Revenue, 2025

$2.3 Trillion

Forecast, 2035

$17.5 Trillion

CAGR, 2025-2035

22.5%

Report Coverage

Global

Market Size and Forecast

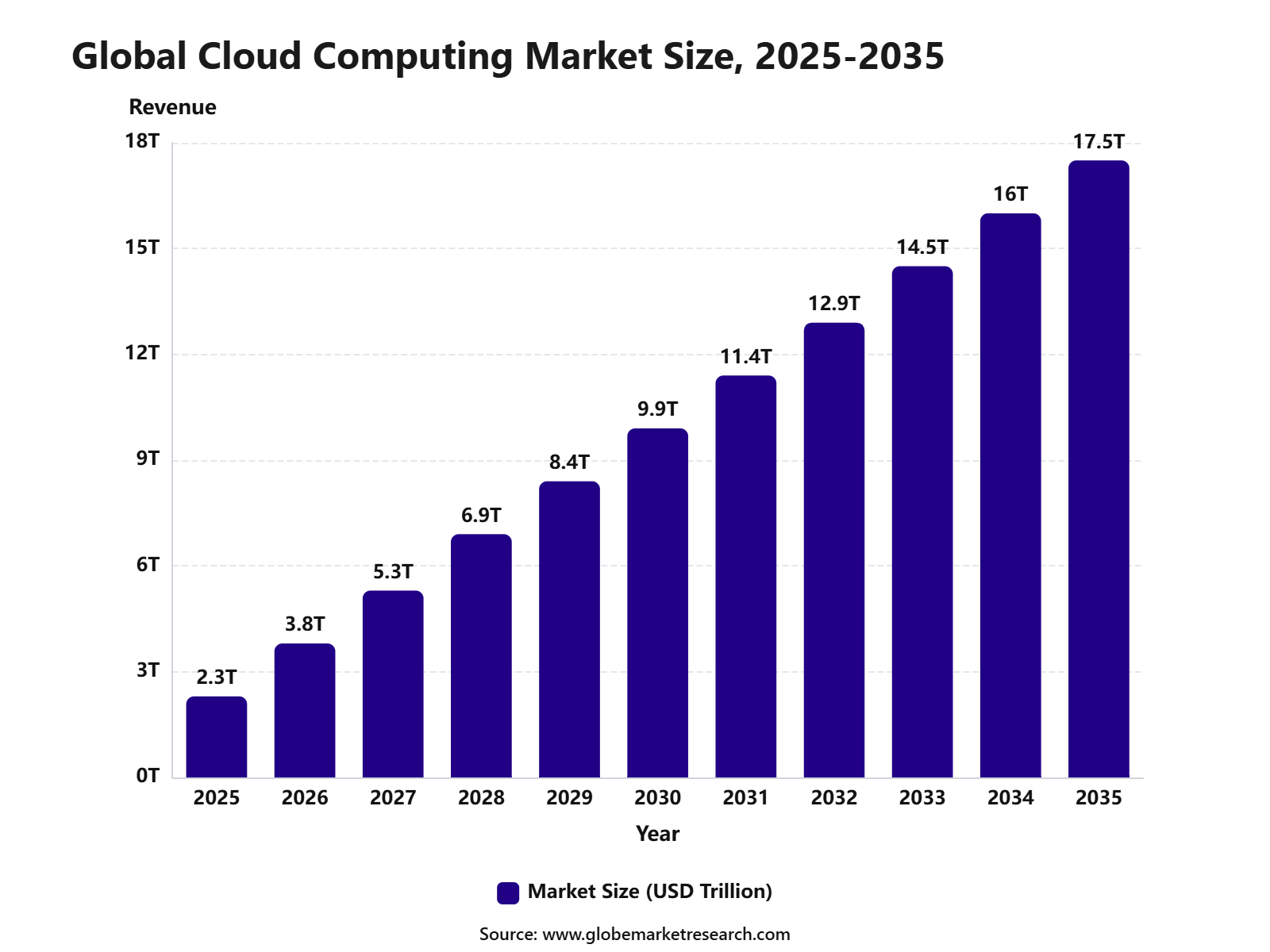

The Global Cloud Computing Market was worth USD 2.3 trillion in 2025 and is expected to reach USD 17.50 trillion by 2035, growing at a CAGR of 22.5% from 2025 to 2035. The growth of the market can be attributed to rising enterprise cloud migration, stronger demand for scalable computing, higher use of AI workloads, and the expansion of hybrid and multi-cloud models. Worldwide public cloud end-user spending to reach USD 723.4 billion in 2025, while also stating that 90% of organizations are expected to adopt hybrid cloud through 2027.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 2.3 Trillion |

