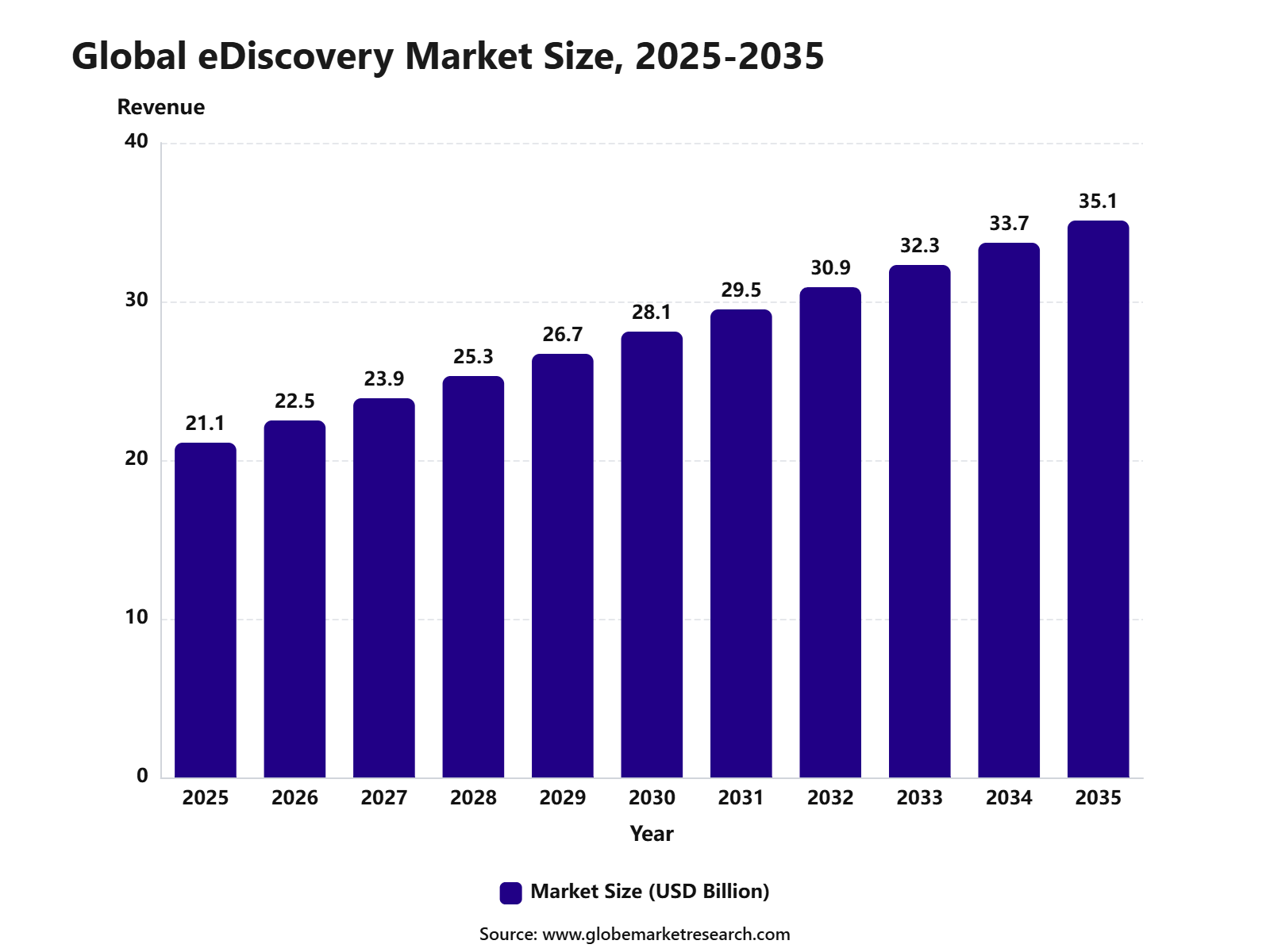

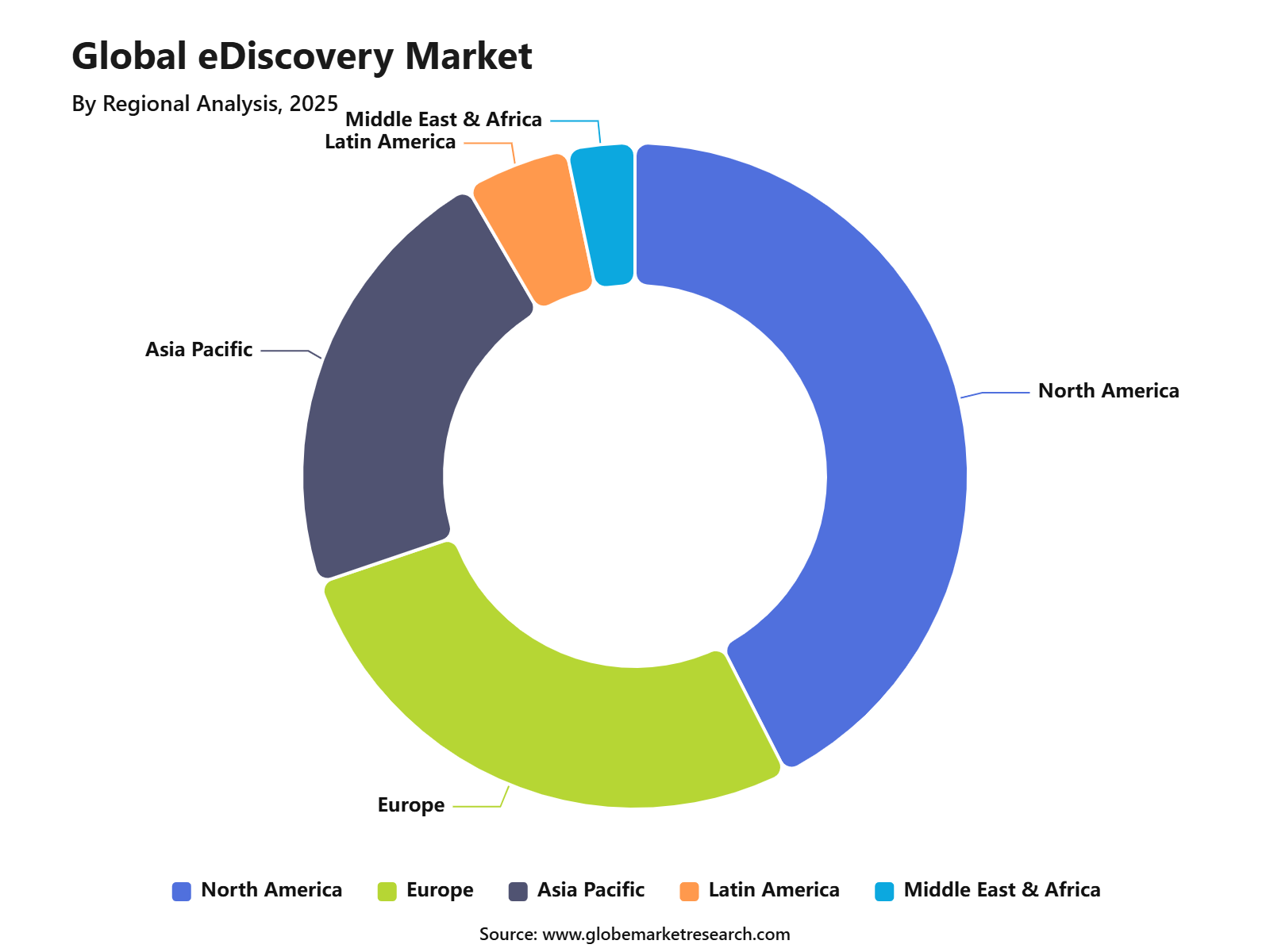

According to Globe Market Research, The Global eDiscovery Market was valued at USD 18.24 billion in 2025 and is forecast to reach USD 35.12 billion by 2035, growing at a CAGR of 10.30% during the forecast period. North America led the global market with a 42.5% share in 2025, contributing around USD 7.75 billion in revenue. The market in the region is supported by strong adoption of digital legal tools, complex corporate litigation, strict data privacy rules, and rising volumes of electronically stored information. Increasing use of automated review, cloud-based discovery, and compliance-focused platforms is expected to create steady demand.

