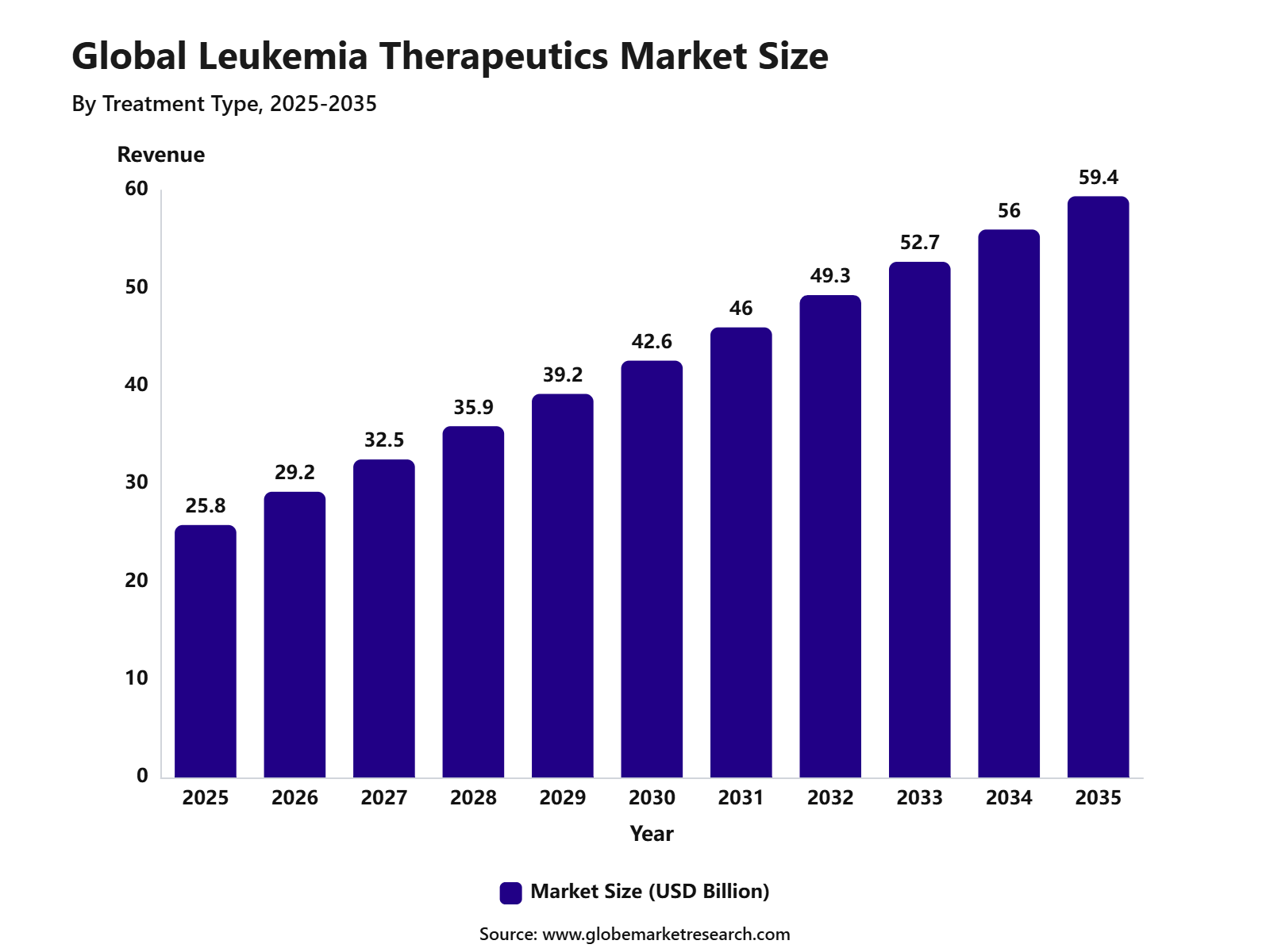

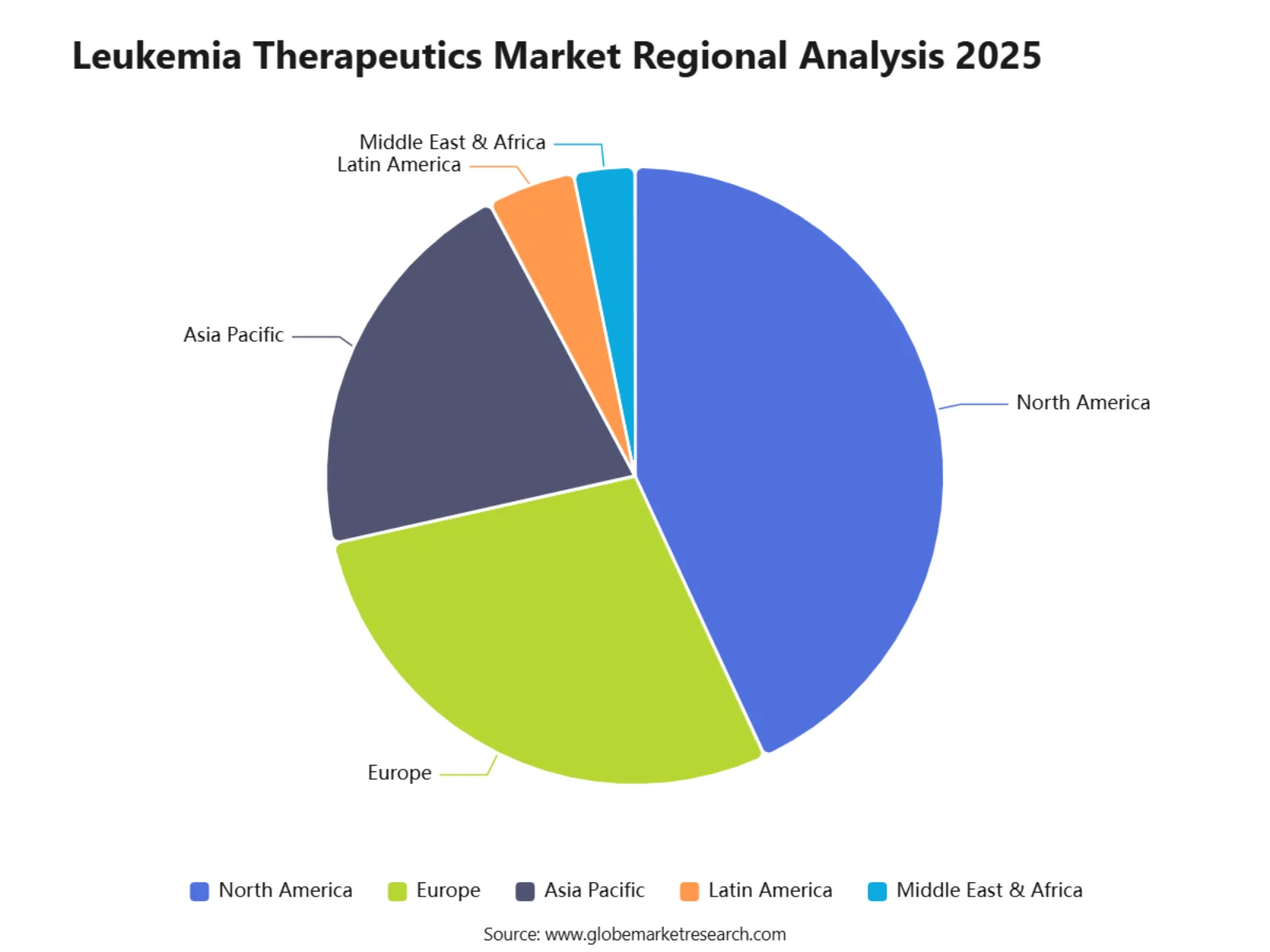

According to Globe Market Research, The Global Leukemia Therapeutics Market stood at USD 25.8 billion in 2025 and is anticipated to reach USD 59.4 billion by 2035. North America held the largest regional share of 43.1% in 2025, supported by advanced oncology treatment infrastructure, high awareness of blood cancer diagnosis, strong availability of targeted therapies, and continuous investment in cancer research.

