Revenue, 2025

$ 7.2 Bn

Forecast, 2035

$ 78.0 Bn

CAGR, 2025-2035

26.9%

Report Coverage

Global

Market Size and Forecast

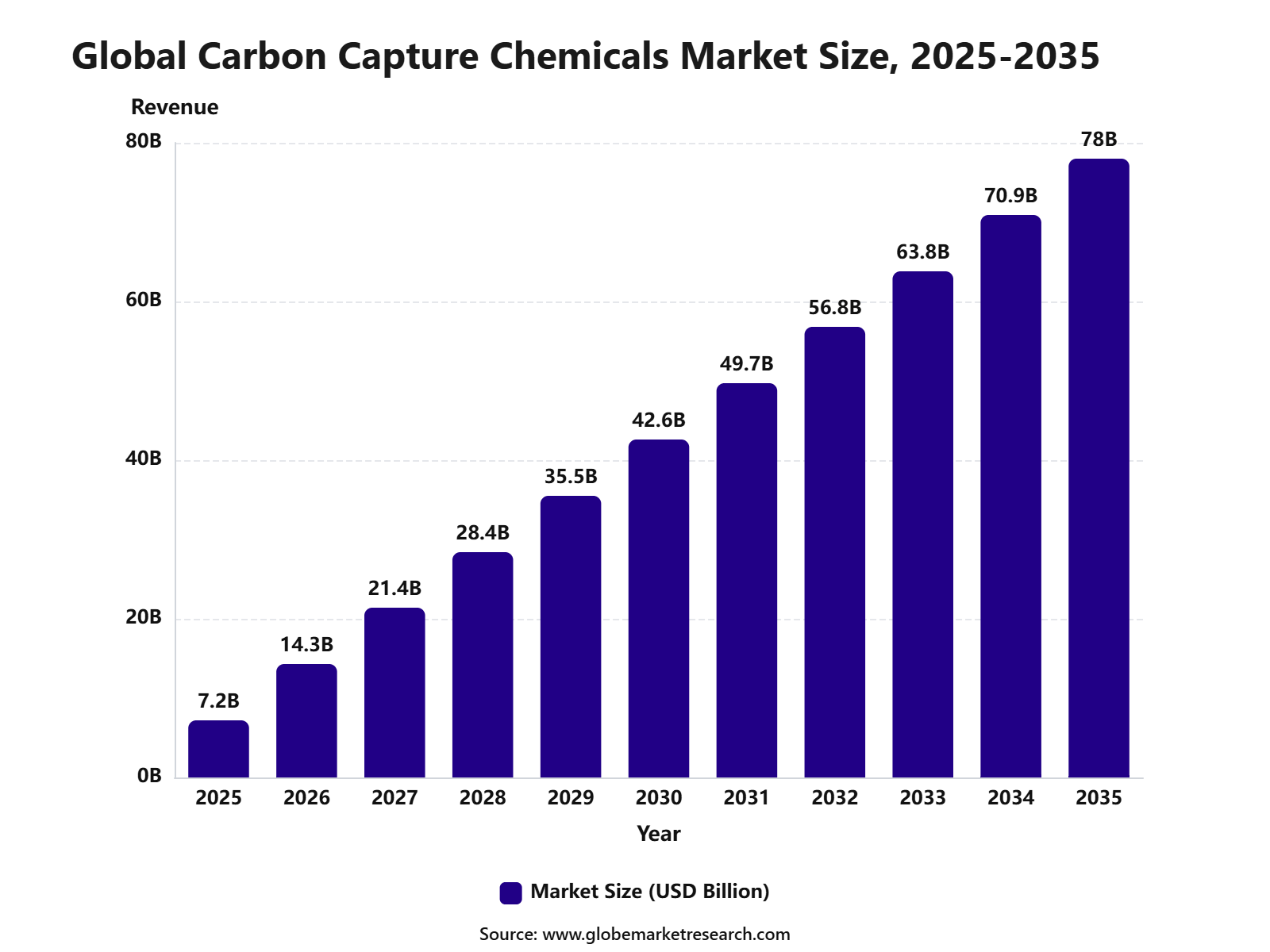

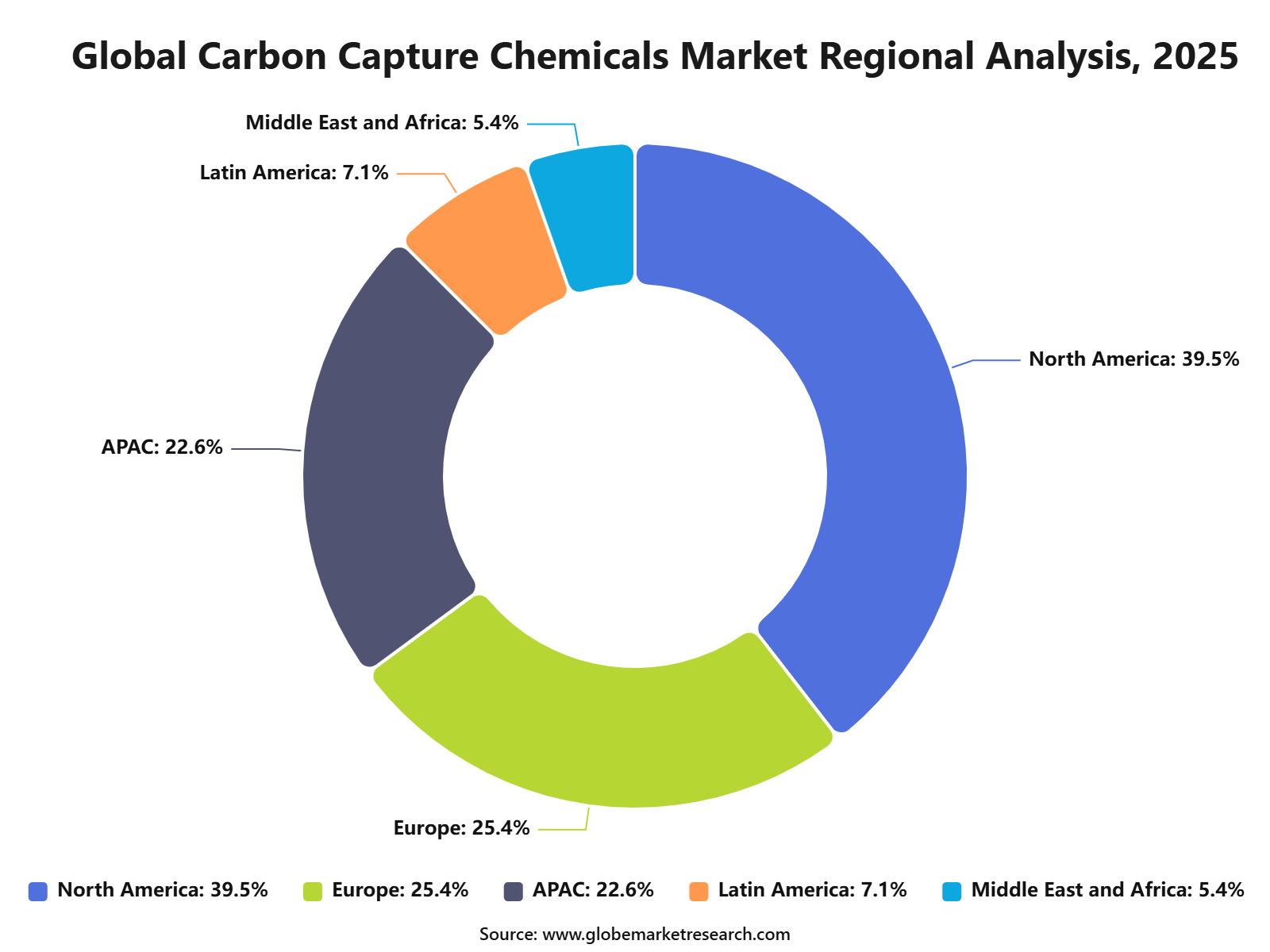

The Global Carbon Capture Chemicals Market was worth USD 7.2 billion in 2025 and is expected to reach USD 78.0 billion by 2035, growing at a CAGR of 26.9% from 2025 to 2035. Based on this growth rate, the market is estimated to reach around USD 14.3 billion in 2026. North America held the largest regional share of 39.5% in 2025, supported by strong carbon capture projects, clean energy investments, industrial decarbonization programs, and supportive policy frameworks.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 7.2 Billion |

Projected Revenue, 2035 | USD 78.0 Billion |

CAGR (2025-2035) | 26.9% |

Largest Region | North America |

Fastest Growing Region | Asia Pacific |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

What is the Carbon Capture Chemicals Market?

