Revenue, 2025

$ 6.7 Bn

Forecast, 2035

$ 14.6 Bn

CAGR, 2025-2035

8.1%

Report Coverage

Global

Market Size and Forecast

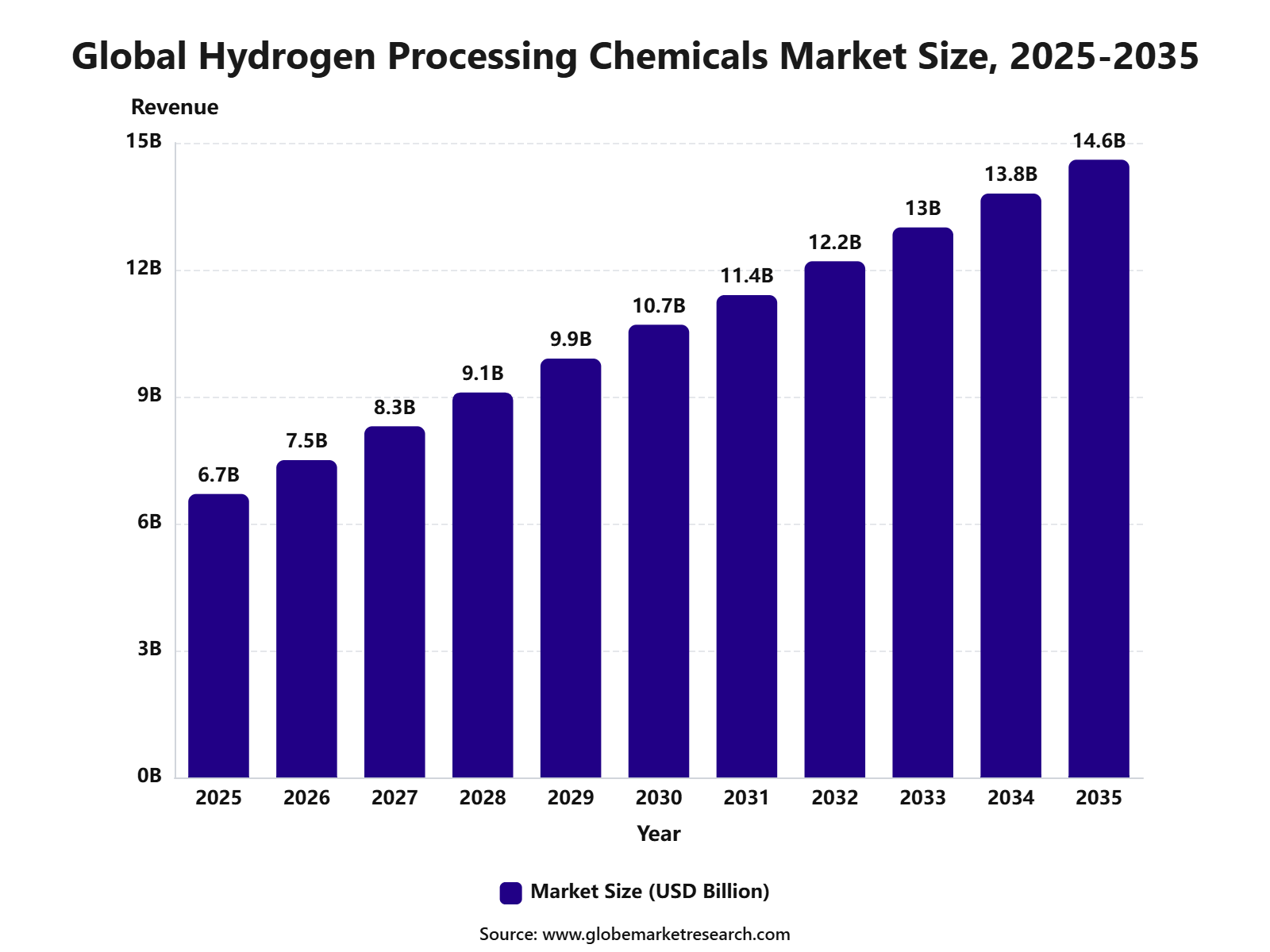

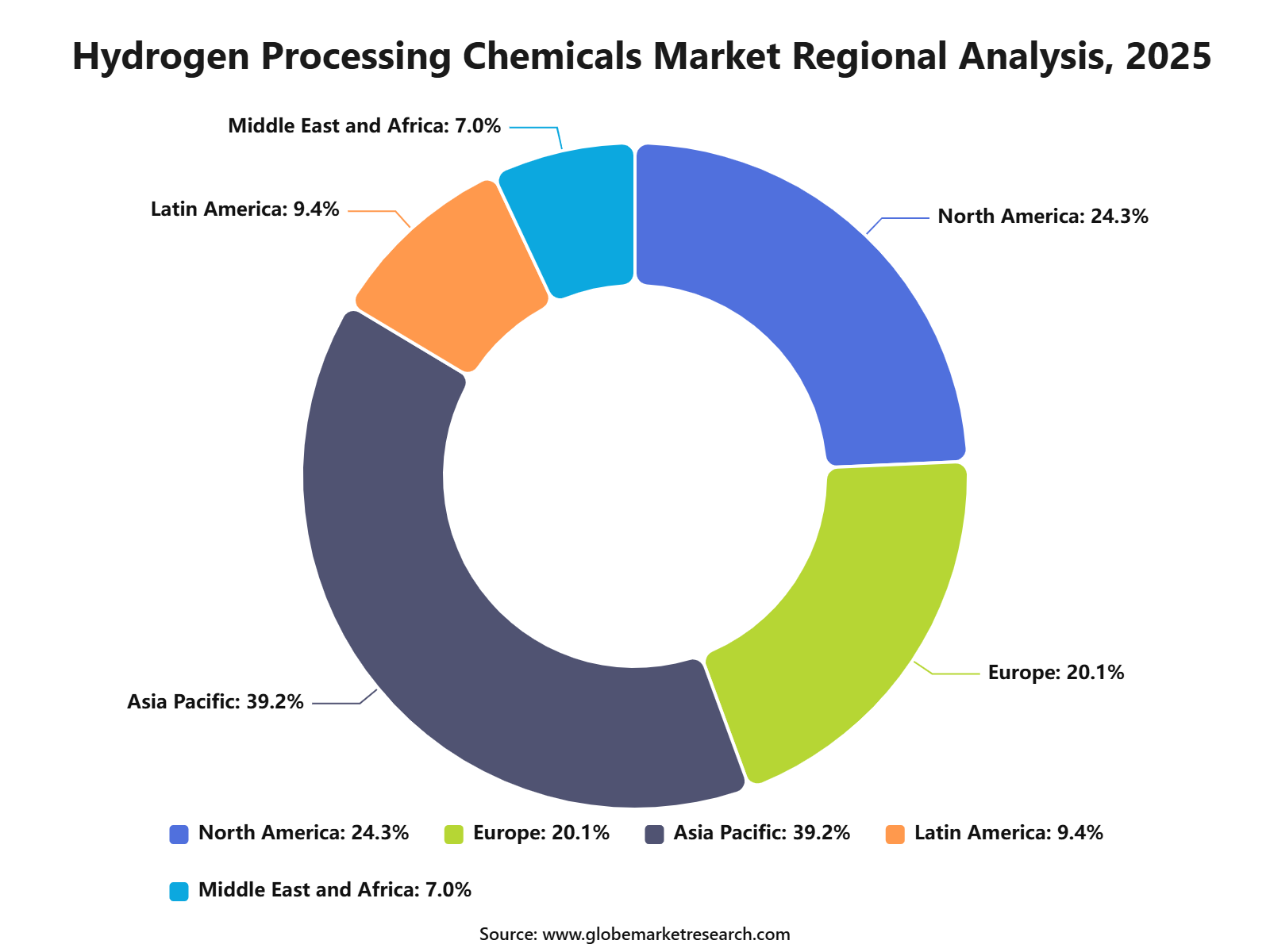

The Global Hydrogen Processing Chemicals Market was worth USD 6.7 billion in 2025 and is expected to reach USD 14.6 billion by 2035, growing at a CAGR of 8.1% from 2025 to 2035. Based on this growth rate, the market is estimated to reach around USD 7.5 billion in 2026. Asia Pacific held the largest regional share of 39.2% in 2025, supported by expanding refinery capacity, growing hydrogen production, strong chemical manufacturing, and rising demand from clean fuel and industrial processing applications.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 6.7 Billion |

Projected Revenue, 2035 | USD 14.6 Billion |

CAGR (2025-2035) | 8.1% |

Largest Region | Asia Pacific |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

What is Hydrogen Processing Chemicals Market?

