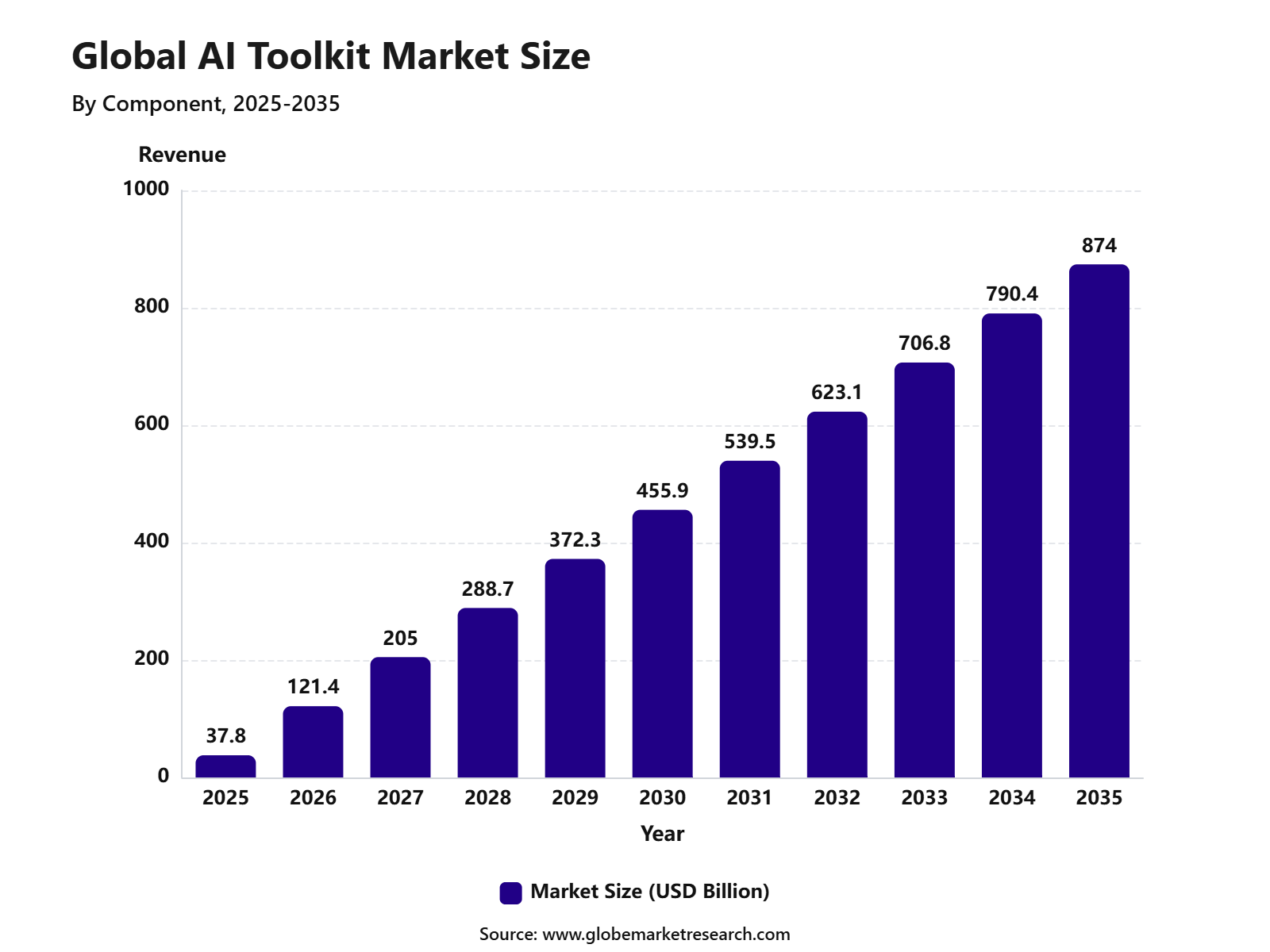

According to Globe Market Research, The Global AI Toolkit Market was valued at USD 37.8 billion in 2025 and is projected to reach USD 874.0 billion by 2035, growing at a CAGR of 36.9% during the forecast period. North America led the market with a 38.7% share in 2025, supported by strong AI adoption across enterprises, advanced cloud infrastructure, high investment in software development, and the presence of leading technology companies.

