Revenue, 2025

$ 13.9 Bn

Forecast, 2035

$ 49.4 Bn

CAGR, 2025-2035

13.5%

Report Coverage

Global

Market Size and Forecast

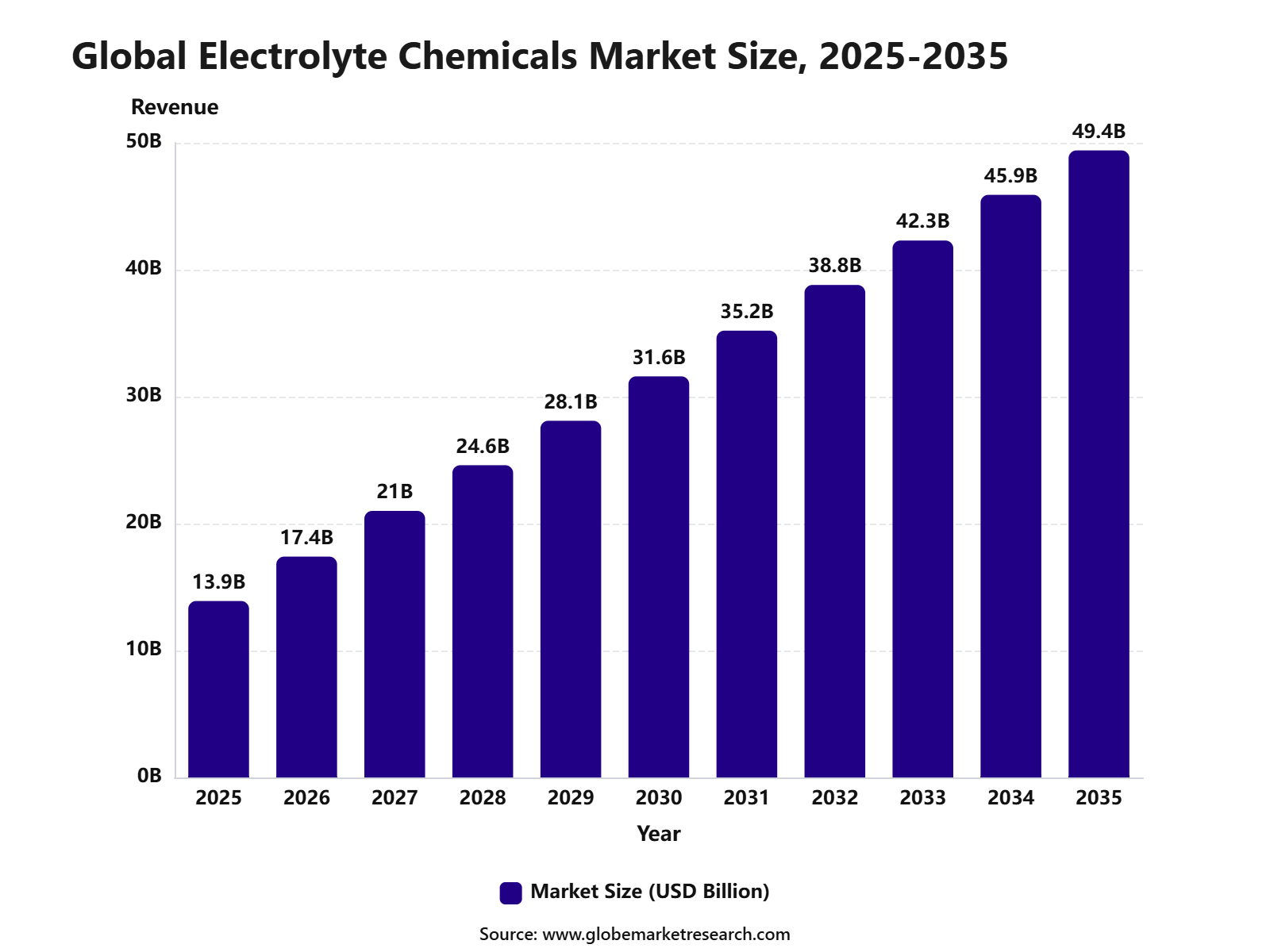

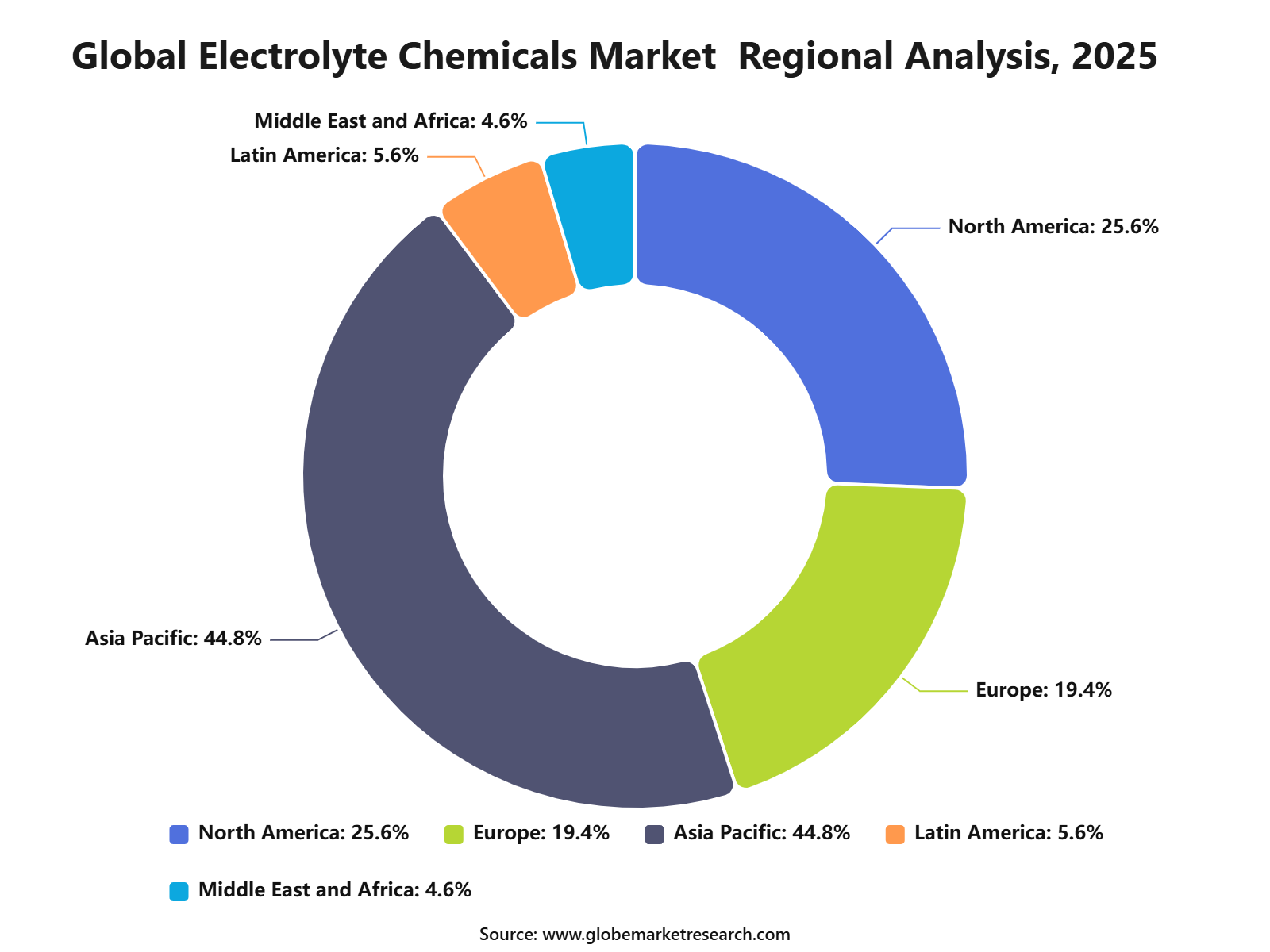

The Global Electrolyte Chemicals Market was worth USD 13.9 billion in 2025 and is expected to reach USD 49.4 billion by 2035, growing at a CAGR of 13.5% from 2025 to 2035. Based on this growth rate, the market is estimated to reach around USD 17.4 billion in 2026. Asia Pacific held the largest regional share of 44.8% in 2025, supported by strong battery manufacturing, electric vehicle production, consumer electronics demand, and expanding energy storage supply chains.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 13.9 Billion |

Projected Revenue, 2035 | USD 49.4 Billion |

CAGR (2025-2035) | 13.5% |

Largest Region | Asia Pacific |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

What is Electrolyte Chemicals Market?

