Revenue, 2025

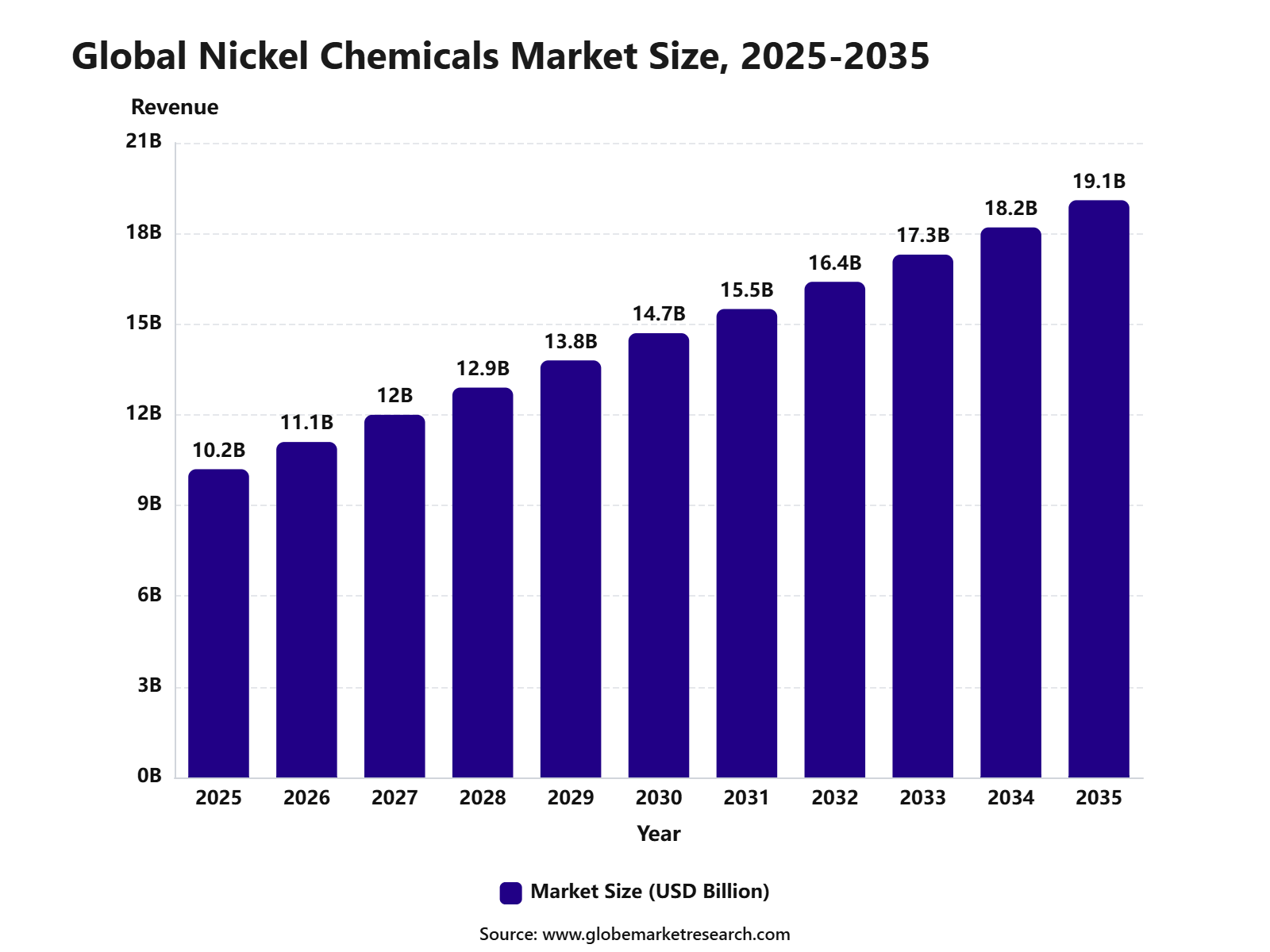

$ 10.2 Bn

Forecast, 2035

$ 19.1 Bn

CAGR, 2025-2035

6.5%

Report Coverage

Global

Market Size and Forecast

The Global Nickel Chemicals Market was valued at USD 10.2 billion in 2025 and is estimated to reach USD 11.1 billion in 2026. The market is projected to reach USD 19.1 billion by 2035, growing at a CAGR of 6.5% from 2025 to 2035. Asia Pacific held the largest regional share of 49.5% in 2025, supported by strong battery manufacturing, stainless steel production, electroplating demand, and expanding electric vehicle supply chains.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 10.2 Billion |

Projected Revenue, 2035 | USD 19.1 Billion |

CAGR (2025-2035) | 6.5% |

Largest Region | Asia Pacific |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

What is Nickel Chemicals Market?

