Revenue, 2025

$134.5 Bn

Forecast, 2035

$722.0 Bn

CAGR, 2025-2035

18.3%

Report Coverage

Global

Market Size and Forecast

2025

$134.5 Bn

2035

$722.0 Bn

CAGR

18.3%

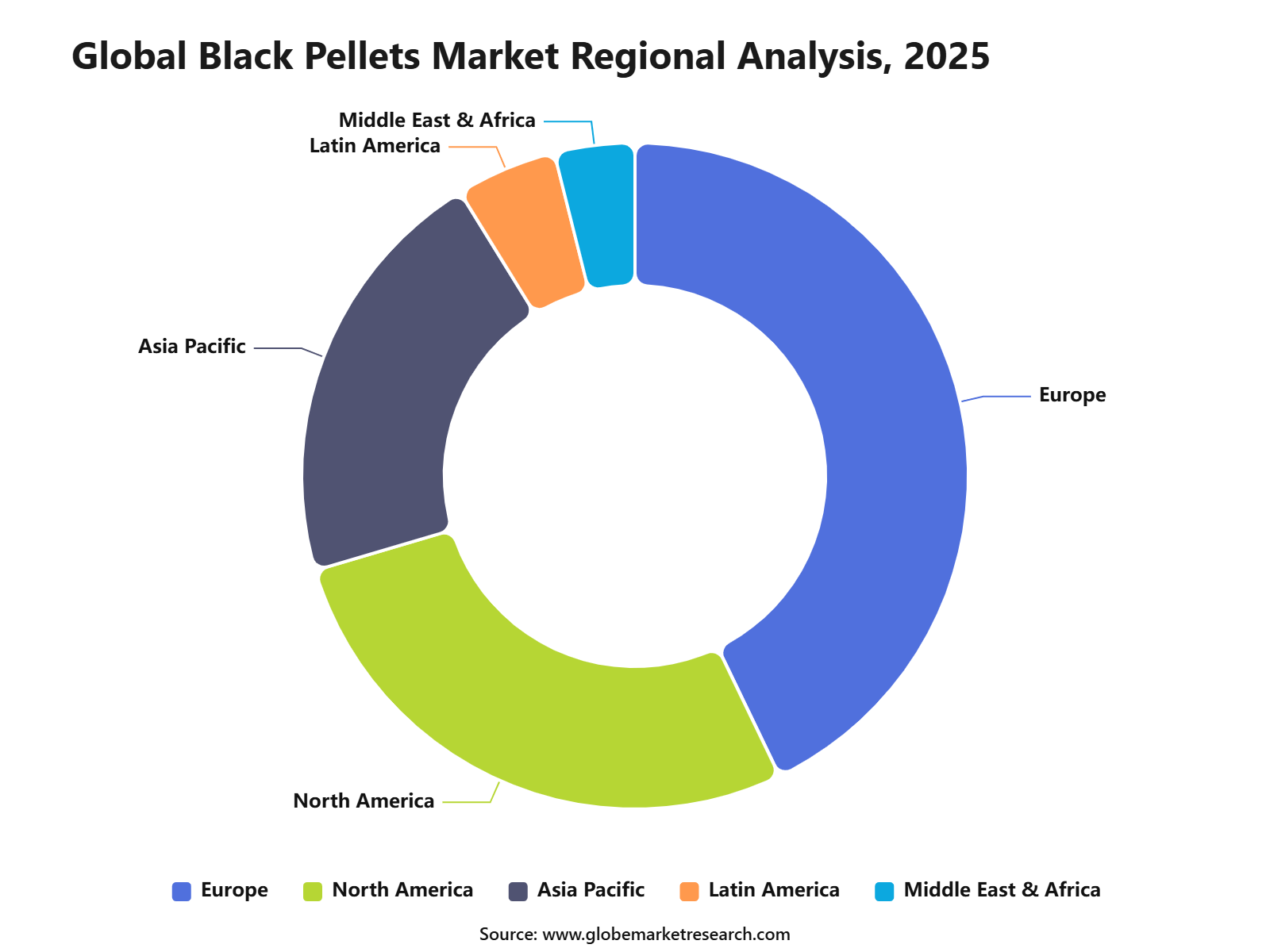

The global Black Pellets Market was valued at USD 134.5 billion in 2025 and is projected to reach USD 722.1 billion by 2035, growing at a CAGR of 18.3%. Europe led the market with a 42.9% share in 2025, supported by strong biomass adoption, strict carbon reduction targets, rising demand for renewable heating fuels, and increasing coal replacement across industrial and utility applications.

