrial development, and infrastructure spending continue to support property demand across major economies.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Residential real estate led the market with a 75.1% share. Growth was supported by urban housing demand, population growth, and rising home ownership needs.

Healthcare real estate held a 19.6% share in the commercial asset segment. Demand was driven by hospitals, clinics, diagnostic centers, and senior care facilities.

Leasing and renting accounted for a 42.3% share by service type. Growth was supported by flexible housing needs, commercial leasing, and rising rental demand.

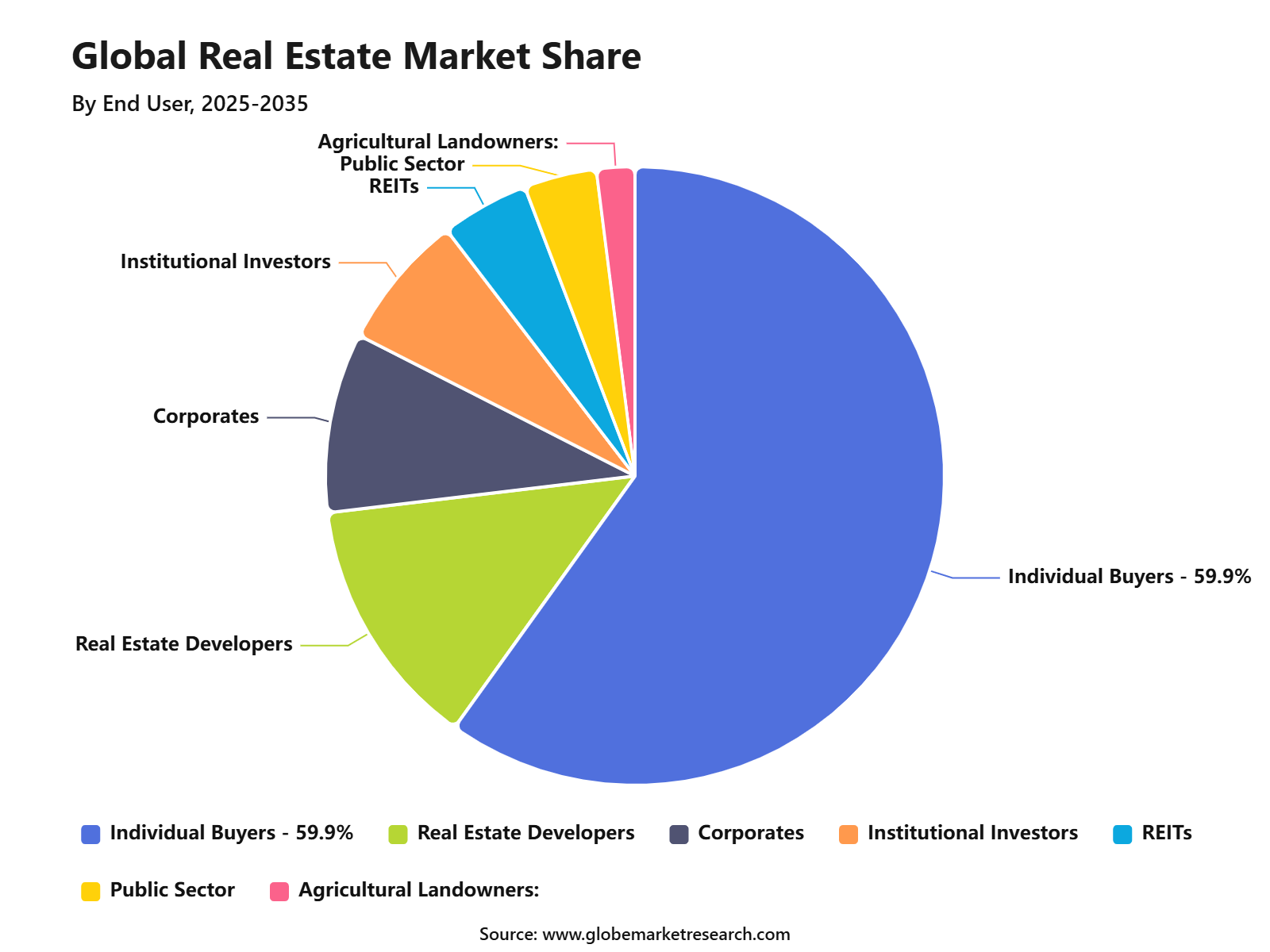

Individual buyers and renters held around a 59.9% share. Demand was supported by household formation, migration, affordability needs, and lifestyle changes.