The Leukemia Therapeutics Market includes drugs and treatment solutions used for different types of leukemia, including acute lymphocytic leukemia, acute myeloid leukemia, chronic lymphocytic leukemia, and chronic myeloid leukemia. Key treatment approaches include chemotherapy, targeted therapy, immunotherapy, monoclonal antibodies, tyrosine kinase inhibitors, and stem cell transplantation support. The market is closely linked with oncology drug development, hematology care, clinical trials, companion diagnostics, and hospital-based cancer treatment.

The market outlook remains strong as demand for advanced and personalized leukemia treatment continues to rise. The U.S. Leukemia Therapeutics Market was valued at USD 7.6 billion in 2025 and is expected to grow at a CAGR of 7.8% from 2025 to 2035, supported by rising diagnosis rates, wider access to innovative therapies, and strong oncology research funding. Growth is also supported by improved survival outcomes, increasing use of precision medicine, and a growing pipeline of targeted and immune-based therapies.

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 25.8 Bn |

Forecast Revenue (2035) | USD 59.4 Bn |

CAGR (2025-2035) | 8.7% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Key Takeaways

Targeted therapy held the largest share of 40.3% in the leukemia therapeutics market, supported by its ability to deliver more precise treatment, improve clinical outcomes, and address specific genetic mutations linked to leukemia.

Chronic lymphocytic leukemia accounted for 31.1% share by leukemia type, driven by its higher occurrence among the ageing population and the growing adoption of advanced treatment protocols.

Small-molecule drugs captured 36.8% share, supported by rising preference for oral therapies, targeted drug mechanisms, and better treatment convenience for patients.

Injectable therapies held 67.2% share by route of administration, owing to the continued use of chemotherapy, monoclonal antibodies, immunotherapies, and other hospital-administered leukemia treatments.