Projected Revenue, 2035 | USD 17.50 Trillion |

CAGR, 2025-2035 | 22.5% |

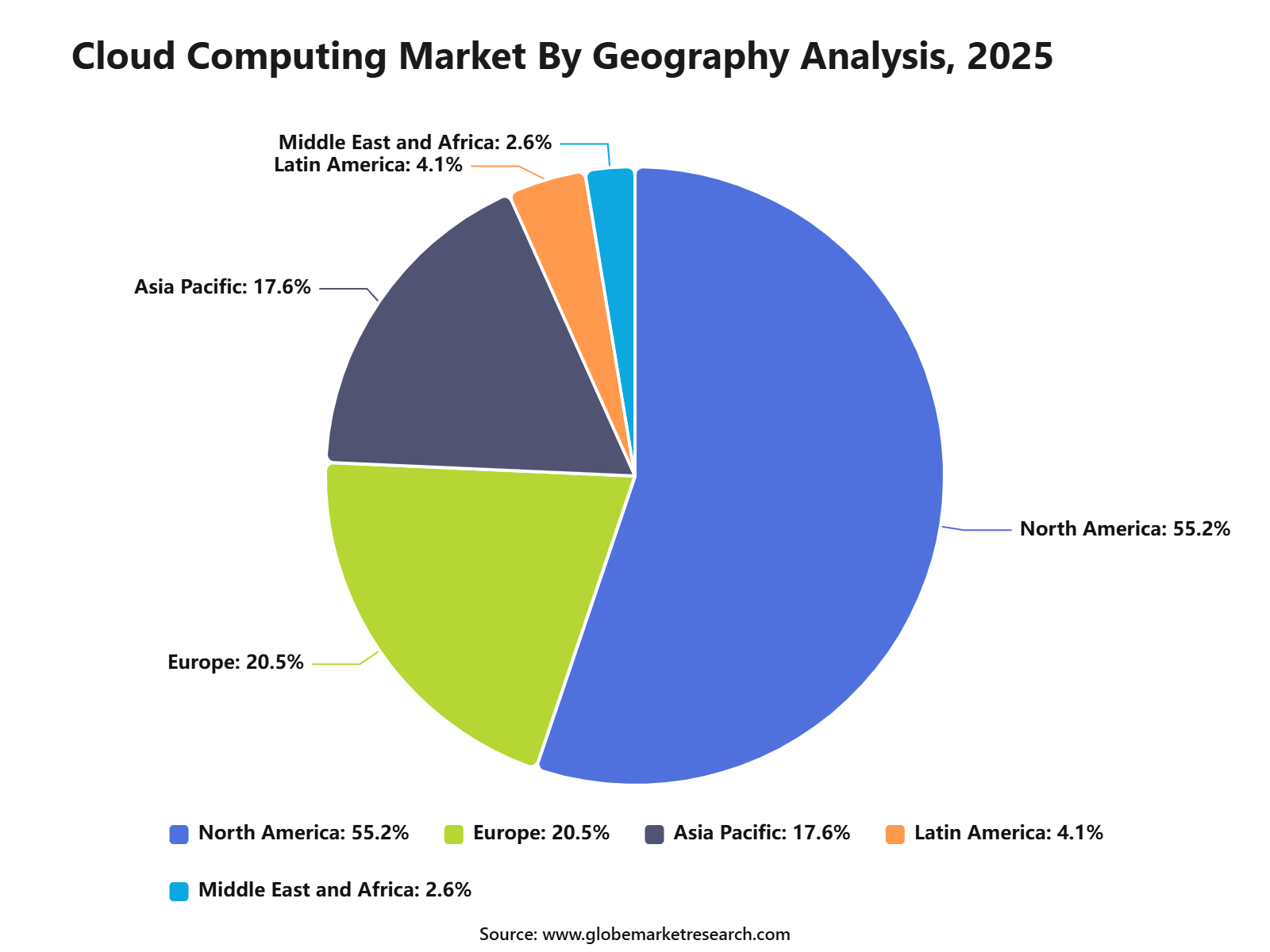

Largest Region | North America (55.2% market share) |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

The Cloud Computing Market includes infrastructure, platforms, software, storage, networking, databases, analytics, security, development tools, and cloud-based business applications delivered through internet-based systems. These services are used across public cloud, private cloud, hybrid cloud, and multi-cloud environments by enterprises, small businesses, governments, healthcare providers, financial institutions, retailers, manufacturers, and digital service companies. Gartner also noted that cloud compute resources used for AI workloads may increase from less than 10% today to 50% by 2029, showing the rising role of cloud infrastructure in AI deployment.

The market outlook remains highly positive as businesses are shifting from traditional IT ownership to flexible, subscription-based, and usage-based cloud models. Growth can be attributed to rising adoption of generative AI, SaaS platforms, cloud-native applications, data analytics, cybersecurity tools, disaster recovery, and edge computing. Flexera reported that enterprise cloud workloads increased from 52% to 54%, while small and medium business cloud workloads rose from 55% to 63% year-over-year, indicating wider cloud usage across business sizes.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFMarket Key Insights

