Revenue, 2025

$16.9 Bn

Forecast, 2035

$112.8 Bn

CAGR, 2026-2035

20.9%

Report Coverage

Global

Market Size and Forecast

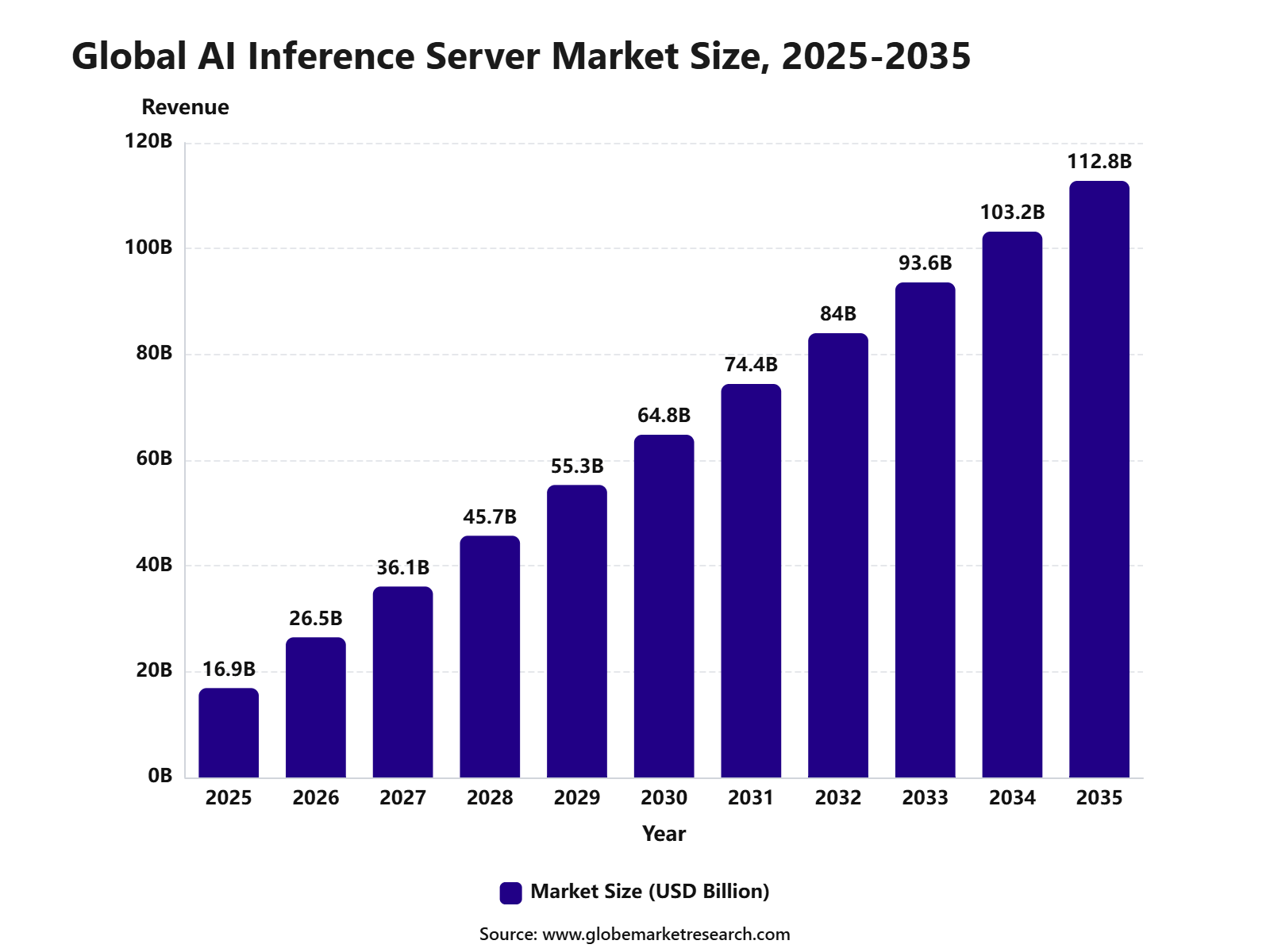

The Global AI Inference Server Market was worth USD 16.9 billion in 2025 and is expected to reach USD 112.8 billion by 2035, growing at a CAGR of 20.9% from 2025 to 2035. Based on this growth rate, the market is estimated to reach around USD 26.5 billion in 2026. North America held the largest regional share of 46.9% in 2025, supported by strong cloud AI infrastructure, hyperscale data center expansion, enterprise AI deployment, GPU server adoption, and growing demand for low-latency generative AI applications.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 16.9 Billion |

Projected Revenue, 2035 | USD 112.8 Billion |

CAGR, 2025-2035 | 20.9% |

Largest Region | North America, 46.9% Share |

Market Concentration | Medium to High |

Base Year | 2025 |

Forecast Period | 2025-2035 |

What is the AI Inference Server Market?

