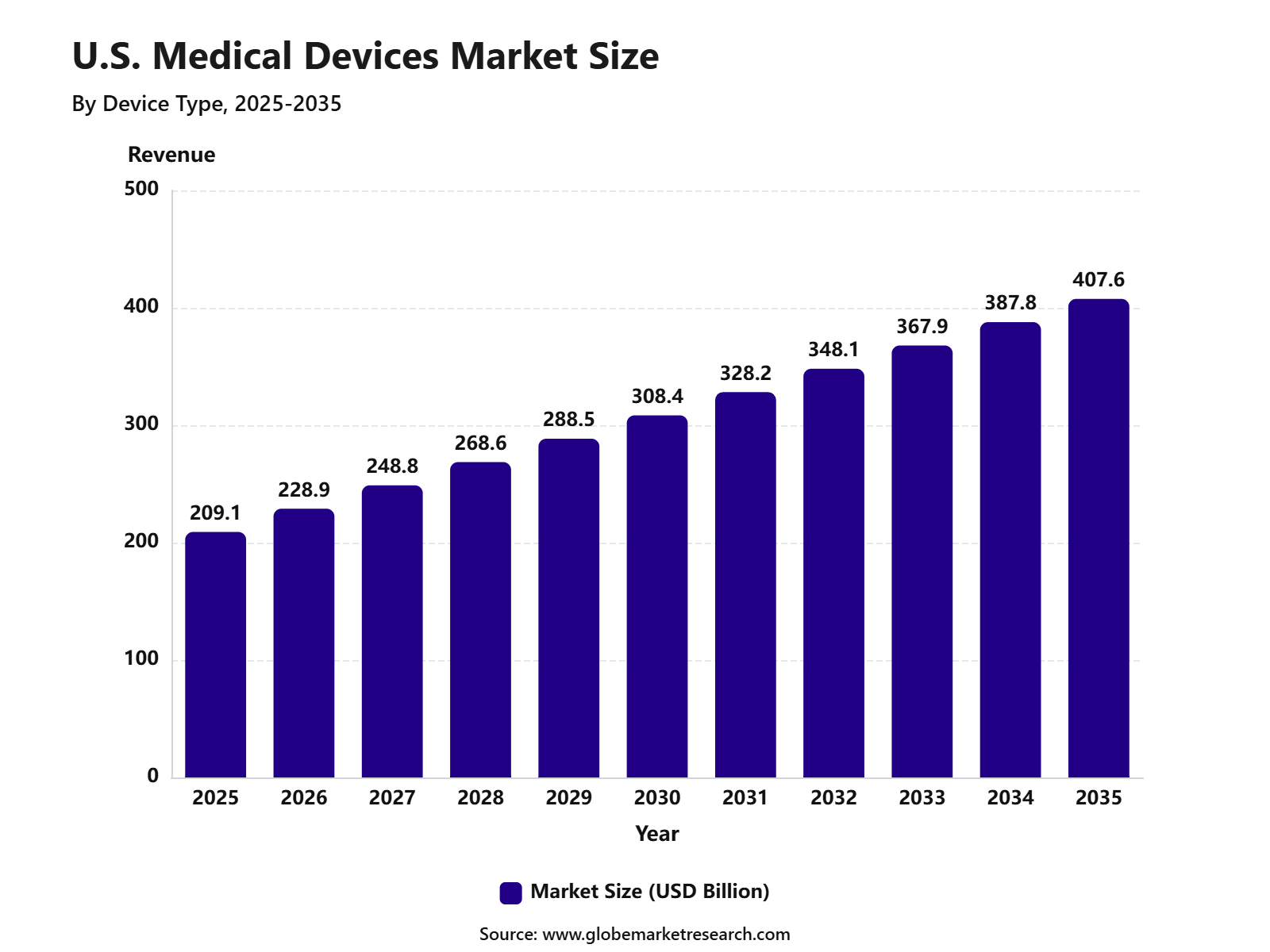

Globe Market Research has released a data-driven report focused on the U.S. Medical Devices Market was worth USD 209.1 billion in 2025 and is expected to reach USD 407.6 billion by 2035, growing at a CAGR of 6.9% from 2025 to 2035. The market growth is supported by advanced healthcare infrastructure, high healthcare spending, strong medical technology adoption, and rising demand for diagnostic, surgical, monitoring, and therapeutic devices.

