Revenue, 2025

$ 690.6 Bn

Forecast, 2035

$ 1,157.5 Bn

CAGR, 2025-2035

5.3%

Report Coverage

Global

Market Size and Forecast

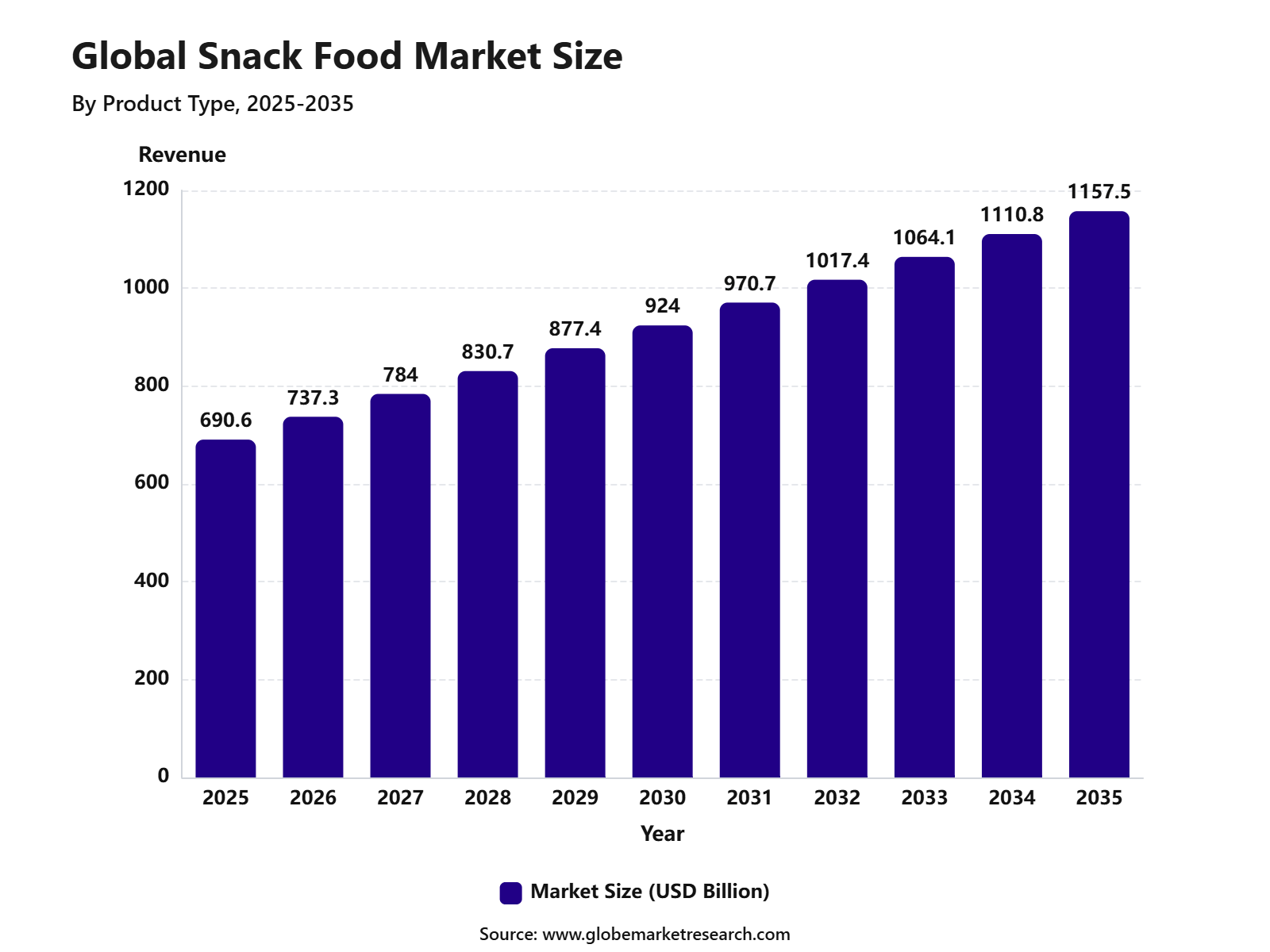

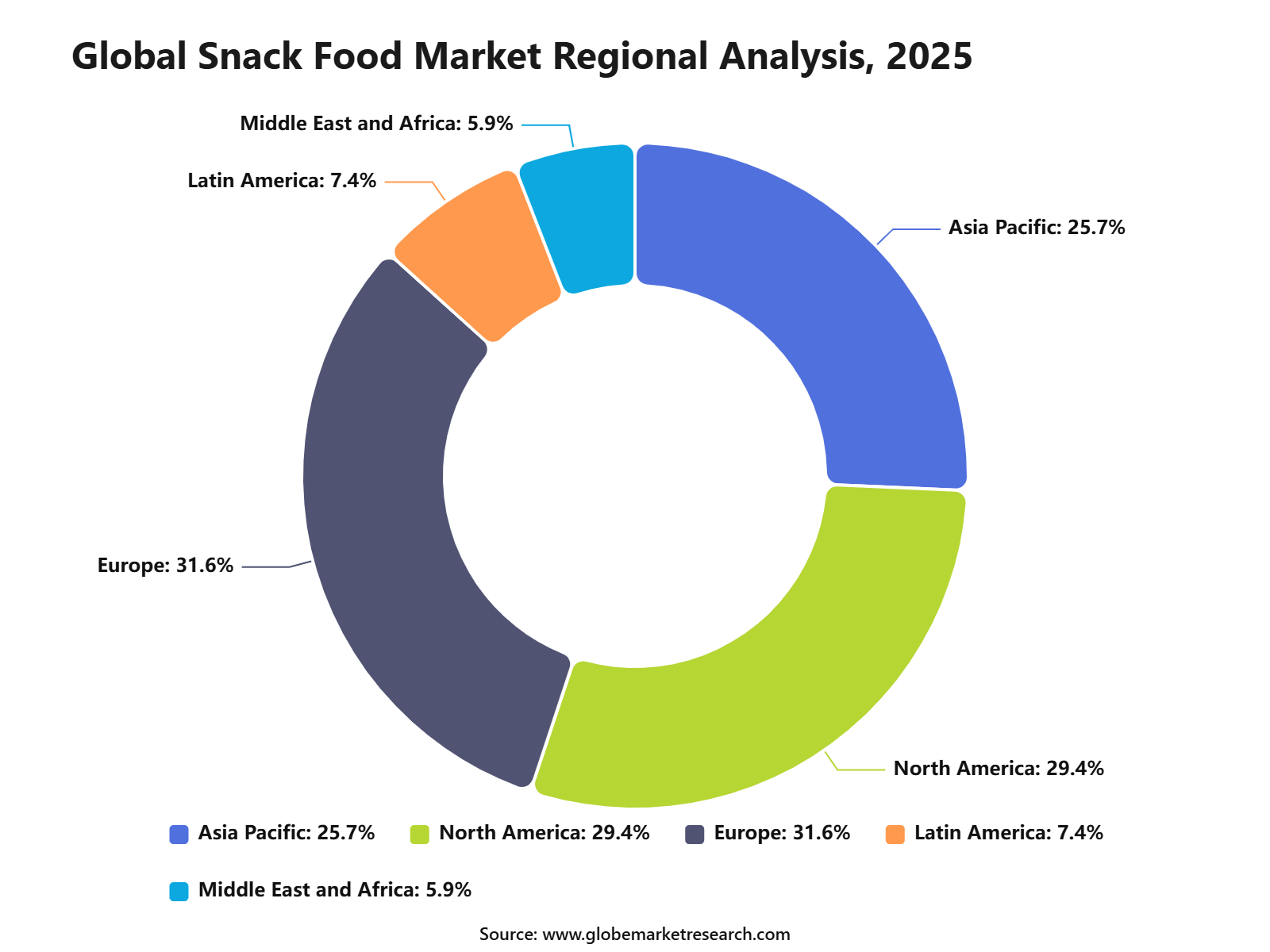

The Global Snack Food Market reached USD 690.6 billion in 2025 and is expected to grow to USD 1,157.5 billion by 2035, registering a CAGR of 5.3% from 2025 to 2035. Europe held the largest regional share of 31.6% in 2025, supported by strong consumption of bakery snacks, savory snacks, confectionery, meat snacks, dairy-based snacks, nuts, seeds, and convenience food products.

The Snack Food Market includes packaged and ready-to-eat food products consumed between regular meals. These products are widely sold through supermarkets, hypermarkets, convenience stores, specialty stores, online grocery platforms, vending machines, and foodservice channels. Demand is increasing as consumers prefer convenient, portion-controlled, tasty, and easy-to-carry food options.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market growth can be attributed to changing eating habits, rising urban lifestyles, growth in on-the-go consumption, and increasing demand for healthier snack alternatives. Europe continues to lead the market due to strong packaged food penetration, high demand for premium snacks, and growing consumer interest in clean-label, organic, low-sugar, and protein-rich snack products. Product innovation, attractive packaging, and expansion of online retail channels are expected to further support market growth.

Key Market Insights

Chips and crisps led the product type segment with 30.5% share, supported by strong consumer demand for ready-to-eat, savory, and convenient snack options.

