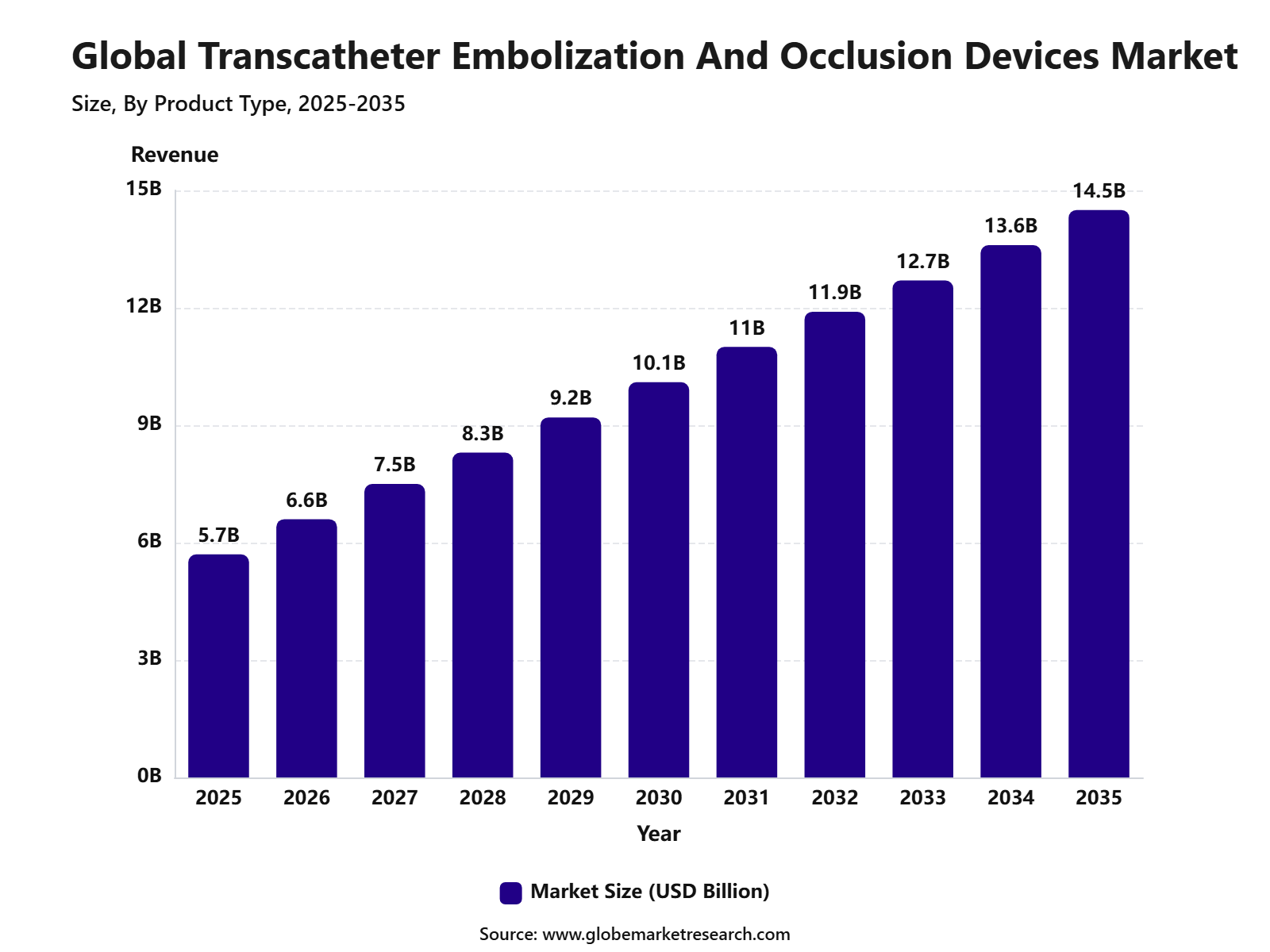

Revenue, 2025

$5.7 billion

Forecast, 2035

$14.5 billion

CAGR, 2025-2035

9.8%

Report Coverage

Global

Market Size and Forecast

What is the Transcatheter Embolization And Occlusion Devices Market Size?

