Revenue, 2025

$ 8.5 Bn

Forecast, 2035

$ 70.2 Bn

CAGR, 2025-2035

23.5%

Report Coverage

Global

Market Size and Forecast

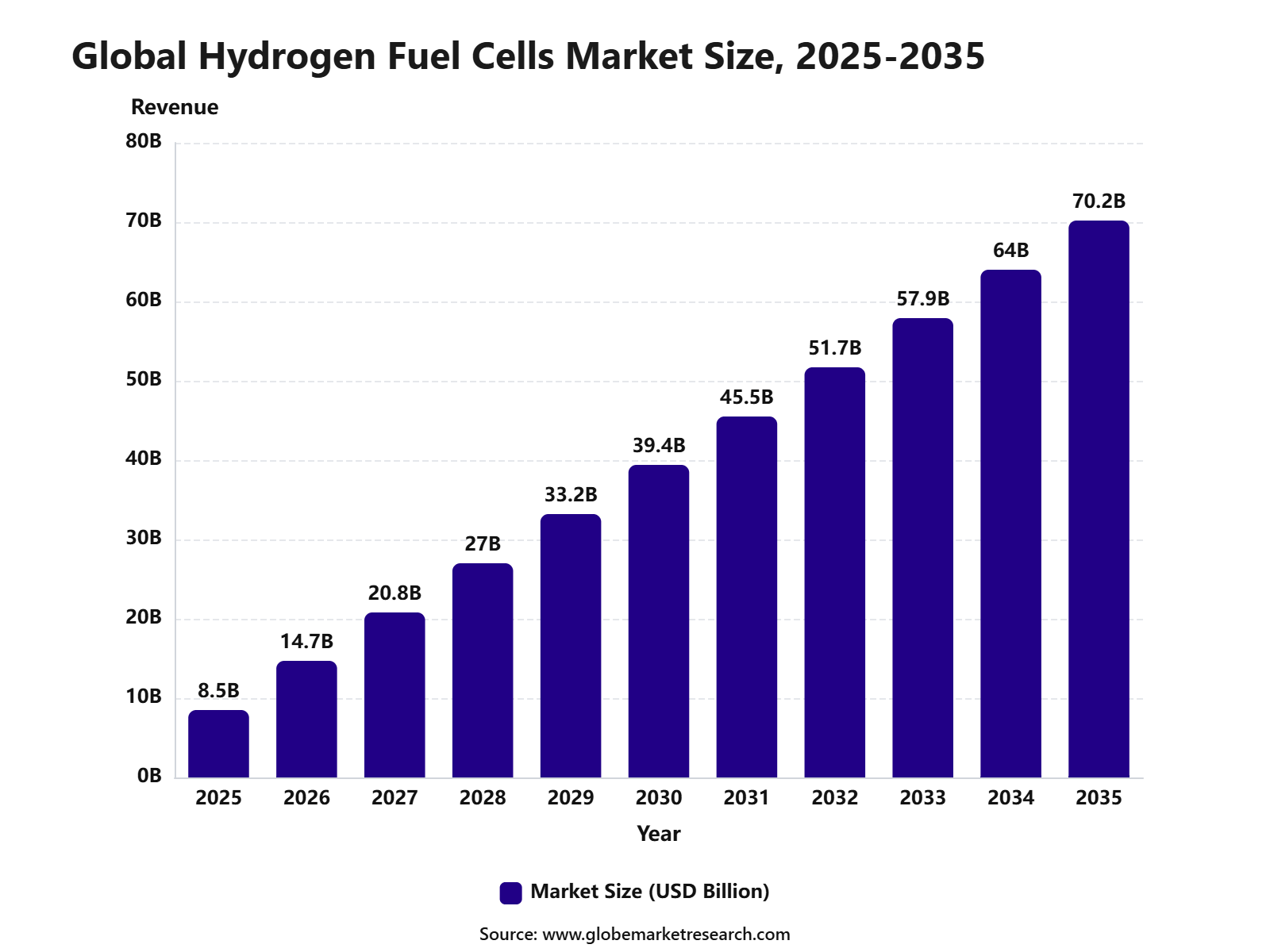

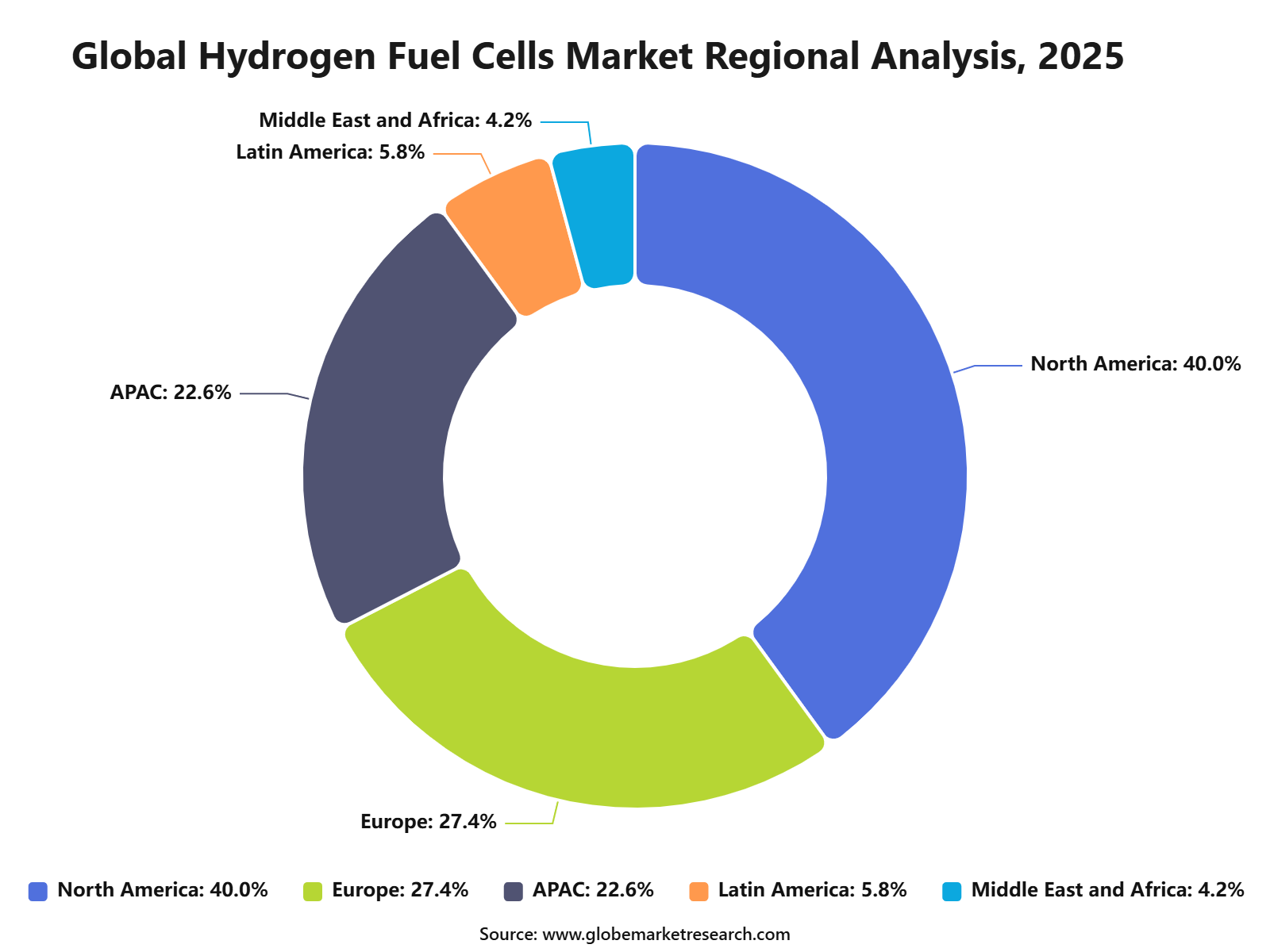

The Global Hydrogen Fuel Cells Market was worth USD 8.5 billion in 2025 and is expected to reach USD 70.2 billion by 2035, growing at a CAGR of 23.5% from 2025 to 2035. Based on this growth rate, the market is estimated to reach around USD 14.7 billion in 2026. North America held the largest regional share of 40.0% in 2025, valued at around USD 3.4 billion, supported by clean mobility investment, hydrogen infrastructure development, fuel cell vehicle adoption, and government-backed decarbonization programs.