The Hydrogen Processing Chemicals Market includes catalysts, adsorbents, solvents, corrosion inhibitors, purification chemicals, and process additives used across hydrogen production, refining, storage, and purification systems. These chemicals are widely used in steam methane reforming, hydrocracking, desulfurization, ammonia production, methanol production, fuel cells, and industrial gas processing. The market is closely linked with refinery upgrades, clean energy projects, petrochemical production, and hydrogen infrastructure development.

The market outlook remains positive as hydrogen continues to gain importance in refining, chemicals, energy storage, and low-carbon fuel applications. Growth can be attributed to rising demand for efficient hydrogen purification, cleaner fuel production, and advanced catalyst systems. The expansion of green hydrogen projects, industrial decarbonization programs, and high-purity hydrogen supply chains is expected to support long-term market demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Catalysts led the chemical type segment with 44.3% share, supported by their critical role in hydrogen production, refining reactions, hydroprocessing, and process efficiency improvement.

Hydroprocessing chemicals accounted for 37.9% share by function, driven by strong use in sulfur removal, fuel upgrading, catalyst protection, and refinery performance enhancement.

Steam methane reforming held 33.5% share by process, supported by its established commercial use, large-scale hydrogen output, and strong integration with refinery and petrochemical operations.

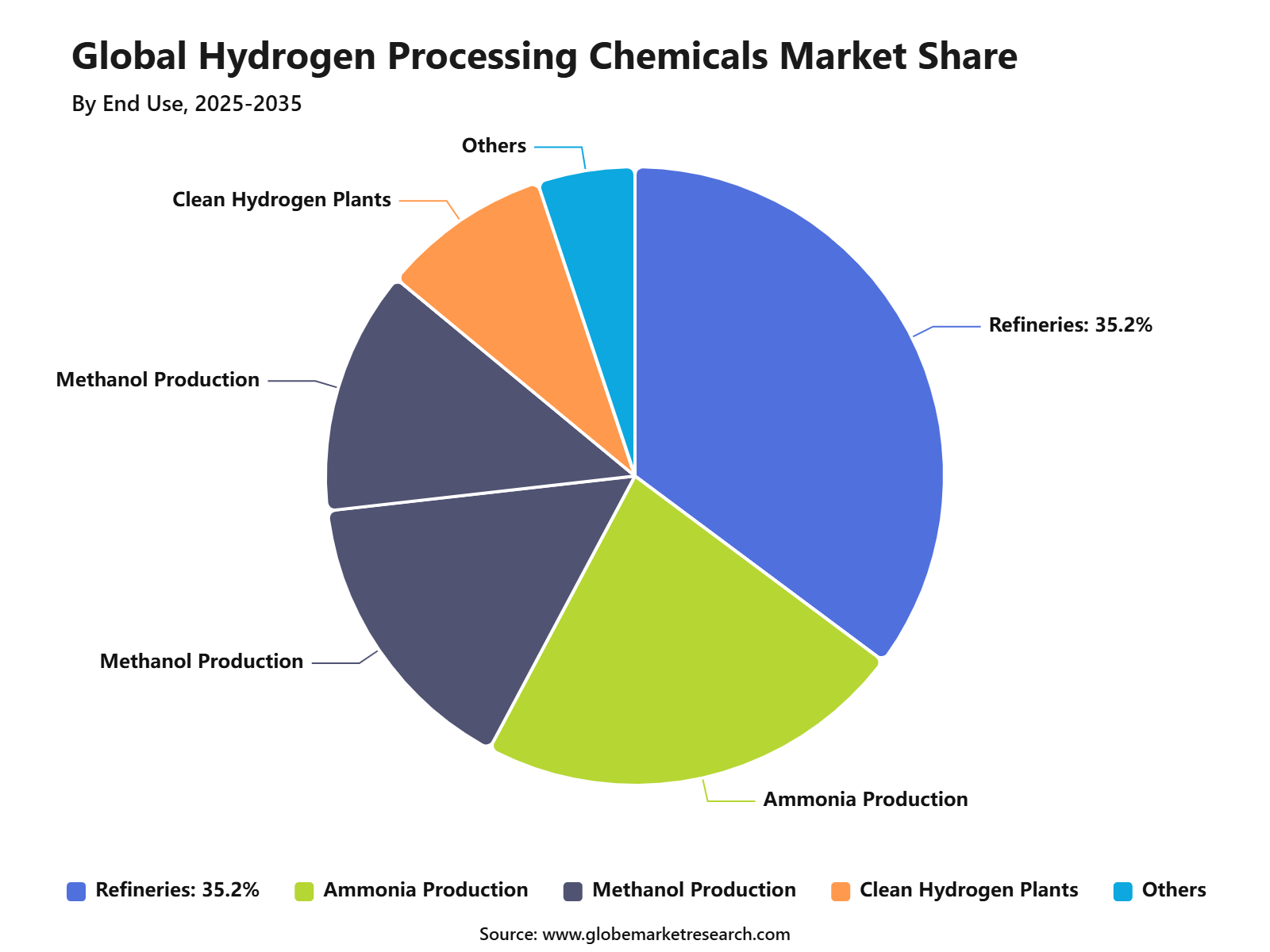

Refineries captured 35.2% share by end use, driven by rising demand for hydrogen processing chemicals in fuel desulfurization, crude upgrading, and cleaner fuel production.

Asia Pacific led the hydrogen processing chemicals market with 39.2% share, supported by strong refining capacity, expanding petrochemical production, rising fuel demand, and high industrial hydrogen consumption across China, India, Japan, and Southeast Asia.

Top Funding and Investment

NEOM Green Hydrogen Company is investing USD 8.4 billion with support from partners and 23 local, regional, and international banks. The project is being built to produce up to 600 tonnes of carbon-free hydrogen per day and export up to 1.2 million tonnes of green ammonia per year. This supports demand for hydrogen purification systems, ammonia synthesis catalysts, water-treatment chemicals, and process-control materials used in large hydrogen-to-ammonia value chains.