The Carbon Capture Chemicals Market includes solvents, sorbents, amines, catalysts, absorbents, and process chemicals used to capture, separate, purify, and store carbon dioxide from industrial emissions. These chemicals are widely used in power plants, cement production, steel manufacturing, oil and gas processing, hydrogen production, chemical plants, and direct air capture systems. The market is closely linked with carbon management, emission reduction technologies, and low-carbon industrial operations.

The market outlook remains strong as industries increase investment in carbon capture, utilization, and storage solutions. Growth can be attributed to rising pressure to reduce industrial emissions, expanding carbon capture infrastructure, and growing demand for efficient CO₂ separation chemicals. The expansion of amine-based solvents, advanced solid sorbents, and next-generation capture technologies is expected to support long-term market demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Amines led the chemical type segment with 46.8% share, supported by their strong CO₂ absorption capacity, proven use in capture systems, and wide adoption in industrial carbon removal processes.

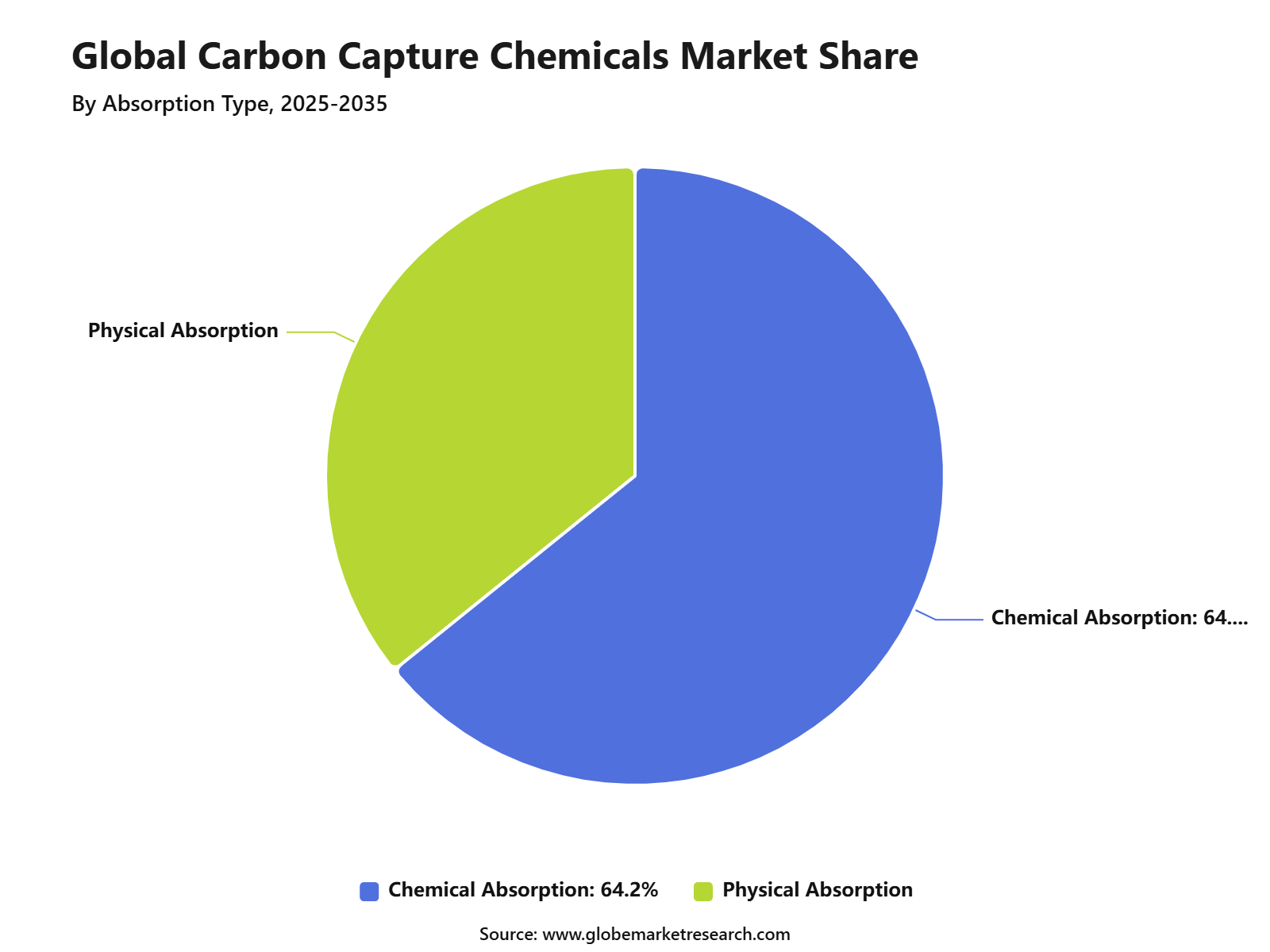

Chemical absorption accounted for 64.2% share, driven by its high efficiency in separating CO₂ from flue gases and process emissions across energy and industrial facilities.

Oil and gas held 35.6% share by end-use industry, supported by rising use of carbon capture chemicals in gas processing, refinery operations, emission control, and decarbonization projects.

Post-combustion capture captured 52.3% share by application, driven by its suitability for existing power plants, refineries, cement facilities, and other large emission sources.

North America led the carbon capture chemicals market with 39.5% share, supported by strong carbon management policies, active CCS project development, and rising investment in industrial emission reduction.

Top Funding and Investment

Occidental agreed to acquire Carbon Engineering for about USD 1.1 billion in cash. The deal is highly relevant to carbon capture chemicals because Carbon Engineering’s liquid direct air capture system uses closed-loop chemistry, while NETL notes that its process uses a potassium hydroxide solvent to remove CO₂ from air.

Climeworks raised CHF 600.0 million, equal to about USD 650.0 million, in equity funding to scale direct air capture. Its DAC platform uses solid sorbent filter materials that bind CO₂ and release it for storage or use. The investment supports demand for advanced sorbents, filter media, and regeneration chemistry.