The growth of the eDiscovery market is mainly driven by rising litigation volumes, stricter compliance rules, and the rapid expansion of digital business records. Companies are required to preserve and review electronic information during legal disputes, audits, investigations, and regulatory inquiries. The wider use of email, messaging platforms, cloud storage, and enterprise applications has increased the volume of discoverable data. This has made automated discovery tools essential for reducing time, cost, and legal risk.

Market Insights

Services led the eDiscovery market with a 70% share. Growth was supported by document review, data processing, legal consulting, forensic collection, and managed review services.

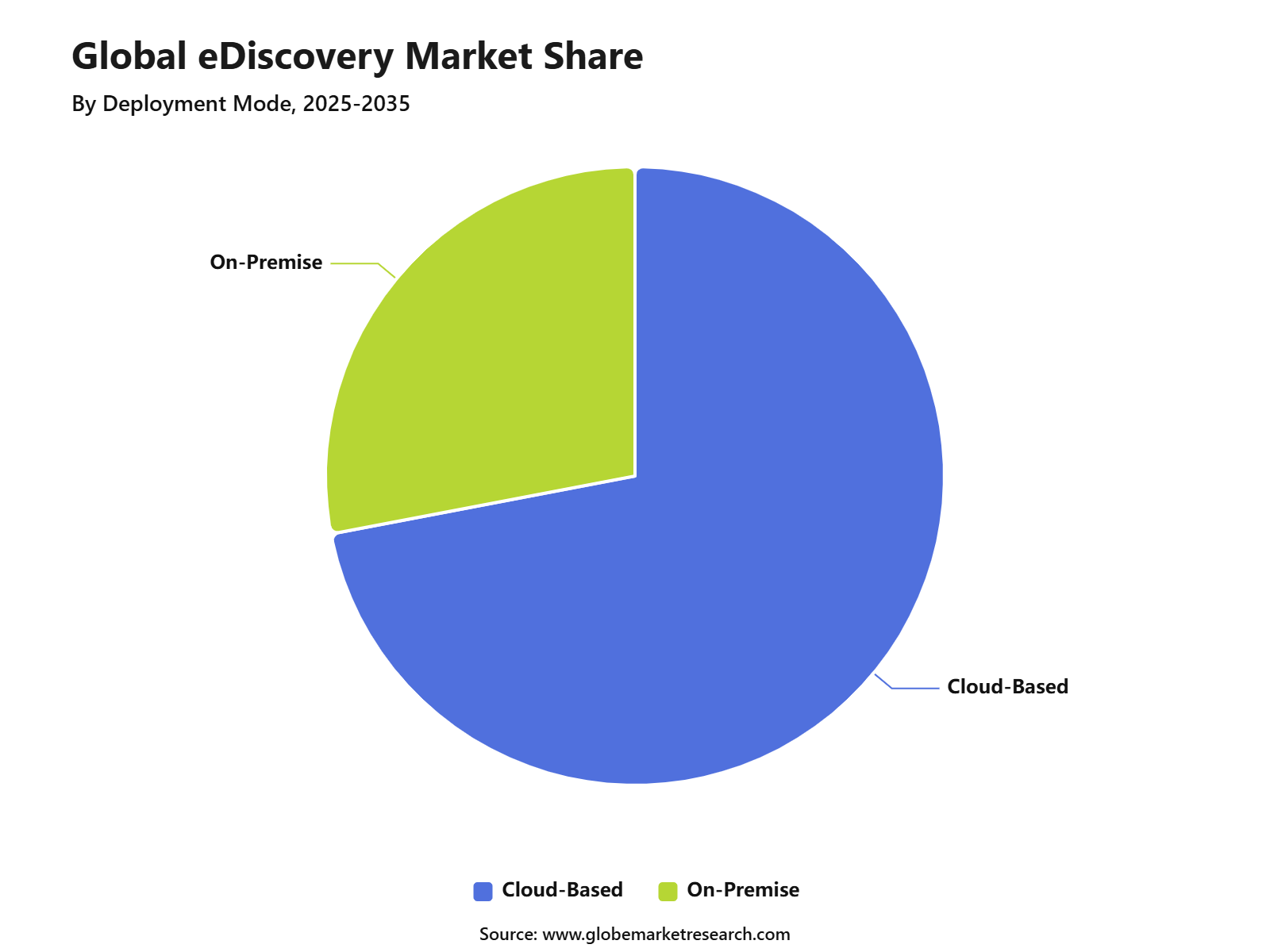

Cloud-based deployment held a 72% share. Demand was driven by scalable storage, faster case access, remote collaboration, and lower infrastructure costs.

