Revenue, 2025

$ 8.5 Bn

Forecast, 2035

$ 21.3 Bn

CAGR, 2025-2035

9.6%

Report Coverage

Global

Market Size and Forecast

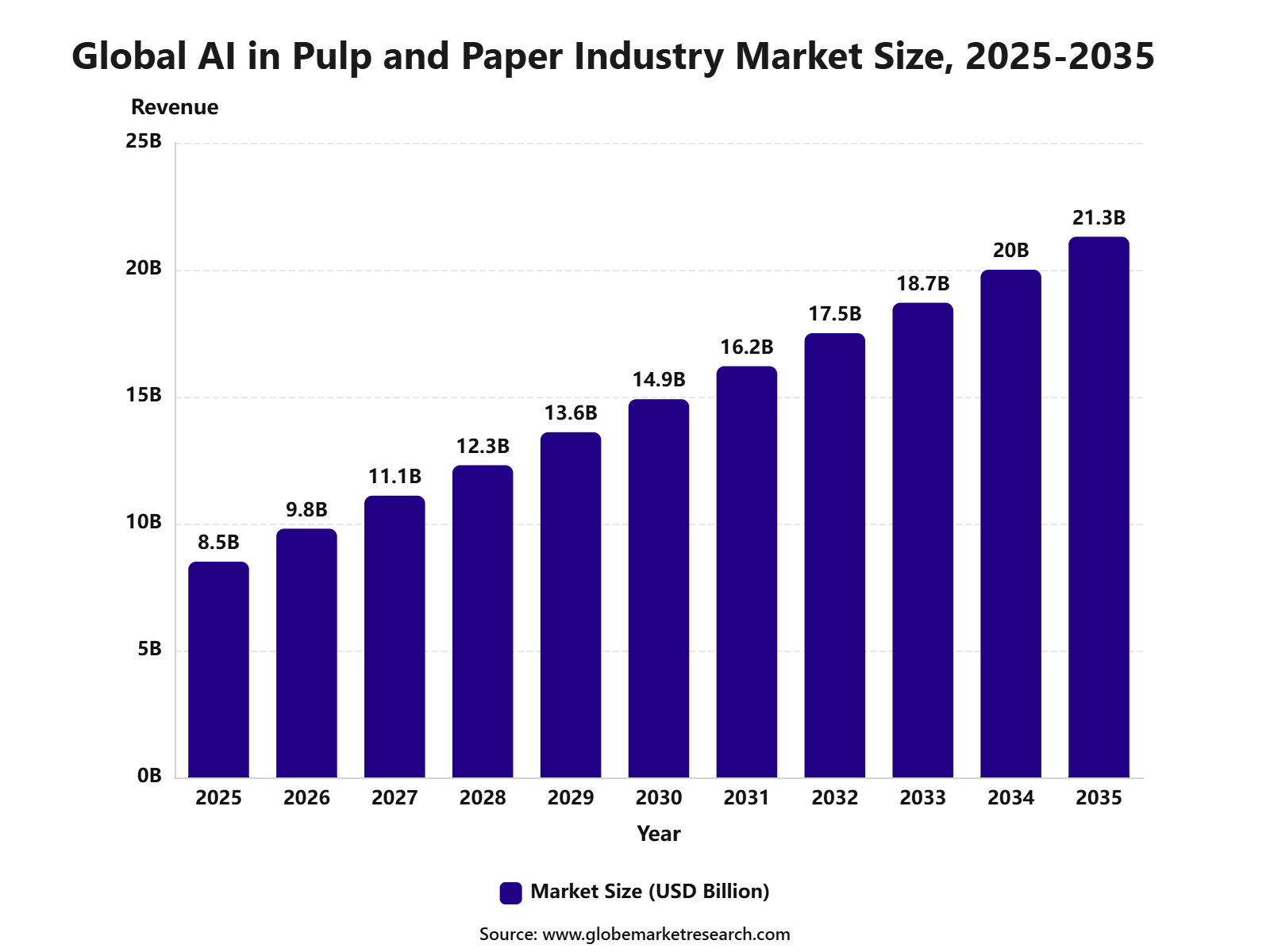

The Global AI in Pulp and Paper Industry Market was worth USD 8.5 billion in 2025 and is expected to reach USD 21.3 billion by 2035, growing at a CAGR of 9.6% from 2025 to 2035. Europe held the largest regional share of 35.6% in 2025, valued at around USD 3.0 billion, supported by strong pulp and paper manufacturing capacity, rising automation in mills, sustainability-focused production, and higher adoption of AI-based process control. European paper and board production declined by 1.5% in 2025, which increased the need for efficiency tools that can help producers manage cost pressure, energy use, quality control, and asset performance.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 8.5 Billion |