Svante raised USD 318.0 million in Series E funding led by Chevron New Energies. The funds were aimed at accelerating production of its carbon capture technology. Svante develops solid sorbent systems, including metal-organic framework materials such as CALF-20, used in modular carbon capture filters.

Carbon Clean raised USD 150.0 million in a funding round led by Chevron, with participation from industrial and energy investors. The company had raised USD 195.0 million in total by that point. Its platform started with advanced solvents and now targets modular capture systems for cement, steel, refining, and other hard-to-abate industries.

ION Clean Energy raised USD 45..0 million from Chevron New Energies and Carbon Direct Capital in April 2024. The capital is being used to support commercial deployment of ICE-31 liquid amine carbon capture technology for hard-to-abate industrial emissions. This directly supports demand for amine-based capture solvents and solvent-management systems.

By Chemical Type

Amines accounted for 46.8% share of the Carbon Capture Chemicals Market. This leading position can be attributed to their strong ability to react with carbon dioxide and support efficient separation from flue gas and industrial gas streams.

Amine-based chemicals such as monoethanolamine, diethanolamine, and methyl diethanolamine are widely used in carbon capture systems because they offer proven absorption performance. These chemicals are commonly applied in power plants, refineries, gas processing units, cement plants, and chemical production facilities.

Demand for amines is expected to remain strong as industries focus on reducing carbon emissions while using established capture technologies. Their proven performance, commercial availability, and compatibility with post-combustion systems support their dominant position in this market.

By Absorption Type

Chemical absorption held 64.2% share of the Carbon Capture Chemicals Market. This dominance is supported by its high capture efficiency and wide use in industrial facilities where carbon dioxide must be separated from mixed gas streams.

The process uses reactive solvents, mainly amine-based chemicals, to bind with carbon dioxide and then release it during regeneration. This method is preferred because it is suitable for large-scale applications and can be integrated into existing industrial emission control systems.