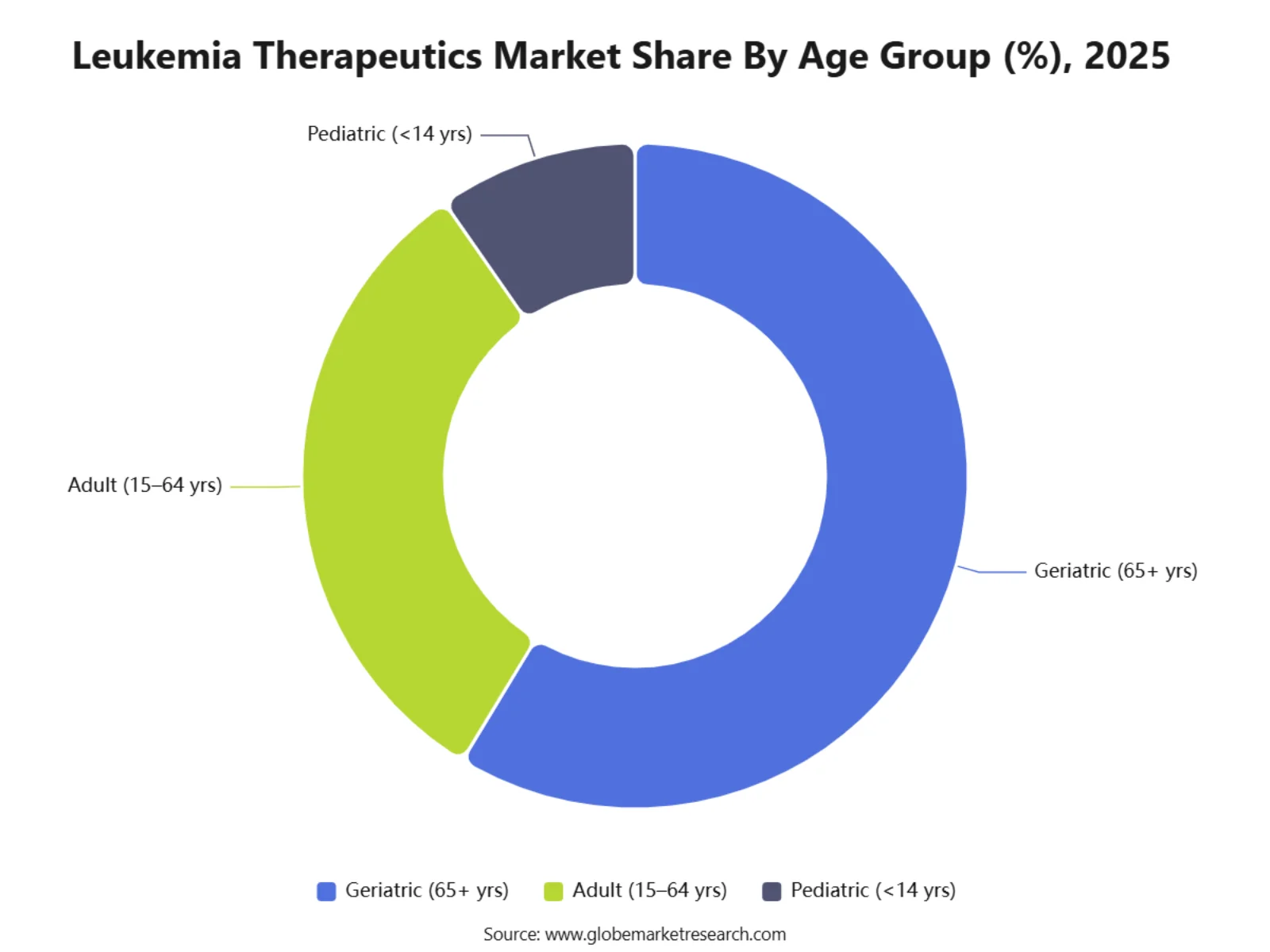

The geriatric population aged 65 years and above accounted for 58.6% share, as leukemia incidence remains significantly higher among older adults due to age-related health risks and immune system decline.

North America accounted for 43.1% share of the leukemia therapeutics market, supported by advanced oncology infrastructure, strong access to innovative drugs, high diagnosis rates, and wider adoption of modern treatment options.

The U.S. leukemia therapeutics market was valued at USD 7.6 billion and is expected to grow at a CAGR of 7.8% , driven by strong cancer research investment, broader therapy access, and increasing use of precision oncology.

Role of AI in Leukemia Therapeutics Market

AI is supporting the Leukemia Therapeutics Market by improving early diagnosis, subtype identification, and risk assessment. This is important because leukemia is expected to account for 67,790 new cases in the U.S. in 2026, representing 3.2% of all new cancer cases. AI-based tools can analyse blood counts, bone marrow images, flow cytometry data, and genetic profiles to help clinicians identify disease patterns faster. This can support earlier referral, better disease classification, and more timely treatment decisions.

AI is also helping improve treatment selection by connecting patient-specific genetic data with drug-response patterns. This is highly relevant because SEER reports the 5-year relative survival rate for leukemia at 68.6%, showing that stronger treatment matching remains an important clinical need. In acute leukemia, AI models are being tested to predict disease subtypes from routine laboratory data, which may help hospitals speed up decision-making in settings with limited specialist access. These tools can support precision therapy, targeted drug use, and more efficient clinical trial matching.

AI is further contributing to drug development and relapse management by supporting resistance prediction, treatment monitoring, and patient stratification. The need for better long-term care is clear because SEER estimates that 563,581 people were living with leukemia in the U.S. in 2023. FDA’s 2025 traditional approval of pirtobrutinib for relapsed or refractory CLL/SLL also reflects continued progress in targeted leukemia treatment, with the pivotal trial including 238 previously treated patients. Overall, AI is expected to strengthen the market by improving diagnostic speed, therapy selection, drug discovery efficiency, and follow-up care.

Customer Acquisition Economics

Customer acquisition in the leukemia therapeutics market is mainly driven by clinical evidence, guideline acceptance, biomarker testing, payer coverage, hospital access, and physician confidence. Buyers and decision-makers include hematologists, cancer centers, hospital pharmacy teams, insurers, government health systems, specialty distributors, and transplant or cellular therapy units. Since leukemia treatment is often urgent and complex, therapy adoption depends on survival benefit, safety profile, molecular eligibility, treatment setting, and ease of patient monitoring.

