Revenue, 2025

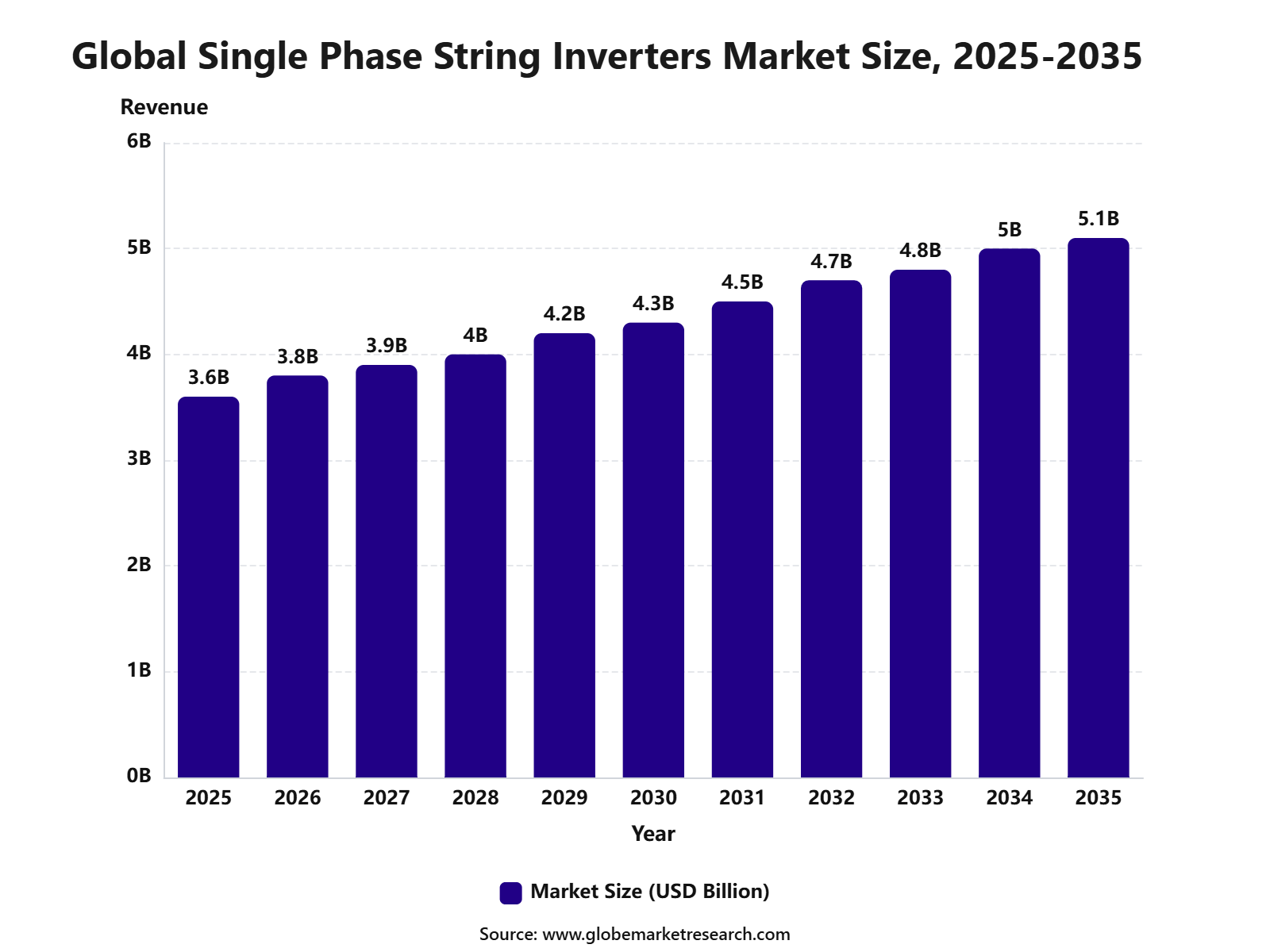

$ 3.6 Bn

Forecast, 2035

$ 5.1 Bn

CAGR, 2025-2035

3.5%

Report Coverage

Global

Market Size and Forecast

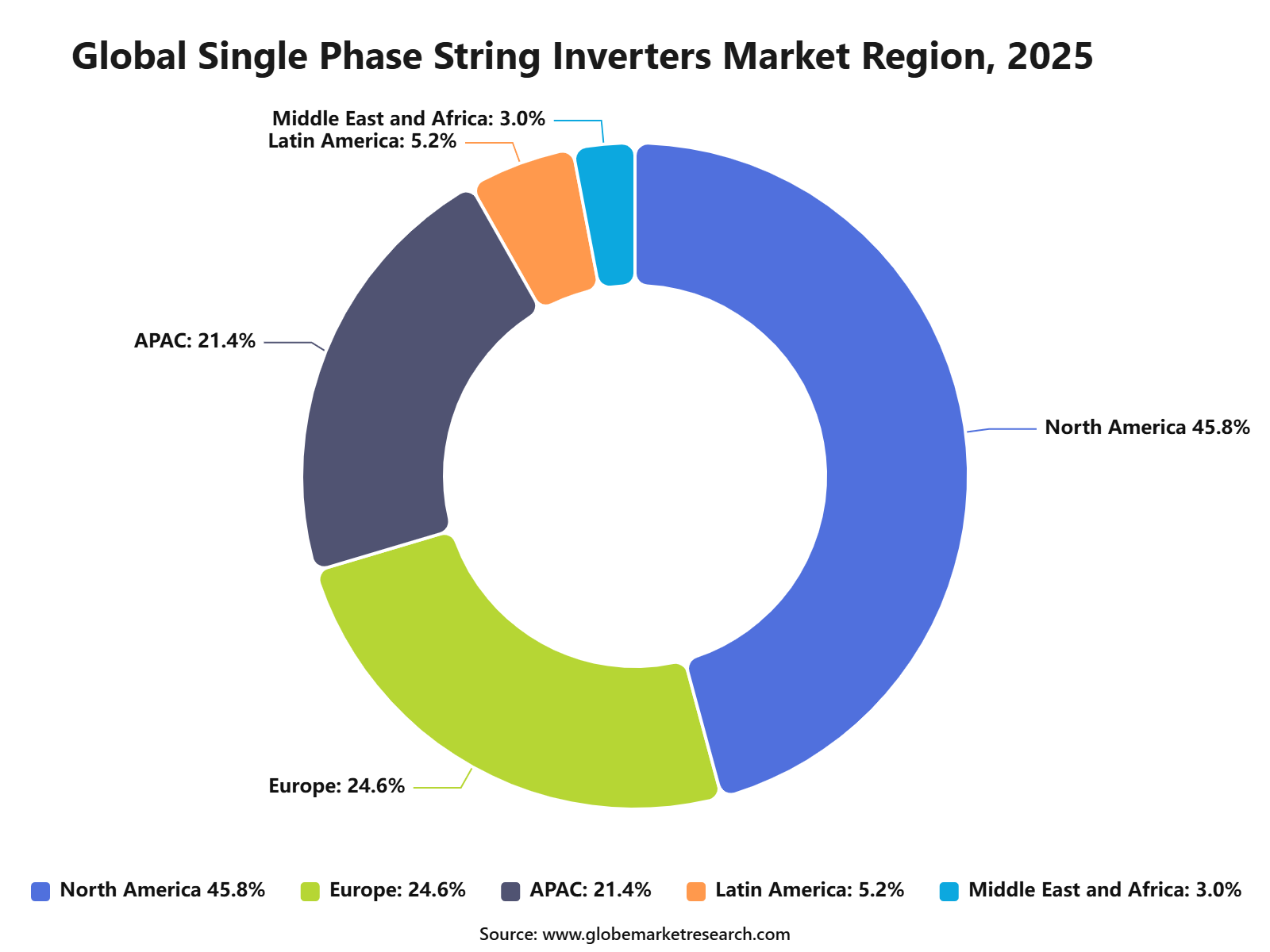

The Global Single Phase String Inverters Market was worth USD 3.6 billion in 2025 and is expected to reach USD 5.1 billion by 2035, growing at a CAGR of 3.5% from 2025 to 2035. Based on this growth rate, the market is estimated to reach around USD 3.8 billion in 2026. North America held the largest regional share of 45.8% in 2025, valued at around USD 1.6 billion, supported by residential solar adoption, rooftop PV installations, net metering programs, and demand for efficient home energy systems.