The U.S. Medical Devices Market includes a wide range of products used for diagnosis, treatment, monitoring, prevention, and patient care. These devices include diagnostic imaging systems, surgical instruments, orthopedic implants, cardiovascular devices, patient monitoring systems, diabetes care devices, dental equipment, wound care products, and wearable medical technologies. The market is closely linked with hospitals, ambulatory surgical centers, specialty clinics, home healthcare providers, and digital health platforms.

The market outlook remains strong as healthcare providers continue to adopt advanced, minimally invasive, and connected medical technologies. Growth can be attributed to the rising aging population, increasing chronic disease burden, higher surgical procedure volumes, and wider use of remote patient monitoring and AI-enabled diagnostic tools. The expansion of home-based care, robotic-assisted surgery, and personalized treatment solutions is expected to support long-term market demand.

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 209.1 Billion |

Forecast Revenue (2035) | USD 407.6 Billion |

CAGR (2025-2035) | 6.9% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Key Market Insights

In vitro diagnostics led the device type segment with 19.9% share. Growth was supported by strong demand for lab testing, disease screening, and point-of-care diagnostics.

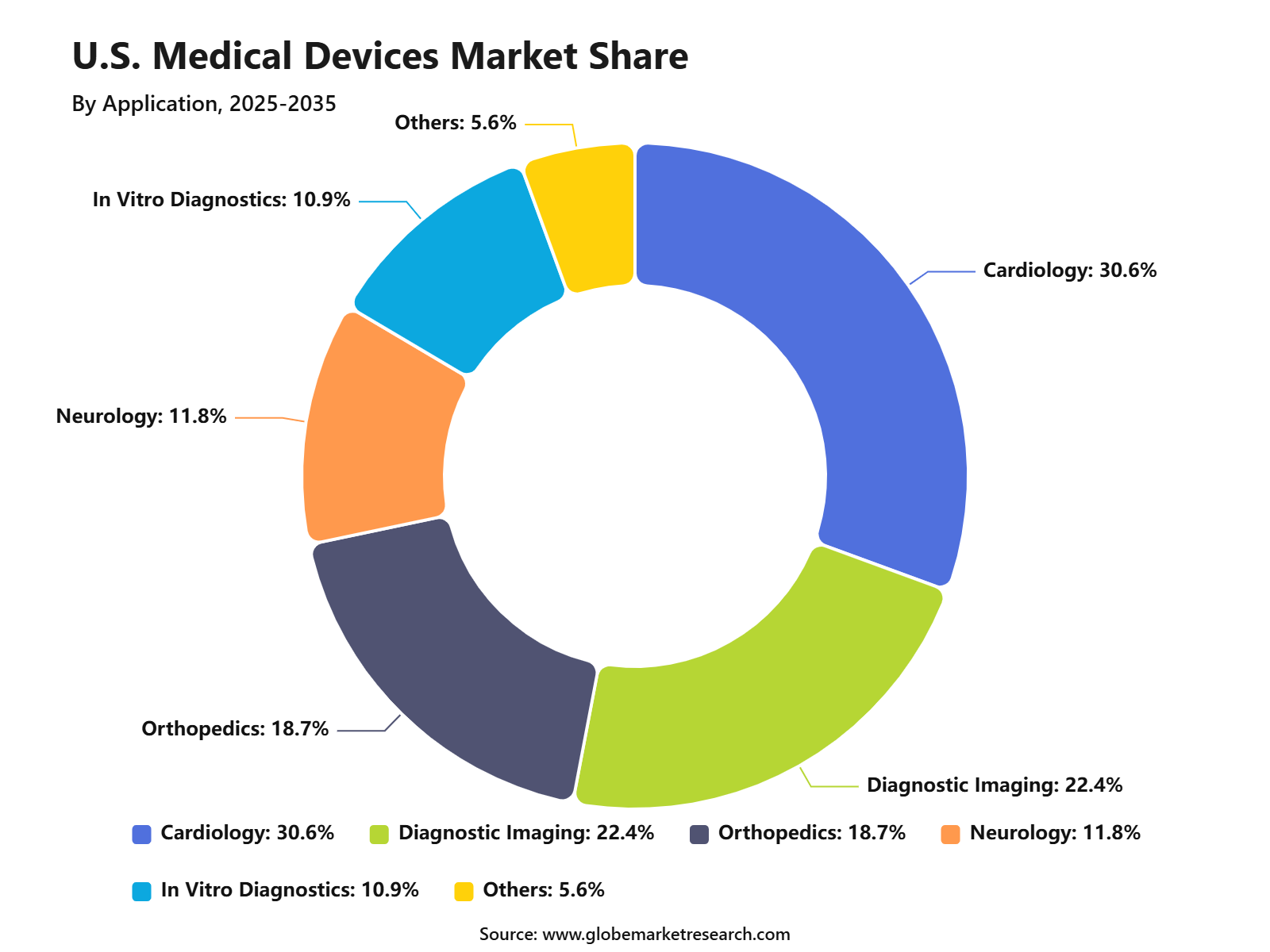

Cardiology held 30.6% share by application. This was driven by rising heart disease cases and higher use of monitoring and treatment devices.

Hospitals and clinics accounted for 56.4% share by end user. Their lead was supported by high patient volume and advanced medical infrastructure.

Conventional devices dominated the technology segment with 68.8% share. This was due to strong clinical acceptance, easier approval pathways, and reliable use in healthcare settings.

Device Type Insights

In vitro diagnostics led the device type segment with 19.9% share, supported by strong demand for laboratory testing, disease screening, point-of-care diagnostics, and routine clinical decision-making. Diagnostic tests are used across hospitals, outpatient centers, physician offices, reference laboratories, and home-based care pathways. Their role is important because diagnosis often comes before treatment, medication selection, surgical planning, and long-term disease monitoring.

The segment is supported by the large scale of clinical testing in the U.S. healthcare system. The CDC states that around 14 billion laboratory tests are performed each year in more than 266,000 CLIA-certified laboratories across the United States. These tests support care decisions for chronic diseases, infections, cancer, kidney disorders, heart conditions, thyroid disease, and diabetes.

