Market Size And Forecast

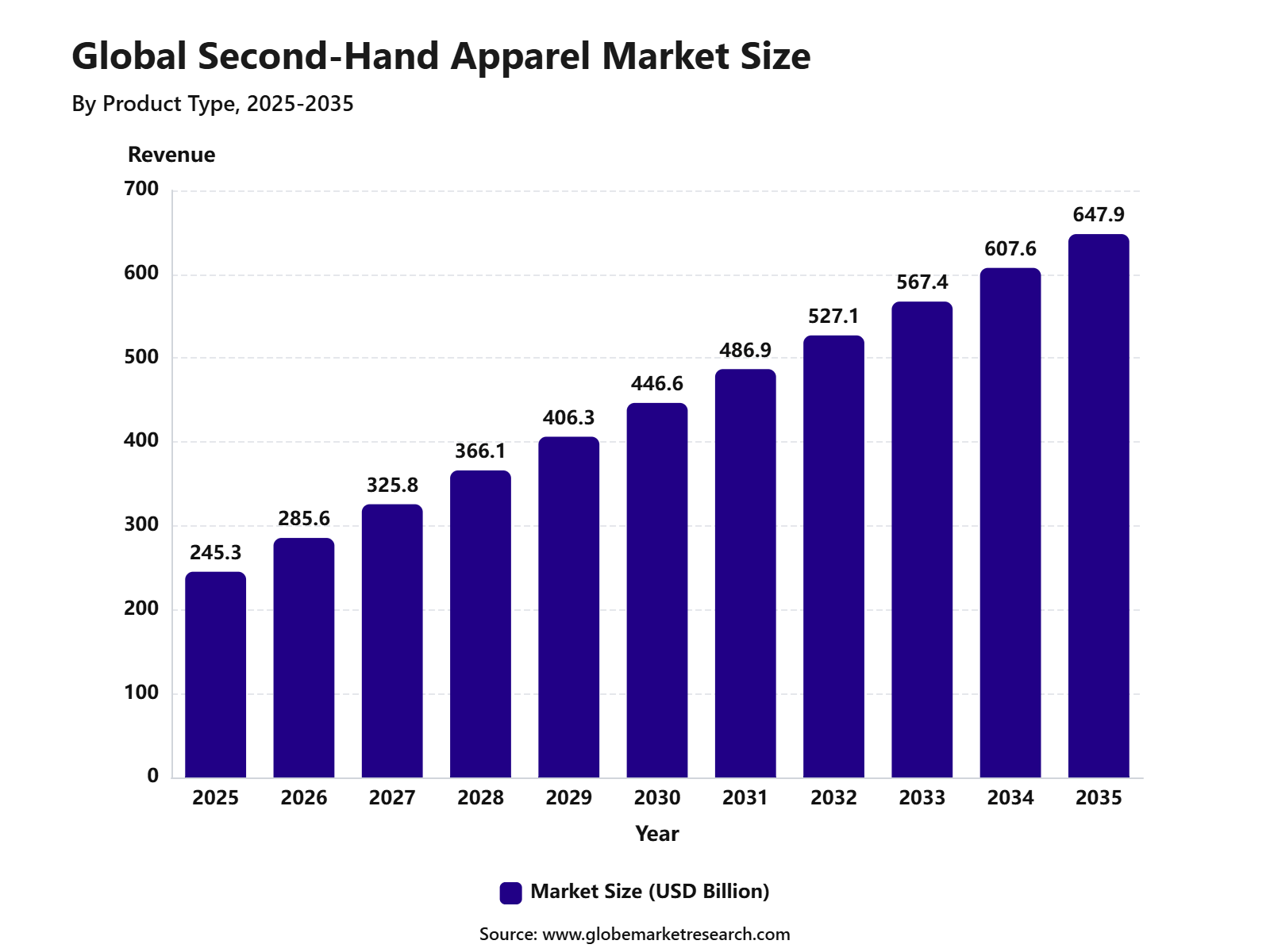

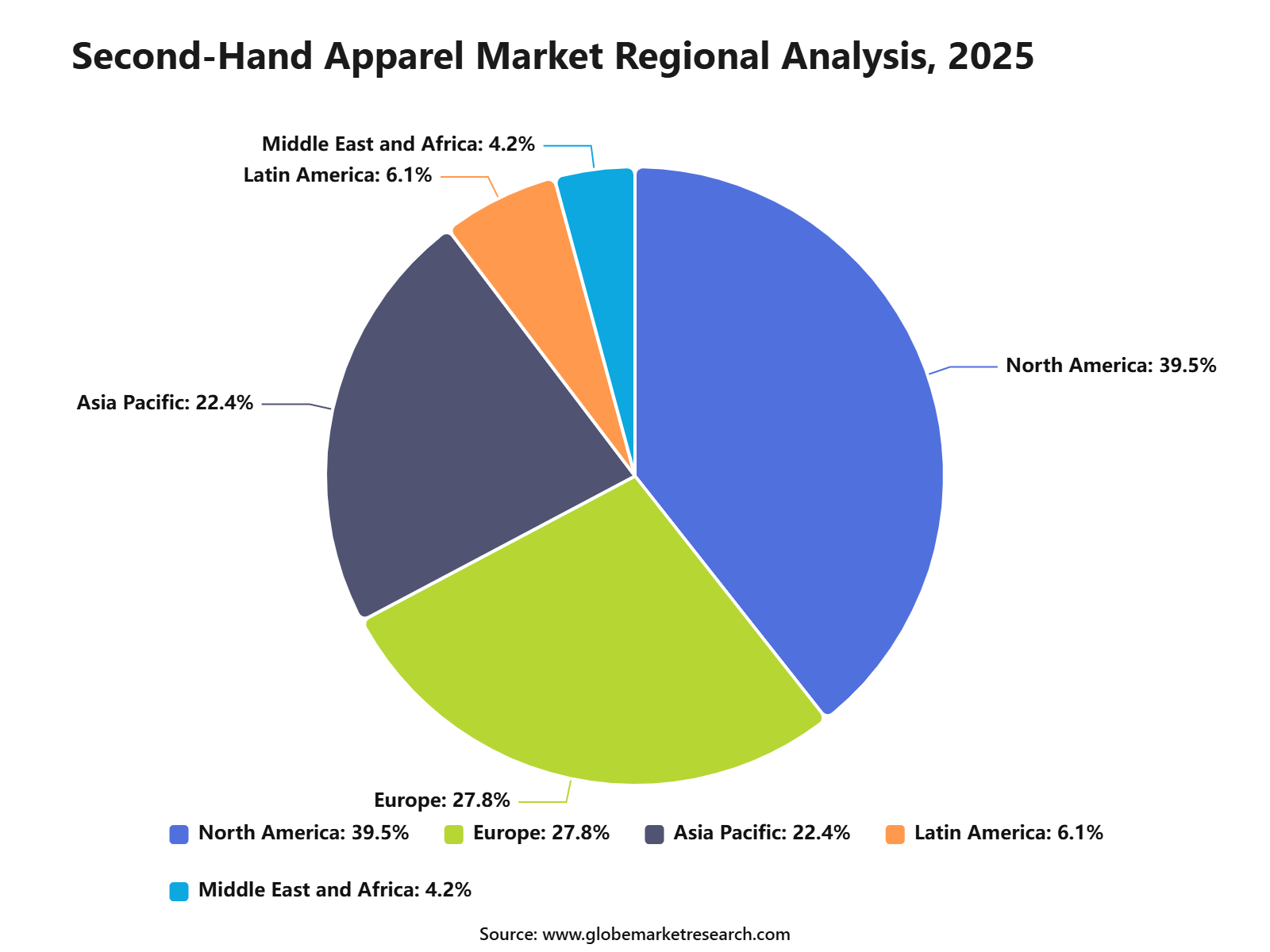

According to Globe Market Research (GMR), The Global Second-Hand Apparel Market was worth USD 245.3 billion in 2025 and reached USD 285.6 billion in 2026. The market is expected to reach USD 647.9 billion by 2035, growing at a CAGR of 10.2% from 2025 to 2035. North America held the largest regional share of 39.5% in 2025, supported by strong resale platform adoption, rising consumer interest in sustainable fashion, high purchasing power, and growing acceptance of pre-owned clothing across online and offline retail channels.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 245.3 Billion |

Projected Revenue, 2035 | USD 647.9 Billion |

CAGR (2025-2035) | 10.2% |

Largest Region | North America |

Leading Segment | Offline platforms |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

What Is The Second-Hand Apparel Market?

The Second-Hand Apparel Market includes the resale, reuse, and redistribution of pre-owned clothing, footwear, accessories, and fashion items through thrift stores, consignment shops, online resale platforms, brand-owned resale programs, and peer-to-peer marketplaces. The market is widely used by value-conscious consumers, fashion-focused buyers, sustainability-driven shoppers, and retailers seeking circular fashion models. It is closely linked with textile waste reduction, affordable fashion access, digital commerce, and changing consumer attitudes toward used clothing.

