Market Size and Growth Forecast

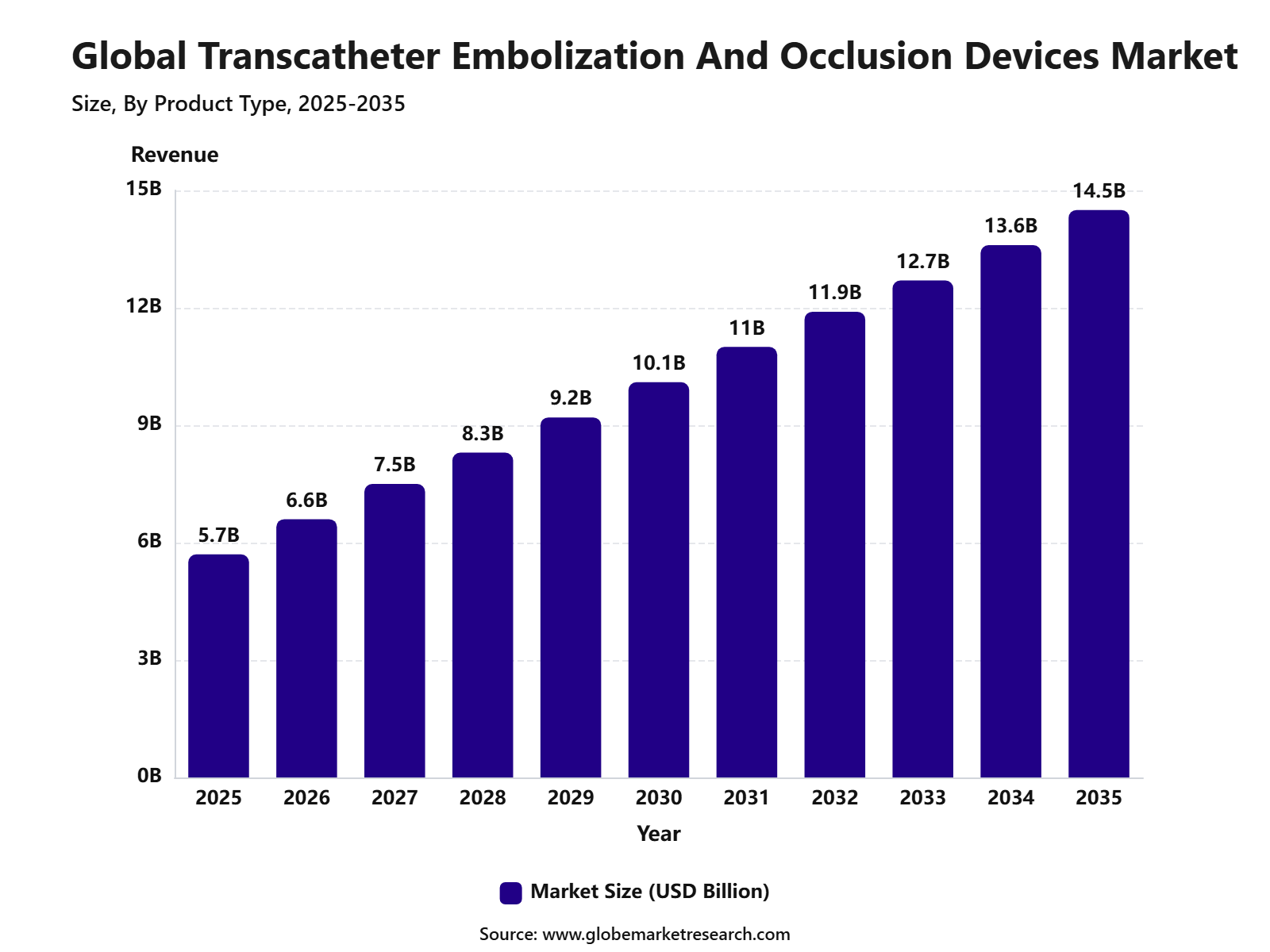

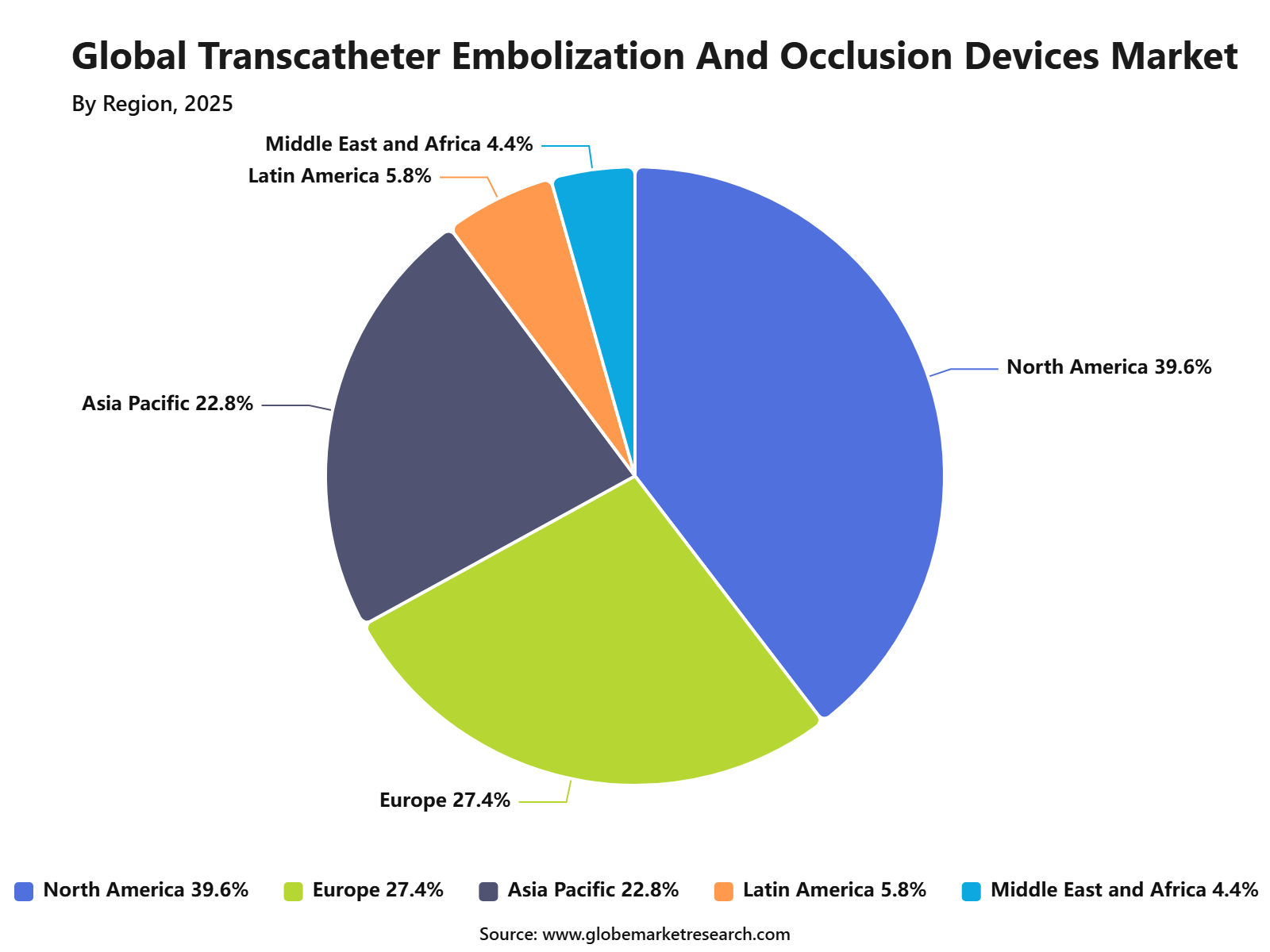

According to Globe Market Research, the global transcatheter embolization and occlusion devices market reached USD 5.7 billion in 2025 and is expected to grow to USD 14.5 billion by 2035, registering a 9.8% CAGR. North America accounted for 39.6% share in 2025, supported by advanced hospitals, strong interventional radiology adoption, high use of minimally invasive vascular procedures, and better access to innovative embolization technologies.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 5.7 Billion |

Projected Revenue, 2035 | USD 14.5 Billion |

CAGR, 2025-2035 | 9.8% |

Largest Region | North America, 38.0% Share |

U.S. Market Revenue, 2025 | USD 1.8 Billion |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

Transcatheter embolization and occlusion devices are used to block, reduce, or redirect blood flow in selected blood vessels. These devices are used in aneurysms, arteriovenous malformations, tumors, hemorrhage, uterine fibroids, varicoceles, and other vascular conditions. Key products include embolization coils, flow diversion devices, liquid embolic agents, embolic particles, detachable balloons, vascular plugs, and microspheres.

