Revenue, 2025

$19.6 Bn

Forecast, 2035

$262.7Bn

CAGR, 2025-2035

29.6%

Report Coverage

Global

Market Size and Forecast

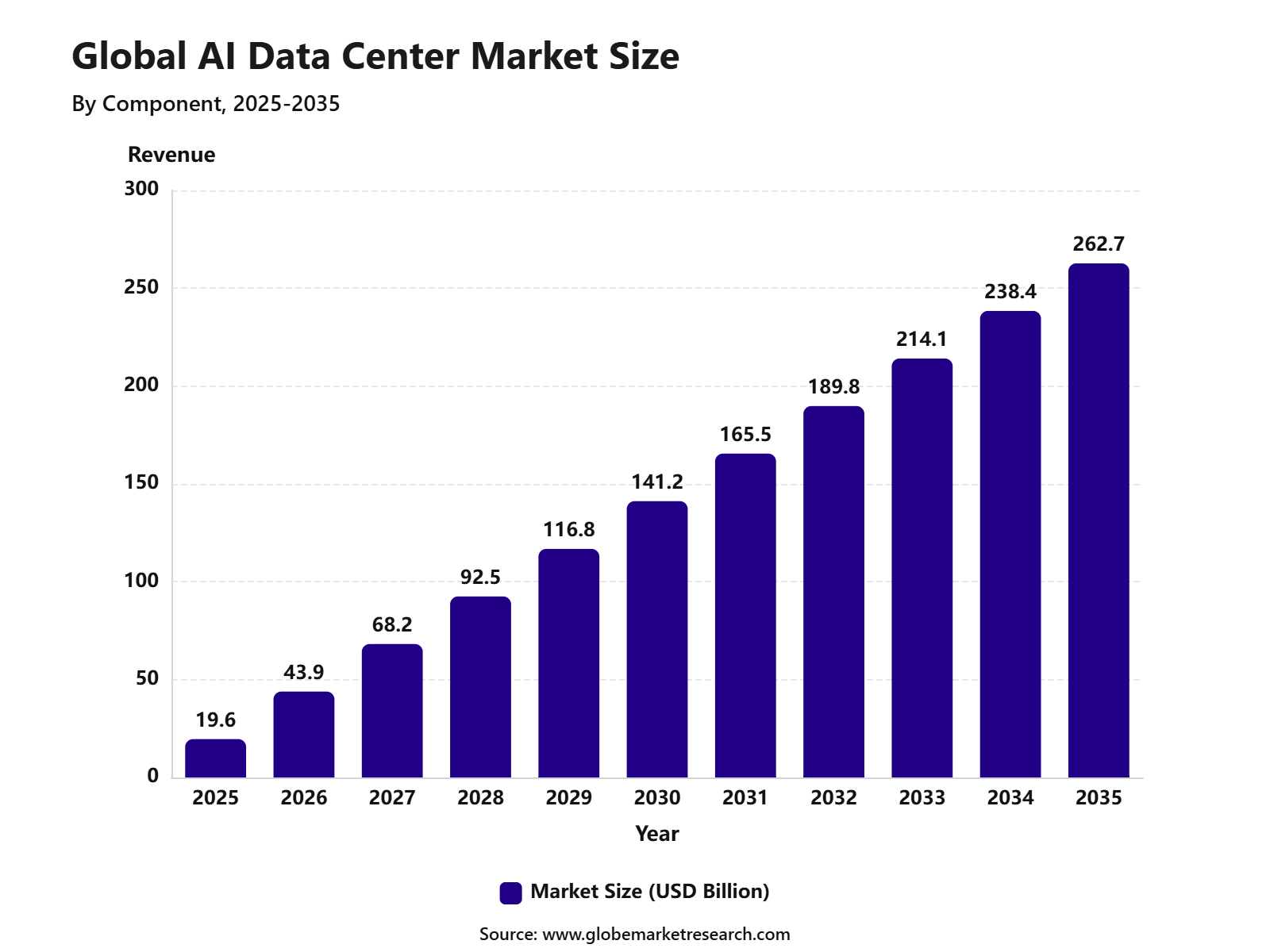

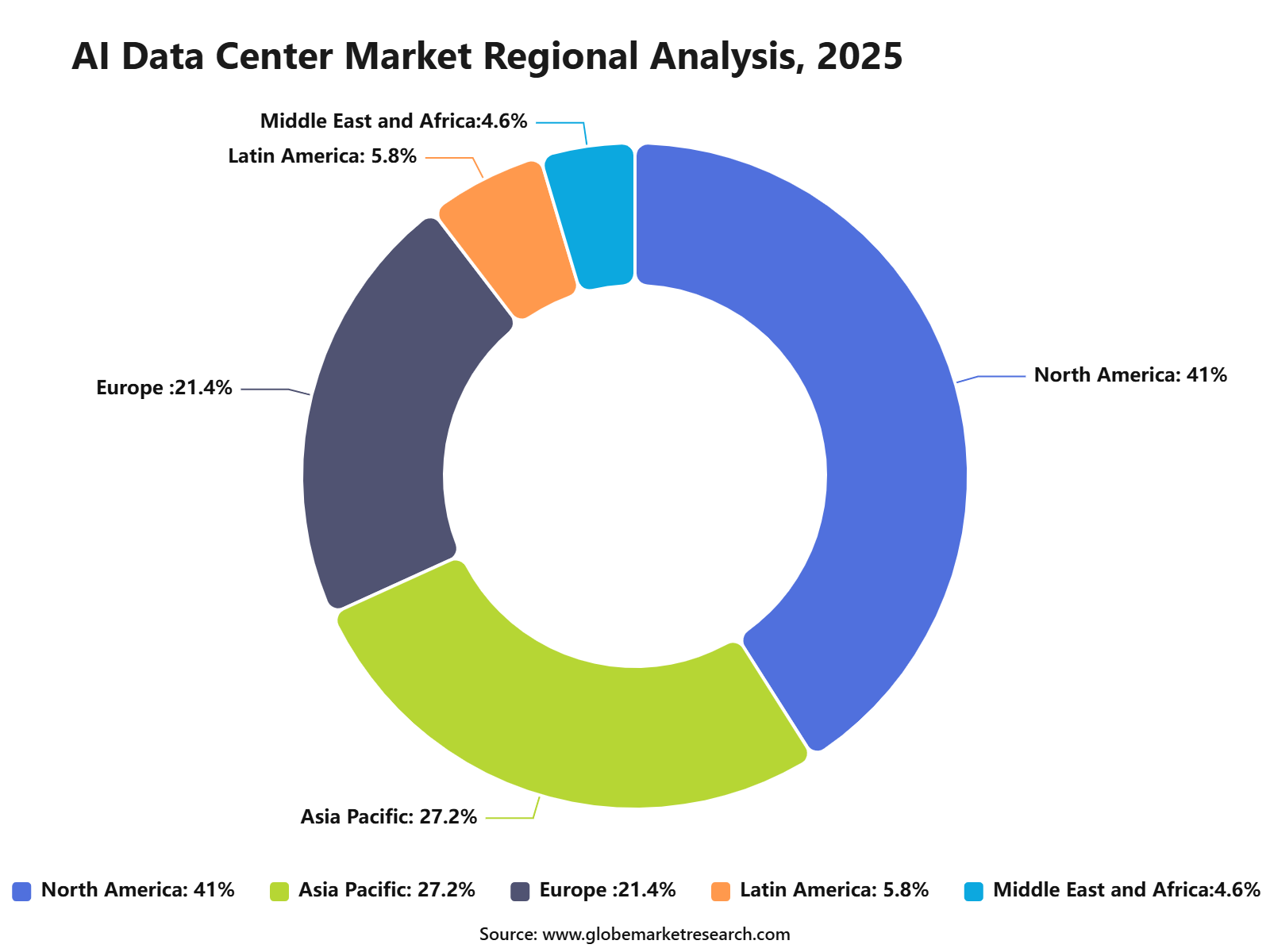

The global AI Data Center Market size was valued at USD 19.6 billion in 2025 and is projected to grow from USD 24.8 billion in 2026 to USD 262.7 billion by 2035, registering a CAGR of 29.6% from 2025 to 2035. North America dominated the market with a revenue share of 41% in 2025. The market growth is supported by rising demand for high-performance computing infrastructure, rapid adoption of generative AI, increasing deployment of cloud-based AI workloads, and growing investments in advanced data center capacity by technology companies, enterprises, and hyperscale cloud providers.