The segment is expected to maintain strong demand as carbon capture projects expand across energy, oil and gas, cement, steel, and chemical sectors. Chemical absorption remains one of the most commercially mature methods for capturing carbon dioxide from flue gas.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy End-Use Industry

The oil and gas industry accounted for 35.6% share of the Carbon Capture Chemicals Market. This leadership is driven by the large use of carbon capture chemicals in gas processing, refinery operations, enhanced oil recovery, and emissions reduction projects.

Carbon capture chemicals are used to remove carbon dioxide from natural gas, refinery gas, hydrogen production streams, and industrial exhaust gases. These chemicals help improve gas quality, meet processing requirements, and support lower-emission operations across upstream and downstream activities.

The segment is expected to remain a major demand center as oil and gas companies invest in carbon management and cleaner production practices. Carbon capture chemicals will remain important for decarbonizing existing assets while maintaining operational reliability.

By Application

Post-combustion capture held 52.3% share of the Carbon Capture Chemicals Market. This leading share is supported by its ability to capture carbon dioxide from flue gases after fuel combustion in power plants and industrial facilities. This application is widely used because it can be retrofitted into existing emission sources without fully changing the core production process.

Chemical solvents, especially amines, are commonly used to absorb carbon dioxide from exhaust gases before compression, transport, or storage. Demand for post-combustion capture is expected to remain strong as industries seek practical ways to reduce emissions from existing plants. Its use across power generation, cement, steel, refining, and chemical manufacturing supports its leading position.

By Region

North America accounted for 39.5% share of the Carbon Capture Chemicals Market, making it the leading regional market. Growth is supported by strong carbon capture project development, established oil and gas operations, advanced industrial infrastructure, and supportive decarbonization initiatives.

The United States and Canada are key contributors due to active investment in carbon capture, utilization, and storage projects. Demand is also supported by refineries, natural gas processing plants, hydrogen production facilities, power plants, and heavy industrial sectors.

North America is expected to maintain a strong position as companies focus on reducing industrial emissions and improving carbon management. The region’s mature energy sector, technical expertise, and growing project pipeline will continue to support demand for carbon capture chemicals.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Europe remains important because of strict climate goals, carbon pricing, and strong industrial decarbonization activity. Asia Pacific is expected to build future demand through cement, steel, refining, power generation, and chemical production in China, India, Japan, and South Korea.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

North America market leadership | +7.0% | North America, 39.5% share in 2025 | Leads value demand. |

U.S. carbon capture project activity | +5.2% | U.S. | Drives regional growth. |

Canada carbon storage and industrial hubs | +3.8% | Canada | Supports capture deployment. |

Europe industrial decarbonization | +3.5% | Germany, UK, Netherlands, Norway | Builds premium demand. |

Asia Pacific heavy industry demand | +3.0% | China, India, Japan, South Korea | Supports future scale. |

Go-To-Market and Sales Economics

The Carbon Capture Chemicals Market should be positioned around high-emission industries such as cement, steel, refining, chemicals, ammonia, hydrogen, power generation, pulp and paper, and waste-to-energy. Demand is mainly driven by solvents, sorbents, amines, potassium carbonate systems, alkaline solutions, catalysts, corrosion inhibitors, antifoams, and CO₂ purification chemicals used in point-source capture and direct air capture systems.

Sales economics are becoming project-based rather than only chemical-volume based. Buyers usually need pilot testing, solvent performance validation, degradation analysis, corrosion control, regeneration-energy assessment, and long-term technical support before commercial adoption. The demand base is expanding because global greenhouse gas emissions reached 53.2 Gt CO₂e in 2024, while fossil CO₂ accounted for 74.5% of total global emissions, creating stronger pressure on industrial decarbonization technologies.

Risk Factors & Market Barriers

The main barriers are high energy demand, solvent degradation, corrosion, emissions control, and long customer qualification timelines. Amine-based capture is technically mature but can suffer from oxidative degradation, solvent loss, foaming, heat-stable salts, and corrosion. These risks increase operating cost and make chemical selection critical for commercial performance.

Regulatory and environmental risk must also be managed. Carbon capture chemicals can create amine emissions, degradation products, wastewater, reclaiming residues, and worker exposure concerns. Projects must prove that capture performance does not create new air, water, or hazardous waste problems, especially near communities, refineries, cement plants, and gas-processing units.