Key Report Takeaways

Tops and T-shirts captured 39.2% share, driven by their everyday usage, low replacement cost, and strong demand across casual, seasonal, and budget-friendly second-hand fashion categories.

Women’s wear held 55.5% share, supported by broader resale supply, faster wardrobe refresh cycles, and rising consumer interest in affordable branded, vintage, and trend-based clothing.

Mid-range apparel accounted for 46.1% share, as consumers increasingly prefer pre-owned clothing that offers better quality, recognizable brands, and stronger value compared to new low-cost fashion.

Offline sales channels represented 57.1% share, supported by thrift stores, resale shops, charity outlets, and boutique formats where buyers can physically check fabric quality, size, and condition.

North America led the second-hand apparel market with 39.5% share, supported by established resale networks, strong sustainability awareness, and growing acceptance of pre-owned fashion among Gen Z and millennial shoppers.

Top Funding and Investment

Investment in the second-hand apparel market is being driven by C2C resale platforms, Gen Z-focused fashion marketplaces, branded resale software, AI-powered second-hand discovery tools, and circular fashion funds. Capital is moving toward platforms that can improve listing quality, authentication, payments, logistics, resale discovery, and seller trust.

In April 2026, Vinted completed a EUR 880 million secondary share transaction at an EUR 8 billion equity valuation. The transaction was led by EQT, Schroders Capital, and Teachers’ Venture Growth, with participation from BlackRock funds, Lombard Odier, Pinegrove Opportunity Partners, and Baillie Gifford. Vinted reported EUR 10.8 billion in GMV, EUR 1.1 billion in annual revenue, and EUR 62 million in net profit in 2025. This reflects strong investor confidence in large-scale C2C second-hand marketplaces with integrated payments and shipping infrastructure.

In February 2026, eBay agreed to acquire Depop from Etsy for about USD 1.2 billion in cash. Depop generated around USD 1 billion in gross merchandise sales in 2025, with nearly 60% year-over-year growth in the U.S. The platform had 7 million active buyers, nearly 90% of whom were under 34, and more than 3 million active sellers. This deal strengthens eBay’s position in Gen Z resale, circular fashion, and consumer-to-consumer apparel commerce.

Naver agreed to acquire Poshmark for an enterprise value of about USD 1.2 billion. Poshmark is a social commerce marketplace for new and second-hand style, with strong user engagement across apparel resale. The deal was positioned around technology investment, international expansion, AI recommendation tools, and community-led commerce. This acquisition remains one of the most important strategic investments in social resale and second-hand apparel platforms.