This is especially important for targeted therapies, CAR-T therapies, bispecific antibodies, menin inhibitors, BCL-2 inhibitors, BTK inhibitors, FLT3 inhibitors, IDH inhibitors, and tyrosine kinase inhibitors. A 2026 leukemia treatment review noted that modern leukemia care now includes immunotherapies, BCR::ABL1 TKIs, BTK inhibitors, BCL-2 inhibitors, IDH inhibitors, FLT3 inhibitors, menin inhibitors, and CAR-T cell therapies, showing how treatment selection has become more specialized.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is strongest across acute myeloid leukemia, chronic lymphocytic leukemia, acute lymphoblastic leukemia, chronic myeloid leukemia, relapsed or refractory disease, measurable residual disease-guided treatment, transplant maintenance, and cellular therapy. AML and CLL remain major commercial areas because of patient volume, older patient burden, relapse risk, and continuing movement toward oral targeted combinations. In 2026, the American Cancer Society estimated 22,720 new AML cases and 11,500 AML deaths in the U.S., while CLL was estimated at 22,760 new cases and 4,350 deaths.

Recent approvals are widening the addressable treatment base. In February 2026, the FDA approved acalabrutinib with venetoclax for adults with CLL or small lymphocytic lymphoma, supporting fixed-duration oral combination use. In May 2026, the FDA approved oral decitabine and cedazuridine tablets with venetoclax for newly diagnosed AML in adults aged 75 years or older, or adults with comorbidities that prevent intensive induction chemotherapy.

The market is also being reshaped by precision medicine. In November 2025, the FDA approved ziftomenib for adults with relapsed or refractory AML with a susceptible NPM1 mutation and no satisfactory alternative treatment options. In 2024, the FDA approved revumenib for relapsed or refractory acute leukemia with KMT2A translocation in adult and pediatric patients aged 1 year and older. These approvals show rising commercial focus on genetically defined leukemia subgroups.

Financial Impact

The financial impact of leukemia therapeutics is supported by high clinical need, chronic treatment use in some subtypes, relapse management, biomarker-led therapy selection, and premium pricing for advanced therapies. Oral targeted therapies can improve revenue durability because patients may continue treatment across defined cycles or longer disease-control periods. Combination regimens also increase value per treated patient, especially where therapies are used with venetoclax, BTK inhibitors, hypomethylating agents, or chemotherapy backbones.

Cell therapy is creating a high-value treatment channel, but it requires specialist infrastructure. In November 2025, NHS England said a CAR-T therapy for relapsed or refractory B-cell acute lymphoblastic leukaemia would be available for people aged 26 and over after NICE approval, with around 50 patients expected to receive it each year in England. This indicates that CAR-T revenue is high value but limited by patient eligibility, manufacturing capacity, treatment-center availability, and reimbursement decisions.

Clinical development remains active, which supports future revenue expansion. ClinicalTrials.gov listings show ongoing studies in AML, ALL, CLL, and related hematologic malignancies, including CAR-T approaches, revumenib combinations, mocravimod maintenance, and other novel agents. This continuing pipeline activity supports revenue opportunities across newly diagnosed disease, relapsed disease, maintenance therapy, and transplant-adjacent settings.

Risk Factors & Market Barriers

Regulatory & Compliance Risks

Regulatory risk is high because leukemia therapies are closely reviewed for survival outcomes, remission durability, adverse events, dosing safety, drug interactions, and post-approval evidence. Many leukemia patients are older, immunocompromised, or heavily pretreated, so safety findings can strongly influence label expansion, physician adoption, and payer coverage. FDA approval pathways may also require strong evidence in small molecularly defined populations, which raises trial complexity.

Cell and gene therapies face additional compliance requirements. CAR-T products need patient-specific collection, manufacturing, release testing, logistics control, infusion-center readiness, cytokine release syndrome management, neurotoxicity monitoring, and long-term follow-up. These requirements can slow broader uptake, even when clinical outcomes are strong.

Payer and health technology assessment risks are also important. High-cost therapies must show clinical value against existing treatments, especially where multiple options already exist in CLL, AML, ALL, and CML. Reimbursement delays, step therapy rules, prior authorization, and country-specific cost-effectiveness reviews can slow patient access and reduce commercial conversion.

Market Adoption Barriers

Market adoption is limited by complex diagnosis pathways, biomarker testing gaps, high therapy cost, treatment-center capacity, adverse event management, and unequal access to specialist care. Precision therapies depend on molecular testing for markers such as NPM1, KMT2A, FLT3, IDH1/2, BCR::ABL1, and TP53-related risk. If testing is delayed or unavailable, eligible patients may not be matched to the right therapy in time.