Input-cost pressure can affect pricing and margins. FRED reported the U.S. Industrial Chemicals Producer Price Index at 344.336 in May 2026, compared with 288.371 in January 2026. Primary Basic Organic Chemicals reached 340.203 in May, showing cost movement across solvent, amine, additive, and process-chemical supply chains.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is strongest in post-combustion capture, pre-combustion capture, direct air capture, CO₂ compression support, flue-gas conditioning, and carbon utilization processes. Chemical absorption remains one of the most mature routes, especially for industrial flue gas streams where amine-based and advanced solvent systems are already being tested or used. Sorbents and alkaline capture chemicals are also gaining attention where lower solvent loss and modular deployment are required.

The project pipeline supports long-term chemical demand. As of Q1 2025, global operating CO₂ capture and storage capacity was just over 50 Mt CO₂, while current project pipelines could lift capture capacity to around 430 Mt CO₂ per year by 2030. Storage capacity could reach about 670 Mt CO₂ by 2030, which indicates a wider deployment base for capture chemicals, solvent management, and plant maintenance services.

Financial Impact

Financial impact is shaped by capture cost, solvent replacement rate, regeneration energy, plant downtime, CO₂ purity requirements, and availability of transport and storage infrastructure. Chemicals that reduce energy use, corrosion, foaming, and degradation can improve project economics because they lower operating cost over the full plant life. This makes performance-based supply contracts more attractive than simple commodity chemical sales.

Public funding and tax incentives are improving project bankability. In the U.S., the Carbon Capture Demonstration Projects Program includes a USD 1.3 billion point-source carbon capture funding opportunity issued in December 2024, along with earlier funding for demonstration and FEED studies. The 45Q incentive also supports project economics, with USD 85 per ton for point-source capture and USD 180 per ton for direct air capture in dedicated geologic storage.

Drivers Impact Analysis

The Carbon Capture Chemicals Market is driven by rising demand for carbon emission reduction, industrial decarbonization, power plant retrofits, blue hydrogen projects, refinery upgrades, cement production control, and chemical plant carbon management. These chemicals are used for CO₂ absorption, solvent regeneration, gas purification, corrosion control, and process stability.

North America leads the market due to strong carbon capture project development, industrial emission reduction programs, hydrogen investments, and policy support for carbon management infrastructure. The U.S. remains the main regional contributor because of large refining, power, natural gas, cement, and chemical processing activity.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising industrial decarbonization demand | +7.2% | North America, Europe, Asia Pacific | Drives core market growth. |

Expansion of carbon capture projects | +6.5% | U.S., Canada, Europe, China | Supports chemical consumption. |

Growth in blue hydrogen production | +5.4% | North America, Middle East, Europe | Adds high-value demand. |

CO₂ reduction targets in heavy industry | +4.8% | Cement, steel, refining, chemicals | Builds long-term use. |

Policy incentives for carbon management | +4.1% | U.S., Canada, Europe | Improves project economics. |

Restraints Impact Analysis

The market faces restraints from high capture cost, energy penalty, solvent degradation, and complex plant integration. Carbon capture systems require reliable chemicals, regeneration energy, corrosion control, and continuous monitoring, which can increase operating expenses.

Another restraint is slow commercial deployment in some industries. Many projects remain capital-intensive and depend on policy support, long-term offtake, carbon storage access, and proven capture performance before full-scale adoption becomes easier.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High capture and operating cost | -3.8% | Global project developers | Slows adoption. |

Energy penalty during solvent regeneration | -3.1% | Power and industrial plants | Raises efficiency burden. |

Solvent degradation and replacement needs | -2.6% | Chemical absorption systems | Increases recurring cost. |

Complex retrofit integration | -2.2% | Existing industrial plants | Delays project execution. |

Storage and transport infrastructure gaps | -1.9% | Emerging carbon capture regions | Limits deployment scale. |

Opportunities Impact Analysis

Opportunities are strong in amine-based solvents, advanced absorbents, corrosion inhibitors, CO₂ separation chemicals, solvent reclaiming systems, and low-energy capture formulations. These areas benefit from demand for better capture efficiency and lower lifecycle cost.

