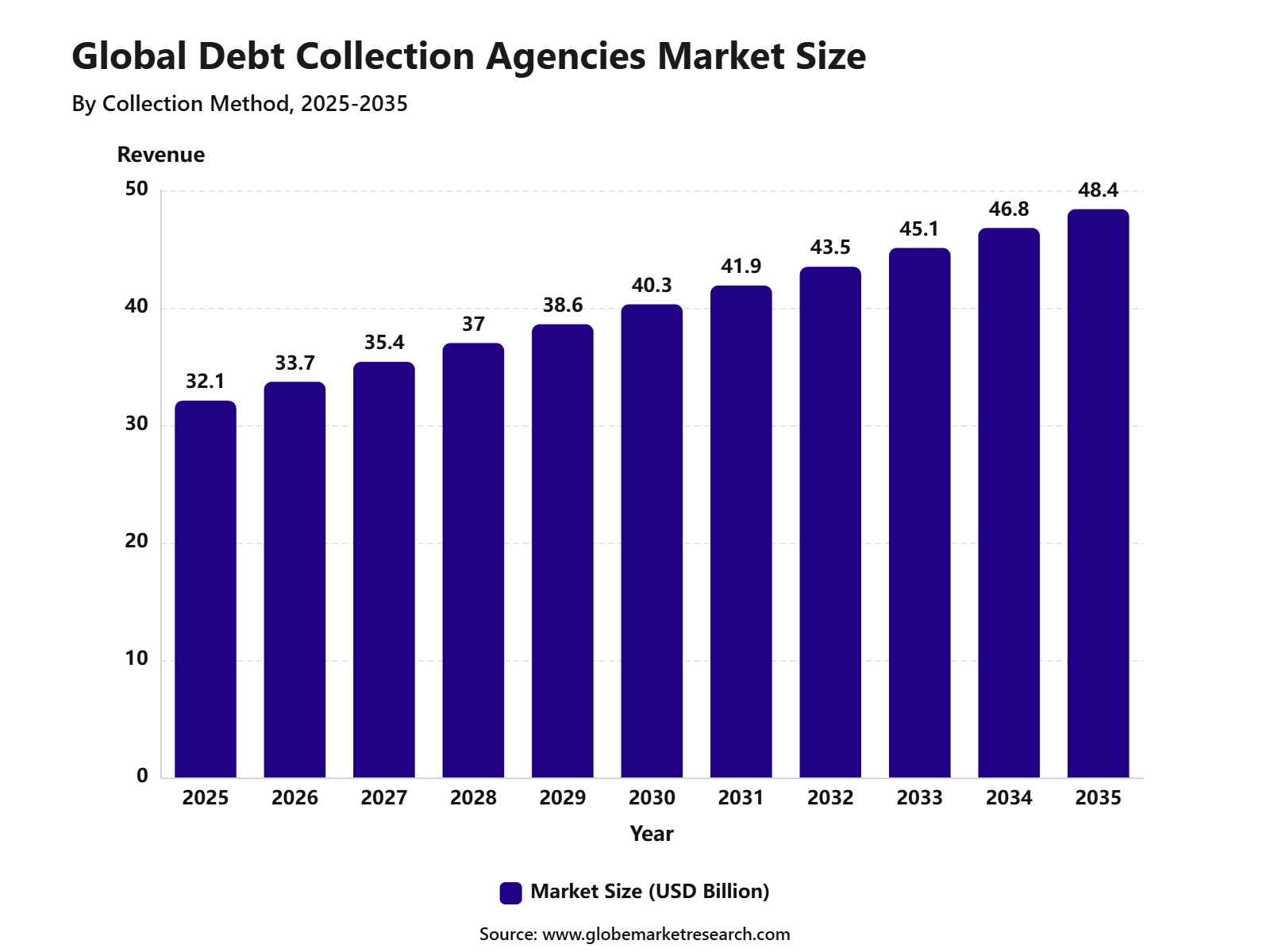

Revenue, 2025

$32.1 Bn

Forecast, 2035

$48.4Bn

CAGR, 2025-2035

4.2%

Report Coverage

Global

Market Size and Forecast

The Global Debt Collection Agencies Market was valued at USD 32.1 billion in 2025 and is projected to attain USD 48.4 billion by 2035, growing at a CAGR of 4.2% from 2025 to 2035. Debt collection agencies help banks, lenders, healthcare providers, telecom companies, utilities, retailers, and government bodies recover overdue payments from consumers and businesses. The market growth is driven by rising consumer debt, higher delinquency levels, demand for outsourced recovery services, and the shift toward compliant digital collection platforms.