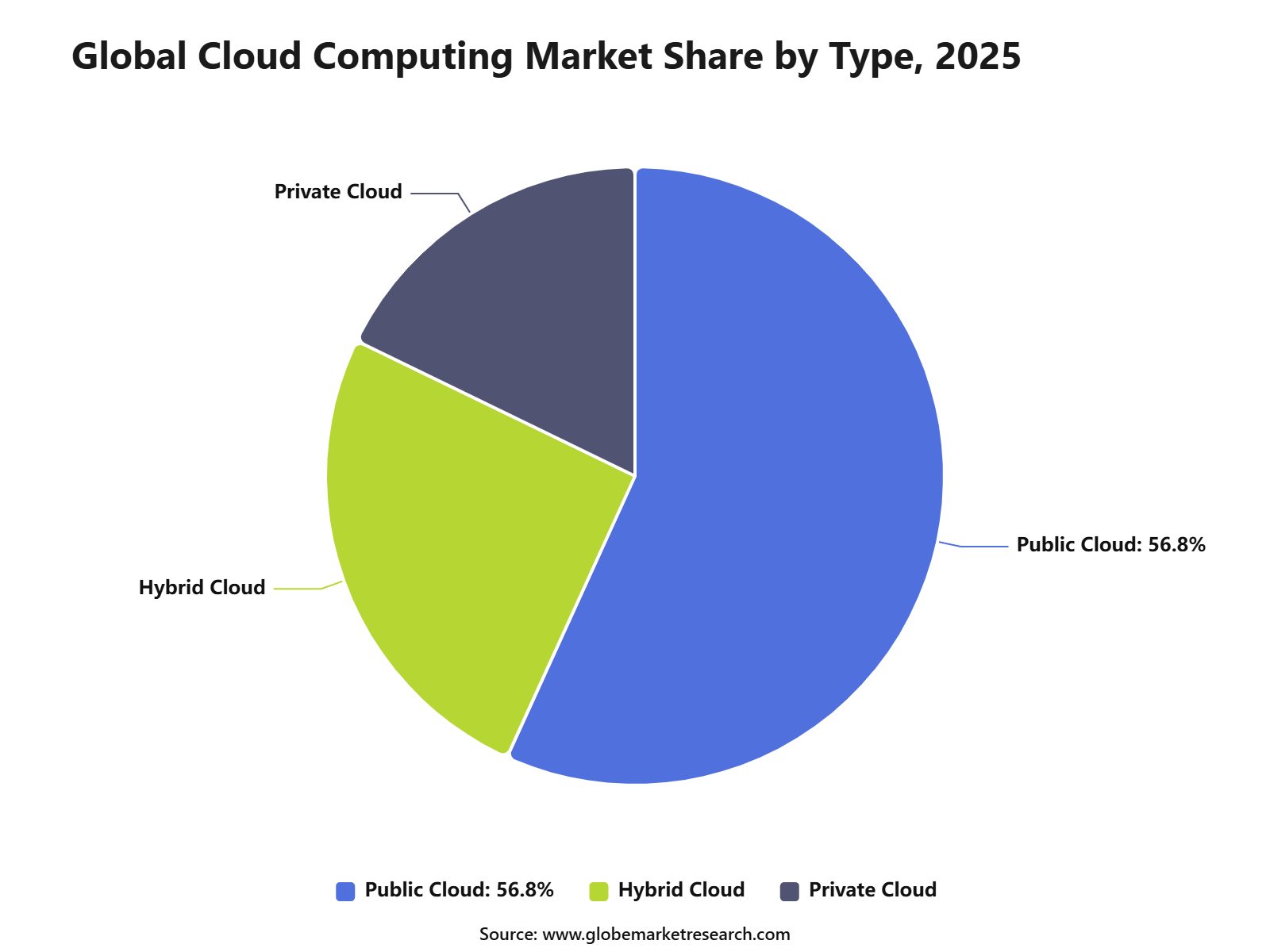

Public cloud led the type segment with 56.8% share, supported by flexible scalability, lower infrastructure costs, faster deployment, and strong adoption across enterprise digital operations.

Software as a Service accounted for 53.7% share by service model, driven by rising use of cloud-based business applications, collaboration tools, CRM platforms, analytics software, and productivity solutions.

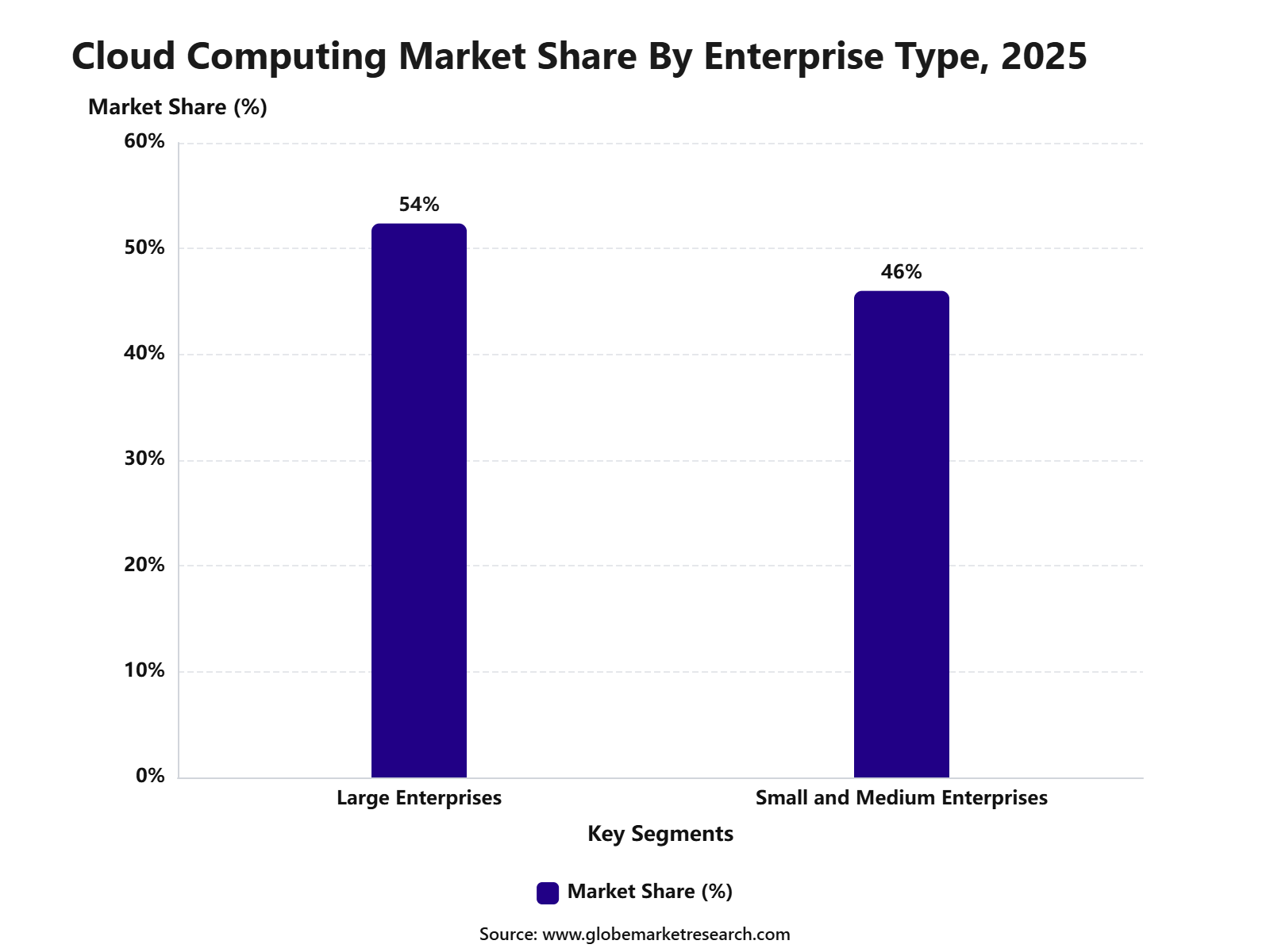

Large enterprises held 54.0% share by enterprise type, supported by higher IT budgets, complex data needs, multi-cloud strategies, and wider adoption of cloud-based automation and security systems.

