Introduction

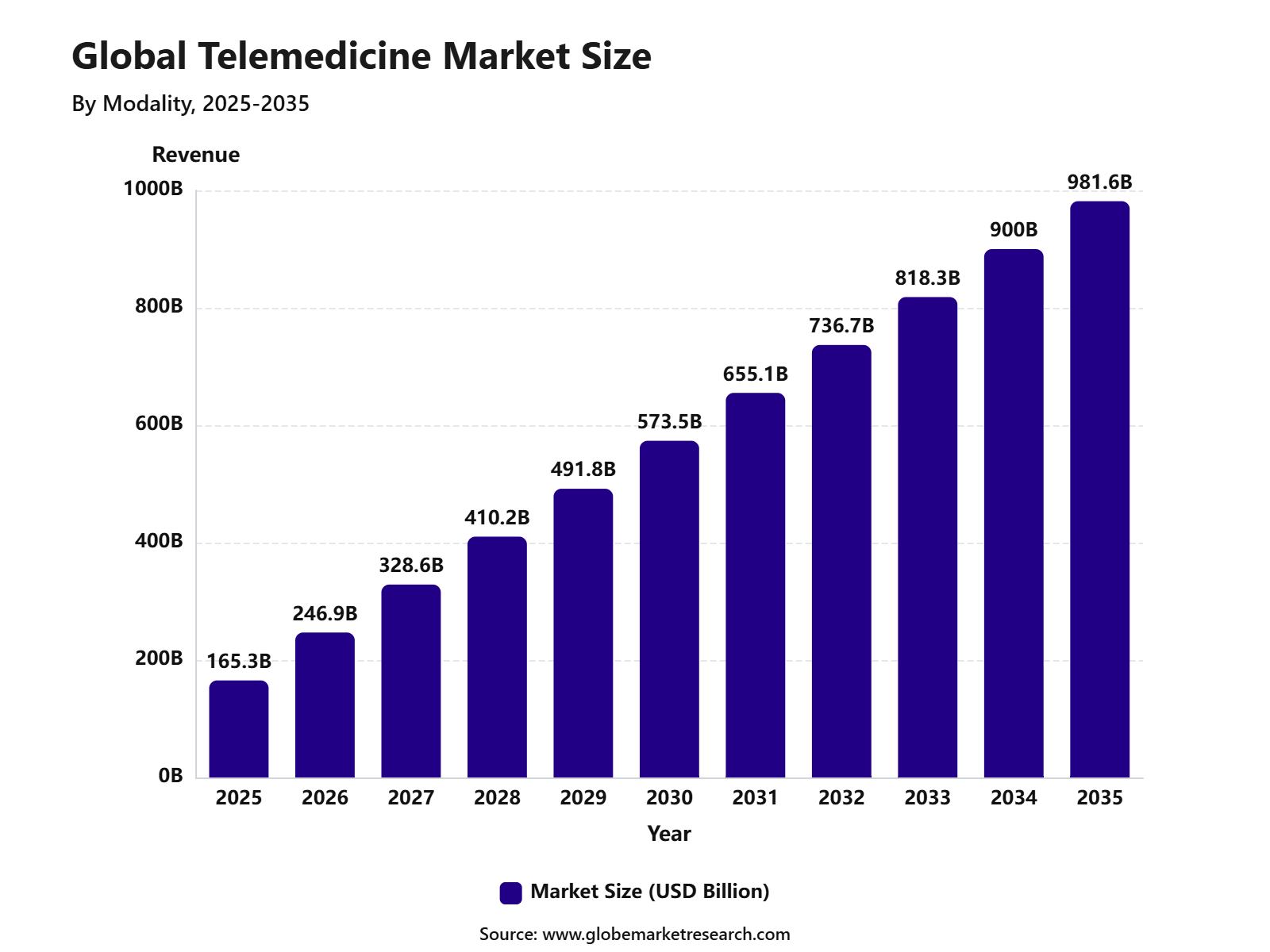

According to Globe Market Research, The Global Telemedicine Market was valued at USD 165.3 billion in 2025 and is projected to reach USD 981.6 billion by 2035, growing at a CAGR of 19.5% from 2025 to 2035. Growth is being supported by rising use of virtual consultations, remote patient monitoring, digital health platforms, and mobile-based healthcare services. North America led the market, supported by strong digital healthcare infrastructure, favorable reimbursement models, and wide adoption of virtual care systems.