The market is becoming more important because hospitals are moving toward image-guided, catheter-based treatment methods that can reduce surgical trauma and shorten recovery time. Demand is being supported by stroke burden, brain aneurysm diagnosis, cancer-related embolization, uterine fibroid embolization, trauma-related bleeding control, and improved embolic materials.

Why is Transcatheter Embolization and Occlusion Devices Market Growing?

The growth of the transcatheter embolization and occlusion devices market can be attributed to the rising preference for minimally invasive procedures. This factor has an estimated positive CAGR impact of +1.2%, especially across North America, Europe, and Asia Pacific. Hospitals are adopting catheter-based procedures because they can support targeted therapy, shorter hospital stays, and lower procedural burden compared with some open surgical approaches.

The disease burden is also large. In the U.S., more than 795,000 people have a stroke every year, and someone has a stroke every 40 seconds. Globally, stroke remains one of the major causes of death and disability, with 11.9 million new stroke cases in 2021 and a lifetime risk of 1 in 4 adults. This supports the need for advanced neurovascular intervention tools and emergency vascular care systems.

Cancer-related embolization is another growth factor. The latest global cancer estimates show nearly 20 million new cancer cases and 9.7 million cancer-related deaths in 2022, with annual new cancer cases expected to rise by 2050. Embolization is used in selected oncology procedures to restrict tumor blood supply, support local therapy, or manage bleeding complications, which strengthens demand for advanced interventional devices.

Embolization Coils Remain the Leading Product Type

Embolization coils led the market with 33.7% share in 2025. Their leadership is supported by wide use in aneurysm treatment, vascular occlusion, hemorrhage control, and neurovascular procedures. Coils are preferred because they allow controlled placement and can be used in complex vessels where accurate blood flow blockage is required.

The demand for embolization coils is also supported by increasing diagnosis of aneurysms and vascular malformations. Aneurysms represented the largest indication segment with 29.8% share, showing that coil-based and related occlusion procedures remain central to minimally invasive aneurysm management.

Product improvements are strengthening this segment further. Better coil design, improved radiopacity, detachable systems, shape control, and compatibility with microcatheters are helping physicians perform procedures with higher precision. Technological improvements in coils, plugs, and embolic agents have an estimated positive CAGR impact of +0.8%.