The Electrolyte Chemicals Market includes chemical compounds and formulations used to enable ion movement within batteries, capacitors, and electrochemical systems. These chemicals are widely used in lithium-ion batteries, sodium-ion batteries, supercapacitors, fuel cells, flow batteries, and advanced energy storage devices. The market is closely linked with battery materials, cathode and anode production, cell manufacturing, and clean energy technologies.

The market outlook remains strong as demand for high-performance batteries continues to increase across mobility, electronics, and grid storage applications. Growth can be attributed to rising electric vehicle adoption, expanding battery gigafactories, and higher need for safer and longer-lasting electrolyte formulations. The expansion of solid-state electrolytes, advanced additives, and localized battery supply chains is expected to support long-term market demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Lithium-ion electrolytes led the battery type segment with 76.2% share, supported by their wide use in electric vehicles, consumer electronics, energy storage systems, and rechargeable battery applications.

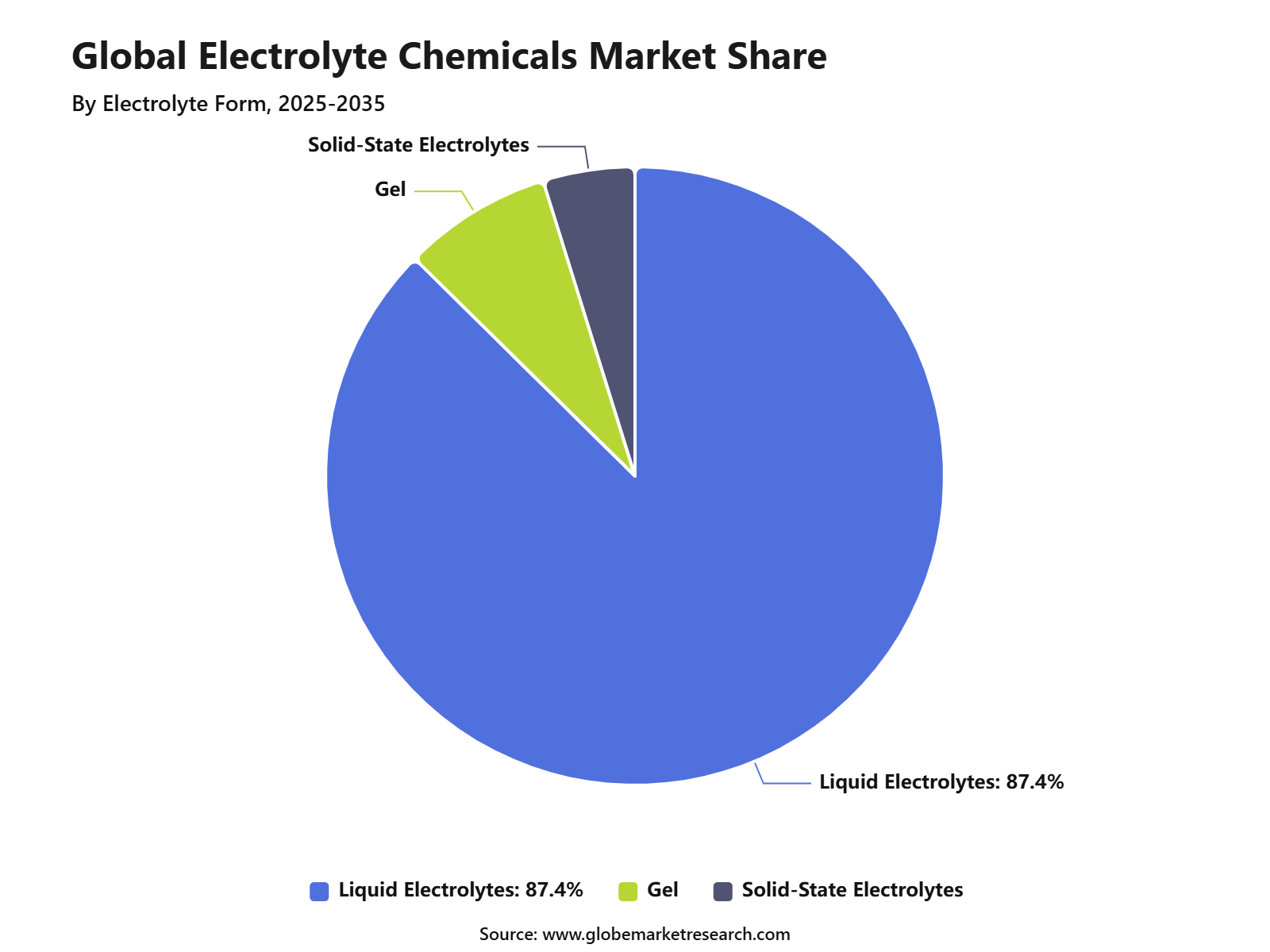

Liquid electrolytes accounted for 87.4% share, driven by their strong ionic conductivity, established commercial use, easier cell integration, and broad compatibility with lithium-ion battery formats.

Electric vehicles held 62.4% share by application, supported by rising EV production, growing battery demand, and increasing use of high-performance electrolyte formulations.

Lithium-based electrolytes captured 83.9% share by product type, driven by their critical role in lithium-ion battery chemistry and strong demand from mobility and energy storage sectors.

Asia Pacific led the electrolyte chemicals market with 44.8% share, supported by large-scale battery manufacturing, strong EV supply chains, and high demand across China, Japan, South Korea, and India.

Top Funding and Investment

GFCL EV Products is developing a battery materials facility in Gujarat, India, with a disclosed project cost of about USD 709.0 million. IFC’s proposed equity investment is up to USD 50.0 million, supporting production of electrolytes, salts, binders, and cathode active materials. Gujarat Fluorochemicals also confirmed that GFCL EV’s portfolio includes LiPF6 electrolyte salt, electrolyte formulations, and performance additives.