The Nickel Chemicals Market includes nickel sulfate, nickel chloride, nickel carbonate, nickel nitrate, nickel acetate, and other nickel-based compounds used across industrial and battery applications. These chemicals are widely used in lithium-ion batteries, electroplating, catalysts, ceramics, pigments, metal treatment, electronics, and specialty chemical manufacturing. The market is closely linked with nickel mining, refining, battery-grade chemical production, and cathode material supply chains.

The market outlook remains steady as demand continues to rise from battery materials, surface finishing, and advanced industrial applications. Growth can be attributed to increasing use of nickel sulfate in electric vehicle batteries, expanding electroplating activity, and rising demand for high-performance nickel-based materials. The expansion of battery recycling, cleaner refining technologies, and regional battery supply chains is expected to support long-term market demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Nickel sulfate led the product type segment with 41.5% share, supported by its strong use in battery materials, electroplating, catalysts, and specialty chemical applications.

Battery grade chemicals accounted for 47.8% share, driven by rising demand for high-purity nickel compounds used in rechargeable batteries and electric vehicle production.

Crystal form held 39.6% share, supported by easier handling, stable storage, and strong suitability for industrial processing and battery chemical formulations.

Batteries captured 44.5% share by application, driven by growing use of nickel chemicals in lithium-ion batteries, energy storage systems, and portable electronic devices.

Automotive end use represented 40.5% share, supported by rising electric vehicle adoption and increasing demand for nickel-rich battery chemistries.

Asia Pacific led the nickel chemicals market with 49.5% share, supported by strong battery manufacturing, expanding EV production, and high chemical consumption across China, Japan, South Korea, and India.

Top Funding and Investment

Vale’s Pomalaa Block investment is valued at USD 4.5 billion for mines and HPAL facilities in Indonesia. The project is planned to produce about 120,000 tonnes of nickel and around 15,000 tonnes of cobalt contained in MHP products each year. This supports battery-grade nickel chemical supply for EV cathode materials.

Nickel Industries reached a positive final investment decision for the Excelsior Nickel Cobalt HPAL project in Indonesia, with construction costs capped at USD 2.3 billion. The project is expected to produce 72,000 metric tons per year of contained nickel equivalent across MHP, nickel sulphate, and nickel cathode. The company also secured USD 400.0 million in financing facilities with BNI.

Terrafame’s Finnish battery chemicals plant required about EUR 240.0 million in investment, supported by earlier and additional funding packages. The facility was designed to produce 170,000 tonnes of nickel sulphate and 7,400 tonnes of cobalt sulphate per year, enough nickel sulphate for roughly 1.0 million EV batteries annually.

Korea Zinc and Trafigura signed an agreement to jointly invest KRW 184.9 billion, about USD 140.0 million, in an all-in-one nickel refinery in South Korea. The refinery is being built through Korea Energy Materials, which already produces up to 100,000 tonnes of nickel sulphate annually and plans to make liquid and crystallized nickel sulphate, cobalt sulphate, and precursors.

By Product Type

Nickel sulfate accounted for 41.5% share of the Nickel Chemicals Market. Its leading position is mainly supported by strong use in lithium-ion battery cathode production, especially for nickel-rich battery chemistries used in electric vehicles and energy storage systems. The material is widely used because it provides a suitable nickel source for cathode active materials such as NMC and NCA.

These chemistries are preferred in applications where higher energy density, longer driving range, and improved battery performance are required. Demand for nickel sulfate is expected to remain strong as battery manufacturing expands across Asia Pacific, Europe, and North America. Its role in electric mobility, grid storage, and battery material processing makes it one of the most important product types in the market.

