Revenue, 2025

$ 326.9 Bn

Forecast, 2035

$ 596.6 Bn

CAGR, 2025-2035

6.2%

Report Coverage

Global

Market Size and Forecast

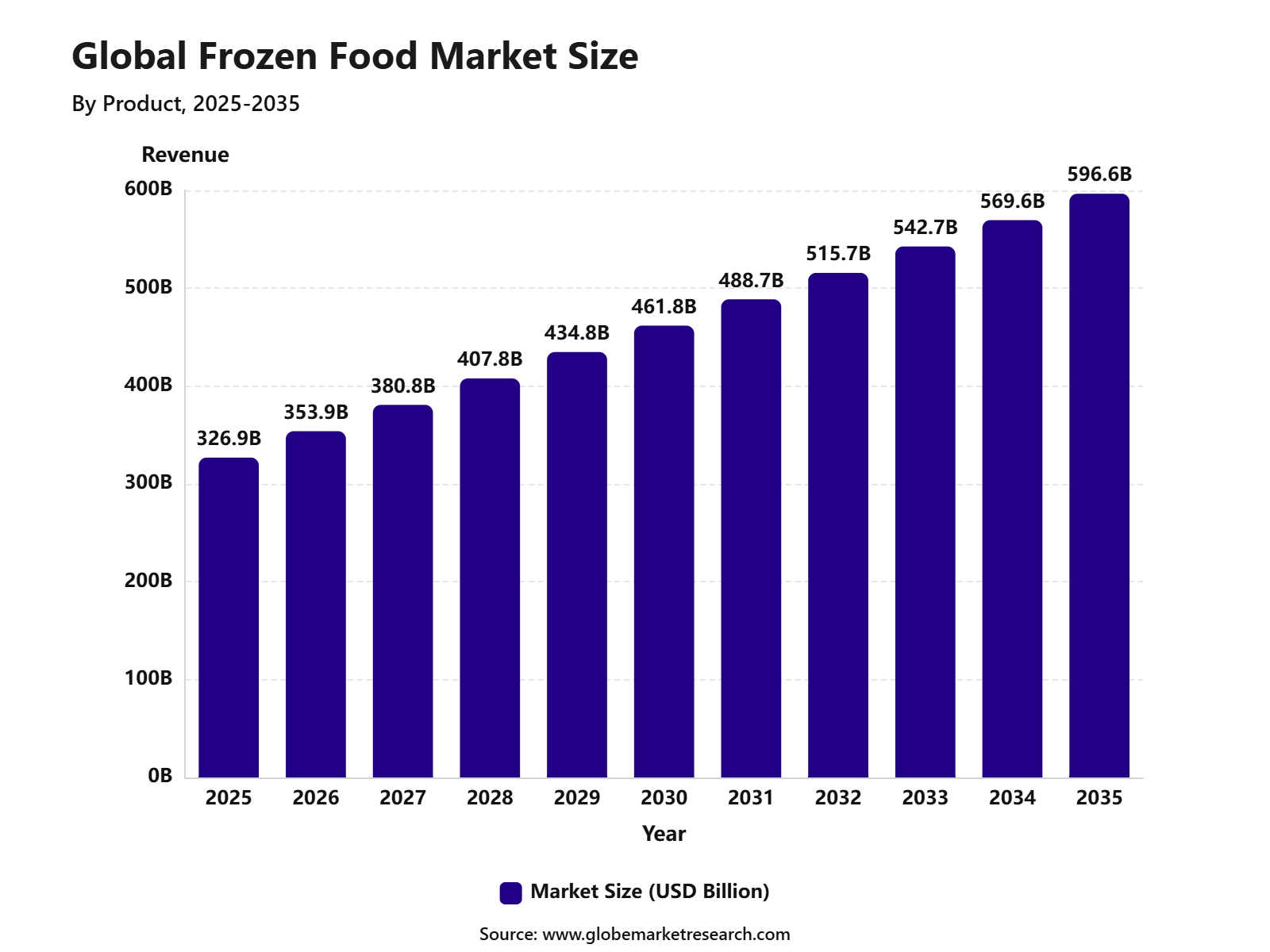

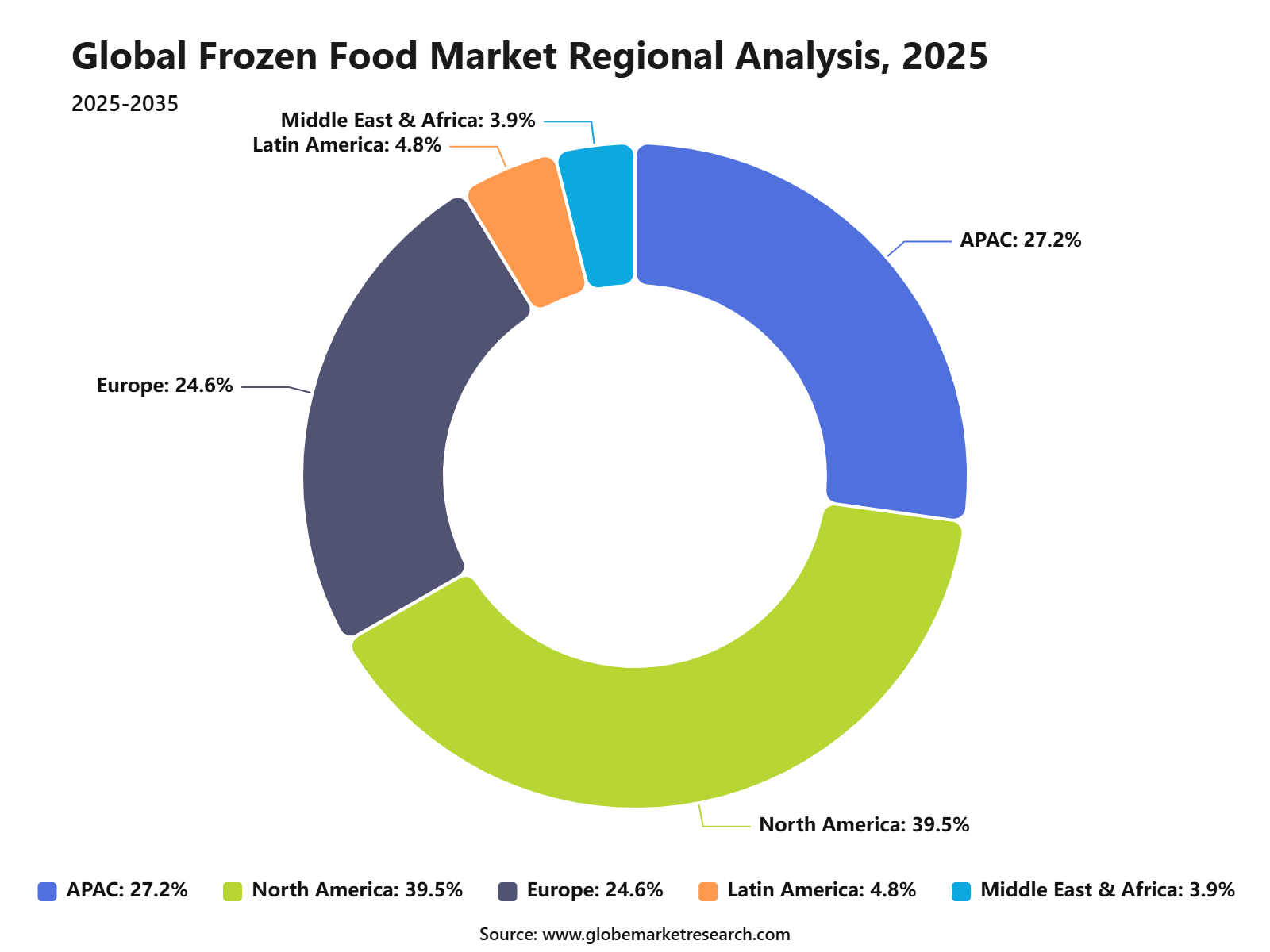

The Global Frozen Food Market reached USD 326.9 billion in 2025 and is expected to grow to USD 596.6 billion by 2035, registering a CAGR of 6.2% from 2025 to 2035. North America held the largest regional share of 39.5% in 2025, supported by high demand for convenient meals, strong cold chain infrastructure, wide supermarket penetration, and growing consumer preference for ready-to-cook and ready-to-eat frozen products.

The Frozen Food Market refers to food products preserved at low temperatures to maintain freshness, taste, texture, and shelf life. These products include frozen desserts, frozen meals, meat, poultry, seafood, fruits and vegetables, snacks, and baked goods. The market is closely linked with cold storage systems, blast freezing technology, individual quick freezing, foodservice demand, retail distribution, and changing household consumption patterns.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market outlook remains steady as consumers continue to prefer convenient, longer-lasting, and easy-to-prepare food options. Growth can be attributed to rising urbanization, busy lifestyles, increasing demand from restaurants and quick-service chains, and improved freezing technologies that help preserve food quality. The expansion of online grocery platforms, private-label frozen food brands, and premium frozen meals is expected to support wider adoption across both retail and foodservice channels.

Key Market Insights

Frozen desserts led the product segment with 25.6% share, supported by strong demand for ice cream, frozen yogurt, sorbets, and ready-to-serve dessert options.