The AI Inference Server Market includes hardware and software infrastructure used to run trained AI models in real-time production environments. These servers process user queries, generate outputs, support AI agents, power recommendation systems, enable computer vision, and deliver chatbot, coding assistant, speech, security, healthcare, and industrial automation applications. The market is closely linked with GPU servers, AI accelerators, edge AI servers, rack-scale systems, inference software, high-speed networking, and energy-efficient data center architecture.

Growth can be attributed to rising adoption of generative AI, agentic AI, private AI deployment, real-time analytics, and AI-powered automation across cloud, data center, and edge environments. Demand is also being supported by the need for faster response times, lower cost per token, higher GPU utilization, and better energy efficiency in AI workloads. In 2026, IBM noted that AI spending is projected to rise from under 15% of IT budgets in 2025 to nearly 25% by 2027, showing stronger enterprise focus on scalable AI infrastructure and cost control.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Air cooling led the cooling type segment with 54.6% share, supported by lower infrastructure cost, easier deployment, and strong suitability for standard AI inference workloads.

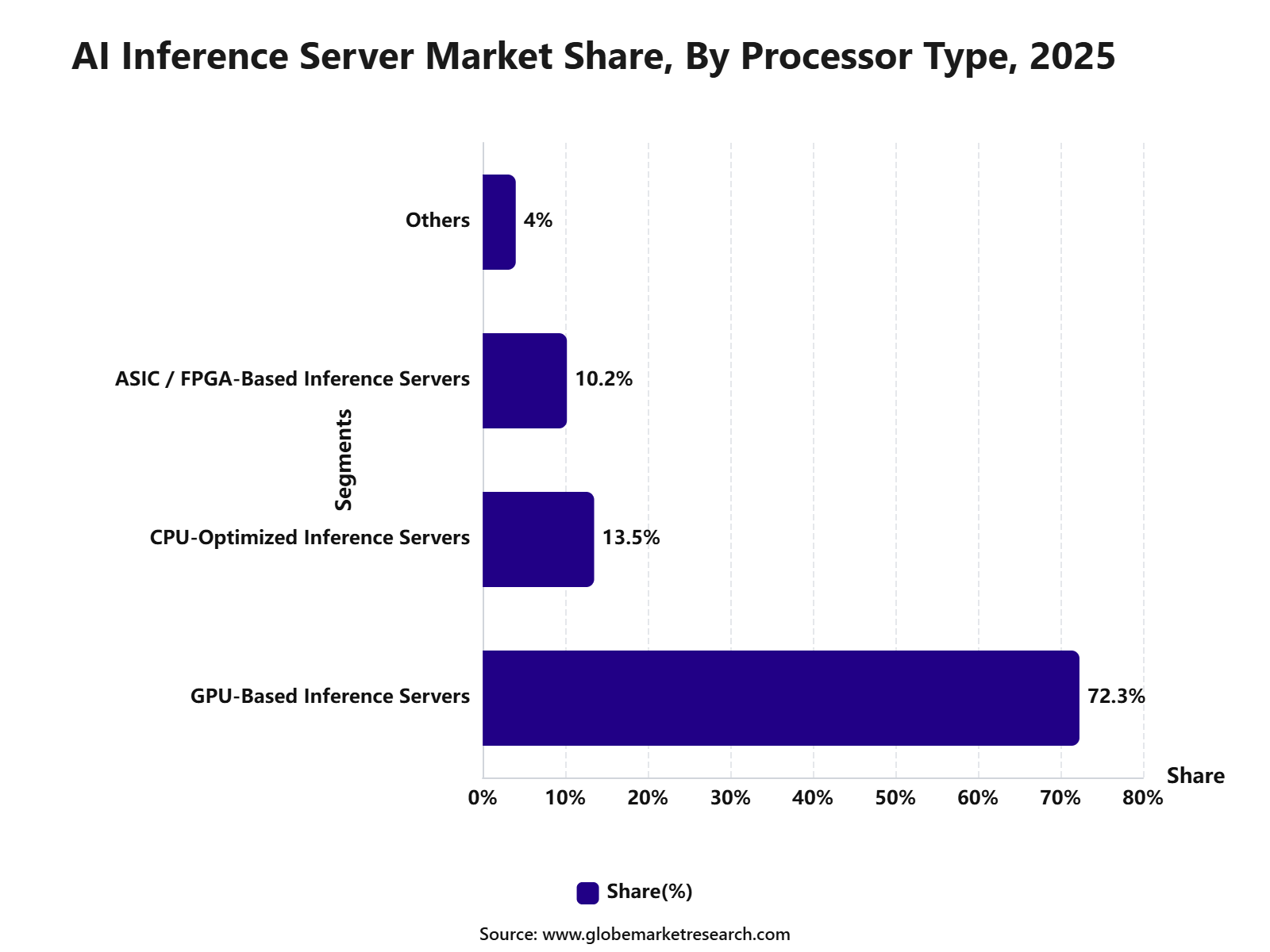

GPU-based inference servers accounted for 72.3% share, driven by high parallel processing capability, faster model execution, and strong use in generative AI, computer vision, and real-time analytics.

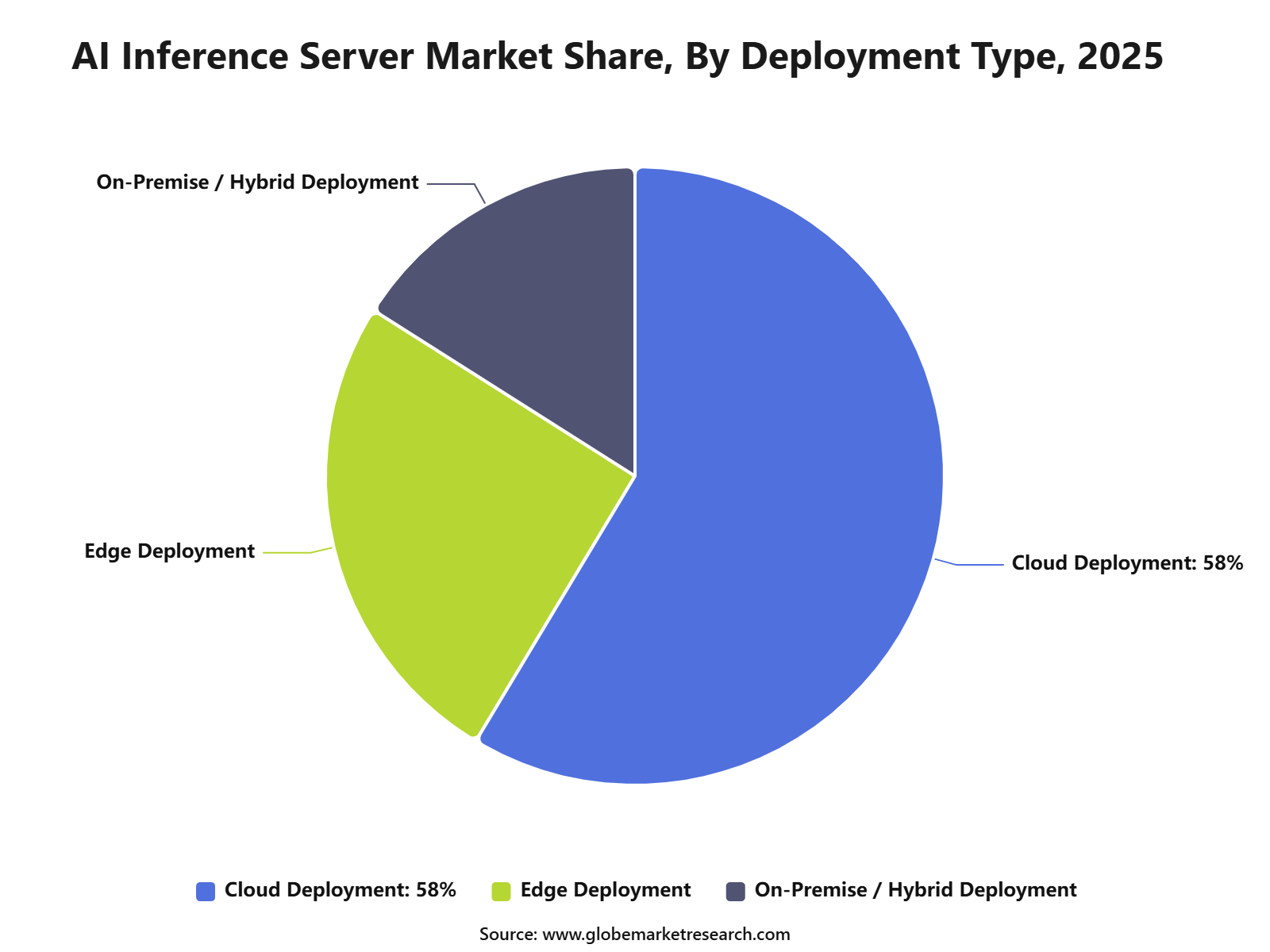

Cloud deployment held 58.6% share, supported by scalable infrastructure, flexible computing access, faster AI model deployment, and growing enterprise use of hosted inference services.