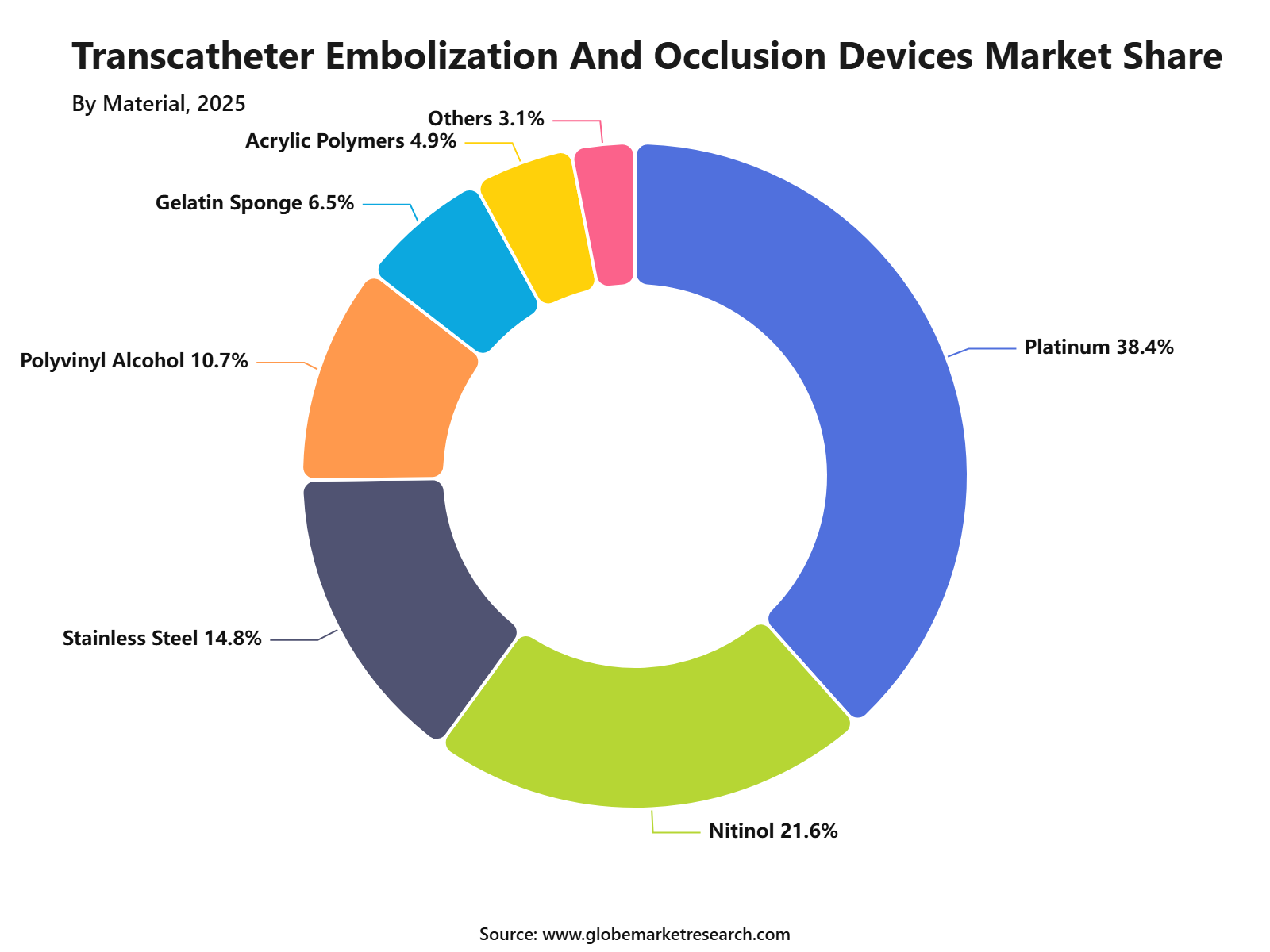

Platinum Is the Leading Material Segment

Platinum accounted for the largest material share at 38.4% in 2025. Its use is supported by flexibility, biocompatibility, long-term stability, and strong visibility during image-guided procedures. These properties make platinum important in embolization coils and other devices where accurate deployment is critical.

Radiopacity is a major advantage of platinum-based devices. During fluoroscopy-guided procedures, physicians need to clearly see the device position before final deployment. This makes platinum highly relevant in neurovascular, peripheral vascular, and complex embolization procedures.

The material segment is also linked with supply chain risk. Platinum, nitinol, polymers, catheter components, and sterile packaging are exposed to global sourcing and pricing pressure. Supply chain pressure for metals and polymers has an estimated negative impact of -0.5%, showing that material planning is important for device manufacturers.

Neurology Is the Leading Application Area

Neurology emerged as the leading application segment with 31.2% share in 2025. The segment is supported by the growing use of embolization devices in brain aneurysms, arteriovenous malformations, and other neurovascular conditions.

The opportunity in neurovascular embolization is strong because these procedures are highly specialized and require advanced devices, imaging systems, and trained interventional teams. Rising demand for neurovascular embolization has an estimated positive CAGR impact of +1.1%, especially in the U.S., Europe, Japan, and China.

Recent device approvals are also supporting this application area. In 2026, the FDA approved Balt’s SQUID Liquid Embolic Agent for embolization of the middle meningeal artery as an adjunct to usual care in selected patients with symptomatic chronic subdural hematoma. This shows that embolization technologies are moving into newer neurovascular treatment areas.

Aneurysms Remain the Leading Indication

Aneurysms held the largest indication share at 29.8% in 2025. The segment is supported by increasing diagnosis of cerebral and peripheral aneurysms, wider availability of neurovascular centers, and rising preference for catheter-based treatment options.

