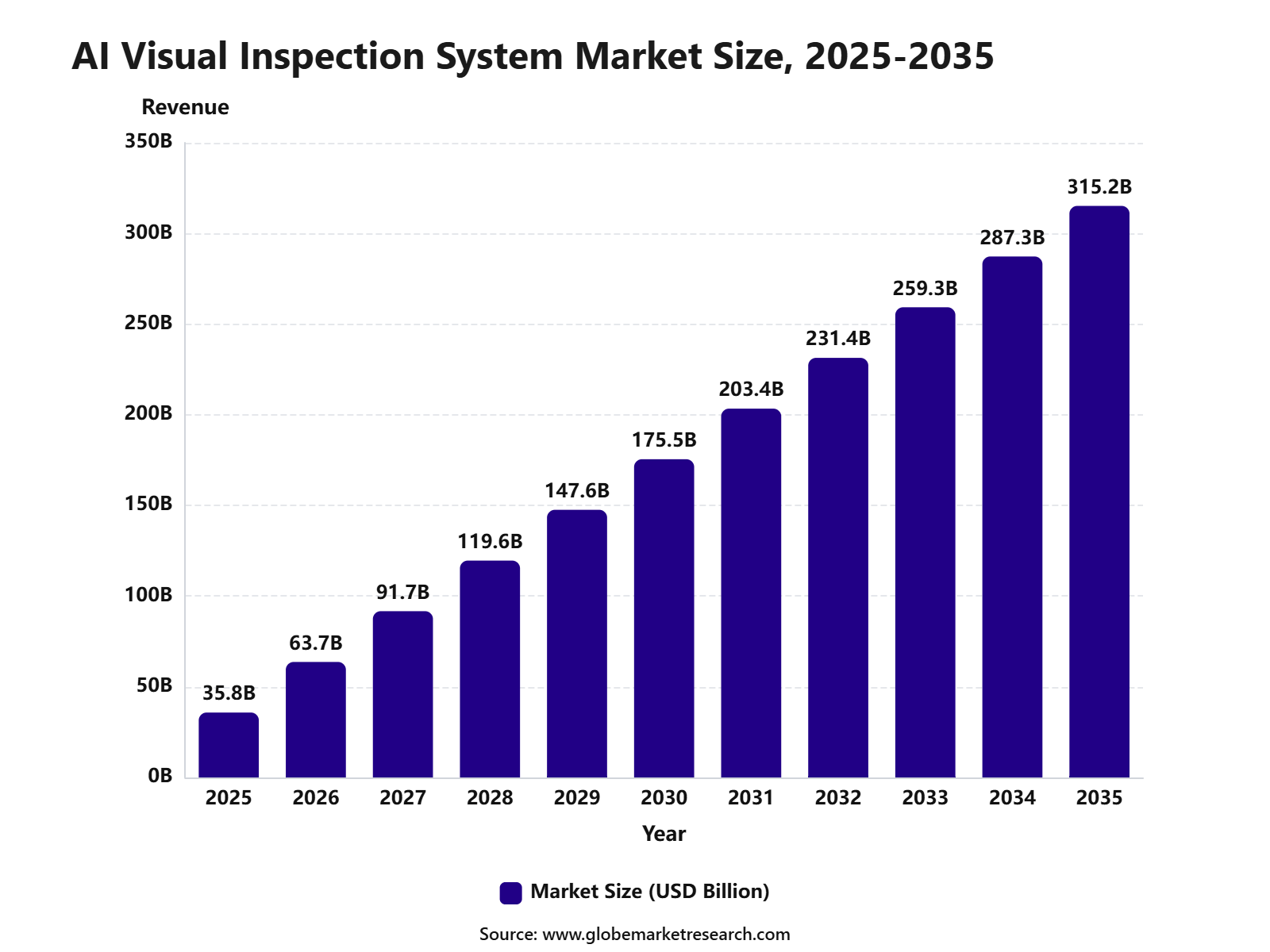

Revenue, 2025

$ 35.8 Bn

Forecast, 2035

$ 315.2 Bn

CAGR, 2025-2035

24.3%

Report Coverage

Global

Market Size and Forecast

The Global AI Visual Inspection System Market was worth USD 35.8 billion in 2025 and is expected to reach USD 315.2 billion by 2035, growing at a CAGR of 24.3% from 2025 to 2035. North America held the largest regional share of 37.6% in 2025, valued at around USD 13.5 billion, supported by advanced manufacturing automation, strong AI infrastructure, higher use of machine vision, and growing demand for real-time quality control. Demand is also supported by wider use of AI cameras and automated inspection tools in automotive, electronics, medical devices, food processing, packaging, and industrial equipment production.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 35.8 Billion |