Air Liquide and TotalEnergies announced two large-scale hydrogen projects in the Netherlands with a combined investment of more than EUR 1.0 billion. The plan includes a 200 MW ELYgator electrolyzer in Rotterdam and a 250 MW electrolyzer in Zeeland, with combined renewable hydrogen production potential of about 53,000 tonnes per year. This investment strengthens demand for electrolyzer materials, hydrogen purification, refinery hydrogen handling, and process chemicals used in low-carbon refinery operations.

Honeywell entered an amended agreement in February 2026 to acquire Johnson Matthey’s Catalyst Technologies business for GBP 1.325 billion, revised from the earlier GBP 1.8 billion value. The business adds catalyst manufacturing and process technology capabilities across refining, petrochemicals, renewable fuels, blue hydrogen, blue ammonia, and sustainable methanol. This is highly relevant for hydrogen processing chemicals because catalysts are central to steam reforming, water-gas shift, purification, and downstream conversion processes.

Technip Energies agreed to acquire Ecovyst’s Advanced Materials & Catalysts business for USD 556.0 million, equal to about 9.8x EBITDA. The acquired business generated USD 223.0 million revenue in 2024, had an EBITDA margin of about 25%, and included advanced silicas and Zeolyst, a supplier of zeolite-based catalysts used in hydrocracking, sustainable fuels, and custom catalyst applications. This deal strengthens catalyst supply for hydrogen-linked refining and fuel-upgrading processes.

By Chemical Type

Catalysts accounted for 44.3% share of the Hydrogen Processing Chemicals Market. This leadership can be attributed to their critical role in improving reaction efficiency, hydrogen yield, feedstock conversion, and overall process performance across refining and chemical production.

Catalysts are widely used in steam methane reforming, hydroprocessing, desulfurization, ammonia production, methanol production, and other hydrogen-linked industrial processes. They help reduce reaction time, improve selectivity, and support stable operation under high-temperature and high-pressure conditions.

Demand for catalysts is expected to remain strong as refineries and industrial producers focus on process efficiency, cleaner fuels, and lower emissions. Their importance in hydrogen generation and fuel upgrading makes them a core chemical type in this market.

By Function

Hydroprocessing chemicals held 37.9% share of the Hydrogen Processing Chemicals Market. This strong position is supported by their wide use in removing sulfur, nitrogen, metals, and other impurities from petroleum feedstocks and refined products. These chemicals support hydrodesulfurization, hydrodenitrogenation, hydrocracking, and fuel upgrading operations.