IT and telecommunications captured 27.30% share by industry, driven by high data traffic, digital service delivery, network modernization, cloud-native applications, and demand for scalable computing infrastructure.

North America led the cloud computing market with 55.2% share, supported by strong hyperscale cloud infrastructure, early enterprise adoption, advanced digital transformation, and high spending on cloud-based technologies.

Adoption and Usage Insights

Cloud Computing Adoption Rate Statistics

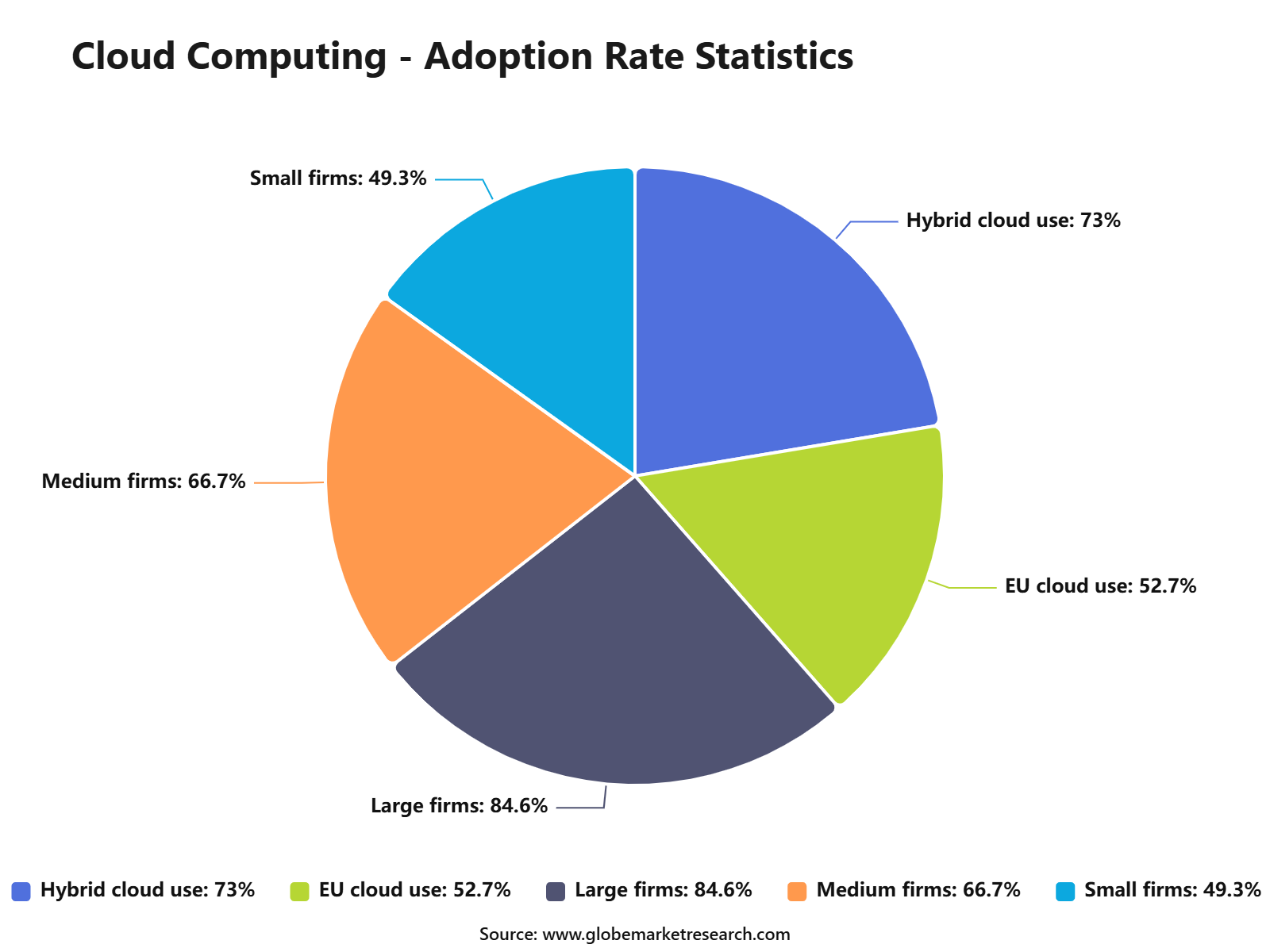

According to Eurostat, Cloud computing adoption continues to increase as enterprises shift toward hybrid cloud, cloud governance, AI workloads, and cost-managed infrastructure. Recent indicators show that 73% of organizations use hybrid cloud, while 52.74% of EU enterprises used paid cloud services in 2025. Adoption is highest among large enterprises at 84.67%, followed by medium firms at 66.78% and small firms at 49.3%. The rise of cloud centers of excellence, FinOps teams, and GenAI workloads shows that cloud is now being used as a core business infrastructure, not only as an IT hosting model.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFCloud Computing Usage Area Statistics

