Revenue, 2025

$548.6Bn

Forecast, 2035

$1,878.8Bn

CAGR, 2025-2035

13.1%

Report Coverage

Global

Market Size and Forecast

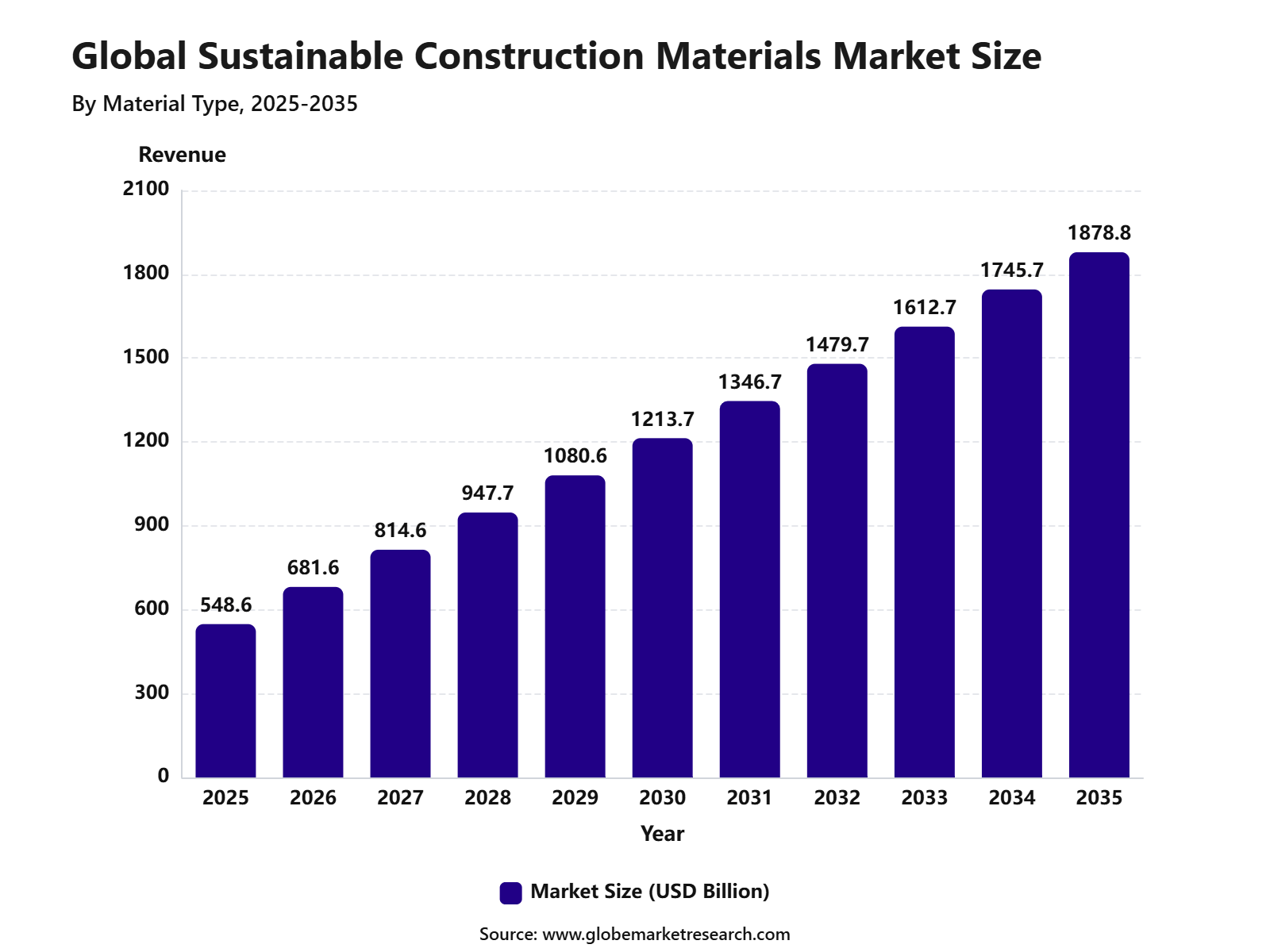

The Global Sustainable Construction Materials Market was valued at USD 548.6 billion in 2025 and is projected to reach USD 1,878.8 billion by 2035, growing at a CAGR of 13.1% during the forecast period. North America held a leading regional share of 46.1% in 2025, supported by strong green building adoption, stricter energy efficiency standards, rising investment in low-carbon construction, and growing demand for recycled and environmentally responsible building materials.