Projected Revenue, 2035 | USD 21.3 Billion |

CAGR, 2025-2035 | 9.6% |

Largest Region | Europe, 35.6% Share |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

The AI in Pulp and Paper Industry Market includes software, sensors, analytics platforms, machine learning models, computer vision systems, and connected automation tools used across pulp processing, paper manufacturing, coating, drying, inspection, packaging paper, tissue, and specialty paper production. These solutions support predictive maintenance, paper break prediction, defect detection, chemical dosing, fiber quality monitoring, energy optimization, demand forecasting, and production planning. In smart papermaking, machine learning is being used to improve quality by detecting defects, improving consistency, and flagging process changes early.

The market outlook remains positive as pulp and paper companies are under pressure to improve productivity, reduce downtime, lower energy consumption, and maintain consistent product quality. Growth can be attributed to wider use of AI-driven condition monitoring, digital twins, automated inspection, predictive maintenance, and process optimization across modern paper mills. AI-based condition monitoring can reduce maintenance downtime by up to 50%, while predictive performance in mechanical refining can deliver energy savings of up to 15%, making AI adoption more valuable for mills facing high energy and operating costs.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

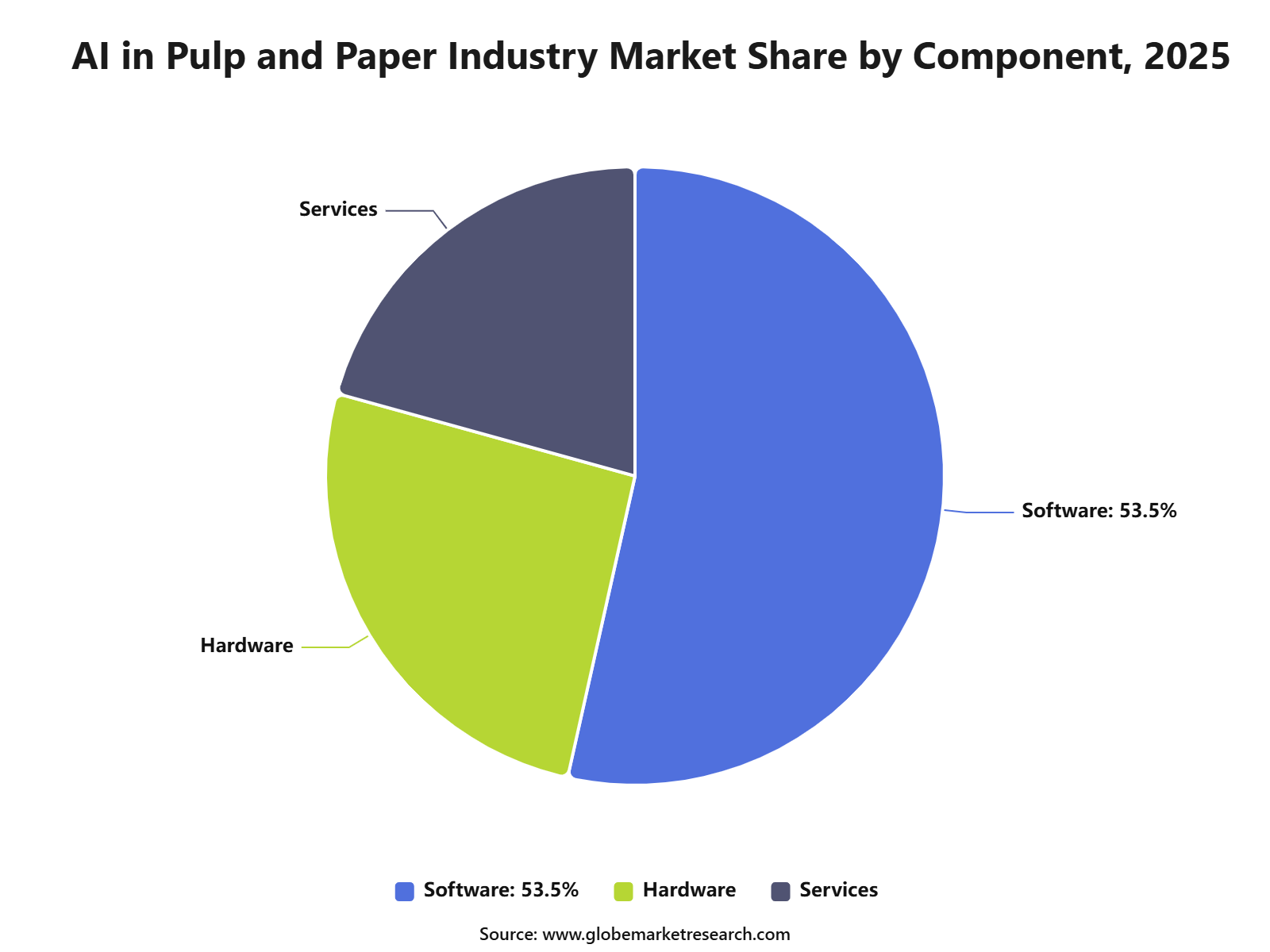

Software led the component segment with 53.5% share, supported by rising use of AI platforms for production monitoring, predictive maintenance, quality control, and workflow automation.

Process optimization accounted for 38.9% share by application, driven by growing demand to reduce energy use, improve machine efficiency, minimize waste, and enhance production consistency.