IT and communication captured 32.6% share by application, driven by rising demand for AI-powered networking, customer support automation, cybersecurity, data processing, and communication intelligence.

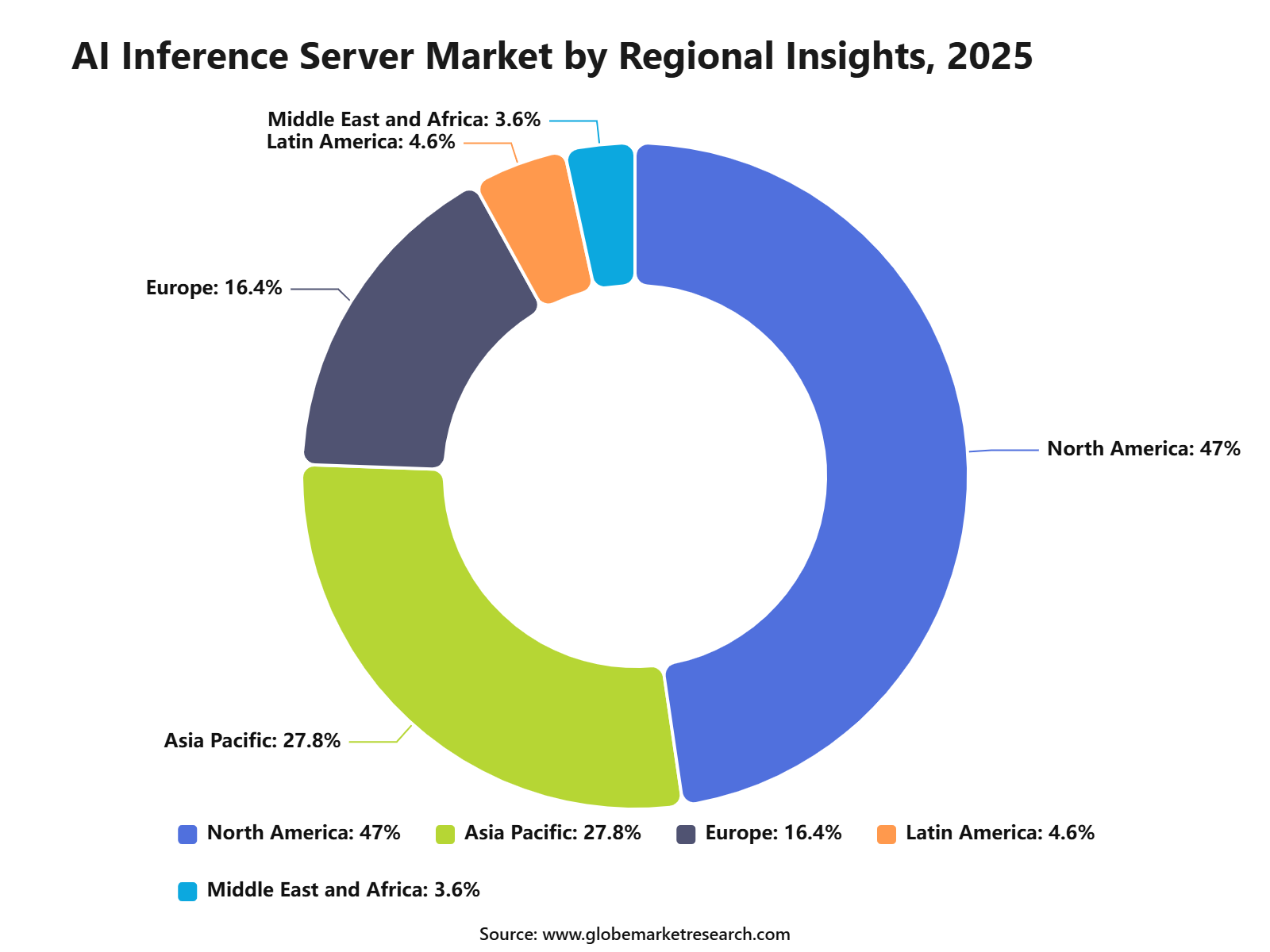

North America led the AI inference server market with 47.6% share, supported by strong cloud infrastructure, advanced AI adoption, major technology companies, and high investment in AI computing capacity.