The Black Pellets Market refers to the production and use of upgraded biomass pellets made through torrefaction, steam explosion, or similar thermal treatment processes. These pellets are darker, drier, denser, and more water-resistant than conventional white wood pellets. They are mainly used as a renewable solid fuel in power generation, industrial heating, district heating, and coal co-firing applications.

Black pellets are produced from biomass feedstocks such as wood residues, forest waste, agricultural residues, sawdust, and other organic materials. Their key advantage is higher energy density and better storage stability compared with regular biomass pellets. Torrefied pellets commonly provide a gross calorific value of about 4,500 to 5,500 kcal/kg, compared with around 3,500 to 4,200 kcal/kg for standard biomass pellets. This makes black pellets suitable for utilities and industrial users that need a fuel with stronger combustion performance and easier logistics.

Key Insight Summary

Torrefied black pellets held 55.9% share in the black pellets market, supported by their higher energy density, improved moisture resistance, and better suitability for coal-fired power plant co-firing.

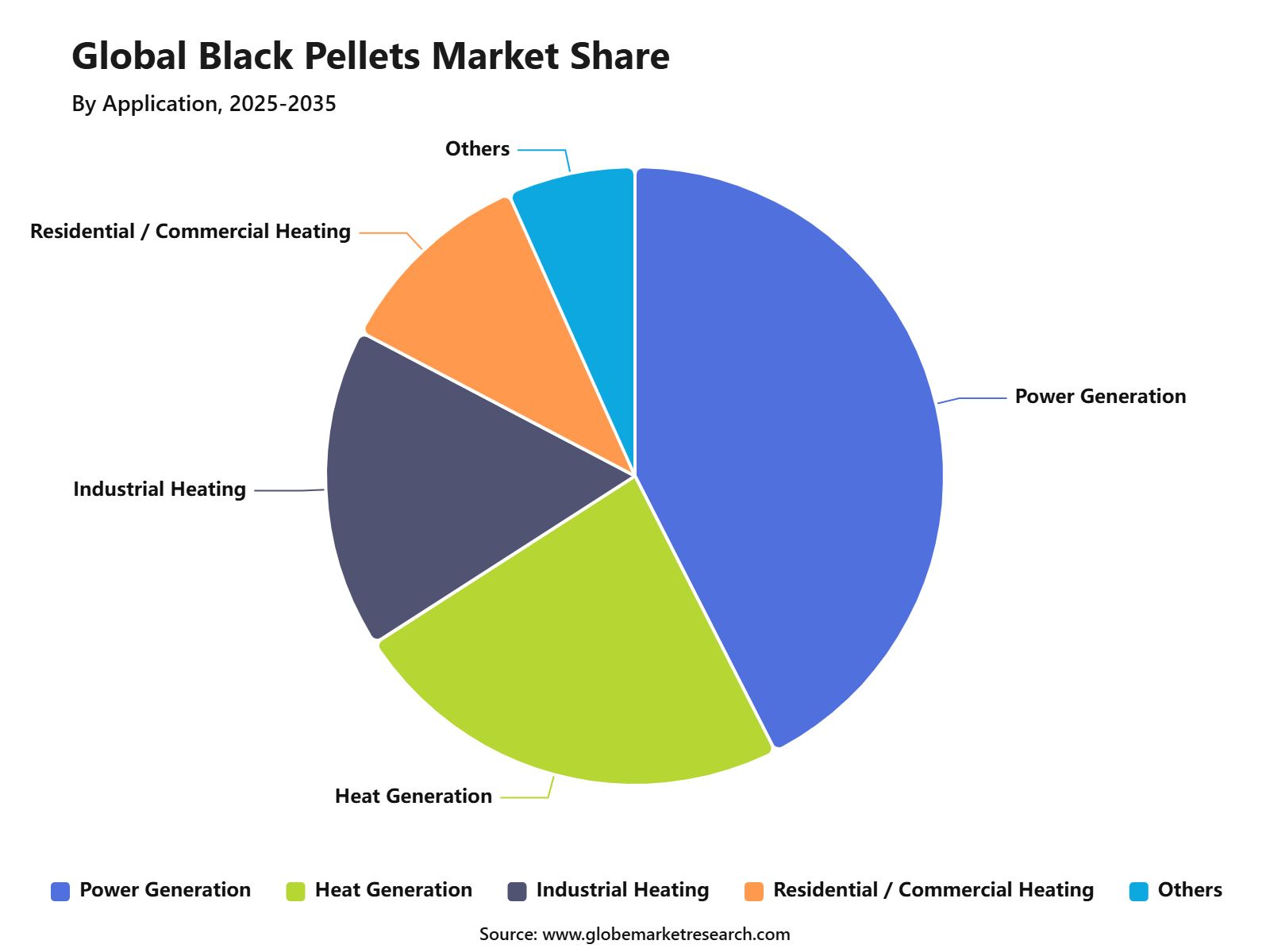

Power generation accounted for 42.5% share, driven by rising use of black pellets as a renewable solid fuel for electricity production and coal replacement.