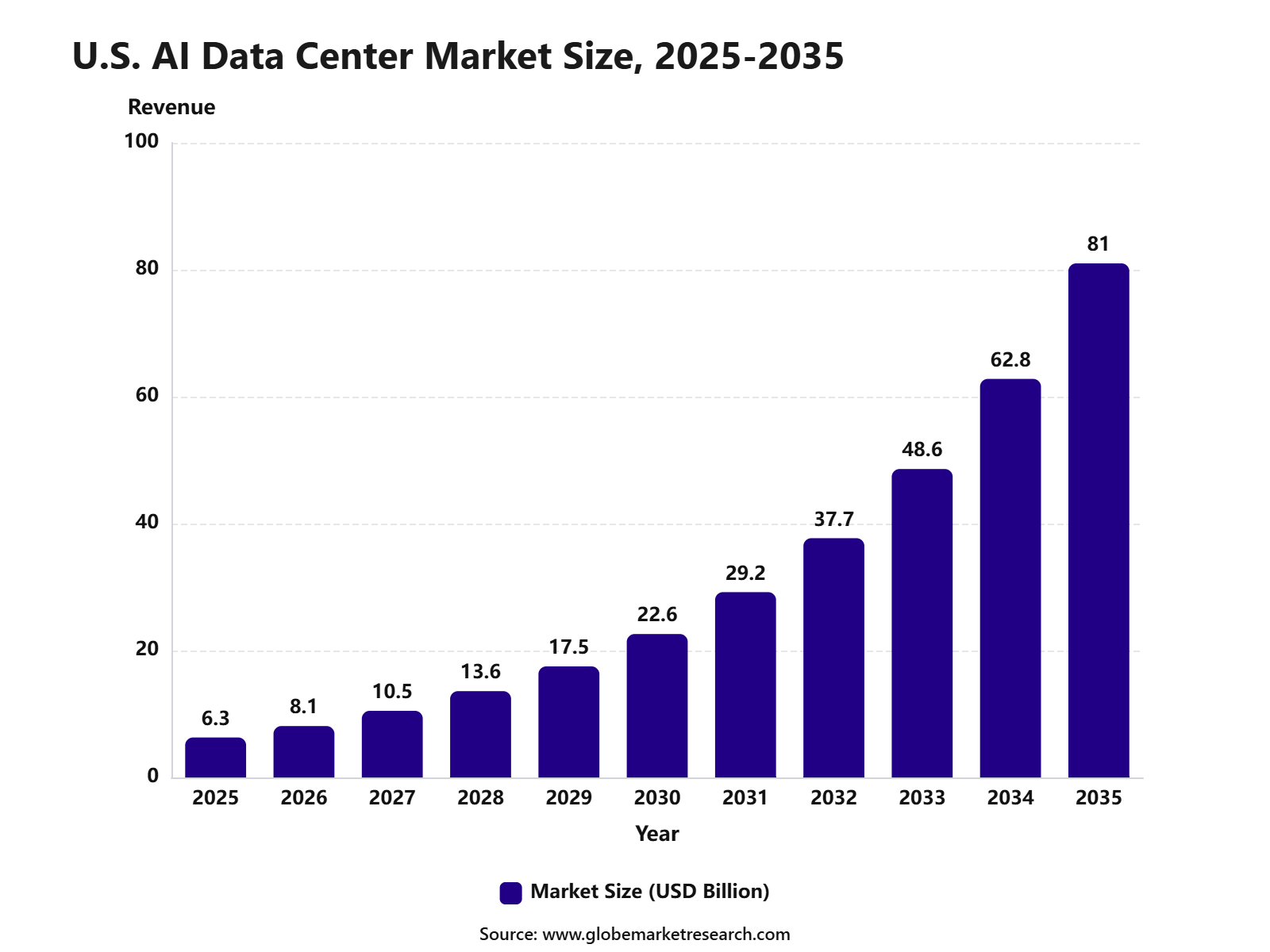

The U.S. AI Data Center Market was valued at USD 6.3 billion in 2025 and is projected to expand at a CAGR of 29.1% from 2025 to 2035, driven by rising demand for AI model training, generative AI workloads, cloud AI services, high-performance computing, and enterprise AI deployment. Investment activity remains strong across the global AI data center ecosystem as cloud providers, colocation companies, chip manufacturers, and enterprises focus on expanding compute capacity, improving energy efficiency, and supporting large-scale AI workloads.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Insights