The Hydrogen Fuel Cells Market includes electrochemical systems that convert hydrogen and oxygen into electricity, heat, and water without direct combustion. These fuel cells are used in vehicles, buses, trucks, forklifts, backup power systems, stationary power generation, marine applications, and industrial energy systems. The market is closely linked with clean transportation, green hydrogen production, energy storage, and low-carbon power solutions.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 8.5 Billion |

Projected Revenue, 2035 | USD 70.2 Billion |

CAGR (2025-2035) | 23.5% |

Largest Region | North America (40.0% share, USD 3.4 Bn) |

Fastest Growing Region | Asia Pacific |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

The market outlook remains strong as industries and governments increase focus on zero-emission energy technologies. Growth can be attributed to rising demand for clean transport, expanding hydrogen refueling networks, and growing use of fuel cells in backup and distributed power. The expansion of North American hydrogen hubs, commercial fleet deployment, and fuel cell system innovation is expected to support long-term market demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Water-cooled fuel cells led the type segment with 63.5% share, supported by better thermal management, stable operating performance, and strong suitability for high-power fuel cell systems.

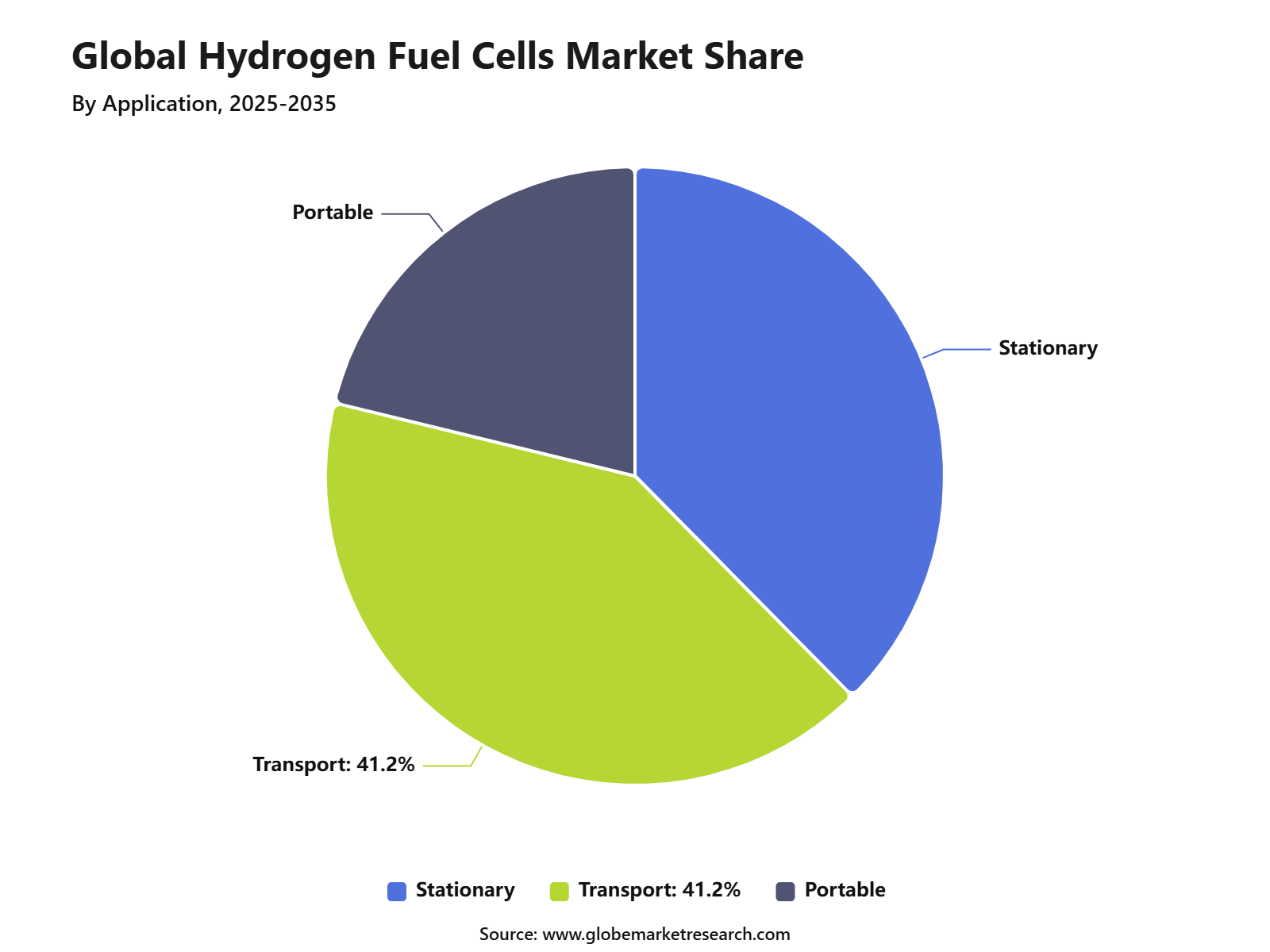

Transport applications accounted for 41.2% share, driven by rising use of hydrogen fuel cells in buses, trucks, trains, marine vessels, and other zero-emission mobility solutions.

North America held 40.0% share of the hydrogen fuel cells market, valued at USD 3.4 billion, supported by clean mobility investment, hydrogen infrastructure development, and growing adoption of fuel cell technology across transport and industrial applications.

Top Funding and Investment

Top Investments

Brookfield expanded its financing framework with Bloom Energy from USD 5 billion to USD 25 billion. The investment framework is intended to finance power projects for AI infrastructure using Bloom’s fuel cell technology and support global expansion of the fuel-cell partnership.