Asia Pacific led the real estate market with a 55.4% share. Growth was supported by urbanization, infrastructure development, rising income levels, and strong residential demand.

Customer Acquisition Strategy

The Real Estate Market requires a location-led and buyer-segment-led go-to-market strategy. Developers, brokers, property managers, and investors need to separate demand across residential housing, commercial assets, rental housing, logistics, healthcare real estate, data centers, and mixed-use properties. Sales economics are strongly influenced by land cost, approval time, construction material prices, financing rates, and buyer affordability. In the U.S., Freddie Mac reported that the 30-year fixed mortgage rate averaged 6.47% as of June 2026, compared with 6.81% a year earlier, showing some relief but still keeping borrowing costs elevated.

For residential real estate, the sales model should focus on affordability, financing support, transparent pricing, and quick possession. For commercial real estate, the stronger sales focus is on lease stability, tenant quality, occupancy, location productivity, and refinancing strength. In May 2026, U.S. housing permits were at an annual rate of 1.413 million units, while single-family authorizations reached 886,000 units, showing that construction activity remains active but cautious.

Tariff Impact

Tariffs affect the Real Estate Market mainly through construction costs, imported building materials, appliances, steel, aluminum, copper, timber, cabinets, and electrical systems. Higher input costs can reduce developer margins, delay new projects, and push selling prices higher for homebuyers and commercial tenants. The White House stated that the U.S. tariff regime includes a 50% ad valorem duty on selected steel, aluminum, and copper products, with 25% on some derivative products and 15% on selected industrial machinery and power equipment.

The impact is stronger in residential and commercial construction because builders cannot always pass higher costs to buyers when affordability is weak. NAHB stated that tariffs are expected to raise the cost of imported construction materials by billions of dollars, depending on the specific rate and product category. This creates pressure on procurement planning, vendor contracts, project budgets, and delivery timelines, especially for developers that depend on imported fixtures, metals, wood products, and equipment.

Revenue Potential Analysis

Revenue Landscape Across

Revenue in the Real Estate Market is spread across residential sales, leasing, renting, property management, commercial leasing, asset management, development, valuation, advisory, and financing services. Residential real estate remains a core revenue base because housing is a primary household need, while rental housing is gaining importance as affordability remains tight. In Europe, Reuters reported that Spain recorded more than 750,000 property sales in 2025, with about 52% of purchases mortgage-financed, showing that demand can remain active even when affordability is under pressure.

Commercial revenue is supported by tenant demand in logistics, healthcare, education, data centers, industrial parks, and modern mixed-use projects. The strongest revenue potential is expected where assets solve clear user needs, such as last-mile distribution, medical access, student housing, senior living, and digital infrastructure. For developers and investors, the revenue landscape is becoming more selective, with higher value placed on location quality, asset efficiency, lease durability, and financing strength.

Financial Impact

The financial impact is mixed but remains attractive for well-capitalized developers and investors with strong land banks, low leverage, and disciplined project selection. Higher mortgage rates and construction costs can reduce short-term sales velocity, but rental income, long-term leases, and asset appreciation can support stable returns over time. BIS data showed that global real house prices fell 0.7% year-on-year in Q3 2025, even though nominal prices rose 2%, showing that inflation-adjusted property returns remain uneven across markets.

Financial performance will depend on capital structure, debt maturity, occupancy, rental growth, and cost control. Construction material pressure remains important, as the U.S. construction materials producer price index reached 363.253 in May 2026, compared with 347.872 in January 2026. This rise shows that developers need stronger procurement planning, escalation clauses, phased construction budgets, and realistic margin assumptions to protect project profitability.

By Property Type Analysis

Residential real estate led the Real Estate Market with a 75.1% share in 2025. Growth was supported by steady housing demand, urban migration, household formation, and rising preference for owned and rented living spaces. Residential assets remained the core of the market because housing is a basic need across income groups, cities, and developing economies.