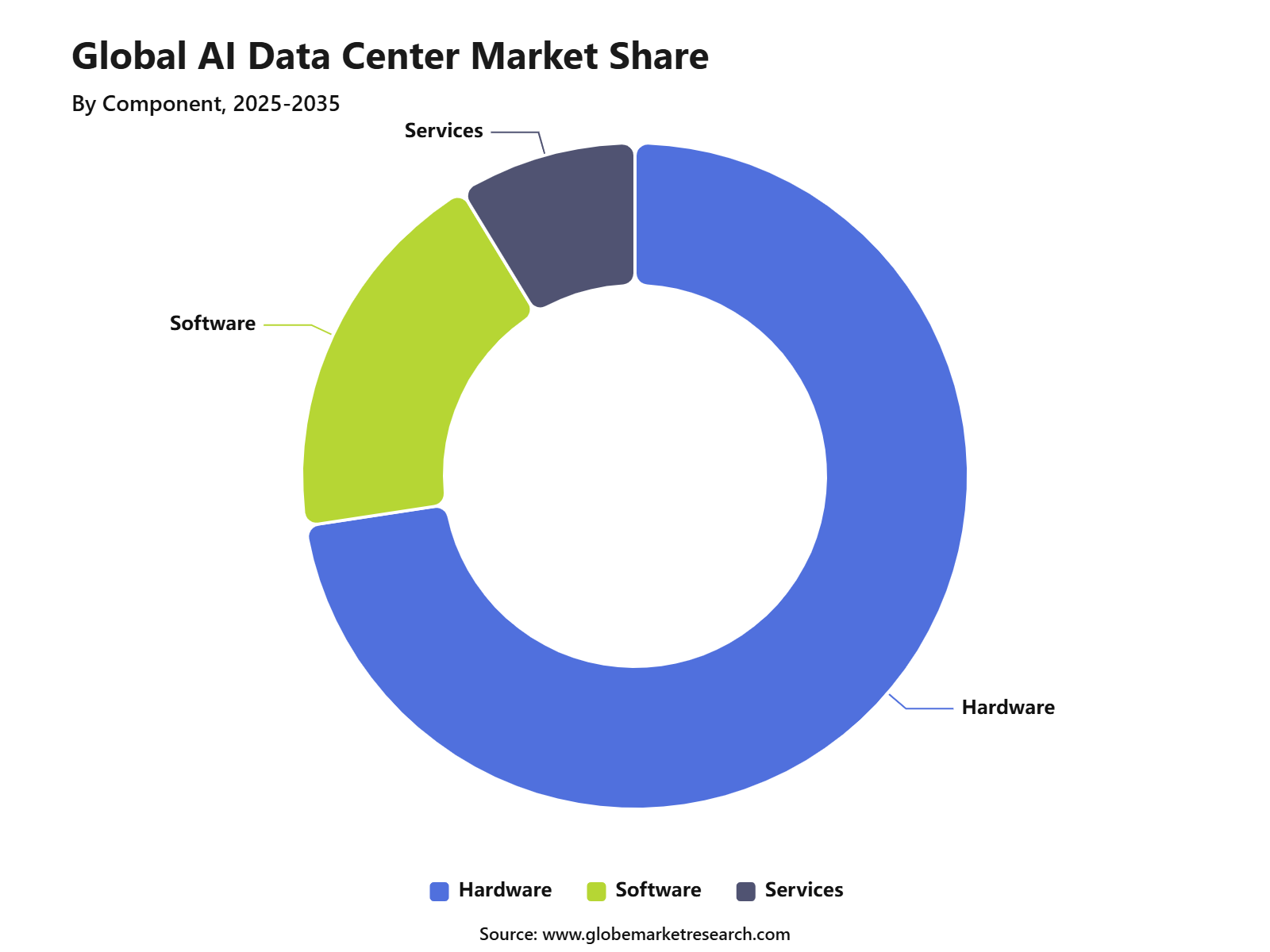

Hardware led the component segment with 72.6% share. Demand was supported by rising investment in GPUs, AI accelerators, high-performance servers, storage systems, networking equipment, and advanced power and cooling infrastructure.

Servers accounted for 41.8% share by infrastructure. The segment remained dominant as AI workloads require high-density computing capacity, fast processing speed, and scalable server clusters for training and inference operations.

Hyperscale data centers held 48.3% share by data center type. Growth was driven by large cloud providers, AI model developers, and enterprises expanding massive computing environments for generative AI and advanced analytics.

Cloud-based deployment captured 56.9% share. Adoption increased as businesses preferred flexible computing capacity, faster AI workload scaling, lower upfront infrastructure burden, and easier access to advanced AI platforms.

Generative AI led the technology segment with 34.7% share. The segment gained strong traction due to rising demand for large language models, image generation, code generation, synthetic data creation, and enterprise AI applications.

AI model training accounted for 38.5% share by application. Growth was supported by the need for large computing clusters, high-speed data processing, and continuous training of complex AI models across industries.

IT and telecommunications led the end-use vertical with 32.4% share. Demand was driven by cloud service expansion, network automation, data traffic growth, edge AI deployment, and higher use of AI for enterprise digital services.

Market Overview

The AI data center market refers to infrastructure designed to support artificial intelligence workloads such as machine learning training, inference processing, generative AI services, and advanced analytics. These data centers use high‑density compute hardware, accelerated processing units, advanced cooling systems, and large‑capacity storage to handle complex AI operations. AI data centers are used by cloud providers, research institutions, enterprises, and technology platforms requiring high‑performance computing at scale.

One of the biggest drivers of the AI data center market is the rapid increase in AI adoption across industries. Organizations are embedding AI into operations such as predictive maintenance, personalized services, automated decision‑making, and real‑time analytics. AI adoption has expanded significantly, with global enterprise AI deployment rates estimated to grow by more than 30% annually, driving demand for specialized data center capacity.

Organizations adopt AI data center infrastructure primarily to support the computational intensity of modern AI applications. AI model training, especially for deep neural networks and large language models, can require 100-1000 times more compute power than traditional analytics workloads, making general‑purpose infrastructure insufficient. Purpose‑built AI data centers provide the scale and performance needed to run these workloads effectively.

