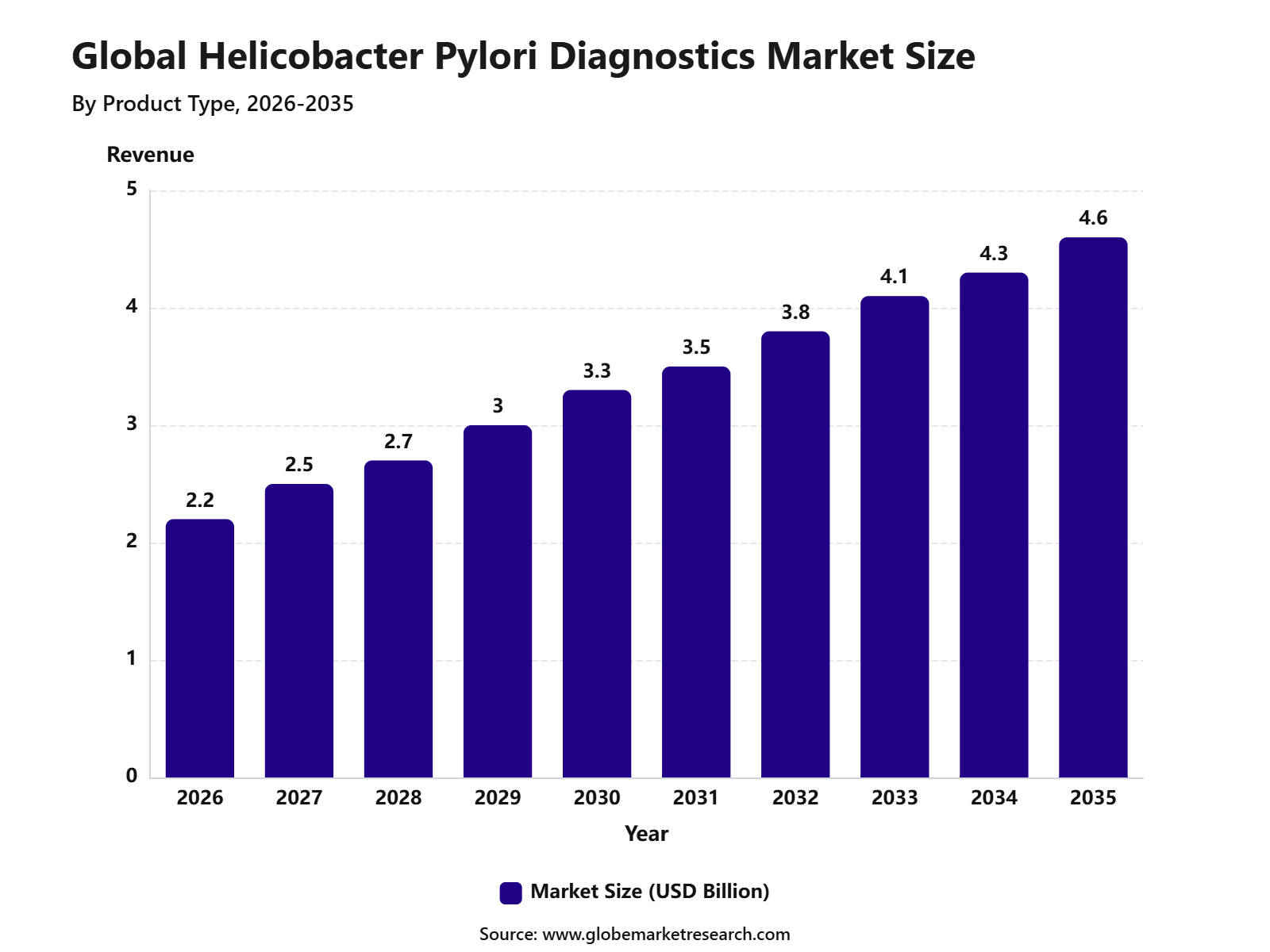

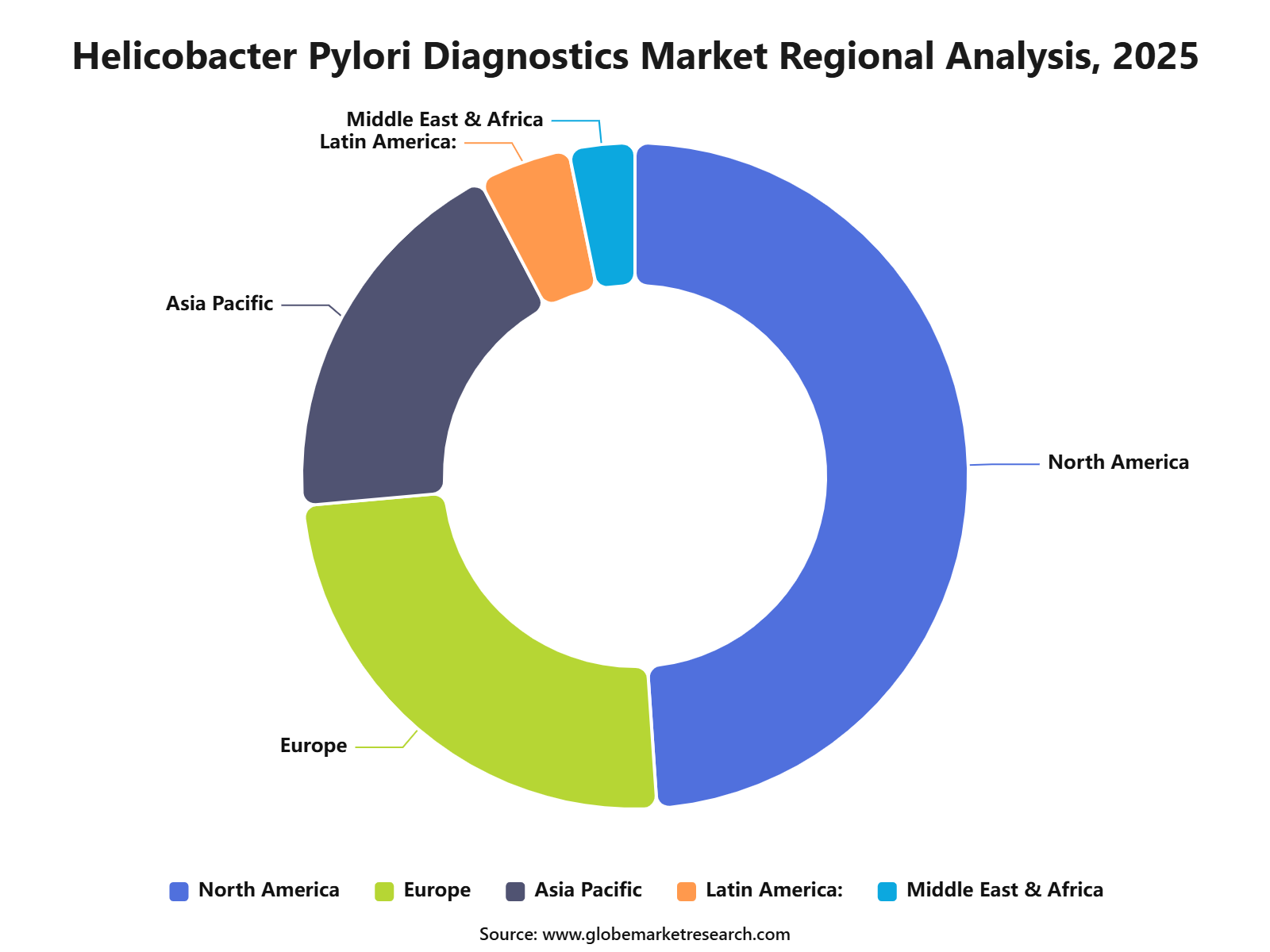

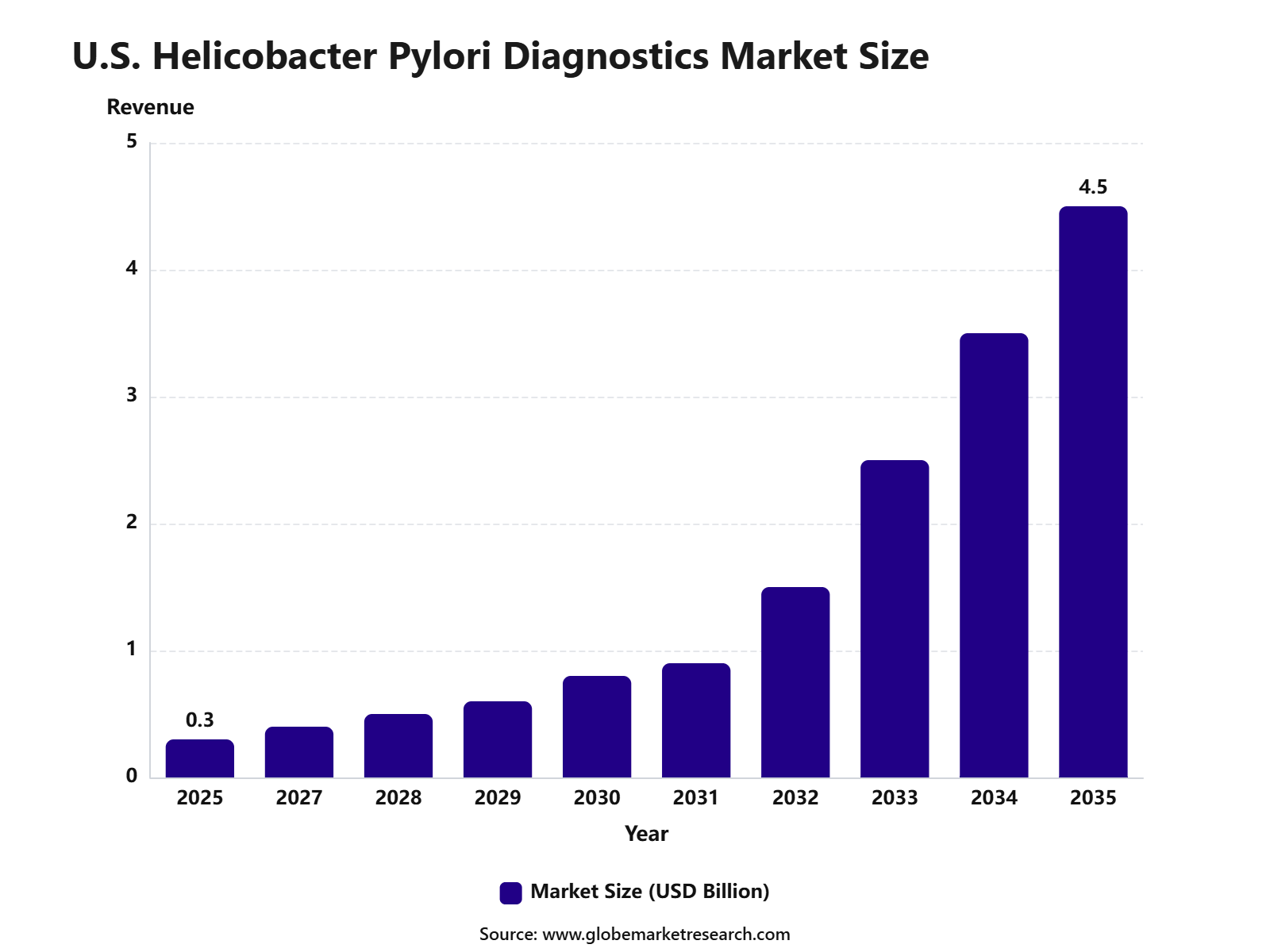

According to Globe Market Research, the Global Helicobacter Pylori Diagnostics Market is expected to increase from USD 2.2 billion in 2025 to USD 4.6 billion by 2035, reflecting a CAGR of 7.6% throughout the forecast period. North America led the market with a 48.9% share in 2025, supported by strong healthcare infrastructure, high diagnostic awareness, wide availability of advanced testing methods, and increasing screening for gastrointestinal infections. The U.S. Helicobacter Pylori Diagnostics Market was valued at USD 0.3 billion in 2025 and is expected to grow at a CAGR of 6.3%, driven by rising cases of gastritis, peptic ulcers, and stomach infection-related complications.

Helicobacter pylori diagnostics refers to tests used to detect H. pylori infection, a common bacterial infection linked to chronic gastritis, peptic ulcer disease, and increased risk of gastric cancer. The market growth can be attributed to rising awareness of early diagnosis, growing use of non-invasive testing methods, and increasing demand for accurate infection confirmation before treatment. Common diagnostic methods include urea breath tests, stool antigen tests, serology tests, rapid urease tests, histology, and molecular diagnostics.