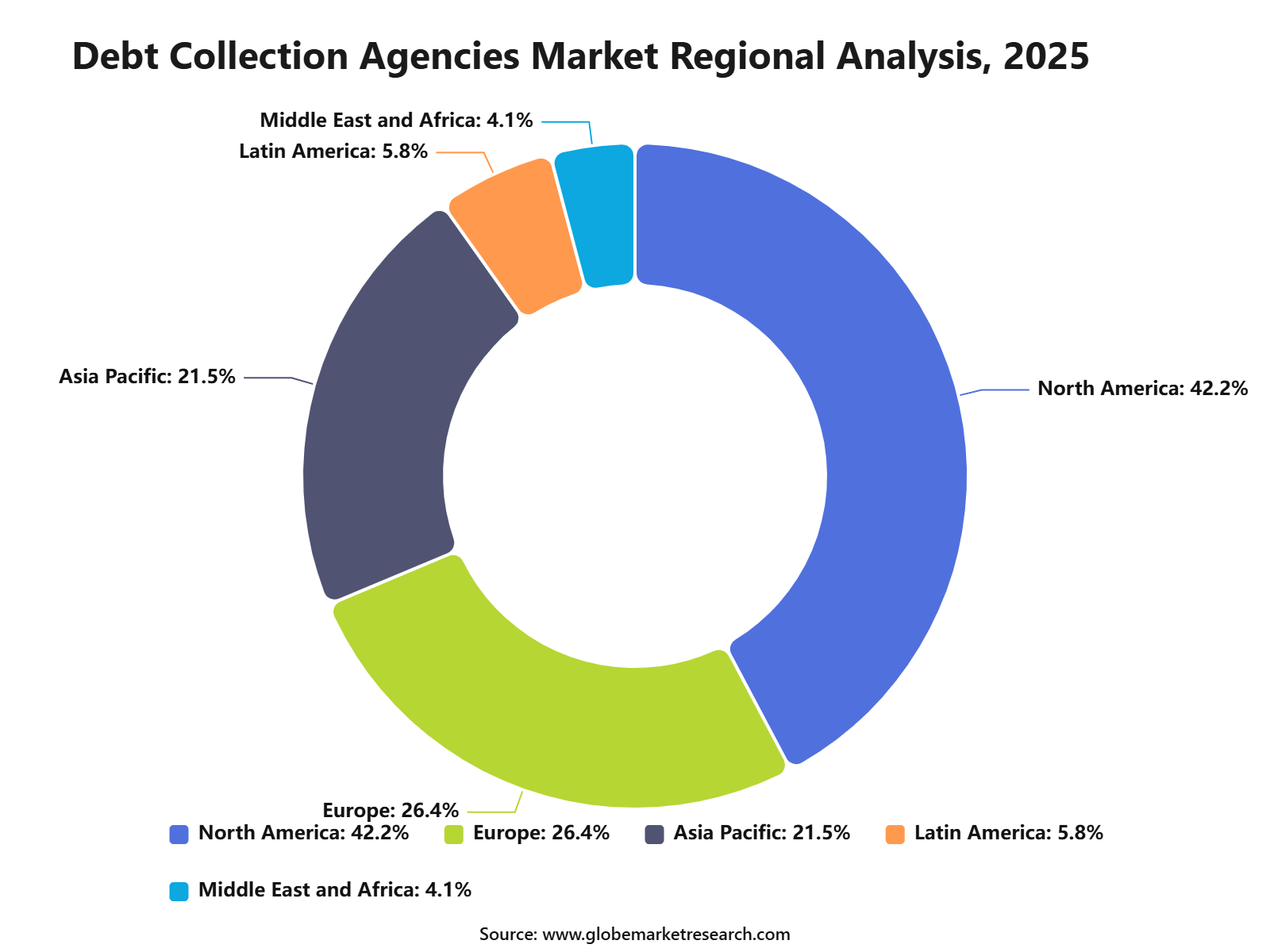

North America led the market with 42.2% share in 2025, supported by a large credit economy, strong use of third-party collection services, and strict regulatory frameworks. The growth of the debt collection agencies market can be attributed to the increasing need for professional, compliant, and technology-enabled recovery solutions. As household borrowing continues to rise, lenders and service providers are relying more on specialized agencies to manage overdue accounts, improve recovery rates, and reduce internal collection costs.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Bad debt led the debt type segment with 65.9% share, supported by rising loan defaults, overdue credit accounts, unpaid invoices, and increasing recovery needs across financial and commercial sectors.

Third-party agencies accounted for 53.6% share by agency type, driven by strong demand for outsourced recovery services, specialized collection expertise, and cost-efficient debt management.

Traditional collection held 48.5% share by collection method, supported by continued use of phone calls, letters, field collection, and direct negotiation methods.