Wood biomass and forest residues dominated the raw material segment with 70.0% share, supported by wide feedstock availability and established biomass supply chains.

Utilities and power plants held 65.0% share, as black pellets are increasingly used to reduce fossil fuel dependence and support renewable energy targets.

Europe accounted for 42.9% share of the black pellets market, supported by strong biomass energy policies, coal phase-out targets, and rising demand for low-carbon fuel alternatives.

Black Pellets Statistics

The Netherlands remains a key industrial pellet market in Europe. In 2024, the country imported 1.50 million metric tons of wood pellets valued at USD 325 million.

The United States was the leading supplier to the Netherlands in 2024, shipping 0.76 million metric tons of wood pellets worth USD 148 million.

Europe’s pellet import dependence remains high. In 2024, the EU imported 4.48 million metric tons of wood pellets valued at around USD 1.0 billion.

EU pellet imports declined compared to 2023, but demand is expected to recover as industrial consumption improves and domestic biomass supply remains limited.

Bioenergy-based power generation is expected to grow strongly. The IEA states that electricity generation from bioenergy could rise from about 700 TWh in 2023 to nearly 1,250 TWh by 2030 under the Net Zero Scenario.

The United States remained the largest wood pellet supplier to the EU in 2024, exporting 1.90 million metric tons valued at USD 425 million.

The U.S. share of EU pellet imports declined from 59% to 42%, showing that Europe is diversifying its biomass supply chain.

Segment Highlights

By Type

In 2025, Torrefied black pellets led the Black Pellets Market with 55.9% share, supported by their higher energy density, better moisture resistance, and easier storage compared with conventional white pellets. These pellets are produced through thermal treatment, which improves grindability and makes them more suitable for coal-fired power plants that are moving toward lower-carbon fuel blends.

The segment is also supported by the growing use of advanced biomass fuels in industrial power and heat applications. In 2025, U.S. wood pellet exports reached more than 10.09 million metric tons, showing continued international demand for densified biomass fuels used in energy markets. In Q1 2026, U.S. wood pellet exports also rose to 2.68 million metric tons, compared with 2.4 million metric tons in Q1 2025.

By Application

In 2025, Power generation accounted for 42.5% share in the Black Pellets Market, driven by rising use of biomass-based fuels in electricity production and coal replacement applications. Black pellets are suitable for power plants because they can offer better handling, higher heating value, and improved compatibility with existing fuel systems.

The demand from power generation is supported by Europe’s continued use of biomass in renewable electricity. IEA Bioenergy reported that biomass-based electricity represented around 6% of EU27 electricity production in recent years, while solid biomass accounted for around half of bio-electricity output. This supports demand for high-density biomass fuels such as black pellets in utility-scale applications.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Raw Material

In 2025, Wood biomass and forest residues dominated the raw material segment with 70.0% share. These feedstocks are widely used because they are available through forestry operations, sawmill by-products, thinning activities, and wood processing residues. Their strong availability makes them the preferred base material for producing torrefied and steam-exploded black pellets.

This segment is also supported by the role of solid biomass in modern bioenergy systems. IEA Bioenergy stated that countries with large forest resources and wood processing industries are among the strongest users of solid biomass for energy. However, countries with limited domestic forest biomass, including the Netherlands, the UK, Belgium, and Denmark, depend heavily on solid biomass imports for energy use.

By End-User

In 2025, Utilities and power plants held 65.0% share of the Black Pellets Market, supported by growing demand for renewable solid fuels in large-scale electricity generation. These end users require fuel that can be transported, stored, and co-fired with existing energy infrastructure. Black pellets are attractive because they can support higher energy output and better logistics compared with untreated biomass.

The segment is also linked to Europe’s industrial pellet demand and import dependence. The UK remained one of the largest global consumers of wood pellets, mainly due to its biomass energy sector, while its biomass imports were forecast at more than 9.6 million metric tons in CY2025. This shows the continued importance of utilities and power plants in the biomass fuel value chain.