Sustainable construction materials include green concrete, recycled steel, engineered wood, bamboo, low-carbon cement, recycled plastics, insulation materials, and other products designed to reduce environmental impact across the building lifecycle. The growth of the market can be attributed to increasing pressure to lower carbon emissions from buildings, rising use of energy-efficient materials, and growing preference for durable products that reduce waste and improve long-term construction performance.

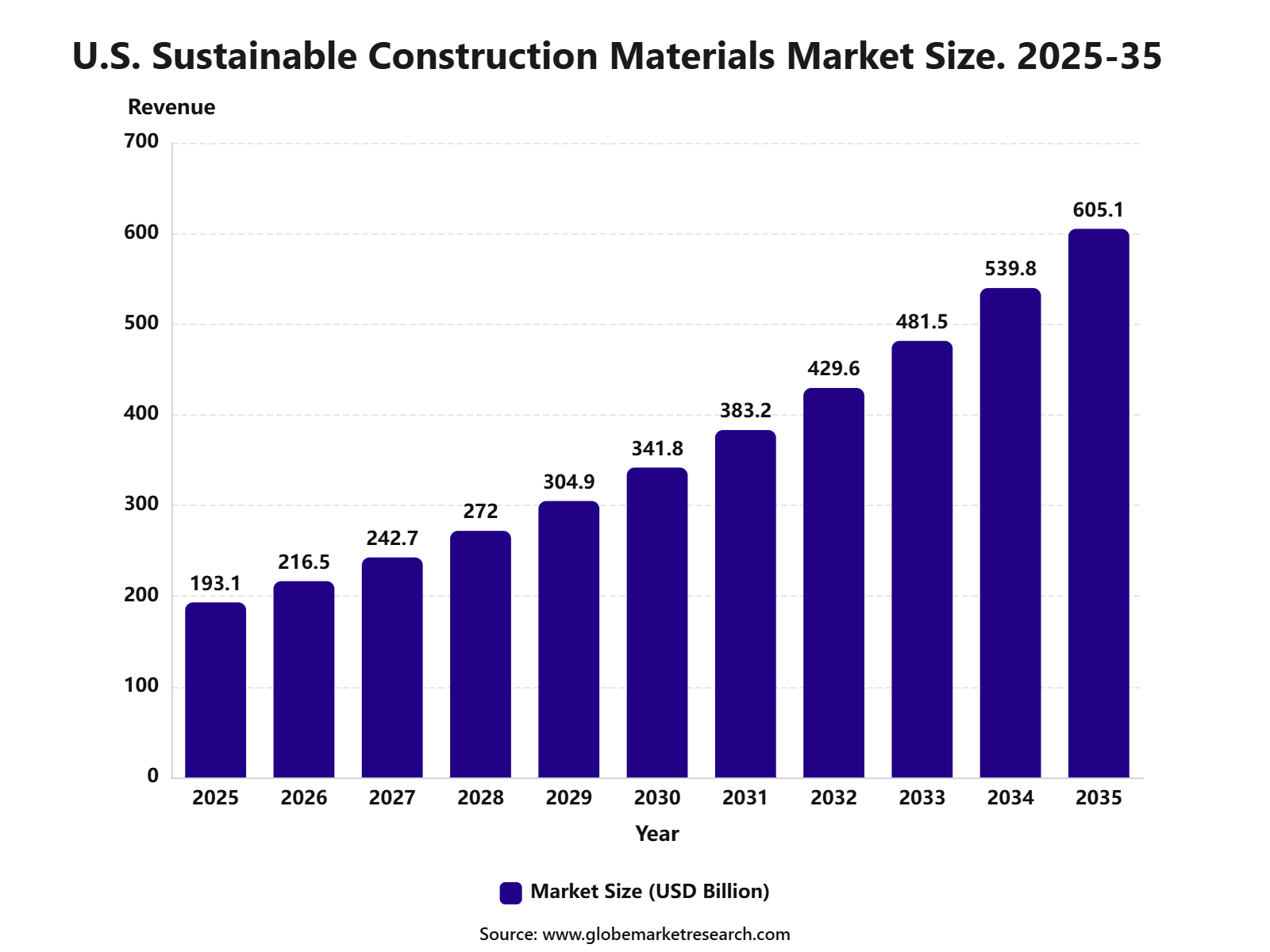

The U.S. Sustainable Construction Materials Market was valued at USD 193.1 billion and is expected to grow at a CAGR of 12.1% during the forecast period. Growth in the U.S. is being driven by expanding green building projects, renovation of aging infrastructure, stricter sustainability requirements, and rising adoption of certified materials in residential, commercial, and public construction. The market outlook remains positive as governments, builders, architects, and real estate developers increase the use of low-carbon and resource-efficient materials.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Bamboo led the material type segment with 42.0% share, supported by its fast renewability, high strength-to-weight ratio, lower environmental impact, and growing use in green building projects.

Structural applications accounted for 39.1% share, driven by rising demand for sustainable materials in beams, panels, flooring, walls, roofing, and load-bearing construction elements.

Residential construction held 35.6% share by end user, supported by increasing adoption of eco-friendly homes, energy-efficient buildings, and low-carbon construction practices.