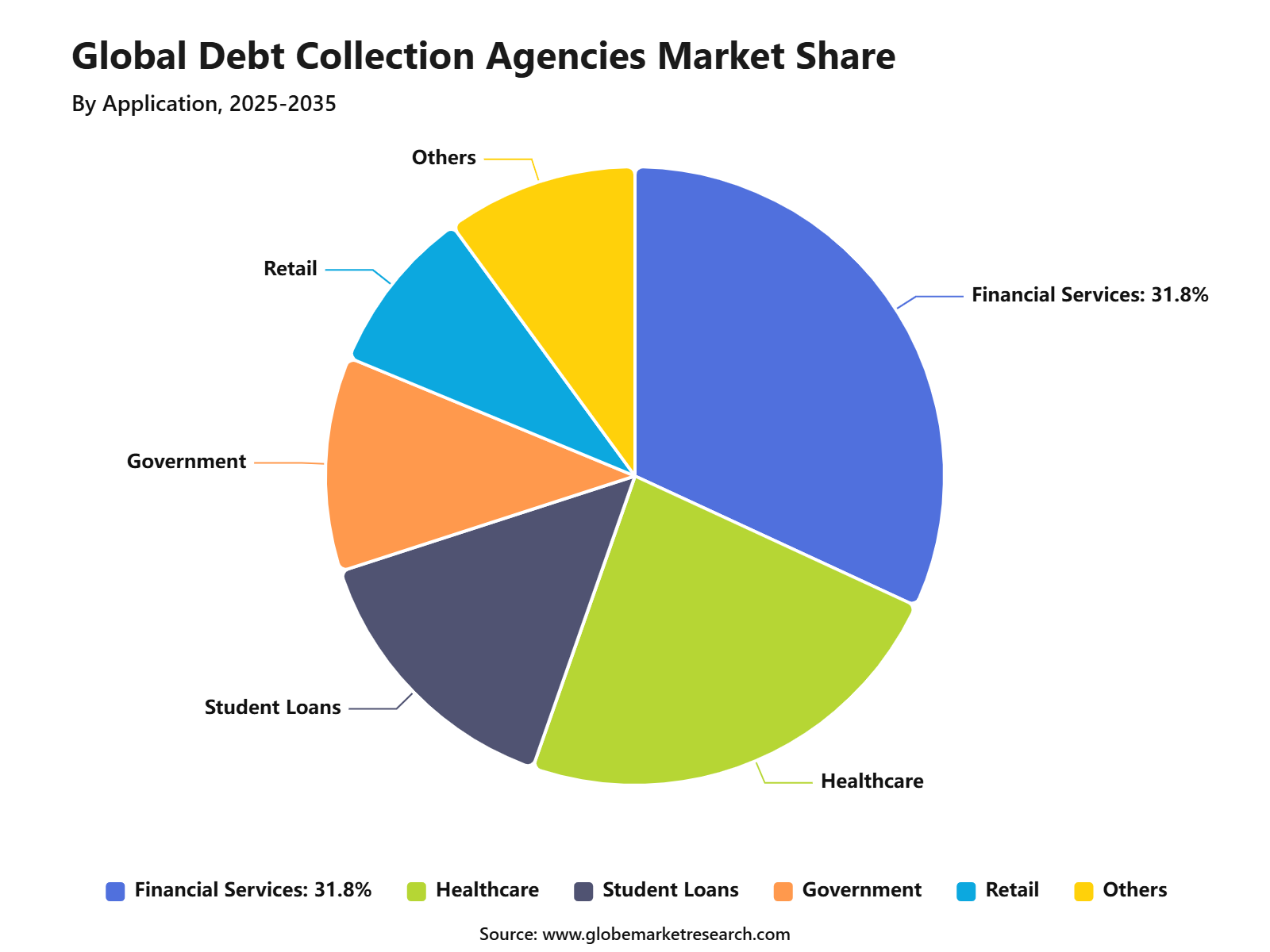

Financial services captured 31.8% share by application, driven by high volumes of credit card debt, personal loans, auto loans, mortgages, and other consumer credit products.

North America led the debt collection agencies market with 42.2% share, supported by a mature credit ecosystem, high consumer borrowing, strong financial services activity, and established debt recovery regulations.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape for debt collection agencies is spread across credit cards, personal loans, auto loans, student loans, healthcare bills, telecom bills, utilities, rent receivables, fintech lending, e-commerce credit, commercial invoices, and purchased debt portfolios. Credit card and unsecured consumer loans remain attractive because account volumes are high and digital repayment tools can improve recovery efficiency. In Q1 2026, U.S. credit card balances stood at USD 1.25 trillion, while auto loan balances reached USD 1.69 trillion, creating large addressable pools for early-stage and late-stage recovery services.

Commercial collections also offer revenue potential as companies seek better working-capital control. Rising business bankruptcies and tighter credit conditions can increase demand for receivables recovery, legal collections, and dispute resolution. U.S. Courts reported that personal and business bankruptcy filings rose 11.5% in the year ending June 30, 2025, reaching 542,529 filings compared with 486,613 in the prior year. This supports demand for collection, restructuring, settlement, and recovery services, but it also signals that some portfolios will carry higher loss risk.

Financial Impact

The financial impact can be positive for agencies that use automation, analytics, compliant omnichannel communication, and segmented recovery strategies. Digital payment links, self-service portals, AI-assisted call prioritization, dispute automation, and hardship-based repayment plans can reduce operating cost and improve consumer engagement. Agencies that can prove higher recovery rates with fewer complaints are better positioned to win contracts from banks, fintech lenders, telecom companies, utilities, and healthcare providers.