Key Parameter | Report Details |

|---|---|

Current Revenue, 2025 | USD 165.3 Billion |

Projected Revenue, 2035 | USD 981.6 Billion |

CAGR, 2025 To 2035 | 19.5% |

Largest Region | North America |

Fastest Growing Region | Asia Pacific |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

What Is the Telemedicine Market?

The Telemedicine Market refers to the delivery of healthcare services through digital communication tools such as video consultation, phone consultation, remote patient monitoring, e-prescriptions, online diagnosis support, and virtual follow-up care. It allows patients to connect with doctors, specialists, nurses, and healthcare providers without visiting a clinic or hospital physically. Telemedicine is now widely used across primary care, mental health, chronic disease management, dermatology, post-surgery follow-up, elderly care, and rural healthcare access.

The market is gaining importance because it helps healthcare systems serve more patients while reducing unnecessary hospital visits. The growth of the market can be attributed to increasing pressure on healthcare systems, shortage of healthcare professionals in remote areas, and rising patient preference for faster access to care. Telemedicine helps providers manage routine consultations, follow-ups, prescription refills, behavioral health visits, and chronic disease monitoring more efficiently.

Market Highlights

Synchronous telemedicine led the modality segment with 45.8% share in 2025. Growth was supported by real-time patient consultations, faster clinical discussion, and stronger acceptance of virtual healthcare services.

Services and support accounted for 58.3% share by component. Demand was driven by telehealth implementation, technical support, training, platform management, and managed healthcare services.