UBE Corporation announced a USD 500.0 million investment to build the first U.S. manufacturing facility for dimethyl carbonate and ethyl methyl carbonate, two key solvents used in lithium-ion battery electrolytes. The plant is expected to produce 100,000 metric tons of DMC and 40,000 metric tons of EMC per year, with operations planned for late 2026.

Koura, Orbia’s fluorinated solutions business, proposed a USD 400.0 million facility in St. Gabriel, Louisiana, to produce lithium hexafluorophosphate, a core electrolyte salt used in lithium-ion batteries. The project is expected to produce 10,000 metric tons of LiPF6 per year and was selected for a USD 100.0 million U.S. Department of Energy award under battery supply chain funding.

Capchem USA announced plans for a USD 350.0 million lithium-ion battery materials plant in Ascension Parish, Louisiana. The facility is planned to produce 200,000 tons of carbonate solvents and 100,000 tons of electrolytes per year, using lithium salts, carbonate solvents, and specialized additives in the electrolyte manufacturing process.

Tinci Materials announced an investment agreement with the Kingdom of Morocco for an integrated electrolyte and raw-material production base in Jorf Lasfar. The project is expected to involve 2.576 billion Moroccan dirhams, about USD 280.0 million, and planned annual capacity of 150,000 tons of electrolyte products and critical raw materials.

By Battery Type

Lithium-ion electrolytes accounted for 76.2% share of the Electrolyte Chemicals Market. This strong position can be attributed to their wide use in rechargeable batteries for electric vehicles, consumer electronics, energy storage systems, power tools, and industrial equipment. These electrolytes are essential because they support ion movement between the battery cathode and anode during charging and discharging.

Their performance directly affects battery safety, energy density, cycle life, charging speed, and operating stability. Demand is expected to remain strong as lithium-ion batteries continue to dominate electric mobility and stationary storage applications. Growth in battery manufacturing capacity and rising demand for high-performance cells will continue to support lithium-ion electrolyte consumption.