The market outlook remains positive as healthcare providers continue to focus on early detection, treatment monitoring, and prevention of severe gastrointestinal disease. Demand is expected to rise for fast, accurate, and patient-friendly diagnostic solutions, especially non-invasive tests used in hospitals, diagnostic laboratories, and outpatient care settings. North America is expected to maintain a strong position due to advanced clinical testing capacity, higher healthcare spending, and strong adoption of evidence-based gastrointestinal disease management.

Market Key Takeaways

Reagents led the Helicobacter pylori diagnostics market with 57.3% share, supported by their broad use in rapid diagnostic kits, laboratory assays, and routine testing workflows.

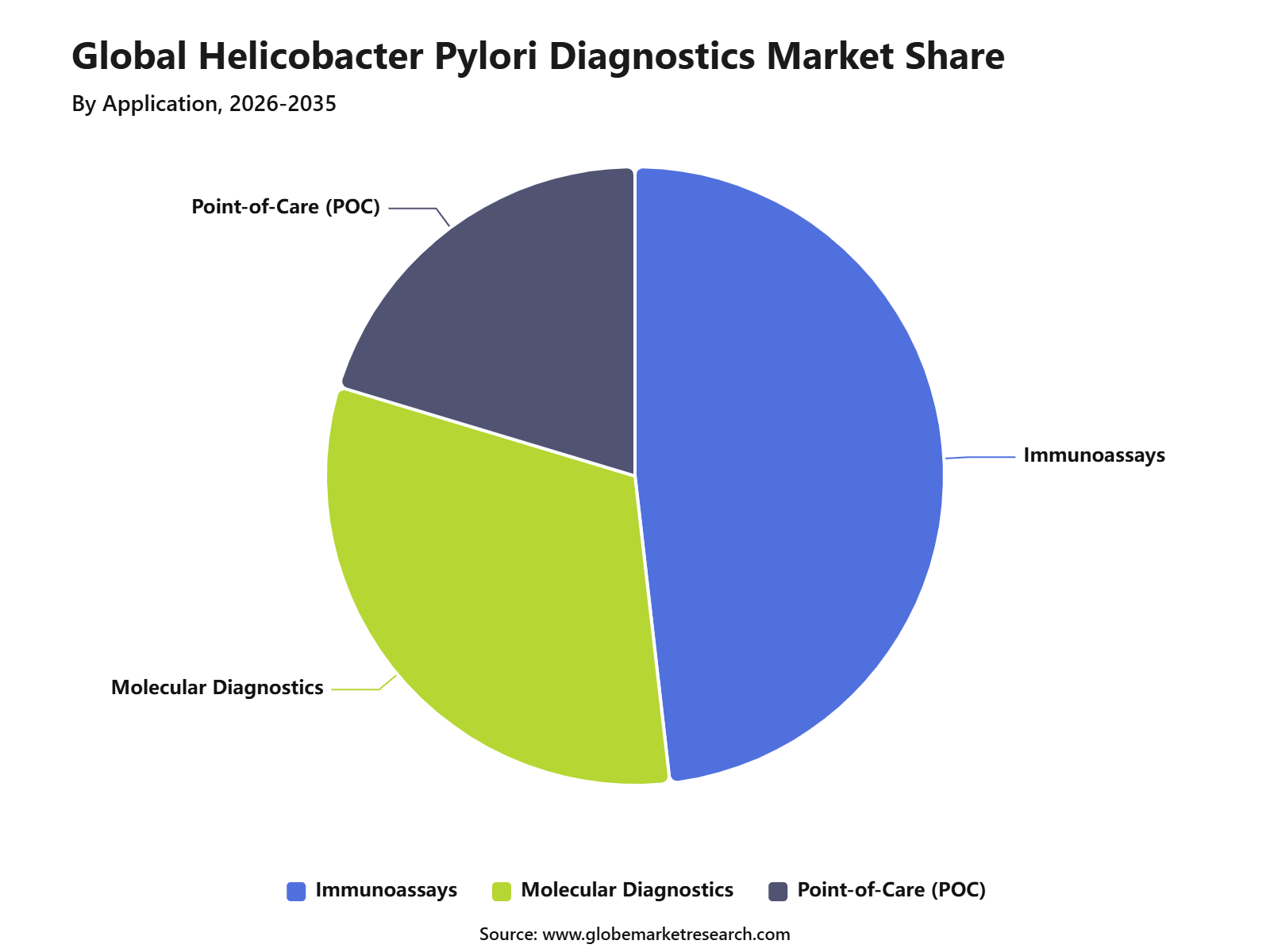

Immunoassays accounted for 48.1% share, driven by their strong accuracy, faster turnaround time, and suitability for high-volume screening across clinical settings.