Projected Revenue, 2035 | USD 315.2 Billion |

CAGR, 2025-2035 | 24.3% |

Largest Region | North America, 37.6% Share |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

The AI Visual Inspection System Market includes camera-based inspection platforms, computer vision software, deep learning models, edge AI devices, sensors, lighting systems, image processing tools, and automated quality control systems. These solutions are used to detect surface defects, cracks, scratches, missing parts, incorrect assembly, packaging errors, labeling issues, dimensional variation, and product contamination. IBM defines visual inspection as defect detection using direct or remote image-based checks, while AI-enabled systems can help manufacturers inspect products more consistently and reduce manual errors.

The market outlook remains positive as manufacturers are under pressure to reduce scrap, improve yield, prevent recalls, and maintain consistent product quality at high production speeds. Growth can be attributed to rising adoption of deep learning, edge computing, industrial cameras, robotics, and real-time defect detection systems across smart factories. Recent industrial studies show that deep learning and computer vision are improving automated defect detection by reducing dependence on manual inspection and helping systems identify visible and complex quality issues across 2D and 3D inspection environments.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFMarket Key Insights

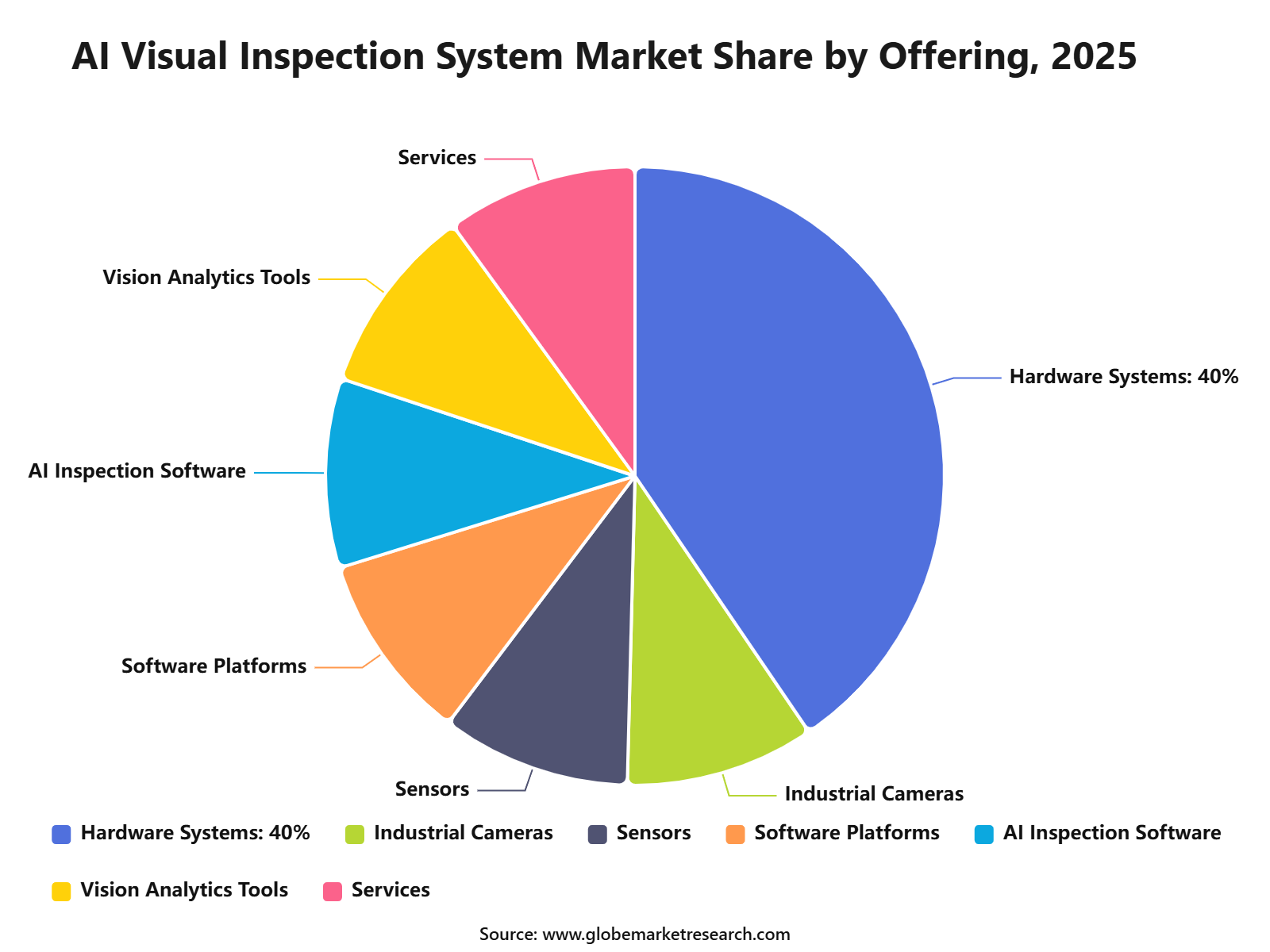

Hardware systems led the offering segment with 40.5% share, supported by strong demand for industrial cameras, sensors, lighting systems, processors, and machine vision equipment used in automated inspection.

Deep learning-based vision systems accounted for 36.5% share, driven by their ability to detect complex defects, learn from image data, and improve inspection accuracy across production lines.

Defect detection and quality control held 43.6% share by application, supported by rising need to reduce product errors, improve manufacturing consistency, and lower manual inspection dependency.

Electronics and semiconductor manufacturing captured 30.5% share by industry vertical, driven by high precision requirements, miniaturized components, and strict quality standards in chip and device production.