Profitability remains sensitive to labor cost, legal cost, data quality, account age, client pricing, and regulatory exposure. Older accounts usually require more effort and produce lower liquidation rates, while poorly documented accounts can increase disputes and reduce recovery success. Strong agencies should focus on clean placement data, early intervention, consumer-friendly repayment options, complaint reduction, audit-ready documentation, and contracts that reward compliant net recovery rather than only gross collections.

Risk Factors & Market Barriers

The main risk in the Debt Collection Agencies Market is compliance failure. Collection calls, letters, texts, emails, credit reporting, dispute handling, and payment negotiations are closely monitored by regulators and consumer protection groups. The CFPB received around 207,800 debt collection complaints in 2024, equal to 7% of total complaints received that year. This shows that debt collection remains a sensitive consumer issue and that poor communication practices can quickly create legal and reputational exposure.

Another market barrier is recoverability risk. Not every overdue account can be collected profitably, especially when accounts are old, poorly documented, disputed, bankrupt, deceased, fraud-linked, or outside the statute of limitations. The New York Fed reported that 4.8% of outstanding U.S. household debt was in some stage of delinquency at the end of March 2026, while the share of consumers with a third-party collection account on their credit report worsened slightly to 5.0%. This supports demand for agencies, but it also shows that portfolio quality and borrower affordability remain critical to recovery performance.