The Single Phase String Inverters Market includes inverter systems used to convert direct current electricity from solar panels into alternating current electricity for residential and small commercial use. These inverters are widely used in rooftop solar systems, home solar arrays, small business installations, grid-connected PV systems, and distributed energy projects. The market is closely linked with residential solar growth, power conversion efficiency, and smart energy monitoring.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 3.6 Billion |

Projected Revenue, 2035 | USD 5.1 Billion |

CAGR (2025-2035) | 3.5% |

Largest Region | North America (45.8%, USD 1.6 Bn) |

Fastest Growing Region | North America |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

The market outlook remains steady as households and small businesses continue adopting solar power to reduce electricity costs and improve energy independence. Growth can be attributed to rising rooftop solar installations, demand for compact inverter systems, and integration with smart monitoring platforms. The expansion of North American residential solar programs, battery-ready inverter designs, and grid-support features is expected to support long-term market demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

On-grid connectivity led the segment with 59.2% share, supported by strong adoption in residential solar systems, net metering programs, and grid-connected rooftop installations.

Inverters with 1 kW to 3 kW power rating accounted for 45.8% share, driven by their suitability for small residential solar systems, compact rooftop setups, and household energy needs.

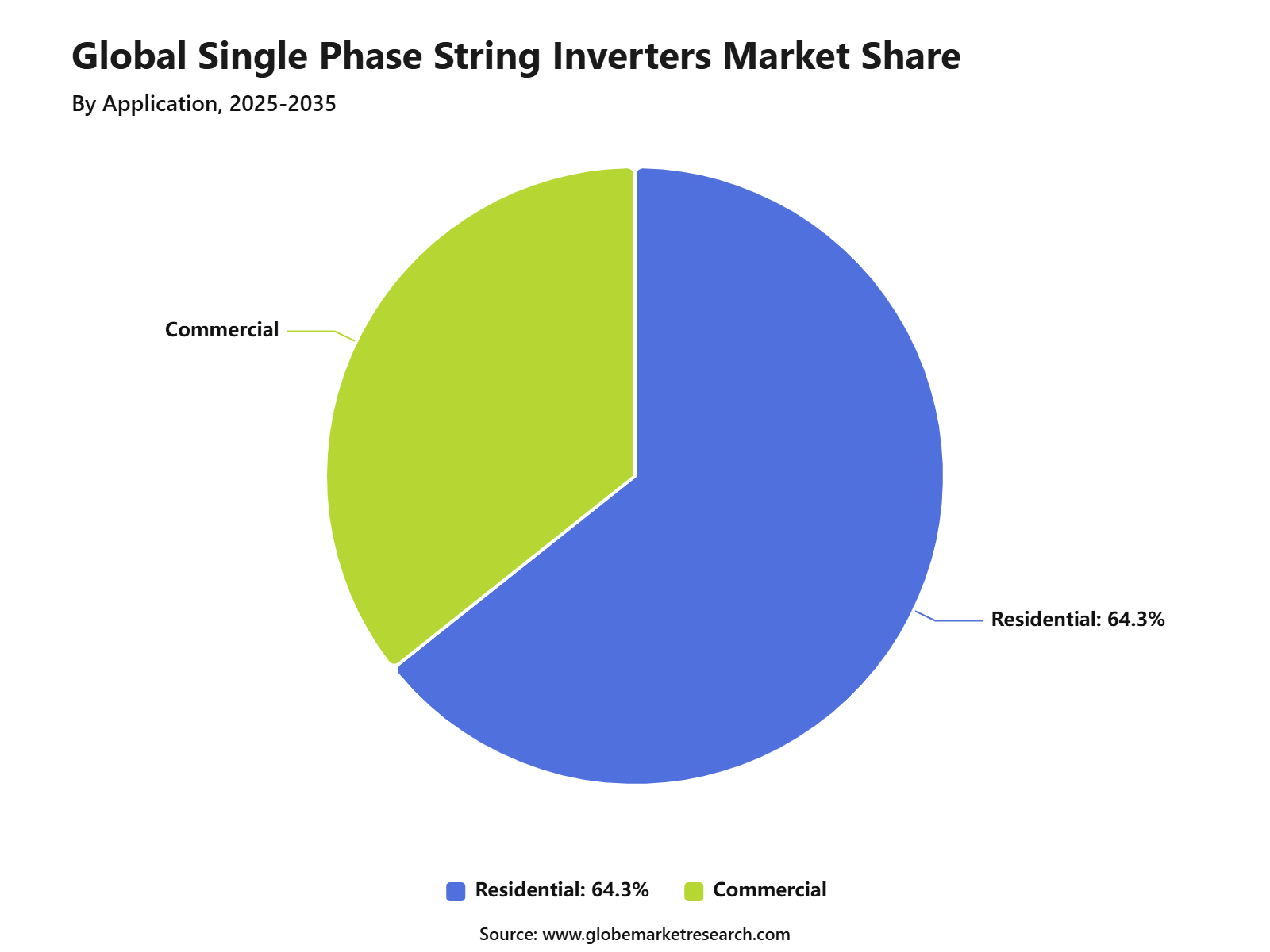

Residential applications held 64.3% share, supported by rising rooftop solar adoption, growing electricity cost concerns, and increasing demand for home-based renewable energy systems.

North America led the single phase string inverters market with 45.8% share, valued at USD 1.6 billion, supported by strong residential solar deployment, supportive clean energy policies, and growing use of grid-connected solar inverter systems.

Top Funding and Investment

Top Investments