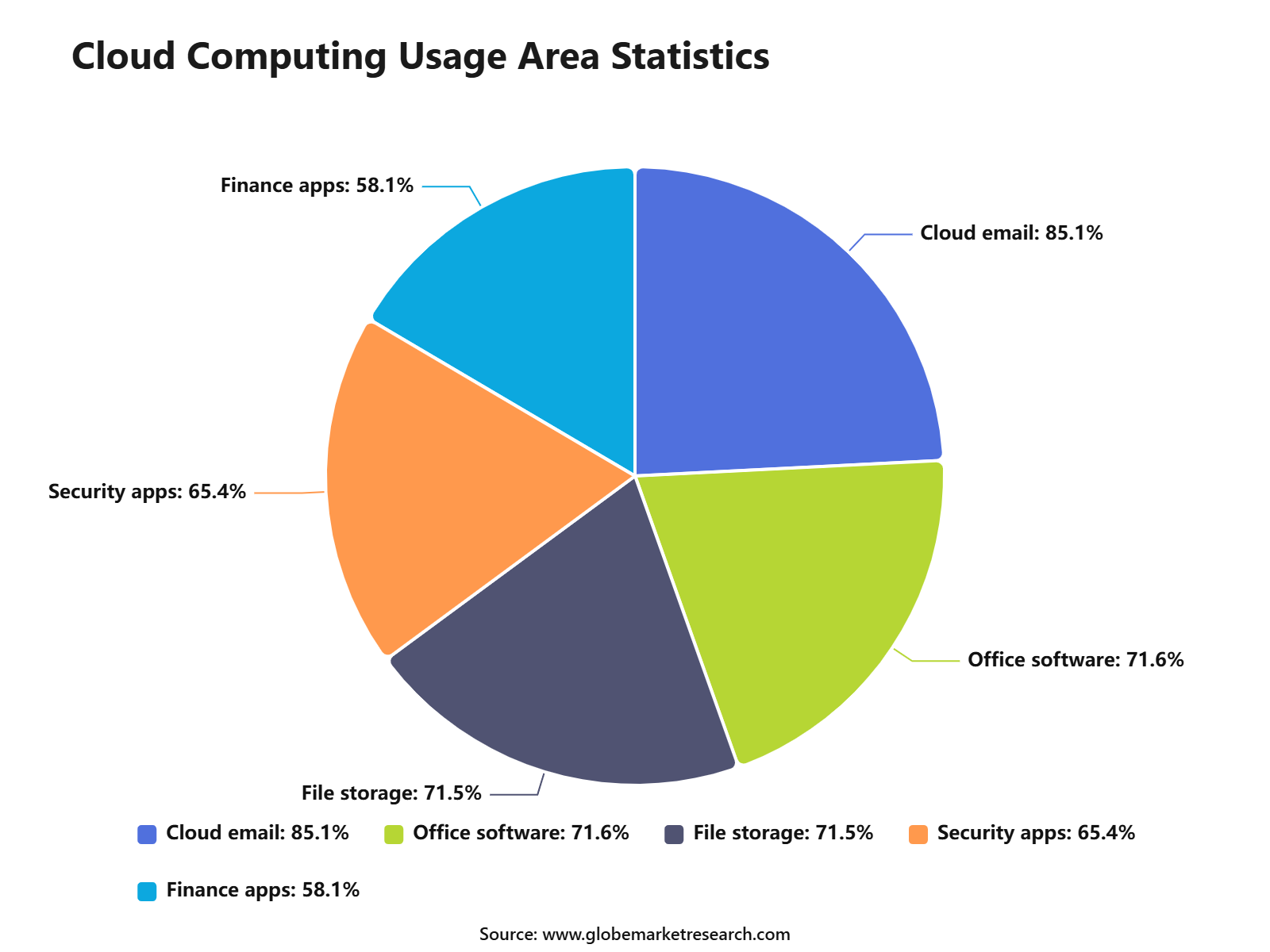

Cloud computing is mainly used for email, office software, file storage, security applications, finance software, databases, ERP, CRM, computing power, and application development. Among enterprises using paid cloud services, email usage reached 85.15%, office software stood at 71.69%, file storage reached 71.53%, and cloud security applications accounted for 65.49%. These usage patterns show that cloud platforms are supporting daily business operations, remote collaboration, data protection, software modernization, and AI-ready digital transformation across industries.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFType Analysis

Public Cloud led the Cloud Computing Market with 56.8% share, supported by strong demand for scalable computing, storage, networking, analytics, security, and AI-ready infrastructure. Enterprises prefer public cloud because it reduces the need for large internal data center investments and allows faster deployment of digital services. The growth of this segment can be attributed to rising use of cloud-native applications, generative AI workloads, hybrid cloud strategies, and remote business operations.

Public cloud services spending was forecast to reach USD 723.4 billion in 2025, with all cloud segments expected to record double-digit growth. Public Cloud is expected to remain the leading type as companies continue to shift workloads from traditional IT infrastructure to flexible cloud platforms. Future demand will remain supported by AI model deployment, enterprise data platforms, cybersecurity tools, application modernization, cloud storage, and industry-specific digital services.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFService Model Analysis

Software as a Service led the service model segment with 53.7% share, supported by wide use of cloud-based business applications across finance, sales, marketing, customer service, human resources, collaboration, and enterprise resource planning. SaaS is preferred because it offers subscription-based access, faster implementation, automatic updates, and lower maintenance needs. The dominance of this segment can be linked to the rising adoption of digital workplace tools and business automation software.

SaaS spending was forecast to reach USD 299.1 billion in 2025, making it one of the largest public cloud service categories by end-user spending. Software as a Service is expected to remain the leading service model as companies replace legacy software with cloud-delivered applications. Future growth will be supported by AI-enabled SaaS tools, customer data platforms, cybersecurity software, HR technology, productivity suites, industry cloud applications, and subscription-based enterprise software.

Enterprise Type Analysis

Large Enterprises led the enterprise type segment with 54.0% share, supported by higher IT budgets, complex application portfolios, global operations, and stronger demand for hybrid and multi-cloud environments. Large companies use cloud computing to improve scalability, data access, business continuity, application development, and digital customer experience. The growth of this segment can be attributed to the rising movement of enterprise workloads and data into public cloud and SaaS environments.