Hospitals held 59.9% share, supported by high patient inflow, advanced laboratory infrastructure, and strong adoption of lab-based diagnostic testing.

North America led the market with 48.9% share, supported by strong healthcare access, higher testing awareness, and wider use of advanced diagnostic methods.

The U.S. Helicobacter pylori diagnostics market was valued at USD 0.3 billion and is projected to grow at a CAGR of 6.3%, supported by improved diagnosis, better patient screening, and growing focus on gastrointestinal disease management.

Urea Breath Test is one of the most widely used non-invasive tests for H. pylori detection. It offers strong diagnostic accuracy, with 96% to 100% sensitivity and 93% to 100% specificity for initial diagnosis, although performance may vary in patients with certain gastric conditions.

Rapid Urease Test is a biopsy-based diagnostic method that provides results within minutes. Its accuracy generally ranges from 74% to 98.9%, depending on biopsy quality, bacterial load, and testing conditions.

Histological staining is used to identify H. pylori in gastric tissue samples. Routine H&E staining offers fair sensitivity with around 75% specificity, while Giemsa staining can improve specificity to nearly 90% and immunohistochemistry may reach 100% specificity.

Serious complications occur in a smaller share of infected patients, but the clinical impact remains significant. Around 1% to 2% of infected individuals may develop gastric cancer, while the bacteria are linked to nearly 70% of gastric ulcers and around 80% of duodenal ulcers.

Treatment gaps continue to affect patient outcomes. Nearly 32% of newly diagnosed patients do not receive guideline-recommended eradication therapy, which increases the need for timely diagnosis, better follow-up, and stronger clinical management.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 2.2 Bn |

Forecast Revenue (2035) | USD 4.6 Bn |

CAGR (2025-2035) | 7.6% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Product Type Analysis

Reagents led the Helicobacter Pylori Diagnostics Market with 57.3% share, supported by their wide use in rapid tests, laboratory assays, stool antigen testing, serology-based testing, and routine diagnostic workflows. These products are essential because they support sample preparation, antigen detection, antibody detection, enzyme reactions, and result interpretation across different testing formats.

The growth of this segment can be attributed to the recurring nature of reagent consumption in diagnostic laboratories and hospitals. Unlike instruments, reagents are used repeatedly for each test, which creates steady demand from high-volume diagnostic centers and healthcare facilities.

Reagents are expected to remain the leading product type as testing volumes increase across primary care, hospitals, gastroenterology clinics, and laboratories. Demand will continue to be supported by the need for reliable, easy-to-use, and cost-effective diagnostic supplies for both initial detection and post-treatment confirmation.

Application Analysis

Immunoassays held a significant share of 48.1%, supported by their accuracy, faster turnaround, and suitability for large-scale screening. These tests are widely used to detect H. pylori antigens or antibodies and are valued for their practical use in clinical laboratories and diagnostic workflows.

The demand for immunoassays is being driven by their ability to support non-invasive testing, especially through stool antigen tests and serological formats. Mayo Clinic notes that stool antigen testing is a common method used to detect proteins linked with H. pylori infection, while published evidence has shown that stool antigen testing can provide strong diagnostic value in untreated patients.

Immunoassays are expected to remain important because they offer a balance of speed, scalability, and clinical utility. Their adoption is likely to remain strong in hospitals, diagnostic laboratories, and outpatient settings where fast screening and practical testing workflows are required.

End User Analysis

Hospitals dominated the Helicobacter Pylori Diagnostics Market with 59.9% share, supported by high patient inflow, advanced diagnostic facilities, and strong use of lab-based testing. Hospitals are often the first point of diagnosis for patients with gastric pain, ulcers, dyspepsia, anemia, gastrointestinal bleeding, and suspected infection-related complications.