By Electrolyte Form

Liquid electrolytes held 87.4% share of the Electrolyte Chemicals Market. Their dominance is supported by mature commercial use, strong ionic conductivity, cost efficiency, and compatibility with large-scale lithium-ion battery production. These electrolytes are widely used because they enable efficient ion transport and stable battery operation across different cell formats.

They are commonly applied in cylindrical, pouch, and prismatic battery cells used in vehicles, electronics, and grid storage systems. The segment is expected to remain dominant in the near term because liquid electrolyte technology is well established and supported by existing battery production lines. However, safety, thermal stability, and performance improvement will remain important focus areas for producers.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Application

Electric vehicles captured 62.4% share of the Electrolyte Chemicals Market. This leadership is driven by strong battery demand from passenger cars, commercial vehicles, two-wheelers, buses, and plug-in hybrid platforms. Electrolyte chemicals are critical for electric vehicle batteries because they influence driving range, charging performance, battery life, and safety.

Automakers and battery manufacturers require high-purity electrolyte formulations to support reliable performance under different temperatures and driving conditions. The segment is expected to remain the largest application area as vehicle electrification continues to expand. Rising investments in gigafactories, battery supply chains, and fast-charging technologies will further strengthen demand for electrolyte chemicals in electric vehicles.

By Product Type

Lithium-based electrolytes accounted for 83.9% share of the Electrolyte Chemicals Market. Their leading position is supported by the continued dominance of lithium-ion battery chemistry across electric vehicles, consumer electronics, and energy storage applications. These electrolytes are preferred because lithium salts and solvent systems provide strong electrochemical performance, high conductivity, and compatibility with major cathode and anode materials.

They support efficient charge transfer and stable battery operation when properly formulated. Demand for lithium-based electrolytes is expected to remain strong as battery makers focus on higher energy density, longer cycle life, and improved safety. The segment will continue to benefit from rising production of lithium iron phosphate, nickel-rich, and other advanced battery chemistries.

By Region

Asia Pacific accounted for 44.8% share of the Electrolyte Chemicals Market, making it the leading regional market. This dominance is supported by strong battery cell manufacturing, electric vehicle production, electronics output, and electrolyte chemical processing capacity.

China, Japan, South Korea, India, and Southeast Asian countries are key contributors to regional demand. The region benefits from large battery plants, cathode and anode material production, strong EV adoption, and established supply chains for lithium-based battery materials.

Asia Pacific is expected to maintain its leading position as battery manufacturing capacity continues to expand. Rising demand for electric vehicles, renewable energy storage, and consumer electronics will further support electrolyte chemical consumption across the region.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFGo-To-Market and Sales Economics

The Electrolyte Chemicals Market is mainly driven by lithium salts, carbonate solvents, additives, gel electrolytes, solid-state electrolyte materials, and sodium-ion electrolyte systems used in EV batteries, energy storage batteries, consumer electronics, power tools, and industrial backup systems. The most important sales route is through cell manufacturers, cathode and anode material producers, battery pack makers, energy storage integrators, and automotive battery supply chains.

Demand is supported by EV battery deployment, which reached around 1.2 TWh in 2025 and is expected to rise strongly with electric mobility adoption. Go-to-market strategies depend on technical approval, purity control, safety testing, and long-term supply reliability. Electrolyte chemicals directly affect ion transport, cycle life, fast-charging behavior, temperature stability, and cell safety. Electric car sales exceeded 20 million units globally in 2025, while electric cars represented 25% of new car sales, creating a strong customer base for lithium-ion electrolyte salts, solvents, and performance additives.

Sales economics are attractive because electrolytes are essential consumable inputs in battery cell manufacturing. Buyers usually prefer qualified suppliers that can provide low-moisture materials, low-metal impurities, stable solvent blends, documentation, transport safety compliance, and local supply assurance. In 2025, batteries accounted for 88% of global lithium end use, while global lithium consumption reached about 263,000 tons, showing how closely electrolyte demand is connected to the battery production chain.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is strongest across electric vehicles, stationary battery storage, consumer electronics, data-center backup power, two-wheelers, commercial vehicles, and emerging sodium-ion batteries. EVs remain the largest demand route because every lithium-ion cell requires electrolyte for ion movement between anode and cathode. Battery storage is also becoming a major revenue area, as 108 GW of new battery storage capacity was deployed worldwide in 2025.

