Revenue, 2025

$ 5.8 Bn

Forecast, 2035

$ 17.9 Bn

CAGR, 2025-2035

11.9%

Report Coverage

Global

Market Size and Forecast

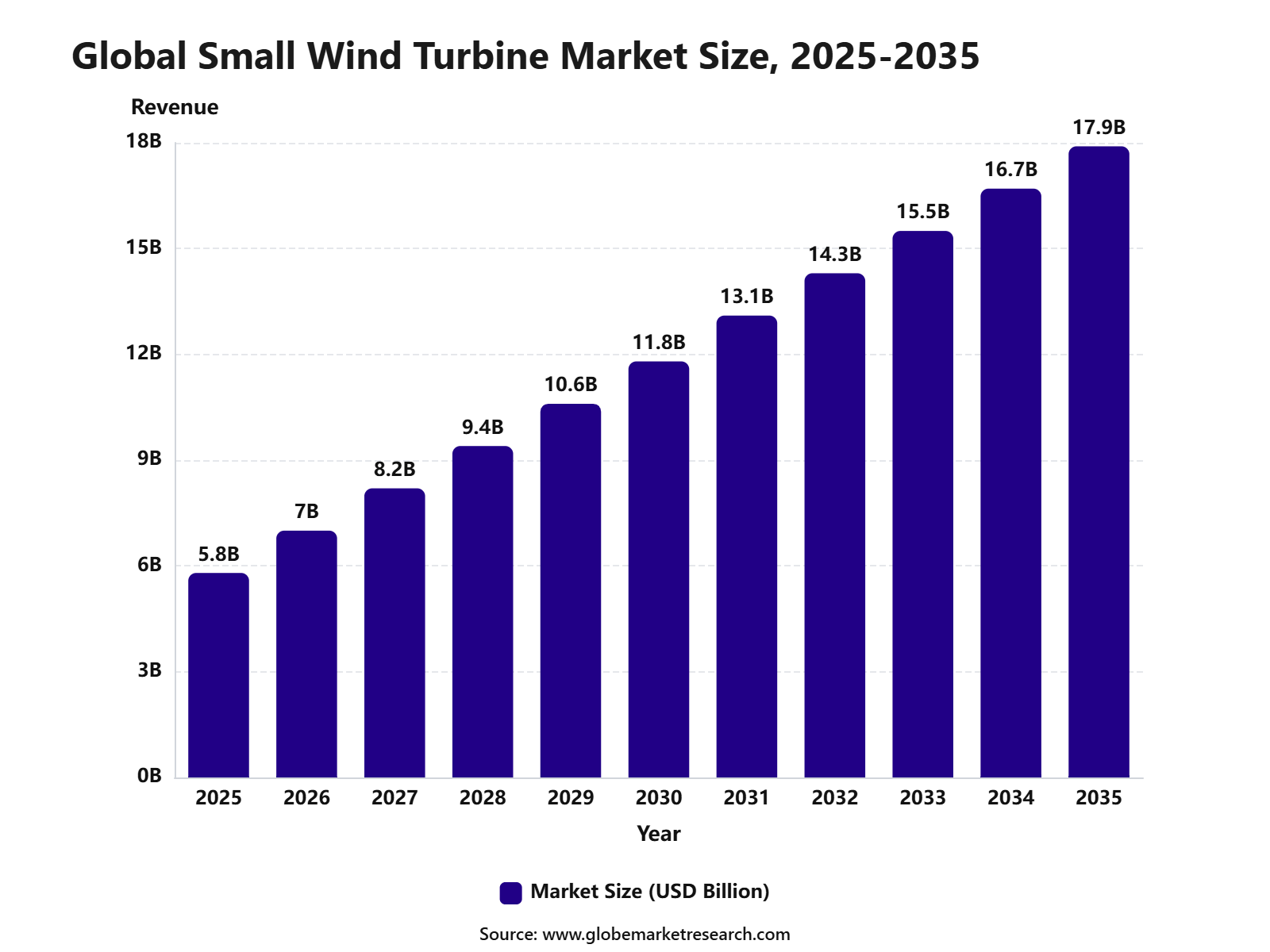

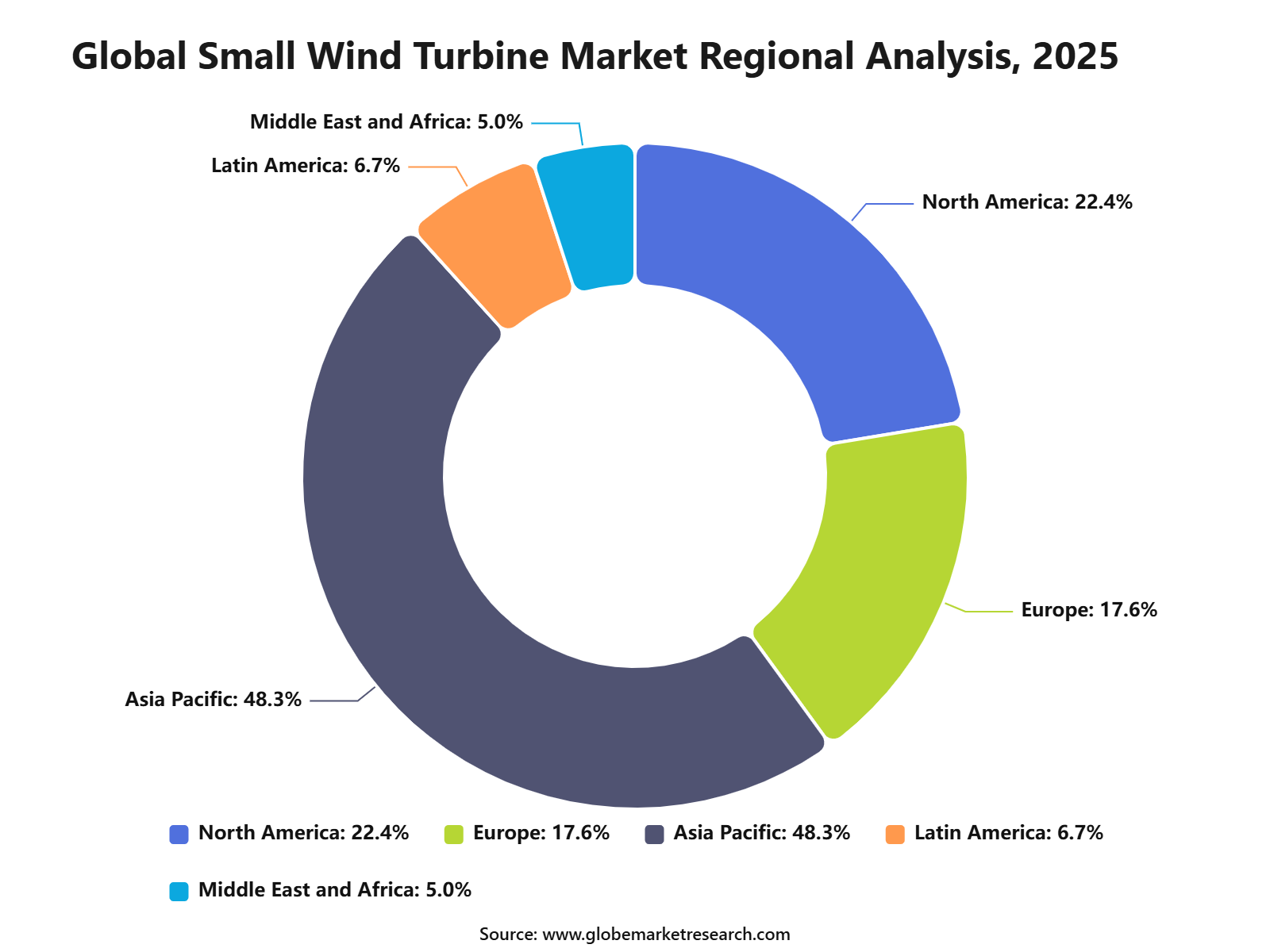

The Global Small Wind Turbine Market was worth USD 5.8 billion in 2025 and is expected to reach USD 17.9 billion by 2035, growing at a CAGR of 11.9% from 2025 to 2035. Based on this growth rate, the market is estimated to reach around USD 7.0 billion in 2026. Asia Pacific held the largest regional share of 48.3% in 2025, valued at around USD 2.8 billion, supported by rural electrification, distributed renewable energy projects, off-grid power demand, and rising small-scale clean energy adoption.