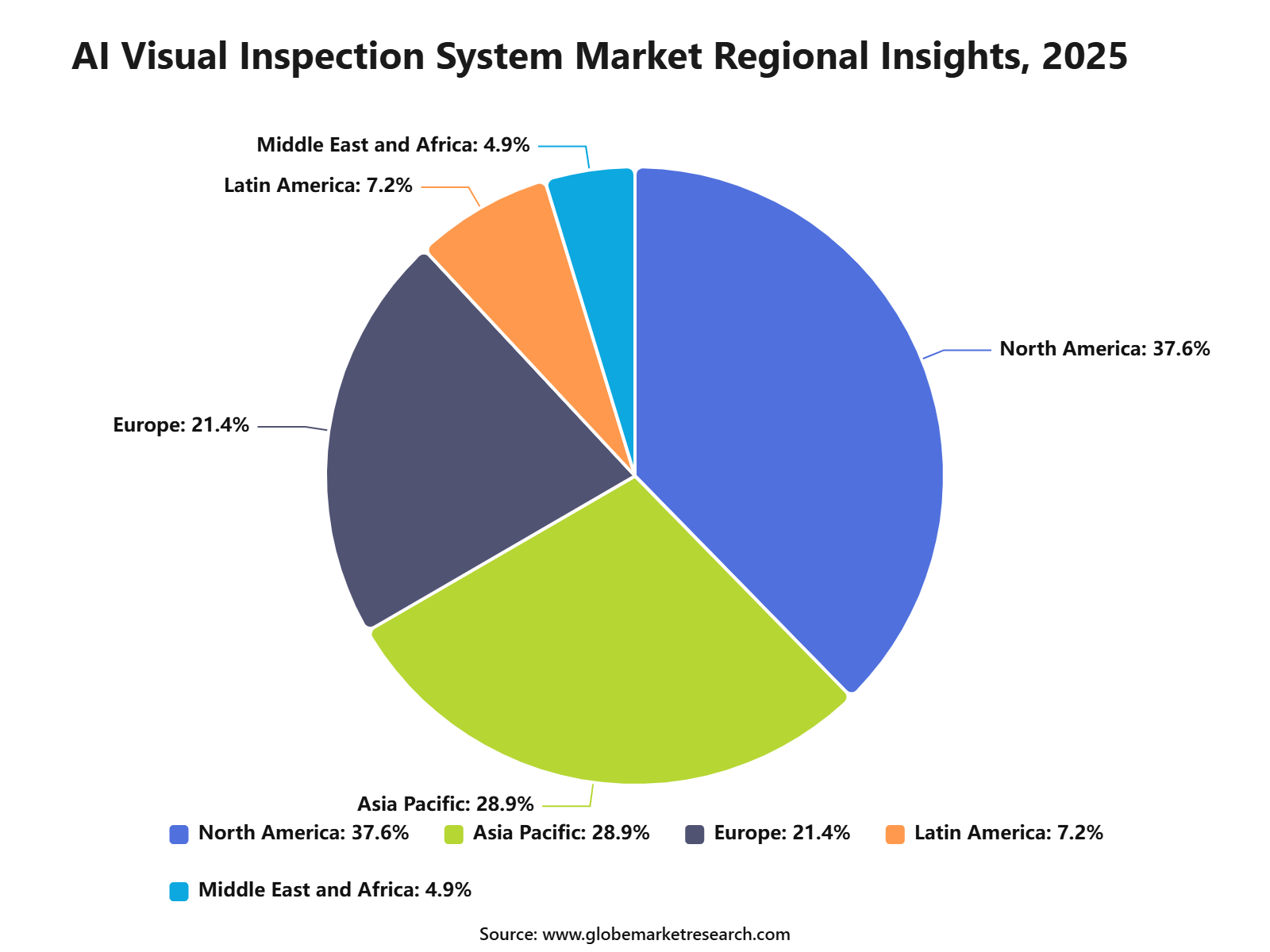

North America led the AI visual inspection system market with 37.6% share, supported by advanced manufacturing adoption, strong automation investment, and wider use of AI-based quality control systems.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFOffering Insights

Hardware Systems led the AI Visual Inspection System Market with 40.5% share, supported by the strong need for cameras, lenses, lighting units, sensors, processors, frame grabbers, and edge computing devices in automated inspection lines. These systems form the physical base required to capture, process, and analyze product images in real time.

The growth of this segment can be attributed to rising factory automation and the need for accurate visual data at high production speeds. Machine vision systems depend on coordinated hardware such as cameras, lenses, lighting, and processors, which makes hardware investment essential before software and AI models can deliver reliable inspection output.

Hardware Systems are expected to remain the leading offering as manufacturers continue to upgrade production lines with high-resolution cameras, 3D sensors, smart cameras, edge AI devices, and industrial lighting. Demand will remain supported by electronics, automotive, packaging, pharmaceuticals, food processing, and semiconductor manufacturing.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFTechnology Analysis Insights

Deep Learning-Based Vision Systems led the technology segment with 36.5% share, supported by their ability to detect complex defects, surface variations, scratches, cracks, missing parts, alignment issues, and pattern-level abnormalities. These systems are preferred where traditional rule-based inspection struggles with product variation and subtle visual differences.

The growth of this segment can be attributed to wider use of neural networks, object detection models, anomaly detection, and image classification in industrial inspection. A 2025 study on mass-produced electronic components showed that a YOLO-based deep learning system achieved 95.50% accuracy and 285 ms detection time for surface and pin-leg defects.