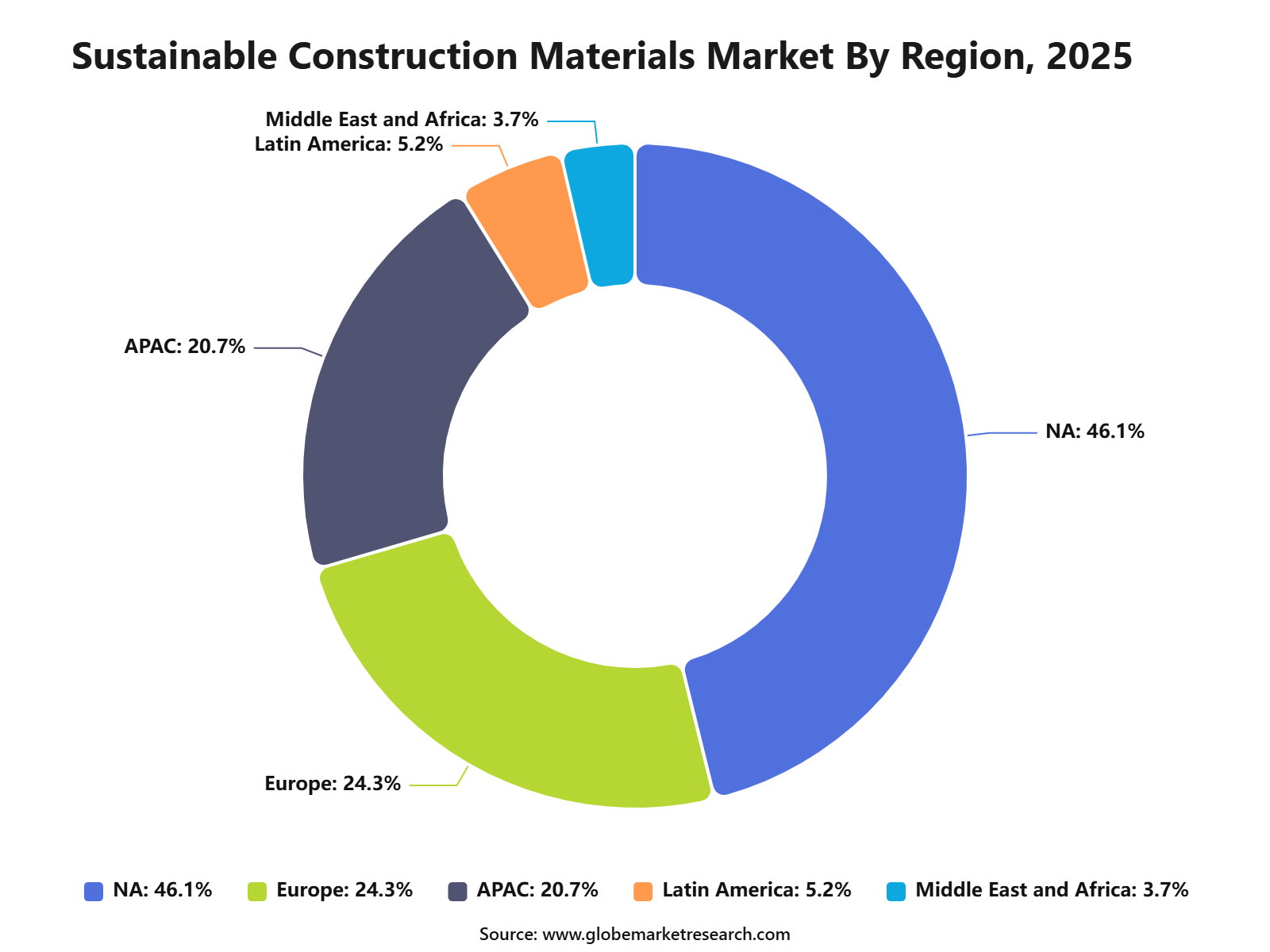

North America led the sustainable construction materials market with 46.1% share, supported by green building standards, rising renovation activity, strong sustainability targets, and growing demand for low-emission building materials.

Go-to-Market Strategy

The Sustainable Construction Materials Market needs a compliance-led and performance-led go-to-market strategy. Buyers are not only looking for lower-carbon materials, but they are also looking for materials that meet building codes, reduce lifecycle emissions, improve energy efficiency, and support green building certification. UNEP reported that the buildings and construction sector consumed 32% of global energy and contributed 34% of global CO2 emissions, while materials such as cement and steel were responsible for 18% of global emissions.

Sales economics are strongly linked to material cost, certification cost, contractor acceptance, and project-level payback. Sustainable materials can create value through lower operating costs, green procurement eligibility, faster approval in low-carbon projects, and stronger investor appeal. However, price pressure remains high, as the U.S. construction materials producer price index reached 363.253 in May 2026, compared with 347.872 in January 2026. This shows why suppliers need clear cost-benefit proof, not only environmental claims.

Tariff Impact

Tariffs can affect the Sustainable Construction Materials Market through steel, aluminum, copper, timber, HVAC components, machinery, fasteners, electrical systems, and imported building products. The White House’s June 2026 tariff update listed a 50% duty on products made of steel, aluminum, or copper, a 25% duty on many derivative products, and a temporarily reduced 15% duty on selected fixed industrial machinery and power equipment. These duties can raise costs for green buildings because sustainable construction still depends on structural metals, equipment, wiring, façades, and mechanical systems.

Tariff pressure may also support local sourcing, recycled-content materials, and regionally produced low-carbon alternatives. NAHB stated that tariffs are projected to raise the cost of imported construction materials by billions of dollars, depending on the rate and product category. For suppliers, this creates an opportunity to promote domestic materials, recycled aggregates, local timber, low-carbon cement blends, and products with shorter supply chains. For developers, tariff exposure makes early procurement, supplier diversification, and escalation clauses more important.

Material Type Analysis

Bamboo led the Sustainable Construction Materials Market with 42.0% share, supported by its renewability, fast growth cycle, high strength-to-weight ratio, and lower environmental impact compared with several conventional materials. It is increasingly used in flooring, panels, structural components, wall systems, roofing support, and interior applications.

The growth of bamboo-based materials can be attributed to rising interest in bio-based construction, carbon-conscious building design, and sustainable housing solutions. Bamboo is especially attractive in residential and low-rise construction where builders seek durable, lightweight, and natural materials that support green building goals.