The U.S. AI Toolkit Market was valued at USD 10.2 billion in 2025 and is expected to grow at a CAGR of 36.4%, driven by rising demand for AI model development, automation tools, data labeling platforms, machine learning frameworks, and generative AI development environments. AI toolkits include software frameworks, APIs, model libraries, development platforms, data processing tools, testing environments, and deployment solutions used to build, train, evaluate, and integrate artificial intelligence systems.

The growth of the market can be attributed to rapid enterprise adoption of AI, increasing use of generative AI applications, growing demand for low-code and no-code AI tools, and wider integration of AI into business workflows. The market outlook remains strong as organizations continue to invest in AI infrastructure, model management, responsible AI systems, and industry-specific AI applications.

Demand is expected to rise for toolkits that support faster model development, secure deployment, workflow automation, natural language processing, computer vision, and predictive analytics. North America is expected to maintain a leading position due to its mature technology ecosystem, high cloud adoption, strong venture funding activity, and early enterprise adoption of AI-driven software solutions.

AI Toolkit Market: Key Insights

Platforms remained the leading component in the AI toolkit market, accounting for 59.5% share. This growth was supported by increasing use of tools for AI model development, training, deployment, testing, and workflow management across industries.

Cloud deployment held the largest share at 72.6%, as enterprises preferred flexible, scalable, and cost-efficient AI infrastructure. Cloud-based AI toolkits are being widely adopted due to faster implementation, easier access to computing resources, and reduced upfront investment.

Machine learning led the application segment with 39.7% share. Its strong position was driven by wide use in predictive analytics, process automation, customer personalization, fraud detection, and data-based business decision-making.

Large enterprises accounted for 65.8% share of the AI toolkit market. Higher technology budgets, mature data systems, skilled AI teams, and wider use of AI across operations, marketing, finance, and customer service supported this dominance.

North America held 38.7% share of the AI toolkit market. The region benefited from strong AI investment, advanced cloud adoption, enterprise digital transformation, and the presence of major technology companies and AI infrastructure providers.

The U.S. AI toolkit market was valued at USD 10.6 billion and is expected to expand at a 36.4% CAGR. Growth is being supported by rising demand for generative AI tools, machine learning platforms, enterprise automation, and AI model deployment solutions.

Sales Strategy and Market Expansion

The AI Toolkit Market needs a developer-led and enterprise-workflow-led go-to-market strategy. Vendors should position tools across coding assistants, AI agents, model APIs, vector databases, prompt management, data pipelines, model evaluation, observability, security, governance, deployment, and workflow automation.