Flexera reported that enterprise workloads running in public cloud increased from 52% to 54%, while 51% of enterprise data was already in public cloud. Large Enterprises are expected to remain the leading buyer group as cloud becomes central to AI adoption, analytics, cybersecurity, application modernization, and global IT operations. Demand will remain strong among banks, telecom operators, retailers, healthcare groups, manufacturers, and technology companies with high data and application needs.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFIndustry Analysis

IT and Telecommunications led the industry segment with 27.30% share, supported by high demand for cloud infrastructure, software development platforms, network virtualization, data storage, cybersecurity, and AI-enabled service delivery. This industry depends heavily on cloud systems to manage digital platforms, customer data, telecom networks, enterprise applications, and real-time services.

The dominance of this segment can be attributed to rapid cloudification of telecom networks and strong use of cloud platforms by IT service providers. IBM and GSMA Intelligence noted that telecom companies are using cloud and AI to improve network operations, security, customer experience, automation, and new service development.

IT and Telecommunications is expected to remain the leading industry segment as 5G, edge computing, AI services, cloud-native networks, and enterprise connectivity continue to expand. Future opportunities are likely to remain strong in telecom cloud, network automation, managed cloud services, cybersecurity platforms, AI infrastructure, and cloud-based digital operations.

Geography Analysis

North America led the Cloud Computing Market with 55.2% share, supported by strong enterprise cloud adoption, mature hyperscale infrastructure, high digital spending, and the presence of major cloud service providers. The region has a large base of cloud users across technology, finance, healthcare, retail, media, telecom, manufacturing, and public-sector organizations.

The region’s dominance can be attributed to strong demand from U.S. enterprises and continued investment in cloud infrastructure. Enterprise cloud spending reached USD 129 billion in the first quarter of 2026, rising 35% year over year, while the U.S. remained the largest cloud market and exceeded the full APAC region in size.

North America is expected to remain the leading regional market as companies expand cloud use for AI, analytics, cybersecurity, SaaS applications, data platforms, and digital customer services. Future demand will remain supported by hyperscale data centers, cloud-native software development, enterprise AI workloads, regulated industry cloud adoption, and strong public cloud consumption.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFSegment Covered in the Report

By Type

Public Cloud

Private Cloud

Hybrid Cloud

By Service Model

Software as a Service

Infrastructure as a Service

Platform as a Service

By Enterprise Type

Large Enterprises

Small and Medium Enterprises

By Industry

BFSI

IT and Telecommunications

Government

Consumer Goods and Retail

Healthcare

Manufacturing

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

The Cloud Computing Market is driven by rising demand for scalable infrastructure, enterprise digital transformation, AI workloads, SaaS platforms, data storage, cybersecurity services, cloud-native applications, and hybrid cloud deployment. Companies are shifting from traditional IT systems to cloud platforms to improve flexibility, speed, automation, and cost control.

North America leads the market due to strong enterprise cloud adoption, mature hyperscale infrastructure, high technology spending, and early use of AI, analytics, and platform-as-a-service models. The U.S. remains the main regional contributor because large enterprises, software companies, financial institutions, healthcare firms, and government agencies rely heavily on cloud services.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Enterprise digital transformation | +6.4% | North America, Europe, Asia Pacific | Drives core cloud adoption. |

Rising AI and machine learning workloads | +5.8% | U.S., Canada, Europe, Asia Pacific | Increases cloud compute demand. |

Growth in SaaS applications | +4.9% | Global enterprise markets | Builds recurring cloud revenue. |

Demand for scalable data storage | +4.1% | Large enterprises and SMEs | Supports workload migration. |

Expansion of remote and hybrid work models | +3.5% | North America and Europe | Strengthens cloud collaboration use. |

Restraints Impact Analysis

The market faces restraints from data privacy concerns, cloud security risks, vendor lock-in, high migration cost, and complex compliance requirements. Enterprises must protect sensitive data while meeting industry-specific rules across banking, healthcare, government, retail, and manufacturing. Another restraint is cloud cost management. As workloads increase, many companies face higher-than-expected spending due to unused resources, poor architecture, data transfer fees, and limited visibility into multi-cloud environments.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Data privacy and security concerns | -3.4% | North America, Europe, Asia Pacific | Slows sensitive workload migration. |

Vendor lock-in risk | -2.9% | Large enterprise cloud users | Limits platform flexibility. |

Cloud cost overruns | -2.5% | Global cloud customers | Pressures IT budgets. |

Compliance and data residency rules | -2.1% | Regulated industries | Adds deployment complexity. |

Legacy system migration challenges | -1.8% | Traditional enterprises | Delays cloud modernization. |

Opportunities Impact Analysis

Opportunities are strong in AI cloud infrastructure, hybrid cloud, multi-cloud management, edge cloud, cloud security, data platforms, industry cloud, serverless computing, and cloud-based business applications. These areas benefit from enterprise demand for speed, automation, and specialized digital infrastructure. Higher-value opportunities are emerging in generative AI platforms, cloud-native cybersecurity, sovereign cloud, healthcare cloud, financial services cloud, cloud data lakes, and application modernization services. Providers that combine performance, security, compliance, and cost optimization can capture stronger long-term demand.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

AI cloud infrastructure expansion | +6.2% | North America, Europe, Asia Pacific | Builds premium compute demand. |

Hybrid and multi-cloud management | +5.1% | Large enterprises globally | Improves platform flexibility. |

Cloud security services | +4.4% | Regulated and data-heavy industries | Adds trust-led adoption. |

Industry-specific cloud platforms | +3.8% | Healthcare, BFSI, manufacturing, retail | Supports vertical growth. |

Edge cloud and low-latency workloads | +3.2% | Telecom, IoT, manufacturing, automotive | Expands distributed computing. |