Sungrow announced a €230 million investment to establish its first European manufacturing facility at the Wałbrzych Special Economic Zone in Poland. The 65,400 m² plant is planned with annual capacity of up to 20 GW of inverters and 12.5 GWh of energy storage systems, supporting local supply of PV inverters and storage products in Europe.

Sigenergy planned a USD 150 million to USD 200 million India manufacturing push for batteries and inverters. The company was evaluating 30 to 50 acres for a 10 GW to 20 GW capacity unit, with production aimed at domestic demand and exports. The company also indicated a later move into commercial, industrial, and residential channels.

Servotech signed a Rs 400 crore MoU with the Haryana Government to expand renewable energy manufacturing and warehousing operations. The phased investment will support EV chargers, solar products, battery packs, BESS, and power electronics, while the company’s portfolio includes solar inverters, Hybrid and GTI models, for commercial and domestic applications.

SolarYaan commissioned a 1 GW solar inverter manufacturing plant near Ahmedabad, Gujarat. The company stated that its portfolio includes string inverters from 2 kW to 136 kW for residential, commercial, and industrial systems. It also announced plans to add 5 GW hybrid inverter and 5 GWh lithium-ion battery capacity with about INR 1,000 crore investment.

Fujiyama Power Systems planned to use Rs 180 crore from its IPO proceeds to part-fund a new manufacturing facility in Ratlam, Madhya Pradesh. The project is expected to add 2 GW each for solar panels and solar inverters and 2 GWh for lithium-ion batteries, with a total estimated project cost of Rs 272 crore.

Top Funding

Sigenergy raised more than HKD 4.4 billion, around USD 562 million, through its Hong Kong IPO. The company develops home battery storage and commercial solar solutions, and its flagship system combines an inverter, EV DC charging module, and battery pack. By the end of 2025, it had annual design capacity of nearly 360,000 inverters and more than 5.6 GWh of energy storage batteries.

Fujiyama Power Systems launched an Rs 828 crore IPO, including a Rs 600 crore fresh issue and a Rs 228 crore offer for sale. The Noida-based company manufactures rooftop solar ecosystem products, including on-grid, off-grid, and hybrid systems, solar inverters, panels, batteries, and power management units.