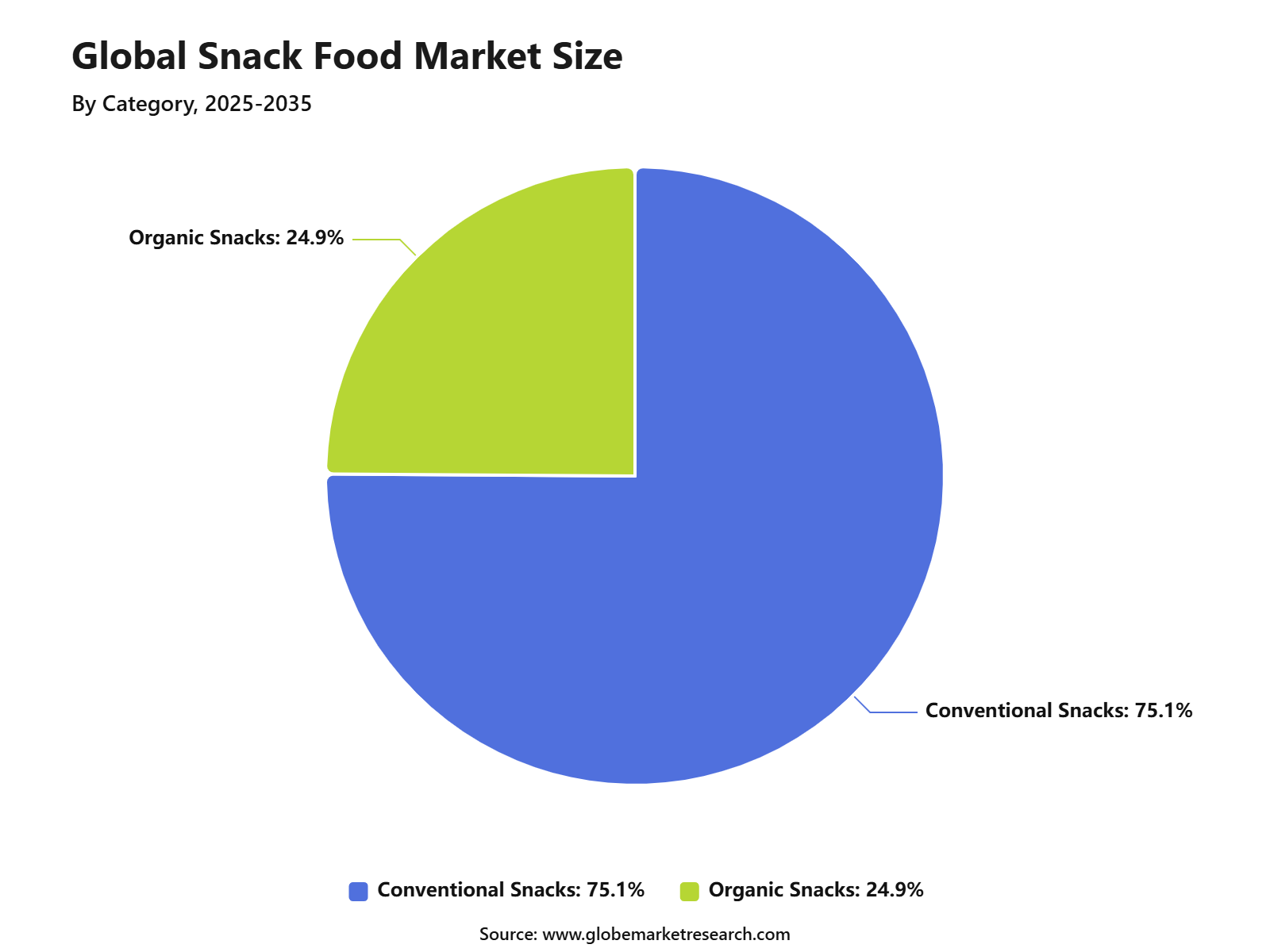

Conventional snacks accounted for 75.1% share by category, driven by broad availability, affordable pricing, familiar taste profiles, and high household consumption.

Supermarkets and hypermarkets held 44.5% share by distribution channel, supported by wide product variety, promotional offers, strong shelf visibility, and high consumer footfall.

Europe led the snack food market with 31.6% share, supported by mature retail networks, strong packaged snack consumption, and rising demand for convenient food products.

Go-To-Market-Strategy

The Snack Food Market should be positioned through an affordability, convenience, and innovation-led strategy in 2026, as consumers continue to buy snacks but are more selective about price, pack size, and nutrition. BLS reported that U.S. food-at-home prices rose 2.7% year over year in May 2026, while food-away-from-home prices rose 3.5%, supporting demand for lower-cost snack options consumed at home, at work, and during travel. Snack brands should therefore focus on single-serve packs, family-value packs, multipacks, and channel-specific pricing across supermarkets, convenience stores, online grocery, quick-commerce, vending, and foodservice outlets.