By Product Type

Tops and T-shirts led the product type segment with 39.2% share, supported by high purchase frequency, affordable pricing, and strong demand for casual and everyday second-hand clothing. These items are widely preferred because they are easy to style, simple to resell, and suitable for regular use across different age groups.

The segment is also supported by frequent wardrobe refresh cycles and strong availability across resale channels. Tops and T-shirts remain among the most accessible second-hand apparel categories because buyers can easily assess design, fabric condition, and usability before purchase.

By Category

Women’s wear accounted for 55.5% share by category, driven by wider product availability, higher fashion rotation, and growing consumer preference for affordable branded and vintage apparel. This category benefits from a broad product mix, including tops, dresses, jackets, casualwear, occasionwear, and seasonal clothing.

The growth of women’s wear can also be linked to stronger resale supply and frequent style changes. Consumers are increasingly using second-hand platforms and thrift outlets to access fashionable clothing at lower prices while supporting more sustainable wardrobe choices.

By Price

Mid-range apparel held 46.1% share in the price segment, supported by strong demand from value-conscious buyers seeking quality clothing at lower prices than new retail products. This segment appeals to consumers who want better fabric quality, recognizable styles, and longer product life without paying premium prices.

The segment is gaining traction because mid-range second-hand apparel offers a balanced mix of affordability and trust. Buyers often prefer this category over very low-cost used clothing when product condition, durability, and brand familiarity are important purchase factors.

By Sales Channel

Offline platforms captured 57.1% share by sales channel, driven by thrift stores, resale boutiques, charity shops, and local second-hand apparel outlets. These channels remain important because consumers can physically check fabric quality, size, fit, color, and garment condition before purchase.

The segment is further supported by the discovery-based shopping experience offered by physical resale stores. Many buyers visit offline outlets to find unique products, vintage styles, and affordable everyday apparel, which keeps store-based second-hand shopping highly relevant.

By Region

North America held the leading regional share of 39.5%, supported by a mature resale culture, strong thrift store networks, rising sustainability awareness, and growing acceptance of pre-owned fashion among younger consumers. The region has a well-developed resale ecosystem across physical stores, consignment outlets, donation-based retail, and digital resale platforms.

The regional lead is also driven by changing consumer attitudes toward second-hand fashion. Younger shoppers are increasingly viewing pre-owned apparel as affordable, practical, and environmentally responsible, which continues to strengthen resale demand across North America.

Competitive Landscape

The Second-Hand Apparel Market is competitive and moderately fragmented, with companies operating across online resale platforms, luxury consignment, peer-to-peer selling, thrift retail, and curated vintage fashion. ThredUp Inc., The RealReal Inc., Vinted, Poshmark Inc., Vestiaire Collective, eBay Inc., Depop, Mercari Inc., Goodwill Industries International, Buffalo Exchange, Crossroads Trading Co., Swap.com, Goodfair, Beyond Retro, and other key players compete through product variety, pricing, seller convenience, authentication, brand trust, and customer experience.

Digital resale platforms such as ThredUp, Vinted, Poshmark, Depop, Mercari, and eBay focus on broad product access, easy listing tools, mobile-first shopping, and strong buyer-seller networks. Luxury-focused players such as The RealReal and Vestiaire Collective compete through authentication, premium brand selection, curated collections, and trust-led resale experiences. These companies are strengthening their position by improving search tools, personalization, logistics support, product verification, and user engagement.

Offline and hybrid players such as Goodwill Industries International, Buffalo Exchange, Crossroads Trading Co., Goodfair, Beyond Retro, and Swap.com continue to hold strong relevance through local sourcing, donation-based supply, curated store formats, affordable pricing, and loyal customer communities. Competition is expected to remain active as resale becomes more accepted among mainstream consumers, while brands and retailers increase their focus on circular fashion, recommerce partnerships, and sustainable apparel models.