SolarSquare raised USD 53 million in Series C funding led by B Capital. The company said the funding would support new city expansion, technology capability, hiring, and scaling of its residential solar platform. SolarSquare reported around 50,000 homes powered and an annual revenue run rate above Rs 1,000 crore, supporting demand for residential rooftop solar hardware, including inverter systems.

Top Acquisitions

IL JIN Electronics India, a subsidiary of Amber Group, signed definitive agreements to acquire a majority stake in Power-One Micro Systems. What it acquired was a Bengaluru-based solar inverter and energy solutions provider with on-grid, off-grid, and hybrid solar inverters ranging from 1 kW to 250 kW, along with UPS systems, BESS, EV chargers, and solar power plant solutions. Power-One had sold more than 7,00,000 products across industrial, residential, data centre, railways, defence, and other segments.

ABB completed the acquisition of Gamesa Electric’s power electronics business from Siemens Gamesa. What it acquired included utility-scale solar inverters, industrial BESS power conversion products, wind converters, around 400 employees, and two converter factories in Madrid and Valencia. The acquired business reported annual revenue of around €145 million for the fiscal year ended September 30, 2025.

By Connectivity

On-grid single phase string inverters accounted for 59.2% share of the Single Phase String Inverters Market. This leading position is supported by strong use in residential rooftop solar systems connected directly to local electricity grids.

The segment is widely preferred because on-grid inverters allow households to use solar power during the day and export excess electricity where net metering or grid export policies are available. These systems also reduce dependence on battery storage, making installations more cost-efficient for homeowners.

Demand is expected to remain strong as residential solar adoption increases across urban and suburban areas. The need for lower electricity bills, cleaner energy use, and easier grid-connected solar installation will continue to support on-grid inverter demand.

By Power Rating

The 1 kW to 3 kW power rating segment held 45.8% share of the Single Phase String Inverters Market. This dominance is driven by its suitability for small residential solar systems, compact rooftops, and households with moderate electricity consumption.

These inverters are commonly used in homes, small apartments, villas, and low-load residential buildings. They offer a practical balance between affordability, output capacity, and ease of installation, making them attractive for first-time solar users.

The segment is expected to maintain strong demand as smaller rooftop solar systems become more common. Growth will be supported by rising household electricity costs, government solar incentives, and increasing consumer interest in affordable clean energy solutions.

By Application

Residential applications accounted for 64.3% share of the Single Phase String Inverters Market. This leading share is supported by high use of single phase electricity connections in homes and the growing adoption of rooftop solar systems for household power needs.

Single phase string inverters are preferred in residential solar projects because they are compact, cost-effective, and easy to install. They help convert direct current from solar panels into usable alternating current for household appliances and grid supply.

The segment is expected to remain the largest application area as homeowners invest in solar energy to reduce monthly power bills and improve energy independence. Demand will also be supported by residential electrification, rooftop space utilization, and wider availability of solar financing options.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Region

North America accounted for 45.8% share of the Single Phase String Inverters Market, reaching USD 1.6 billion. The region’s leadership is supported by strong residential solar adoption, favorable clean energy policies, and rising household interest in distributed power generation.

The United States and Canada are key contributors due to expanding rooftop solar installations, net metering programs, and growing demand for reliable home energy systems. Single phase string inverters are widely used in residential solar projects because they offer efficient power conversion and simple system integration.

North America is expected to maintain a strong position as homeowners continue to invest in grid-connected solar systems. Demand will remain supported by electricity cost savings, solar tax incentives, energy resilience concerns, and ongoing growth in residential clean energy installations.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

North America leads the Single Phase String Inverters Market with 45.8% share in 2025, valued at around USD 1.6 billion, supported by residential solar demand, rooftop PV installations, clean energy incentives, and growing adoption of smart solar systems. The U.S. remains the main regional driver due to strong distributed solar deployment.