Patient age and fitness are also major barriers. AML is more common in older adults, and SEER data shows AML death rates are higher among adults aged 65 and older. This creates demand for lower-intensity and oral regimens, but it also increases safety monitoring needs due to frailty, infections, cytopenias, and comorbidities.

Competition is increasing as more targeted drugs enter the market. BTK inhibitors, BCL-2 inhibitors, menin inhibitors, FLT3 inhibitors, IDH inhibitors, monoclonal antibodies, bispecifics, TKIs, chemotherapy combinations, and CAR-T therapies are all competing for defined patient groups. The strongest adoption is expected for therapies that show clear survival benefit, manageable safety, convenient administration, biomarker precision, payer acceptance, and strong fit within real-world hematology workflows.

Top Two Opportunities

1. Precision therapies for mutation-defined acute leukemia

The first major opportunity is the development of targeted therapies for genetically defined leukemia groups, especially AML patients with NPM1 mutations, KMT2A rearrangements, FLT3 mutations, IDH alterations, and other actionable markers. The need remains significant, as SEER estimates 67,790 new leukemia cases and 23,910 deaths in the U.S. in 2026. This supports demand for treatments that are selected through molecular testing rather than a one-size-fits-all chemotherapy approach.

Menin inhibitors are becoming an important opportunity in this area. The FDA approved revumenib in November 2024 for relapsed or refractory acute leukemia with KMT2A translocation in adults and children aged 1 year and above, and later approved ziftomenib in November 2025 for adults with relapsed or refractory AML carrying an NPM1 mutation. These approvals show that targeted drug development is moving into difficult leukemia subtypes where treatment options have historically been limited.

The recommended strategy is to build therapies around biomarker testing, companion diagnostics, and specialist hematology centers. Companies should focus on oral targeted agents, combination regimens, and post-remission maintenance approaches where relapse risk remains high. The FDA’s May 2026 approval of oral decitabine and cedazuridine tablets with venetoclax for newly diagnosed AML in adults aged 75 years or older, or those unfit for intensive induction chemotherapy, also supports the opportunity for easier treatment options in older and medically fragile patients.

2. Cell therapy, immunotherapy, and MRD-guided treatment for relapsed leukemia

The second major opportunity is the expansion of cell therapy and immune-based treatment for relapsed or refractory leukemia. This is especially important in B-cell acute lymphoblastic leukemia and hard-to-treat chronic lymphocytic leukemia, where patients may fail earlier lines of therapy. The American Cancer Society estimates 6,250 new ALL cases and 1,600 ALL deaths in the U.S. in 2026, showing that better treatment access remains important even in a smaller patient population.

CAR T-cell therapy is a key growth area because it offers a new treatment pathway for patients with limited options. In November 2024, the FDA approved obecabtagene autoleucel for adults with relapsed or refractory B-cell precursor ALL. For CLL and SLL, the FDA also granted traditional approval to pirtobrutinib in December 2025 for adults previously treated with a covalent BTK inhibitor, showing continued movement toward advanced treatment sequencing after earlier targeted therapy failure.

The recommended strategy is to develop therapies that fit into MRD-guided care pathways. MRD testing is increasingly being used to measure deeper response, identify relapse risk, and guide treatment after remission or transplant. NCCN’s 2026 AML guideline insights highlight MRD monitoring in AML management, including use around allogeneic transplantation, which supports demand for therapies that can convert patients to MRD-negative status or maintain remission for longer periods.