Customer Acquisition Strategy

The AI data center market is being sold less as a simple hosting or server capacity business and more as a power-secured infrastructure business. Buyers now assess megawatts, grid access, GPU availability, cooling design, latency, and long-term expansion rights before signing large contracts. This is supported by the sharp rise in electricity demand, as global data center electricity consumption is projected to reach about 945 TWh by 2030, while accelerated servers driven by AI are expected to grow electricity use by around 30% annually. In the U.S., data centers used about 176 TWh in 2023 and could reach 325 to 580 TWh by 2028, equal to about 6.7% to 12% of total U.S. electricity use.

Sales economics are being shaped by tight supply and high-density demand. According to CBRE, In North American primary markets, data center supply reached 8,155 MW in H1 2025, but vacancy fell to only 1.6%, showing that new capacity is being absorbed quickly. Larger 10 MW-plus deployments saw pricing increases of up to 19%, while 74.3% of under-construction capacity was already preleased, mainly due to demand from cloud and AI users. Construction cost pressure is also significant, with average global data center shell and core construction cost forecast at USD 11.3 million per MW in 2026, while AI-related technology fit-out can cost up to USD 25 million per MW.

Tariff Impact

Tariffs are becoming a direct cost risk for AI data center developers because the sector depends heavily on imported metals, power equipment, semiconductor components, servers, cooling systems, and advanced chips. In June 2026, the U.S. adjusted tariffs on aluminum, steel, and copper, with 50% duty on products made of those metals, 25% duty on certain derivative products, and a temporary 15% duty on selected fixed industrial machinery and power equipment. The White House also announced a 25% tariff on a narrow category of semiconductors in January 2026, while indicating that broader semiconductor tariffs could be considered after trade negotiations.

The impact is important because AI data centers are semiconductor-heavy assets. A 2026 policy analysis estimated that the U.S. is on track to invest more than USD 2.7 trillion in data center infrastructure by 2030, with semiconductors representing about 54 cents of every dollar spent. Under current metal tariff exposure, the additional cost was estimated at about USD 48 million for a USD 1 billion facility and around USD 130 billion across a USD 2.7 trillion buildout. A broader semiconductor tariff scenario would be more severe, with a 25% tariff on all semiconductors and chip-embedded products adding about USD 360 billion, a 50% tariff adding USD 720 billion, and a 100% tariff adding USD 1.44 trillion in extra cost.