Higher-value opportunities are also emerging in direct air capture, bioenergy with carbon capture, blue hydrogen, and carbon capture for cement and steel plants. Companies that improve solvent stability, regeneration efficiency, and corrosion protection can capture strong long-term value.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Advanced amine solvent development | +6.8% | North America, Europe, Asia Pacific | Builds core chemical demand. |

Direct air capture chemical systems | +5.9% | U.S., Canada, Europe, Japan | Creates future growth. |

Blue hydrogen capture applications | +5.0% | North America, Middle East, Europe | Adds industrial demand. |

Cement and steel carbon capture | +4.4% | Europe, U.S., China, India | Expands heavy industry use. |

Solvent reclaiming and recycling | +3.6% | Large capture facilities | Reduces operating cost. |

Challenges Impact Analysis

The main challenge is improving CO₂ capture efficiency while reducing energy use. Chemical absorption systems must capture carbon reliably, regenerate quickly, and maintain low degradation under industrial gas conditions.

Another challenge is handling impurities in flue gas and process gas streams. Sulfur oxides, nitrogen oxides, oxygen, particulates, and moisture can reduce solvent life, increase corrosion, and raise maintenance needs.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Reducing solvent regeneration energy | -3.5% | Chemical absorption plants | Affects operating economics. |

Managing flue gas impurities | -2.9% | Power, cement, refining sectors | Reduces solvent life. |

Controlling corrosion in capture systems | -2.4% | Industrial capture units | Raises maintenance cost. |

Scaling from pilot to commercial plants | -2.1% | Global carbon capture projects | Adds execution risk. |

Meeting long-term performance guarantees | -1.7% | Project developers and operators | Affects financing confidence. |

Segment Covered in the Report

By Chemical Type

Amines

Carbonates

Ionic Liquids

Solid Sorbent Chemicals

Others

By Absorption Type

Chemical Absorption

Physical Absorption

By End-Use Industry

Oil and Gas

Chemical and Petrochemical

Cement

Iron and Steel

Others

By Application

Post-combustion Capture

Pre-combustion Capture

Industrial Gas Separation

Direct Air Capture

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward amines, advanced solvents, solid sorbents, chemical absorption systems, post-combustion capture, and direct air capture chemicals. Amines remain important because they are widely used for CO₂ absorption in industrial and gas treatment applications.

Newer capture chemicals are gaining attention because operators need lower energy use, better stability, reduced corrosion, and lower solvent loss. North America remains the value leader, while Europe and Asia Pacific are increasing demand through industrial decarbonization and carbon neutrality plans.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Amine-based solvents remain key | +6.4% | Global capture facilities | Leads chemical absorption use. |

Post-combustion capture adoption rises | +5.5% | Power, cement, refining sectors | Supports broad deployment. |

Advanced solvent formulations grow | +4.8% | North America, Europe, Japan | Improves efficiency. |

Solid sorbent development gains traction | +4.0% | Direct air capture and gas treatment | Adds technology diversity. |

Direct air capture trend expands | +3.5% | U.S., Canada, Europe | Supports future demand. |

Investor Type Impact Matrix

Investors should focus on carbon capture chemical producers with strong solvent technology, project partnerships, industrial customer access, and proven performance in large-scale capture systems. Chemical stability, low regeneration energy, and corrosion control are key value drivers.

Strategic investors can also target direct air capture chemical platforms, advanced absorbents, solvent management services, and carbon capture integration suppliers. Companies that lower capture cost while improving reliability are better positioned for long-term growth.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Carbon Capture Chemical Producers | +6.0% | Global | Expands capture chemical supply. |

Advanced Solvent Developers | +5.2% | North America, Europe, Asia Pacific | Improves capture efficiency. |

Oil, Gas and Industrial Suppliers | +4.3% | North America, Middle East, Europe | Drives project demand. |

Direct Air Capture Technology Companies | +3.7% | U.S., Canada, Europe, Japan | Builds future market value. |

Strategic and Climate Infrastructure Investors | +3.1% | Global carbon management hubs | Funds commercial deployment. |

Recent Developments

In March 2026, Svante acquired Carbon Alpha and related subsidiaries to expand its commercial-scale carbon removal and CCS project development business in Western Canada. The deal added the North Star BECCS project, CO₂ storage expertise, regional pipeline capability, and a geological storage hub asset. This acquisition strengthens the connection between capture materials, project ownership, and verified carbon removal credits.