The Transcatheter Embolization and Occlusion Devices Market reached USD 5.7 billion in 2025 and is expected to grow to USD 14.5 billion by 2035, registering a CAGR 9.8%. North America accounted for 38% share in 2025. The market growth is supported by the rising prevalence of cancer, aneurysms, arteriovenous malformations, uterine fibroids, and trauma-related bleeding, along with increasing preference for minimally invasive procedures, improved catheter-based technologies, wider hospital adoption, and growing use of embolization devices in interventional radiology and vascular treatment.

The U.S. Transcatheter Embolization and Occlusion Devices Market was valued at approximately USD 1.8 billion in 2025 and is projected to expand at a CAGR of 9.6% from 2025 to 2035, driven by rising demand for minimally invasive vascular procedures, increasing cases of cancer, aneurysms, arteriovenous malformations, trauma-related bleeding, and uterine fibroids. The growth of the market can be attributed to the strong presence of advanced hospitals, wider use of interventional radiology, high adoption of catheter-based treatment methods, growing healthcare spending, and continuous improvements in embolization coils, vascular plugs, liquid embolic agents, and flow diversion devices.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Insights

Embolization coils accounted for 33.7% share, supported by their wide use in aneurysm treatment, vascular occlusion, and neurovascular procedures.

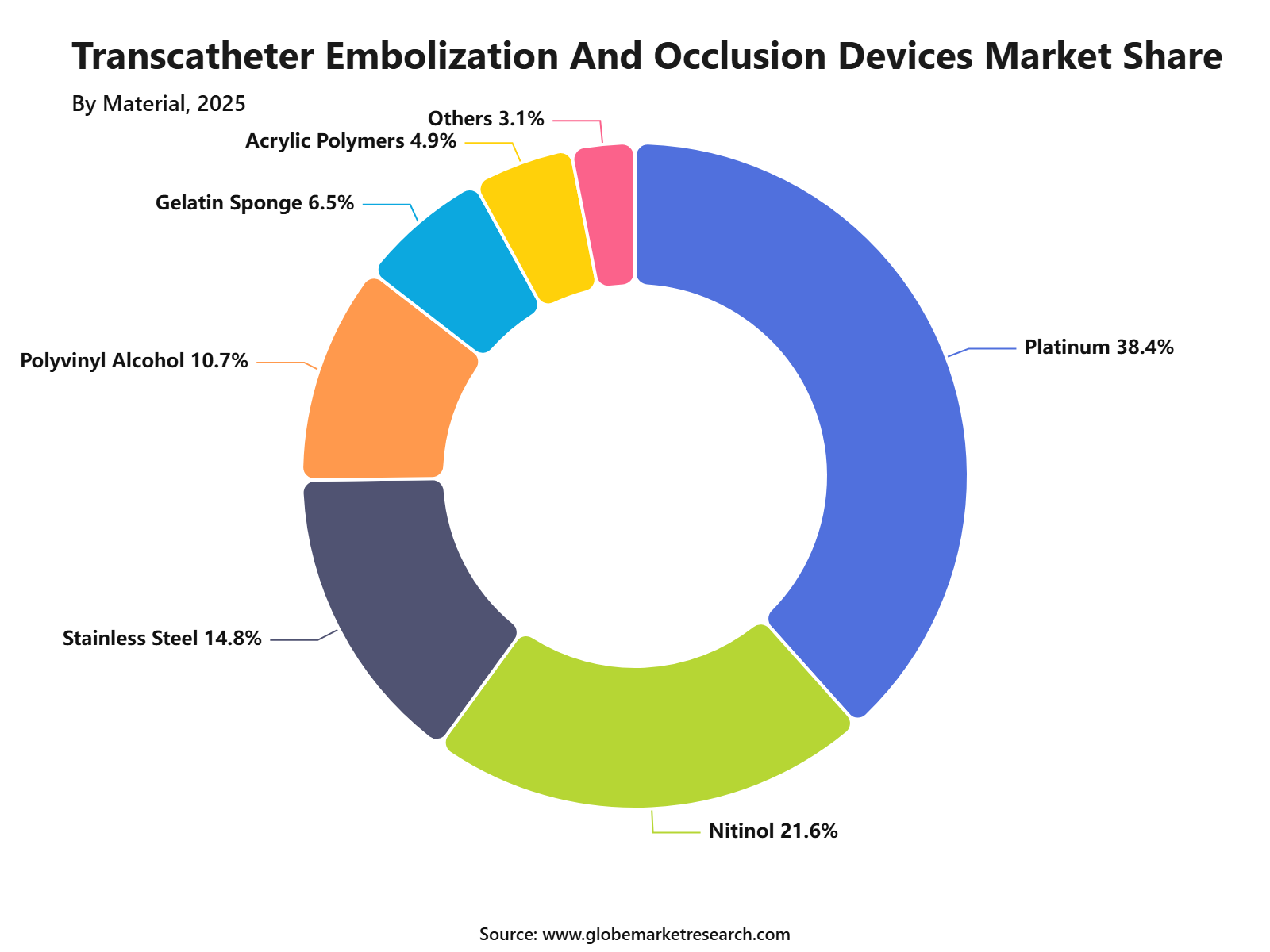

Platinum held 38.4% share, driven by its flexibility, biocompatibility, and strong visibility during image-guided procedures.

Neurology captured 31.2% share, supported by the rising use of embolization devices in brain aneurysms, arteriovenous malformations, and other neurovascular conditions.

Aneurysms represented 29.8% share, as increasing diagnosis of cerebral and peripheral aneurysms continues to support demand for minimally invasive treatment.

Hospitals accounted for 61.5% share, owing to the availability of advanced imaging systems, skilled interventional specialists, and emergency vascular care facilities.