By Grade

Battery grade nickel chemicals held 47.8% share of the Nickel Chemicals Market. This dominance is driven by rising demand for high-purity nickel materials used in advanced rechargeable batteries, particularly for electric vehicles and stationary energy storage. Battery grade materials must meet strict quality standards related to purity, consistency, impurity control, and electrochemical performance.

These requirements are important because small variations in material quality can affect battery efficiency, safety, cycle life, and production yield. The segment is expected to gain further importance as battery makers increase demand for reliable raw materials. Growing investment in cathode production, battery recycling, and localized supply chains will continue to support the use of battery grade nickel chemicals.

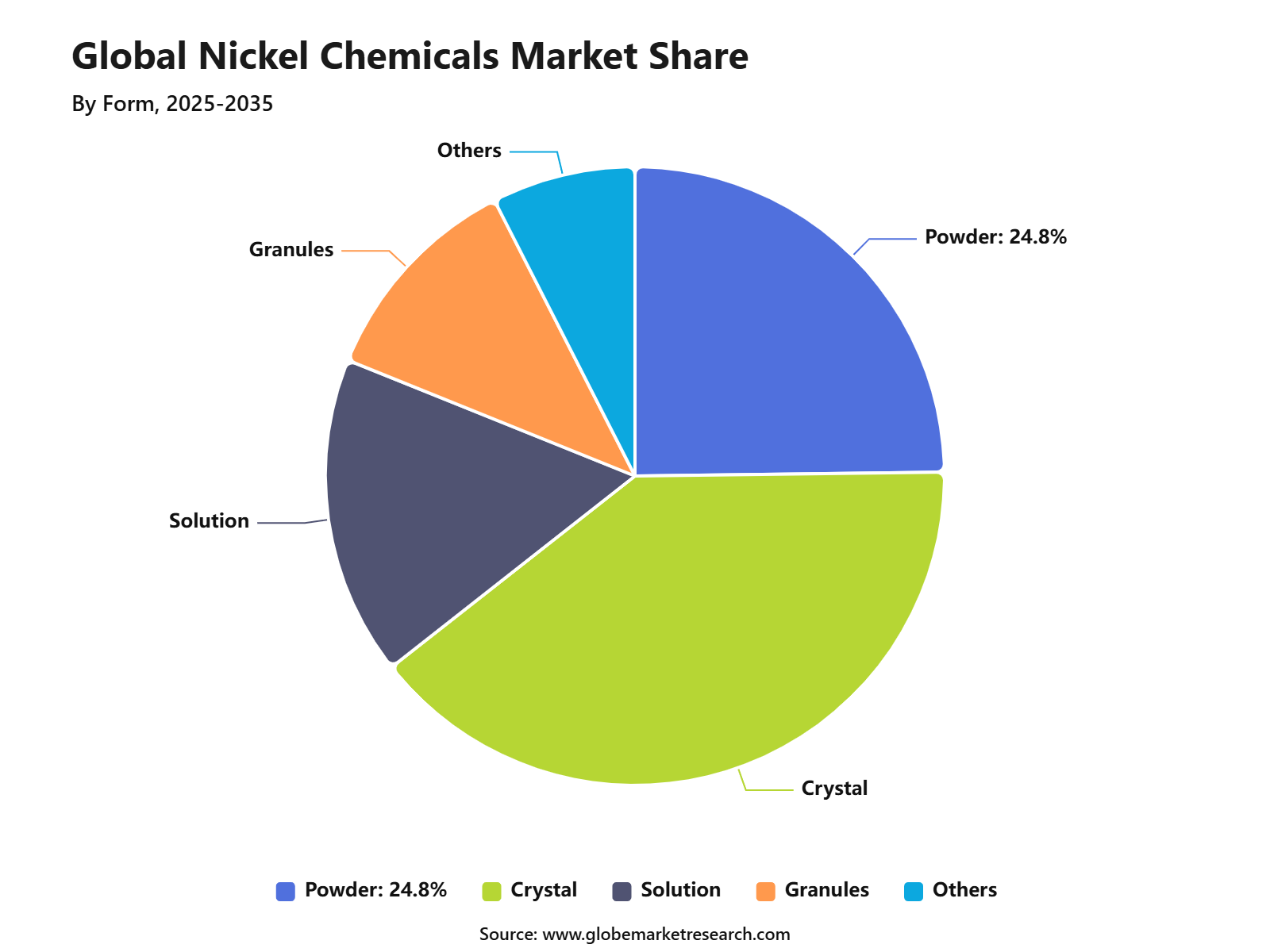

By Form

Crystal form accounted for 39.6% share of the Nickel Chemicals Market. This form is widely preferred because it offers good stability, easier handling, controlled dosing, and suitability for industrial processing and chemical conversion. Nickel chemicals in crystal form are commonly used in battery precursor production, electroplating, catalysts, ceramics, pigments, and specialty chemical applications.

Their defined physical structure supports better storage, transport, and process control during manufacturing. Demand for crystal form nickel chemicals is expected to remain steady due to their practical use in high-volume production. As battery materials and surface treatment industries expand, crystal-based nickel compounds will continue to support consistent and efficient processing.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Application

Battery applications captured 44.5% share of the Nickel Chemicals Market. This strong share is supported by the growing use of nickel chemicals in cathode materials for electric vehicles, plug-in hybrids, consumer electronics, and energy storage systems. Nickel improves battery energy density, which helps increase driving range and reduce battery weight in electric vehicles.

Nickel sulfate and related compounds are therefore important inputs for battery manufacturers focusing on performance, efficiency, and longer battery life. The batteries segment is expected to remain a major demand center as global electrification accelerates. Demand will be further supported by battery gigafactories, renewable energy storage projects, and the development of advanced cathode chemistries.

By End Use

The automotive segment held 40.5% share of the Nickel Chemicals Market. This leadership is mainly linked to the rapid use of nickel-based battery materials in electric vehicles, hybrid vehicles, and advanced mobility platforms. Automotive manufacturers use nickel-rich batteries to improve energy density, range, charging performance, and vehicle efficiency.

As electric vehicle production increases, the need for high-quality nickel chemicals in battery supply chains continues to grow. The segment is expected to maintain strong demand as automakers invest in battery platforms, local sourcing, and recycling systems. Nickel chemicals will remain important for vehicle electrification, especially in models requiring longer range and higher battery performance.