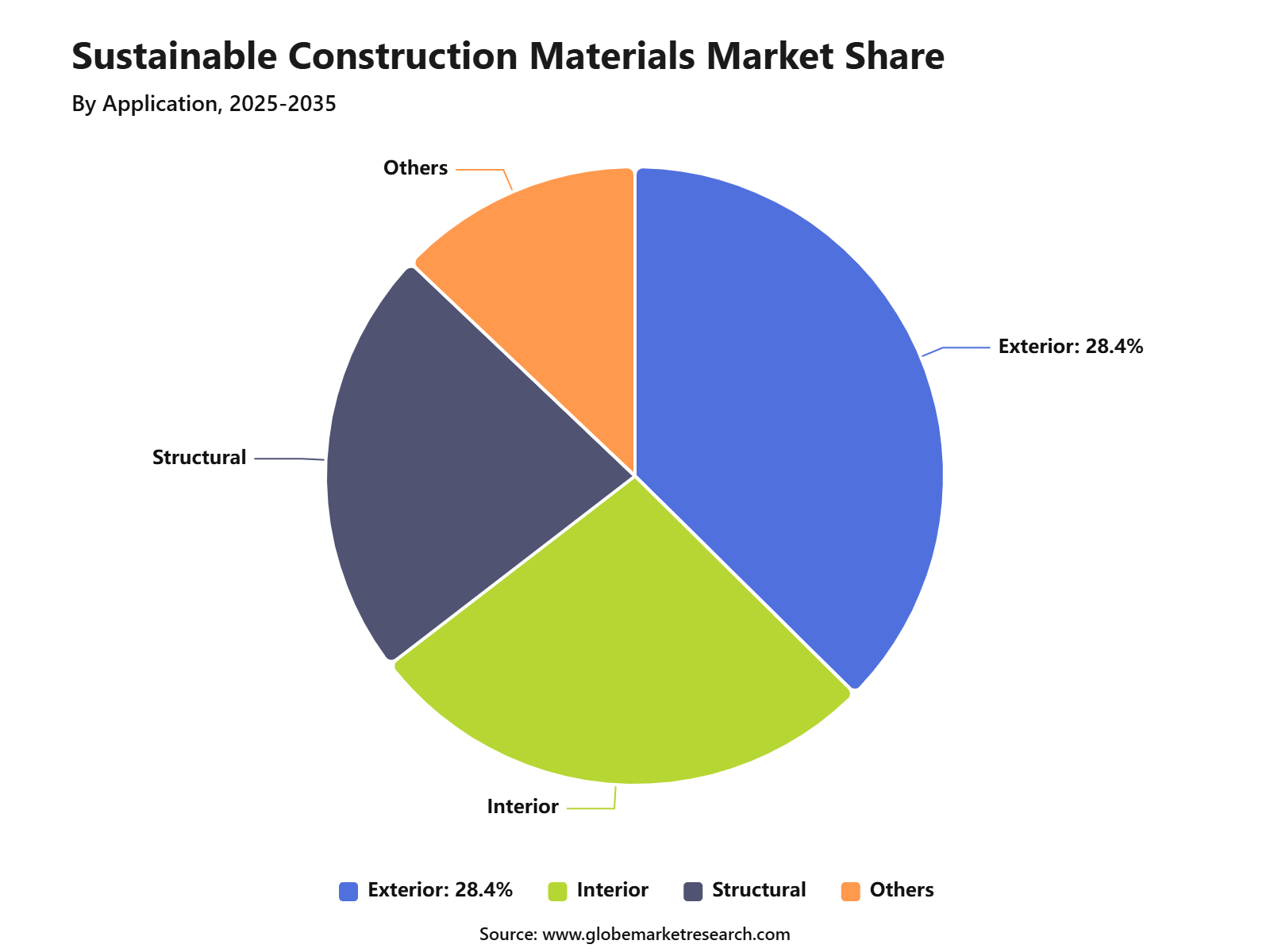

Application Analysis

Structural applications accounted for 39.1% share, making them a leading use area in the Sustainable Construction Materials Market. Demand is supported by the use of sustainable materials in beams, columns, frames, wall systems, roofing structures, and load-bearing building components.