The growth of this segment can be attributed to the availability of gastroenterology departments, endoscopy units, pathology laboratories, and specialist physicians. Hospitals can perform both non-invasive and invasive diagnostic methods, including stool antigen tests, urea breath tests, serology, biopsy-based tests, histology, and rapid urease testing.

Hospitals are expected to remain the leading end-user group because H. pylori testing is closely linked with digestive disease management and post-treatment follow-up. The segment is also supported by rising awareness of gastric cancer risk, stronger diagnostic access, and increasing use of evidence-based treatment confirmation.

Regional Analysis

North America led the Helicobacter Pylori Diagnostics Market with 48.9% share, supported by better healthcare access, high testing awareness, advanced diagnostic infrastructure, and strong adoption of modern testing methods. The region benefits from a large network of hospitals, clinical laboratories, gastroenterology practices, and insurance-supported diagnostic services.

Growth in North America is being supported by higher awareness of peptic ulcer disease, gastric cancer risk, antibiotic resistance concerns, and post-treatment confirmation needs. The American College of Gastroenterology emphasizes that eradication must be confirmed after treatment, which supports repeat testing and continued use of fecal antigen tests, urea breath tests, and biopsy-based methods.

North America is expected to remain a leading regional market as healthcare providers continue to focus on accurate diagnosis, treatment monitoring, and improved gastrointestinal care. Demand is likely to remain strong for rapid tests, immunoassays, stool antigen kits, urea breath testing systems, and laboratory-based diagnostic solutions.

U.S. Market Outlook

The U.S. Helicobacter Pylori Diagnostics Market was valued at USD 0.3 billion and is projected to grow at a 6.3% CAGR. Growth is supported by better healthcare access, high testing awareness, strong use of diagnostic laboratories, and wider adoption of guideline-based testing practices.

The U.S. market is also supported by demand for accurate diagnosis among patients with ulcers, gastritis, dyspepsia, and gastric cancer risk factors. Testing is increasingly important because H. pylori management requires not only detection but also confirmation that the infection has been cleared after treatment.

Opportunities in the U.S. market are expected to remain strong across stool antigen testing, urea breath testing, immunoassays, molecular tests, and biopsy-based diagnostics. Companies offering accurate, easy-to-use, fast, and cost-effective testing solutions are likely to benefit from continued clinical demand.

Competitive Landscape Assessment

The Helicobacter Pylori Diagnostics Market is shaped by the rising use of non-invasive testing, higher awareness of gastric disorders, and the need to confirm bacterial eradication after treatment. Competition is mainly focused on test accuracy, ease of use, time to result, sample flexibility, regulatory clearance, and compatibility with hospital or laboratory workflows. Urea breath tests and stool antigen tests remain widely used because they help detect active infection and support post-treatment confirmation without the need for endoscopy.

Large diagnostic companies compete through broad infectious disease portfolios, automated immunoassay platforms, and strong hospital laboratory relationships. Mid-sized and specialized players are active in rapid stool antigen tests, ELISA kits, breath testing systems, and molecular assays. The competitive field is not limited to one technology, as hospitals, reference labs, gastroenterology clinics, and point-of-care settings often use different testing methods based on patient condition, cost, infrastructure, and clinical need.

Product differentiation is becoming stronger as healthcare providers look for tests that can support faster diagnosis and better treatment decisions. Stool antigen tests are valued for convenience and suitability for current infection detection, while urea breath tests are preferred where breath analyzers and trained staff are available. Molecular testing is gaining attention because antibiotic resistance, especially clarithromycin resistance, is becoming an important factor in treatment planning.

The market also shows strong competition between centralized laboratory testing and decentralized rapid testing. Centralized labs benefit from automation, higher throughput, and quality control, while rapid tests support quicker clinical decisions in smaller facilities. Companies with both instrument-based and kit-based solutions are better positioned because they can serve hospitals, diagnostic laboratories, outpatient clinics, and regional healthcare networks.