Airbus and MTU Aero Engines announced plans to create a joint venture for a fully electric hydrogen fuel cell engine for aircraft. The official plan covers development, testing, certification, manufacturing, and commercial support. The venture was reported to have a valuation of more than €1.2 billion.

Hyundai Motor announced a KRW 930 billion investment in a new hydrogen fuel cell production plant in Ulsan, South Korea. The plant is planned for completion in 2027 and is designed for annual output of 30,000 fuel cell units, along with PEM electrolyzers for hydrogen production.

Toyota launched its second hydrogen fuel-cell manufacturing joint venture in China with Shudao Group. The planned USD 137 million factory is intended to produce fuel cells for heavy-duty vehicles, including trucks made by Sinotruk.

India approved road transport pilot projects with financial support of about Rs 208 crore under the National Green Hydrogen Mission. The pilots cover 37 hydrogen vehicles, including 15 hydrogen fuel cell-based vehicles, across 10 routes, supported by 9 hydrogen refueling stations.

Top Funding

FuelCell Energy upsized its public offering to USD 225 million, covering 10,714,286 shares at USD 21.00 per share. The company stated that proceeds would support manufacturing capacity expansion, capital expenditure, working capital, and general corporate purposes.

Nekkar Power secured Rs 75 crore in second-round funding from Syndicate Finance, taking its total capital raised to Rs 125 crore. The company said the funding would support R&D, hydrogen fuel-cell stack development, manufacturing expansion in Andhra Pradesh, and hiring.

H2 Carbon Zero, operating as Umagine Hydrogen, raised USD 850,000 in seed funding led by Venture Catalysts, with participation from Faad Networks. The funding was directed toward a planned gigawatt-scale hydrogen fuel cell factory, field trials, and engineering expansion for modular fuel-cell systems.

Top Acquisitions

Ballard Power Systems agreed to acquire 100% of GeoPura at an enterprise value of £301.1 million, around U£301.1 million, around USD 400 millionSD 400 million. What it acquired was GeoPura’s hydrogen-based stationary power platform, Hydrogen Power Unit business, hydrogen fuel supply network, three production sites, and a 50% stake in HyMarnham Power.