Product strategy should be built around chips, crisps, popcorn, nuts, biscuits, bars, crackers, extruded snacks, fruit snacks, protein snacks, and indulgent confectionery-linked snacks. The 2026 Sweets and Snacks Expo included more than 1,000 food brands, showing strong innovation in textures, pickle flavors, functional ingredients, coffee-inspired snacks, caffeine formats, matcha, ube, and limited-edition launches. This indicates that shelf visibility, seasonal launches, taste variety, and social-media-friendly product formats will remain important for customer acquisition.

Risk Factors & Market Barriers

The main risk in the Snack Food Market is rising input cost pressure across grains, edible oils, sugar, cocoa, dairy, packaging, labor, and fuel. FAO reported that the Food Price Index averaged 130.8 points in May 2026, while the Cereal Price Index rose 2.6% from April and 4.9% year over year. Higher wheat, maize, rice, and oilseed-linked costs can directly affect chips, crackers, biscuits, bars, popcorn, baked snacks, and extruded snacks, reducing margin flexibility for manufacturers.

Health regulation and labeling pressure are also important barriers for snack producers in 2026. The FDA proposed front-of-package nutrition labeling for most packaged foods, with simplified information on saturated fat, sodium, and added sugars shown as "Low" "Med" or "High". This creates a clear compliance and reformulation challenge for salty snacks, sweet snacks, cookies, candy, and fried products, as brands may need to reduce sodium, sugar, artificial ingredients, and saturated fat while still protecting taste and texture.