Challenges Impact Analysis

The main challenge is managing cloud complexity across multiple platforms, applications, regions, and compliance systems. Enterprises need strong architecture, governance, security policies, and cost controls to use cloud efficiently. Another challenge is talent shortage. Cloud engineering, DevOps, cybersecurity, data engineering, and AI infrastructure skills are essential for successful deployment, but many organizations still lack enough trained professionals.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Multi-cloud management complexity | -3.0% | Large enterprises | Increases operational burden. |

Cloud skill shortages | -2.6% | Global enterprise markets | Slows project execution. |

Cybersecurity threat exposure | -2.4% | Public and hybrid cloud users | Raises risk management needs. |

Data transfer and latency issues | -2.0% | Global distributed workloads | Affects performance planning. |

Cloud governance gaps | -1.7% | Enterprise IT teams | Weakens cost and security control. |

Go-to-Market and Sales Economics

According to Globe Market Research, the go-to-market approach for the Cloud Computing Market should focus on AI-ready infrastructure, secure migration, hybrid cloud, industry cloud and cost governance. Enterprises are no longer buying cloud only for storage and basic computing. They are buying scalable platforms for AI workloads, data analytics, cybersecurity, app modernization, backup, disaster recovery and digital operations. Microsoft reported that Azure and other cloud services revenue grew 40% in its FY2026 Q3, supported by demand across platform workloads.

Sales economics are being shaped by large enterprise cloud contracts and rising demand for AI compute capacity. AWS segment sales increased 28% year over year to USD 37.6 billion in Q1 2026, while AWS operating income reached USD 14.2 billion. This shows that cloud providers with strong compute, storage, database, AI and security portfolios can convert infrastructure demand into high operating income.

The strongest commercial model is a bundled cloud platform model, where infrastructure, managed databases, AI services, cybersecurity, developer tools and professional services are sold together. Google Cloud revenue rose 63% to USD 20 billion in Q1 2026, while cloud operating income reached USD 6.6 billion and operating margin improved to 32.9%. This indicates that AI, data platforms and enterprise cloud services are becoming major revenue engines for hyperscale providers.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is spread across infrastructure-as-a-service, platform-as-a-service, software-as-a-service, database cloud, cloud security, AI cloud, edge cloud, backup, disaster recovery, cloud migration and managed services. Oracle reported Q4 FY2026 total cloud revenue of USD 9.9 billion, up 47%, while cloud infrastructure revenue reached USD 5.8 billion, up 93%. This shows that cloud revenue is expanding beyond the largest hyperscalers as enterprises look for more AI infrastructure capacity.

SaaS and cloud-based business applications are also creating a strong revenue layer. Flexera’s 2026 cloud report noted that the largest group of SaaS spenders, at 18% of respondents, reported monthly spending between USD 200,001 and USD 500,000. This supports demand for subscription-based software, cloud cost management, identity tools, collaboration platforms and integration services.

AI workloads are now one of the strongest drivers of cloud infrastructure demand. Flexera reported in 2026 that 81% of respondents were using generative AI, compared with 72% in the previous year, while wasted cloud spend increased to 29%. This creates revenue opportunities for cloud optimization, FinOps, GPU scheduling, workload placement, usage monitoring and managed AI infrastructure services.

Financial Impact

The financial impact of cloud computing is mainly linked to faster scalability, lower upfront infrastructure ownership, improved software deployment speed and better access to advanced AI tools. However, cloud cost discipline is becoming critical. Flexera reported that 76% of large enterprises now spend more than USD 5 million per month on public cloud, showing why cloud governance, workload rightsizing and contract optimization are becoming direct financial priorities.

Capital spending and infrastructure intensity are increasing as cloud providers build AI-ready data centers. Alphabet said its Q1 2026 capital expenditure was USD 35.7 billion, with most of the spend directed toward technical infrastructure. It also raised its full-year 2026 capital expenditure guidance to USD 180 billion to USD 190 billion, reflecting strong internal and external demand for AI compute resources.

Energy use is becoming one of the main cost and risk factors for cloud providers and large customers. The IEA projects that global data center electricity consumption will double to around 945 TWh by 2030, with AI being the most important growth driver. This makes power sourcing, cooling efficiency, renewable energy contracts, location strategy and data center utilization important financial levers for the Cloud Computing Market.

Recent Developments

Market News

In January 2026, Oracle expanded its AI infrastructure roadmap with Oracle Cloud Infrastructure projects in Texas, New Mexico, Wisconsin, and Michigan to support large-scale AI workloads.

In February 2026, Microsoft expanded Sovereign Private Cloud with Azure Local, Microsoft 365 Local, and Foundry Local to support secure workloads in connected, hybrid, and fully disconnected environments.

In April 2026, AWS announced new cloud and AI updates, including Amazon Connect agentic AI solutions and expanded OpenAI model availability through Amazon Bedrock.

In April 2026, Google Cloud introduced Cloud Next ’26 updates, including 8th Generation TPUs, new storage and networking capabilities, Agentic Data Cloud, cross-cloud Lakehouse, and Knowledge Catalog.

Mergers

In April 2026, AWS and OpenAI expanded their cloud partnership by bringing OpenAI models to Amazon Bedrock and introducing Amazon Bedrock Managed Agents in limited preview.

In April 2026, Oracle and Google Cloud showcased new AI integrations and continued expansion of Oracle AI Database@Google Cloud at Google Cloud Next 2026.

Acquisitions

In February 2026, Snowflake closed its acquisition of Observe to add AI-powered observability for customers running critical data and AI workloads.

In March 2026, Google completed its acquisition of Wiz, strengthening Google Cloud’s multicloud security, hybrid cloud protection, and AI-era threat detection capabilities.

In July 2026, MasTec announced an agreement to acquire Superior Group in a USD 1.65 billion deal to expand electrical systems capabilities for hyperscale data center infrastructure.