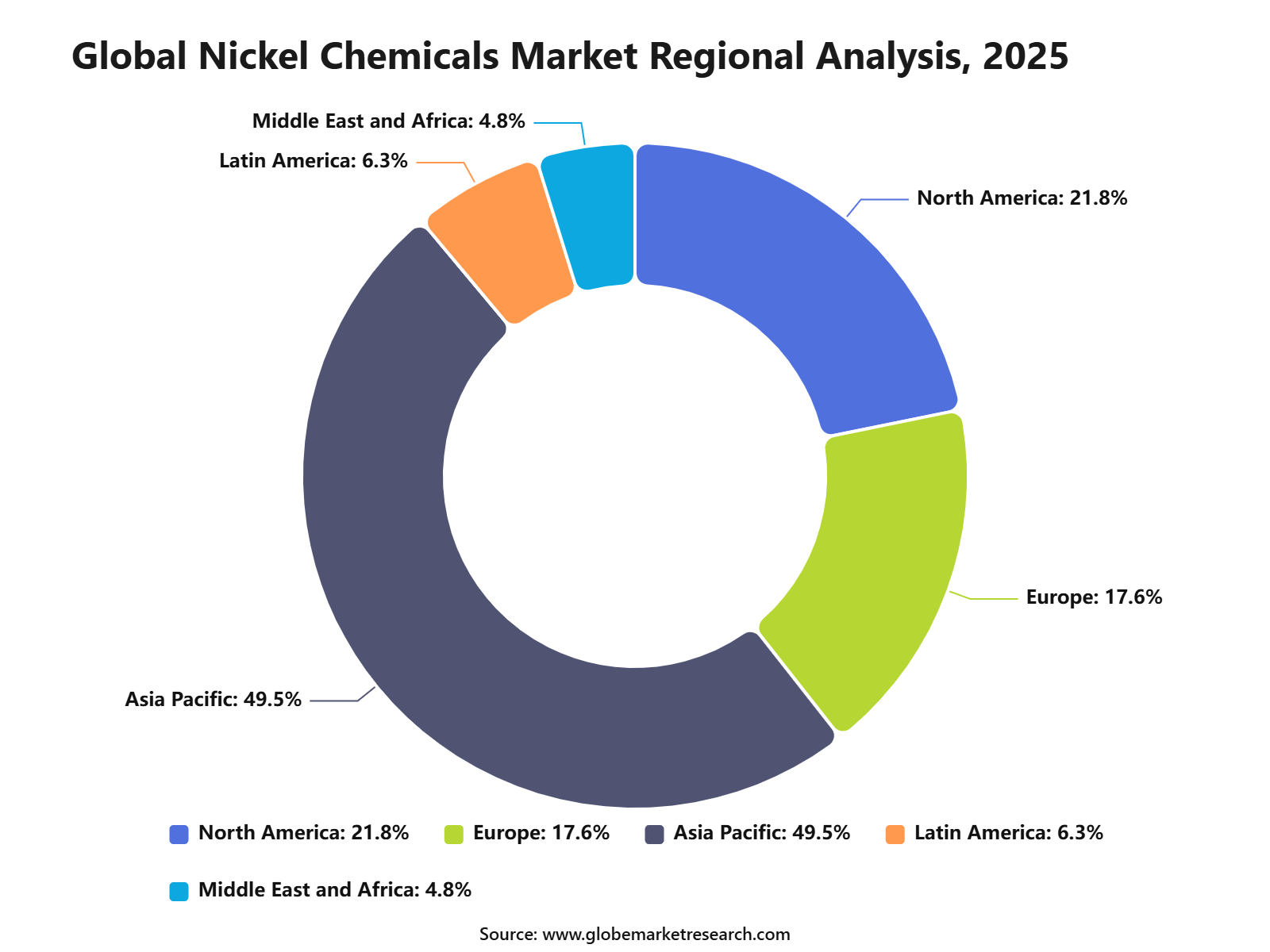

By Region

Asia Pacific accounted for 49.5% share of the Nickel Chemicals Market, making it the leading regional market. This dominance is supported by strong battery manufacturing, electric vehicle production, electronics output, and chemical processing capacity across the region. China, Japan, South Korea, India, and Southeast Asian countries are key contributors to regional demand.

The region benefits from established cathode production, large-scale refining activity, growing battery plants, and strong downstream consumption from automotive and electronics industries. Asia Pacific is expected to maintain its leading position as battery supply chains continue to expand. Rising investment in electric vehicles, energy storage systems, and battery material processing will further support regional demand for nickel chemicals.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFGo-To-Market and Sales Economics

The Nickel Chemicals Market is mainly driven by nickel sulfate, nickel chloride, nickel carbonate, nickel hydroxide, nickel nitrate, nickel oxide, and other nickel-based compounds used in batteries, electroplating, catalysts, ceramics, pigments, and surface finishing. The strongest go-to-market route is through battery material producers, cathode manufacturers, electroplating companies, stainless steel-linked chemical processors, and industrial catalyst users.

In 2025, global nickel mine production reached an estimated 3.9 million tons, with Indonesia alone producing about 2.6 million tons, making feedstock access a critical sales advantage. Sales economics are strongest in battery-grade nickel chemicals because customers require high purity, low impurity levels, consistent crystallization, traceability, and reliable long-term supply.

Nickel sulfate remains important for NMC and NCA cathode supply chains, although lithium iron phosphate batteries are limiting nickel demand growth in some EV segments. In 2025, global EV battery deployment reached 1.2 TWh, and electric vehicles accounted for more than 70% of total lithium-ion battery deployment, supporting continued demand for battery-grade inputs.

Risk Factors & Market Barriers

The main barriers are nickel price volatility, feedstock concentration, complex refining routes, and customer qualification requirements. INSG forecast world primary nickel production at 3.715 million tonnes in 2026 and usage at 3.747 million tonnes, implying a 32,000-tonne deficit. This tighter balance can affect nickel chemical pricing and procurement security.