Revenue Potential Analysis

Revenue Landscape Across

The AI data center market has strong revenue potential across hardware, cloud infrastructure, colocation capacity, power systems, cooling equipment, networking, storage, and managed services. The revenue pool is expected to remain hardware-heavy in the near term because GPUs, accelerators, servers, switches, storage systems, and liquid cooling units carry high upfront spending. NVIDIA reported record Data Center revenue of USD 75.2 billion in Q1 FY2027, up 92% year over year, showing how strongly AI compute demand is flowing into chip and server supply chains.

Revenue is also expanding through cloud and leased capacity models, where AI companies, enterprises, and hyperscalers pay for ready power, high-density racks, and GPU-enabled compute rather than building everything internally. Microsoft reported Microsoft Cloud revenue of USD 54.5 billion in Q3 FY2026, up 29%, while Azure and other cloud services revenue increased 40%, showing that AI workloads are already supporting strong cloud consumption growth. In North America, primary data center supply reached 8,155 MW in H1 2025, but vacancy dropped to only 1.6%, while 74.3% of under-construction capacity was already preleased.

Financial Impact

The financial impact of AI data centers is capital-intensive but revenue-positive for companies that can secure capacity early. High-density AI deployments are raising lease rates, with CBRE reporting that pricing for large 10 MW-plus deployments increased by up to 19% in H1 2025 due to tight supply, higher build-out costs, and strong demand from cloud and AI tenants. This supports stronger revenue per MW for colocation and wholesale data center operators. However, it also increases entry barriers because developers must finance land, power connections, substations, cooling systems, backup power, security, and advanced server infrastructure before revenue is fully realized.

Component Analysis

Hardware led the AI Data Center Market with 72.6% share, supported by strong demand for GPUs, AI accelerators, servers, storage systems, networking equipment, cooling systems, and power infrastructure. AI workloads require high-performance computing capacity, which makes hardware the largest spending area in data center development.

The growth of this segment can be attributed to the rapid adoption of generative AI, large language models, machine learning training, and high-density computing. Data center operators are investing heavily in advanced chips, high-bandwidth networking, liquid cooling, and power distribution systems to support AI workloads. Hardware is expected to remain the leading component as enterprises and cloud providers continue to expand AI compute capacity. Demand will remain strong for AI servers, accelerator chips, rack-scale systems, advanced cooling, storage clusters, and energy-efficient infrastructure.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFInfrastructure Analysis

Servers accounted for 41.8% share in the AI Data Center Market, making them the leading infrastructure segment. AI servers are critical because they host high-performance processors, accelerators, memory, and storage systems needed for model training, inference, analytics, and enterprise AI applications. The segment is growing as AI workloads require higher compute density and faster processing than traditional enterprise workloads.

Servers designed for AI are being built with GPUs, tensor processors, advanced memory, high-speed interconnects, and improved thermal management. Server demand is expected to stay strong as AI adoption increases across cloud services, software platforms, healthcare, finance, telecom, manufacturing, and public sector applications. Providers that deliver scalable, energy-efficient, and high-density AI server systems are likely to gain stronger demand.

Data Center Type Analysis

Hyperscale data centers held 48.3% share, supported by large-scale AI computing needs, cloud platform expansion, and growing demand for model training and inference capacity. These facilities are designed to support massive compute, storage, networking, and power requirements. The growth of hyperscale data centers is being driven by cloud providers, AI model developers, large enterprises, and digital platform companies.

Hyperscale facilities offer economies of scale, advanced automation, high server density, and stronger ability to support large AI workloads. This segment is expected to remain dominant as AI systems continue to require larger compute clusters and faster data processing. Future investments are likely to focus on high-density campuses, liquid cooling, renewable power sourcing, grid access, and advanced AI infrastructure management.

Deployment Mode Analysis

Cloud-based deployment accounted for 56.9% share, supported by strong enterprise demand for scalable AI infrastructure without heavy upfront investment. Cloud platforms allow companies to access AI compute, storage, development tools, and model deployment services through flexible usage-based models. The growth of cloud-based AI data centers is being driven by businesses that need fast access to GPUs, AI platforms, and managed infrastructure.

Cloud deployment helps enterprises avoid complex hardware ownership while supporting model training, inference, analytics, automation, and application development. Cloud-based deployment is expected to remain a leading model as more companies adopt AI across daily operations. Demand will remain strong for cloud AI clusters, managed machine learning platforms, AI-as-a-service offerings, and secure enterprise AI environments.

Technology Analysis

Generative AI led the technology segment with 34.7% share, supported by rising demand for large language models, image generation, code generation, enterprise copilots, synthetic data, search tools, and automation systems. Generative AI workloads require intensive computing capacity, which increases demand for advanced data center infrastructure. The segment is expanding because companies are deploying generative AI across customer service, content creation, software development, research, marketing, legal operations, and business productivity.

These applications require strong server capacity, high-speed networking, advanced storage, and reliable cooling systems. Generative AI is expected to remain a major growth driver for AI data centers. As models become larger and enterprise use cases expand, demand will increase for high-performance hardware, scalable cloud infrastructure, energy-efficient compute, and secure AI deployment environments.