Deep Learning-Based Vision Systems are expected to remain a high-growth technology area as manufacturers move toward adaptive, self-improving, and real-time inspection systems. Future demand will be supported by electronics assembly, wafer inspection, PCB inspection, battery manufacturing, automotive components, precision parts, and high-volume quality control.

Application Insights

Defect Detection & Quality Control accounted for 43.6% share, making it the leading application segment in the AI Visual Inspection System Market. AI visual inspection is used to identify surface defects, missing components, incorrect assembly, contamination, dimensional errors, print defects, soldering issues, and packaging faults before products reach customers.

The dominance of this segment can be linked to the rising cost of product recalls, rework, warranty claims, and customer returns. A3 noted that machine vision is increasingly used across inspection, product assembly, identification, traceability, and automated operations as manufacturers seek more accurate and reliable imaging for complex applications.

Defect Detection & Quality Control is expected to remain the strongest application area as manufacturers increase the use of 100% inline inspection rather than sample-based checks. Future growth will be supported by smart factories, automated optical inspection, real-time defect alerts, process control, production traceability, and higher product quality standards.

Industry Vertical Insights

Electronics & Semiconductor Manufacturing led the industry vertical segment with 30.5% share, supported by high inspection needs across wafers, chips, printed circuit boards, displays, sensors, connectors, and electronic assemblies. These industries require precise visual inspection because even small defects can affect yield, product performance, and device reliability.

