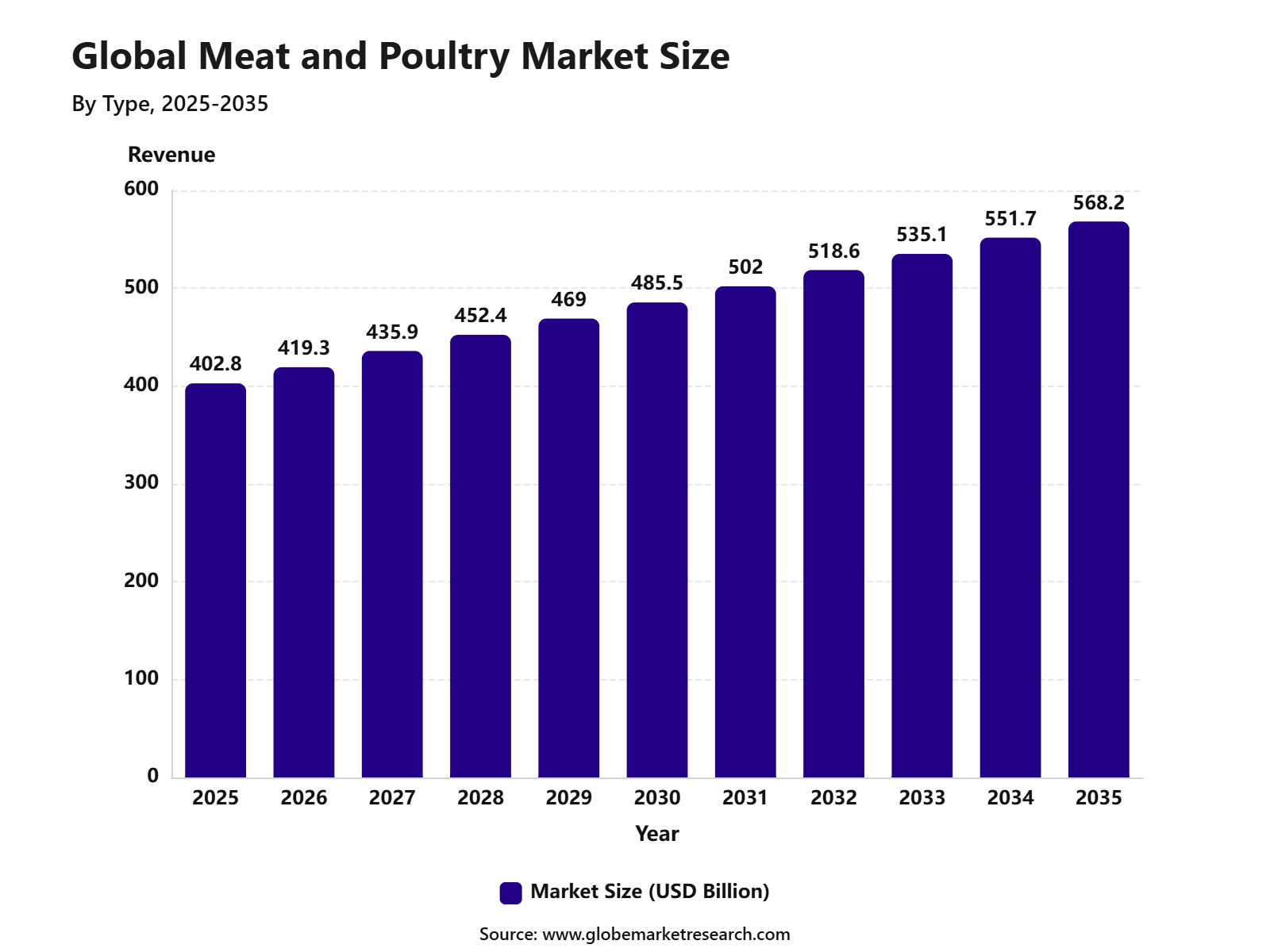

Revenue, 2025

$ 402.8 Bn

Forecast, 2035

$ 568.2 Bn

CAGR, 2025-2035

3.5%

Report Coverage

Global

Market Size and Forecast

The Global Meat and Poultry Market was valued at USD 402.8 billion in 2025 and is projected to reach USD 568.2 billion by 2035, growing at a CAGR of 3.5% from 2025 to 2035. The growth of the market can be attributed to rising protein consumption, population growth, increasing demand for processed meat products, and wider availability of chilled and frozen meat across retail and foodservice channels. Demand is also supported by changing food habits, urbanization, and the expansion of quick-service restaurants and ready-to-cook meal formats.