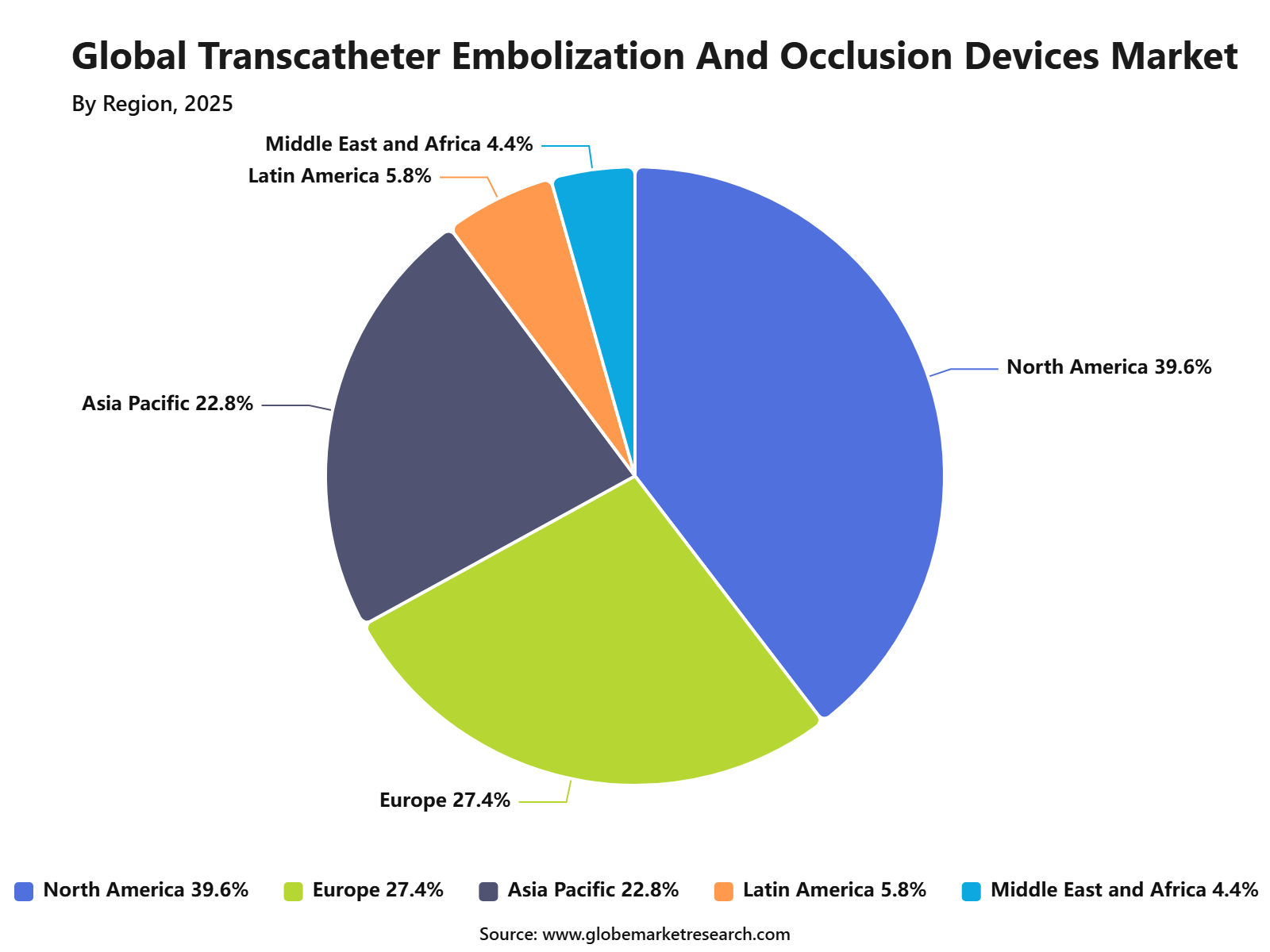

North America held 39.6% share, supported by advanced healthcare infrastructure, high adoption of minimally invasive procedures, strong reimbursement access, and early use of innovative embolization technologies.

Market Overview

The Transcatheter Embolization and Occlusion Devices Market covers catheter-based devices used to block, reduce, or redirect blood flow in targeted vessels. These devices are used for aneurysms, arteriovenous malformations, tumors, uterine fibroids, hemorrhage, and other vascular conditions. The FDA classifies vascular and neurovascular embolization devices under Class II special controls. At the same time, CDC data shows that more than 795,000 people in the U.S. have a stroke every year, supporting the need for advanced neurovascular and vascular intervention tools.

Demand is also being supported by the high number of patients with brain aneurysms and women’s health conditions. About 6.8 million people in the U.S. are estimated to have an unruptured brain aneurysm, and nearly 30,000 brain aneurysm ruptures occur each year. In women’s health, uterine leiomyomata affect an estimated 20% to 40% of females of reproductive age, creating a steady demand for uterine fibroid embolization as a less invasive alternative to surgery.

Top driving factors include the shift toward minimally invasive treatment, rising stroke and aneurysm burden, growing cancer-related embolization use, and stronger hospital adoption of image-guided procedures. Globally, almost 12 million new strokes occur each year, and 1 in 4 people above 25 years of age is expected to experience a stroke during their lifetime. This large disease burden is increasing the role of embolization coils, liquid embolic agents, flow diverters, and vascular plugs in urgent and planned vascular care.

Customer Acquisition Strategy

Customer acquisition in the Transcatheter Embolization and Occlusion Devices Market is mainly driven through hospitals, interventional radiology departments, neurovascular centers, oncology centers, and vascular surgery teams, which together account for nearly 85% to 90% of total device procurement. The buying process is highly clinical and evidence-based, as these devices are used in complex procedures such as aneurysm treatment, tumor embolization, hemorrhage control, arteriovenous malformations, and uterine fibroid embolization, with over 70% of purchasing decisions influenced by clinical outcomes and physician preference.

Manufacturers usually acquire customers by working with key opinion leaders, offering physician training, supporting procedure education, and helping hospitals understand coding, reimbursement, and product performance. Training programs and physician engagement initiatives contribute to approximately 60% of successful product adoption in new hospitals. Since these devices are linked to minimally invasive treatment, shorter recovery, and image-guided precision, customer conversion is stronger where hospitals are trying to reduce open surgery burden, which has declined by nearly 25% in favor of minimally invasive procedures, and improve procedural efficiency by up to 30%.