The segment is gaining importance as developers, architects, and contractors focus on reducing embodied carbon in buildings. Sustainable structural materials help lower construction-related emissions while supporting durability, safety, and long-term building performance.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFEnd User Analysis

Residential construction held 35.6% share, supported by rising demand for eco-friendly homes, energy-efficient buildings, and low-carbon housing materials. Homeowners and developers are increasingly using sustainable materials in flooring, walls, insulation, roofing, framing, finishes, and modular housing systems.

The growth of this segment can be linked to green building awareness, urban housing demand, and stricter energy-efficiency expectations. Residential builders are adopting sustainable materials to improve indoor comfort, reduce energy use, support healthier living spaces, and meet buyer demand for environmentally responsible homes.

Regional Analysis

North America led the Sustainable Construction Materials Market with 46.1% share, supported by strong green building adoption, advanced construction standards, higher awareness of embodied carbon, and growing demand for energy-efficient buildings. The region has a mature ecosystem of architects, developers, contractors, certification bodies, and material suppliers focused on sustainable construction.

The growth of North America is also supported by investment in low-carbon buildings, renovation activity, and public and private efforts to reduce construction-related emissions. Demand is expected to remain strong for bamboo products, recycled materials, low-carbon concrete, sustainable insulation, engineered wood, and other eco-friendly construction solutions.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFU.S. Market Analysis

The U.S. Sustainable Construction Materials Market was valued at USD 193.1 billion and is projected to grow at a CAGR of 12.1%. Growth is being supported by rising green building adoption, stronger focus on embodied carbon reduction, renovation activity, and increasing demand for energy-efficient residential and commercial buildings.

The market is also benefiting from wider use of bamboo products, recycled materials, low-carbon concrete, sustainable insulation, engineered wood, and other eco-friendly construction materials. Builders, developers, and architects are increasingly selecting sustainable materials to meet regulatory expectations, improve building performance, and support long-term environmental goals.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRisk Factors & Market Barriers

The main risk factor is the gap between sustainability claims and proven technical performance. Construction buyers require strength, fire resistance, durability, moisture control, thermal performance, acoustic performance, and long-term warranty support. If a sustainable material lacks recognized testing, code approval, environmental product declarations, or contractor familiarity, adoption can slow even when the material has a lower carbon profile. This is especially important in structural concrete, steel, insulation, façades, and load-bearing timber systems.

Cement and steel remain difficult areas because they carry large emissions but are deeply embedded in construction practice. IEA reported that total CO2 emissions from cement and concrete are higher today than in 2015, while direct CO2 emissions intensity remains unchanged. Reuters also reported that the steel sector is responsible for 7% to 9% of global CO2 emissions, while only USD 20 billion has been pledged against an estimated USD 1.5 trillion needed for steel decarbonization. These figures show that supply-side transition is moving, but not fast enough to remove cost and availability barriers.

Regulatory & Compliance Risks

Regulatory risk is increasing because governments are moving from voluntary green-building labels toward formal carbon disclosure and lifecycle reporting. The revised EU Energy Performance of Buildings Directive requires the lifecycle global warming potential of all new buildings with floor area above 1,000 m² to be calculated and disclosed in the energy performance certificate from 2028. This requirement will extend to all new buildings from 2030. It directly increases demand for materials with verified embodied-carbon data.

Compliance risks also include building codes, fire safety rules, structural testing, indoor air quality, product labeling, and environmental product declarations. Suppliers of timber, insulation, recycled materials, low-carbon concrete, and bio-based products must prove that sustainability does not reduce safety or durability. The EU’s harmonized framework for lifecycle carbon assessment of new buildings was published in May 2026 and enters into force in 2026, which shows that measurement standards are becoming more formal.

Market Adoption Barriers

Market adoption is slowed by higher upfront cost, limited contractor experience, uncertain product availability, and lack of standard specifications in many projects. Developers may support sustainable materials in principle, but final decisions are often driven by budget, construction timeline, lender requirements, and contractor risk. If a product needs special installation, new equipment, or additional approvals, it may be avoided in cost-sensitive projects.