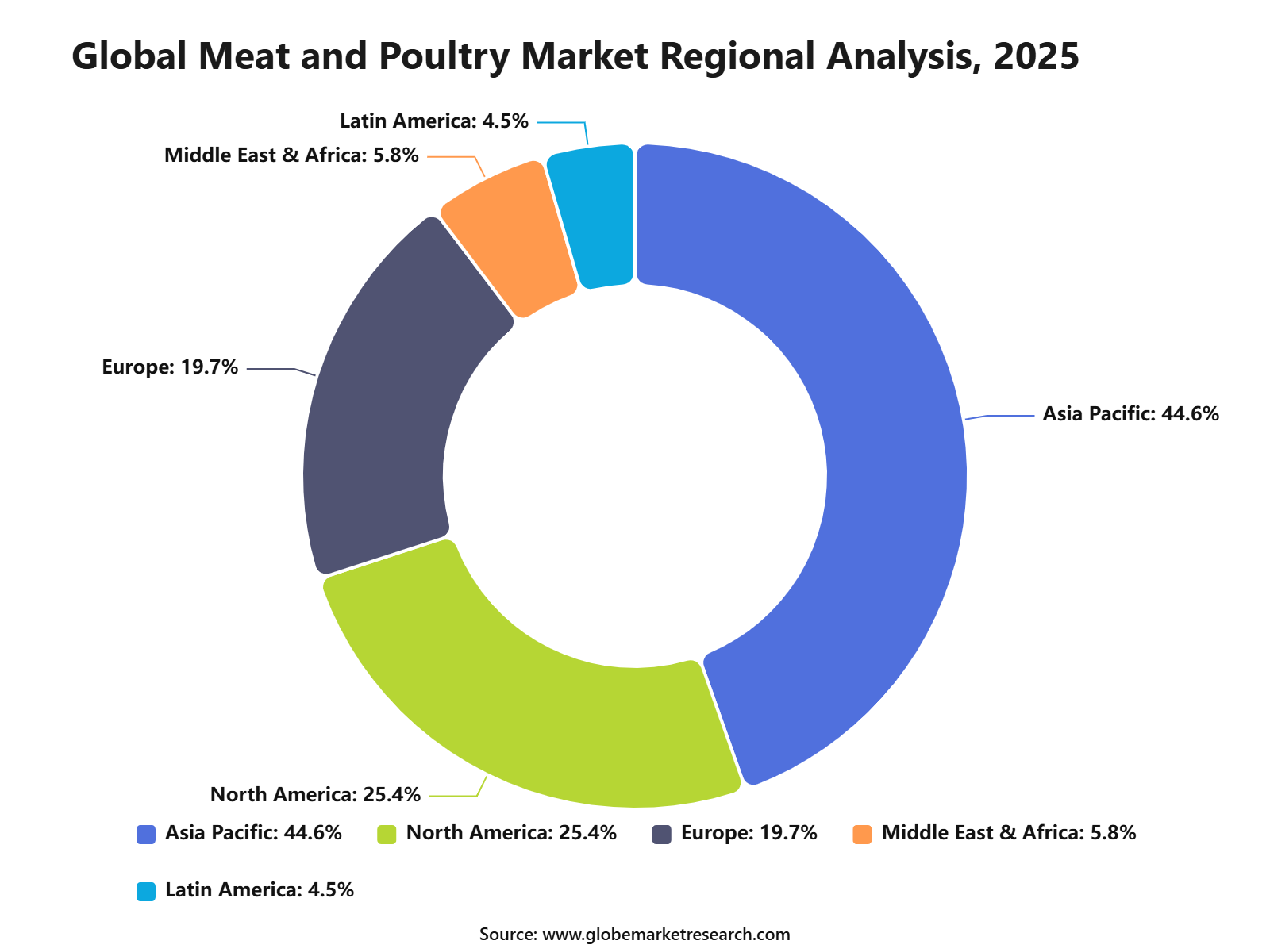

Asia Pacific held the largest regional share of 44.6% in 2025, valued at approximately USD 179.6 billion. The region’s dominance can be linked to its large population base, rising disposable income, strong poultry consumption, and growing demand for affordable animal protein across China, India, Japan, South Korea, and Southeast Asian countries. Market growth is further supported by expanding cold chain infrastructure, organized meat retail, and increasing investment in poultry processing and meat packaging facilities.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Unflavoured white meat and poultry led the type segment with 74.5% share, supported by high consumer preference for fresh, versatile, and protein-rich meat products used in daily meals.