The Small Wind Turbine Market includes compact wind power systems used to generate electricity for homes, farms, telecom towers, small businesses, remote sites, and community energy projects. These turbines are designed for low to medium power output and are often installed in off-grid, hybrid, and distributed energy setups. The market is closely linked with decentralized power generation, clean energy access, and local renewable infrastructure.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 5.8 Billion |

Projected Revenue, 2035 | USD 17.9 Billion |

CAGR (2025-2035) | 11.9% |

Largest Region | Asia-Pacific (48.3%, USD 2.8 Bn) |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

The market outlook remains positive as demand grows for reliable renewable power in remote and semi-urban locations. Growth can be attributed to rising electricity needs, supportive clean energy policies, and increasing use of hybrid wind-solar systems. The expansion of Asia Pacific rural energy programs, microgrid projects, and affordable turbine technologies is expected to support long-term market demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Horizontal axis designs led the axis type segment with 69.2% share, supported by higher energy conversion efficiency, proven turbine design, and strong use in residential, agricultural, and small commercial power systems.

0 to 5 kW micro-class turbines accounted for 46.0% share by capacity rating, driven by demand for small-scale power generation in homes, farms, remote sites, and off-grid locations.

Off-grid systems held 56.3% share by connectivity, supported by rising use in rural areas, remote properties, telecom sites, and locations with limited grid access.

Freestanding tower installations captured 73.6% share, driven by better wind exposure, easier placement flexibility, and stronger suitability for open land, farms, and standalone renewable power setups.