Regulatory & Compliance Risks

Regulatory risk is high because debt collection is governed by the Fair Debt Collection Practices Act, Regulation F, the Fair Credit Reporting Act, TCPA rules, state collection laws, licensing rules, privacy laws, and data security requirements. Regulation F implements the FDCPA and sets rules for debt collectors’ communication practices. It also places strong focus on harassment prevention, validation information, dispute handling, and responsible consumer contact.

Call-frequency compliance is especially important. Under Regulation F, a debt collector is generally presumed to comply if it does not place more than seven calls within seven consecutive days for a particular debt and does not call within seven days after a phone conversation about that debt. Exceeding these limits can create a presumption of violation. Agencies must therefore invest in dialer controls, consent records, call suppression, dispute coding, complaint tracking, and compliance audits.

Market Adoption Barriers

Market adoption barriers are linked to consumer distrust, reputational concerns, legal complexity, and client hesitation to outsource sensitive customer relationships. Banks, healthcare providers, fintech lenders, and utilities may avoid aggressive third-party collections if they fear brand damage or regulatory scrutiny. The Federal Trade Commission states that the purpose of the FDCPA is to eliminate abusive debt collection practices and protect collectors that follow the law from being competitively disadvantaged. This makes ethical collection practices a central adoption requirement, not only a compliance formality.

Healthcare collections face a special adoption barrier because medical debt rules have shifted and remain politically sensitive. The CFPB’s rule on medical information and credit reporting was vacated by the U.S. District Court for the Eastern District of Texas in July 2025. Even with that rule vacated, healthcare providers and agencies still need careful policies for patient communication, insurance disputes, charity care screening, credit reporting, and hardship-based repayment plans.

Debt Type Analysis

Bad debt led the Debt Collection Agencies Market with 65.9% share, supported by rising overdue consumer loans, credit card balances, unpaid medical bills, personal loans, and defaulted financial accounts. This segment remains dominant because lenders, banks, healthcare providers, telecom companies, and retailers depend on collection agencies to recover unpaid balances and reduce financial losses.

The growth of this segment can be attributed to increasing household borrowing, higher delinquency pressure, and tighter credit risk management across lending institutions. Bad debt collection agencies are being used to improve recovery rates, manage aged receivables, and support creditors with structured collection processes.

Agency Type Analysis

Third-party agencies accounted for 53.6% share, making them the leading agency type in the Debt Collection Agencies Market. These agencies are hired by creditors to recover unpaid debts after internal collection efforts become less effective or when accounts are transferred to specialist recovery teams.

The segment is supported by the need for professional collection expertise, legal process knowledge, compliance management, and large-scale account handling. Third-party agencies remain important because they allow creditors to focus on core operations while improving recovery efforts through trained collectors, digital tools, and structured follow-up systems.

Collection Method Analysis

Traditional collection held 48.5% share, supported by continued use of phone calls, letters, notices, field follow-ups, and direct communication with debtors. Many creditors still rely on traditional methods because they remain effective for certain debt categories, older accounts, and customer groups that respond better to direct outreach.

The segment continues to hold a strong position despite growing adoption of digital collection methods. Traditional collection is especially useful where personal communication, negotiation, repayment planning, and dispute resolution are required to recover overdue payments.

Application Analysis

Financial services led the application segment with 31.8% share, driven by strong demand from banks, credit card issuers, non-bank lenders, mortgage providers, auto lenders, fintech companies, and insurance-linked finance businesses. This sector generates large volumes of receivables, overdue accounts, and delinquent loans that require organized recovery support.

The growth of this segment is being supported by rising consumer credit use, increasing digital lending activity, and stricter risk management needs among financial institutions. Debt collection agencies help financial service providers recover unpaid balances, manage customer contact, reduce charge-offs, and maintain stronger portfolio performance.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Analysis

North America led the Debt Collection Agencies Market with 42.2% share, supported by high consumer credit usage, large financial services activity, mature legal recovery systems, and strong demand for professional debt recovery services. The region has a large base of banks, credit card companies, healthcare providers, telecom firms, and retail lenders that require collection support.