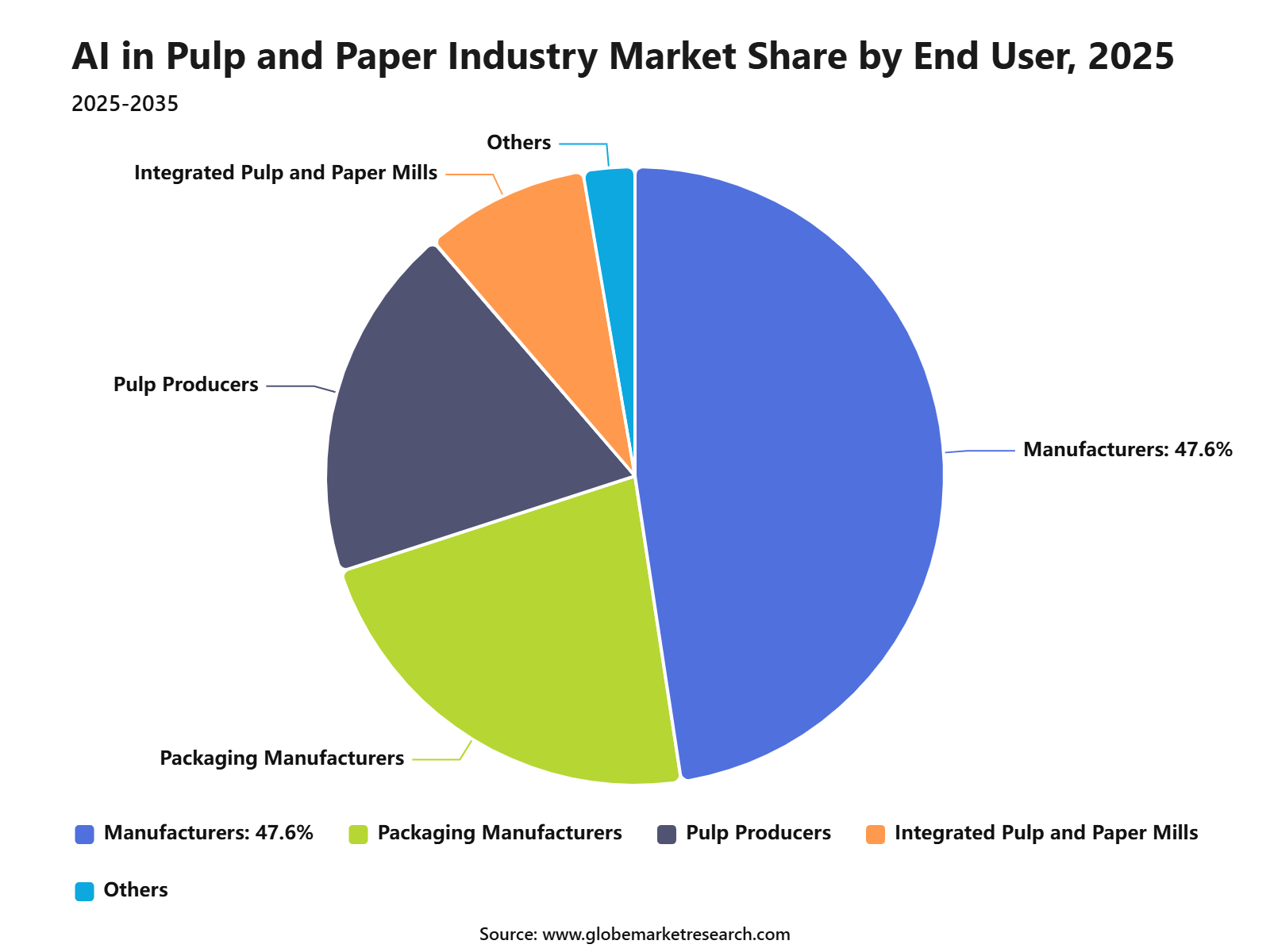

Paper manufacturers held 47.6% share by end user, supported by increasing adoption of AI tools to improve pulp processing, paper quality, asset performance, and operational productivity.