Alstom completed the acquisition of Cummins’ hydrogen fuel cell activities dedicated to rail. What it acquired included engineering, product, and support capabilities linked with hydrogen train fleets. The transaction strengthened Alstom’s hydrogen rail technology base and aftersales support capability.

By Type

Water-cooled type fuel cells accounted for 63.5% share of the Hydrogen Fuel Cells Market. This leading position is supported by their ability to manage heat more effectively in high-power and continuous operating applications.

These systems are widely used in transport, stationary power, backup power, and industrial applications where stable temperature control is required. Water-cooled fuel cells help improve operating efficiency, system durability, and performance consistency under demanding load conditions.

Demand for water-cooled fuel cells is expected to remain strong as hydrogen-powered buses, trucks, trains, marine vessels, and heavy-duty mobility platforms expand. Their suitability for higher power output makes them a preferred option in commercial and industrial hydrogen applications.

By Application

Transport accounted for 41.2% share of the Hydrogen Fuel Cells Market. This dominance is driven by rising adoption of hydrogen fuel cells in buses, trucks, passenger vehicles, trains, forklifts, and marine transport.

Fuel cells are gaining attention in transport because they offer fast refueling, longer driving range, and zero tailpipe emissions. These advantages are especially important for heavy-duty vehicles and fleet operations where battery charging time and payload limits can create operational challenges.

The segment is expected to remain a major demand center as governments and companies invest in hydrogen mobility infrastructure. Growth will be supported by fuel cell electric vehicles, hydrogen refueling stations, clean public transport programs, and decarbonization of commercial fleets.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Region

North America accounted for 40.0% share of the Hydrogen Fuel Cells Market, reaching USD 3.4 billion. The region’s leadership is supported by strong investment in hydrogen infrastructure, fuel cell vehicle programs, clean energy projects, and stationary power applications.

The United States and Canada are key contributors due to active deployment of hydrogen buses, trucks, forklifts, backup power systems, and industrial fuel cell solutions. Demand is also supported by policies focused on clean transport, low-carbon energy, and domestic hydrogen production.

North America is expected to maintain a strong position as hydrogen supply chains, refueling networks, and fuel cell manufacturing capacity continue to expand. Demand will remain supported by transport electrification, industrial decarbonization, and the need for reliable clean power systems.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

North America leads the Hydrogen Fuel Cells Market with 40.0% share in 2025, valued at around USD 3.4 billion, supported by clean energy policies, hydrogen infrastructure investment, fleet deployment, and strong demand from material handling, transport, and backup power. The U.S. remains the main regional driver due to hydrogen hub development and early commercial fuel cell use.

Europe remains important because of hydrogen mobility programs, industrial decarbonization, public transport projects, and strong climate policy support. Asia Pacific is expected to build future demand through Japan, South Korea, China, and India, supported by hydrogen roadmaps, fuel cell manufacturing, and clean transport deployment.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

North America market leadership | +6.8% | North America, 40.0% share in 2025 | Leads global value demand. |

U.S. hydrogen hub development | +5.2% | U.S. | Drives regional growth. |

Canada clean hydrogen and transport projects | +3.6% | Canada | Supports steady expansion. |

Europe hydrogen mobility and industry demand | +3.2% | Germany, France, UK, Netherlands | Builds policy-led growth. |

Asia Pacific fuel cell manufacturing scale | +3.8% | Japan, South Korea, China, India | Supports future demand. |

Go-To-Market and Sales Economics

Hydrogen fuel cells are commercialized through vehicle OEMs, fleet operators, transit agencies, stationary power buyers, electrolyzer partners, hydrogen distributors, and long-term service agreements. Demand is strongest in buses, trucks, rail, backup power, and data-center power. FCEV stock grew 20% in 2025 to almost 130,000 vehicles, led by China trucks and Korea cars.