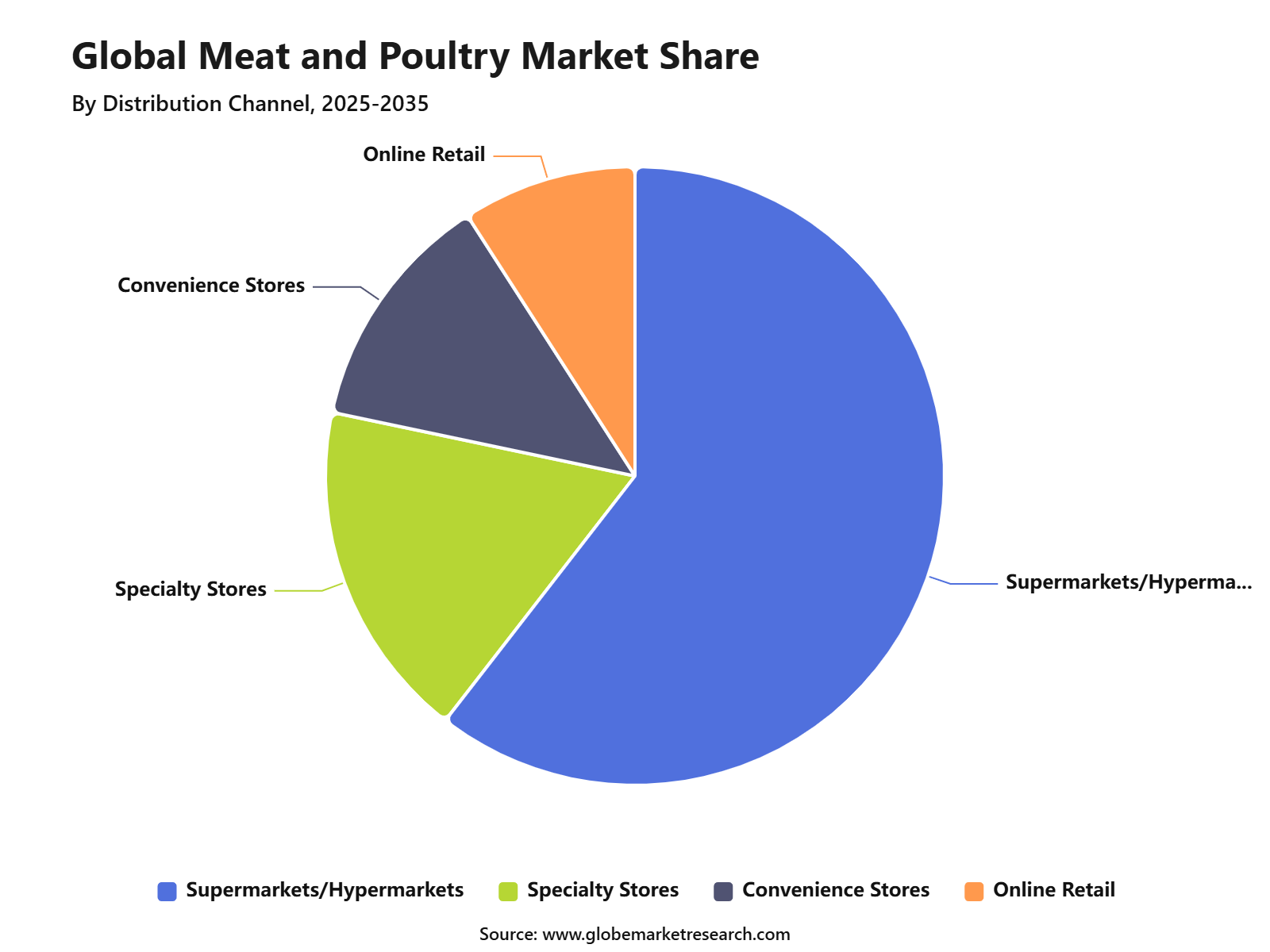

Supermarkets and hypermarkets accounted for 60.5% share by distribution channel, driven by wide product availability, organized cold-chain storage, competitive pricing, and strong consumer footfall.