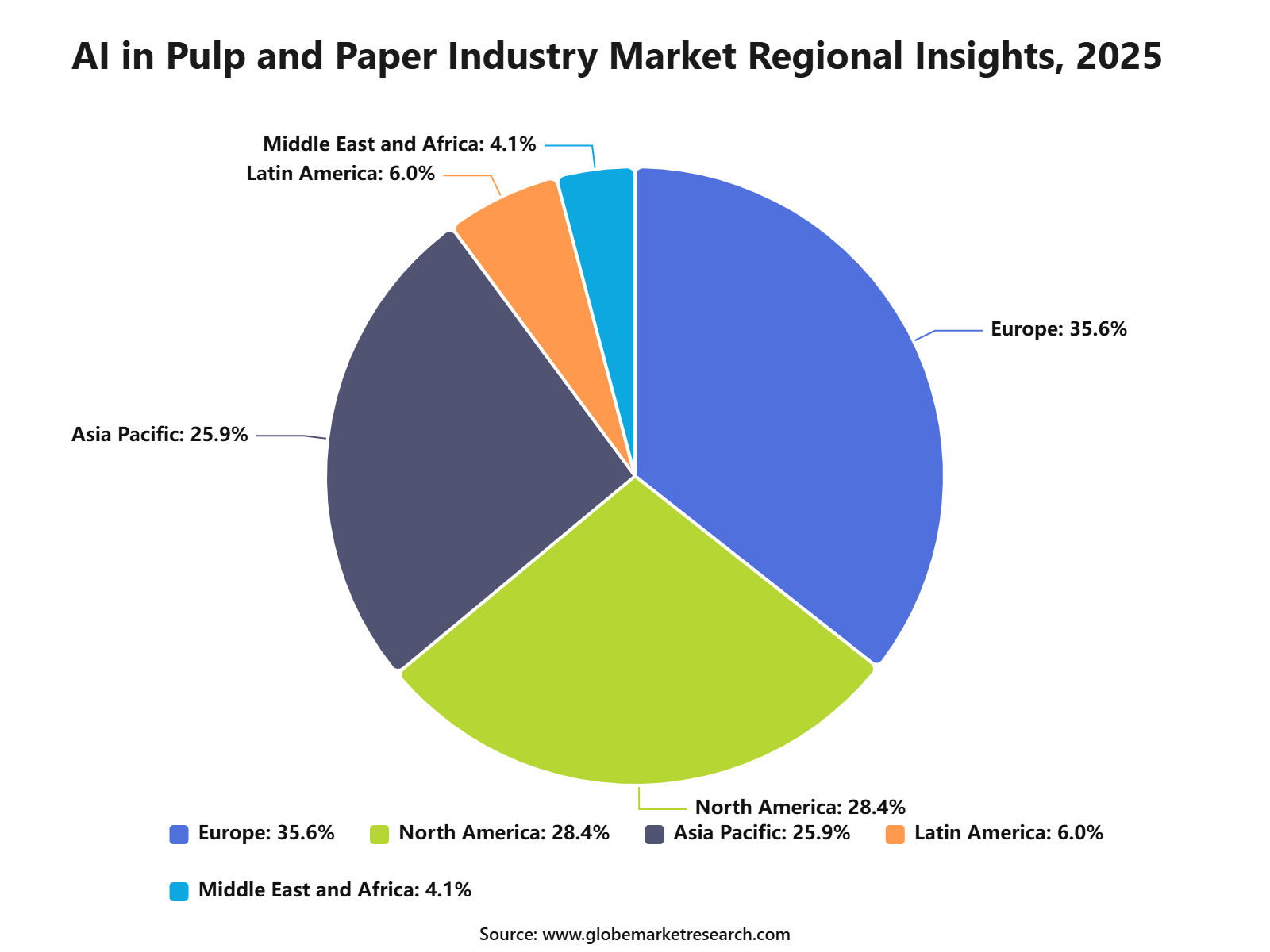

Europe led the AI in pulp and paper industry market with 35.6% share, supported by advanced manufacturing practices, strong sustainability goals, and rising investment in smart paper production technologies.

Component Insights

Software led the component segment with 53.5% share. The segment remained dominant because AI adoption in pulp and paper mills depends heavily on analytics platforms, process control software, predictive maintenance tools, quality monitoring systems, and production optimization solutions.

Software is becoming more important as mills generate large volumes of operating data from sensors, machines, dryers, refiners, boilers, and quality inspection systems. AI-based software helps convert this data into practical decisions, such as adjusting machine speed, improving chemical dosing, reducing defects, and detecting early signs of equipment failure.

The segment is also supported by wider digital transformation across manufacturing. In 2025, industry analysis highlighted that process manufacturing sectors, including pulp and paper, already use AI routines in operations, while the next phase is being shaped by cloud platforms, connected assets, data intelligence, and workforce support tools.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFApplication Insights

Process optimization led the application segment with 38.9% share. The segment is leading because pulp and paper production is highly energy-intensive and depends on stable control of refining, drying, dewatering, bleaching, pulping, and paper machine operations.

AI is being used to improve process stability by monitoring operating conditions and adjusting parameters in real time. This is especially important in paper mills, where small changes in moisture, temperature, fiber quality, pressure, and machine speed can affect output quality and operating cost.

The importance of process optimization is supported by recent technical findings. A 2025 review found that AI-based optimization in mechanical refining can deliver up to 15% energy savings, while AI-driven heat recovery strategies in dewatering and drying can reduce energy use by 10% to 20%.

End User Insights