They are essential for producing cleaner gasoline, diesel, jet fuel, and petrochemical feedstocks that meet strict quality and emission standards. The segment is expected to maintain steady demand as refineries continue to process heavier and more complex crude oils. Hydroprocessing chemicals help improve product quality, protect equipment, and support compliance with cleaner fuel regulations.

By Process

Steam methane reforming accounted for 33.5% share of the Hydrogen Processing Chemicals Market. This dominance is driven by its established use as one of the most common industrial methods for large-scale hydrogen production. The process uses natural gas and steam to produce hydrogen, with catalysts playing an important role in improving conversion efficiency and operating stability.

Chemicals used in this process support reforming, shift conversion, purification, and protection of processing equipment. Steam methane reforming is expected to remain important due to its mature infrastructure, high hydrogen output, and cost efficiency. Demand will also be supported by refinery hydrogen needs, ammonia production, methanol production, and industrial gas applications.

By End Use

Refineries held 35.2% share of the Hydrogen Processing Chemicals Market. This leading share is mainly supported by the heavy use of hydrogen in fuel desulfurization, hydrocracking, reforming, and upgrading of petroleum products. Hydrogen processing chemicals are used to improve refinery efficiency, remove impurities, protect catalysts, and produce cleaner transportation fuels.

These chemicals help refineries meet product quality standards while handling different crude oil grades and process conditions. The refinery segment is expected to remain a major demand center as fuel quality requirements and operational efficiency targets continue to increase. Hydrogen chemicals will remain essential for cleaner fuel production, residue upgrading, and long-term refinery performance.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Region

Asia Pacific accounted for 39.2% share of the Hydrogen Processing Chemicals Market, making it the leading regional market. Growth is supported by large refinery capacity, expanding petrochemical production, rising fuel demand, and industrial hydrogen consumption across major economies.

China, India, Japan, South Korea, and Southeast Asian countries are key contributors to regional demand. The region benefits from refinery expansion, chemical manufacturing growth, ammonia production, methanol production, and investment in hydrogen-related infrastructure.

Asia Pacific is expected to maintain its leading position as energy demand and industrial output continue to grow. The need for cleaner fuels, higher refinery efficiency, and reliable hydrogen production will further support demand for hydrogen processing chemicals across the region.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFGo-To-Market and Sales Economics

The Hydrogen Processing Chemicals Market is driven by chemicals, catalysts, adsorbents, purification media, corrosion inhibitors, desulfurization agents, reforming catalysts, shift catalysts, hydroprocessing catalysts, amines, and process additives used across hydrogen production, refining, ammonia, methanol, fuel upgrading, and low-emissions hydrogen projects. The strongest sales route is through refineries, ammonia plants, methanol producers, industrial gas suppliers, EPC contractors, hydrogen unit operators, and electrolyser project developers.

Go-to-market success depends on process reliability, catalyst life, hydrogen purity, sulfur removal performance, plant uptime, and technical service. Hydrogen demand surpassed 100 million tonnes in 2025, with almost all demand coming from industry and refining. This makes established industrial users the core customer base for hydrogen processing chemicals, especially in steam methane reforming, hydrocracking, hydrotreating, ammonia synthesis, methanol production, and hydrogen purification.

Sales economics are supported by repeated chemical consumption and scheduled catalyst replacement. Refineries and chemical plants do not purchase only a product; they need performance testing, turnaround support, feedstock analysis, catalyst loading guidance, contamination control, and emergency troubleshooting. Low-emissions hydrogen production grew by 20% in 2025 and is expected to cross 1% of global production in 2026, which is creating additional demand for purification, water treatment, electrolyser chemicals, and process-control additives.

Risk Factors & Market Barriers

The main barriers are feedstock volatility, catalyst poisoning, safety compliance, and customer qualification time. Hydrogen processing depends heavily on natural gas, refinery gas, water, steam, sulfur control, and high-temperature reactors. DOE notes that natural gas reforming uses methane to produce hydrogen through steam-methane reforming and partial oxidation routes.

Refinery-linked demand can fluctuate with utilization rates and fuel regulations. EIA data showed U.S. refinery operable utilization at 94.7% for the week ending May, 2026. High utilization supports hydroprocessing chemicals, but outages, turnarounds, crude quality shifts, and low fuel margins can delay catalyst replacement and chemical ordering.