Cooling Type Insights

Air cooling led the cooling type segment with 54.6% share. The segment remained dominant because it is simple to install, easier to maintain, and more cost-effective than advanced liquid cooling systems. Air cooling is widely used in traditional data center environments where AI inference workloads are moderate and server heat levels can be managed through standard airflow systems.

This makes it suitable for enterprises that are expanding AI capacity without making major changes to existing infrastructure. The segment is also supported by lower operational complexity. Many organizations prefer air cooling because it allows faster deployment of inference servers, reduces maintenance needs, and fits well with current rack-based server designs.

Processor Type Insights

GPU-based inference servers dominated the processor type segment with 72.3% share. GPUs are preferred because they can process several AI tasks at the same time and support fast response times for advanced AI applications. The segment is strongly supported by the rising use of generative AI, image recognition, recommendation engines, fraud detection, virtual assistants, and natural language processing.

These workloads require high parallel processing power, which makes GPU-based servers a practical choice. GPU-based inference servers also offer flexibility across different AI models and enterprise use cases. This has made them important for cloud providers, AI developers, data centers, and companies that need scalable infrastructure for real-time AI decision-making.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFDeployment Type Insights

Cloud deployment accounted for 58.6% share. The segment is leading because cloud infrastructure allows businesses to access AI inference capacity without building expensive in-house server environments. Cloud deployment is especially useful for companies that need flexible scaling.

AI workloads can rise sharply during peak usage periods, and cloud-based inference servers allow enterprises to adjust capacity based on demand. The segment also benefits from faster deployment cycles. Businesses can test, launch, and expand AI applications more quickly through cloud platforms, making this deployment model suitable for SaaS companies, digital platforms, and enterprise AI teams.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFApplication Insights

IT and communication led the application segment with 32.6% share. The segment is driven by the strong use of AI inference servers in network management, cybersecurity, customer service automation, virtual assistants, and real-time data processing.

Telecom and IT companies rely on AI inference infrastructure to improve service quality and reduce response delays. AI models are increasingly used to detect network issues, manage traffic, support automated troubleshooting, and improve customer interactions.

The segment is also gaining importance as communication networks become more data-intensive. With the growth of cloud services, connected devices, and enterprise digital platforms, IT and communication companies need faster inference systems to support low-latency AI workloads.

Regional Insights

North America dominated the regional segment with 47.6% share. The region leads due to strong AI adoption, advanced cloud infrastructure, high data center investment, and early deployment of AI-based enterprise applications.

The regional market is supported by strong demand from technology, finance, healthcare, retail, communication, and cloud service sectors. These industries are using AI inference servers for automation, fraud detection, diagnostics support, personalization, customer support, and real-time analytics.

North America also benefits from a mature digital infrastructure ecosystem. The presence of large enterprise users, advanced data center networks, and strong AI development activity continues to support demand for high-performance inference server systems.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFSegment Covered in the Report

By Cooling Type

Air Cooling

Liquid Cooling

By Processor Type

GPU-Based Inference Servers

CPU-Optimized Inference Servers

ASIC / FPGA-Based Inference Servers

Others

By Deployment Type

Cloud Deployment

Edge Deployment

On-Premise / Hybrid Deployment

By Application

IT and Communication

Intelligent Manufacturing

Electronic Commerce

Security

Finance

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

The AI Inference Server Market is driven by rising deployment of generative AI applications, enterprise AI assistants, real-time analytics, recommendation engines, autonomous systems, and AI-enabled cloud services. Inference servers are critical because they process trained AI models and deliver fast responses for users, applications, and connected devices.

North America leads the market due to strong cloud infrastructure, hyperscale data center investment, AI software adoption, and early deployment of enterprise AI workloads. The U.S. remains the key regional contributor because of large cloud providers, AI chip innovation, and strong demand from technology, finance, healthcare, retail, and communication sectors.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising generative AI application deployment | +5.8% | North America, Europe, Asia Pacific | Drives core server demand. |

Growth in enterprise AI assistants | +4.7% | U.S., Canada, UK, Germany, Japan | Supports real-time inference workloads. |

Expansion of hyperscale data centers | +4.1% | North America, Asia Pacific, Europe | Builds infrastructure demand. |

Increasing real-time analytics usage | +3.5% | Finance, retail, telecom, healthcare | Expands application coverage. |

Demand for low-latency AI processing | +2.9% | Cloud, edge, and telecom networks | Supports high-performance servers. |

Restraints Impact Analysis

The market faces restraints from high hardware costs, power consumption, cooling needs, GPU supply constraints, and complex infrastructure planning. AI inference servers require advanced processors, memory, networking, storage, and thermal systems, which increases capital and operating costs.