Large enterprises accounted for a 74% share. Growth was supported by high data volumes, complex litigation, regulatory risk, and cross-border compliance needs.

BFSI led the end-use segment with a 41% share. Demand was driven by audits, fraud investigations, financial disputes, compliance monitoring, and digital records.

EDRM reports activity across 145 countries and 6 continents. This shows that eDiscovery has become a global legal and compliance process.

Generative AI use in the legal sector increased from 14% in 2024 to 26% in 2025. This shows rising adoption of AI tools in legal workflows.

In 2026, 87% of general counsel used generative AI in legal teams. This was a sharp rise from 44% in 2025.

Civil litigation firms had the highest AI adoption at 27% in 2025. Personal injury and family law firms followed with 20% each.

North America eDiscovery market Size

North America led the global eDiscovery market with a 42.5% share in 2025, contributing around USD 7.75 billion in revenue. The region maintained its leading position due to strong legal technology adoption, a mature litigation environment, strict regulatory compliance requirements, and high digital data generation across enterprises.

The growth of the North American market was supported by rising use of cloud-based eDiscovery platforms, AI-assisted document review, legal hold tools, forensic data collection, and managed review services. Demand remained strong across law firms, large enterprises, financial institutions, healthcare organizations, and government agencies due to increasing litigation complexity and growing pressure to manage electronic records securely.

The U.S. remained the key contributor within North America, supported by a large corporate legal ecosystem, frequent regulatory investigations, and advanced adoption of digital legal workflows. Continued investment in data privacy, cybersecurity, internal investigations, and cross-border compliance is expected to support steady demand for eDiscovery solutions across the region.

Component Analysis: Services

Services led the eDiscovery market with a 70% share, supported by strong demand for document review, data processing, legal consulting, forensic collection, and managed review services. These services are essential because legal teams often need expert support to collect, filter, review, and produce large volumes of electronic evidence.

The growth of this segment can be attributed to rising litigation complexity, expanding digital records, and stricter compliance requirements. Law firms, corporations, and government agencies continue to rely on specialist service providers to reduce review time, improve accuracy, and manage sensitive case data securely.

Deployment Analysis: Cloud-Based

Cloud-based deployment held a 72% share, driven by scalable storage, faster case access, remote collaboration, and lower infrastructure costs. Cloud platforms allow legal teams to upload, search, review, and share case documents from different locations while maintaining centralized control over data.

The segment is gaining momentum as legal departments and law firms handle larger volumes of emails, chat records, contracts, audio files, financial records, and business documents. Cloud-based systems are also preferred because they support faster case setup, flexible user access, automated updates, and stronger support for distributed legal teams.

Organization Size Analysis: Large Enterprises

Large enterprises accounted for a 74% share, supported by high data volumes, complex litigation, regulatory risk, and cross-border compliance needs. These organizations generate large volumes of structured and unstructured data across emails, messaging platforms, enterprise systems, cloud storage, contracts, and financial records.

The growth of this segment is being driven by the need to manage legal exposure, internal investigations, audits, mergers, employee disputes, and regulatory inquiries. Large enterprises are expected to remain major buyers of eDiscovery solutions because they require scalable platforms, strong data governance, secure workflows, and advanced analytics for legal review.

End-Use Analysis: BFSI

BFSI led the end-use segment with a 41% share, driven by audits, fraud investigations, financial disputes, compliance monitoring, and digital records. Banks, insurers, asset managers, and financial institutions rely on eDiscovery tools to manage sensitive communications, transaction records, customer data, contracts, and regulatory evidence.

The segment is expected to maintain strong demand because financial institutions operate under strict recordkeeping, data privacy, and compliance requirements. Rising digital transactions, off-channel communication risks, fraud cases, and regulatory reviews are increasing the need for secure document review, legal hold management, and evidence preservation systems.