Regulatory activity has also kept in vitro diagnostics in focus. The FDA noted that its laboratory developed test rule was vacated by a federal district court on March 2025, and the agency issued a final rule on September 2025, reverting the regulation text to its earlier form. This shows that IVD regulation remains active and closely watched by laboratories, device makers, healthcare providers, and payers.

By Application Insights

Cardiology accounted for 30.6% share by application, driven by the high burden of heart-related conditions and the continued use of monitoring, imaging, diagnostic, and therapeutic devices. Demand is supported by regular use of ECG systems, cardiac monitors, implantable devices, catheters, stents, defibrillators, and diagnostic testing tools. These devices are used across emergency care, hospitals, outpatient cardiology clinics, surgical centers, and long-term patient monitoring.

The clinical need remains strong because cardiovascular disease continues to be one of the largest health burdens in the United States. The CDC states that one person dies every 34 seconds from cardiovascular disease, and 919,032 people died from cardiovascular disease in 2023, equal to about 1 in 3 deaths. This disease burden supports high procedure volumes and sustained demand for cardiology-focused medical devices.

Cardiology device demand is also supported by recurring care needs. The CDC reports that about 805,000 people in the U.S. have a heart attack each year, including 605,000 first-time heart attacks and 200,000 repeat heart attacks. These figures show why cardiac diagnosis, acute intervention, rhythm management, and post-event monitoring remain central parts of the U.S. medical device landscape.

By End User Insights

Hospitals and clinics held 56.4% share by end user, supported by high patient volume, advanced care infrastructure, and wide use of diagnostic, surgical, therapeutic, and monitoring devices. These facilities require large installed bases of medical equipment, from imaging and laboratory systems to patient monitors, surgical instruments, infusion systems, and emergency care devices. Their purchasing demand is also supported by strict quality, safety, and workflow requirements.

The U.S. hospital base remains large and equipment-intensive. The American Hospital Association’s 2026 hospital statistics list 6,100 hospitals in the United States, including 5,121 community hospitals. The same source reports 907,216 staffed beds across all U.S. hospitals, which reflects the scale of infrastructure that depends on medical devices for diagnosis, treatment, patient monitoring, and care delivery.

Patient flow further supports this end-user segment. The AHA reported 35,658,583 total admissions across all U.S. hospitals and 33,553,725 admissions in community hospitals in its 2026 hospital statistics. This level of clinical activity keeps hospitals and clinics as the primary purchasing and utilization centers for medical devices in the U.S. market.