Application Analysis

AI model training accounted for 38.5% share, making it the leading application segment. Training large AI models requires high compute power, large datasets, advanced accelerators, fast storage, and high-bandwidth networking, which makes it one of the most infrastructure-intensive AI workloads. The growth of this segment is being driven by large language models, multimodal AI, recommendation engines, autonomous systems, scientific computing, and enterprise-specific AI models.

Organizations are investing in training infrastructure to improve model accuracy, domain relevance, and competitive capability. AI model training is expected to remain a high-value application area, especially among cloud providers, AI labs, research institutions, and large enterprises. However, rising power consumption and hardware costs are increasing demand for optimized training methods, efficient chips, and better workload management.

End Use Vertical Analysis

IT and telecommunications led the end-use vertical segment with 32.4% share, supported by strong demand for cloud services, network automation, AI-powered customer support, cybersecurity, data analytics, and digital infrastructure management. These industries are among the earliest adopters of AI because they handle large data volumes and complex digital operations. The segment is growing as telecom companies use AI to optimize networks, predict outages, manage traffic, improve customer service, and support 5G and edge computing services.

IT companies are also using AI data centers to support software development, enterprise platforms, cloud applications, and managed AI services. IT and telecommunications are expected to remain leading end users as AI becomes more important to digital services and network performance. Demand is likely to grow for AI-ready cloud infrastructure, edge data centers, network AI platforms, cybersecurity AI systems, and high-performance compute services.

Regional Analysis

North America dominated the AI data center market with a revenue share of 41% in 2025. The region’s leadership was supported by strong cloud infrastructure, high AI model training demand, advanced semiconductor access, and large-scale investments by technology companies. The U.S. remained the main contributor due to its strong base of hyperscale data centers, enterprise AI adoption, and advanced digital infrastructure. The presence of major cloud platforms, chip suppliers, AI software companies, and colocation providers has strengthened the region’s position.

The growth of North America can also be linked to rising demand for high-performance computing, generative AI workloads, and real-time data processing. Data center operators are expanding capacity to support AI training, AI inference, cloud applications, and enterprise automation. The International Energy Agency reported that electricity demand from data centers rose by 17% in 2025, while AI-focused data centers grew even faster than the broader data center segment. This shows that AI workloads are becoming a major force behind regional infrastructure expansion.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe U.S. AI data center market was valued at USD 6.3 billion in 2025 and is projected to expand at a CAGR of 29.1% from 2025 to 2035. The country is expected to remain the leading national market because it has strong demand from cloud service providers, AI developers, government workloads, financial institutions, healthcare companies, and large enterprises. The U.S. also benefits from a mature colocation industry, strong venture funding, and a large base of AI model development activity. Growth is being supported by the need for advanced servers, liquid cooling, high-density racks, and reliable power systems.

Power availability is becoming one of the most important factors shaping the U.S. AI data center market. The IEA has stated that the United States and China are expected to account for nearly 80% of global data center electricity consumption growth to 2030. In the U.S., data center electricity consumption is projected to increase by around 240 TWh from the 2024 level by 2030. This is creating strong demand for grid upgrades, on-site power generation, renewable procurement, and better energy management systems.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRisk Factors & Market Barriers

Regulatory & Compliance Risks

The AI data center market faces rising regulatory pressure linked to energy use, grid impact, water consumption, carbon emissions, cybersecurity, data protection, and export controls. As AI workloads grow, governments and regulators are paying closer attention to how data centers affect electricity supply, local communities, and environmental targets.

Energy reporting rules are becoming stricter in major regions. In Europe, data centers with an installed IT power demand of at least 500 kW are required to report annual energy performance data. This increases the need for accurate tracking of power usage, cooling efficiency, renewable energy use, and water consumption.

Environmental compliance is becoming a major project risk. Large AI data centers may face permitting delays if local authorities are concerned about power demand, water usage, land use, noise, emissions, or grid reliability. Operators must show clear plans for energy sourcing, heat management, water conservation, and community impact.

Market Adoption Barriers

High capital cost is the biggest adoption barrier in the AI data center market. AI-ready facilities require expensive GPUs, servers, power systems, cooling equipment, buildings, grid upgrades, backup systems, and skilled engineering teams. Smaller enterprises may avoid building private AI data centers and instead use cloud or colocation services.

Power availability is another major barrier. AI data centers need large and stable electricity supply, but grid connections can take years in some locations. Limited transformer supply, slow permitting, transmission congestion, and rising electricity demand can delay projects and increase costs.

Hardware supply constraints can slow market growth. Demand for GPUs, high-bandwidth memory, advanced networking, power equipment, and liquid cooling components remains high. Any shortage can raise prices, extend delivery timelines, and affect project schedules.