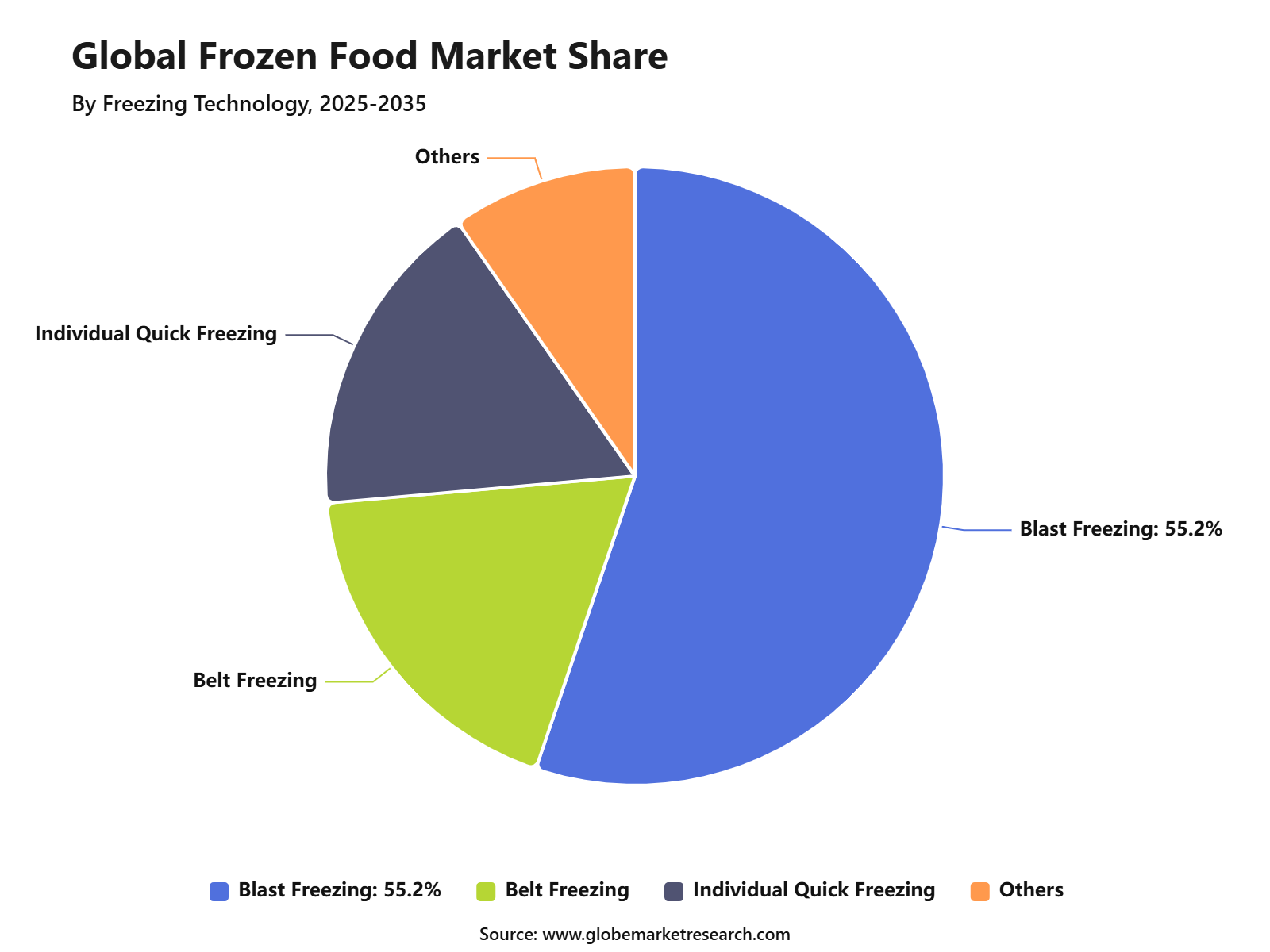

Blast freezing accounted for 55.2% share by freezing technology, driven by its ability to preserve food texture, freshness, nutrition, and product shelf life.

Foodservice held 72.3% share by distribution channel, supported by high demand from restaurants, hotels, cafeterias, catering services, and quick-service food outlets.

North America led the frozen food market with 39.5% share, supported by strong cold-chain infrastructure, high frozen food consumption, and wide retail and foodservice availability.

Go-To-Market-Strategy

The Frozen Food Market should be positioned through a convenience, nutrition, and waste-reduction strategy in 2026, as frozen products are becoming a regular part of household meal planning. According to the American Frozen Food Institute’s 2026 Power of Frozen in Retail findings, 40.0% of consumers use frozen foods daily or every few days, up from 35% in 2019. In addition, 77% of consumers purchase frozen foods with a specific meal or day in mind, showing that frozen products are being planned into weekly eating routines rather than used only as backup food.

Product strategy should focus on frozen meals, frozen vegetables, frozen fruits, frozen snacks, frozen meat and poultry, frozen seafood, pizza, desserts, breakfast foods, and high-protein options. High-protein frozen foods generate about USD 12.0 billion annually and are growing at double-digit volume rates, supported by demand for convenient nutrition and portion-controlled meals. Strong placement should be built across supermarkets, hypermarkets, club stores, online grocery, quick-commerce, foodservice distributors, and convenience retail.

Product Analysis

Frozen desserts led the Frozen Food Market with 25.6% share, supported by strong demand for ice cream, frozen yogurt, gelato, sorbet, frozen novelties, frozen cakes, and dairy-free frozen treats. This segment benefits from regular household consumption, impulse buying, foodservice demand, and seasonal peaks during warmer months.

The growth of this segment can be attributed to rising consumer interest in indulgent, premium, and better-for-you dessert options. Manufacturers are expanding product lines with low-sugar, plant-based, high-protein, lactose-free, and portion-controlled frozen desserts to meet changing consumer preferences.

Frozen desserts are expected to remain a strong product category as brands continue to innovate with new flavors, clean-label ingredients, convenient pack sizes, and premium formats. Demand will also be supported by supermarket freezer aisles, quick-service restaurants, cafés, dessert chains, and online grocery platforms.

Freezing Technology Analysis

Blast freezing accounted for 55.2% share, making it the leading freezing technology in the Frozen Food Market. This method uses rapid cold air circulation to freeze products quickly, helping maintain texture, freshness, taste, and quality by reducing the formation of large ice crystals.