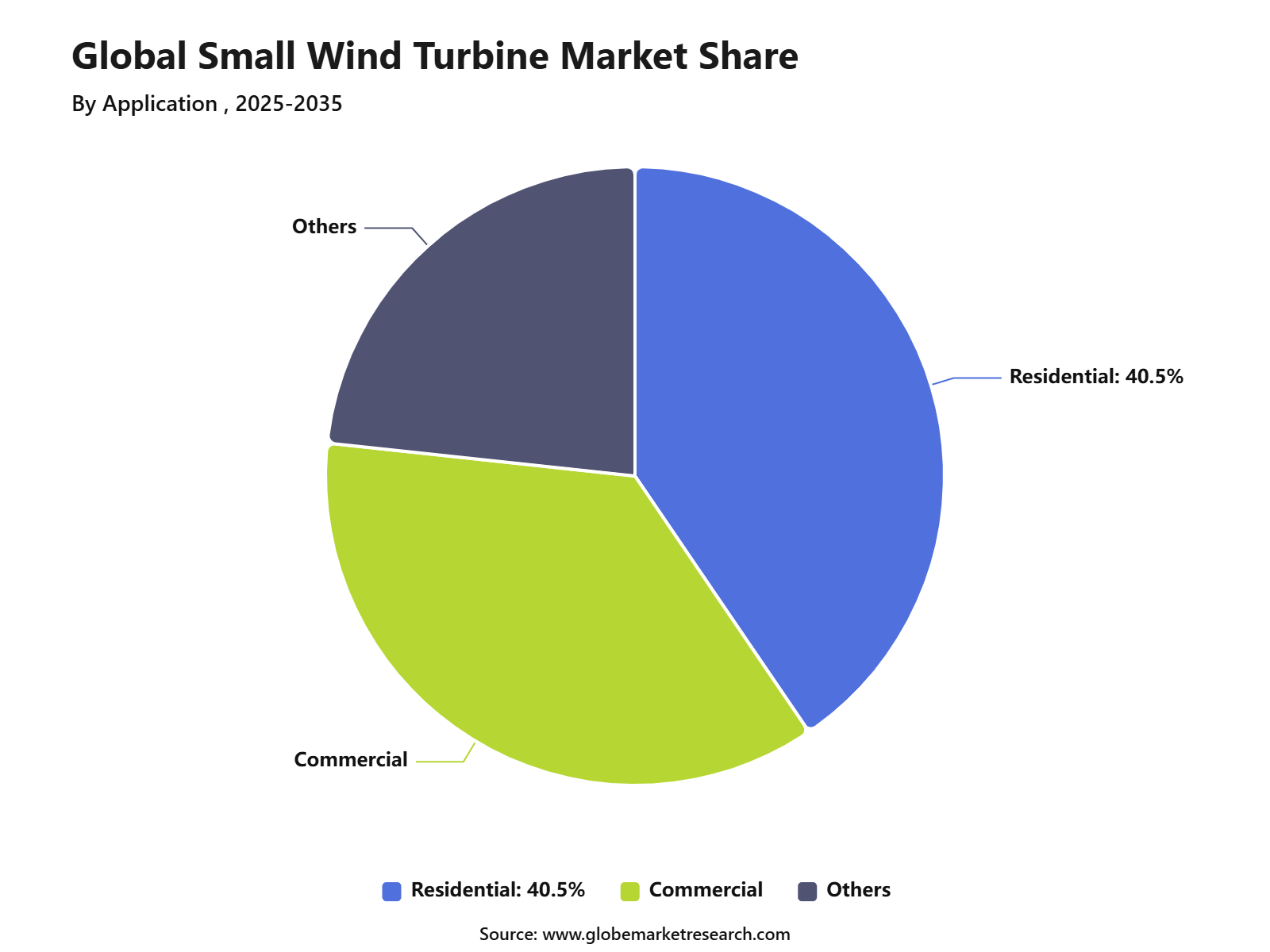

Residential use accounted for 40.5% share by application, supported by growing interest in distributed clean energy, backup power, and lower household electricity dependence.

Asia Pacific led the small wind turbine market with 48.3% share, valued at USD 2.8 billion, supported by rural electrification needs, rising renewable energy adoption, and growing deployment across China, India, Japan, and Southeast Asia.

Top Funding and Investment

Top Investments i

NREL selected five companies for six new distributed wind projects under the 2025 Competitiveness Improvement Project, with USD 4.4 million in DOE funding and USD 2.3 million in private-sector cost-share support. The selected work covers small and medium wind turbines below 1 MW, including Bergey Windpower’s new 75 kW turbine, NPS Solutions’ 100 kW turbine platform, and XFlow Energy’s vertical-axis wind turbine development.

Wind Harvest signed a strategic MOU with Chair Capital for a milestone-based funding partnership of up to USD 80 million plus. The investment roadmap is linked to scaling Wind Harvest’s vertical-axis wind turbine technology for renewable energy markets, including on-grid and off-grid project applications.

Wind Harvest signed an LOI with Port Hamilton Refining and Transportation in St. Croix for a hybrid renewable energy project. The proposed system includes up to 6 MW of vertical-axis wind turbines, 6 MW of solar generation, and battery energy storage to support industrial onsite power reliability.

Udupi Tollway planned India’s first rooftop 10 kW vertical-axis wind turbine pilot at the Hejamadi toll plaza. The system is expected to generate around 38 to 72 kWh per day and reduce about 20 tonnes of CO2 emissions annually, supporting small wind use in highway and public infrastructure.

A 0.5 kW rooftop vertical-axis wind turbine was installed at a community centre near Trichy under the Union Education Ministry’s Unnat Bharat Abhiyan. The turbine cost about Rs 1 lakh, with another Rs 25,000 contributed for installation, and can support lighting and fans for village community use.

Top Funding Developments

GEVI raised €2.7 million in seed funding led by 360 Capital and CDP Venture Capital, with participation from NextSTEP One. The funds will be used for industrialization, serial production of its micro wind turbines, AI control system improvement, and new turbine versions. Its vertical-axis micro wind turbine has 5 kW nominal output, starts below 2.5 m/s wind speed, and has a compact rotor design of 3 m height and 5.4 m diameter.

Wind Harvest crossed USD 1 million raised through its StartEngine campaign. The company stated that the capital supports construction of more Wind Harvester turbines, third-party certification, and commercialization of its vertical-axis turbine technology.

Epic Angels made its first Peru investment in Eolic Wall, alongside Market Impact Capital. The funding amount was not disclosed publicly, but the capital is planned for commercial pilot units, IP strengthening, team expansion, and first deployments in 2026. Eolic Wall is developing compact modular wind systems for factories, data centers, buildings, and remote communities.