Segment Covered in Report

By Component

Hardware

Software

Services

By Infrastructure

Servers

Storage Systems

Networking Equipment

Power and Cooling Systems

Security Infrastructure

Others

By Data Center Type

Hyperscale Data Centers

Colocation Data Centers

Enterprise Data Centers

Edge Data Centers

By Deployment Mode

On-Premise

Cloud-Based

Hybrid

By Technology

Machine Learning

Deep Learning

Generative AI

Natural Language Processing

Computer Vision

Predictive Analytics

Others

By Application

AI Model Training

AI Inference

Data Processing and Analytics

High-Performance Computing

Cloud AI Services

Automation and Monitoring

Others

By End Use Vertical

BFSI

Healthcare and Life Sciences

IT and Telecommunications

Retail and E-Commerce

Automotive

Manufacturing

Government and Public Sector

Media and Entertainment

Energy and Utilities

Others

By Region

Asia Pacific

North America

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for generative AI training and inference workloads | +3.4% | High in North America, Europe, China, Japan, South Korea, and India | Increases demand for high-density data centers built for GPUs, accelerators, fast networking, and large-scale storage. |

Expansion of hyperscale cloud infrastructure | +3.0% | Strong in the U.S., Western Europe, China, India, Singapore, and the Middle East | Supports large AI cluster deployment for cloud AI services, enterprise AI platforms, and model hosting. |

Growing enterprise adoption of AI applications | +2.7% | High across BFSI, healthcare, retail, manufacturing, telecom, and government sectors | Drives demand for AI-ready colocation, private cloud, and hybrid data center capacity. |

Increasing use of high-performance GPUs and AI accelerators | +2.5% | Strong in advanced digital economies and semiconductor supply hubs | Raises demand for advanced power distribution, high-speed interconnects, liquid cooling, and dense server racks. |

Rising need for low-latency AI inference | +2.1% | High in North America, Asia Pacific, and telecom-led edge markets | Supports regional and edge AI data center growth for real-time applications such as autonomous systems, fraud detection, robotics, and voice AI. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Power availability and grid connection delays | -2.8% | High in the U.S., Ireland, U.K., Germany, Singapore, and India | Delays new AI data center projects where grid capacity, transmission access, and utility approvals are limited. |

High capital expenditure for AI-ready facilities | -2.4% | Strong impact across emerging markets and smaller operators | Restricts market entry because GPU clusters, liquid cooling, electrical systems, and backup power require heavy upfront investment. |

Shortage of advanced AI chips and critical components | -2.0% | Global relevance, with high impact in import-dependent markets | Slows deployment schedules for AI clusters and increases procurement costs for servers, GPUs, memory, and networking equipment. |

Rising energy cost and sustainability pressure | -1.8% | High in Europe, North America, Japan, Singapore, and Australia | Reduces margin stability and increases pressure to use renewable power, efficient cooling, and better workload scheduling. |

Land, water, and local approval constraints | -1.5% | Strong in dense urban hubs and water-stressed regions | Limits site selection and increases permitting risk for large-scale AI campuses and hyperscale expansions. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth of liquid cooling and advanced thermal management | +2.6% | High in North America, Europe, China, Japan, South Korea, and the Middle East | Creates strong demand for direct-to-chip cooling, immersion cooling, rear-door heat exchangers, and high-density rack design. |

Expansion of AI-focused colocation services | +2.3% | Strong in the U.S., Europe, India, Southeast Asia, and GCC countries | Opens revenue opportunities for operators offering GPU-ready capacity, high power density, secure connectivity, and managed infrastructure. |

Renewable energy and on-site power integration | +2.0% | High in the U.S., Europe, Middle East, Australia, and India | Supports data center growth through power purchase agreements, solar, wind, fuel cells, battery storage, and microgrid models. |

Edge AI data center development | +1.8% | High in telecom-heavy markets, smart cities, and industrial hubs | Enables low-latency AI workloads for autonomous vehicles, robotics, surveillance analytics, AR/VR, and real-time decision systems. |

AI infrastructure modernization in emerging economies | +1.6% | Strong in India, Southeast Asia, Latin America, and the Middle East | Supports new investment in sovereign AI, public cloud regions, enterprise AI platforms, and digital government infrastructure. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Managing extreme rack power density | -2.3% | High in hyperscale and AI training clusters worldwide | Creates design pressure on cooling systems, electrical distribution, floor loading, and maintenance workflows. |

Balancing fast AI demand with infrastructure build timelines | -2.0% | High in North America, Europe, and Asia Pacific | Creates capacity shortages because data center construction, power procurement, and utility upgrades take longer than AI workload growth. |

Ensuring energy efficiency under heavy AI workloads | -1.8% | Strong in regions with high electricity costs and sustainability rules | Requires better PUE performance, efficient cooling, dynamic workload placement, and optimized server utilization. |

Managing grid stability and peak power demand | -1.6% | High in data center clusters such as Northern Virginia, Ireland, Singapore, and major Asian hubs | Raises risks around power curtailment, connection delays, local opposition, and higher utility charges. |

Cybersecurity and data sovereignty risks | -1.3% | High in government, BFSI, healthcare, defense, and regulated enterprise markets | Increases demand for secure AI infrastructure, regional hosting, access controls, encryption, and compliance-ready architecture. |

Recent Development

NVIDIA Corporation, January 2026 - NVIDIA launched the Rubin platform, including six new chips designed to support next-generation AI supercomputers and large-scale AI data center infrastructure.

Intel Corporation, April 2026 - Intel deepened its collaboration with Google Cloud to support AI, inference, and general-purpose workloads using Intel Xeon processors and custom infrastructure processing units.

Dell Technologies Inc., March 2026 - Dell expanded the Dell AI Factory with NVIDIA, adding enterprise AI infrastructure, data orchestration, high-performance storage, and new NVIDIA-powered server platforms for large-scale AI workloads.