Emerging Trends Analysis

The eDiscovery market is moving toward AI-assisted review, automated summarization, early case assessment, and faster document classification. A 2026 general counsel report found that 87% of general counsel now use generative AI within legal teams, compared with 44% in 2025. The same report noted strong use of AI for summarization, legal research, document review, transcription, foreign language material analysis, and first-pass review, which directly supports eDiscovery workflow automation.

Another important trend is the shift from email-based discovery to multi-source discovery across messaging apps, collaboration tools, cloud platforms, and enterprise systems. Legal teams are now expected to collect and review data from tools such as Microsoft 365, Google Workspace, Slack, shared drives, and cloud document links. Microsoft’s retirement of classic Purview eDiscovery experiences in August 2025 also shows how enterprise platforms are moving users toward newer, unified eDiscovery environments.

Driver Analysis

The main growth driver is the rising volume and complexity of digital evidence across corporate legal, compliance, and investigation workflows. A 2026 legal department report stated that more than 20 areas are driving higher legal workloads, especially new regulations. This has increased demand for legal hold tools, cloud collection, review analytics, managed review, and defensible information governance.

Adoption is also being supported by the wider role of chief legal officers in risk management and technology decisions. The 2026 ACC Chief Legal Officers Survey covered 1,049 CLOs across 43 countries and highlighted the shift of legal leaders into business strategy and technology leadership. As legal teams face AI, cyber, privacy, and regulatory pressure, eDiscovery platforms are becoming a core tool for managing legal risk and enterprise data control.

Restraint Analysis

The key restraint is the high level of implementation complexity across legal, IT, compliance, and security teams. Legal organizations are now evaluating multiple AI platforms, vendor relationships, governance policies, cybersecurity controls, records retention rules, and data handling obligations at the same time. Without clear planning, technology adoption can lead to fragmented workflows, duplicate spending, and change fatigue.

Accuracy, confidentiality, and defensibility risks are also slowing adoption, especially for AI-enabled eDiscovery tools. Courts and regulators are paying closer attention to AI-generated work because some tools can create false legal citations, misstate legal material, or produce unsupported outputs. In June 2026, Rhode Island joined other U.S. states in issuing AI guidance for lawyers, including requirements to independently review AI-generated work.

Opportunity Analysis

A strong opportunity exists in AI-enabled managed review, legal operations platforms, and cloud-based eDiscovery services. Around 70% of legal departments in a 2026 general counsel report planned to invest in new technologies over the next 12 months, while 53% had a formal technology roadmap. This creates room for vendors that can offer secure review workflows, measurable cost control, faster document analysis, and simple integration with enterprise systems.

Cross-border discovery and information governance also offer long-term revenue potential. EDRM reports an international presence across 145 countries and 6 continents, showing that eDiscovery has become a global legal and compliance discipline. Demand is expected to strengthen for platforms that can support privacy rules, multilingual review, audit trails, defensible collection, and consistent workflows across jurisdictions.

Challenge Analysis

The major challenge is fragmented enterprise data. Legal teams must now manage hyperlinked content, version histories, platform logs, comments, cloud permissions, and structured data in addition to traditional documents. This creates difficulty in proving authenticity, preserving complete document families, and showing who created, changed, shared, or approved specific content.

Another challenge is balancing speed with legal defensibility. AI can reduce review time, but legal teams must still verify outputs, protect privileged material, and maintain a clear audit record for court or regulatory review. The U.S. judiciary has already been asked to consider a nationwide rule requiring certification that AI-assisted filings contain accurate legal authorities, which shows the rising need for strict verification controls.

Key Market Players

eDiscovery Market Key Companies

AccessData Group Inc.

Commvault Systems Inc.

Conduent Inc.

Driven Inc. (Xplenty)

Fronteo Inc. (Formerly UBIC)

IBM

FTI Technology LLC

Kcura LLC

Zylab Technologies

Xerox Corp.

Hewlett Packard Enterprise

Logik

Lexbe

Ernst & Young Global Ltd.

Navigant Consulting

Other Key Players

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 18.24 Bn |

Forecast Revenue (2035) | USD 35.12 Bn |

CAGR (2025-2035) | 10.30% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |