Revenue, 2025

$333.52 Mn

Forecast, 2035

$638 Mn

CAGR, 2025-2035

6.7%

Report Coverage

Global

Market Size and Forecast

2025

$333.52 Mn

2035

$638 Mn

CAGR

6.7%

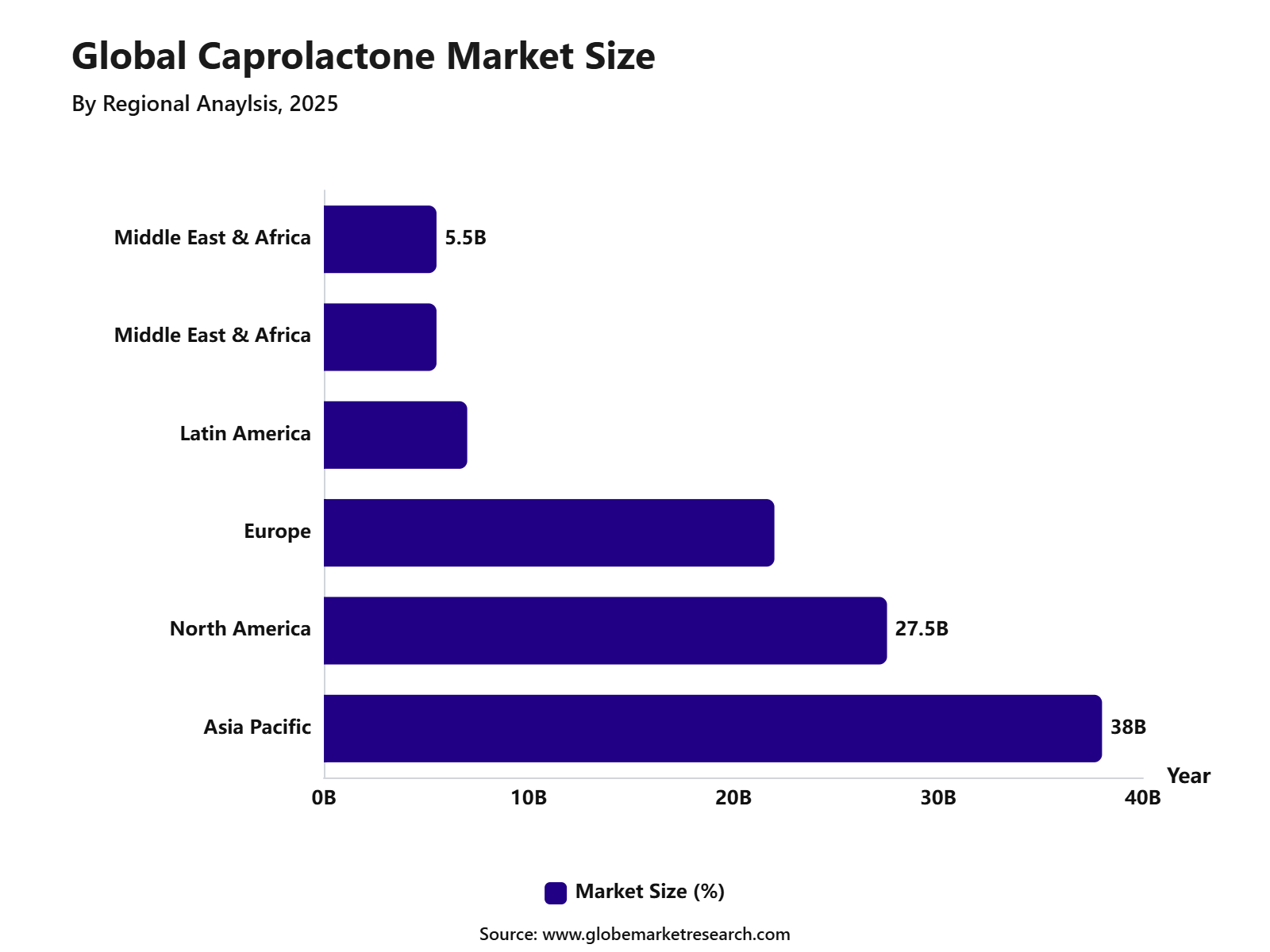

The global Caprolactone Market was valued at USD 333.52 million in 2025 and is projected to reach USD 638 million by 2035, growing at a CAGR of 6.7% during the forecast period. Asia Pacific held a leading position in the Caprolactone Market, accounting for 38% of the market share in 2026.

Demand for caprolactone is mainly supported by polycaprolactone applications, which account for around 48.6% of the market. The 99.5% purity grade holds nearly 61.3% share due to its wider use in high-performance polymer and industrial formulations. Industrial applications represent about 55.4% of demand, supported by rising use in coatings, sealants, adhesives, and polyurethane modification.

The growth of the market can be attributed to increasing demand for sustainable materials, expansion of specialty chemical applications, and rising use of advanced polymers in end-use industries. Asia Pacific accounts for nearly 40.2% of the market, driven by strong manufacturing activity, growing chemical production, and higher demand from industrial users. The market is expected to grow at a stable pace as manufacturers continue to focus on durable, lightweight, and environmentally safer materials.

Key Market Insights

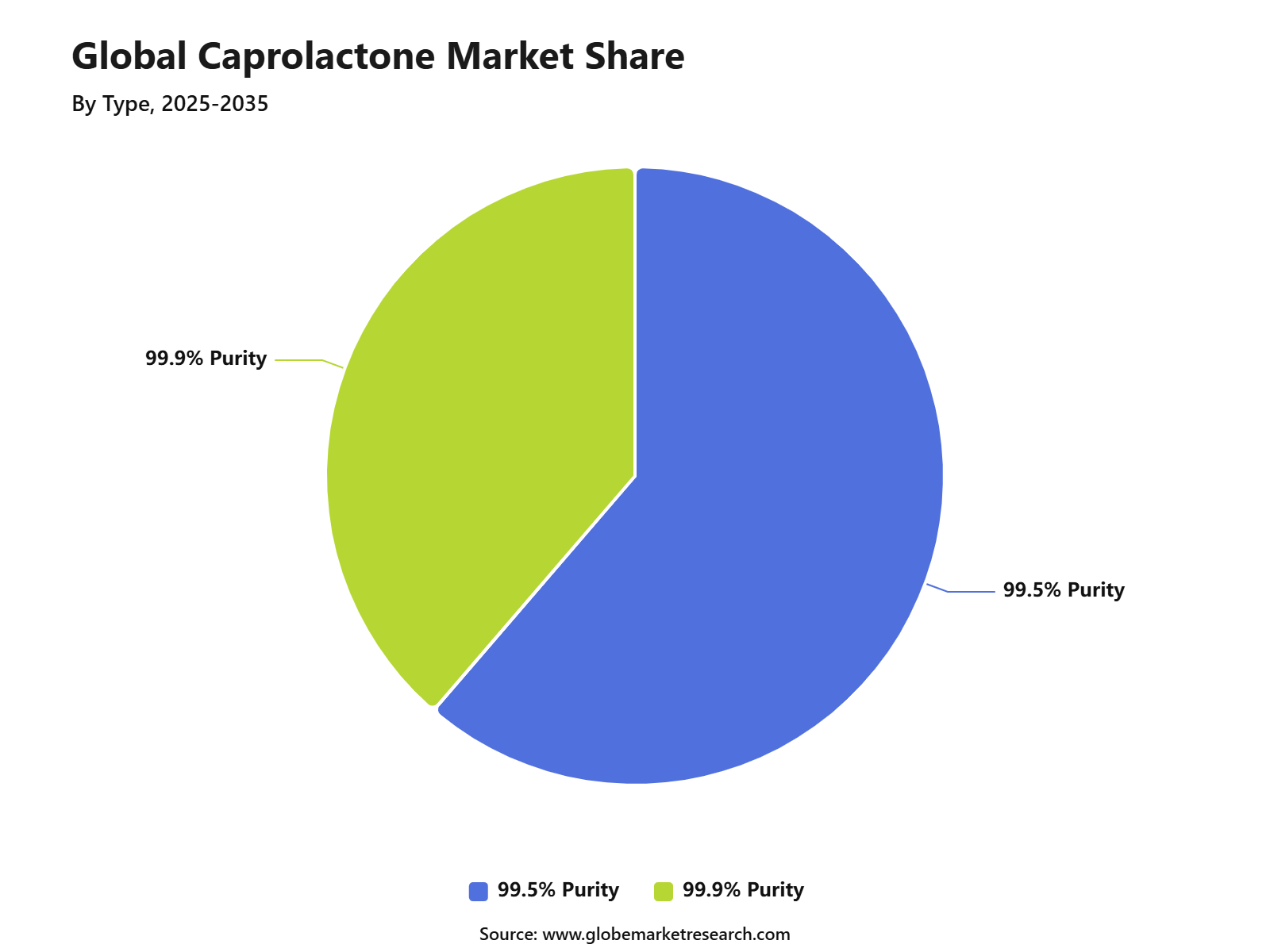

By type, 99.5% purity leads the Caprolactone market with 61.3% share, supported by its wide use in high-performance polymer production and specialty chemical applications.

The strong position of 99.5% purity can be linked to its better consistency and quality, which makes it suitable for applications where stable material performance is required.

By application, Polycaprolactone (PCL) holds the leading share of 48.6%, driven by its use in biodegradable plastics, coatings, adhesives, and medical-grade materials.

Demand for PCL is increasing due to its flexibility, biodegradability, and processing ease, which support its adoption across both industrial and advanced material applications.

By end-use industry, industrial applications account for 55.4% of the market, reflecting strong consumption in coatings, resins, elastomers, and performance materials.

Industrial users prefer Caprolactone due to its ability to improve durability, flexibility, and chemical resistance in finished products.

Asia Pacific dominates the regional market with a 40.2% share, supported by strong manufacturing activity, expanding chemical production, and growing demand from plastics and industrial material sectors.

The region’s leadership is also supported by cost-efficient production capacity and rising downstream demand, especially from packaging, automotive, construction, and specialty polymer applications.

Market Dynamics

Drivers Impact Analysis

Factor | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Line |

|---|---|---|---|

Rising demand for polycaprolactone in biodegradable polymers | 1.8% | North America, Europe, Asia Pacific | Growth is supported by wider use of PCL in sustainable plastics and specialty polymer applications. |

Expanding use in healthcare and drug delivery systems | 1.5% | North America, Europe, Japan, South Korea | Caprolactone demand is increasing due to its role in medical-grade polymers, implants, and controlled drug release. |

Growth in coatings, adhesives, and elastomer applications | 1.2% | Asia Pacific, Europe | Industrial use is rising as manufacturers seek flexible, durable, and high-performance polymer materials. |

Increasing demand from packaging and consumer goods | 1.0% | Asia Pacific, North America | Demand is supported by the shift toward recyclable and biodegradable material solutions. |

Restraint Impact Analysis

Factor | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Line |

|---|---|---|---|

High production cost of caprolactone-based materials | -1.4% | Global | Higher cost limits adoption in price-sensitive applications and restricts large-scale replacement of conventional polymers. |

Limited availability of raw materials | -1.1% | Asia Pacific, Europe | Supply uncertainty can affect production planning and increase procurement pressure for manufacturers. |

Competition from alternative biodegradable polymers | -0.9% | Global | Substitutes such as PLA, PBS, and other bio-based polymers may reduce caprolactone demand in some applications. |

Strict chemical handling and environmental regulations | -0.7% | Europe, North America | Compliance requirements may increase operating costs and slow capacity expansion. |

Opportunity Impact Analysis

Factor | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Line |

|---|---|---|---|

Rising investment in bio-based and specialty polymers | 1.6% | Europe, North America, Asia Pacific | New material development is expected to support higher use of caprolactone in premium polymer applications. |

Growth in medical-grade PCL applications | 1.4% | United States, Germany, Japan, South Korea | Strong demand from implants, tissue engineering, and drug delivery creates high-value growth opportunities. |

Expansion of biodegradable packaging materials | 1.2% | Asia Pacific, Europe | Packaging producers are expected to increase adoption of caprolactone-based materials due to sustainability targets. |

Emerging use in 3D printing and advanced manufacturing | 0.9% | North America, Europe, China | Caprolactone-based polymers are gaining interest due to flexibility, biodegradability, and processing benefits. |

Segment Insights

By Type

The 99.5% purity segment dominates the Caprolactone market with 61.3% share. This grade is widely preferred because it offers better purity control, stable chemical behavior, and reliable performance in polymer and specialty chemical production. Manufacturers use this purity level where product consistency and process efficiency are important.

The demand for 99.5% purity Caprolactone is strongly supported by its use in polycaprolactone production, coatings, elastomers, adhesives, and high-performance material formulations. Its low impurity content helps improve the quality of the final product and reduces processing issues. As industries continue to focus on durable and controlled polymer solutions, this segment is expected to maintain a strong position in the market.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Application

Polycaprolactone (PCL) is the leading application segment in the Caprolactone market, accounting for 48.6% share. The segment is gaining strong demand due to the increasing use of biodegradable polymers and flexible plastic materials. PCL is valued for its low melting point, good blend compatibility, and ability to support sustainable material development.

The use of PCL is increasing across medical devices, drug delivery systems, packaging, adhesives, coatings, and polymer blending applications. Its biodegradable nature makes it suitable for industries looking for alternative materials with improved environmental performance. The segment is also supported by growing demand for specialty polymers that offer flexibility, strength, and controlled degradation properties.

By End-Use Industry

Industrial applications hold the largest share of the Caprolactone market with 55.4% . This segment includes the use of Caprolactone in coatings, adhesives, sealants, elastomers, resins, and specialty polymer manufacturing. Demand is mainly driven by the need for materials that provide flexibility, durability, chemical resistance, and improved processing performance.

The growth of industrial applications can be attributed to rising use in manufacturing, construction-related materials, automotive components, and performance coatings. Caprolactone-based materials help improve product life, surface quality, and mechanical strength. As industrial users continue to adopt advanced polymer materials for better performance and reliability, this segment is likely to remain a key revenue contributor in the market.

By Regional Analysis

Asia Pacific leads the market with 38.0% share, supported by strong industrial demand, growing manufacturing activity, and rising product use across key application sectors. North America and Europe hold notable shares due to established end-use industries, advanced production capabilities, and steady demand for high-purity materials. Latin America and the Middle East & Africa represent emerging markets, supported by gradual industrial expansion and infrastructure development.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Segment

By Type

99.5% Purity

99.9% Purity

By Application

Polycaprolactone (PCL)

Acrylic Resin Modified

Polyesters Modified

Epoxy Resin Modified

Others

By End-Use Industry

Industrial Applications

Packaging

Healthcare

Automotive

Construction

Key Regions and Countries

North America

The U.S.

Canada

Europe

Germany

France

The U.K.

Spain

Italy

Russia & CIS

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

ASEAN

Rest of Asia Pacific

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

GCC

South Africa

Rest of Middle East & Africa

Emerging Trends

The caprolactone market is witnessing steady demand from biodegradable polymers and specialty materials. Its use in polycaprolactone is increasing because the material offers flexibility, low toxicity, and suitability for controlled degradation. This trend is gaining importance in packaging, medical devices, and advanced material applications.

Another key trend is the rising use of caprolactone in coatings, adhesives, sealants, and polyurethane products. Manufacturers are focusing on materials that improve durability, elasticity, and performance under different operating conditions. Demand is also supported by growing interest in sustainable and high-value chemical intermediates.

Growth Factors

The growth of the caprolactone market can be attributed to its expanding use in industrial applications. Demand is increasing in thermoplastic polymers, resins, and performance coatings due to their need for strength, flexibility, and chemical resistance. These properties make caprolactone useful across automotive, construction, packaging, and manufacturing sectors.

Growth is also supported by rising demand from healthcare and biomedical applications. Caprolactone-based polymers are used in drug delivery systems, tissue engineering, sutures, and implantable materials due to their biodegradability and compatibility. Increasing investment in advanced healthcare materials and sustainable polymer development is expected to support market expansion.

Competetive Analysis

The Caprolactone market is moderately competitive, with a mix of large chemical producers, specialty chemical suppliers, and laboratory-grade chemical providers. Companies such as BASF SE, Daicel Corporation, Ingevity Corp., Perstorp Holding AB, and Merck KGaA hold a strong position due to their wider product portfolios, technical expertise, and established supply networks. These players focus on product quality, purity levels, and stable supply to serve demand from polycaprolactone, coatings, adhesives, elastomers, and specialty polymer applications.