Technical risk is high because sulfur, chlorine, arsenic, metals, carbon deposition, and moisture can shorten catalyst life. NETL states that hydrodesulfurization consumes large amounts of hydrogen, needs catalysts that are easily poisoned, and operates under severe temperature and pressure conditions. This raises the need for strong pretreatment chemistry.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is strongest across refining, ammonia, methanol, fertilizers, low-emissions hydrogen, hydrogen-based fuels, and industrial gas supply. Ammonia and methanol together represent roughly half of global hydrogen consumption, while disruptions in 2026 showed how closely hydrogen-based products are linked with fertilizers, chemicals, and food security. Urea prices doubled between January and May 2026, and methanol prices increased sharply, which increased the focus on reliable hydrogen processing and feedstock security.

Refining remains a major revenue channel because hydrogen is used for hydrotreating, hydrocracking, sulfur reduction, and fuel quality improvement. In March 2026, more than 3 million barrels per day of refining capacity in the Middle East had already shut due to attacks and export restrictions, while more than 4 million barrels per day was at risk. Such disruptions increase the need for process chemicals that support refinery reliability, rapid restart, sulfur control, catalyst protection, and flexible feedstock processing.

Low-emissions hydrogen is creating a new revenue layer. New offtake agreements reached 1.7 million tonnes per year in 2025, while more than 0.3 million tonnes per year had been contracted by Q1 2026, mostly in refining and fertilizers. Based on committed projects, 2.5 million tonnes of low-emissions hydrogen is expected to be produced and consumed in refineries and industrial facilities by 2030, supporting demand for catalysts, purification systems, water treatment chemicals, and process additives.

Financial Impact

The financial impact in 2026 will depend on natural gas cost, catalyst metals, adsorbent replacement cycles, plant uptime, regeneration cost, hydrogen purity requirements, and emissions compliance. FRED reported the U.S. industrial gas manufacturing index for argon and hydrogen at 114.110 in May 2026, showing a measurable pricing base.

Input-cost pressure also affects producers of inorganic processing chemicals. FRED reported the basic inorganic chemicals producer price index at 376.905 in May 2026, compared with 359.265 in January 2026. This can affect caustic, acids, adsorbents, sulfur-treatment chemicals, and catalyst-support materials used in hydrogen processing systems.

Profitability can improve where suppliers combine chemicals, catalysts, monitoring, and technical service. Higher returns are expected from long-life catalysts, impurity guards, low-carbon hydrogen projects, refinery turnaround services, and ammonia plant optimization. Companies that reduce downtime, extend catalyst cycles, and improve hydrogen purity can protect margins despite volatile feedstock and energy costs.

Drivers Impact Analysis

The Hydrogen Processing Chemicals Market is driven by rising hydrogen production, refinery upgrading, hydroprocessing, ammonia production, petrochemical processing, fuel desulfurization, and clean fuel demand. These chemicals support catalyst activity, gas purification, corrosion control, process stability, and impurity removal.

Asia Pacific leads the market due to strong refining capacity, petrochemical production, fertilizer manufacturing, and industrial hydrogen consumption. China, India, Japan, South Korea, and Southeast Asia remain important demand centers because of large energy, chemical, and manufacturing operations.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising refinery hydroprocessing demand | +2.0% | Asia Pacific, Middle East, North America | Drives core chemical usage. |

Growth in hydrogen production capacity | +1.7% | China, India, U.S., Europe | Supports process chemical demand. |

Fuel desulfurization requirements | +1.5% | Asia Pacific, Europe, North America | Increases catalyst and treatment use. |

Expansion of ammonia and methanol production | +1.2% | Asia Pacific, Middle East | Adds industrial demand. |

Petrochemical processing growth | +1.0% | China, India, Southeast Asia | Supports recurring chemical consumption. |

Restraints Impact Analysis

The market faces restraints from high catalyst cost, feedstock price volatility, and strict handling requirements. Hydrogen processing chemicals must perform under high temperature, pressure, and reactive operating conditions, which increases technical and safety requirements. Another restraint is process dependency on refinery and petrochemical investment cycles. If refinery expansion or upgrading slows, demand for hydroprocessing chemicals, catalysts, corrosion inhibitors, and purification chemicals may also weaken.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High catalyst and specialty chemical cost | -1.0% | Global refineries and chemical plants | Pressures operating budgets. |