Top Acquisitions

The TPG and MAVCO-led consortium acquired Siemens Gamesa’s onshore wind business in India and Sri Lanka and launched the independent company Vayona Energy. What it acquired includes onshore wind turbine manufacturing, installation, and service operations, nearly 1,000 employees, more than 12 GW of operational and development assets, an order book above 1 GW, and an O&M portfolio exceeding 8 GW.

ABB completed the acquisition of Gamesa Electric, the power electronics division of Siemens Gamesa. What it acquired includes wind converters, industrial battery energy storage power electronics, utility-scale solar inverters, two converter factories in Spain, around 400 employees, and a business with annual revenue of about €145 million for the fiscal year ended September 30, 2025.

By Axis Type

Horizontal designs accounted for 69.2% share of the Small Wind Turbine Market. This leading position is supported by their higher efficiency, mature design structure, and strong suitability for residential, agricultural, telecom, and remote power applications.

These turbines are widely preferred because they can capture wind more effectively when installed at suitable heights. Horizontal-axis small wind turbines also offer proven performance, easier availability, and better compatibility with standard freestanding tower systems.

Demand is expected to remain strong as users seek reliable off-grid and distributed renewable power solutions. Their use in homes, farms, rural facilities, and small commercial sites will continue to support the dominance of horizontal designs.

By Capacity Rating

The 0 to 5 kW micro class segment held 46.0% share of the Small Wind Turbine Market. This dominance is driven by strong demand from households, small farms, telecom sites, remote cabins, and low-load off-grid applications.

Micro wind turbines are preferred because they are easier to install, require lower upfront investment, and are suitable for locations with limited power needs. These systems can support lighting, battery charging, small appliances, water pumping, and backup power requirements.

The segment is expected to maintain strong demand as rural electrification, residential renewable adoption, and decentralized power systems continue to expand. Their compact size and practical power output make them suitable for small-scale clean energy users.

By Connectivity

Off-grid systems accounted for 56.3% share of the Small Wind Turbine Market. This leading position is supported by strong use in remote areas where grid access is limited, unreliable, or too costly to extend.

Small wind turbines are widely used in off-grid homes, farms, islands, telecom towers, rural schools, and remote monitoring stations. These systems are often combined with batteries or solar panels to provide more stable and continuous power supply.

Demand for off-grid connectivity is expected to remain strong as energy access, resilience, and local power generation become more important. Small wind systems offer a practical solution for users seeking independence from centralized electricity networks.

By Installation Location

Freestanding towers held 73.6% share of the Small Wind Turbine Market. This dominance is supported by their ability to place turbines at better wind heights, away from roof turbulence, buildings, and nearby obstructions.

These towers are commonly used in residential properties, farms, rural businesses, telecom sites, and remote energy systems. Freestanding installations help improve turbine performance by allowing better wind exposure and more stable airflow.

The segment is expected to remain dominant because tower height and location have a direct impact on energy output. As small wind users focus on higher efficiency and reliable generation, freestanding towers will continue to be the preferred installation format.

By Application

Residential use accounted for 40.5% share of the Small Wind Turbine Market. This leading share is supported by rising household interest in renewable power, lower electricity bills, backup energy, and energy independence.

Small wind turbines are used in rural homes, farmhouses, remote cabins, island homes, and off-grid residential properties. They can supply power for lighting, appliances, heating support, water pumping, and battery storage systems.

The segment is expected to remain a major demand area as homeowners adopt hybrid renewable systems and decentralized energy solutions. Residential users are increasingly combining small wind turbines with solar panels and batteries to improve year-round power availability.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Region

Asia-Pacific accounted for 48.3% share of the Small Wind Turbine Market, reaching USD 2.8 billion. The region’s leadership is supported by rural electrification needs, strong renewable energy programs, and rising demand for decentralized power across remote and semi-urban areas.

China, India, Japan, Australia, and Southeast Asian countries are key contributors to regional demand. The region benefits from agricultural power needs, island electrification projects, telecom expansion, and growing interest in hybrid renewable systems.

Asia-Pacific is expected to maintain its leading position as distributed energy adoption and off-grid power investment continue to rise. Demand will remain supported by residential users, farms, rural businesses, and public electrification projects seeking affordable clean power solutions.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Asia Pacific leads the Small Wind Turbine Market with 48.3% share in 2025, valued at around USD 2.8 billion, supported by rural electrification, agricultural energy needs, island power systems, and growing adoption of distributed renewable energy. China and India remain major regional contributors due to large rural populations and rising clean energy investment.