The segment is widely used across frozen desserts, seafood, meat, poultry, bakery products, fruits, vegetables, ready meals, and foodservice ingredients. Fast freezing is especially important for products that need to retain shape, moisture, color, and sensory appeal after thawing or reheating.

Blast freezing is expected to remain the preferred technology as manufacturers focus on product quality and longer shelf life. Demand will be supported by cold-chain expansion, frozen meal production, export-oriented food processing, and rising use of high-quality frozen ingredients in foodservice operations.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFDistribution Channel Analysis

Foodservice led the distribution channel segment with 72.3% share, supported by strong demand from restaurants, hotels, cafés, catering companies, quick-service chains, cloud kitchens, institutional kitchens, and entertainment venues. Frozen foods help these operators maintain consistent quality, reduce preparation time, control waste, and manage large-volume operations.

The growth of this segment can be linked to rising food-away-from-home spending and the need for efficient kitchen operations. Foodservice operators use frozen vegetables, desserts, bakery items, meat, seafood, fries, pizza bases, ready meals, sauces, and appetizers to support fast service and menu consistency.

Foodservice is expected to remain a leading channel as operators continue to manage labor pressure, food cost control, and demand fluctuations. Products that offer easy preparation, portion control, consistent taste, and reliable cold-chain supply are likely to gain stronger adoption in this segment.

Regional Analysis

North America led the Frozen Food Market with 39.5% share, supported by mature cold-chain infrastructure, high freezer ownership, strong retail penetration, and established demand for convenience foods. The region has high consumption of frozen desserts, frozen meals, frozen vegetables, frozen meat, seafood, pizza, snacks, and bakery products.

The growth of North America is supported by busy lifestyles, meal planning needs, foodservice demand, and strong online grocery adoption. Consumers are increasingly using frozen foods for convenience, longer shelf life, reduced food waste, and reliable access to seasonal products throughout the year.

North America is expected to remain a leading regional market as brands invest in healthier frozen meals, premium desserts, plant-based frozen foods, sustainable packaging, and improved cold-chain logistics. Demand will remain strong across supermarkets, foodservice operators, club stores, convenience retail, and e-commerce platforms.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

North America market leadership | +1.9% | North America, 39.5% share in 2025 | Leads frozen food demand. |

Europe premium frozen food adoption | +1.2% | Germany, UK, France, Italy | Supports value growth. |

Asia Pacific urban consumption growth | +1.3% | China, India, Japan, South Korea | Drives future volume. |

Latin America cold-chain expansion | +0.7% | Brazil, Mexico, Chile, Colombia | Builds steady adoption. |

Middle East and Africa food retail growth | +0.6% | GCC, South Africa, Egypt | Supports gradual demand. |

Risk Factors & Market Barriers

The major risk in the Frozen Food Market is the high cost and strict management of cold-chain operations. Frozen products require controlled storage, refrigerated transportation, freezer capacity, and stable energy supply from manufacturing to retail shelves. Any disruption in temperature control can affect quality, food safety, shelf life, and retailer acceptance, which makes logistics efficiency a key barrier for small and mid-sized producers.

Food safety and recall risk also remain important barriers in 2026. In June 2026, USDA FSIS announced a recall of around 5,795 pounds of frozen meatloaf products due to misbranding and undeclared soy allergen. Earlier in 2026, frozen meatballs sold through Aldi were recalled after possible metal contamination was identified, covering about 9,462 pounds of ready-to-eat frozen Italian-style meatballs. These cases show that labeling control, foreign material detection, allergen management, and supplier audits are critical for protecting consumer trust and avoiding financial losses.

Revenue Potential Analysis

Revenue Landscape Across

Revenue opportunities across the Frozen Food Market are spread across everyday meals, snacks, desserts, breakfast items, vegetables, fruits, meat, seafood, and family-size products. Frozen foods serve multiple consumer needs, including quick preparation, long shelf life, portion control, reduced food waste, and affordable meal planning. Multi-serve meals, pizzas, and frozen sides represent roughly USD 12.0 billion in sales, showing the strength of frozen products in family and shared eating occasions.