Supply risk is strongly linked with Indonesia. USGS estimated global nickel mine production at 3.9 million tonnes in 2025, with Indonesia producing 2.6 million tonnes. INSG also noted that Indonesia introduced tighter 2026 mining controls and a revised benchmark pricing mechanism, making policy changes important for nickel chemical buyers.

Technical and environmental barriers also remain high. Battery-grade nickel chemicals require strict control of cobalt, copper, iron, sodium, magnesium, and moisture. Plating chemicals must meet bath stability and deposition quality needs. Producers must also manage acid use, wastewater, sulfate discharge, worker exposure, transport classification, and product stewardship documentation.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is concentrated across batteries, electroplating, stainless steel-linked chemicals, catalysts, ceramics, and specialty industrial applications. Batteries provide high-value demand because nickel chemicals are converted into cathode precursor materials for EVs and energy storage. Stainless steel remains the volume anchor for nickel demand, as global stainless steel melt shop production reached 64.2 million tonnes in 2025, with Asia producing 55.3 million tonnes.

Asia remains the most important revenue region because nickel mining, refining, stainless steel production, battery manufacturing, and cathode material processing are highly concentrated there. In 2026, Indonesia is expected to account for around 51.4% of world primary nickel output, while China is projected to account for 26.9%. This concentration supports strong regional demand for nickel sulfate, nickel cathode, nickel intermediate products, and chemical conversion capacity.

Battery-linked demand is promising, but it is more selective than lithium chemicals because not every battery chemistry uses nickel. In 2025, battery electric vehicles accounted for 65% of total electric car sales, while global electric car sales exceeded 20 million units. However, the rising share of LFP batteries means nickel chemical suppliers need to focus on premium EVs, long-range vehicles, hybrid battery platforms, and high-performance applications where nickel-rich cathodes remain relevant.

Financial Impact

The financial impact in 2026 will depend on nickel metal cost, intermediate feedstock, acid use, crystallization yield, energy, waste treatment, logistics, and customer qualification. FRED reported the nickel and nickel-base alloy mill shapes index at 159.401 in May 2026, compared with 156.749 in January, showing moderate monthly pricing movement.

Margins can improve where producers convert mixed hydroxide precipitate, matte, recycled black mass, or refined nickel into battery-grade sulfate with high recovery. USGS reported Australia’s 2025 nickel mine output fell 54% as several mines moved to care-and-maintenance due to low prices, showing how weak margins can reduce supply flexibility.

Financial returns can be strengthened through recycling, long-term offtake contracts, local processing, and traceability systems. IEA and OECD surveyed more than 80 companies across copper, lithium, nickel, cobalt, graphite, and rare earth supply chains in 2025, highlighting traceability as a growing requirement for resilient and responsible mineral sourcing.

Drivers Impact Analysis

The Nickel Chemicals Market is driven by rising demand from batteries, electroplating, catalysts, pigments, ceramics, metal finishing, and specialty chemical applications. Nickel sulfate, nickel chloride, nickel carbonate, and nickel nitrate are widely used where conductivity, corrosion resistance, surface finishing, and chemical stability are required.

Asia Pacific leads the market due to strong battery manufacturing, electronics production, metal finishing, stainless steel-related industries, and electric vehicle supply chains. China, Japan, South Korea, and India remain key demand centers because of their large manufacturing base and expanding clean energy ecosystem.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising battery-grade nickel sulfate demand | +1.7% | Asia Pacific, Europe, North America | Drives battery chemical growth. |

Growth in electroplating applications | +1.3% | China, India, Southeast Asia | Supports industrial usage. |

Expansion of EV battery supply chains | +1.2% | China, South Korea, Japan, Europe | Adds future demand. |

Demand from catalysts and specialty chemicals | +0.9% | Global chemical producers | Builds value demand. |

Growth in electronics and metal finishing | +0.8% | Asia Pacific manufacturing hubs | Supports steady consumption. |

Restraints Impact Analysis

The market faces restraints from nickel price volatility, feedstock availability, and dependency on mining and refining supply chains. Nickel chemical producers need consistent raw material quality, but nickel ore, intermediate products, and refined nickel prices can move sharply. Environmental and regulatory concerns also affect production. Nickel compounds require careful handling, waste treatment, worker safety controls, and emission management, which increases compliance cost for producers and end users.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Nickel price volatility | -0.9% | Global supply chains | Pressures margins. |