The growing burden of aneurysms and vascular disorders has an estimated CAGR impact of +1.0%. This indicates that demand is being shaped not only by procedure growth but also by wider disease detection through imaging and specialist referral pathways.

Aneurysm treatment remains clinically sensitive because device performance, placement accuracy, and long-term occlusion are critical. This creates demand for proven embolization coils, flow diverters, liquid embolics, and delivery systems that can support safer outcomes in complex vascular anatomy.

Hospitals Dominate End-User Demand

Hospitals accounted for 61.5% share of the transcatheter embolization and occlusion devices market in 2025. Hospitals lead because most procedures require catheterization laboratories, advanced imaging systems, trained interventional radiologists, neurointervention specialists, vascular surgeons, anesthetic support, and emergency care capability.

Hospital purchasing is highly evidence-based. Device selection is influenced by physician preference, clinical outcomes, safety profile, reimbursement, training support, and product availability. This makes hospital partnerships, specialist education, and procedural support important parts of commercial strategy.

Ambulatory surgical centers and specialty clinics may gain share over time, especially for selected lower-risk procedures. However, high-complexity neurovascular, oncology, hemorrhage, and emergency interventions are expected to remain concentrated in hospitals.

North America Leads the Market

North America held the leading regional share of 39.6% in 2025. The region benefits from advanced healthcare infrastructure, high adoption of minimally invasive procedures, strong reimbursement access, and early use of innovative embolization technologies.

The U.S. market was valued at approximately USD 1.8 billion in 2025 and is projected to grow at a 9.6% CAGR from 2025 to 2035. Growth is being supported by advanced hospitals, wider use of interventional radiology, increasing cases of cancer, aneurysms, trauma-related bleeding, vascular malformations, and uterine fibroids.

Asia Pacific is also becoming an important opportunity area. Hospital modernization in China, India, Brazil, and Saudi Arabia has an estimated positive CAGR impact of +0.6%, while expansion of interventional radiology infrastructure has an estimated impact of +0.7% across Asia Pacific, the Middle East, and Latin America.

Analyst Perspective

What the Data Is Telling Transcatheter Embolization and Occlusion Devices Market Companies?

From an analyst perspective, the data shows that the market is shifting toward high-value, specialist-led, minimally invasive care. A market value of USD 5.7 billion in 2025 and a projected value of USD 14.5 billion by 2035 indicate strong long-term demand, but growth will favor companies with proven clinical performance and deep hospital relationships.

The strongest signal is the leadership of embolization coils, neurology, aneurysms, hospitals, and North America. Embolization coils held 33.7% share, neurology accounted for 31.2%, aneurysms represented 29.8%, hospitals held 61.5%, and North America captured 39.6%. This shows that complex hospital-based procedures remain the center of demand.

What Opportunities Are Emerging?

The biggest opportunity is in neurovascular embolization. New indications, advanced liquid embolics, better flow diversion systems, and high-value aneurysm treatment are expected to support strong product differentiation. Oncology and uterine fibroid embolization also offer growth potential.

Cancer burden remains high globally, and uterine fibroids affect a large share of women of reproductive age, creating demand for targeted, minimally invasive procedures. Emerging markets are also becoming more attractive as hospitals invest in interventional radiology infrastructure. Companies that support training, device availability, and local clinical education can improve adoption outside mature markets.

What Risks Should Companies Be Aware Of?

The biggest risk is adoption friction caused by cost, reimbursement gaps, and specialist shortages. Advanced embolization devices can be expensive, and procedure growth may remain limited in hospitals without trained interventional teams. Regulatory and clinical evidence pressure is another major risk.

New products and new indications require strong safety data, quality systems, and post-market monitoring. Any device failure can quickly affect hospital confidence. Supply chain pressure should also be watched carefully. Platinum, nitinol, polymers, microcatheters, and sterile packaging require stable sourcing. Material cost changes and logistics delays can reduce margins and affect hospital supply reliability.

What Decisions Should Clients Make Next?

Clients should first decide which clinical segment they want to prioritize: neurovascular care, oncology embolization, uterine fibroid embolization, trauma bleeding control, or peripheral vascular occlusion. Each segment has different buyers, training needs, clinical evidence requirements, and reimbursement pathways.