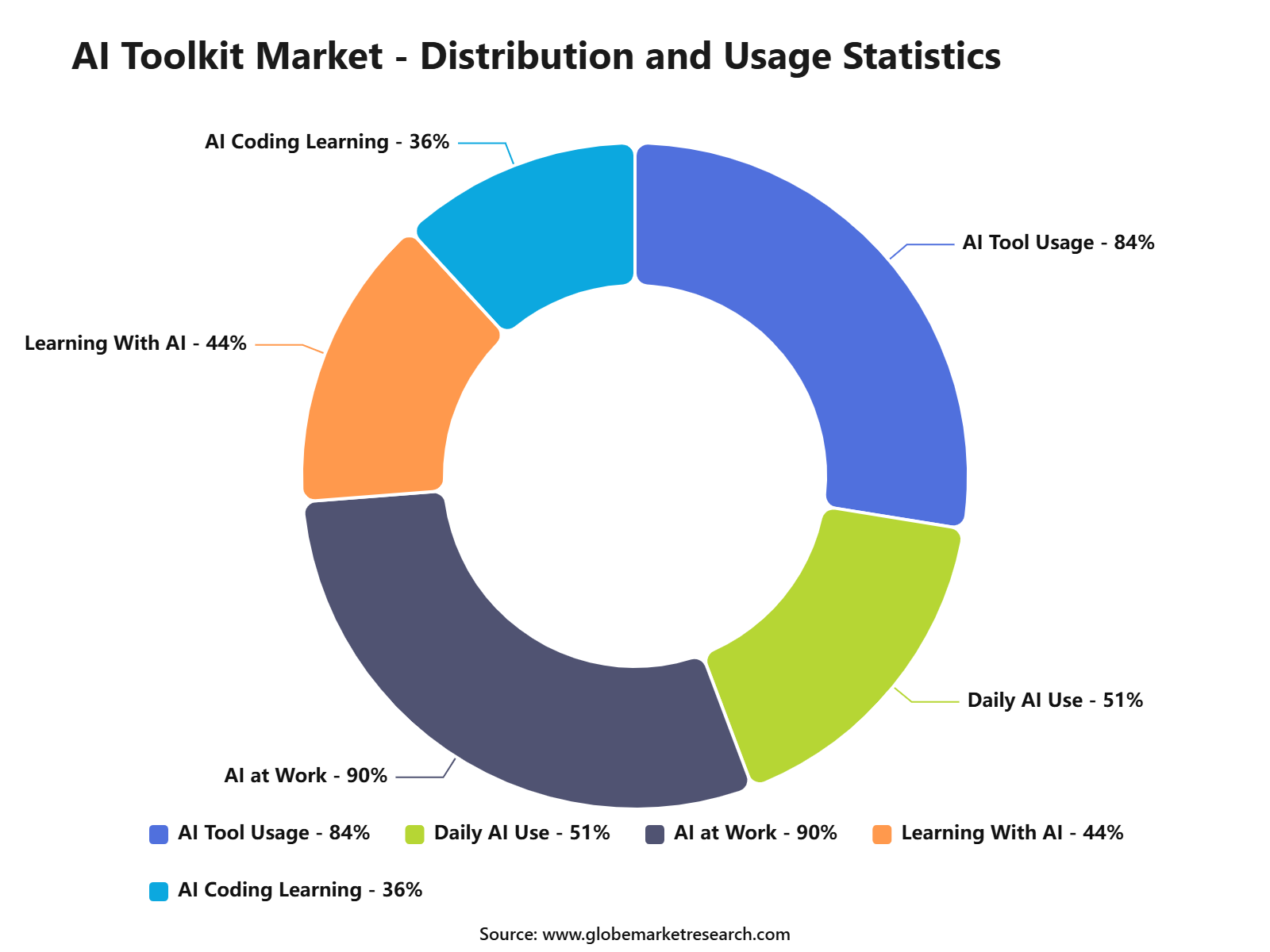

Demand is being supported by fast developer adoption, as Stack Overflow’s 2025 Developer Survey found that 84% of respondents were using or planning to use AI tools in their development process, while 51% of professional developers used AI tools daily. Sales economics are strongest when vendors combine usage-based pricing, enterprise seats, integration support, security controls, and measurable productivity outcomes.

AI toolkit buyers are no longer looking only for chat interfaces. They need tools that connect with IDEs, GitHub, CI/CD systems, cloud platforms, data warehouses, ticketing systems, documentation, and internal knowledge bases. GitHub reported in Octoverse 2025 that AI, agents, and typed languages are driving one of the largest shifts in software development in more than a decade, while a new developer was joining GitHub every second.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape for AI toolkits is spread across developer tools, coding assistants, AI agents, model APIs, workflow automation, MLOps, LLMOps, vector search, retrieval-augmented generation, data labeling, synthetic data, model testing, monitoring, compliance, security, and enterprise knowledge tools. Developer tools are one of the most visible revenue areas because AI is now being embedded directly into IDEs, code repositories, pull request review, documentation, testing, and deployment workflows.

Revenue is also expanding through usage-based AI infrastructure. OpenAI’s API pricing shows how AI toolkit economics are increasingly linked to token usage, cached input, output generation, tool calls, file search, hosted code execution, and storage. This supports flexible monetization, but it also makes cost management a core buying factor for customers that run large-scale AI workflows.

Financial Impact

The financial impact can be positive for vendors that build sticky workflow integrations and move beyond simple prompt tools. Stronger margins can be created through enterprise subscriptions, API usage, private deployment, governance modules, developer productivity analytics, security scanning, compliance features, and agent orchestration. GitHub Copilot crossed 20 million all-time users in 2025, showing that AI-assisted development has moved from early experimentation into mainstream developer adoption.

Financial risk remains linked to compute cost, model provider dependency, customer churn, regulatory compliance, data protection, and output liability. AI toolkit vendors also face competition from cloud platforms, open-source models, coding assistants, low-code tools, and internal enterprise AI systems. The strongest financial resilience is expected from vendors that provide measurable productivity value, strong governance, secure deployment, reliable integrations, and transparent usage-based pricing rather than depending only on broad AI excitement.