Market Concentration: Medium

The Second-Hand Apparel Market shows a medium level of market concentration because demand is spread across online resale platforms, thrift stores, consignment retailers, social commerce sellers, brand-owned resale programs, and local offline channels. Large digital marketplaces have strong reach, but no single player controls the full resale ecosystem.

eBay reported 135 million active buyers and 2.5 billion live listings globally at the end of 2025, while ThredUp reported 1.65 million active buyers and 6.08 million orders in 2025, showing that scaled platforms are gaining influence without making the market highly consolidated. The concentration level is also shaped by category specialization. Luxury resale platforms focus on authenticated designer goods, general marketplaces support mass resale, and peer-to-peer apps attract individual sellers with low entry barriers.

Vestiaire Collective lists 3 million items across more than 12,000 brands, while Vinted generated €1.1 billion in 2025 revenue and expanded across 26 countries, reflecting stronger platform scale in selected regions and price segments. However, the large number of independent sellers, local thrift networks, and brand-led recommerce programs keeps competition broad and fragmented.

Recent Developments

In 2026, Zalando partnered with Vestiaire Collective to bring authenticated second-hand luxury fashion to customers across 14 European markets. The assortment includes ready-to-wear, footwear, handbags, and accessories from more than 50 luxury brands, making resale more visible inside a mainstream fashion platform.

In 2026, ThredUp reported stronger resale platform activity in its first quarter results. Revenue reached USD 81.7 million, up 15% year over year, while active buyers increased 25% to 1.71 million. This indicates that online thrift and managed resale models are gaining stronger consumer traction.

In 2026, The RealReal reported first quarter GMV of USD 606 million, up 24% from the same period in 2025. Total revenue rose 19% to USD 190 million, while trailing twelve-month active buyers reached 1.08 million. This shows stronger demand for authenticated luxury resale and consignment-led apparel platforms.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

People Also Ask

What is the Second-Hand Apparel Market?

The Second-Hand Apparel Market includes the buying and selling of pre-owned clothing through thrift stores, resale boutiques, charity shops, online marketplaces, social commerce platforms, and brand-led resale programs. It covers used tops, T-shirts, denim, dresses, jackets, footwear, accessories, luxury resale, vintage apparel, and refurbished clothing.

How big is the Second-Hand Apparel Market?

The Global Second-Hand Apparel Market was worth USD 245.3 billion in 2025 and reached USD 285.6 billion in 2026. The market is expected to reach USD 647.9 billion by 2035, growing at a CAGR of 10.2% from 2025 to 2035.

What is driving the growth of the Second-Hand Apparel Market?

The growth of the market can be attributed to affordability, sustainability awareness, social commerce, inflation-led value shopping, and higher acceptance of pre-owned fashion among younger buyers. Resale is also expected to grow faster than overall apparel retail because consumers are becoming more comfortable buying used clothing online.

Why are consumers buying second-hand apparel?

Consumers are buying second-hand apparel to save money, access branded clothing at lower prices, find unique fashion, and reduce waste. In 2025, Vinted reported that buyers saved EUR 21.6 billion on adult fashion compared with original retail prices, while average fashion items on the platform were 72% lower than original retail prices.

How important are Gen Z and millennials in the Second-Hand Apparel Market?

Gen Z and millennials are major demand drivers because they are more comfortable with app-based resale, social shopping, vintage fashion, and sustainability-led purchasing. A 2026 resale report stated that these two groups are expected to drive more than 70% of market growth through 2030.

What is the future outlook for the Second-Hand Apparel Market?

The outlook remains positive as resale becomes a regular part of fashion shopping. Growth is expected to be supported by value-conscious buyers, social commerce, AI-led product discovery, brand-owned resale programs, and stronger circular fashion policies. In Europe, rising textile consumption and low separate collection rates continue to support policy interest in reuse and recycling