Grid storage creates a different revenue profile from EVs because it favors low-cost, long-cycle, and thermally stable battery chemistries. LFP batteries accounted for around 90% of battery storage deployments in 2025, which supports demand for electrolyte systems optimized for LFP cells, frequent cycling, and long-duration operation. This is important for suppliers of LiPF6, LiFSI, carbonate solvents, flame-retardant additives, film-forming additives, and electrolyte blends designed for high-cycle performance.

Asia remains the most important revenue center because battery cell manufacturing and material conversion are highly concentrated there. However, North America and Europe are trying to localize strategic battery materials. In 2025, the U.S. Department of Energy highlighted electrolyte and electrolyte salts as a supply-chain investment gap and noted that nearly all electrolyte salt was sourced through foreign-entity-of-concern supply chains.

Financial Impact

The financial impact of electrolyte chemicals is linked to battery yield, warranty cost, safety performance, and energy density. A high-quality electrolyte can improve cell formation, reduce gas generation, support stable solid-electrolyte interphase formation, and lower the risk of early battery degradation. For cell makers, even small performance improvements can have a direct effect on scrap rates, warranty exposure, charging speed, and customer approval.

Funding support is improving the economics of domestic electrolyte and battery material production. In March 2026, the U.S. Department of Energy announced up to USD 500 million to expand critical material processing, derivative battery manufacturing, and recycling, including materials used in commercially available batteries. This type of funding can reduce project risk for electrolyte salts, solvent systems, recycling-linked feedstocks, and localized battery material facilities.

Electrolyte suppliers also benefit from the shift toward higher-performance batteries. Fast charging, high-voltage cathodes, silicon-rich anodes, low-temperature operation, and safer storage systems require advanced additives and customized solvent packages. This allows qualified suppliers to move beyond commodity solvent sales and capture higher-value opportunities through application-specific electrolyte formulations, technical service, and long-term qualification with battery customers.

Drivers Impact Analysis

The Electrolyte Chemicals Market is driven by rising demand from lithium-ion batteries, electric vehicles, energy storage systems, consumer electronics, and advanced battery manufacturing. Electrolyte chemicals are essential for ion movement, battery efficiency, cycle life, safety, and charging performance.

Asia Pacific leads the market due to its strong battery cell production, cathode and anode material ecosystem, EV manufacturing, and electronics supply chain. China, South Korea, Japan, and India remain key regional contributors because of large-scale battery investments and growing clean energy demand.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising electric vehicle battery production | +3.8% | Asia Pacific, Europe, North America | Drives core demand. |

Expansion of lithium-ion battery manufacturing | +3.2% | China, South Korea, Japan, U.S. | Supports chemical consumption. |

Growth in energy storage systems | +2.6% | China, India, U.S., Europe | Builds long-term demand. |

Increasing consumer electronics output | +2.0% | Asia Pacific manufacturing hubs | Adds steady usage. |

Demand for faster charging batteries | +1.6% | Advanced EV and electronics markets | Supports premium formulations. |

Restraints Impact Analysis

The market faces restraints from raw material price volatility, safety concerns, and high-purity production requirements. Electrolyte chemicals depend on lithium salts, solvents, additives, and specialty fluorinated compounds, so supply disruptions can affect pricing and availability. Safety is another important restraint because liquid electrolytes can be flammable and sensitive to moisture. Battery producers need strict quality control, safe handling, and stable formulations to reduce thermal risk and improve reliability.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Raw material price volatility | -1.5% | Global battery supply chains | Pressures margins. |

Safety concerns in liquid electrolytes | -1.3% | EV and storage batteries | Raises testing needs. |

High-purity manufacturing cost | -1.1% | Battery chemical producers | Limits cost efficiency. |

Dependence on specialty lithium salts | -0.9% | Asia Pacific, Europe, North America | Creates supply risk. |

Strict transport and storage requirements | -0.7% | Global chemical logistics | Adds handling burden. |