Sales economics depend on stack durability, fuel price, uptime, service cost, and refueling access. DOE targets include hydrogen production cost of USD 2/kg by 2026, dispensed hydrogen cost of USD 7/kg for heavy-duty vehicles by 2028, and heavy-duty fuel cell system cost of USD 80/kW by 2030.

Commercial traction is improving in fleet and stationary applications. Toyota announced in May 2026 that it plans fuel cell-powered Class 8 trucks for commercial logistics by early 2027, with Hyroad collaboration starting in 2026 and Air Liquide fuel supply for its California fleet. This supports depot-led adoption before mass passenger use.

Risk Factors & Market Barriers

The main barrier is hydrogen availability and cost. IEA reported that global hydrogen demand surpassed 100 Mt in 2025, but low-emissions hydrogen remained close to 1 Mt after 20% growth. New applications still represent a very small share, so fuel cell adoption depends on faster clean hydrogen supply formation.

Infrastructure remains a major commercial risk. IEA reported that announced hydrogen pipeline projects exceed 40,000 km by 2035, but only 9% of this length is operational or has committed investment. This limits refueling confidence, regional fleet expansion, and industrial user conversion in markets without strong hub planning.

Demand certainty is still weak. New offtake agreements for low-emissions hydrogen reached 1.7 Mtpa in 2025, but only one-fifth were firm contractual commitments. This creates financing risk for hydrogen producers, fueling infrastructure owners, and fuel cell suppliers that need visible utilization before scaling manufacturing and service networks.

Revenue Potential Analysis

Revenue Landscape Across

Revenue is spread across fuel cell buses, trucks, rail, marine, forklifts, stationary power, backup systems, distributed generation, electrolyzer-linked projects, and hydrogen fuel services. Ballard reported Q1 2026 revenue of USD 19.4 million, up 26%, with stationary revenue up 775% and rail revenue up 4,472% year over year.

Stationary power and data-center applications are becoming a stronger revenue pool. Bloom Energy reported Q1 2026 revenue of USD 751.1 million, up 130.4%, with product revenue up 208.4%. The company also raised its full-year 2026 revenue guidance to USD 3.4 billion to USD 3.8 billion.

Hydrogen fuel supply is another revenue landscape. Plug Power stated that hydrogen fuel sales increased 22% in Q1 2026, while its fuel margin rate improved by 54 percentage points. Its Georgia, Tennessee, and Louisiana production facilities provide around 40 tons per day of total capacity for internal and commercial demand.

Financial Impact

Hydrogen fuel cells create financial value where fast refueling, long range, high utilization, and payload protection matter more than lowest vehicle purchase cost. Heavy-duty transport, transit fleets, ports, logistics corridors, and backup power are better early markets than private passenger cars because utilization can justify dedicated fueling infrastructure and service support.

Supplier financial impact depends on volume scale, stack cost, service margin, fuel margin, and factory utilization. Ballard ended Q1 2026 with USD 516.8 million in cash, reduced operating expenses by 36%, and improved adjusted EBITDA from negative USD 27.5 million to negative USD 11.4 million, showing better cost discipline.

The strongest financial returns are expected from integrated fuel cell systems, hydrogen fuel supply, stationary power, and fleet-service contracts. IEA reported nearly USD 7 billion in low-emissions hydrogen project capital spending in 2025 and expects nearly USD 10 billion in 2026, supporting the wider fuel cell value chain.

Drivers Impact Analysis

The Hydrogen Fuel Cells Market is driven by rising demand for zero-emission mobility, clean power systems, backup power, heavy-duty transport, hydrogen-powered buses, forklifts, trucks, marine systems, and stationary energy applications. Fuel cells are gaining attention because they produce electricity with water as the main by-product when using hydrogen.