The growth of the North American market is also being shaped by strict regulatory oversight and rising demand for compliant collection practices. Agencies in the region are investing in better data management, consumer communication controls, digital payment tools, and compliance systems to improve recovery outcomes while reducing legal and reputational risk.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

North America market leadership | +1.3% | U.S. and Canada | Leads collection activity. |

Europe regulated collection growth | +0.9% | UK, Germany, France, Italy | Supports compliant services. |

Asia Pacific credit expansion | +0.8% | India, China, Southeast Asia | Drives new demand. |

Latin America consumer lending growth | +0.5% | Brazil, Mexico, Chile, Colombia | Builds agency demand. |

Middle East and Africa early adoption | +0.4% | UAE, Saudi Arabia, South Africa | Shows gradual growth. |

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Rest of Asia Pacific

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Shift toward digital collections | +1.0% | North America, Europe, Asia Pacific | Reduces manual effort. |

Customer-friendly collection practices | +0.8% | U.S., Europe, Australia | Improves repayment response. |

AI-driven borrower segmentation | +0.7% | Developed markets | Improves recovery targeting. |

Growth of third-party agencies | +0.6% | Global | Expands outsourced services. |

Compliance-first collection models | +0.5% | Regulated markets | Builds lender confidence. |

Technology Adoption Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

AI and predictive analytics | +0.9% | U.S., Europe, India | Improves collection scoring. |

Digital payment portals | +0.8% | Global | Speeds repayment. |

CRM and case management platforms | +0.7% | Global agencies | Improves workflow control. |

Automated messaging systems | +0.6% | North America, Europe, Asia Pacific | Improves contact frequency. |

Data security and compliance tools | +0.5% | Regulated markets | Protects consumer data. |

Segment Covered in the Report

By Debt Type

Bad Debt

Early Out Debt

By Agency Type

First-Party Agencies

Third-Party Agencies

By Collection Method

Traditional Collection

Digital Debt Collection

Legal Collection

By Application

Financial Services

Healthcare

Student Loans

Government

Retail

Telecom and Utility

Mortgage

Others

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising consumer credit usage | +1.1% | North America, Europe, Asia Pacific | Increases recovery demand. |

Growth in bad debt volumes | +1.0% | U.S., Europe, India, Brazil | Drives agency outsourcing. |

Expansion of financial services lending | +0.8% | Global | Supports collection activity. |

Increasing healthcare and utility receivables | +0.7% | North America, Europe | Expands collection cases. |

Adoption of digital collection tools | +0.6% | Developed and urban markets | Improves recovery efficiency. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Strict debt collection regulations | -0.8% | U.S., Europe, Australia | Raises compliance burden. |

Consumer privacy concerns | -0.6% | North America, Europe, Asia Pacific | Limits aggressive outreach. |

Reputation risk for lenders | -0.5% | Global | Restricts outsourcing. |

Low recovery rates in stressed accounts | -0.4% | Global | Affects profitability. |

High operational compliance cost | -0.4% | Regulated markets | Pressures agency margins. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in digital debt collection | +1.0% | North America, Europe, Asia Pacific | Improves customer engagement. |

AI-based recovery analytics | +0.8% | U.S., UK, India, Singapore | Enhances account prioritization. |

Expansion in healthcare collections | +0.7% | U.S., Europe | Supports receivables recovery. |

Demand from fintech lenders | +0.6% | U.S., India, Southeast Asia, Brazil | Opens new client base. |

Omnichannel communication models | +0.5% | Global | Improves contact success. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Managing consumer complaints | -0.6% | North America, Europe | Affects agency reputation. |

Compliance with changing rules | -0.5% | U.S., Europe, Asia Pacific | Increases monitoring needs. |

Data security and breach risks | -0.4% | Global | Raises trust concerns. |

Difficulty reaching delinquent borrowers | -0.4% | Global | Lowers recovery success. |

Competition from in-house collection teams | -0.3% | Large lenders | Limits outsourcing growth. |

Recent Developments

January 2026, The U.S. Department of Education delayed involuntary collection efforts such as Administrative Wage Garnishment and the Treasury Offset Program while new repayment options were being implemented. The department said the delay would give defaulted borrowers more time to evaluate repayment, consolidation, and rehabilitation options. This development is important for collection agencies because student loan collection activity affects recovery volumes, borrower outreach, credit reporting, and compliance workflows.