Across channels, supermarkets and hypermarkets remain the core revenue base because they provide freezer space, wide product variety, promotions, and private-label visibility. Online grocery and quick-commerce are also becoming important, especially for repeat purchases of frozen vegetables, snacks, meals, and protein items. Revenue growth is expected to be stronger for products that combine health claims, better taste, easy preparation, strong packaging, and clear cooking instructions.

Financial Impact

The financial impact of the Frozen Food Market in 2026 will depend on how well companies manage input costs, energy costs, packaging, labor, and freezer logistics. FAO reported that the Food Price Index averaged 130.8 points in May 2026, while cereal and sugar prices increased during the month, creating cost pressure for frozen meals, pizza, bakery items, desserts, and prepared snacks. Wheat prices also remained under pressure, with U.S. Hard Red Winter wheat prices in May 2026 reported 28% higher than in May 2025, affecting dough-based frozen foods and bakery-linked frozen products.

Profitability can be improved through automation, better freezing technology, high freezer utilization, efficient route planning, and stronger demand forecasting. Frozen food companies can also improve margins through premium products, private-label manufacturing, high-protein meals, value packs, and reduced wastage from longer shelf life. The market remains financially attractive, but stronger returns are expected for companies that can balance affordable pricing with cold-chain discipline, safe production, and consistent product quality.

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Frozen desserts category growth | +1.5% | North America, Europe, Asia Pacific | Leads product demand. |

Blast freezing technology adoption | +1.2% | Food processors globally | Preserves product quality. |

Foodservice channel strength | +1.3% | North America, Europe, Asia Pacific | Drives bulk volume. |

Premium frozen meals and snacks | +1.0% | Developed markets | Supports higher margins. |

Clean-label frozen foods | +0.8% | U.S., Europe, Japan | Builds consumer trust. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Frozen Food Manufacturers | +1.4% | Global | Expands product capacity. |

Cold-Chain Logistics Investors | +1.2% | North America, Europe, Asia Pacific | Supports frozen delivery. |

Foodservice Companies | +1.0% | Global | Drives bulk purchasing. |

Retail and Grocery Chains | +0.9% | Global | Strengthens shelf availability. |

Private Equity Firms | +0.8% | North America, Europe, Asia Pacific | Enables brand scaling. |

Segment Covered in the Report

By Product

Frozen Desserts

Frozen Meals

Meat/Poultry/Seafood

Fruits and Vegetables

Snacks

Baked Goods

By Freezing Technology

Blast Freezing

Belt Freezing

Individual Quick Freezing

Others

By Distribution Channel

Foodservice

Retail

By Region

Asia Pacific

North America

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for convenient meal options | +1.6% | North America, Europe, Asia Pacific | Drives daily consumption. |

Growth in frozen desserts and snacks | +1.3% | North America, Europe, urban Asia | Supports category expansion. |

Expansion of cold-chain infrastructure | +1.1% | Global | Improves product reach. |

Increasing demand from foodservice operators | +1.0% | North America, Europe, Asia Pacific | Supports bulk purchases. |

Longer shelf life and reduced food waste | +0.8% | Global | Improves product value. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High cold storage and logistics cost | -0.9% | Emerging markets | Raises distribution cost. |

Consumer preference for fresh food | -0.8% | Global | Limits repeat usage. |

Energy cost volatility | -0.6% | North America, Europe, Asia Pacific | Pressures margins. |

Quality loss during poor handling | -0.5% | Emerging and rural markets | Affects product trust. |

Regulatory pressure on additives and labeling | -0.5% | U.S., Europe, developed Asia | Increases compliance burden. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in frozen dessert products | +1.5% | North America, Europe, Asia Pacific | Builds premium demand. |