By Regional Analysis

In 2025, Europe led the Black Pellets Market with 42.9% share, supported by strong biomass energy policies, industrial pellet demand, and the use of solid biomass in renewable power generation. The region has a mature biomass fuel supply chain, with demand coming from power plants, district heating, industrial heating, and co-firing applications.

Europe also remains highly dependent on pellet imports in several markets. In 2024, EU wood pellet imports totaled around 4.48 million metric tons, valued at about USD 1.0 billion, while imports from the U.S. reached 1.90 million metric tons worth USD 425 million. In 2025, EU pellet imports were expected to recover as industrial use improved and power plant demand stabilized.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFMarket Dynamics

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for renewable energy | +4.8% | Europe, North America, Asia Pacific | Supports biomass fuel adoption. |

Growth in coal replacement initiatives | +4.2% | Europe, Japan, South Korea, Canada | Drives demand in power generation. |

Higher energy density than white pellets | +3.6% | Global | Improves transport and storage efficiency. |

Increasing industrial decarbonization | +3.4% | Europe, U.S., Japan, South Korea | Supports low-carbon fuel switching. |

Growth in biomass-based power generation | +3.1% | Europe, Asia Pacific, North America | Expands utility-scale usage. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High production cost | -2.6% | Global | Limits price competitiveness. |

Limited commercial-scale production | -2.1% | North America, Europe, Asia Pacific | Restricts supply availability. |

Feedstock supply constraints | -1.8% | Europe, North America, Asia Pacific | Affects production stability. |

Competition from white pellets | -1.5% | Global | Slows substitution rate. |

Policy and certification barriers | -1.3% | Europe, Japan, South Korea | Raises compliance burden. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Expansion of torrefaction technology | +4.0% | Europe, U.S., Canada, Japan | Improves black pellet output. |

Growth in industrial heat applications | +3.5% | Europe, Asia Pacific, North America | Opens non-power demand. |

Rising demand from coal-fired power plants | +3.8% | Japan, South Korea, Europe | Supports co-firing use. |

Long-term biomass supply contracts | +3.0% | Europe, North America, Asia Pacific | Improves revenue visibility. |

Emerging demand in Asia Pacific | +3.4% | Japan, South Korea, China, India | Creates new growth markets. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Scaling torrefaction capacity | -2.2% | Global | Delays large-scale adoption. |

Logistics and handling issues | -1.6% | Export markets, power utilities | Impacts supply chain efficiency. |

Price volatility in biomass feedstock | -1.7% | North America, Europe, Asia Pacific | Pressures producer margins. |

Lack of standardization | -1.4% | Global | Affects buyer confidence. |

Technology commercialization risk | -1.8% | Global | Slows investor commitment. |

Demand and Growth Outlook

Demand Analysis

Demand for black pellets is closely linked to the wider growth of biomass power, renewable heat, and industrial decarbonization. Bioenergy generated about 711 TWh of electricity in 2024, representing around 7% of global renewable electricity, while bioenergy supplied about 73% of renewable heat worldwide. These figures show that solid bioenergy remains important in sectors where direct electrification is difficult or costly.

Demand is also supported by the large wood pellet ecosystem already present in Europe, North America, and Asia. The European Union remains one of the leading regions for wood pellet production and consumption, supported by heating demand, biomass-based power generation, and sustainability policies. In 2024, EU wood pellet production capacity was expected to reach around 27.5 million metric tons per year, up from 27.2 million metric tons in the previous year.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Demand from power generation | +4.6% | Europe, Japan, South Korea | Drives core consumption. |

Demand for coal alternatives | +4.1% | Global | Supports fuel substitution. |

Demand from industrial boilers | +3.2% | Europe, North America, Asia Pacific | Expands end-use adoption. |

Demand for lower logistics cost fuels | +2.9% | Export markets | Improves trade economics. |

Demand for dispatchable renewable energy | +3.4% | Europe, Asia Pacific, North America | Supports stable biomass power. |

Growth Factors

The main growth factor for black pellets is the increasing need for low-carbon fuels in industries that still depend on coal, gas, or oil for process heat. Renewable energy consumption across power, heat, and transport is projected by the IEA to rise by nearly 60% between 2024 and 2030, increasing the renewable share of final energy consumption to nearly 20% by 2030, compared with 13% in 2023. This wider renewable energy expansion is expected to create stronger demand for biomass-based fuels in heat and power applications.