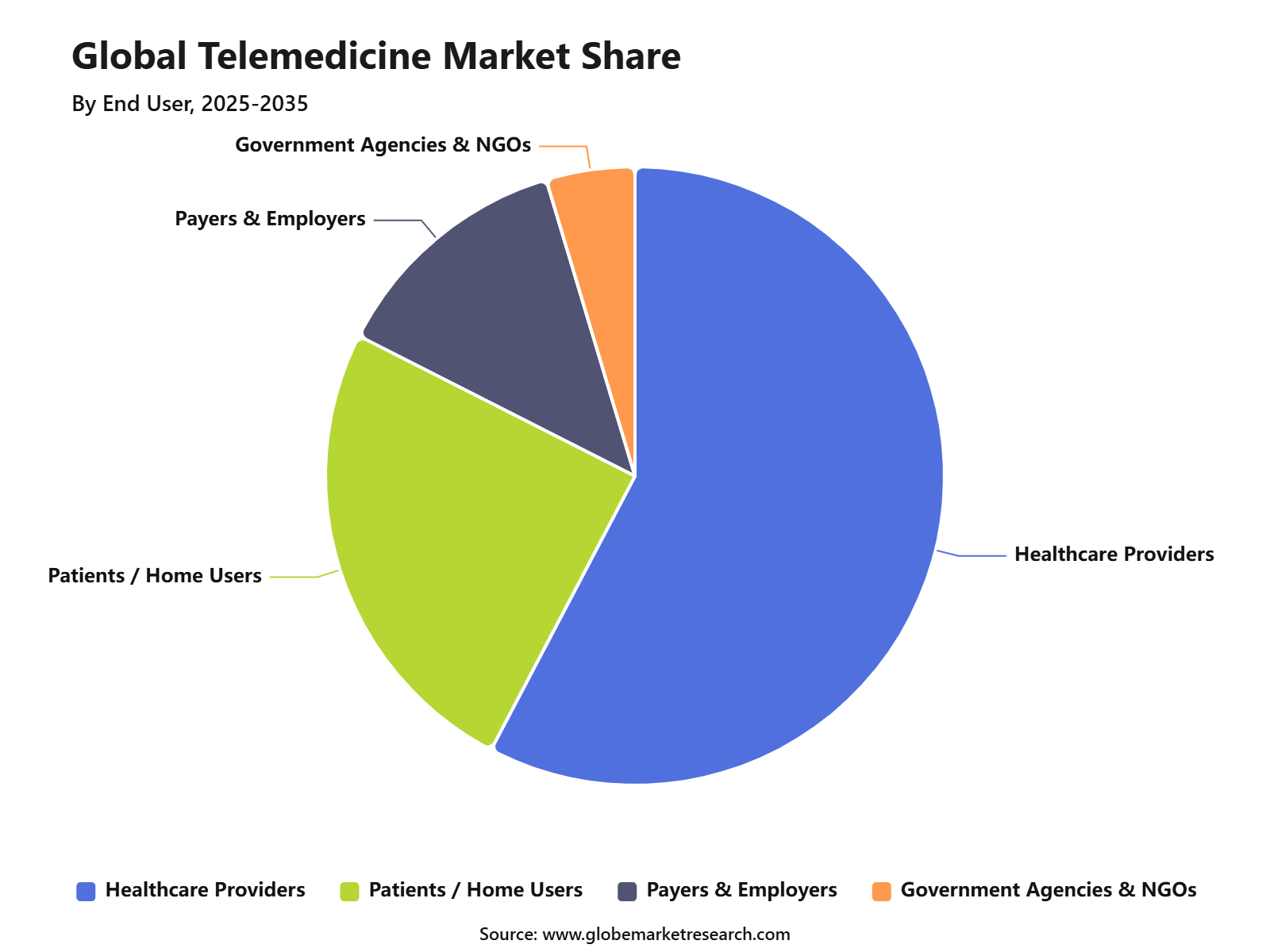

Healthcare providers held 57.3% share by end user. Growth was supported by rising use of virtual care platforms, remote patient monitoring, digital consultation tools, and follow-up care systems.