Demand is also limited where buyers are unwilling to pay a green premium. Reuters reported that many steel customers are still unwilling to pay more for green steel, while about half of planned green steel projects face setbacks due to funding shortages, weak demand, and limited green hydrogen availability. This barrier is relevant across sustainable construction materials because developers need policy support, procurement rules, and tenant demand before they can consistently absorb higher material costs.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape is spread across low-carbon cement, supplementary cementitious materials, recycled steel, green steel, engineered timber, bamboo, recycled aggregates, low-carbon insulation, cool roofing, green roofing, bio-based panels, recycled plastics, and geopolymer concrete. Stronger revenue potential is expected in projects where carbon reporting, energy performance, and green certification are required. Public infrastructure, commercial buildings, institutional projects, data centers, logistics facilities, and premium residential developments are likely to be early adopters because they are more exposed to ESG reporting and lifecycle cost analysis.

Low-carbon cement and concrete remain among the most important revenue areas because concrete is widely used and difficult to replace at scale. IEA stated that cement and concrete emissions need to fall through material efficiency, alternative fuels, supplementary cementitious materials, and carbon capture. This supports revenue opportunities for fly ash, slag, calcined clay, limestone cement blends, recycled aggregates, and carbon-cured concrete where local standards allow their use.

Financial Impact

The financial impact can be positive for suppliers that combine sustainability with technical reliability, cost control, and regulatory documentation. Higher-margin opportunities are likely in certified products, application-ready systems, prefabricated low-carbon components, engineered timber systems, energy-efficient insulation, and materials with verified environmental product declarations. Buyers are more likely to accept sustainable materials when they can reduce lifecycle cost, qualify for green procurement, improve building ratings, or lower future compliance risk.

Financial risk remains high because construction is price-sensitive and material substitution can be slow. In May 2026, Reuters reported that U.S. single-family housing starts fell to an eight-month low, while overall housing starts dropped to a six-year low, with rising mortgage rates, construction material costs, labor shortages, and land costs affecting activity. This means sustainable material suppliers need resilient pricing, local supply partnerships, and proof of project-level savings to protect demand during weaker construction cycles.

Segment Covered in the Report

By Material Type

Green Cement

Bamboo

Recycled Glass

Hempcrete

Recycled Tires

Reclaimed Wood

Cork

Mycelium

Ferrock

Sheep Wool

Recycled Metal

Recycled Plastic

Ashcrete

Timbercrete

Cellulose Fiber

By Application

Exterior

Interior

Structural

Others

By End User

Residential

Commercial

Offices

Institutes

Hospitality & Leisure

Industrial

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising green building adoption | +3.4% | North America, Europe, Asia Pacific | Drives material demand. |

Stricter carbon reduction targets | +3.0% | Europe, U.S., China, Japan | Supports low-carbon materials. |

Growth in sustainable infrastructure projects | +2.7% | Asia Pacific, Middle East, North America | Expands construction usage. |

Increasing demand for energy-efficient buildings | +2.4% | Global urban markets | Improves building performance. |

Rising use of recycled and renewable materials | +2.1% | Europe, North America, developed Asia | Reduces construction waste. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High cost of sustainable materials | -1.8% | Emerging markets, small builders | Limits faster adoption. |

Limited availability of certified materials | -1.5% | Asia Pacific, Latin America, MEA | Slows project procurement. |

Lack of awareness among contractors | -1.2% | Developing construction markets | Reduces usage speed. |

Performance concerns in some applications | -1.0% | Structural and heavy construction | Affects buyer confidence. |

Complex certification and compliance needs | -0.9% | Europe, North America, Asia Pacific | Raises project cost. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Expansion of green building certifications | +3.2% | North America, Europe, Asia Pacific | Supports premium demand. |

Growth in bamboo and bio-based materials | +2.8% | Asia Pacific, North America, Europe | Opens renewable material use. |

Rising demand for recycled concrete and steel | +2.6% | Global construction markets | Supports circular construction. |