Asia Pacific held 44.6% share of the meat and poultry market, supported by large population, rising protein consumption, growing urban retail networks, and strong demand for affordable poultry products.

Go-to-Market and Sales Economics

The Meat and Poultry Market needs a protein-type-led and channel-led go-to-market strategy. Suppliers should position beef, pork, chicken, turkey, lamb, processed meat, fresh meat, frozen meat, ready-to-cook products, and value-added cuts based on price, convenience, taste, nutrition, food safety, and cooking occasion. Poultry remains the strongest affordability-led protein in many markets, as USDA forecast global chicken meat production to rise by nearly 3% in 2026 to 110.7 million tons, supported by expansion in China and Brazil.

Sales economics are strongest when producers combine scale, cold-chain control, feed-cost management, slaughter efficiency, brand trust, and retail distribution. Beef pricing remains more pressured than poultry because U.S. cattle supplies are tight, while USDA ERS reported that beef and veal prices were 14.8% higher in April 2026 than in April 2025 and are predicted to rise 12.1% in 2026. Poultry prices were only 0.5% higher year-on-year in April 2026 and are predicted to increase 0.5% in 2026, which supports poultry’s value positioning for households and foodservice buyers.

Risk Factors & Market Barriers

The main risk factor is animal disease. Highly pathogenic avian influenza remains a continuing poultry-sector risk because it can reduce flock availability, disrupt exports, and raise operating costs. USDA APHIS states that HPAI can wipe out entire domestic poultry flocks within days, and detections tend to increase in fall and spring due to wild bird migration. APHIS also noted that the U.S. processed more than 9.4 billion broiler chickens and 218 million turkeys in 2023, showing the scale of potential exposure when disease pressure rises.

Beef supply tightness is another major barrier. USDA FAS forecast global beef production to decline 1% in 2026 to 61.6 million tons, with lower production in Brazil, the United States, China, the European Union, and Australia more than offsetting gains in India, Mexico, and New Zealand. For the U.S., USDA stated that constrained steer and heifer availability, plus restrictions on cattle imports from Mexico, are expected to lower beef production and exports.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape is spread across fresh meat, frozen meat, poultry, beef, pork, lamb, turkey, sausages, deli meats, marinated cuts, ready-to-cook products, foodservice supply, retail packs, private label, quick-service restaurants, hotels, institutional catering, and export channels. Chicken remains the most scalable volume opportunity because it has shorter production cycles, better feed conversion, and stronger price accessibility than beef. USDA forecast U.S. chicken meat production to rise 2% in 2026 to 22.2 million tons, supported by heavier weights, positive margins, and firm domestic demand.

Pork remains important where affordability and processed meat demand are strong. USDA forecast global pork production to rise 1% in 2026 to 120.2 million tons, with higher output in the United States, Brazil, China, and Canada offsetting lower EU production. U.S. pork production is forecast to reach 12.7 million tons in 2026, while U.S. exports are expected to rise 3% due to demand in Mexico and Asia.

Financial Impact

The financial impact can be positive for companies with efficient feed sourcing, integrated farming, modern processing plants, strong cold chains, disease control, and diversified sales channels. Poultry processors are better placed when feed costs are stable and consumer demand shifts toward affordable proteins. Beef processors may benefit from high prices, but tight cattle availability can reduce slaughter volumes, raise procurement costs, and pressure plant utilization. USDA ERS reported farm-level cattle prices were 17.7% higher in April 2026 than in April 2025, while wholesale beef prices were 14.2% higher year-on-year.

Financial risk remains linked to feed costs, animal disease, labor, energy, cold-chain logistics, export restrictions, tariffs, food safety recalls, and cattle supply cycles. Large processors may improve resilience through value-added products, branded meat, private label contracts, automation, export diversification, and stronger biosecurity. The strongest financial position is expected for companies that balance beef, pork, and poultry exposure, because each protein reacts differently to price, feed cost, disease risk, and consumer affordability.

Type Analysis

Unflavoured white meat and poultry led the Meat and Poultry Market with 74.5% share, supported by strong demand for chicken, turkey, and other poultry products in fresh, chilled, and frozen formats. This segment is preferred because it is versatile, affordable, easy to cook, and widely accepted across different diets and cuisines. The growth of this segment can be attributed to rising consumer preference for lean protein and convenient meal preparation.