Another growth factor is the rising use of biomass co-firing in coal-based power plants. In India, biomass pellet use in thermal power plants has increased strongly as part of efforts to reduce crop residue burning and lower coal dependence. Reported biomass pellet co-firing across 65 thermal plants in 15 Indian states reached more than 2.04 million metric tons during the reviewed period, with Punjab and Haryana showing sharp increases in pellet use.

Key Market Segments

By Type

Torrefied Black Pellets

Hydrothermal Carbonized Pellets

Steam-Exploded Pellets

By Application

Heat Generation

Power Generation

Industrial Heating

Residential / Commercial Heating

By Raw Material

Wood Biomass / Forest Residues

Agricultural Residues

Energy Crops

Others

By End-User

Utilities / Power Plants

Industrial Users

Commercial Heating Users

Residential Users

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Rest of Asia Pacific

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Recent Developments

January 2026 – Idemitsu Kosan highlighted its black pellet expansion roadmap in Japan’s low-carbon energy transition. The company reported net sales of about USD 61.3 billion and positioned black pellets as a coal-alternative fuel for utilities and industrial users. Its strategy supports Japan’s co-firing demand and long-term biomass fuel security.

November 2025 – PowerWood Canada Corp. announced plans to build two black pellet production facilities in Northern Alberta. The facilities will convert wildfire deadwood into low-carbon black pellets for Japanese power plants. The project is expected to create around 500 jobs and start production by the end of 2026.

June 2025 – PEARL Infrastructure Capital II acquired a 65% majority stake in Arbaflame AS, a Norway-based advanced black pellet producer. The acquisition is expected to support scale-up of Arbaflame’s Arba One production facility and strengthen Europe’s supply of advanced biomass fuels.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 134.5 Bn |

Forecast Revenue (2035) | USD 722.1 Bn |

CAGR (2025-2035) | 18.3% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI impact analysis, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends |

Segments Covered | By Type (Torrefied Black Pellets, Hydrothermal Carbonized Pellets, Steam-Exploded Pellets), By Application (Heat Generation, Power Generation, Industrial Heating, Residential / Commercial Heating and Others), By Raw Material (Wood Biomass / Forest Residues, Agricultural Residues, Energy Crops and Others), By End-User (Utilities / Power Plants, Industrial Users, Commercial Heating Users, Residential Users), By Regional Insights |

Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Idemitsu Kosan. co., Valmet Oyj, Verdo A/S, Bionet, Airex Energy Inc., Zilkha Biomass Energy LLC, Blackwood Technology B.V., Biomass Secure Power Inc., Foresta Group Holdings Limited, Boreal Bioenergy Corporation, Arbaflame AS, CoAlternative Energy Ltd., Futerra Fuels, Bioendev AB, Other Key Players |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Idemitsu Kosan Co.Ltd.

Valmet Oyj

Verdo A/S

Bionet

Airex Energy Inc.

Zilkha Biomass Energy LLC

Blackwood Technology B.V.

Biomass Secure Power Inc.

Foresta Group Holdings Limited

Boreal Bioenergy Corporation

CoAlternative Energy Ltd.

Arbaflame AS

Futerra Fuels

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Suraj is a Senior Management Consultant with over 7 years of experience in market research, business strategy, and consulting. He has worked with Fortune 500 companies and growing startups, helping them with market entry, cross-border expansion, demand analysis, competitive assessment, and growth planning. His analytical thinking and strong industry knowledge help clients make clear, confident, and informed business decisions.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Water and Wastewater Treatment Equipment Market to Exceed USD 136.6 Billion by 2035

Global Water and Wastewater Treatment Equipment Market Size By Application (Municipal, Industrial), By Process (Primary Treatment, Secondary Treatment, Tertiary Treatment), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Marine Composites Market to hit USD 15.7 Bn By 2035

Global Marine Composites Market Size By Composite Type (Polymer-Matrix Composites, Metal-Matrix Composites, Ceramic-Matrix Composites), By Resin Type (Epoxy, Polyester, Others), By Vessel Type (Sailboats, Cruise Ships & Yachts, Power Boats, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Caprolactone Market Size to Reach USD 638 Mn by 2035

Global Caprolactone Market Size and Trade Analysis Report By Type (99.5% Purity, 99.9% Purity), By Application (Polycaprolactone (PCL), Acrylic Resin Modified, Polyesters Modified, Epoxy Resin Modified, Others), By End-Use Industry (Industrial Applications, Packaging, Healthcare, Automotive, Construction), By Regional Insights, Leading Companies and Growth Forecasts by 2025-2035