Opportunities Impact Analysis

Opportunities are strong in lithium-based electrolytes, electrolyte additives, solid-state electrolytes, high-voltage electrolyte systems, and localized battery chemical production. These areas benefit from EV growth, grid storage demand, and battery technology upgrades. Higher-value opportunities are emerging in safer electrolytes, non-flammable formulations, and performance-enhancing additives. Companies that can improve battery life, charging speed, temperature stability, and safety can capture stronger demand from premium EV and energy storage applications.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Lithium-based electrolyte expansion | +3.5% | Asia Pacific, Europe, North America | Builds core market demand. |

Electrolyte additive innovation | +2.9% | Battery technology hubs | Improves battery performance. |

Solid-state electrolyte development | +2.5% | Japan, South Korea, U.S., Europe | Creates future opportunity. |

High-voltage electrolyte systems | +2.1% | EV battery manufacturers | Supports energy density. |

Regional electrolyte chemical capacity | +1.8% | India, Europe, U.S., Japan | Improves supply security. |

Challenges Impact Analysis

The main challenge is maintaining electrolyte purity and consistency at commercial scale. Even trace impurities can affect battery cycle life, safety, conductivity, and cell performance, making quality control a critical success factor. Another challenge is adapting electrolyte chemistry to changing battery formats and cathode materials. Different chemistries, such as LFP, NMC, sodium-ion, and solid-state batteries, require different electrolyte systems and additives.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining ultra-high purity | -1.4% | Battery-grade producers | Affects cell qualification. |

Matching changing battery chemistries | -1.2% | EV and storage markets | Increases formulation complexity. |

Scaling specialty additive production | -1.0% | Battery chemical suppliers | Raises technical burden. |

Managing moisture sensitivity | -0.8% | Electrolyte production and storage | Impacts product stability. |

Meeting battery safety standards | -0.7% | Automotive and grid storage sectors | Increases validation cost. |

Segment Covered in the Report

By Battery Type

Lithium-ion Electrolytes

Lead-acid Electrolytes

Flow Battery Electrolytes

Others

By Electrolyte Form

Liquid Electrolytes

Gel

Solid-State Electrolytes

By Application

Electric Vehicles

Energy Storage Systems

Consumer Electronics

Industrial and Motive Batteries

Others

By Product Type

Lithium-Based Electrolytes

Sulfide-Based Electrolytes

Polymer-Based Electrolytes

Oxide-Based Electrolytes

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward lithium-ion electrolytes, liquid electrolyte systems, lithium-based salts, advanced additives, and safer formulations. Liquid electrolytes remain widely used because they are commercially mature and compatible with current lithium-ion battery production.

At the same time, solid-state and semi-solid electrolyte research is gaining attention for future battery safety and energy density improvements. Asia Pacific remains the largest production and demand region, while North America and Europe are investing in local battery supply chains.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Lithium-ion electrolytes remain dominant | +3.4% | Global battery markets | Leads product demand. |

Liquid electrolytes maintain large usage | +2.9% | Asia Pacific, Europe, North America | Supports current battery scale. |

Lithium-based electrolyte salts grow | +2.4% | Battery manufacturing hubs | Adds chemical demand. |

Safer electrolyte formulations gain focus | +2.0% | EV and grid storage markets | Improves reliability. |

Solid-state electrolyte R&D expands | +1.7% | Japan, South Korea, U.S., Europe | Supports future technology shift. |

Investor Type Impact Matrix

Investors should focus on electrolyte chemical producers with strong battery-grade purification, lithium salt access, formulation expertise, and customer relationships with battery cell manufacturers. Consistent quality, safety performance, and supply reliability are key investment factors.

Strategic investors can also target electrolyte additive companies, lithium salt producers, solid-state electrolyte developers, and regional battery material suppliers. Companies that improve battery safety, cycle life, and supply security are better positioned for long-term value creation.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Electrolyte Chemical Producers | +3.2% | Global battery markets | Expands chemical supply. |

Lithium Salt Manufacturers | +2.7% | Asia Pacific, Europe, North America | Supports core electrolyte demand. |

Battery Material Companies | +2.3% | China, South Korea, Japan, Europe | Drives formulation use. |

Solid-State Electrolyte Developers | +1.9% | Japan, South Korea, U.S., Europe | Builds future technology value. |

Strategic and Clean Energy Investors | +1.6% | Global EV and storage markets | Funds capacity growth. |

Recent Developments

In 2026, Orbia Fluor & Energy Materials completed the expansion of its custom electrolyte facility in Madison, Wisconsin. The expansion increased site production capacity by roughly 300% and supports lithium-ion, lithium-sulfur, sodium-ion, and other emerging battery chemistries. The site supplies industrial, medical, EV, energy storage, aerospace, and defense battery applications.