North America remains important because of demand from farms, remote homes, small businesses, and off-grid power users. Europe supports value growth through community energy projects, renewable self-consumption, rural installations, and hybrid distributed power systems.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +3.6% | Asia Pacific, 48.3% share in 2025 | Leads global value demand. |

China distributed renewable growth | +2.3% | China | Supports regional scale. |

India rural and agricultural energy demand | +1.9% | India | Builds future adoption. |

North America farm and off-grid use | +1.3% | U.S. and Canada | Adds steady demand. |

Europe community energy projects | +1.1% | Germany, UK, France, Nordic countries | Supports local renewable power. |

Go-To-Market and Sales Economics

Small wind turbines are commercialized through rural energy installers, electrical contractors, farm cooperatives, telecom power vendors, microgrid developers, and direct sales to homes, farms, schools, islands, and remote facilities. DOE defines distributed wind as turbines installed near the point of use, including off-grid systems serving local energy needs.

Sales economics are strongest where electricity prices are high, wind resources are steady, and solar-only systems do not meet evening or seasonal loads. EIA reported U.S. average retail electricity revenue of 13.88 cents/kWh in April 2026, up 6.0% year over year, improving the value of on-site generation.

Technology commercialization is being supported by certification and manufacturing programs. NREL’s 2026 Competitiveness Improvement Project selected five companies for six projects, with USD 4.4 million in DOE funding and USD 2.3 million in private cost-share support for turbines, converters, blades, and controls below 1 MW.

Risk Factors & Market Barriers

The main barrier is project economics, as small wind requires proper wind-resource assessment, tower height, permitting, installation labor, electrical work, and maintenance support. DOE reported the average capacity-weighted installed cost for new small wind projects from 2014 to 2023 at USD 11,410/kW, while 2023 projects averaged USD 7,370/kW.

Performance risk is high because output depends strongly on site quality, turbulence, tower placement, and local wind speed. DOE found the average 2023 net capacity factor for a sample of 100 small wind projects was 13%, with observed results ranging up to 28%, showing wide variation by location.

Certification and product availability can also slow adoption. DOE reported that only seven small wind turbines had active certifications as of June 2024, although at least 23 small turbine models had been certified between 2011 and 2023. This limits bankable options for buyers, lenders, and incentive programs.

Revenue Potential Analysis

Revenue Landscape Across

Revenue is spread across residential systems, farms, rural businesses, telecom towers, schools, municipal sites, island grids, mining camps, water pumping, and hybrid solar-wind-battery microgrids. DOE reported more than 92,000 distributed wind turbines installed across the U.S. from 2003 through 2023, totaling 1,110 MW of cumulative capacity.

Small wind remains a niche but useful part of distributed energy. DOE documented about 94 MW of new global small wind capacity in 2023 across six countries, with total cumulative global small wind capacity estimated at just under 2.0 GW. China represented 86.5 MW, or 92% of 2023 additions.

The wider wind sector supports supplier confidence. IRENA reported record wind additions of 158.7 GW in 2025, up 14.0% from 2024, while GWEC reported 165 GW of new wind capacity and 1,299 GW of installed global wind power in 2025.

Financial Impact

Small wind turbines create financial impact by reducing grid purchases, improving energy security, and supporting hybrid power systems in windy locations. The strongest returns are expected for farms, rural businesses, telecom sites, and remote assets where diesel fuel, outage risk, or high retail electricity prices increase the value of local generation.

Financial returns depend on equipment cost, installation cost, incentives, annual output, maintenance, and avoided electricity price. DOE reported that 2023 distributed wind projects received USD 12.4 million in state incentives, production tax credits, and USDA REAP grants, more than double the USD 5 million reported in 2022 and 2021.

The strongest financial upside is expected from certified turbines, repowering, better inverters, taller towers, and hybrid systems with solar and batteries. EIA projects U.S. wind capacity to rise from 158 GW in 2025 to 170 GW in 2026 and 178 GW in 2027, supporting broader service and component demand.

Drivers Impact Analysis

The Small Wind Turbine Market is driven by rising demand for distributed renewable power, rural electrification, off-grid energy systems, farm power generation, telecom tower backup, and hybrid solar-wind systems. Small wind turbines are useful where grid access is limited or where users want local clean power generation.