Paper manufacturers led the end user segment with 47.6% share. The segment remained ahead because paper producers directly operate the equipment, production lines, and quality systems where AI delivers the most visible operational benefits. Paper manufacturers are using AI to improve yield, reduce waste, control energy use, lower downtime, and maintain product consistency. These benefits are important because mills face pressure from rising operating costs, changing demand patterns, and stricter sustainability requirements.

Maintenance is also becoming a major AI use case for paper manufacturers. A 2026 paper and packaging operations report stated that AI-supported maintenance can improve overall equipment effectiveness by 1 to 2% points, reduce mean time to repair by 5% to 15%, and lower maintenance cost per ton by 17% to 23%.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Insights

Europe held 35.6% share in the AI in Pulp and Paper Industry Market. The region is a major adoption base because its paper industry is highly focused on energy efficiency, circular materials, carbon reduction, and better use of digital manufacturing tools. AI adoption in Europe is being supported by pressure to improve competitiveness.

In 2025, European paper and board production declined by 1.6% to 77.4 million tonnes, while early 2026 signals showed output was down 2.4% in the first quarter compared with the same period in 2025. The region also has a strong sustainability driver for AI adoption. European pulp and paper producers reduced specific CO₂ emissions by 10.2% in 2025 and sourced an all-time high 92% of wood from Europe, which strengthens the case for AI tools that improve energy control, resource efficiency, and production resilience.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFSegment Covered in the Report

By Component

Software

Hardware

Services

By Application

Process Optimization

Quality Control

Predictive Maintenance

Supply Chain Management

Energy Management

Others

By End User

Paper Manufacturers

Pulp Producers

Packaging Manufacturers

Integrated Pulp and Paper Mills

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

The AI in Pulp and Paper Industry Market is driven by rising demand for process automation, predictive maintenance, quality control, energy optimization, and waste reduction across paper mills. AI helps manufacturers improve production consistency, reduce downtime, lower operating costs, and manage complex pulp and paper production lines more efficiently.