Market Segmentation

By Treatment Type

Chemotherapy

Immunotherapy

Targeted Therapy

CAR-T Cell Therapy

Gene Therapy

Stem Cell Transplantation

Other Treatment Types

By Leukemia Type

Acute Lymphoblastic Leukemia

Acute Myeloid Leukemia

Chronic Lymphocytic Leukemia

Chronic Myeloid Leukemia

Other Leukemia Types

By Therapy Modality

Small-Molecule Drugs

Monoclonal Antibodies

CAR-T Cell Therapies

Gene Therapies

Bispecific Antibodies

RNA-based Therapies

Other Modalities

By Route of Administration

Oral

Intravenous

Subcutaneous

Other Routes

By Age Group

Pediatric (<14 yrs)

Adult (15–64 yrs)

Geriatric (65+ yrs)

By Region

North America

Europe

Asia Pacific

Latin America

Recent Developments

June 2026: Cycle Pharmaceuticals received FDA approval for Cavhanza, an orally disintegrating nilotinib tablet for adults with Philadelphia chromosome-positive chronic myeloid leukemia. The formulation is designed to support dosing flexibility, including use with proton pump inhibitors and H2 blockers.

June 2026: Roche and Nurix Therapeutics entered a global collaboration for bexobrutideg, an oral BTK degrader planned for Phase 3 testing in chronic lymphocytic leukemia. Nurix will receive USD 700 million upfront and may receive total payments of up to USD 2.3 billion.

June 2026: Kura Oncology and Kyowa Kirin reported updated long-term results for ziftomenib with intensive chemotherapy in newly diagnosed AML. The companies reported a 12-month overall survival rate of 94% in NPM1-mutated AML patients and 71% in KMT2A-rearranged AML patients in the single-arm KOMET-007 trial.

May 2026: FDA approved oral decitabine and cedazuridine tablets with venetoclax for newly diagnosed AML in adults aged 75 years or older, or adults with comorbidities that prevent intensive induction chemotherapy. This approval supports broader use of all-oral hypomethylating agent-based regimens in AML.

People Also Ask

What is the Leukemia Therapeutics Market?

The Leukemia Therapeutics Market includes medicines and treatment approaches used to manage acute and chronic leukemia. It covers chemotherapy, targeted therapy, immunotherapy, monoclonal antibodies, CAR T-cell therapy, stem cell transplant support, and combination regimens used across AML, ALL, CLL, and CML. Leukemia is a cancer of blood-forming tissues, including bone marrow and the lymphatic system.

How big is the Leukemia Therapeutics Market?

The Global Leukemia Therapeutics Market was valued at USD 25.8 billion in 2025 and is projected to reach USD 59.4 billion by 2035, growing at a CAGR of 8.7% from 2025 to 2035. North America led the market with a 43.1% share in 2025, while the U.S. market reached USD 7.6 billion and is expected to grow at a 7.8% CAGR. Growth is supported by rising diagnosis rates, wider access to advanced therapies, targeted oncology drugs, and strong hematology research investment.

What are the main types of leukemia?

The main types of leukemia are acute myeloid leukemia, acute lymphocytic leukemia, chronic lymphocytic leukemia, and chronic myeloid leukemia. Acute leukemia usually progresses quickly and needs earlier treatment, while chronic leukemia often develops more slowly. In the U.S., SEER estimated 67,790 new leukemia cases and 23,910 deaths in 2026, with a five-year relative survival rate of 68.6% for cases diagnosed during 2016 to 2022.

What treatments are used for leukemia?

Common leukemia treatments include chemotherapy, targeted therapy, immunotherapy, radiation therapy, stem cell transplant, supportive care, and clinical trial-based treatments. NCI lists chemotherapy, immunotherapy, targeted therapy, radiation therapy, and blood stem cell transplant among major cancer treatment types. Stem cell transplants are most often used for blood cancers such as leukemia, lymphoma, multiple myeloma, and myelodysplastic syndromes.

Why is the Leukemia Therapeutics Market growing?

The growth of the Leukemia Therapeutics Market can be attributed to higher blood cancer diagnosis, longer treatment duration, improved survival, precision medicine, and new drug approvals for genetically defined leukemia groups. SEER data show that leukemia death rates in the U.S. fell by an average of 1.8% per year during 2015 to 2024, while survival has improved due to better treatment options and earlier disease management.

What is targeted therapy for leukemia?

Targeted therapy for leukemia uses medicines designed to block specific genes, proteins, or pathways that help leukemia cells grow and survive. These treatments are highly important in CML, AML, ALL, and CLL because many cases are driven by identifiable genetic changes or cell-surface markers. NCI notes that leukemia treatment has moved beyond traditional chemotherapy, with major progress coming from targeted agents and immune-based approaches.