Hewlett Packard Enterprise Company, March 2026 - HPE introduced new NVIDIA-powered AI infrastructure innovations, including Blackwell-based ProLiant server support for edge AI, small language models, vector databases, and analytics workloads.

Cisco Systems, Inc., June 2026 - Cisco positioned its AI-ready data center solutions around secure, scalable infrastructure for AI and traditional workloads, with a focus on higher speed, power, and security requirements

Microsoft Corporation, May 2026 - Microsoft confirmed that its largest India data center was on track to go live by mid-2026, supporting Azure cloud and AI service demand in one of its fastest-growing markets.

Meta Platforms, Inc., June 2026 - Meta partnered with Reliance Industries to lease its first AI-enabled data center in India, located in Jamnagar, Gujarat, to support AI infrastructure closer to a major user base.

Fujitsu Limited, March 2026 - Fujitsu promoted its data center services as foundations for generative AI and digital transformation, supported by major facilities using 100% renewable power for customer systems.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 19.6 Bn |

Forecast Revenue (2035) | USD 262.2 Bn |

CAGR (2025-2035) | 29.6% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Component (Hardware, Software, Services), By Infrastructure (Servers, Storage Systems, Networking Equipment, Power and Cooling Systems, Security Infrastructure, Others), By Data Center Type (Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, Edge Data Centers), By Deployment Mode (On-Premise, Cloud-Based, Hybrid), By Technology (Machine Learning, Deep Learning, Generative AI, Natural Language Processing, Computer Vision, Predictive Analytics, Others), By Application (AI Model Training, AI Inference, Data Processing and Analytics, High-Performance Computing, Cloud AI Services, Automation and Monitoring, Others), By End Use Vertical (BFSI, Healthcare and Life Sciences, IT and Telecommunications, Retail and E-Commerce, Automotive, Manufacturing, Government and Public Sector, Media and Entertainment, Energy and Utilities, Others) By Regional |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | NVIDIA Corporation, Advanced Micro Devices, Inc., Intel Corporation, Broadcom Inc., Dell Technologies Inc., Hewlett Packard Enterprise Company, Super Micro Computer, Inc., Cisco Systems, Inc., Arista Networks, Inc., Juniper Networks, Inc., Lenovo Group Limited, IBM Corporation, Oracle Corporation, Microsoft Corporation, Amazon Web Services, Inc., Google LLC, Meta Platforms, Inc., Equinix, Inc., Digital Realty Trust, Inc., NTT Global Data Centers, Schneider Electric SE, Vertiv Holdings Co., Eaton Corporation plc, ABB Ltd., Legrand SA, Johnson Controls International plc, Fujitsu Limited, Huawei Technologies Co., Ltd., NEC Corporation, Siemens AG |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Broadcom Inc.

Dell Technologies Inc.

Hewlett Packard Enterprise Company

Super Micro Computer, Inc.

Cisco Systems, Inc.

Arista Networks, Inc.

Juniper Networks, Inc.

Google LLC

Amazon Web Services, Inc.

Meta Platforms, Inc.

Siemens AG

Huawei Technologies Co., Ltd.

Fujitsu Limited

Others

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Information and Technology

Debt Collection Agencies Market to hit USD 48.4 billion by 2035

Global Debt Collection Agencies Market Size, Share Analysis By Debt Type (Bad Debt, Early Out Debt), By Agency Type (First-Party Agencies, Third-Party Agencies), By Collection Method (Traditional Collection, Digital Debt Collection, Legal Collection), By Application (Financial Services, Healthcare, Student Loans, Government, Retail, Telecom and Utility, Mortgage, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Operating Room Integration Market to hit USD 10.3 Bn by 2035

Global Operating Room Integration Market Size, Share Report By Component (Software, Hardware, Services), By Device Type (Audio and Video Management Systems, Display Systems, Others), By Application (General Surgery, Orthopedic Surgery, Others), By End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), By Deployment Mode On-premise, Cloud-based, Hybrid), By Operating Room Type (Hybrid Operating Rooms, Integrated Operating Rooms), By Technology (Surgical Workflow Integration, Image and Video Integration, Others), By Regional (North America, Europe, Asia Pacific, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Sharing Economy Apps Market to hit 1,411.2 Bn by 2035

Global Sharing Economy Apps Market By Product / Service Type (Shared Transportation, Shared Space, Sharing Financial, Sharing Food, Shared Healthcare, Shared Knowledge & Education, Shared Task Services, Shared Items, Others), By Distribution Channel (Online, Offline), By End User (Generation Z, Millennials, Generation X, Boomers), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

AI Receptionist Market to hit USD 23.8 Bn by 2035

Global AI Receptionist Market Size, Share Analysis Report By Component (Solutions, Services), By Deployment (Cloud-based, On-premises), By Service Type (Voice Reception Services, Chat Reception Services, Appointment Scheduling, Call Routing, Lead Qualification, Customer Support), By Service Model (24/7 Receptionist Solutions, Business Hours Receptionist Solutions, Hybrid Receptionist Solutions), By Technology (Voice AI Integration, Conversational AI, Natural Language Processing, Speech Recognition and Others), By Enterprise Size (Small and Medium Enterprises, Large Enterprises), By End-use (Healthcare, Legal Services, Real Estate, Retail and E-commerce, BFSI, Hospitality, Automotive, Home Services, IT and Telecom, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035