March 2026, The CFPB reported that it received about 387,400 debt collection complaints in 2025. Around 304,700 complaints, or 79%, were sent to companies for review and response. Companies responded to 97% of debt collection complaints sent to them, while 66% were closed with an explanation and 23% with non-monetary relief. This shows that compliance, documentation, response quality, and dispute handling are becoming central operating priorities for collection agencies.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 32.1 Billion |

Forecast Revenue (2035) | USD 48.4 Billion |

CAGR (2025-2035) | 4.2% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Debt Type (Bad Debt, Early Out Debt), By Agency Type (First-Party Agencies, Third-Party Agencies), By Collection Method (Traditional Collection, Digital Debt Collection, Legal Collection), By Application (Financial Services, Healthcare, Student Loans, Government, Retail, Telecom and Utility, Mortgage, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Encore Capital Group, PRA Group, Intrum AB, EOS Group, Credit Collection Services, IC System, Resurgent Capital Services, Northland Group, Convergent Outsourcing, Transworld Systems, CBE Group, Midland Credit Management, Apex Asset Management, Account Control Technology and Other Key Players |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Encore Capital Group

PRA Group

Intrum AB

EOS Group

Credit Collection Services

IC System

Resurgent Capital Services

Northland Group

Convergent Outsourcing

Transworld Systems

CBE Group

Midland Credit Management

Apex Asset Management

Account Control Technology

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Information and Technology

AI Data Center Market to hit USD 262.7 Bn by 2035

Global AI Data Center Market By Component (Hardware, Software, Services), By Infrastructure (Servers, Storage Systems, Networking Equipment, Power and Cooling Systems, Security Infrastructure, Others), By Data Center Type (Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, Edge Data Centers), By Deployment Mode (On-Premise, Cloud-Based, Hybrid), By Technology (Machine Learning, Deep Learning, Generative AI, Natural Language Processing, Computer Vision, Predictive Analytics, Others), By Application (AI Model Training, AI Inference, Data Processing and Analytics, High-Performance Computing, Cloud AI Services, Automation and Monitoring, Others), By End Use Vertical (BFSI, Healthcare and Life Sciences, IT and Telecommunications, Retail and E-Commerce, Automotive, Manufacturing, Government and Public Sector, Media and Entertainment, Energy and Utilities, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Operating Room Integration Market to hit USD 10.3 Bn by 2035

Global Operating Room Integration Market Size, Share Report By Component (Software, Hardware, Services), By Device Type (Audio and Video Management Systems, Display Systems, Others), By Application (General Surgery, Orthopedic Surgery, Others), By End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), By Deployment Mode On-premise, Cloud-based, Hybrid), By Operating Room Type (Hybrid Operating Rooms, Integrated Operating Rooms), By Technology (Surgical Workflow Integration, Image and Video Integration, Others), By Regional (North America, Europe, Asia Pacific, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Sharing Economy Apps Market to hit 1,411.2 Bn by 2035

Global Sharing Economy Apps Market By Product / Service Type (Shared Transportation, Shared Space, Sharing Financial, Sharing Food, Shared Healthcare, Shared Knowledge & Education, Shared Task Services, Shared Items, Others), By Distribution Channel (Online, Offline), By End User (Generation Z, Millennials, Generation X, Boomers), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

AI Receptionist Market to hit USD 23.8 Bn by 2035

Global AI Receptionist Market Size, Share Analysis Report By Component (Solutions, Services), By Deployment (Cloud-based, On-premises), By Service Type (Voice Reception Services, Chat Reception Services, Appointment Scheduling, Call Routing, Lead Qualification, Customer Support), By Service Model (24/7 Receptionist Solutions, Business Hours Receptionist Solutions, Hybrid Receptionist Solutions), By Technology (Voice AI Integration, Conversational AI, Natural Language Processing, Speech Recognition and Others), By Enterprise Size (Small and Medium Enterprises, Large Enterprises), By End-use (Healthcare, Legal Services, Real Estate, Retail and E-commerce, BFSI, Hospitality, Automotive, Home Services, IT and Telecom, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035