Competition is mainly driven by pricing, product consistency, distribution reach, and the ability to meet customized industrial requirements. Companies such as Tokyo Chemical Industry, Thermo Fisher Scientific, Santa Cruz Biotechnology Inc., Otto Chemie Pvt. Ltd., and Hunan Juren Chemical Hitechnology Co. Ltd. support the market through research-grade chemicals, regional supply, and small to mid-volume demand. Other key players are also entering the market by focusing on cost-effective production and regional partnerships, which is expected to increase competition across Asia Pacific, Europe, and North America.

Recent Development

BASF SE, May 2026 - BASF SE introduced its ReducedPCF Elastollan TPU portfolio in Asia Pacific, supporting lower product carbon footprint needs in polymer and specialty material applications.

Ingevity Corp., February 2026 - Ingevity Corp. announced a temporary extraordinary surcharge on Capa caprolactone products, reflecting cost pressure and supply-side adjustment in its caprolactone portfolio.

Santa Cruz Biotechnology Inc., 2026 - Santa Cruz Biotechnology Inc. continued to expand its ChemCruz specialty biochemical portfolio, which includes a wide range of research chemicals used in laboratory and life science applications.

Thermo Fisher Scientific, February 2025 - Thermo Fisher Scientific agreed to acquire Solventum’s purification and filtration business for around USD 4.1 billion.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 353.55 Million |

Forecast Revenue (2035) | USD 638.0 Million |

CAGR (2025-2035) | 6.7% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2023 |

Forecast Period | 2026-2035 |

Report Coverage | AI impact analysis, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends |

Segments Covered | By Type (99.5% Purity, 99.9% Purity), By Application (Polycaprolactone (PCL), Acrylic Resin Modified, Polyesters Modified, Epoxy Resin Modified, Others), By End-Use Industry (Industrial Applications, Packaging, Healthcare, Automotive, Construction), By Regional Insights, Adoption Trends, Leading Companies |

Regional Analysis | Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; North America – US, Canada; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | BASF SE, Merck KGaA, Daicel Corporation, Ingevity Corp., Tokyo Chemical Industry, Santa Cruz Biotechnology Inc., Otto Chemie Pvt. Ltd., Hunan Juren Chemical Hitechnology Co. Ltd., Thermo Fisher Scientific, Perstorp Holding AB, Other Key Players |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

BASF SE

Merck KGaA

Ingevity Corp.

Santa Cruz Biotechnology Inc.

Thermo Fisher Scientific

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Sayali is a Research Analyst with expertise in market intelligence, industry assessment, competitive analysis, and data-driven research. Her work focuses on evaluating market dynamics, growth opportunities, demand patterns, regulatory developments, and strategic business trends across diverse industries. She specializes in market sizing, forecasting, segmentation analysis, regional evaluation, company profiling, and competitive benchmarking. Her analytical approach combines secondary research, industry validation, and structured data interpretation to deliver clear, reliable, and decision-focused insights.

Suraj is a Senior Management Consultant with over 7 years of experience in market research, business strategy, and consulting. He has worked with Fortune 500 companies and growing startups, helping them with market entry, cross-border expansion, demand analysis, competitive assessment, and growth planning. His analytical thinking and strong industry knowledge help clients make clear, confident, and informed business decisions.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Water and Wastewater Treatment Equipment Market to Exceed USD 136.6 Billion by 2035

Global Water and Wastewater Treatment Equipment Market Size By Application (Municipal, Industrial), By Process (Primary Treatment, Secondary Treatment, Tertiary Treatment), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Marine Composites Market to hit USD 15.7 Bn By 2035

Global Marine Composites Market Size By Composite Type (Polymer-Matrix Composites, Metal-Matrix Composites, Ceramic-Matrix Composites), By Resin Type (Epoxy, Polyester, Others), By Vessel Type (Sailboats, Cruise Ships & Yachts, Power Boats, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Black Pellets Market Revenue to Hit USD 722.1 Bn by 2035

Global Black Pellets Market Size, Share and Trends Analysis Report By Type (Torrefied Black Pellets, Hydrothermal Carbonized Pellets, Steam-Exploded Pellets), By Application (Heat Generation, Power Generation, Industrial Heating, Residential / Commercial Heating and Others), By Raw Material (Wood Biomass / Forest Residues, Agricultural Residues, Energy Crops and Others), By End-User (Utilities / Power Plants, Industrial Users, Commercial Heating Users, Residential Users), By Regional Insights, Adoption Trends, Leading Companies and Growth Forecasts By 2025-2035