Sustainable residential construction growth | +2.3% | U.S., Europe, India, China | Drives volume demand. |

Government incentives for eco-friendly buildings | +2.0% | Europe, North America, GCC, Asia Pacific | Improves adoption rates. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Scaling sustainable material production | -1.5% | Global | Affects supply reliability. |

Quality standardization issues | -1.3% | Emerging markets | Slows wider acceptance. |

Construction industry resistance to change | -1.1% | Traditional building markets | Delays adoption. |

Supply chain gaps for renewable inputs | -1.0% | Asia Pacific, Africa, Latin America | Increases sourcing risk. |

Measuring lifecycle carbon impact | -0.9% | Global | Complicates project selection. |

Recent Developments

January 2026, Heidelberg Materials said it expected slight volume growth in 2026, supported by infrastructure, defense, and large construction demand. The company also indicated it had a roughly EUR 10 billion acquisition capacity, showing that large building materials producers are still looking for strategic deals despite weaker housing demand in some regions. This points to consolidation in cement, aggregates, ready-mix concrete, recycled materials, and sustainable product portfolios

January 2026, HHallett Group received a AUD 12 million state government loan for its Green Cement Transformation Project in South Australia. The total project cost was estimated at AUD 220 million and is focused on using supplementary cementitious materials from industrial waste streams to reduce cement-related emissions by up to 30%. The project is expected to support 150 construction jobs and 50 ongoing roles.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 548.6 Billion |

Forecast Revenue (2035) | USD 1,878.8 Billion |

CAGR (2025-2035) | 13.1% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Material Type (Green Cement, Bamboo, Recycled Glass, Hempcrete, Recycled Tires, Reclaimed Wood, Cork, Mycelium, Ferrock, Sheep Wool, Recycled Metal, Recycled Plastic, Ashcrete, Timbercrete, Cellulose Fiber), By Application (Exterior, Interior, Structural, Others), By End User (Residential, Commercial (Offices, Institutes,Hospitality & Leisure), Industrial), By Regional Insights |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | 3M, Alumasc Group Plc, BASF SE, Bauder Limited, Binderholz GmbH, CertainTeed, DuPont, Forbo Group, Interface Inc., Kingspan Group, Lafarge, National Fiber, Owens Corning, PPG Industries, RedBuil, LLC, Redware Wall Systems, Structurlam Mass Timber Corporation |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

3M

Alumasc Group Plc

Bauder Limited

BASF SE

CertainTeed

DuPont

Forbo Group

Interface Inc.

Kingspan Group

Lafarge

National Fiber

Owens Corning

PPG Industries

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Manufacturing and Construction

Industrial Robotics Market to hit USD 192.1 billion by 2035

Global Industrial Robotics Market Size, Share Analysis By Robot Type (Articulated Robots, Linear Robots, SCARA Robots, Collaborative Robots, Cartesian / Gantry Robots, Parallel / Delta Robots, Cylindrical Robots), By Payload Capacity (Up to 15 kg, 16 to 225 kg, 226 to 500 kg, Above 500 kg), By Application (Material Handling and Packaging, Welding and Soldering, Assembly and Dispensing, Machine Tending and CNC, Painting and Coating, Quality Inspection), By End-User Industry (Automotive, Electrical and Electronics, Food and Beverage, Machinery and Metal, Pharmaceuticals and Healthcare, Construction Materials, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Real Estate Market to hit USD 8,602.5 billion by 2035

Global Real Estate Market Size, Share Analysis By Property Type (Residential Real Estate, Commercial Real Estate, Agricultural Land), By Commercial Asset Type (Office and Business Space, Retail, Industrial and Logistics, Hospitality, Healthcare Real Estate, Education Real Estate, Data Centers, Mixed-use Properties, Student Accommodation, Affordable Housing), By Service Type (Buying and Selling, Leasing and Renting, Property Management, Asset Management, Valuation, Development, Finance, Advisory and Consultancy), By End User (Individual Buyers and Renters, Real Estate Developers, Corporates, Institutional Investors, REITs, Government and Public Sector, Agricultural Landowners), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035