By Technology Insights

Conventional devices dominated the technology segment with 68.8% share, driven by broad clinical acceptance, established use protocols, lower implementation complexity, and reliable performance across healthcare settings. These devices include widely used diagnostic, surgical, monitoring, implantable, and therapeutic products that are already integrated into hospital and clinic workflows. Their continued dominance reflects trust, physician familiarity, service availability, and compatibility with existing infrastructure.

Regulatory familiarity also supports conventional device adoption. The FDA’s CDRH Portal states that all 510(k) submissions, unless exempted, must be submitted electronically using eSTAR, while all De Novo submissions became subject to eSTAR submission requirements as of October 2025. This structured pathway supports review consistency and gives manufacturers a clearer process for bringing many device categories to market.

At the same time, conventional devices remain important even as digital and AI-enabled technologies expand. The FDA’s eSTAR program was updated in 2026 and is designed to guide applicants through comprehensive medical device submissions, including both non-IVD and IVD devices. This reflects a market where new technology is advancing, but proven device platforms continue to account for the larger installed and clinical-use base.

Driver Analysis

Chronic Disease Burden and High Clinical Demand

The U.S. Medical Devices Market is strongly driven by the rising burden of chronic diseases and the need for continuous diagnosis, monitoring, and treatment. CDC states that chronic diseases are the leading cause of illness, disability, and death in the U.S., while three in four American adults have at least one chronic condition. This supports steady demand for diagnostic devices, cardiovascular devices, diabetes care devices, imaging systems, surgical tools, and patient monitoring products.

Healthcare spending also supports device demand across hospitals, clinics, laboratories, and outpatient care settings. CMS reported that U.S. national health expenditure reached USD 5.3 trillion in 2024, equal to USD 15,474 per person and 18.0% of GDP. Hospital spending alone reached USD 1,634.7 billion, while physician and clinical services spending reached USD 1,109.7 billion, creating a large installed base for medical device use.

Restraint Analysis

Cost Pressure and Reimbursement Scrutiny

A major restraint for the U.S. Medical Devices Market is the rising pressure to control healthcare costs. CMS projects that national health expenditure will grow faster than GDP from 2025 to 2034, increasing the health spending share from 18.0% of GDP in 2024 to 20.6% by 2034. This can make hospitals, payers, and procurement teams more selective when approving new devices, especially products with high upfront costs or unclear clinical value.

Reimbursement pressure can also slow adoption for advanced devices used in imaging, surgery, remote monitoring, and digital health. Medical device companies must provide strong clinical evidence, workflow benefits, and cost-saving value before broad adoption can be achieved. As Medicare spending is projected to grow faster than other major funding sources, pricing, coverage, and payment decisions are expected to remain important market restraints.

Opportunity Analysis

AI-Enabled Devices and Digital Health Innovation

A strong opportunity is emerging from AI-enabled medical devices, digital diagnostics, remote monitoring, and software-driven care tools. FDA’s AI-enabled medical device list is designed to identify AI-enabled devices authorized for marketing in the U.S., helping providers and patients understand where AI is being used in regulated medical technologies. FDA also stated that these devices have met applicable premarket requirements, including review of safety and effectiveness.

Innovation activity remains strong in the U.S. device ecosystem. FDA’s Center for Devices and Radiological Health authorized 124 novel medical devices in 2025, one of the highest annual totals in more than 40 years. The center also highlighted work around generative AI-enabled digital mental health devices and a CMS collaboration through the TEMPO pilot for digital health devices, which shows rising regulatory attention toward digital medical technologies.

Challenge Analysis

Cybersecurity, Recalls, and Quality Compliance

The main challenge for the U.S. Medical Devices Market is the need to maintain patient safety while devices become more connected, software-driven, and AI-enabled. FDA updated its medical device cybersecurity guidance in February 2026, with recommendations on cybersecurity design, labeling, and documentation for premarket submissions. This shows that cybersecurity is now a core regulatory requirement, not only an IT issue for manufacturers.

Recall and quality risks also remain serious because medical devices are used directly in diagnosis, monitoring, and treatment. FDA’s recall database includes medical device recalls classified since November 2002, and it also includes correction or removal actions initiated before FDA review in some cases. For manufacturers, this creates pressure to strengthen quality systems, post-market surveillance, supplier controls, and complaint handling to reduce product safety risks.