The growth of this segment can be attributed to rising semiconductor capacity expansion and stronger demand for AI-related chips, advanced memory, and high-performance electronics. SEMI reported that global semiconductor equipment billings reached USD 135.1 billion in 2025, up 15% year over year, with test equipment billings rising 55%.

Electronics & Semiconductor Manufacturing is expected to remain the leading industry vertical as production becomes more complex and quality tolerance becomes tighter. Demand will remain supported by wafer inspection, advanced packaging, chip testing, PCB defect detection, display inspection, semiconductor equipment monitoring, and electronics assembly automation.

Regional Insights

North America led the AI Visual Inspection System Market with 37.6% share, supported by strong automation adoption, advanced manufacturing investment, semiconductor expansion, and early use of AI-enabled quality systems. The region has a strong base of electronics, automotive, aerospace, medical device, packaging, and semiconductor manufacturers.

The region’s dominance can be attributed to large-scale investment in domestic chip production and advanced manufacturing infrastructure. SIA reported that semiconductor ecosystem companies had announced more than 140 projects across 30 U.S. states, totaling over USD 645.3 billion in private investments since 2020.

North America is expected to remain the leading regional market as manufacturers continue to invest in smart factories, automated inspection, edge AI, and semiconductor supply chain resilience. Future opportunities are likely to remain strong in electronics inspection, automotive quality control, medical device manufacturing, aerospace components, and high-precision industrial production.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFGo-to-Market and Sales Economics

According to Globe Market Research, the go-to-market approach for the AI Visual Inspection System Market should focus on defect reduction, faster quality control and lower manual inspection dependency. Manufacturers are using AI vision systems for surface defect detection, assembly verification, label inspection, PCB inspection, weld inspection, packaging checks and dimensional quality control. Deloitte reported that 29% of manufacturers were already using AI or machine learning at facility or network level, showing that AI inspection is moving into wider smart factory adoption.

Sales economics are strongest where inspection errors create high scrap, recall or warranty cost. Electronics, automotive, medical devices, food packaging, semiconductors and batteries are the most practical early buyers because quality failures can quickly affect yield and customer trust. IPC noted in 2025 that AI in automated optical inspection can improve detection accuracy, reduce manual intervention and improve production efficiency in electronics manufacturing.

The strongest sales model is solution-led deployment, where cameras, lighting, edge AI, software, integration, data labeling and operator training are sold together. Cognex reported USD 268 million in Q1 2026 revenue, up 24% year over year, supported by broad-based strength across major end markets. This shows that machine vision suppliers with AI capability, application expertise and service support are gaining commercial traction.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is spread across electronics inspection, automotive parts, battery cells, semiconductors, pharmaceuticals, food and beverages, packaging, textiles, metal fabrication, plastics and logistics automation. Robotics adoption is also supporting demand because vision systems are often paired with robotic pick, place, inspect and reject workflows. IFR reported 542,000 industrial robot installations in 2024, with Asia accounting for 74% of new deployments.

Semiconductor and electronics manufacturing provide one of the highest-value revenue pools because microscopic defects can reduce yield and increase rework. SIA reported global semiconductor sales of USD 120.6 billion in May 2026, the highest monthly total recorded, with sales rising 104.1% from May 2025. This supports demand for wafer inspection, PCB inspection, package inspection and AI-assisted defect classification.

EV and battery production also create strong demand for AI visual inspection systems. The IEA reported that electric car sales exceeded 20 million globally in 2025, equal to 25% of new car sales. Battery cells, modules, wiring, connectors, welds and surface coatings require high-speed inspection, making AI vision important for quality control at scale.

Financial Impact

The financial impact of AI visual inspection systems is mainly linked to lower scrap, reduced rework, faster line speed and fewer customer complaints. Automated inspection can run continuously and identify defects that may be missed during manual checks, especially on fast-moving or high-precision production lines. This makes the technology financially attractive where quality failures create warranty claims, rejected shipments or production downtime.

Profitability for suppliers is supported by premium hardware, recurring software licenses, data services, model retraining, maintenance and integration work. Cognex reported a 71.1% gross margin in Q1 2026 and adjusted EBITDA margin of 26.9%, showing that advanced machine vision products can support strong earnings when volume, mix and software value are favorable.