Second, companies should invest in physician education and hospital partnerships. Device adoption is stronger when physicians are confident in handling, visualization, deployment control, and patient outcomes.

Finally, clients should strengthen supply chain resilience and regulatory readiness. Dual sourcing, clinical evidence planning, quality documentation, and post-market surveillance should be treated as growth enablers, not only compliance requirements.

Competitive Landscape

The market is competitive, with established medical device companies and specialist neurovascular firms competing through product innovation, clinical evidence, physician training, partnerships, and geographic expansion. Key companies include Medtronic plc, Boston Scientific Corporation, Terumo Corporation, MicroVention, Inc., Stryker Corporation, Cook Medical LLC, Penumbra, Inc., Abbott Laboratories, Johnson & Johnson MedTech, Cerenovus, Merit Medical Systems, W. L. Gore & Associates, B. Braun, Kaneka Corporation, Balt Group, Shape Memory Medical, Acandis, Wallaby Medical, Spartan Micro, ArtVentive Medical Group, and Zylox-Tonbridge Medical Technology.

Competition is expected to increase in embolization coils, liquid embolic agents, vascular plugs, flow diversion devices, and microspheres. Companies with strong physician trust, proven safety, advanced delivery systems, and global regulatory capability are likely to remain better positioned. Smaller innovators may gain opportunities in specialized materials, bioactive embolics, shape-memory platforms, and image-guided embolization systems. However, market entry will require strong evidence, reliable manufacturing, and hospital acceptance.

Recent Developments

Market News

In 2026, Medtronic Neurovascular received FDA approval for a reduced shake time for Onyx 18 and Onyx 34 Liquid Embolic System products. The approved preparation time was reduced to at least 1 minute from the earlier 20-minute shake time, supporting faster procedure readiness for embolization use cases.

In 2026, Boston Scientific received FDA clearance for the “Any Day Dosing” feature on its TheraSphere 360 Y-90 management platform. The update improves scheduling flexibility for TheraSphere Y-90 glass microspheres used in liver cancer radioembolization workflows.

In 2026, ABK Biomedical completed patient enrollment in the ROUTE90 pivotal study for Eye90 microspheres. The study is evaluating a Y-90 transarterial radioembolization device for hepatocellular carcinoma under an FDA investigational device exemption.

In 2026, Instylla initiated the commercial launch of its Embrace Hydrogel Embolic System following first commercial use. The launch is important because Embrace is positioned as a liquid embolic approved for hypervascular tumor embolization.

Funding

In 2025, ABK Biomedical raised USD 35.1 million in Series D financing. The funding is being used to support clinical operations, commercialization preparation for Eye90 microspheres, and scale-up of manufacturing and supply chain operations.

In 2025, Polyembo closed a new funding round led by a multinational strategic investor. The capital will be used to advance regulatory clearances and product development for vascular embolic technologies such as Scrunchy, Sphere, and PuffyCoil.

Mergers and Acquisitions

In 2026, Boston Scientific agreed to acquire Penumbra in a cash-and-stock transaction valued at about USD 14.5 billion. The deal gives Boston Scientific access to Penumbra’s portfolio for stroke, pulmonary embolism, deep vein thrombosis, acute limb ischemia, heart attack, and aneurysm treatment.

In 2025, Argon Medical acquired certain assets of Accurate Medical Therapeutics from Guerbet, including SeQure and DraKon microcatheters. These microcatheters are used in interventional procedures where therapeutic agents or devices are delivered into small vessels feeding tumors or abnormalities.

In 2025, Balt acquired its Canadian distributor Yocan Medical Systems, which now operates as Balt Canada. The move strengthens Balt’s direct presence in Canada and supports wider commercialization of neurovascular products such as stents, coils, and catheters.

Conclusion

The transcatheter embolization and occlusion devices market is entering a stronger growth phase driven by minimally invasive treatment, neurovascular intervention, aneurysm care, oncology embolization, uterine fibroid embolization, and hospital-based image-guided procedures. Growth is supported by a large disease burden, technology improvements, and expanding interventional radiology infrastructure.

Future growth will be led by embolization coils, liquid embolic agents, flow diversion devices, vascular plugs, platinum-based devices, neurovascular procedures, and hospital adoption. Companies that combine clinical evidence, physician training, product reliability, and supply chain strength will be better positioned in this market.