North America leads the market due to strong clean energy investment, hydrogen infrastructure development, fuel cell vehicle programs, and demand from logistics, power backup, and industrial users. The U.S. remains the main regional contributor because of growing hydrogen hubs, clean transport funding, and fuel cell deployment across material handling and stationary power.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for zero-emission transport | +6.5% | North America, Europe, Asia Pacific | Drives core market adoption. |

Growth in hydrogen infrastructure | +5.4% | U.S., Canada, Japan, Germany, South Korea | Supports commercial deployment. |

Demand from heavy-duty vehicles | +4.8% | North America, Europe, China | Builds long-term mobility demand. |

Expansion of backup and stationary power | +3.9% | Data centers, telecom, industrial sites | Adds stable applications. |

Government clean energy support | +3.3% | U.S., Canada, Europe, Japan | Improves investment confidence. |

Restraints Impact Analysis

The market faces restraints from high fuel cell system cost, limited hydrogen refueling infrastructure, high hydrogen production cost, and uncertain long-term economics. Fuel cell systems need expensive catalysts, balance-of-plant components, storage systems, and reliable hydrogen supply.

Another restraint is competition from battery-electric technologies. In passenger cars and light commercial transport, batteries are often more established, while fuel cells are stronger in long-range, high-utilization, and heavy-duty use cases.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High fuel cell system cost | -3.4% | Global manufacturers | Limits faster adoption. |

Limited hydrogen refueling network | -3.0% | North America, Europe, Asia Pacific | Slows vehicle deployment. |

High clean hydrogen production cost | -2.6% | Industrial and mobility users | Affects operating economics. |

Competition from battery-electric systems | -2.2% | Passenger and light-duty transport | Impacts market positioning. |

Storage and safety infrastructure complexity | -1.8% | Hydrogen supply chains | Raises project cost. |

Opportunities Impact Analysis

Opportunities are strong in heavy-duty trucks, buses, forklifts, trains, marine vessels, stationary power, microgrids, data center backup, and industrial power systems. These applications benefit from long operating hours, fast refueling needs, high payload requirements, and clean energy goals.

Higher-value opportunities are also emerging in green hydrogen integration, fuel cell stacks, hydrogen storage systems, electrolyzer-linked fuel cell projects, and distributed power solutions. Companies that reduce cost, improve durability, and secure hydrogen supply can capture stronger long-term demand.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Heavy-duty fuel cell truck adoption | +6.2% | North America, Europe, China | Builds large mobility opportunity. |

Fuel cell buses and fleet vehicles | +5.0% | U.S., Canada, Europe, Japan | Supports public transport demand. |

Stationary power and microgrids | +4.3% | Industrial and remote power users | Adds reliable clean power. |

Fuel cells for data center backup | +3.6% | North America and Europe | Creates premium power demand. |

Green hydrogen-linked fuel cells | +3.0% | Clean energy hubs | Improves sustainability value. |

Challenges Impact Analysis

The main challenge is scaling hydrogen supply and fuel cell manufacturing at competitive cost. The market needs reliable hydrogen production, storage, transport, refueling, and distribution systems before large-scale adoption can accelerate.

Another challenge is improving durability under real operating conditions. Fuel cells used in trucks, buses, industrial sites, and backup systems must handle long duty cycles, temperature changes, vibration, fuel purity issues, and maintenance needs.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Scaling hydrogen supply chains | -3.2% | North America, Europe, Asia Pacific | Limits commercial rollout. |

Reducing fuel cell stack cost | -2.7% | Global fuel cell producers | Affects affordability. |

Improving durability and lifetime | -2.3% | Mobility and stationary systems | Supports customer confidence. |

Building refueling infrastructure | -2.0% | Transport corridors and cities | Determines fleet adoption. |

Ensuring hydrogen purity and safety | -1.6% | Industrial and mobility users | Protects system performance. |

Segment Covered in the Report

By Type

Air-Cooled Type

Water-Cooled Type

By Application

Stationary

Transport

Portable

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward heavy-duty mobility, hydrogen-powered buses, fuel cell trucks, stationary backup power, green hydrogen integration, and modular fuel cell systems. Fuel cells are increasingly positioned for applications where fast refueling, long range, and continuous operation matter.