Another restraint is workload optimization complexity. Enterprises need the right balance between GPUs, CPUs, accelerators, model compression, software frameworks, and cloud deployment models to avoid overpaying for compute capacity.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High server and accelerator cost | -2.8% | Global enterprise buyers | Slows large-scale adoption. |

Power and cooling requirements | -2.4% | Data center operators | Raises operating cost. |

GPU and accelerator supply constraints | -2.0% | North America, Asia Pacific, Europe | Affects deployment speed. |

Complex workload optimization | -1.7% | Enterprise AI users | Increases technical burden. |

Data center capacity limitations | -1.4% | Major cloud regions | Restricts rapid scaling. |

Opportunities Impact Analysis

Opportunities are strong in GPU-based inference servers, liquid-cooled infrastructure, edge inference servers, AI-optimized networking, model-serving platforms, and cloud inference-as-a-service. These areas benefit from rising demand for faster, cheaper, and scalable AI deployment.

Higher-value opportunities are also emerging in industry-specific inference systems for healthcare, finance, telecom, retail, manufacturing, and communication networks. Companies that reduce inference cost per query while improving speed and reliability can capture strong long-term demand.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

GPU-based inference server expansion | +5.5% | North America, Asia Pacific, Europe | Builds core market value. |

Liquid cooling and thermal upgrades | +4.6% | Hyperscale and AI data centers | Supports high-density deployment. |

Edge AI inference infrastructure | +4.0% | Telecom, manufacturing, automotive | Expands real-time use cases. |

Cloud inference-as-a-service | +3.4% | U.S., Europe, Asia Pacific | Improves access for enterprises. |

Industry-specific AI server solutions | +2.9% | Healthcare, BFSI, retail, telecom | Creates premium demand. |

Challenges Impact Analysis

The main challenge is controlling inference cost while maintaining low latency and high throughput. AI models are becoming larger and more complex, so server operators must optimize hardware usage, batching, model compression, and energy efficiency.

Another challenge is matching infrastructure to fast-changing model architectures. New multimodal models, reasoning models, small language models, and agentic AI workloads may require different memory, processor, and networking configurations.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Reducing cost per inference | -2.6% | Cloud and enterprise AI users | Affects commercial scalability. |

Managing latency at high traffic levels | -2.2% | AI apps and digital platforms | Impacts user experience. |

Supporting fast-changing AI models | -1.9% | AI infrastructure providers | Raises upgrade pressure. |

Balancing performance and energy use | -1.6% | Data center operators | Increases efficiency needs. |

Integrating hardware and software stacks | -1.3% | Enterprise deployment teams | Adds implementation complexity. |

Go-to-Market and Sales Economics

According to Globe Market Research, the go-to-market approach for the AI Inference Server Market should focus on production-ready AI infrastructure rather than only GPU availability. Buyers are now looking for full rack-scale systems that combine accelerators, CPUs, memory, networking, storage, power delivery, cooling and deployment services. NVIDIA reported USD 81.6 billion in Q1 fiscal 2027 revenue, with Data Center revenue reaching USD 75.2 billion, showing that accelerated computing has become the core engine of AI infrastructure spending.

Sales economics are being shaped by server OEM capacity, supply availability and customer backlog. Dell reported that in Q1 fiscal 2027 it booked USD 24.4 billion in AI orders, recognized USD 16.1 billion in AI server revenue and exited the quarter with USD 51.3 billion in AI backlog. This shows that buyers are moving from testing to large-scale inference deployment across neocloud, sovereign AI and enterprise customers.

The strongest sales model is integrated infrastructure selling, where suppliers deliver validated systems instead of separate components. Microsoft said Q3 fiscal 2026 capital expenditures were USD 31.9 billion, and roughly two-thirds of that spending was for short-lived assets, mainly GPUs and CPUs. This supports demand for AI inference servers that can be deployed quickly, refreshed faster and linked to cloud monetization.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is spread across hyperscale cloud, neocloud providers, enterprise AI factories, sovereign AI data centers, telecom AI infrastructure, edge inference, managed AI hosting and private model deployment. Dell stated that its AI customer count surpassed 5,000, with growth across neocloud, sovereign and enterprise customers. This indicates that inference server demand is no longer limited to a small group of hyperscalers.