The segment also benefited from continued urban expansion. The World Bank states that cities generate about 80% of global GDP, while nearly 7 in 10 people are expected to live in urban areas by 2050. This long-term urban shift continues to support demand for apartments, plotted developments, affordable housing, and mixed-use residential communities.

By Commercial Asset Type Analysis

Healthcare real estate accounted for a 19.6% share in 2025 within the commercial asset type segment. Demand was supported by hospitals, clinics, diagnostic centers, specialty care facilities, senior care centers, and medical office buildings. This asset class gained importance as healthcare providers expanded physical infrastructure to improve access, patient capacity, and service delivery.

The segment is being supported by ageing populations and rising care requirements. WHO reported that by 2030, 1 in 6 people globally will be aged 60 years or older, while the population aged 60 and above is expected to reach 2.1 billion by 2050. This demographic shift is increasing demand for healthcare spaces, long-term care facilities, rehabilitation centers, and outpatient care properties.

By Service Type Analysis

Leasing and renting led the service type segment with a 42.3% share in 2025. Growth was supported by high property prices, urban workforce mobility, flexible living needs, and rising demand for commercial lease structures. Renting remained important for households, businesses, retailers, healthcare operators, and logistics users that preferred lower upfront capital commitment.

The segment also benefited from affordability pressure in housing markets. OECD data shows that about 24% of households across OECD countries rented their homes on average in 2022, while rental housing remains higher in several European markets. This supports the continued role of leasing and renting as a major real estate service category.

By End User Analysis

Individual buyers and renters accounted for around 59.9% share in 2025. Growth was supported by demand for primary homes, rental apartments, second homes, affordable housing, and urban living spaces. This end-user group remained dominant because real estate decisions are strongly linked to household income, family needs, job location, lifestyle preference, and long-term wealth creation.

Demand from individuals was also shaped by affordability and access to suitable housing. OECD notes that one in three low-income tenant households are considered overburdened by housing costs because they spend over 40% of disposable income on housing. This shows why both ownership and rental options remain central to real estate demand, especially in cities with rising land and housing costs.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Regional Analysis

Asia Pacific led the Real Estate Market with a 55.4% share in 2025. Growth was supported by large population bases, rapid city development, infrastructure investment, rising middle-class income, and strong demand for residential and commercial properties. Countries such as China, India, Japan, South Korea, Australia, Indonesia, and Vietnam continued to support regional activity across housing, offices, logistics, retail, and healthcare spaces.

The region’s leadership is strongly linked to urbanization. UN-Habitat states that Asia’s urban population is expected to grow by 50% by 2050, adding about 1.2 billion people. This expansion is expected to increase demand for housing, transport-linked developments, healthcare infrastructure, commercial hubs, and planned urban communities across Asia Pacific.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFSegment covered in the Report

By Property Type

Residential Real Estate

Commercial Real Estate

Agricultural Land

By Commercial Asset Type

Office and Business Space

Retail

Industrial and Logistics

Hospitality

Healthcare Real Estate

Education Real Estate

Data Centers

Mixed-use Properties

Student Accommodation

Affordable Housing

By Service Type

Buying and Selling

Leasing and Renting

Property Management

Asset Management

Valuation

Development

Finance

Advisory and Consultancy

By End User

Individual Buyers and Renters

Real Estate Developers

Corporates

Institutional Investors

REITs

Government and Public Sector

Agricultural Landowners

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising urban population | +1.7% | Asia Pacific, North America, Middle East | Drives housing demand. |

Growth in residential property demand | +1.5% | Global urban markets | Supports transaction volume. |

Expansion of commercial leasing | +1.2% | U.S., Europe, Asia Pacific | Strengthens rental income. |

Infrastructure and smart city development | +1.1% | India, China, GCC, Southeast Asia | Improves property value. |

Rising investment in rental assets | +0.9% | North America, Europe, Asia Pacific | Supports recurring revenue. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High property prices | -1.0% | Global metro markets | Limits affordability. |

Rising mortgage interest rates | -0.9% | North America, Europe, developed Asia | Slows home buying. |

Regulatory approval delays | -0.7% | Asia Pacific, Latin America, MEA | Delays project execution. |

Construction cost inflation | -0.6% | Global | Pressures developer margins. |

Land availability constraints | -0.5% | Dense urban markets | Limits new supply. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in affordable housing projects | +1.5% | Asia Pacific, Africa, Latin America | Expands buyer base. |