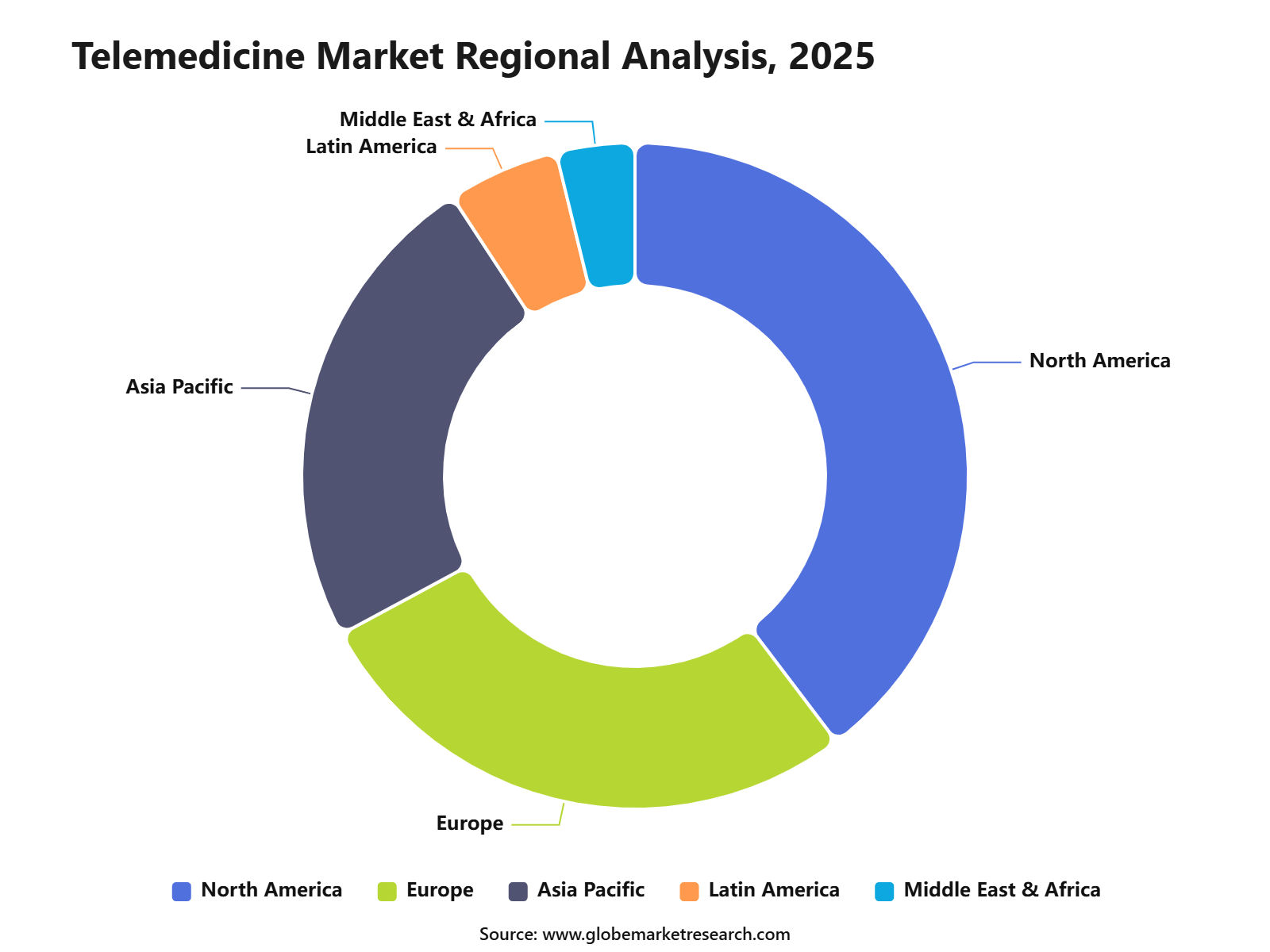

North America accounted for about 39.6% share of the market. The region benefits from advanced healthcare infrastructure, strong digital health adoption, favorable reimbursement frameworks, and high provider participation.