Top Two Opportunities

Enterprise AI Workflow Toolkits

The strongest opportunity is in enterprise AI workflow toolkits that help companies move from experimentation to measurable productivity. Adoption is already high, but value capture remains uneven. Stanford AI Index 2026 reported that organizational AI adoption reached 88% of surveyed organizations in 2025, while generative AI was used in at least one business function by 70% of organizations.

However, Reuters reported that 77% of surveyed French mid-sized companies used generative AI, but only 17% of users had seen time savings. This creates a clear demand gap for toolkits that connect AI models with real business workflows, approvals, governance, data access, and performance tracking. The recommended focus should be on toolkits for sales, customer support, legal review, finance operations, HR, procurement, software development, and knowledge management.

These areas have repeatable tasks, measurable outputs, and clear ROI tracking. The toolkit should include prompt libraries, model evaluation, workflow automation, role-based access, audit trails, data connectors, cost monitoring, and human review controls. This would help enterprises reduce scattered AI use and shift toward governed, department-level deployment.

Agent Governance and AI Safety Toolkits

The second major opportunity is in AI agent governance, monitoring, and safety toolkits. AI agents are still in the early stage, but the need for secure deployment is rising quickly as companies begin to connect AI systems with emails, files, customer records, codebases, finance systems, and internal applications. Stanford AI Index 2026 reported that AI agent deployment remained in single digits across nearly all business functions, which shows that the market is still early but positioned for expansion.

The recommended focus should be on toolkits that provide policy enforcement, permission control, agent testing, red-teaming, activity logs, approval workflows, rollback options, and compliance reporting. Microsoft’s 2026 Work Trend Index noted that securing agents requires monitoring, policy enforcement, and auditability to reduce risks such as data exfiltration, unintended system actions, and unauthorized access. This makes governance toolkits highly valuable for regulated sectors such as banking, healthcare, insurance, legal services, public sector, and enterprise IT.

Competitive Landscape Assessment

The AI Toolkits Market is expanding rapidly as enterprises, developers, data science teams, and product teams increase the use of AI platforms for model development, training, deployment, monitoring, governance, and agent-based automation. The market is supported by rising adoption of machine learning, generative AI, large language models, retrieval-augmented generation, model orchestration, and MLOps platforms. Demand is also being driven by the need to move AI projects from experimentation to production.

Competition is strongest among cloud AI platforms, open-source AI ecosystems, enterprise MLOps providers, GPU-accelerated software platforms, and model development frameworks. Large technology companies compete through integrated cloud infrastructure, foundation model access, developer tools, security controls, and enterprise support. Open-source platforms compete through flexibility, community adoption, faster experimentation, and lower entry barriers.

The competitive landscape is moving from standalone model-building tools toward full AI lifecycle platforms. Buyers increasingly prefer solutions that support data preparation, model selection, training, fine-tuning, evaluation, deployment, monitoring, cost control, security, and compliance from one environment. Companies that provide open model choice, strong governance, and flexible deployment across cloud, on-premises, and hybrid infrastructure are expected to remain better positioned.

Implementation Complexity & Technology Readiness

AI Toolkit Technology | Implementation Complexity | Technology Readiness | Market Position |

|---|---|---|---|

Machine learning frameworks | Moderate to High | High | Widely used for model development. |

Cloud AI platforms | High | High | Strong enterprise adoption. |

Generative AI development platforms | High | Moderate to High | Rapidly growing for AI applications. |

MLOps platforms | High | High | Critical for production AI workflows. |

Model hubs and open-source repositories | Low to Moderate | High | Strong developer adoption. |

Agent-building toolkits | High | Moderate | Rising adoption, but reliability remains a challenge. |

Competitive Landscape by Product Category

Product Category | Competitive Intensity | Key Buying Factors | Competitive Position |

|---|---|---|---|

Cloud AI platforms | Very High | Model choice, scalability, security, integration, pricing, governance | Strongest in enterprise AI lifecycle support. |

Open-source frameworks | High | Flexibility, community support, performance, documentation, ecosystem | Strong developer preference. |