Expansion of healthcare real estate | +1.2% | North America, Europe, Asia Pacific | Supports specialized assets. |

Rising demand for rental housing | +1.1% | Urban global markets | Builds steady income. |

Growth in data centers and logistics assets | +1.0% | U.S., Europe, Asia Pacific | Creates high-value demand. |

PropTech-enabled property transactions | +0.8% | Developed and urban markets | Improves market efficiency. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Housing affordability pressure | -0.9% | Global cities | Reduces buyer access. |

Market cyclicality and price corrections | -0.8% | Global | Creates investment risk. |

Delayed construction timelines | -0.6% | Emerging markets | Slows supply delivery. |

Climate risk for property assets | -0.5% | Coastal and flood-prone regions | Raises insurance cost. |

Vacancy risk in commercial assets | -0.5% | Office-heavy markets | Impacts rental yield. |

Recent Developments

June 2026: Emaar Properties announced plans to develop a nearly USD 55 billion urban district in Dubai. The project is expected to cover around 4.5 million square meters and accommodate nearly 150,000 residents, with residential towers, villas, offices, and retail spaces included in the master plan.

June 2026: Warburg Pincus agreed to acquire Japan-based student housing provider J.S.B. in a deal valued at about USD 1.2 billion. The deal strengthens Warburg Pincus’ position in Japan’s rental housing segment and marks its first take-private transaction in Japan since opening its Tokyo office in 2025.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 4,640.0 Billion |

Forecast Revenue (2035) | USD 8,602.5 Billion |

CAGR (2025-2035) | 7.3% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Property Type (Residential Real Estate, Commercial Real Estate, Agricultural Land), By Commercial Asset Type (Office and Business Space, Retail, Industrial and Logistics, Hospitality, Healthcare Real Estate, Education Real Estate, Data Centers, Mixed-use Properties, Student Accommodation, Affordable Housing), By Service Type (Buying and Selling, Leasing and Renting, Property Management, Asset Management, Valuation, Development, Finance, Advisory and Consultancy), By End User (Individual Buyers and Renters, Real Estate Developers, Corporates, Institutional Investors, REITs, Government and Public Sector, Agricultural Landowners) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Brookfield Asset Management Inc., ATC IP LLC., Prologis, Inc., Simon Property Group, L.P., Coldwell Banker, RE/MAX, LLC., Keller Williams Realty, Inc., CBRE Group, Inc., Sotheby’s International Realty Affiliates LLC., Colliers |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Prologis, Inc.

Coldwell Banker

SIMON PROPERTY GROUP, L.P.

Brookfield Asset Management Inc.

Keller Williams Realty, Inc.

CBRE Group, Inc.

Sotheby’s International Realty Affiliates LLC.

Colliers

JLL

Cushman & Wakefield

Savills plc

Blackstone Inc.

Welltower Inc.

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Manufacturing and Construction

Sustainable Construction Materials Market to hit USD 1,878.8 billion by 2035

Global Sustainable Construction Materials Market Size, Go-to-Market Analysis By Material Type (Green Cement, Bamboo, Recycled Glass, Hempcrete, Recycled Tires, Reclaimed Wood, Cork, Mycelium, Ferrock, Sheep Wool, Recycled Metal, Recycled Plastic, Ashcrete, Timbercrete, Cellulose Fiber), By Application (Exterior, Interior, Structural, Others), By End User (Residential, Commercial (Offices, Institutes,Hospitality & Leisure), Industrial), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Industrial Robotics Market to hit USD 192.1 billion by 2035

Global Industrial Robotics Market Size, Share Analysis By Robot Type (Articulated Robots, Linear Robots, SCARA Robots, Collaborative Robots, Cartesian / Gantry Robots, Parallel / Delta Robots, Cylindrical Robots), By Payload Capacity (Up to 15 kg, 16 to 225 kg, 226 to 500 kg, Above 500 kg), By Application (Material Handling and Packaging, Welding and Soldering, Assembly and Dispensing, Machine Tending and CNC, Painting and Coating, Quality Inspection), By End-User Industry (Automotive, Electrical and Electronics, Food and Beverage, Machinery and Metal, Pharmaceuticals and Healthcare, Construction Materials, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035