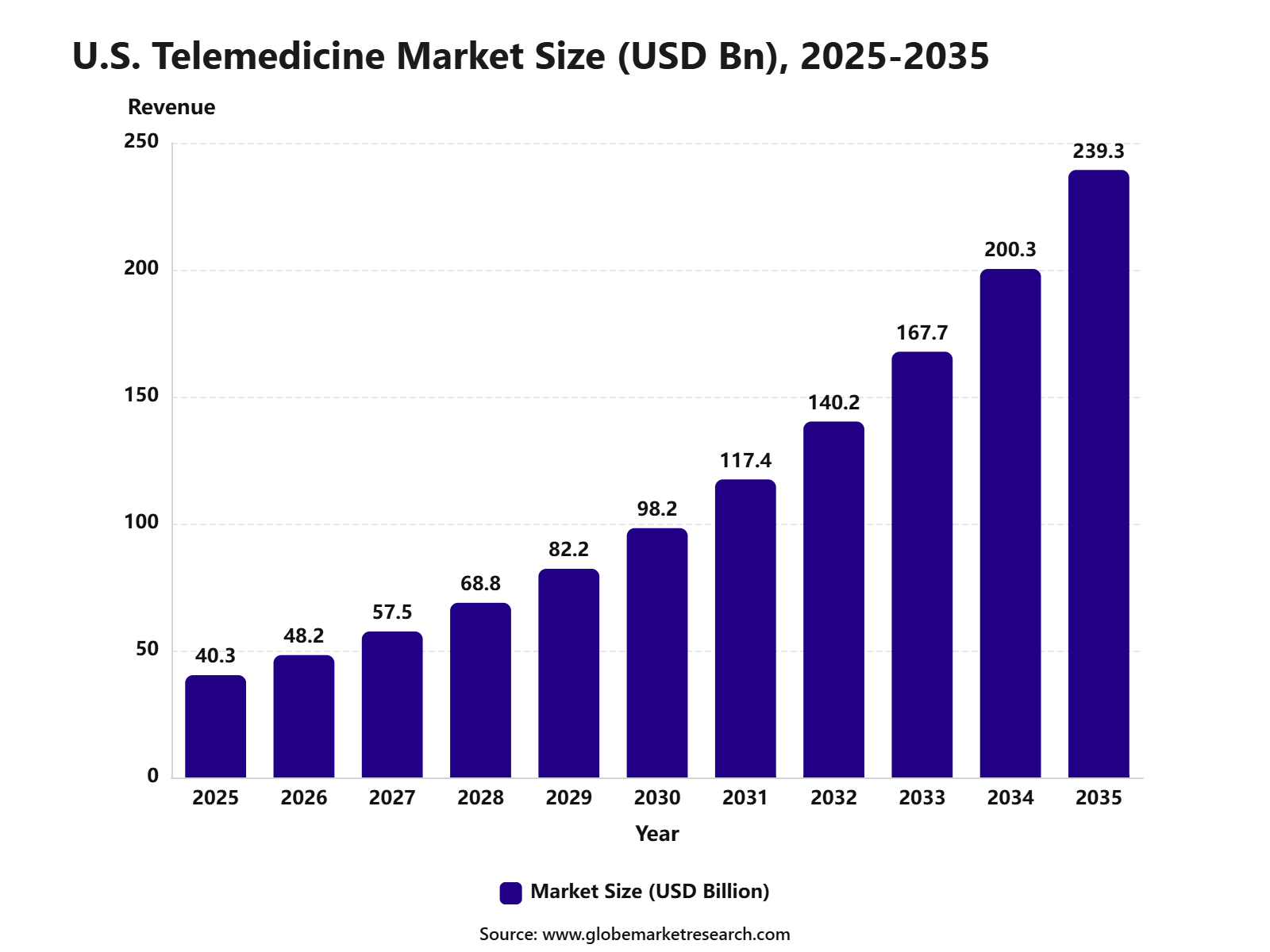

In the U.S., telehealth activity increased again in early 2026. FAIR Health reported that telehealth represented 5.51% of medical claim lines in Q1 2026, compared with 5.01% in Q4 2025, showing a 10.1% relative increase. The share of patients with a telehealth claim also rose from 17.3% in Q4 2025 to 18.4% in Q1 2026.

Emerging Trends

Mental health is becoming the largest telemedicine use case: Mental health is now the strongest demand area in telemedicine. In Q1 2026, mental health conditions accounted for 52.1% of U.S. patients with a telehealth claim, making it the top diagnostic category across every age group and every U.S. region. This shows that virtual care is becoming a preferred route for therapy, psychiatric follow-ups, medication management, and ongoing behavioral health support.

Hybrid care models are becoming more practical: Telemedicine is increasingly being used with in-person care rather than as a full replacement. The model is useful for follow-up visits, medication reviews, chronic care checks, test-result discussions, and pre-consultation triage. OECD data shows teleconsultations remained above pre-pandemic levels, with remote consultations averaging 1.0 per patient per year in 2023, compared with 0.5 in 2019.

Public telemedicine platforms are scaling fast: Government-backed telemedicine is becoming important in countries with large rural and underserved populations. India’s eSanjeevani platform has delivered over 47 crore telemedicine consultations, showing how public digital health platforms can expand doctor access at national scale. This supports wider use of telemedicine in primary care, rural healthcare, and specialist access.

Factors Affecting the Telemedicine Market

Regulation and reimbursement strongly influence adoption: Telemedicine adoption depends heavily on payment rules, licensing policies, audio-only visit coverage, and insurance acceptance. In 2026, Medicare telehealth coverage was renewed for two years, giving physicians and patients more certainty after policy disruptions in 2025. This supports continued use of virtual visits among older adults and patients who need regular care access.

Urban access is still ahead of rural access: Telemedicine is designed to improve access, but digital gaps remain visible. In Q1 2026, 18.6% of urban commercially insured patients in the U.S. had a telehealth claim, compared with 10.3% of rural patients. However, rural growth was stronger at 7.8%, compared with 6.2% growth in urban areas, showing that rural adoption is improving but still has room to expand.

Digital infrastructure and patient confidence remain key barriers: Strong broadband access, secure platforms, electronic health records, and patient digital literacy are required for wider telemedicine use. OECD noted that legal, financial, and operational barriers still need to be addressed, along with stronger broadband infrastructure and integration of teleconsultations into mainstream care pathways.

By Modality

Synchronous led the market by modality with 45.8% share, supported by real-time video and audio consultations between patients and healthcare professionals. This format is widely used because it allows direct clinical discussion, faster decision-making, follow-up care, prescription support, and improved access for patients who may not need a physical visit.

The segment is also supported by continued telehealth use above pre-pandemic levels. OECD reported that remote consultations averaged 1.0 per patient per year in 2023 across OECD countries, compared with 0.5 in 2019. This shows that live virtual care has become part of routine healthcare delivery rather than only an emergency response tool.

By Component

Services and support accounted for 58.3% share by component, driven by rising demand for telehealth implementation, platform integration, technical assistance, staff training, compliance support, and managed virtual care services. Healthcare organizations often need external support to connect telemedicine with scheduling systems, electronic health records, billing workflows, cybersecurity tools, and patient engagement systems.

The segment is gaining importance as digital health systems become more complex. OECD stated that wider telemedicine use requires stronger payment systems, broadband infrastructure, legal clarity, and integration of teleconsultations into mainstream care pathways. This creates steady demand for service providers that can help hospitals, clinics, and payers run virtual care programs more efficiently.