Europe leads the market due to its strong paper manufacturing base, high focus on sustainability, strict environmental rules, and early adoption of industrial automation. Germany, Finland, Sweden, France, Italy, and the UK remain important markets because of their advanced paper mills, packaging demand, and focus on energy-efficient manufacturing.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising adoption of process automation | +2.5% | Europe, North America, Asia Pacific | Drives core market growth. |

Demand for predictive maintenance | +2.1% | Advanced paper mills | Reduces downtime and repair cost. |

Energy efficiency requirements | +1.8% | Europe and high-cost energy markets | Improves operating margins. |

Growth in packaging paper production | +1.5% | Europe, China, India, U.S. | Supports AI-based production control. |

Need for consistent product quality | +1.2% | Tissue, packaging, printing paper mills | Improves output reliability. |

Restraints Impact Analysis

The market faces restraints from high implementation cost, legacy mill infrastructure, limited digital readiness, and shortage of skilled industrial AI professionals. Many pulp and paper mills still operate with older control systems, making AI integration more complex.

Another restraint is data quality. AI systems need reliable sensor data, production history, machine condition data, and process parameters, but many mills have fragmented or incomplete datasets.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High AI implementation cost | -1.3% | Small and mid-sized mills | Slows adoption. |

Legacy production infrastructure | -1.1% | Older paper mills | Raises integration complexity. |

Poor data quality and fragmented systems | -0.9% | Global manufacturing sites | Limits AI accuracy. |

Shortage of AI and automation talent | -0.8% | Industrial regions | Delays project execution. |

Cybersecurity concerns in connected mills | -0.6% | Digitized paper plants | Raises risk management needs. |

Opportunities Impact Analysis

Opportunities are strong in predictive maintenance, AI-based quality inspection, process control optimization, chemical usage reduction, energy management, yield improvement, and supply chain planning. These use cases directly support cost savings and productivity gains.

Higher-value opportunities are also emerging in computer vision for paper defect detection, AI-driven pulp quality prediction, digital twins, and autonomous mill operations. Companies that can connect AI with real-time mill data can create strong value for pulp and paper producers.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Predictive maintenance platforms | +2.4% | Europe, North America, Asia Pacific | Builds recurring software demand. |

AI-based quality inspection | +2.0% | Packaging, tissue, specialty paper mills | Reduces defects and waste. |

Energy optimization software | +1.7% | Europe and energy-intensive mills | Improves cost efficiency. |

Digital twin deployment | +1.4% | Advanced industrial plants | Supports process simulation. |

AI-based supply chain planning | +1.1% | Global paper manufacturers | Improves inventory and delivery planning. |

Challenges Impact Analysis

The main challenge is connecting AI models with real-time production environments. Pulp and paper production involves moisture control, fiber quality, chemical dosing, steam usage, drying speed, coating quality, and machine performance, which all require accurate process data.

Another challenge is proving return on investment. Paper manufacturers need clear evidence that AI can reduce downtime, lower waste, improve yield, save energy, and improve product quality before expanding adoption across multiple mills.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Integrating AI with mill control systems | -1.2% | Global pulp and paper plants | Increases deployment complexity. |

Proving clear ROI | -1.0% | Cost-sensitive manufacturers | Affects investment decisions. |

Managing real-time production data | -0.8% | Connected paper mills | Impacts model performance. |

Scaling AI across multiple plants | -0.7% | Large paper groups | Requires standardization. |

Operator resistance to automation | -0.5% | Traditional manufacturing sites | Slows adoption. |

Go-to-Market and Sales Economics

According to Globe Market Research, the go-to-market approach for the AI in Pulp and Paper Industry Market should focus on mill-level efficiency, not broad digital transformation. Paper and pulp producers need AI for predictive maintenance, process control, paper quality optimization, energy management, chemical dosing, fiber yield improvement, defect detection and autonomous operations.

Sales economics are being shaped by pressure on production cost, energy use and equipment uptime. AI tools are most valuable when they are connected with sensors, distributed control systems, quality control systems, mill historians and asset performance platforms. Valmet states that digital and autonomous operations are becoming a guiding principle for board and paper producers, with data from sensors and online measurements forming the base for full process optimization.