Chip and accelerator suppliers are also expanding the revenue landscape. AMD reported USD 5.8 billion in Data Center segment revenue in Q1 2026, up 57% year over year, driven by EPYC processors and AMD Instinct GPU shipments. This supports a broader supplier base for inference servers, especially for enterprises and cloud buyers seeking alternatives to single-vendor dependency.

Custom silicon and AI networking are becoming important revenue pools. Broadcom reported that Q2 semiconductor revenue from AI reached USD 10.8 billion, up 143% year over year, supported by custom AI accelerators and AI networking demand. This shows that inference server revenue is expanding beyond GPUs into Ethernet, custom ASICs, switching, optical connectivity and rack-scale networking.

Financial Impact

The financial impact of AI inference servers is mainly linked to utilization, power efficiency, memory availability and faster model serving. Google Cloud announced Ironwood TPUs for general availability, stating that the system offers 10x peak performance improvement over TPU v5p and more than 4x better performance per chip compared with TPU v6e for training and inference workloads. This highlights why buyers are evaluating cost per token, latency and performance per watt, not only hardware purchase price.

Power and cooling are becoming major cost factors. The IEA reported that data center electricity consumption is projected to rise from 485 TWh in 2025 to 950 TWh by 2030, while electricity use from AI-focused data centers is expected to triple over the same period. This makes liquid cooling, high-density racks, power management and energy-efficient accelerators important financial levers for inference server buyers.

The main financial risk is infrastructure intensity. Meta expects 2026 capital expenditures, including finance leases, to be in the range of USD 125 billion to USD 145 billion, partly due to higher component pricing and additional data center costs. AI inference server suppliers that can reduce deployment time, improve rack density, manage memory constraints and offer lifecycle services are expected to capture stronger margins than vendors selling basic hardware alone.

Recent Developments

Market News

NVIDIA made a major 2026 update with its Rubin platform, which introduced the NVIDIA Inference Context Memory Storage Platform. This system is designed to scale inference context at very large levels by improving reuse of key-value cache data, which is critical for long-context LLMs, agentic AI, and high-volume token generation.

Dell expanded its AI Factory with NVIDIA in March 2026 and confirmed global availability timelines for new PowerEdge AI systems. Dell stated that the PowerEdge XE9812 would be available globally in the second half of 2026, while the XE9880L and XE9885L would be available in Q3 2026.

AMD strengthened its inference server position in 2026 through the Instinct MI350P PCIe GPU. AMD stated that the MI350P cards are dual-slot drop-in cards for standard air-cooled servers and are built to deploy inference on premises within existing data center power, cooling, and rack infrastructure. This is relevant for enterprises that want inference capacity without rebuilding full liquid-cooled AI factories.

Funding

Funding activity in 2026 shows strong investor confidence in AI inference infrastructure. Baseten announced a USD 1.5 billion Series F round in June 2026 to support the next era of AI inference. The round was led by Altimeter Capital, Conviction, and Spark Capital, with Sands Capital and Wellington Management as co-leads. This funding highlights the rising value of inference platforms that help enterprises deploy, scale, and optimize model serving.

Groq raised USD 650 million in new growth capital in June 2026 to expand its AI inference cloud. The company stated that the capital would support the growth of its inference cloud business. Groq is relevant to the AI inference server market because its LPU architecture is purpose-built for inference rather than adapted from training-focused GPUs.

SambaNova also announced USD 350 million in funding alongside its SN50 launch in February 2026. The company positioned the SN50 chip and SambaRack SN50 system around agentic AI inference and lower inference cost compared with GPUs. This funding supports a clear market theme: capital is moving toward platforms that reduce latency, improve token throughput, and lower operating cost for production AI workloads.

Together AI raised USD 800 million in July 2026 at an USD 8.3 billion valuation. The company supports businesses that train and operate AI workloads using open-source models. While it is broader than server hardware, the funding is relevant because model-serving platforms increase demand for inference servers, GPU clouds, and optimized accelerator infrastructure.

Oxmiq raised USD 35 million in July 2026 to build a unified chip architecture that combines graphics chips, CPUs, and tensor engines into a licensable IP block. The company’s approach reflects a growing push to reduce AI system cost through more integrated compute architectures, which could influence future inference server designs.

Market Impact

The AI inference server market is becoming more specialized in 2026. Training-focused systems remain important, but the fastest commercial demand is moving toward servers that can run models continuously, serve many users at low latency, reduce cost per token, and support agentic workflows. This favors systems with high memory capacity, fast interconnects, better KV-cache handling, strong power efficiency, and production-grade orchestration.