Tariff Impact

Tariff impact remains an important cost factor because embolization coils, catheters, delivery systems, microcatheters, platinum components, nitinol parts, polymers, packaging materials, and electronics used in imaging-supported procedures may depend on global supply chains, with nearly 40% to 50% of components sourced internationally. U.S. tariff policy on Chinese industrial and medical imports has remained active, with tariffs ranging between 7% and 25%, although several exclusions have been extended, reducing immediate cost pressure for some imported medical inputs by approximately 10% to 15%.

Even with exclusions, suppliers face uncertainty from customs classification, component sourcing, logistics cost, and hospital price sensitivity, with logistics expenses increasing by nearly 12% in recent years. As a result, companies are expected to protect margins through supplier diversification, regional inventory planning, dual sourcing strategies adopted by over 55% of manufacturers, local assembly, and stronger contracting with group purchasing organizations and hospital networks, which influence nearly 65% of hospital procurement decisions.

Revenue Potential Analysis

Revenue Opportunities

Expansion in minimally invasive procedures creates a strong revenue opportunity, as hospitals are increasingly using embolization and occlusion devices for aneurysms, tumors, bleeding control, uterine fibroids, and vascular malformations. Device makers can benefit from rising procedure volumes, especially in neurovascular, oncology, and peripheral vascular care.

Premium products such as detachable coils, liquid embolic agents, vascular plugs, and microspheres offer better pricing potential because they are used in complex and high-risk procedures. These products also support recurring revenue, as multiple devices may be required in a single procedure depending on lesion size and clinical complexity.

Hospital and specialty center partnerships can improve long-term sales by supporting physician training, procedure education, product trials, and clinical workflow integration. Companies that provide strong technical support and easy-to-use delivery systems are likely to gain stronger adoption among interventional radiologists and neurovascular specialists.

Financial Impact

Revenue growth can be supported by high-value procedures, as embolization devices are used in specialized hospital settings where clinical reliability and procedural success are key buying factors. This allows established suppliers to maintain stronger pricing than basic medical consumables.

Profit margins may improve when companies focus on differentiated products such as next-generation coils, bioactive embolics, shape-memory materials, and controlled-release embolization platforms. These products can command better pricing when backed by clinical evidence and physician confidence.

Supply chain costs may affect profitability because platinum, nitinol, polymers, catheter components, and sterile packaging are exposed to global material pricing and tariff-related uncertainty. Companies with diversified sourcing and regional manufacturing can reduce cost pressure and protect margins.

By Product Type

Embolization coils led the Transcatheter Embolization and Occlusion Devices Market with a 33.7% share, supported by their widespread use in minimally invasive procedures designed to block abnormal blood flow. These devices are commonly used in the treatment of aneurysms, vascular malformations, hemorrhage control, and tumor embolization due to their precision and controlled deployment capabilities.

The segment continues to benefit from growing preference for catheter-based interventions that reduce surgical trauma, shorten recovery periods, and improve procedural outcomes. Advances in coil design, enhanced visibility during imaging, and improved delivery systems are further supporting their adoption across interventional radiology and neurovascular procedures.

By Material

Platinum accounted for the largest share at 38.4%, owing to its excellent flexibility, biocompatibility, radiopacity, and long-term stability within blood vessels. These properties make platinum an ideal material for embolization devices, particularly in procedures where accurate placement and visualization are essential.

The increasing use of platinum-based embolization products is also supported by the rising number of complex vascular interventions and neurovascular treatments. Physicians prefer platinum devices because they can be clearly visualized during fluoroscopic guidance, allowing precise deployment and improved procedural control.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Application

Neurology emerged as the leading application segment with a 31.2% share, driven by the growing use of embolization procedures for treating cerebral aneurysms, arteriovenous malformations, and other neurovascular disorders. The increasing prevalence of stroke-related conditions and neurological vascular abnormalities has contributed significantly to demand within this segment.