Asia Pacific leads the market due to rising electricity demand, rural energy needs, agricultural power use, island electrification, and strong renewable energy programs. China, India, Japan, Australia, and Southeast Asian countries remain key contributors because of growing interest in decentralized and hybrid clean energy systems.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for distributed renewable power | +3.2% | Asia Pacific, Europe, North America | Drives core market growth. |

Rural and off-grid electrification needs | +2.7% | India, China, Southeast Asia, Africa | Supports localized power use. |

Growth in hybrid solar-wind systems | +2.3% | Asia Pacific and remote regions | Improves energy reliability. |

Demand from farms and small businesses | +1.9% | Rural and semi-urban markets | Builds steady adoption. |

Clean energy policy support | +1.5% | Asia Pacific, Europe, North America | Improves investment confidence. |

Restraints Impact Analysis

The market faces restraints from high upfront installation cost, variable wind resource availability, permitting issues, and maintenance requirements. Small wind turbines need suitable wind speeds, proper siting, tower installation, and regular service to deliver stable performance.

Another restraint is competition from rooftop solar and battery storage. Solar systems are often easier to install and maintain, so small wind turbines must show strong value in windy locations, farms, coastal areas, and off-grid sites.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High initial installation cost | -1.5% | Global small wind users | Limits wider adoption. |

Variable wind resource availability | -1.3% | Rural and distributed sites | Affects power output. |

Competition from solar PV systems | -1.1% | Residential and small commercial markets | Pressures demand. |

Permitting and zoning restrictions | -0.9% | North America, Europe, urban Asia | Slows installations. |

Maintenance and tower safety needs | -0.7% | Remote and off-grid locations | Raises operating responsibility. |

Opportunities Impact Analysis

Opportunities are strong in rural electrification, telecom towers, agricultural farms, island power systems, small commercial facilities, residential clean power, and hybrid renewable microgrids. These applications benefit from local generation, reduced diesel use, and lower dependence on unreliable grids.

Higher-value opportunities are emerging in vertical-axis turbines, smart controllers, battery-integrated systems, low-noise designs, and community-scale wind projects. Companies that provide reliable turbines, easy maintenance, and strong site assessment support can capture stronger long-term demand.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rural electrification projects | +3.0% | Asia Pacific, Africa, Latin America | Builds high-growth demand. |

Hybrid wind-solar microgrids | +2.5% | Remote and island communities | Improves power reliability. |

Telecom tower power supply | +2.0% | India, Southeast Asia, Africa | Reduces diesel dependence. |

Agricultural and farm power systems | +1.7% | Asia Pacific, Europe, North America | Adds practical use cases. |

Battery-integrated small wind systems | +1.4% | Off-grid and backup power markets | Improves energy storage value. |

Challenges Impact Analysis

The main challenge is matching turbine performance with local wind conditions. Small wind projects need proper site assessment, tower height, wind mapping, and installation quality to avoid weak output and poor customer returns.

Another challenge is building customer confidence. Many buyers need clear payback analysis, warranty support, reliable maintenance networks, and proof that the turbine can perform well in their location.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Site-specific wind performance risk | -1.2% | Global small wind installations | Affects project returns. |

Limited installer and service networks | -1.0% | Emerging and remote markets | Slows deployment. |

Customer payback uncertainty | -0.9% | Residential and small business users | Reduces buying confidence. |

Noise and visual concerns | -0.7% | Residential and suburban markets | Affects acceptance. |

Product quality variation | -0.6% | Low-cost turbine markets | Weakens trust. |

Segment Covered in the Report

By Axis Type

Horizontal Axis Wind Turbines

Vertical Axis Wind Turbines

By Capacity Rating

0 To 5 KW

6 To 20 KW

21-100 KW

By Connectivity

Off-Grid

On-Grid

Hybrid

By Installation Location

Rooftop/Building-Integrated

Freestanding Tower

By Application

Residential

Commercial

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward hybrid solar-wind systems, vertical-axis small turbines, battery-connected wind systems, smart charge controllers, low-maintenance designs, and off-grid renewable energy packages. Buyers increasingly prefer complete systems instead of standalone turbines.