Segment Covered in the Report

By Device Type

In Vitro Diagnostics (IVD)

Diagnostic Imaging

Cardiovascular Devices

Orthopedic Devices

Surgical Devices

Patient Monitoring Devices

Others

By Application

Cardiology

Diagnostic Imaging

Orthopedics

Neurology

In Vitro Diagnostics

Others

By End User

Hospitals and Clinics

Ambulatory Surgical Centers

Diagnostic Laboratories

Home Healthcare

Others

By Technology

Conventional Devices

Connected Medical Devices

AI-Enabled Medical Devices

Robotic-Assisted Devices

Recent Developments, Mergers, Acquisitions and Funding

June 2026: Medtronic completed its acquisition of Scientia Vascular, a Salt Lake City-based neurovascular device company. The transaction was valued at USD 550 million, with additional undisclosed earn-out and milestone payments possible after acquisition. The deal strengthens Medtronic’s stroke care portfolio through guidewires and catheters used in complex neurovascular procedures.

June 2026: Medtronic received FDA 510(k) clearance for its Nellcor pulse oximetry system with Nell-EQ intelligent processor. The technology is designed to improve oxygen saturation and pulse rate monitoring reliability across different skin tones, patient groups, and clinical settings. This is important because pulse oximeter accuracy across skin pigmentation has become a major U.S. regulatory and patient-safety issue.

June 2026: ARPA-H listed new awards under maternal-fetal monitoring and obstetric hypoxia risk assessment. The selected projects include wearable ultrasound, wireless fetal EEG monitoring, microfluidic point-of-care testing, wearable photoacoustic imaging, and smart maternal-fetal monitoring belts. These awards show continued U.S. government support for next-generation diagnostic and monitoring devices.

May 2026: Medtronic announced its intent to acquire SPR Therapeutics, a company focused on temporary peripheral nerve stimulation for chronic pain. Public deal reporting placed the upfront cash payment at about USD 650 million. The acquisition supports non-opioid pain management and expands Medtronic’s neuromodulation device portfolio.

May 2026: Boston Scientific invested USD 1.5 billion in MiRus LLC for an approximately 34% equity stake. The deal gives Boston Scientific access to MiRus’ cardiovascular and orthopedic device technologies, including the SIEGEL balloon-expandable TAVR system, with a potential option to acquire the heart-valve business later.

April 2026: CMS and FDA announced the RAPID coverage pathway for eligible breakthrough medical devices. The pathway is intended to align FDA review and Medicare coverage decisions earlier in development, with possible national Medicare coverage as soon as about two months after FDA authorization for qualifying devices.

April 2026: Medtronic completed its acquisition of CathWorks, a medical device company focused on coronary artery disease assessment. The transaction was valued at USD 585 million, with potential undisclosed earn-out payments. CathWorks’ FFRangio system uses AI and computational science to assess coronary physiology from routine angiograms without pressure wires.

People Also Ask

How big is the U.S. medical devices market?

The U.S. medical devices market was valued at USD 209.1 billion in 2025 and is projected to reach USD 407.6 billion by 2035, growing at a CAGR of 6.9% from 2025 to 2035.

What is driving the growth of the U.S. medical devices market?

The growth of the market can be attributed to rising chronic disease cases, higher use of diagnostic testing, growth in minimally invasive procedures, hospital technology upgrades, and wider adoption of connected and AI-enabled devices. Demand is also supported by the strong U.S. healthcare infrastructure and continued investment in medtech innovation.

Which device type leads the U.S. medical devices market?

In vitro diagnostics led the device type segment with 19.9% share, supported by strong demand for laboratory testing, disease screening, point-of-care diagnostics, and routine clinical decision-making.

Which application dominates the U.S. medical devices market?

Cardiology accounted for 30.6% share by application, driven by the high burden of cardiovascular diseases, wider use of cardiac monitoring systems, and rising adoption of interventional and diagnostic cardiac devices.

Which end user holds the largest share in the U.S. medical devices market?

Hospitals and clinics held 56.4% share, supported by high patient footfall, advanced treatment infrastructure, strong purchasing capacity, and wide use of diagnostic, surgical, and therapeutic devices.