The strongest commercial model is solution-led selling, where AI is sold with automation, analytics, remote monitoring and process expertise. ANDRITZ’s Metris Copilot is positioned as a generative AI-powered industrial assistant for pulp and paper operations, connecting mill data, process applications and knowledge repositories through a conversational interface. This shows that AI is moving from dashboard-based reporting toward operator support, expert recommendations and faster decision-making inside mills.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is spread across predictive maintenance, machine vision inspection, quality control, energy optimization, process simulation, autonomous cranes, digital twins, supply-chain planning, chemical optimization and AI-supported maintenance services. Packaging paper is one of the strongest demand channels because packaging mills require stable production, lower waste and consistent paper quality. AF&PA reported that U.S. packaging papers and specialty packaging shipments increased 12% in May 2026 compared with May 2025, while shipments were up 6% for the first five months of 2026.

Containerboard and fiber-based packaging create a large operational base for AI deployment. U.S. containerboard production reached 36.1 million tons in 2025, and mills maintained a 91.9% operating rate despite lower capacity. High utilization makes predictive maintenance, break prevention, moisture control, basis-weight control and production scheduling important revenue opportunities for AI and automation providers.

Europe also provides a strong AI adoption case because the sector is facing weak demand, high costs and industrial pressure. Cepi reported that paper and board production in member countries decreased 1.5% in 2025, while market pulp production increased 2.1%. This creates demand for AI tools that help mills protect margins through better energy efficiency, raw material use, product mix decisions and process stability.

Financial Impact

The financial impact of AI in pulp and paper is mainly linked to lower downtime, reduced energy consumption, better yield and fewer quality losses. Maintenance is another major financial lever because unplanned stoppages can lead to paper breaks, rejected output and higher repair cost. The same 2025 review found that AI-driven condition monitoring can reduce maintenance downtime by up to 50%, improving machine efficiency and production reliability.

The main financial challenge is scale-up. Deloitte’s 2026 AI in Manufacturing survey found that 84% of manufacturers already generate measurable value from AI, but only 20% of use cases are scaled. For pulp and paper companies, this means vendors must move beyond pilot projects and provide secure integration, operator training, explainable recommendations, mill-specific models and measurable savings in energy, uptime and quality performance.

Recent Developments

Market News

In June 2026, Valmet introduced the Valmet DNAe Optimization Suite, a scalable software suite designed to improve plant performance, reduce process variability, improve energy efficiency, and increase throughput across process plants.

In 2026, ANDRITZ promoted its AI Expert Agent powered by Metris Copilot for pulp and paper mills, using generative AI, multimodal interaction, mill data, and internal knowledge sources to support operators and maintenance teams.

In 2026, ABB highlighted ABB Ability MES for Pulp and Paper as a traceability and EUDR compliance solution, with integration to EU TRACES and support for reference numbers, verification numbers, due diligence documentation, and reel-level traceability.

Acquisitions

In July 2026, Valmet completed the acquisition of all remaining shares in FactoryPal GmbH from Körber, making FactoryPal a fully owned Valmet subsidiary. FactoryPal provides software for tissue converting operations and uses advanced data analytics and AI to improve efficiency, process stability, and machine settings management.

In December 2025, India’s Competition Commission approved ITC’s acquisition of Aditya Birla Real Estate’s paper and pulp business for Rs 3,498 crore. This deal is not AI-specific, but it is relevant to pulp and paper modernization because larger integrated paper producers are better positioned to invest in automation, digital traceability, and efficiency-focused upgrades.

Funding

In May 2026, Business Finland granted EUR 15 million in funding for Valmet’s Industrial NEXUS program, while another EUR 40 million was being prepared for ecosystem projects. Valmet also planned to invest EUR 55 million in the program over five years.

Market Impact

In 2026, AI adoption in pulp and paper is shifting from isolated analytics pilots to mill-wide decision support. The key focus areas are process stability, predictive maintenance, production planning, quality control, energy efficiency, traceability, and knowledge preservation.

In 2026, AI assistants are becoming important because many mills face skilled labor shortages and operational complexity. Tools such as Metris Copilot and FactoryPal are designed to help operators make faster decisions using production data, machine learning, anomaly detection, and plant knowledge.

In 2026, regulatory pressure is also supporting digital investment. EUDR compliance is increasing the need for traceability, raw material verification, batch-level documentation, and integrated data flows from forest source to finished pulp and paper products.