Feedstock and energy price volatility | -0.8% | Asia Pacific, Europe, North America | Affects production economics. |

Complex handling and storage needs | -0.7% | Refinery and hydrogen plants | Raises safety burden. |

Dependence on refinery upgrade cycles | -0.6% | Mature refining markets | Limits steady expansion. |

Environmental compliance requirements | -0.5% | Europe, North America, Japan | Increases treatment cost. |

Opportunities Impact Analysis

Opportunities are strong in hydroprocessing catalysts, hydrogen purification chemicals, sulfur removal chemicals, corrosion inhibitors, reforming process chemicals, and ammonia-linked hydrogen applications. These areas benefit from cleaner fuel standards and stronger demand for high-quality process output.

Higher-value growth is also emerging in blue hydrogen, green hydrogen support chemicals, and low-carbon fuel processing. Companies that improve catalyst life, process efficiency, impurity control, and plant reliability can capture stronger demand from refiners and industrial hydrogen users.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Hydroprocessing catalyst demand | +1.9% | Asia Pacific, Middle East, North America | Builds core market value. |

Hydrogen purification solutions | +1.6% | Industrial hydrogen hubs | Improves gas quality. |

Sulfur removal chemical expansion | +1.4% | Refining and fuel processing markets | Supports cleaner fuels. |

Blue hydrogen process support | +1.1% | North America, Europe, Middle East | Adds low-carbon opportunity. |

Green hydrogen integration chemicals | +0.9% | Japan, Europe, India, South Korea | Creates future demand. |

Challenges Impact Analysis

The main challenge is maintaining chemical performance under severe process conditions. Hydrogen processing often involves high pressure, high temperature, sulfur compounds, hydrocarbons, and reactive gases, which can reduce catalyst life and increase maintenance needs. Another challenge is matching chemical selection with process design. Steam methane reforming, hydroprocessing, gas purification, ammonia synthesis, and refinery hydrogen systems require different chemical packages, catalyst systems, and operating support.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining catalyst life | -0.9% | Refineries and hydrogen plants | Affects operating cost. |

Managing high-pressure process risk | -0.8% | Hydrogen production facilities | Raises safety requirements. |

Controlling sulfur and impurity loads | -0.7% | Refining and gas treatment | Protects process stability. |

Matching chemicals to process design | -0.6% | Industrial hydrogen users | Increases technical complexity. |

Reducing unplanned downtime | -0.5% | Large processing plants | Impacts profitability. |

Segment Covered in the Report

By Chemical Type

Catalysts

Adsorbents

Solvents

Corrosion Inhibitors

Scavengers

Others

By Function

Reforming Chemicals

Purification Chemicals

Hydroprocessing Chemicals

Gas Treatment Chemicals

Corrosion Control Chemicals

Others

By Process

Steam Methane Reforming

Hydrocracking

Hydrotreating

Pressure Swing Adsorption

Water-Gas Shift Reaction

Others

By End Use

Refineries

Ammonia Production

Methanol Production

Petrochemicals

Clean Hydrogen Plants

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward catalysts, hydroprocessing chemicals, hydrogen purification chemicals, reforming support chemicals, and process protection additives. Catalysts remain the most important product area because they directly influence reaction efficiency and product quality.

Refineries and chemical plants are also focusing on longer catalyst life, lower emissions, and better sulfur removal performance. Asia Pacific continues to lead demand, while North America and Europe support high-value demand through cleaner fuel standards and low-carbon hydrogen projects.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Catalysts remain leading chemical type | +1.8% | Global hydrogen processing markets | Leads value demand. |

Hydroprocessing chemicals gain usage | +1.5% | Refineries and fuel processors | Supports cleaner output. |

Hydrogen purification demand rises | +1.3% | Industrial hydrogen producers | Improves gas quality. |

Corrosion control chemicals expand | +1.0% | Refineries and petrochemical plants | Protects assets. |

Low-carbon hydrogen trend increases | +0.9% | Europe, North America, Asia Pacific | Supports future demand. |