Feedstock supply uncertainty | -0.8% | Asia Pacific, Europe, North America | Affects production planning. |

Environmental compliance cost | -0.7% | China, Europe, North America | Raises operating burden. |

Health and handling concerns | -0.6% | Industrial and chemical plants | Requires strict controls. |

Competition from low-nickel battery chemistries | -0.5% | EV and battery markets | Limits some demand growth. |

Opportunities Impact Analysis

Opportunities are strong in battery-grade nickel sulfate, high-purity nickel chemicals, catalysts, plating chemicals, and recycling-based nickel recovery. Battery applications offer long-term upside as nickel-rich cathodes continue to support higher energy density in selected EV segments.

Higher-value opportunities are also emerging in localized refining, closed-loop recycling, and specialty nickel chemical processing. Companies that can deliver consistent purity, stable supply, and technical support can capture stronger demand from battery, electronics, and industrial customers.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Battery-grade nickel sulfate production | +1.6% | Asia Pacific, Europe, North America | Builds premium demand. |

High-purity nickel chemical processing | +1.3% | Battery and electronics markets | Supports quality needs. |

Nickel recycling and recovery | +1.1% | China, Europe, U.S., Japan | Improves circular supply. |

Specialty catalyst applications | +0.9% | Chemical and refining sectors | Adds value usage. |

Localized chemical conversion capacity | +0.8% | India, Europe, North America | Reduces supply dependence. |

Challenges Impact Analysis

The main challenge is meeting strict purity requirements for battery and electronics applications. Even small impurities can affect cathode performance, electroplating quality, or chemical reliability, so producers need strong purification and testing systems. Another challenge is demand uncertainty from changing battery chemistry trends. Some EV batteries use nickel-rich cathodes, while others use lower-nickel or nickel-free alternatives, making long-term planning more complex for nickel chemical producers.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining battery-grade purity | -0.8% | Battery material producers | Affects product qualification. |

Managing battery chemistry shifts | -0.7% | EV supply chains | Creates demand uncertainty. |

Controlling waste and emissions | -0.6% | Chemical production sites | Raises compliance needs. |

Scaling high-purity production | -0.5% | Nickel chemical converters | Adds technical burden. |

Securing long-term customer contracts | -0.4% | Battery and industrial markets | Affects investment confidence. |

Segment Covered in the Report

By Product Type

Nickel Sulfate

Nickel Hydroxide

Nickel Chloride

Nickel Nitrate

Nickel Carbonate

Nickel Acetate

Others

By Grade

Battery Grade

Plating Grade

Industrial Grade

High-Purity Grade

Others

By Form

Powder

Crystal

Solution

Granules

Others

By Application

Batteries

Electroplating

Catalysts

Ceramics and Pigments

Chemical Intermediates

Others

By End Use

Automotive

Electronics

Chemicals

Aerospace

Industrial Manufacturing

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward nickel sulfate, high-purity nickel chemicals, recycling-based feedstock, and battery-linked chemical conversion. Nickel sulfate remains important because it is widely used in cathode precursor production for nickel-containing lithium-ion batteries.

Electroplating and metal finishing remain stable demand areas, especially in automotive, electronics, machinery, and industrial components. At the same time, sustainable sourcing and recycling are becoming more important as battery makers seek traceable and lower-impact materials.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Nickel sulfate remains key product | +1.5% | Asia Pacific, Europe, North America | Leads battery demand. |

Battery-linked refining expands | +1.3% | China, South Korea, Japan, Europe | Supports cathode supply. |

Recycling-based nickel chemicals rise | +1.1% | Europe, China, North America | Builds circular supply. |

Electroplating chemicals remain stable | +0.9% | Asia Pacific manufacturing hubs | Supports industrial demand. |

Traceable sourcing gains importance | +0.7% | Battery and electronics sectors | Improves customer trust. |

Investor Type Impact Matrix

Investors should focus on nickel chemical producers with secured feedstock, high-purity processing capability, battery customer access, and exposure to electroplating and specialty chemical applications. Stable quality and supply reliability are key success factors. Strategic investors can also target nickel recycling, battery-grade nickel sulfate, chemical conversion plants, and cathode-linked supply chains. Companies that reduce feedstock risk while meeting battery-grade specifications are better positioned for long-term value creation.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Nickel Chemical Producers | +1.5% | Global | Expands chemical supply. |