Advancements in neurointerventional techniques and imaging technologies have further expanded the use of transcatheter embolization procedures in neurological care. Healthcare providers increasingly favor minimally invasive approaches that reduce procedural risk while improving patient outcomes in complex brain and vascular conditions.

By Indication

Aneurysms held the largest indication share at 29.8%, reflecting the increasing adoption of embolization therapies as an alternative to open surgical procedures. Embolization devices play an important role in isolating weakened blood vessel areas, helping reduce the risk of rupture and severe complications.

The growth of this segment is supported by rising awareness of early diagnosis, improved imaging capabilities, and greater availability of specialized neurovascular treatment centers. Minimally invasive aneurysm treatment continues to gain preference due to shorter hospitalization periods and lower procedural burden compared to conventional surgery.

By End User

Hospitals dominated the market with a 61.5% share, supported by their advanced infrastructure, availability of specialized interventional teams, and capacity to perform complex embolization procedures. Most transcatheter interventions require sophisticated imaging equipment, catheterization laboratories, and multidisciplinary clinical expertise, making hospitals the primary treatment setting.

The segment is also benefiting from increasing investments in minimally invasive treatment programs and expanding access to interventional radiology services. Hospitals continue to be the preferred destination for patients requiring emergency vascular interventions, neurological procedures, and advanced cardiovascular care.

By Region

North America accounted for the leading regional share of 39.6%, supported by advanced healthcare infrastructure, high adoption of minimally invasive procedures, and strong availability of specialized interventional radiology and neurovascular treatment centers. The region has witnessed significant utilization of embolization technologies across neurological, oncological, and vascular applications.

Growth in the region is further supported by increasing awareness of catheter-based treatments, favorable access to advanced medical technologies, and rising procedural volumes. Continuous investment in healthcare innovation, physician training, and specialized treatment facilities has strengthened North America's position as a key market for transcatheter embolization and occlusion devices.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRisk Factors & Market Barriers

Regulatory & Compliance Risks

Strict device approval requirements remain a key risk because transcatheter embolization and occlusion devices are used in high-risk vascular and neurovascular procedures. Any failure in safety testing, biocompatibility, sterility, clinical evidence, or post-market surveillance can delay approvals and increase product development costs.

Product recalls, adverse event reporting, and quality system failures can affect company reputation and hospital confidence. Since these devices are placed inside blood vessels, even small performance issues such as migration, thrombosis, catheter incompatibility, or incomplete occlusion can create serious clinical and regulatory concerns.

Compliance requirements differ across major markets such as the U.S., Europe, China, Japan, and India. This creates additional documentation, testing, labeling, and approval challenges for companies planning international expansion.

Reimbursement and coding uncertainty can also slow adoption. If hospitals face unclear payment coverage or low procedure reimbursement, purchasing decisions may be delayed even when the technology is clinically useful.

Market Adoption Barriers

High product cost is a major adoption barrier, especially in cost-sensitive hospitals and developing healthcare markets. Advanced embolization coils, liquid embolics, plugs, and delivery systems may require higher upfront spending compared to conventional treatment options.

Limited availability of trained interventional radiologists, neurointervention specialists, and vascular surgeons can restrict procedure volumes. Adoption is stronger in advanced hospitals, but smaller facilities may face skill gaps, infrastructure limitations, and limited access to imaging-guided procedure rooms.

Clinical preference and physician familiarity can slow switching from established brands to newer products. Hospitals often prefer devices with strong safety records, predictable handling, and proven outcomes, which makes market entry difficult for smaller or newer suppliers.

Supply chain disruptions can create barriers to consistent product availability. Dependence on specialized materials such as platinum, nitinol, polymers, microcatheter components, and sterile packaging can affect delivery timelines and hospital procurement planning.

Patient access remains uneven across regions due to differences in healthcare spending, insurance coverage, and specialist availability. This can limit revenue growth in markets where minimally invasive vascular treatment is still developing.