Revenue Potential Analysis

Revenue Landscape Across

Revenue opportunities across the Snack Food Market are spread across savory snacks, sweet snacks, bakery snacks, frozen snacks, protein snacks, fruit snacks, nuts, seeds, and better-for-you formats. Savory snacks remain highly attractive because they support frequent consumption, strong impulse sales, and wide flavor innovation across chips, popcorn, pretzels, crackers, and extruded products. SNAC International’s 2026 State of the Industry Report also highlighted that private-label snack sales increased 15.0%, showing that affordability and retailer-owned products are becoming stronger revenue drivers.

Across channels, supermarkets and hypermarkets remain central due to shelf space, promotions, and multipack sales, while convenience stores, vending, e-commerce, and quick-commerce support impulse and repeat demand. Revenue can be strengthened through premium flavors, local taste profiles, healthier ingredients, resealable packs, portion-controlled packs, and seasonal product drops. Functional snacks are gaining attention as products with protein, probiotics, collagen, biotin, vitamin E, and caffeine move into popcorn, candy, bars, and mixed snack formats.

Financial Impact

The financial impact of the Snack Food Market in 2026 will depend on pricing discipline, commodity sourcing, packaging costs, and promotional planning. BLS data shows that cereals and bakery product prices rose 1.9% year over year in May 2026, while nonalcoholic beverages rose 5.8% and fruits and vegetables rose 6.1%, which can affect snack categories using flour, fruit ingredients, sweeteners, oils, and beverage-paired impulse formats. This makes cost control and product mix management important for protecting margins.

Snack companies can improve profitability through automation, local sourcing, high-speed packaging lines, optimized pack sizes, and stronger private-label partnerships. Premium snacks, high-protein products, clean-label items, global flavors, and limited-edition launches can support better unit economics, while value packs can protect volume among price-sensitive consumers. The market remains financially attractive, but stronger returns are expected for companies that balance affordability with taste, nutrition, compliance, and strong retail execution.

Product Type Analysis

Chips and crisps led the Snack Food Market with 30.5% share, supported by strong consumer preference for convenient, ready-to-eat, and flavor-rich snack products. These products are widely consumed across households, offices, schools, travel, entertainment venues, and social occasions because they are affordable, portable, and easy to share.

The growth of this segment can be attributed to continuous flavor innovation, attractive packaging, and strong availability across retail channels. Consumers are increasingly choosing chips and crisps in classic salted, cheese, barbecue, spicy, regional, and premium gourmet flavors, which supports repeat purchases.

Chips and crisps are expected to remain a leading product type as brands continue to launch healthier, baked, low-fat, reduced-salt, and premium variants. Demand will also be supported by portion-controlled packs, family-size packs, private-label products, and impulse purchases through supermarkets, hypermarkets, convenience stores, and online channels.

Category Analysis

Conventional snacks accounted for 75.1% share, making them the leading category in the Snack Food Market. This segment includes widely consumed snacks such as chips, crisps, extruded snacks, salted snacks, crackers, popcorn, pretzels, and other traditional packaged snack formats.

The dominance of conventional snacks can be linked to affordability, mass availability, strong brand familiarity, and regular consumption across different age groups. These products remain popular because they offer familiar taste, easy access, and broad suitability for daily snacking and social eating occasions.

Conventional snacks are expected to maintain a strong position due to their deep retail penetration and high purchase frequency. However, brands are also improving product appeal through better ingredients, lower sodium options, baked formats, clean-label claims, and new regional flavors to match changing consumer preferences.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFDistribution Channel Analysis

Supermarkets and hypermarkets held 44.5% share of the Snack Food Market, supported by high consumer footfall, wide shelf availability, and strong product visibility. These outlets offer chips, crisps, crackers, popcorn, cookies, snack bars, confectionery snacks, and private-label snack products under one roof.