Implementation Complexity & Technology Readiness

Diagnostic Technology | Implementation Complexity | Technology Readiness | Market Position |

|---|---|---|---|

Stool antigen rapid tests | Low to Moderate | High | Strong for outpatient and POC use. |

Stool antigen ELISA tests | Moderate | High | Suitable for lab batch testing. |

Urea breath tests | Moderate | High | Established but analyzer-dependent. |

Serology and antibody tests | Low | High | Easy and low-cost, but limited for active infection. |

Endoscopy-based biopsy testing | High | High | Used when endoscopy is required. |

Immunohistochemistry testing | High | High | Supports biopsy confirmation. |

PCR and molecular resistance testing | High | Moderate to High | Useful for resistance detection. |

Key Players in the Helicobacter Pylori Diagnostics Market

Company | Competitive Focus |

|---|---|

Meridian Bioscience | Urea breath systems and stool antigen tests for active detection and monitoring. |

TECHLAB, Inc. | Stool antigen ELISA and rapid immunoassay tests for non-invasive detection. |

Abbott | Rapid antigen and antibody tests for selected point-of-care markets. |

QuidelOrtho Corporation | Rapid stool antigen immunoassays for diagnosis and post-treatment detection. |

bioMérieux | Automated H. pylori antibody detection through VIDAS platforms. |

DiaSorin S.p.A. | LIAISON-based stool antigen and antibody diagnostic solutions. |

Thermo Fisher Scientific | Stool antigen lateral flow and ELISA tests for laboratory use. |

FUJIFILM Wako Pure Chemical Corporation | Latex immunoassay antibody testing for automated clinical workflows. |

CerTest Biotec | Real-time PCR testing for H. pylori and clarithromycin resistance. |

Roche Diagnostics | Biopsy-based immunohistochemistry for gastric tissue detection. |

Siemens Healthineers | H. pylori IgG assays within infectious disease immunoassay menus. |

SEKISUI Diagnostics | OSOM antibody testing for rapid qualitative detection. |

Key Players List

Meridian Bioscience, TECHLAB, Inc., Abbott, QuidelOrtho Corporation, bioMérieux, DiaSorin S.p.A., Thermo Fisher Scientific, FUJIFILM Wako Pure Chemical Corporation, CerTest Biotec, Roche Diagnostics, Siemens Healthineers, SEKISUI Diagnostics.

Strategic Outlook

The Helicobacter Pylori Diagnostics Market is expected to remain highly dependent on non-invasive testing, laboratory automation, and post-treatment confirmation needs. Stool antigen and urea breath tests are likely to maintain strong adoption because they support active infection detection and reduce dependence on invasive procedures. Companies that offer accurate, easy-to-use, and workflow-friendly products are expected to hold a stronger position across hospitals, diagnostic labs, and outpatient care settings.

Technology readiness is already high for stool antigen tests, urea breath tests, serology, and biopsy-based testing. The next area of differentiation is expected to come from molecular diagnostics, especially tests that identify antibiotic resistance markers. As treatment decisions become more guided by resistance patterns, suppliers with PCR capability, validated workflows, and strong clinical evidence may gain a larger role in advanced diagnostic settings.

Recent Developments

January 2026, Medical policy updates in 2026 continued to identify urea breath tests and stool antigen tests as important non-invasive methods for detecting active H. pylori infection and confirming eradication. This supports market growth because serology is less useful for post-treatment confirmation, while active-infection tests are better aligned with clinical decision-making. Stool antigen testing is also used for both initial diagnosis and post-treatment testing, which increases test volume across hospitals, clinics, and reference laboratories.

January 2026, Cepheid received FDA clearance for its Xpert GI Panel, a multiplex PCR test for 11 clinically relevant gastrointestinal pathogens. The panel is not positioned as an H. pylori test, but it is important for the broader gastrointestinal diagnostics market because it shows continued movement toward automated, sample-to-answer PCR systems in digestive disease testing. This trend may support future demand for molecular H. pylori testing, especially where resistance markers and faster lab workflows are required.

March 2026, The International Agency for Research on Cancer, part of WHO, published guidance on population-based H. pylori screen-and-treat strategies for gastric cancer prevention. The guidance covers screening methods, treatment regimens, antibiotic stewardship, quality measures, equity, and cost-benefit considerations. This is a major demand signal for diagnostics because organized screen-and-treat programs require reliable, scalable, and affordable testing platforms.

Key Market Segments

By Product Type

Instruments

Services

Reagents

By Application

Immunoassays

Molecular Diagnostics

Point-of-Care (POC)

By End User

Hospitals

Diagnostic Laboratories

Clinics

By Regional

North America

Europe

Asia Pacific

Latin America

Middle East and Africa