Key Market Segment

By Product Type

Embolization Coils

Flow Diversion Devices

Liquid Embolic Agents

Embolic Particles

Detachable Balloons

Vascular Plugs

Microspheres

Others

By Material

Platinum

Nitinol

Stainless Steel

Polyvinyl Alcohol

Gelatin Sponge

Acrylic Polymers

Others

By Application

Peripheral Vascular Disease

Oncology

Neurology

Urology

Gastroenterology

Trauma Management

Others

By Indication

Aneurysms

Arteriovenous Malformations

Tumors

Hemorrhage

Varicoceles

Uterine Fibroids

Others

By End User

Hospitals

Ambulatory Surgical Centers

Specialty Clinics

Catheterization Laboratories

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

vidIQ

Driver Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising preference for minimally invasive procedures | +1.2% | North America, Europe, Asia Pacific | Supports faster adoption and higher procedure volumes. |

Growing burden of aneurysms and vascular disorders | +1.0% | North America, Europe, China, Japan | Increases demand for embolization and occlusion devices. |

Increasing use in oncology and tumor embolization | +0.9% | U.S., Europe, China, India | Expands usage beyond vascular procedures. |

Technological improvements in coils, plugs, and embolic agents | +0.8% | U.S., Germany, Japan, South Korea | Improves precision, safety, and physician confidence. |

Expansion of interventional radiology infrastructure | +0.7% | Asia Pacific, Middle East, Latin America | Improves access in emerging healthcare markets. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High procedure and device cost | -0.9% | Asia Pacific, Latin America, Middle East and Africa | Limits adoption in cost-sensitive hospitals. |

Complex regulatory approval requirements | -0.8% | U.S., Europe, Japan | Delays product entry and commercialization. |

Limited availability of trained interventional specialists | -0.7% | India, Southeast Asia, Africa, Latin America | Restricts procedure growth outside major cities. |

Risk of procedure complications | -0.6% | Global | May affect physician and patient confidence. |

Reimbursement variation across countries | -0.5% | Europe, Asia Pacific, Latin America | Reduces access in under-covered markets. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for neurovascular embolization | +1.1% | U.S., Europe, Japan, China | Creates strong demand for high-value devices. |

Wider use in uterine fibroid treatment | +0.8% | North America, Europe, India | Supports growth in women’s health applications. |

Growth in outpatient interventional care | +0.7% | U.S., Europe, GCC countries | Increases procedural capacity and patient access. |

Innovation in image-guided embolic materials | +0.7% | U.S., Germany, Japan, South Korea | Improves targeting and clinical outcomes. |

Hospital modernization in emerging markets | +0.6% | China, India, Brazil, Saudi Arabia | Creates new demand for advanced embolization systems. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Lack of procedure standardization | -0.7% | Global | Creates variation in treatment outcomes. |

Competition from alternative therapies | -0.6% | North America, Europe, Asia Pacific | Limits use in some indications. |

Supply chain pressure for metals and polymers | -0.5% | Global | Affects pricing and product availability. |

High evidence requirements for new indications | -0.5% | U.S., Europe, Japan | Slows expansion into newer applications. |

Hospital pricing pressure | -0.4% | U.S., Europe, China | Reduces margins for device suppliers. |

Recent Development

W. L. Gore & Associates, Inc., February 2026 - W. L. Gore received an FDA PMA supplement decision for the GORE CARDIOFORM ASD Occluder and GORE CARDIOFORM Septal Occluder. The update supports the company’s established position in transcatheter septal occlusion devices.

B. Braun SE, 2026 - B. Braun continued to support interventional vascular therapy through its vascular implant and interventional device portfolio. Its offering remains focused on improving vascular treatment outcomes, including products used across minimally invasive vascular procedures.

Balt Group, February 2026 - Balt received FDA approval for the Squid Liquid Embolic Agent for embolization of the middle meningeal artery as an adjunctive treatment for symptomatic chronic subdural hematoma. This development expanded Balt’s liquid embolic role in neurovascular care.