Poultry products are widely used in home cooking, restaurants, quick-service outlets, ready-to-cook products, frozen meals, and processed meat applications. Unflavoured white meat and poultry are expected to maintain their leading position because they offer flexibility for seasoning, processing, and value-added product development. Demand is likely to remain strong as consumers continue to seek protein-rich food options that are practical, accessible, and suitable for daily consumption.

Distribution Channel Analysis

Supermarkets and hypermarkets accounted for 60.5% share of the Meat and Poultry Market, supported by strong consumer preference for organized retail, product variety, quality assurance, and convenient shopping. These outlets offer fresh meat, frozen poultry, processed meat, ready-to-cook products, and packaged protein items under one roof.

The growth of this segment is being supported by cold-chain expansion, better in-store refrigeration, private-label meat products, and attractive promotional pricing. Consumers often prefer supermarkets and hypermarkets because they provide visible product quality, clear labeling, hygiene standards, and easy access to both branded and unbranded meat products.

Supermarkets and hypermarkets are expected to remain a leading channel as urban consumers continue to shift from traditional wet markets to organized retail formats. Demand will also be supported by packaged meat, frozen poultry, value packs, marinated products, and ready-to-cook options designed for busy households.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Analysis

Asia Pacific led the Meat and Poultry Market with 44.6% share, supported by a large population base, rising disposable income, expanding urban food demand, and strong poultry consumption across China, India, Japan, South Korea, and Southeast Asia. The region has a broad consumer base that supports high demand for fresh, frozen, processed, and ready-to-cook meat products. The growth of Asia Pacific is being supported by rapid expansion of modern retail, foodservice chains, cold-chain logistics, and packaged food distribution.

Poultry demand is especially strong because it is relatively affordable, widely available, and culturally acceptable across many countries in the region. Asia Pacific is expected to remain a key growth center as consumers shift toward protein-rich diets and convenient food products. Opportunities are likely to remain strong in frozen poultry, chilled meat, value-added products, ready-to-cook formats, supermarket retail, and foodservice supply chains.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +1.4% | Asia Pacific, 44.6% share in 2025 | Leads consumption volume. |

North America processed meat demand | +0.7% | U.S. and Canada | Supports value-added products. |

Europe premium and certified meat growth | +0.6% | Germany, UK, France, Italy | Drives quality-focused demand. |

Latin America poultry and beef supply strength | +0.5% | Brazil, Argentina, Mexico | Supports export growth. |

Middle East and Africa protein demand | +0.5% | GCC, South Africa, Nigeria | Builds steady consumption. |

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Poultry remains preferred protein | +0.8% | Asia Pacific, Latin America, Middle East | Drives affordable consumption. |

Growth of unflavoured white meat and poultry | +0.7% | Global | Supports staple demand. |

Expansion of packaged meat products | +0.6% | North America, Europe, Asia Pacific | Improves retail sales. |

Rising demand for antibiotic-free meat | +0.5% | U.S., Europe, developed Asia | Supports premium positioning. |

Growth in online meat delivery | +0.4% | Urban Asia Pacific, U.S., Europe | Improves consumer access. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Meat and Poultry Producers | +0.8% | Global | Expands processing capacity. |

Food Processing Companies | +0.7% | Asia Pacific, North America, Europe | Builds value-added products. |

Cold-Chain Logistics Investors | +0.6% | Emerging and export markets | Supports fresh delivery. |

Private Equity Firms | +0.5% | Global | Enables business scaling. |

Retail and Foodservice Companies | +0.5% | Global | Drives direct demand. |

Segment Covered in the Report

By Type

Flavoured Meat and Poultry

Unflavoured White Meat and Poultry

By Distribution Channel

Supermarkets/Hypermarkets

Specialty Stores

Convenience Stores

Online Retail

By Region

Asia Pacific

North America

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising protein consumption | +0.9% | Asia Pacific, North America, Middle East | Drives meat demand. |

Growth in poultry consumption | +0.8% | Asia Pacific, Latin America, Africa | Supports volume growth. |

Expansion of organized retail | +0.6% | Global urban markets | Improves product access. |

Increasing demand for processed meat products | +0.5% | North America, Europe, Asia Pacific | Supports value-added sales. |

Growth in foodservice and quick-service restaurants | +0.4% | Asia Pacific, U.S., GCC, Europe | Increases bulk demand. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Health concerns over processed meat | -0.6% | North America, Europe, urban Asia | Limits frequent consumption. |