In 2026, the competitive advantage is expected to move toward suppliers that can combine process equipment, automation, AI software, digital services, and lifecycle support. Mills are likely to prefer practical AI solutions that reduce downtime, improve runnability, cut waste, stabilize quality, and help operators act before production issues become costly.

Research Methodology

Step 1: Primary Research - Primary research is conducted through direct discussions with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. These interviews help understand real market demand, pricing movement, supply chain conditions, production trends, and customer requirements.

Step 2: Secondary Research - Secondary research is carried out using company filings, annual reports, regulatory databases, government publications, trade association data, and verified industry sources. This step helps collect reliable background information and supports the overall market assessment.

Step 3: Data Validation - Collected data is validated through source triangulation, historical trend review, demand-side checks, and supply-side assessment. Multiple sources are compared to reduce errors and improve the accuracy of the final insights.

Step 4: Market Estimation - Market estimation is completed using both bottom-up and top-down approaches. Product demand, regional consumption, company presence, application-level usage, and end-use industry adoption are reviewed to estimate the market size and structure.

Step 5: Forecasting Approach - Market forecasts are prepared by studying regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. This approach helps identify future growth patterns and possible market changes.

Step 6: Quality Review - The final data and findings are reviewed by analysts through peer validation, outlier checks, internal consistency checks, and final publication approval. This ensures that the report maintains accuracy, clarity, and research quality.

Step 7: AI Policy - AI is not used as a primary data source. All published insights are checked against human-verified evidence, and final conclusions are reviewed by analysts before publication.

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

ABB Ltd.

AFRY AB

Andritz AG

Aspen Technology Inc.

AVEVA Group Plc

Ecolab Inc.

Emerson Electric Co.

General Electric Co.

Honeywell International Inc.

Kadant Inc.

Metso Corporation

Rockwell Automation Inc.

Schneider Electric SE

Seeq Corporation

Tietoevry

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Information and Technology

AI Visual Inspection System Market Revenue to Hit USD 315.2 billion by 2035

Global AI Visual Inspection System Market Size, Growth Analysis By Offering (Hardware Systems, Industrial Cameras, Sensors and Imaging Hardware, Software Platforms, AI Inspection Software, Vision Analytics Tools, Services), By Technology (Deep Learning-Based Vision Systems, Machine Learning Algorithms, Traditional Computer Vision Systems, Edge AI Vision Processing, Other AI Vision Technologies), By Application (Defect Detection & Quality Control, Assembly Verification, Measurement & Gauging, Packaging & Label Inspection, Other Industrial Inspection Applications), By Industry Vertical (Electronics & Semiconductor Manufacturing, Automotive Industry, Pharmaceuticals & Healthcare, Food & Beverage Manufacturing, Logistics & Warehousing, Other Industrial Verticals), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Cloud Computing Market Size to Surpass USD 17.5 Trillion by 2035

Global Cloud Computing Market Size, Share Analysis By Type (Public Cloud, Private Cloud, Hybrid Cloud), By Service Model (Software as a Service, Infrastructure as a Service, Platform as a Service), By Enterprise Type (Large Enterprises, Small and Medium Enterprises), By Industry (BFSI, IT and Telecommunications, Government, Consumer Goods and Retail, Healthcare, Manufacturing, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Agentic AI For Financial Services Market Size to Reach USD 315.5 billion by 2035

Agentic AI For Financial Services Market Size, Share Segmented by Application (Fraud Detection and Anti-Money Laundering, Virtual Assistants and Chatbots, Credit Assessment, Risk and Compliance Management, Investment Advisory, Claims Processing, and Others), By Component (Solutions and Services), By Deployment Mode (Cloud, On-Premise, and Hybrid), By End-User (Commercial Banks, Investment Banks, Asset Management Firms, and Other Financial Institutions), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Agentic AI in HR & Recruitment Market Size to Reach USD 120.5 billion by 2035

Global Agentic AI in HR & Recruitment Market Size, Go-to-Market and Sales Strategy Analysis By Deployment Mode (Cloud-Based, On-Premises), By Enterprises (Small and Medium Enterprises (SMEs), Large Enterprises), By Application (Talent Acquisition & Recruitment, Employee Onboarding, Employee Engagement & Retention, Workforce Analytics, Others), By End-User Industry (IT & Telecommunications, Healthcare, Retail & E-commerce, BFSI, Manufacturing, Education, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035