Funding

In April 2026, CoreWeave’s newsroom highlighted Jane Street’s plan to invest USD 6.1 billion in CoreWeave’s AI cloud and USD 1.1 billion in equity, supporting high-performance cloud infrastructure growth.

In April 2026, Crusoe confirmed its USD 1.3 billion Series E funding round at a valuation above USD 10.1 billion to scale AI infrastructure and Crusoe Cloud.

In July 2026, Yotta Data Services raised around USD 150.1 million at a valuation of about USD 3.9 billion to accelerate AI and cloud infrastructure expansion.

In July 2026, SambaNova completed the first close of a USD 1.1 billion financing round at an USD 11.1 billion valuation to expand AI chips, integrated hardware systems, and cloud services for inference.

Market Impact

In 2026, cloud computing is becoming more AI-centered. Enterprises are no longer buying only virtual machines, storage, and databases. They are also buying GPU capacity, AI accelerators, managed agents, data governance, model deployment tools, and inference-ready infrastructure.

In 2026, sovereign cloud is becoming a stronger buying priority. Microsoft’s Sovereign Private Cloud and India’s Swaraj Cloud show that regulated sectors want cloud services that support local control, data residency, offline operations, and stronger compliance boundaries.

In 2026, multicloud security is becoming a major growth driver. Google’s Wiz acquisition shows that enterprises need security tools that work across public cloud, private cloud, hybrid infrastructure, and AI workloads instead of depending on single-cloud controls.

In 2026, AI cloud providers such as CoreWeave, Crusoe, Yotta, and SambaNova are gaining attention because demand for training and inference capacity is rising quickly. The strongest opportunities are expected in AI infrastructure, sovereign cloud, cloud security, cloud data platforms, hybrid cloud, and industry-specific cloud services.

Cloud Computing Market Concentration

The Cloud Computing Market is moderately consolidated, with a limited number of hyperscale providers holding strong positions across infrastructure, platforms, software, storage, networking, and AI-enabled cloud services. Their market influence is supported by large global data center networks, broad service portfolios, established enterprise relationships, high capital investment, and the ability to deliver secure and scalable computing resources across multiple regions.

Competition remains active because regional cloud providers, managed service companies, telecom operators, and specialized vendors continue to expand their presence. These participants compete through hybrid cloud services, industry-specific platforms, data sovereignty, cybersecurity, compliance support, and cost-efficient deployment models. Demand from regulated industries is also creating space for providers that can offer local hosting, stronger control over sensitive data, and customized cloud environments.

Market concentration is being reinforced by rising demand for AI workloads, advanced analytics, cloud-native applications, and enterprise modernization. Large providers are expected to retain an advantage due to their computing capacity, innovation resources, partner ecosystems, and acquisition strategies. However, the continued growth of hybrid cloud, sovereign cloud, edge computing, and specialized managed services is expected to preserve strong competition and create opportunities for emerging providers.

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

IBM Corporation

Oracle Corporation

Alibaba Cloud

Salesforce, Inc.

SAP SE

Adobe Inc.

VMware LLC

Tencent Cloud

Huawei Cloud

Dell Technologies

Cisco Systems, Inc.

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Prashant is a skilled research analyst with five years of practical experience in market intelligence, strategic research, and business consulting. His expertise covers primary research, secondary research, competitive benchmarking, and industry trend analysis across sectors such as semiconductors, automotive, transportation and logistics, machinery, and industrial equipment. Prashant focuses on delivering clear, data-backed insights that help clients understand market shifts, technology adoption, regulatory developments, and emerging growth opportunities.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Information and Technology

AI Visual Inspection System Market Revenue to Hit USD 315.2 billion by 2035

Global AI Visual Inspection System Market Size, Growth Analysis By Offering (Hardware Systems, Industrial Cameras, Sensors and Imaging Hardware, Software Platforms, AI Inspection Software, Vision Analytics Tools, Services), By Technology (Deep Learning-Based Vision Systems, Machine Learning Algorithms, Traditional Computer Vision Systems, Edge AI Vision Processing, Other AI Vision Technologies), By Application (Defect Detection & Quality Control, Assembly Verification, Measurement & Gauging, Packaging & Label Inspection, Other Industrial Inspection Applications), By Industry Vertical (Electronics & Semiconductor Manufacturing, Automotive Industry, Pharmaceuticals & Healthcare, Food & Beverage Manufacturing, Logistics & Warehousing, Other Industrial Verticals), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Agentic AI For Financial Services Market Size to Reach USD 315.5 billion by 2035

Agentic AI For Financial Services Market Size, Share Segmented by Application (Fraud Detection and Anti-Money Laundering, Virtual Assistants and Chatbots, Credit Assessment, Risk and Compliance Management, Investment Advisory, Claims Processing, and Others), By Component (Solutions and Services), By Deployment Mode (Cloud, On-Premise, and Hybrid), By End-User (Commercial Banks, Investment Banks, Asset Management Firms, and Other Financial Institutions), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Agentic AI in HR & Recruitment Market Size to Reach USD 120.5 billion by 2035

Global Agentic AI in HR & Recruitment Market Size, Go-to-Market and Sales Strategy Analysis By Deployment Mode (Cloud-Based, On-Premises), By Enterprises (Small and Medium Enterprises (SMEs), Large Enterprises), By Application (Talent Acquisition & Recruitment, Employee Onboarding, Employee Engagement & Retention, Workforce Analytics, Others), By End-User Industry (IT & Telecommunications, Healthcare, Retail & E-commerce, BFSI, Manufacturing, Education, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

AI in Pulp and Paper Industry Market Size to Reach USD 21.3 Bn by 2035

Global AI in Pulp and Paper Industry Market Size, Go-to-Market and Sales Strategy Analysis By Component (Software, Hardware, Services), By Application (Process Optimization, Quality Control, Predictive Maintenance, Supply Chain Management, Others), By End User (Paper Manufacturers, Pulp Producers, Packaging Industry), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035