Generative AI APIs | Very High | Model quality, latency, cost, context length, multimodal support, safety | Rapid adoption across AI applications. |

MLOps platforms | High | Deployment control, monitoring, versioning, collaboration, compliance | Important for production AI workloads. |

Model hubs | High | Model availability, dataset access, community trust, licensing clarity | Strong role in prototyping and open AI. |

Key Players in the AI Toolkit Market

Company | Competitive Focus |

|---|---|

Microsoft | Azure AI Foundry, Azure OpenAI, model catalog, AI agents, governance, and developer tools. |

Google Cloud | Gemini Enterprise Agent Platform, custom model training, GenAI, ML lifecycle, and cloud AI infrastructure. |

Amazon Web Services | Amazon Bedrock, SageMaker, model choice, guardrails, agent development, and cloud AI services. |

IBM | watsonx.ai, RAG development, model tuning, AI agents, governance, and workflow automation. |

OpenAI | AI models, APIs, Responses API, Agents SDK, multimodal AI, coding tools, and enterprise A |

Recent Developments

February 2026, Anthropic announced that Apple’s Xcode 26.3 added native support for the Claude Agent SDK. The integration gives developers access to Claude Code inside Xcode, including subagents, background tasks, and plugins. This development strengthens the AI toolkit ecosystem by embedding agentic coding directly into mainstream software development environments.

February 2026, GitHub made Claude by Anthropic and OpenAI Codex available as coding agents for Copilot Business and Copilot Pro users. GitHub also said Copilot’s coding agent gained a model picker, self-review, built-in security scanning, custom agents, and CLI handoff. This shows that AI toolkits are moving from single coding assistants toward multi-agent development platforms.

March 2026, NVIDIA introduced Agent Toolkit, including OpenShell secure runtime, AI-Q Blueprint, Nemotron models, and tools for building self-evolving agents with stronger safety and security controls. NVIDIA said the AI-Q Blueprint, built with LangChain, topped DeepResearch Bench accuracy leaderboards and could reduce query costs by half through a hybrid model approach. This development supports enterprise demand for agent development, secure runtime, and AI workflow orchestration.

People Also Ask

How big is the AI toolkit market?

The global AI toolkit market is projected to reach USD 874.0 billion by 2035. Growth is being supported by rising demand for AI development platforms, AI APIs, coding assistants, model deployment tools, and enterprise automation solutions.

What is an AI toolkit?

An AI toolkit is a set of tools used to build, train, test, deploy, and manage artificial intelligence applications. It can include software libraries, APIs, model frameworks, cloud platforms, data tools, testing systems, and monitoring dashboards. AI toolkits help developers and businesses create AI solutions faster and more efficiently.

Why are AI toolkits important?

AI toolkits are important because they reduce the technical effort required to build and deploy AI applications. They help teams manage models, connect data, test outputs, automate workflows, and improve development speed. Without these tools, AI deployment can become slow, costly, and difficult to scale.

What are examples of AI toolkits?

Examples of AI toolkits include TensorFlow, PyTorch, Hugging Face Transformers, NVIDIA AI Enterprise, Amazon SageMaker, Google Vertex AI, Microsoft Azure AI Studio, IBM watsonx, OpenAI API, GitHub Copilot, LangChain, LlamaIndex, and MLflow. These tools support model development, generative AI applications, coding assistance, deployment, and monitoring.

What is driving demand for AI toolkits?

Demand is being driven by generative AI adoption, software automation, cloud AI infrastructure, enterprise AI transformation, and the need for faster application development. Businesses want tools that can help them build AI solutions without creating every component from the beginning. Developers also need AI toolkits that fit into existing coding, testing, and deployment workflows.

Which industries use AI toolkits the most?

AI toolkits are widely used in technology, banking, healthcare, retail, manufacturing, telecom, media, education, logistics, and cybersecurity. Technology companies use them for software development and automation, while healthcare and finance use them for decision support, analytics, and risk management. Retail and media companies use AI toolkits for personalization, content creation, and customer engagement.

What are the latest trends in AI toolkits?

The latest trends include AI agents, multimodal AI, enterprise copilots, private AI deployment, AI governance, retrieval-augmented generation, and automated model evaluation. Toolkits are also becoming more user-friendly through low-code interfaces and prebuilt integrations. This makes AI development more accessible to non-specialist business teams.