Shape Memory Medical Inc., 2026 - Shape Memory Medical secured EU MDR CE Mark approval for its IMPEDE Embolization Plug family. The approval supports wider European commercialization of its shape memory polymer embolization platform.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 5.7 Bn |

Forecast Revenue (2035) | USD 14.5 Bn |

CAGR (2025-2035) | 9.8% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Product Type (Embolization Coils, Flow Diversion Devices, Liquid Embolic Agents, Embolic Particles, Detachable Balloons, Vascular Plugs, Microspheres, Others), By Material (Platinum, Nitinol, Stainless Steel, Polyvinyl Alcohol, Gelatin Sponge, Acrylic Polymers, Others), By Application (Peripheral Vascular Disease, Oncology, Neurology, Urology, Gastroenterology, Trauma Management, Others), By Indication (Aneurysms, Arteriovenous Malformations, Tumors, Hemorrhage, Varicoceles, Uterine Fibroids, Others), By End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Catheterization Laboratories, Others), By Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa), By Regional Insights, Business plan and and project report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035. |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Medtronic plc, Boston Scientific Corporation, Terumo Corporation, MicroVention, Inc., Stryker Corporation, Cook Medical LLC, Penumbra, Inc., Abbott Laboratories, Johnson & Johnson MedTech, Cerenovus, Merit Medical Systems, Inc., W. L. Gore & Associates, Inc., B. Braun SE, Kaneka Corporation, Balt Group, Shape Memory Medical Inc., Acandis GmbH, Wallaby Medical, Spartan Micro, Inc., ArtVentive Medical Group, Inc., Zylox-Tonbridge Medical Technology Co., Ltd. |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Medtronic plc

Boston Scientific Corporation

Terumo Corporation

MicroVention, Inc.

Stryker Corporation

Cook Medical LLC

Penumbra, Inc.

Abbott Laboratories

Johnson & Johnson MedTech, Cerenovus

Merit Medical Systems, Inc.

W. L. Gore & Associates, Inc.

B. Braun SE

Kaneka Corporation

Balt Group

Shape Memory Medical Inc.

Acandis GmbH

Wallaby Medical

Spartan Micro, Inc.

Others

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Healthcare and Pharmaceuticals

US Medical Devices Market to hit USD 407.6 billion by 2035

US Medical Devices Market Size, Go-to-Market Strategy Analysis By Device Type (In Vitro Diagnostics (IVD), Diagnostic Imaging, Cardiovascular Devices, Orthopedic Devices, Surgical Devices, Patient Monitoring Devices, Others), By Application (Cardiology, Diagnostic Imaging, Orthopedics, Neurology, In Vitro Diagnostics, Others), By End User (Hospitals and Clinics, Ambulatory Surgical Centers, Diagnostic Laboratories, Home Healthcare, Others), By Technology (Conventional Devices, Connected Medical Devices, AI-Enabled Medical Devices, Robotic-Assisted Devices), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Skin Care Products Market to Cross USD 285.8 Bn by 2035

Global Skin Care Products Market By Type (Facial Care, Body Care, Lip Care), By Packaging (Tubes, Bottles, Jars, Others), By Products (Face Creams & Moisturizers, Cleansers & Face Wash, Sunscreen, Body Creams & Moisturizers, and Others), By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, and Others), By End-User (Female, Male, Unisex), By Category (Premium Skincare Products, Mass Skincare Products), By Ingredient (Chemical, Natural), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Biohacking Market to Exceed USD 231.3 Billion by 2035

Global Biohacking Market Size, Share Analysis Report By Product Type (Wearable Devices, Smart Implants, Gene-Editing Kits, Nootropics & Supplements, Sensors & Biomonitoring Patches, Others), By Biohacking Type (Nutrigenomics, DIY Biology, Grinder, and Others), By End User (Consumers, Healthcare Facilities, and Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Telemedicine Market to Exceed USD 981.6 Billion by 2035

Global Telemedicine Market Size, Share Analysis Report By Modality (Synchronous, Asynchronous, Remote Patient Monitoring), By Component (Software Platforms, Hardware & Peripherals, Services), By End User (Healthcare Providers, Payers & Employers, Patients / Home Users, Government Agencies & NGOs), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035