Expansion of ready-to-cook frozen meals | +1.3% | Urban global markets | Supports convenience buying. |

Rising demand from foodservice channels | +1.2% | North America, Europe, Asia Pacific | Drives high-volume sales. |

Health-focused frozen food innovation | +1.0% | U.S., Canada, Europe, Japan | Improves product positioning. |

Online grocery and frozen delivery growth | +0.8% | Global urban markets | Expands consumer access. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining frozen temperature integrity | -0.8% | Global | Protects product quality. |

Managing cold-chain disruptions | -0.7% | Emerging and export markets | Impacts availability. |

Ingredient and packaging cost pressure | -0.6% | Global producers | Reduces margins. |

Competition from fresh and chilled products | -0.5% | Global retail markets | Limits pricing power. |

Sustainability pressure on frozen packaging | -0.4% | Europe, North America | Raises packaging cost. |

Recent Developments

April 2026: The Kraft Heinz Company launched Kraft Mac & Cheese Restaurant Edition, positioned around restaurant-inspired at-home meals. The launch supports the company’s broader focus on affordable, easy-preparation food formats, while Kraft Heinz reported approximately USD 25.0 billion in net sales in 2025.

March 2026: General Mills, Inc. relaunched La Tiara and added three new flavors: Chorizo, Tinga, and Reduced Sodium. The move supports convenient meal preparation through Mexican-style packaged meal components, while General Mills reported USD 19.0 billion in fiscal 2025 net sales

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 326.9 Billion |

Forecast Revenue (2035) | USD 596.6 Billion |

CAGR (2025-2035) | 6.2% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Product (Frozen Desserts, Frozen Meals, Meat/Poultry/Seafood, Fruits and Vegetables, Snacks, Baked Goods), By Freezing Technology (Blast Freezing, Belt Freezing, Individual Quick Freezing, Others), By Distribution Channel (Foodservice, Retail) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Nestlé S.A., Conagra Brands, Inc., General Mills, Inc., Tyson Foods, Inc., Kraft Heinz Company, Nomad Foods Limited, McCain Foods Limited, Ajinomoto Co., Inc., Unilever PLC, Kellanova |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Nestlé S.A.

Conagra Brands, Inc.

General Mills, Inc.

Tyson Foods, Inc.

Kraft Heinz Company

Nomad Foods Limited

McCain Foods Limited

Ajinomoto Co., Inc.

Unilever PLC

Kellanova

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Food and Beverages

Snack Food Market Size to hit USD 1,157.5 Bn by 2035

Global Snack Food Market Size, Share Analysis By Product Type (Chips and Crisps, Nuts and Seeds, Biscuits and Cookies, Popcorn, Meat Snacks, Others), By Category (Conventional Snacks, Healthy Snacks), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online, Specialty Stores, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Canned Food Market Size to Exceed USD 233.8 Billion by 2035

Global Canned Food Market Size, Share Analysis By Product Type (Canned Seafood, Canned Meat, Canned Fruits and Vegetables, Canned Ready Meals, Others), By Type (Conventional, Organic), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Ready-to-Eat Food Market to Exceed USD 846.5 Billion by 2035

Global Ready-to-Eat Food Market Size, Share Analysis By Product Type (Meat/Poultry, Vegetarian, Cereal-Based, Others), By Packaging (Frozen/Chilled, Canned, Retort, Others), By Distribution Channel (Hypermarkets, Convenience Stores, Online, Others), By End User (Residential, Foodservice, Institutional), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Cereals and Grains Market to Exceed USD 1,928.1 Billion by 2035

Global Cereals and Grains Market Size, Share Analysis By Product Type (Wheat, Rice, Maize, Barley, Oats, Sorghum, Others), By Application (Food and Beverage, Animal Feed, Biofuel, Industrial Use, Others), By Form (Whole Grain, Flour, Processed Grain, Others), By Distribution Channel (Direct Sales, Wholesalers and Distributors, Retail, Online), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035