Asia Pacific remains the largest value region because of rural power demand, renewable energy programs, and growing distributed generation needs. North America and Europe support value growth through farms, remote homes, small businesses, and community energy projects.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Hybrid solar-wind systems expand | +2.8% | Asia Pacific, Europe, North America | Leads future installations. |

Vertical-axis turbine interest rises | +2.1% | Urban-edge and low-noise sites | Adds design flexibility. |

Battery-connected systems gain demand | +1.8% | Off-grid and backup power users | Improves energy reliability. |

Smart turbine controllers improve | +1.5% | Distributed renewable systems | Supports better output control. |

Community-scale wind projects grow | +1.2% | Rural and remote communities | Builds shared clean power access. |

Investor Type Impact Matrix

Investors should focus on small wind companies with strong turbine reliability, site assessment capability, hybrid system integration, battery compatibility, and after-sales service networks. Performance validation, installation quality, and maintenance support are key success factors.

Strategic investors can also target small wind turbine manufacturers, hybrid microgrid developers, remote monitoring providers, rural electrification firms, and distributed energy platforms. Companies that combine wind, solar, storage, and service support are better positioned for long-term growth.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Small Wind Turbine Manufacturers | +2.5% | Global | Expands distributed wind supply. |

Hybrid Renewable System Providers | +2.1% | Asia Pacific, Europe, North America | Supports reliable clean power. |

Rural Electrification Developers | +1.7% | Emerging and remote markets | Builds off-grid adoption. |

Smart Controller and Monitoring Firms | +1.3% | Distributed energy systems | Improves operating performance. |

Strategic Distributed Energy Investors | +1.1% | Global renewable energy markets | Funds system integration and scale. |

Recent Developments

January 2026: Eocycle’s M-21 spec sheet highlighted active power curtailment and integrated energy storage capability, supporting remote, commercial and agricultural wind systems designed for extreme climates and on-site consumption.

April 2026: ClassNK’s small-wind certification registry listed Ghrepower’s GHRE19.8J certification renewal to 2031, while Ghrepower continued offering 5 kW to 100 kW small and mid-scale turbines for distributed projects.

February 2026: Northern Power Systems obtained UL 1741 SB certification for its NPS 100C wind turbine power converter, supporting IEEE 1547 grid-interconnection compliance and distributed wind deployment across the U.S.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

UNITRON Energy Systems Pvt Ltd

Northern Power Systems Inc.

Shanghai Ghrepower Green Energy Co. Ltd

TUGE Energia OU

Ryse Energy

Kingspan Group Plc (Wind Division)

Eocycle Technologies Inc.

XZERES Wind Corp.

Fortis Wind Energy BV

HY Energy Co. Ltd

Endurance Wind Power Inc.

Kliux Energies International

Aeolos Wind Energy Ltd

Bergey Windpower Co.

City Windmills Holdings PLC

Wind Energy Solutions BV

SD Wind Energy Ltd

Pika Energy (Generac)

Envergate Energy AG

Suzlon Energy Ltd (≤100 kW segment)

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Energy and Power

Hydropower Generation Market to Hit USD 560.9 Billion by 2035

Hydropower Generation Market Size, Share, Analysis By Plant Type (Large Hydropower Plant, Small Hydropower Plant, Pumped Storage Hydropower), By Application (Utility, Industrial, Rural Electrification), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Power Generation Market to Hit USD 2,539.5 Billion by 2035

Power Generation Market Size, Share, Analysis By Type (Conventional/Non-Renewable (Nuclear and Fossil Fuels), Non-Conventional/Renewable (Solar, Wind, Hydro, and Others)), By End-User (Residential, Commercial, Industrial, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Single Phase String Inverters Market to Hit USD 5.1 Billion by 2035

Single Phase String Inverters Market Size, Share, Analysis By Connectivity (On-Grid, Off-Grid), By Power Rating (Below 1 kW, 1 kW to 3 kW, 3 kW to 5 kW, Above 5 kW), By Application (Residential, Commercial), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Fuel Cells Market to Hit USD 70.2 Billion by 2035

Hydrogen Fuel Cells Market Size, Share, Analysis By Type (Air-Cooled Type, Water-Cooled Type), By Application (Stationary, Transport, Portable), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035