Feed cost volatility | -0.5% | Global producers | Pressures margins. |

Animal disease outbreaks | -0.4% | Asia Pacific, Europe, Americas | Disrupts supply. |

Environmental and emission concerns | -0.4% | Europe, North America | Raises regulatory pressure. |

Cold-chain infrastructure gaps | -0.3% | Emerging markets | Limits distribution quality. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in frozen and chilled meat | +0.7% | Asia Pacific, Europe, North America | Improves shelf life. |

Expansion of ready-to-cook products | +0.6% | Urban global markets | Supports convenience demand. |

Demand for high-quality poultry products | +0.6% | Asia Pacific, Middle East, Africa | Drives affordable protein use. |

Growth in halal and certified meat | +0.5% | Middle East, Asia Pacific, Europe | Expands consumer reach. |

Modernization of processing facilities | +0.4% | Global | Improves supply efficiency. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining food safety standards | -0.5% | Global | Requires strict controls. |

Managing livestock disease risk | -0.4% | Asia Pacific, Europe, Americas | Affects supply stability. |

Price pressure in mass retail | -0.4% | Global | Reduces margin strength. |

Sustainability pressure on producers | -0.3% | Europe, North America, developed Asia | Raises operating burden. |

Supply chain and cold storage risk | -0.3% | Emerging markets | Impacts product freshness. |

Recent Developments

June 2026, Pilgrim’s Pride announced a USD 75 million investment to expand and modernize its poultry facility in Ellijay, Georgia. The company also planned to close harvesting operations at its Chattanooga, Tennessee plant as production shifts toward higher-value boneless chicken products. This shows that poultry processors are investing in value-added formats instead of only commodity chicken capacity.

June 2026, JBS USA announced closures affecting beef operations in Souderton, Pennsylvania and Memphis, Tennessee. The Souderton closure was reported to affect about 1,500 workers, while the Memphis facility involved around 200 employees. The move reflects industry consolidation as processors adjust to limited cattle supply, higher operating costs, and underused beef capacity.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 402.8 Billion |

Forecast Revenue (2035) | USD 568.2 Billion |

CAGR (2025-2035) | 3.5% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Type (Flavoured Meat and Poultry, Unflavoured White Meat and Poultry), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, Online Retail) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Tyson Foods, Inc., JBS S.A., Cargill, Incorporated, BRF S.A., WH Group Limited, Pilgrim’s Pride Corporation, Perdue Farms Inc., Hormel Foods Corporation, Sanderson Farms, Marfrig Global Foods S.A. , Other Key Players |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Tyson Foods, Inc.

JBS S.A.

Cargill, Incorporated

BRF S.A.

WH Group Limited

Pilgrim’s Pride Corporation

Perdue Farms Inc.

Hormel Foods Corporation

Sanderson Farms

Marfrig Global Foods S.A.

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Food and Beverages

Snack Food Market Size to hit USD 1,157.5 Bn by 2035

Global Snack Food Market Size, Share Analysis By Product Type (Chips and Crisps, Nuts and Seeds, Biscuits and Cookies, Popcorn, Meat Snacks, Others), By Category (Conventional Snacks, Healthy Snacks), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online, Specialty Stores, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Canned Food Market Size to Exceed USD 233.8 Billion by 2035

Global Canned Food Market Size, Share Analysis By Product Type (Canned Seafood, Canned Meat, Canned Fruits and Vegetables, Canned Ready Meals, Others), By Type (Conventional, Organic), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Frozen Food Market Size to Exceed USD 596.6 Billion by 2035

Global Frozen Food Market Size, Share Analysis By Product (Frozen Desserts, Frozen Meals, Meat/Poultry/Seafood, Fruits and Vegetables, Snacks, Baked Goods), By Freezing Technology (Blast Freezing, Belt Freezing, Individual Quick Freezing, Others), By Distribution Channel (Foodservice, Retail), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Ready-to-Eat Food Market to Exceed USD 846.5 Billion by 2035

Global Ready-to-Eat Food Market Size, Share Analysis By Product Type (Meat/Poultry, Vegetarian, Cereal-Based, Others), By Packaging (Frozen/Chilled, Canned, Retort, Others), By Distribution Channel (Hypermarkets, Convenience Stores, Online, Others), By End User (Residential, Foodservice, Institutional), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035