The main financial risk is implementation failure. AI inspection systems need clean image data, correct lighting, stable camera placement, trained defect libraries and clear pass-fail rules. A 2026 PCB inspection benchmark found that general vision-language models still struggle with dense layouts, subtle defect patterns and fine-grained localization, which shows why domain training and industrial validation remain essential before full deployment.

Segment Covered in the Report

By Offering

Hardware Systems

Industrial Cameras

Sensors and Imaging Hardware

Software Platforms

AI Inspection Software

Vision Analytics Tools

Services

By Technology

Deep Learning-Based Vision Systems

Machine Learning Algorithms

Traditional Computer Vision Systems

Edge AI Vision Processing

Other AI Vision Technologies

By Application

Defect Detection & Quality Control

Assembly Verification

Measurement & Gauging

Packaging & Label Inspection

Other Industrial Inspection Applications

By Industry Vertical

Electronics & Semiconductor Manufacturing

Automotive Industry

Pharmaceuticals & Healthcare

Food & Beverage Manufacturing

Logistics & Warehousing

Other Industrial Verticals

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

The AI Visual Inspection System Market is driven by rising demand for automated quality inspection, defect detection, production monitoring, process control, and real-time manufacturing analytics. Industries are adopting AI-based inspection systems to reduce manual errors, improve product quality, lower rejection rates, and increase production speed.

North America leads the market due to strong automation adoption, advanced manufacturing infrastructure, high labor cost, and early use of AI in automotive, electronics, pharmaceuticals, food processing, and medical device production. The U.S. remains the key regional contributor because manufacturers are investing in machine vision, robotics, and AI-enabled quality control systems.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising factory automation adoption | +6.8% | North America, Europe, Asia Pacific | Drives core market growth. |

Demand for real-time defect detection | +5.9% | Automotive, electronics, pharma | Improves product quality. |

Growth in smart manufacturing systems | +5.0% | U.S., Germany, Japan, China | Supports connected production. |

Need to reduce manual inspection errors | +4.3% | High-volume manufacturing sectors | Improves inspection accuracy. |

Expansion of AI-powered machine vision | +3.7% | Global industrial markets | Builds long-term adoption. |

Restraints Impact Analysis

The market faces restraints from high installation cost, complex integration, limited skilled workforce, and data quality challenges. AI visual inspection systems need cameras, lighting, sensors, software, training data, edge devices, and integration with production lines, which can raise upfront investment. Another restraint is model reliability across changing production conditions. Lighting variation, product movement, material changes, camera calibration issues, and rare defect types can affect inspection accuracy if systems are not continuously trained and monitored.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High upfront deployment cost | -3.2% | SMEs and cost-sensitive manufacturers | Slows adoption speed. |

Integration with legacy production lines | -2.8% | Traditional manufacturing plants | Adds implementation complexity. |

Limited AI and vision system expertise | -2.4% | Global industrial markets | Delays project rollout. |

Need for high-quality training data | -2.0% | Defect-sensitive industries | Affects model accuracy. |

Variation in production environments | -1.7% | Food, automotive, electronics | Impacts inspection consistency. |

Opportunities Impact Analysis

Opportunities are strong in automotive inspection, electronics quality control, pharmaceutical packaging, food safety inspection, semiconductor manufacturing, metal surface inspection, medical device inspection, and packaging defect detection. These sectors need high accuracy, traceability, and fast inspection at production scale. Higher-value opportunities are emerging in edge AI inspection, robotic vision, 3D visual inspection, predictive quality analytics, cloud-connected inspection platforms, and AI-based root cause analysis. Vendors that offer flexible, accurate, and easy-to-integrate systems can capture stronger enterprise demand.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Automotive quality inspection | +6.4% | North America, Europe, Asia Pacific | Builds large industrial demand. |

Electronics and semiconductor inspection | +5.6% | U.S., China, Japan, South Korea, Taiwan | Supports precision manufacturing. |

Pharmaceutical and medical device inspection | +4.8% | North America and Europe | Adds regulated value. |

Food and beverage safety inspection | +4.0% | Global processing markets | Improves safety compliance. |

Edge AI and robotic vision systems | +3.5% | Smart factories globally | Expands automation use. |