Investor Type Impact Matrix

Investors should focus on hydrogen processing chemical suppliers with strong catalyst portfolios, refinery customer access, purification technologies, and technical service capability. Stable performance, safety support, and long operating life are key buying factors. Strategic investors can also target low-carbon hydrogen process chemicals, advanced hydroprocessing catalysts, sulfur removal technologies, and corrosion control solutions. Companies that improve efficiency while lowering emissions and downtime are better positioned for long-term growth.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Hydrogen Processing Chemical Producers | +1.7% | Global | Expands chemical supply. |

Catalyst Manufacturers | +1.5% | Asia Pacific, Middle East, North America | Drives process efficiency. |

Refinery and Petrochemical Suppliers | +1.2% | Industrial processing hubs | Supports recurring demand. |

Industrial Gas and Hydrogen Companies | +1.0% | Global hydrogen markets | Builds process demand. |

Strategic and Clean Energy Investors | +0.8% | Asia Pacific, Europe, North America | Funds low-carbon growth. |

Recent Developments

In 2026, BASF started up the world’s first production plant for 3D-printed catalysts based on X3D technology at Ludwigshafen, Germany. The facility supports industrial-scale additive manufacturing of catalysts and is relevant for process units where catalyst shape, pressure drop, conversion efficiency, and long operating cycles are critical.

In 2026, Johnson Matthey was selected by Phelan Green Hydrogen for a planned e-SAF facility in South Africa. The project will use JM Catalyst Technologies’ HyCOgen process, which converts CO₂ and electrolytic hydrogen into carbon monoxide, followed by syngas conversion through FT CANS technology. The first phase is expected to produce around 35,000 tonnes of e-SAF annually, with all phases expected to reach about 140,000 tonnes per year.

In 2026, Axens signed a collaboration with Green Sky Capital for a 200,000 tonnes per year sustainable aviation fuel facility in Egypt. Axens will provide its Vegan HEFA technology, along with integrated catalyst and adsorbent solutions, operational support, and training services. This development supports demand for hydrogenation and hydroprocessing catalysts used in renewable fuel production.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Carbon Capture Chemicals Market Size to Reach USD 78.0 Billion by 2035

Carbon Capture Chemicals Market By Chemical Type (Amines, Carbonates, Ammonia-based Solvents, Ionic Liquids, Solid Sorbent Chemicals, Others), By Absorption Type (Chemical Absorption, Physical Absorption), By End-Use Industry (Oil and Gas, Power Generation, Chemical and Petrochemical, Cement, Iron and Steel, Others), By Application (Post-combustion Capture, Pre-combustion Capture, Industrial Gas Separation, Direct Air Capture, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Bio-based Chemicals Market Size to Hit USD 296.7 Bn by 2035

Bio-based Chemicals Market By Product Category (Platform Chemicals, Polymers for Plastics, Paints, Coatings, Inks and Dyes, Surfactants, Cosmetics and Personal Care Products, Adhesives, Man-made Fibers, Others), By Application (Industrial, Agricultural, Pharmaceutical, Others), By Source (Plant-based, Animal-based, Microbial-based, Waste-based), By End Use (Chemical Manufacturing, Agriculture, Food and Beverage, Personal Care, Pharmaceuticals, Automotive), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Electrolyte Chemicals Market to Cross USD 49.4 Billion by 2035

Electrolyte Chemicals Market By Battery Type (Lithium-ion Electrolytes, Lead-acid Electrolytes, Flow Battery Electrolytes, Others), By Electrolyte Form (Liquid Electrolytes, Gel, Solid-State Electrolytes), By Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, Industrial and Motive Batteries, Others), By Product Type (Lithium-Based Electrolytes, Sulfide-Based Electrolytes, Polymer-Based Electrolytes, Oxide-Based Electrolytes, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Nickel Chemicals Market to Cross USD 19.1 Billion by 2035

Nickel Chemicals Market By Product Type (Nickel Sulfate, Nickel Hydroxide, Nickel Chloride, Nickel Nitrate, Nickel Carbonate, Nickel Acetate, Others), By Grade (Battery Grade, Plating Grade, Industrial Grade, High-Purity Grade, Others), By Form (Powder, Crystal, Solution, Granules, Others), By Application (Batteries, Electroplating, Catalysts, Ceramics and Pigments, Chemical Intermediates, Others), By End Use (Automotive, Electronics, Chemicals, Aerospace, Industrial Manufacturing, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035