In 2026, Idemitsu Kosan made a final investment decision and started construction of a large pilot facility for solid electrolytes used in all-solid-state batteries. The company is working with Toyota and aims to support BEVs using all-solid-state batteries in 2027 to 2028. The pilot facility is expected to reach several hundred tons of annual production capacity after completion.

In 2026, Orbia continued building its lithium hexafluorophosphate facility in St. Gabriel, Louisiana. LiPF6 remains the most widely used lithium salt in lithium-ion battery electrolytes because it supports conductivity, thermal stability, and electrochemical performance. The planned facility is designed to produce up to 10,000 metric tons of LiPF6 annually and strengthen North American electrolyte salt supply.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Tinci Materials

CAPCHEM

Soulbrain

Mitsubishi Chemical Group

Central Glass

UBE Corporation

BASF SE

LG Chem

Dongwha Electrolyte

Morita Chemical Industries

Zhejiang Yongtai Technology

Shanshan Technology

Targray

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Prashant is a skilled research analyst with five years of practical experience in market intelligence, strategic research, and business consulting. His expertise covers primary research, secondary research, competitive benchmarking, and industry trend analysis across sectors such as semiconductors, automotive, transportation and logistics, machinery, and industrial equipment. Prashant focuses on delivering clear, data-backed insights that help clients understand market shifts, technology adoption, regulatory developments, and emerging growth opportunities.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Carbon Capture Chemicals Market Size to Reach USD 78.0 Billion by 2035

Carbon Capture Chemicals Market By Chemical Type (Amines, Carbonates, Ammonia-based Solvents, Ionic Liquids, Solid Sorbent Chemicals, Others), By Absorption Type (Chemical Absorption, Physical Absorption), By End-Use Industry (Oil and Gas, Power Generation, Chemical and Petrochemical, Cement, Iron and Steel, Others), By Application (Post-combustion Capture, Pre-combustion Capture, Industrial Gas Separation, Direct Air Capture, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Bio-based Chemicals Market Size to Hit USD 296.7 Bn by 2035

Bio-based Chemicals Market By Product Category (Platform Chemicals, Polymers for Plastics, Paints, Coatings, Inks and Dyes, Surfactants, Cosmetics and Personal Care Products, Adhesives, Man-made Fibers, Others), By Application (Industrial, Agricultural, Pharmaceutical, Others), By Source (Plant-based, Animal-based, Microbial-based, Waste-based), By End Use (Chemical Manufacturing, Agriculture, Food and Beverage, Personal Care, Pharmaceuticals, Automotive), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Processing Chemicals Market Size to Hit USD 14.6 Billion by 2035

Hydrogen Processing Chemicals Market By Chemical Type (Catalysts, Adsorbents, Solvents, Corrosion Inhibitors, Scavengers, Others), By Function (Reforming Chemicals, Purification Chemicals, Hydroprocessing Chemicals, Gas Treatment Chemicals, Corrosion Control Chemicals, Others), By Process (Steam Methane Reforming, Hydrocracking, Hydrotreating, Pressure Swing Adsorption, Water-Gas Shift Reaction, Others), By End Use (Refineries, Ammonia Production, Methanol Production, Petrochemicals, Clean Hydrogen Plants, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Nickel Chemicals Market to Cross USD 19.1 Billion by 2035

Nickel Chemicals Market By Product Type (Nickel Sulfate, Nickel Hydroxide, Nickel Chloride, Nickel Nitrate, Nickel Carbonate, Nickel Acetate, Others), By Grade (Battery Grade, Plating Grade, Industrial Grade, High-Purity Grade, Others), By Form (Powder, Crystal, Solution, Granules, Others), By Application (Batteries, Electroplating, Catalysts, Ceramics and Pigments, Chemical Intermediates, Others), By End Use (Automotive, Electronics, Chemicals, Aerospace, Industrial Manufacturing, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035