Challenges Impact Analysis

The main challenge is maintaining inspection accuracy across different product types, defect sizes, materials, speeds, and lighting conditions. AI systems must detect small and rare defects while avoiding false positives that slow production. Another challenge is proving return on investment. Manufacturers need clear benefits in lower scrap rates, less rework, higher throughput, better compliance, and lower labor dependency before scaling AI inspection across multiple production lines.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Detecting rare and complex defects | -3.0% | Electronics, pharma, automotive | Raises model training difficulty. |

Reducing false positives and false negatives | -2.6% | High-speed production lines | Protects inspection reliability. |

Proving ROI for plant-wide rollout | -2.2% | Manufacturing enterprises | Affects investment decisions. |

Maintaining camera and lighting calibration | -1.9% | Factory environments | Supports consistent output. |

Managing production data security | -1.6% | Connected industrial systems | Reduces cyber and IP risk. |

Recent Developments

Market News

In March 2026, Cognex released AI machine vision research based on more than 500 manufacturers, OEMs, and system integrators, showing that 57% already use AI in machine vision and another 30% plan near-term deployments.

In March 2026, UnitX launched FleX, an AI-driven inline visual inspection platform designed to reduce escape rates, improve deployment speed, and support advanced defect detection on complex surfaces.

In March 2026, MVTec announced MERLIC 26.03 with new features for easier integration and use of machine vision, supporting manufacturers with more accessible visual inspection workflows.

In April 2026, Basler introduced a complete CoaXPress-over-Fiber TDI vision system, including a TDI line scan camera, frame grabber, software, cooling solutions, and components for high-speed inspection applications.

In May 2026, MVTec announced HALCON 26.05, with a focus on speed and performance improvements for AI-based and rule-based machine vision methods.

In May 2026, Overview AI and Advantech demonstrated an edge AI vision inspection setup at Computex 2026, combining Advantech ICAM image acquisition with Overview AI deep learning inference for factory-floor inspection.

Acquisitions

In May 2026, Mistral AI entered into a definitive agreement to acquire Emmi AI, a Physics AI company focused on industrial engineering workflows. While this is broader than visual inspection, it is relevant because industrial AI is increasingly being used in defect monitoring, simulation, digital twins, and production optimization.

In 2026, direct acquisitions of pure-play AI visual inspection system companies remained limited in verified public sources. Most larger players appear to be building capabilities internally or expanding through hardware-software ecosystems rather than buying standalone visual inspection startups.

Funding

In May 2026, Scope raised USD 20.1 million in Series A funding led by Index Ventures to expand its AI-powered inspection workflow platform for the testing, inspection, and certification industry.

In May 2026, Scope also reported strong operational traction, including 9x ARR growth since launch, 100% pilot conversion, and usage by inspectors from six of the top ten global inspection companies.

In May 2025, Frinks AI raised USD 5.4 million in Pre-Series A funding led by Prime Venture Partners to expand Vision AI tools for visual inspection in sectors such as automotive and medical devices.

In May 2025, Prime Venture Partners said Frinks AI was building manufacturing-specific vision models for quality control and visual inspection, including real-time performance below 100 milliseconds and a no-code platform for custom inspection workflows.

Market Impact

In 2026, AI visual inspection is moving from basic defect detection to full quality intelligence. Manufacturers are now looking for systems that can detect small surface defects, verify labels, inspect packages, classify anomalies, support 3D inspection, and generate usable quality data for factory operations.

In 2026, usability is becoming as important as accuracy. Cognex’s research shows that experienced AI vision users place higher value on easier scaling, faster deployment, audit trails, lower data requirements, and reduced dependence on specialist teams.

In 2026, edge deployment is becoming a major requirement. Overview AI and Advantech’s setup shows that manufacturers want inspection models to run locally on industrial camera systems without cloud round trips, especially in high-volume production environments where cycle time and reliability are critical.

In 2026, synthetic defect generation is becoming more important for new product introduction. UnitX’s FleX-Gen and 2026 research on few-shot defect synthesis both show that manufacturers are trying to reduce the need for large real-world defect datasets before deploying inspection models.

Research Methodology

Step 1: Primary Research - Primary research is conducted through direct discussions with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. These interviews help understand real market demand, pricing movement, supply chain conditions, production trends, and customer requirements.