North America remains the value leader because of strong clean energy funding, hydrogen hub development, and early fuel cell use in logistics and backup power. Europe and Asia Pacific are also expanding through hydrogen mobility policies, industrial decarbonization plans, and public-private infrastructure programs.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Heavy-duty fuel cell mobility expands | +6.0% | North America, Europe, Asia Pacific | Leads future demand. |

Green hydrogen integration strengthens | +5.1% | Clean energy regions | Improves low-carbon value. |

Stationary fuel cell power grows | +4.0% | Data centers, telecom, industrial sites | Adds reliable demand. |

Hydrogen fleet projects increase | +3.4% | U.S., Canada, Europe, Japan | Supports commercial scale. |

Modular fuel cell systems gain use | +2.8% | Industrial and backup power markets | Improves deployment flexibility. |

Investor Type Impact Matrix

Investors should focus on fuel cell companies with strong stack technology, system integration capability, hydrogen partnerships, fleet relationships, and proven durability. Cost reduction, power density, supply security, and infrastructure readiness are key success factors.

Strategic investors can also target fuel cell stack producers, hydrogen storage companies, refueling infrastructure providers, heavy-duty fuel cell vehicle firms, stationary power developers, and green hydrogen project integrators. Companies that connect fuel cell systems with reliable hydrogen supply are better positioned for long-term growth.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Fuel Cell Stack Manufacturers | +5.3% | Global | Expands core fuel cell supply. |

Hydrogen Mobility Companies | +4.4% | North America, Europe, Asia Pacific | Supports transport decarbonization. |

Stationary Fuel Cell Power Providers | +3.7% | Industrial and backup power markets | Builds stable demand. |

Hydrogen Storage and Refueling Firms | +3.1% | Clean transport corridors | Enables commercial deployment. |

Strategic Clean Energy Investors | +2.6% | Global hydrogen economy markets | Funds scale and infrastructure. |

Recent Developments

March 2026: Ballard signed a commercial agreement with New Flyer for 500 FCmove-HD+ fuel cell engines, totaling 50 MW, to power Xcelsior CHARGE FC hydrogen buses in North America.

June 2026: Plug Power completed commissioning of a 5 MW GenEco PEM electrolyzer system at European Energy’s Måde PtX facility in Denmark, supporting operational green hydrogen production in Europe.

June 2026: FuelCell Energy secured USD 49 million in EXIM financing to support U.S.-made fuel cell exports, including five 2.8 MW Energy Blocks for Gyeonggi Green Energy in South Korea.

April 2026: Alstom acquired Cummins’ hydrogen fuel cell activities dedicated to rail, including engineering, product and support capabilities previously linked to hydrogen train systems supplied by Cummins.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Ballard Power Systems

Plug Power

FuelCell Energy

Hydrogenics

ITM Power

PowerCell Sweden AB

Ceres Power

Nel ASA

Air Products and Chemicals

Siemens Energy

Bloom Energy

Bosch

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Energy and Power

Small Wind Turbine Market to Hit USD 17.9 Billion by 2035

Small Wind Turbine Market Size, Share, Analysis By Axis Type (Horizontal Axis Wind Turbines and Vertical Axis Wind Turbines), By Capacity Rating (0 To 5 KW, 6 To 20 KW, and 21-100 KW), By Connectivity (Off-Grid, On-Grid, and Hybrid), By Installation Location (Rooftop/Building-Integrated and Freestanding Tower), By Application (Residential, Commercial, and Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydropower Generation Market to Hit USD 560.9 Billion by 2035

Hydropower Generation Market Size, Share, Analysis By Plant Type (Large Hydropower Plant, Small Hydropower Plant, Pumped Storage Hydropower), By Application (Utility, Industrial, Rural Electrification), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Power Generation Market to Hit USD 2,539.5 Billion by 2035

Power Generation Market Size, Share, Analysis By Type (Conventional/Non-Renewable (Nuclear and Fossil Fuels), Non-Conventional/Renewable (Solar, Wind, Hydro, and Others)), By End-User (Residential, Commercial, Industrial, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Single Phase String Inverters Market to Hit USD 5.1 Billion by 2035

Single Phase String Inverters Market Size, Share, Analysis By Connectivity (On-Grid, Off-Grid), By Power Rating (Below 1 kW, 1 kW to 3 kW, 3 kW to 5 kW, Above 5 kW), By Application (Residential, Commercial), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035