The growth of this channel can be attributed to promotional pricing, bulk packs, seasonal displays, and strong in-store merchandising. Consumers often prefer supermarkets and hypermarkets because they can compare brands, pack sizes, prices, flavors, and nutritional labels before purchase.

Supermarkets and hypermarkets are expected to remain a key sales channel due to their strong role in routine grocery shopping. Demand will also be supported by private-label snacks, value packs, premium snack displays, festive promotions, and placement near checkout counters to encourage impulse buying.

Regional Analysis

Europe led the Snack Food Market with 31.6% share, supported by strong packaged food consumption, mature retail networks, high demand for savory snacks, and a well-developed food manufacturing base. The region has strong demand for chips, crisps, crackers, popcorn, bakery snacks, confectionery snacks, and premium snack products.

The growth of Europe can be attributed to changing snacking habits, busy lifestyles, and rising demand for convenient food products between meals. Consumers in the region are also showing interest in premium flavors, healthier snack options, plant-based snacks, and products with clearer ingredient labels.

Europe is expected to remain a leading regional market due to its strong food retail structure and continued snack innovation. Opportunities are likely to remain strong in healthier chips and crisps, baked snacks, reduced-salt products, private-label snacks, premium gourmet flavors, and sustainable snack packaging.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Europe market leadership | +1.6% | Europe, 31.6% share in 2025 | Leads snack demand. |

North America premium snack adoption | +1.1% | U.S. and Canada | Supports higher-value products. |

Asia Pacific volume growth | +1.2% | China, India, Japan, Southeast Asia | Drives future consumption. |

Latin America packaged snack expansion | +0.7% | Brazil, Mexico, Chile, Colombia | Builds steady demand. |

Middle East and Africa retail growth | +0.6% | GCC, South Africa, Egypt | Supports gradual adoption. |

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Chips and crisps category growth | +1.3% | Europe, North America, Asia Pacific | Leads product demand. |

Conventional snacks remain dominant | +1.1% | Global | Supports mass consumption. |

Supermarket and hypermarket channel strength | +1.0% | Europe, North America, Asia Pacific | Drives retail volume. |

Better-for-you snack adoption | +0.9% | Europe, U.S., developed Asia | Improves consumer appeal. |

Flavor innovation and regional tastes | +0.8% | Global | Expands repeat purchases. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Snack Food Manufacturers | +1.3% | Global | Expands product capacity. |

Food and Beverage Companies | +1.1% | Europe, North America, Asia Pacific | Builds category growth. |

Retail and Grocery Chains | +0.9% | Global | Strengthens shelf availability. |

Packaging Material Investors | +0.7% | Europe, North America, Asia Pacific | Supports sustainable formats. |

Private Equity Firms | +0.7% | Europe, North America, Asia Pacific | Enables brand scaling. |

Segment Covered in the Report

By Product Type

Chips and Crisps

Nuts and Seeds

Biscuits and Cookies

Popcorn

Meat Snacks

Others

By Category

Conventional Snacks

Healthy Snacks

By Distribution Channel

Supermarkets and Hypermarkets

Convenience Stores

Online

Specialty Stores

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for convenient snacking | +1.4% | Europe, North America, Asia Pacific | Drives daily consumption. |

Growth in chips and crisps consumption | +1.2% | Europe, North America, urban Asia | Supports core category sales. |

Increasing urban lifestyle and on-the-go eating | +1.0% | Global urban markets | Expands snack usage. |

Strong supermarket and hypermarket availability | +0.9% | Europe, Asia Pacific, North America | Improves retail access. |

Product innovation in flavors and formats | +0.8% | Global | Builds consumer interest. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Health concerns over salt, sugar, and fats | -0.8% | Europe, North America, urban Asia | Limits frequent consumption. |