Step 2: Secondary Research - Secondary research is carried out using company filings, annual reports, regulatory databases, government publications, trade association data, and verified industry sources. This step helps collect reliable background information and supports the overall market assessment.

Step 3: Data Validation - Collected data is validated through source triangulation, historical trend review, demand-side checks, and supply-side assessment. Multiple sources are compared to reduce errors and improve the accuracy of the final insights.

Step 4: Market Estimation - Market estimation is completed using both bottom-up and top-down approaches. Product demand, regional consumption, company presence, application-level usage, and end-use industry adoption are reviewed to estimate the market size and structure.

Step 5: Forecasting Approach - Market forecasts are prepared by studying regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. This approach helps identify future growth patterns and possible market changes.

Step 6: Quality Review - The final data and findings are reviewed by analysts through peer validation, outlier checks, internal consistency checks, and final publication approval. This ensures that the report maintains accuracy, clarity, and research quality.

Step 7: AI Policy - AI is not used as a primary data source. All published insights are checked against human-verified evidence, and final conclusions are reviewed by analysts before publication.

Market Concentration

The AI Visual Inspection System Market is moderately fragmented, with established machine vision companies, industrial automation suppliers, camera manufacturers, AI software developers, and specialized inspection firms competing across manufacturing applications. Large providers maintain strong positions through integrated cameras, sensors, processors, software platforms, technical support, and existing relationships with industrial customers. However, no small group of companies controls the full market because inspection requirements vary significantly by product, production environment, defect type, and industry.

Competition is increasing as specialized providers introduce AI-based solutions for surface defect detection, assembly verification, component identification, packaging inspection, dimensional checks, and predictive quality control. New systems are being designed for electronics, automotive, pharmaceuticals, food processing, semiconductors, metals, and consumer goods. Research has also demonstrated that AI inspection systems can deliver high defect-detection performance when computer vision, anomaly detection, and optical character recognition are combined.

Market concentration is expected to remain balanced as large automation companies expand complete inspection platforms while smaller firms focus on industry-specific models, edge AI, low-code configuration, and customized deployment. The growing need for consistent quality, lower inspection costs, faster production lines, and reduced human error will support wider adoption. However, data availability, system validation, integration complexity, lighting conditions, and model reliability will continue to influence vendor selection.

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Information and Technology

Cloud Computing Market Size to Surpass USD 17.5 Trillion by 2035

Global Cloud Computing Market Size, Share Analysis By Type (Public Cloud, Private Cloud, Hybrid Cloud), By Service Model (Software as a Service, Infrastructure as a Service, Platform as a Service), By Enterprise Type (Large Enterprises, Small and Medium Enterprises), By Industry (BFSI, IT and Telecommunications, Government, Consumer Goods and Retail, Healthcare, Manufacturing, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Agentic AI For Financial Services Market Size to Reach USD 315.5 billion by 2035

Agentic AI For Financial Services Market Size, Share Segmented by Application (Fraud Detection and Anti-Money Laundering, Virtual Assistants and Chatbots, Credit Assessment, Risk and Compliance Management, Investment Advisory, Claims Processing, and Others), By Component (Solutions and Services), By Deployment Mode (Cloud, On-Premise, and Hybrid), By End-User (Commercial Banks, Investment Banks, Asset Management Firms, and Other Financial Institutions), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Agentic AI in HR & Recruitment Market Size to Reach USD 120.5 billion by 2035

Global Agentic AI in HR & Recruitment Market Size, Go-to-Market and Sales Strategy Analysis By Deployment Mode (Cloud-Based, On-Premises), By Enterprises (Small and Medium Enterprises (SMEs), Large Enterprises), By Application (Talent Acquisition & Recruitment, Employee Onboarding, Employee Engagement & Retention, Workforce Analytics, Others), By End-User Industry (IT & Telecommunications, Healthcare, Retail & E-commerce, BFSI, Manufacturing, Education, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

AI in Pulp and Paper Industry Market Size to Reach USD 21.3 Bn by 2035

Global AI in Pulp and Paper Industry Market Size, Go-to-Market and Sales Strategy Analysis By Component (Software, Hardware, Services), By Application (Process Optimization, Quality Control, Predictive Maintenance, Supply Chain Management, Others), By End User (Paper Manufacturers, Pulp Producers, Packaging Industry), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035