In February 2026, Terradot agreed to acquire assets of Eion, a U.S. based enhanced rock weathering company. The deal added Eion’s intellectual property, project footprint, operating capabilities, contracts, and technical team. Although this is more aligned with carbon removal materials than amine solvents, it shows that carbon capture and removal platforms are consolidating around stronger measurement, verification, and delivery capacity.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Market Concentration: Medium

The Carbon Capture Chemicals Market shows medium concentration because established chemical companies have advantages in solvent manufacturing, process chemistry, bulk supply, safety documentation, and industrial customer access. However, the market is not highly concentrated because many technology developers, specialty chemical firms, sorbent producers, membrane developers, and direct air capture companies are entering with differentiated capture media.

Medium concentration is supported by the expanding CCS project base. The Global CCS Institute reported that operational CCS projects increased 54% year-on-year, rising from 50 to 77 in 2025. It also reported 47 projects in construction with 44 Mtpa of cumulative capture capacity and 610 projects in various development stages. This creates room for both large suppliers and specialized innovators, especially in advanced solvents, solid sorbents, and DAC chemicals.

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Shell

ExxonMobil

Equinor

Chevron

China National Petroleum Corporation

TotalEnergies

Linde

TechnipFMC

Saudi Aramco

Gazprom

BASF SE

Mitsubishi Heavy Industries

Aker Carbon Capture

Fluor Corporation

Carbon Clean

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Bio-based Chemicals Market Size to Hit USD 296.7 Bn by 2035

Bio-based Chemicals Market By Product Category (Platform Chemicals, Polymers for Plastics, Paints, Coatings, Inks and Dyes, Surfactants, Cosmetics and Personal Care Products, Adhesives, Man-made Fibers, Others), By Application (Industrial, Agricultural, Pharmaceutical, Others), By Source (Plant-based, Animal-based, Microbial-based, Waste-based), By End Use (Chemical Manufacturing, Agriculture, Food and Beverage, Personal Care, Pharmaceuticals, Automotive), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Processing Chemicals Market Size to Hit USD 14.6 Billion by 2035

Hydrogen Processing Chemicals Market By Chemical Type (Catalysts, Adsorbents, Solvents, Corrosion Inhibitors, Scavengers, Others), By Function (Reforming Chemicals, Purification Chemicals, Hydroprocessing Chemicals, Gas Treatment Chemicals, Corrosion Control Chemicals, Others), By Process (Steam Methane Reforming, Hydrocracking, Hydrotreating, Pressure Swing Adsorption, Water-Gas Shift Reaction, Others), By End Use (Refineries, Ammonia Production, Methanol Production, Petrochemicals, Clean Hydrogen Plants, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Electrolyte Chemicals Market to Cross USD 49.4 Billion by 2035

Electrolyte Chemicals Market By Battery Type (Lithium-ion Electrolytes, Lead-acid Electrolytes, Flow Battery Electrolytes, Others), By Electrolyte Form (Liquid Electrolytes, Gel, Solid-State Electrolytes), By Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, Industrial and Motive Batteries, Others), By Product Type (Lithium-Based Electrolytes, Sulfide-Based Electrolytes, Polymer-Based Electrolytes, Oxide-Based Electrolytes, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Nickel Chemicals Market to Cross USD 19.1 Billion by 2035

Nickel Chemicals Market By Product Type (Nickel Sulfate, Nickel Hydroxide, Nickel Chloride, Nickel Nitrate, Nickel Carbonate, Nickel Acetate, Others), By Grade (Battery Grade, Plating Grade, Industrial Grade, High-Purity Grade, Others), By Form (Powder, Crystal, Solution, Granules, Others), By Application (Batteries, Electroplating, Catalysts, Ceramics and Pigments, Chemical Intermediates, Others), By End Use (Automotive, Electronics, Chemicals, Aerospace, Industrial Manufacturing, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035