Raw material price volatility | -0.6% | Global producers | Pressures margins. |

Strong competition from local brands | -0.5% | Global | Reduces pricing power. |

Regulatory pressure on nutrition labeling | -0.5% | Europe, U.S., Asia Pacific | Raises compliance cost. |

Consumer shift toward fresh foods | -0.4% | Developed markets | Slows some categories. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in healthier snack options | +1.3% | Europe, North America, Asia Pacific | Supports premium demand. |

Expansion of baked and low-fat snacks | +1.0% | U.S., Europe, Japan, urban Asia | Improves health positioning. |

Rising demand for premium and gourmet snacks | +0.9% | Europe, North America, Middle East | Builds higher-value sales. |

Online grocery and quick-commerce growth | +0.8% | Global urban markets | Expands consumer reach. |

Growth in private-label snack products | +0.7% | Europe, North America | Supports retail margins. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Managing ingredient cost inflation | -0.7% | Global | Affects profitability. |

Maintaining taste with healthier formulations | -0.6% | Europe, North America | Creates innovation pressure. |

Packaging sustainability pressure | -0.5% | Europe, North America | Raises packaging cost. |

Supply chain disruption risk | -0.5% | Global | Impacts product availability. |

Brand differentiation in crowded shelves | -0.4% | Mature markets | Limits consumer loyalty. |

Recent Developments

In 2026, Kellanova operated under Mars Snacking after the USD 36.0 billion acquisition closed in December 2025. The deal added Pringles, Cheez-It, and Pop-Tarts to a larger global snacking platform.

In 2026, Mondelez reported USD 10.10 billion in net revenue, above market expectations, supported by chocolates and biscuits. India sales grew 11.4%, while Europe sales increased 9% year-on-year.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 690.6 Billion |

Forecast Revenue (2035) | USD 1,157.5 Billion |

CAGR (2025-2035) | 5.3% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Product Type (Chips and Crisps, Nuts and Seeds, Biscuits and Cookies, Popcorn, Meat Snacks, Others), By Category (Conventional Snacks, Healthy Snacks), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online, Specialty Stores, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | PepsiCo, Inc., Mondelez International, Nestlé S.A., The Kellogg Company, General Mills, Inc., The Kraft Heinz Company, Conagra Brands, Inc., Calbee, Inc., ITC Limited, and Hormel Foods Corporation. |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Food and Beverages

Canned Food Market Size to Exceed USD 233.8 Billion by 2035

Global Canned Food Market Size, Share Analysis By Product Type (Canned Seafood, Canned Meat, Canned Fruits and Vegetables, Canned Ready Meals, Others), By Type (Conventional, Organic), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Frozen Food Market Size to Exceed USD 596.6 Billion by 2035

Global Frozen Food Market Size, Share Analysis By Product (Frozen Desserts, Frozen Meals, Meat/Poultry/Seafood, Fruits and Vegetables, Snacks, Baked Goods), By Freezing Technology (Blast Freezing, Belt Freezing, Individual Quick Freezing, Others), By Distribution Channel (Foodservice, Retail), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Ready-to-Eat Food Market to Exceed USD 846.5 Billion by 2035

Global Ready-to-Eat Food Market Size, Share Analysis By Product Type (Meat/Poultry, Vegetarian, Cereal-Based, Others), By Packaging (Frozen/Chilled, Canned, Retort, Others), By Distribution Channel (Hypermarkets, Convenience Stores, Online, Others), By End User (Residential, Foodservice, Institutional), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Cereals and Grains Market to Exceed USD 1,928.1 Billion by 2035

Global Cereals and Grains Market Size, Share Analysis By Product Type (Wheat, Rice, Maize, Barley, Oats, Sorghum, Others), By Application (Food and Beverage, Animal Feed, Biofuel, Industrial Use, Others), By Form (Whole Grain, Flour, Processed Grain, Others), By Distribution Channel (Direct Sales, Wholesalers and Distributors, Retail, Online), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035