By End User

Healthcare providers held 57.3% share by end user, supported by rising adoption of virtual care platforms, remote patient monitoring, digital consultation services, and hybrid care models. Hospitals, clinics, physician groups, and specialty care centers are using telemedicine to manage follow-ups, behavioral health visits, chronic disease support, test-result reviews, and routine consultations.

Provider adoption is also supported by stronger reimbursement certainty in key markets. In the U.S., Medicare telehealth coverage was renewed for two years in 2026, giving patients and physicians more confidence to continue virtual care services. The AMA also noted that telehealth improves continuity of care and is valuable for older adults, patients with mobility issues, and underserved populations.

By Region

North America accounted for 39.6% share of the telemedicine market, supported by advanced healthcare infrastructure, strong digital health adoption, favorable reimbursement policies, and high use of virtual care platforms. The region benefits from mature provider networks, wider insurance coverage for digital care, strong patient familiarity with telehealth, and continued investment in connected care systems.

The North American telemedicine market was valued at USD 65.4 billion, reflecting strong demand for remote healthcare delivery, digital consultation platforms, connected care solutions, and virtual behavioral health services. The market is being supported by healthcare providers that want to reduce access gaps, manage patient volumes, improve follow-up care, and support patients outside traditional care settings.

Top Use Cases

Behavioral health and therapy: Behavioral health is the most established telemedicine use case because many visits can be managed through video or audio consultation. In Q1 2026, mental health was the leading telehealth diagnostic category nationally, with 52.1% of telehealth patients having a mental health-related claim.

Primary care and routine follow-ups: Telemedicine is widely used for established patient office visits, follow-ups, test-result discussions, minor illness assessment, and care coordination. FAIR Health reported that established patient office or outpatient services ranked as the top telehealth procedure category nationally in Q1 2026.

Chronic disease management: Telemedicine supports diabetes, hypertension, obesity care, medication reviews, lifestyle follow-ups, and remote patient monitoring. In Q1 2026, overweight and obesity ranked among the top five telehealth diagnostic categories nationally, while endocrine and metabolic disorders were also listed among major telehealth diagnosis groups.

Rural and underserved healthcare access: Telemedicine is valuable for patients who face distance, transport, specialist shortages, or long waiting times. India’s more than 47 crore eSanjeevani consultations show how telemedicine can be used to connect patients with doctors across large and underserved geographies.

Market Concentration: Low

The market is highly fragmented because it includes many types of players, such as virtual care platforms, hospital-owned telehealth systems, health insurers, pharmacy-linked care platforms, remote monitoring providers, mental health platforms, chronic care providers, and regional digital health startups. No single company controls the overall market, and competition differs strongly by service type, specialty, geography, payer model, and healthcare regulation.

A 2026 industry update also describes the global telemedicine market as a highly fragmented competitive environment, with no single entity shaping the market’s overall growth path. Telehealth usage remains meaningful as well, with over 12.6% of Medicare beneficiaries receiving a telehealth service in Q4 2023, which supports broad provider participation rather than dominance by only a few firms.

Competitive Landscape

The Telemedicine Market is competitive, with digital health companies, hospital technology providers, remote monitoring firms, virtual care platforms, insurers, and healthcare service providers expanding their offerings. Companies are focusing on video consultation platforms, AI-enabled triage, chronic care monitoring, e-prescription tools, behavioral health services, and connected care solutions.

Key companies active in the telemedicine ecosystem include Teladoc Health, Amwell, MDLIVE, Doctor On Demand, Hims & Hers Health, Amazon One Medical, Siemens Healthineers, Philips, GE HealthCare, Oracle Health, Medtronic, and American Well.

Key Market Segments

By Modality

Synchronous

Asynchronous

Remote Patient Monitoring

By Component

Services

Software Platforms

Hardware & Peripherals

By End User

Healthcare Providers

Patients / Home Users

Payers & Employers

Government Agencies & NGOs

By Region

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Conclusion

Telemedicine is becoming a core part of modern healthcare delivery. The market is being supported by patient demand for convenience, provider need for operational efficiency, remote patient monitoring adoption, and stronger digital health policies. The strongest opportunity will be seen in platforms that combine easy access, clinical reliability, secure data handling, remote monitoring, and smooth integration with existing healthcare systems. As healthcare demand continues to rise, telemedicine is expected to remain an important tool for improving access, continuity of care, and patient engagement.