Enterprise buyers are expected to compare inference servers using practical metrics such as time-to-first-token, tokens per second, tokens per watt, uptime, cooling requirement, model compatibility, deployment speed, and software support. As private AI adoption grows, air-cooled PCIe inference servers, rack-scale GPU systems, and specialized inference accelerators are likely to coexist rather than replace one another.

The strongest opportunity is expected in sectors where low-latency AI decisions are business-critical. These include cloud AI platforms, coding assistants, customer service automation, financial services, healthcare workflows, cybersecurity, video analytics, search, robotics, and sovereign AI infrastructure. Vendors that can combine hardware performance with lower operating cost, secure deployment, and reliable model-serving software will be better positioned in 2026.

Research Methodology

Step 1: Primary Research: Primary research is conducted through direct discussions with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. These interviews help understand real market demand, pricing movement, supply chain conditions, production trends, and customer requirements.

Step 2: Secondary Research: Secondary research is carried out using company filings, annual reports, regulatory databases, government publications, trade association data, and verified industry sources. This step helps collect reliable background information and supports the overall market assessment.

Step 3: Data Validation: Collected data is validated through source triangulation, historical trend review, demand-side checks, and supply-side assessment. Multiple sources are compared to reduce errors and improve the accuracy of the final insights.

Step 4: Market Estimation: Market estimation is completed using both bottom-up and top-down approaches. Product demand, regional consumption, company presence, application-level usage, and end-use industry adoption are reviewed to estimate the market size and structure.

Step 5: Forecasting Approach: Market forecasts are prepared by studying regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. This approach helps identify future growth patterns and possible market changes.

Step 6: Quality Review: The final data and findings are reviewed by analysts through peer validation, outlier checks, internal consistency checks, and final publication approval. This ensures that the report maintains accuracy, clarity, and research quality.

Step 7: AI Policy: AI is not used as a primary data source. All published insights are checked against human-verified evidence, and final conclusions are reviewed by analysts before publication.

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

NVIDIA Corporation

Intel Corporation

Inspur Systems

Dell Technologies

Hewlett Packard Enterprise

Lenovo Group

Huawei Technologies Co., Ltd.

IBM Corporation

Gigabyte Technology Co., Ltd.

H3C Technologies

Super Micro Computer, Inc.

Fujitsu Limited

Powerleader Computer System

xFusion Digital Technologies Co., Ltd.

Dawning Information Industry Co., Ltd.

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Prashant is a skilled research analyst with five years of practical experience in market intelligence, strategic research, and business consulting. His expertise covers primary research, secondary research, competitive benchmarking, and industry trend analysis across sectors such as semiconductors, automotive, transportation and logistics, machinery, and industrial equipment. Prashant focuses on delivering clear, data-backed insights that help clients understand market shifts, technology adoption, regulatory developments, and emerging growth opportunities.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Information and Technology

Answer Engine Optimization (AEO) Market Size to Reach USD 91.3 Billion By 2035

Global Answer Engine Optimization (AEO) Market Size, Go-to-Market and Sales Strategy Analysis By Offering (Software / Platforms, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (SMEs, Large Enterprises), By Channel Type (Search Engines, AI Chat Interfaces, Voice Search), By Functionality (Query & Intent Optimization, NLP / Semantic Optimization, Analytics & Performance Tracking), By End-Use Industry (BFSI, Retail & E-commerce, Healthcare, IT & Telecom, Media & Entertainment, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Agentic AI Travel Booking Platforms Market Size to Reach USD 31.4 Billion By 2035

Global Agentic AI Travel Booking Platforms Market Size, Go-to-Market and Sales Strategy Analysis By Technology (AI Trip Planning Agents, Machine-Readable Rate APIs, Loyalty Integration, Autonomous Price Comparison and Others), By User Type (Business Travelers, Group Bookings, Leisure Travelers and Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

5G RAN Market Size to hit USD 108.5 billion by 2035

Global 5G RAN Market Size, Go-to-Market and Sales Strategy Analysis By Component (Hardware, Software, Services), By Architecture Type (Traditional RAN, Open RAN), By Deployment (Public Networks, Private Networks), By End Use (Telecom Operators, Enterprise and Industrial Users), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Online Dating Market Size to hit USD 29.5 Bn by 2035

Global Online Dating Market Size, Go-to-Market Strategy Analysis By Type (Paying Online Dating, Non-Paying Online Dating), By Revenue Model (Subscription, Advertising-Supported, Other Model), By Platform (Web Portals, Applications), By Age Group (Adult, Baby Boomer, Generation X, Generation Z, Millennials), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035