Battery Material Companies | +1.3% | Asia Pacific, Europe, North America | Drives nickel sulfate demand. |

Mining and Refining Companies | +1.0% | Indonesia, Australia, China, Canada | Supports feedstock security. |

Electroplating Chemical Suppliers | +0.8% | Asia Pacific manufacturing hubs | Builds steady demand. |

Recycling and Strategic Investors | +0.7% | China, Europe, North America | Funds circular supply. |

Recent Developments

In 2026, Electra Battery Materials advanced engineering work for a proposed battery-grade nickel refinery in the United States. The refinery is being evaluated for about 15,000 tonnes per year of nickel sulfate and metal, along with 1,000 tonnes per year of cobalt metal, using hydrometallurgical refining. This supports North American localization of nickel chemical supply for EV batteries.

In 2026, Nickel Industries completed Sphere Corp’s acquisition of a 10% interest in the Excelsior Nickel Cobalt HPAL project in Indonesia at a USD 2.4 billion valuation. Nickel Industries also revised its ownership schedule and increased its ENC holding from 44% to 46% through a final USD 46 million payment. The ENC project supports low-carbon Class 1 nickel production for battery and advanced material supply chains.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Jinchuan Group

Sumitomo Metal Mining Co., Ltd.

Vale S.A.

Glencore plc

Norilsk Nickel

Umicore

BHP

Eramet

Sherritt International

Huayou Cobalt

CNGR Advanced Material Co., Ltd.

GEM Co., Ltd.

Guangxi Yinyi Science and Technology Co., Ltd.

Boliden Group

Outokumpu

Other Key players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Carbon Capture Chemicals Market Size to Reach USD 78.0 Billion by 2035

Carbon Capture Chemicals Market By Chemical Type (Amines, Carbonates, Ammonia-based Solvents, Ionic Liquids, Solid Sorbent Chemicals, Others), By Absorption Type (Chemical Absorption, Physical Absorption), By End-Use Industry (Oil and Gas, Power Generation, Chemical and Petrochemical, Cement, Iron and Steel, Others), By Application (Post-combustion Capture, Pre-combustion Capture, Industrial Gas Separation, Direct Air Capture, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Bio-based Chemicals Market Size to Hit USD 296.7 Bn by 2035

Bio-based Chemicals Market By Product Category (Platform Chemicals, Polymers for Plastics, Paints, Coatings, Inks and Dyes, Surfactants, Cosmetics and Personal Care Products, Adhesives, Man-made Fibers, Others), By Application (Industrial, Agricultural, Pharmaceutical, Others), By Source (Plant-based, Animal-based, Microbial-based, Waste-based), By End Use (Chemical Manufacturing, Agriculture, Food and Beverage, Personal Care, Pharmaceuticals, Automotive), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Processing Chemicals Market Size to Hit USD 14.6 Billion by 2035

Hydrogen Processing Chemicals Market By Chemical Type (Catalysts, Adsorbents, Solvents, Corrosion Inhibitors, Scavengers, Others), By Function (Reforming Chemicals, Purification Chemicals, Hydroprocessing Chemicals, Gas Treatment Chemicals, Corrosion Control Chemicals, Others), By Process (Steam Methane Reforming, Hydrocracking, Hydrotreating, Pressure Swing Adsorption, Water-Gas Shift Reaction, Others), By End Use (Refineries, Ammonia Production, Methanol Production, Petrochemicals, Clean Hydrogen Plants, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Electrolyte Chemicals Market to Cross USD 49.4 Billion by 2035

Electrolyte Chemicals Market By Battery Type (Lithium-ion Electrolytes, Lead-acid Electrolytes, Flow Battery Electrolytes, Others), By Electrolyte Form (Liquid Electrolytes, Gel, Solid-State Electrolytes), By Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, Industrial and Motive Batteries, Others), By Product Type (Lithium-Based Electrolytes, Sulfide-Based Electrolytes, Polymer-Based Electrolytes, Oxide-Based Electrolytes, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035