Europe remains important because of household solar adoption, energy security concerns, and demand for efficient grid-connected PV systems. Asia Pacific supports future demand through rooftop solar growth, small commercial installations, and rising electricity consumption in urban markets.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

North America market leadership | +1.4% | North America, 45.8% share in 2025 | Leads global value demand. |

U.S. residential solar adoption | +1.0% | U.S. | Drives regional growth. |

Canada rooftop solar expansion | +0.6% | Canada | Supports steady demand. |

Europe energy security and rooftop PV | +0.5% | Germany, UK, France, Italy | Builds stable growth. |

Asia Pacific small-scale solar growth | +0.5% | China, India, Japan, Australia | Supports future scale. |

Go-To-Market and Sales Economics

Single phase string inverters are mainly sold through residential solar installers, EPC firms, electrical distributors, rooftop solar vendors, and battery-ready solar system providers. Demand is supported by distributed solar growth, as the U.S. added 7.8 GW of new solar capacity in Q1 2026 and crossed 6 million cumulative solar installations.

The sales model is shifting from basic conversion hardware to smart energy control, app monitoring, optimizer compatibility, grid-support functions, and storage readiness. SolarEdge reported Q1 2026 revenue from about 50,500 inverters, 2.4 million optimizers, and 331 MWh of batteries, showing higher value from bundled rooftop solar electronics.

Asia and Europe remain important routes for single phase string inverter suppliers because residential rooftop solar is expanding quickly. India reported grid-connected rooftop solar capacity of 30.11 GW as of May 30, 2026, while the EU’s 271 million buildings could host around 2.3 TWp of rooftop solar capacity.

Risk Factors & Market Barriers

The main barrier is policy-linked residential demand volatility. Enphase reported that U.S. sell-through demand for its products fell 48% in Q1 2026 compared with Q4 2025 and 18% compared with Q1 2025, mainly due to tax credit changes and seasonality. Similar shifts can affect single phase string inverter order cycles.

Grid compliance is another key barrier because single phase inverters must meet local interconnection, voltage regulation, safety, and smart inverter rules. The California Energy Commission updates its solar equipment lists three times a month and includes inverters, smart inverters, batteries, meters, and power control systems used for interconnection and incentive support.

Cybersecurity, certification, and product-listing requirements can also slow market access. Australia’s Clean Energy Council states that more than 1,800 inverter and power conversion equipment models are approved, while new secure communication requirements are being introduced for inverters and smart devices connected to energy networks.

Revenue Potential Analysis

Revenue Landscape Across

Revenue is spread across residential rooftop solar, small commercial rooftops, hybrid solar-battery systems, replacement inverters, monitoring subscriptions, power optimizers, installation accessories, and service contracts. Global renewable capacity additions reached 800 GW in 2025, and solar PV provided more than three-quarters of those additions, strengthening inverter demand.

Residential rooftop programs create a strong revenue base for single phase string inverter suppliers. India’s PM Surya Ghar scheme targeted one crore residential rooftop solar households by FY 2026-27, while more than 31 lakh households had already benefited by March 2026. This supports local demand for compliant residential inverter systems.

Australia also shows strong long-term demand for residential inverter upgrades and grid-support functions. CSIRO reported that by June 2025, Australia had 4.2 million rooftop solar systems and 26.8 GW of rooftop capacity connected to local networks, with around 40% of homes generating their own power.

Financial Impact

Single phase string inverters create financial value by converting rooftop solar output, improving self-consumption, enabling export control, supporting battery integration, and reducing household electricity purchases. Their financial role increases when tariffs reward self-use more than exports, making monitoring, optimizer pairing, and storage-ready design important for customer payback.

Supplier profitability depends on product reliability, warranty cost, channel inventory, tariffs, certification expense, installer loyalty, and attachment rates for storage and optimizers. Enphase reported Q1 2026 revenue of USD 282.9 million, non-GAAP gross margin of 43.9%, and 627.6 MWdc of microinverter shipments, showing the pricing strength of advanced residential power electronics.

The strongest financial impact is expected from battery-ready residential inverters, grid-support smart inverters, replacement demand, and solar-plus-storage packages. Residential system pricing averaged USD 3.39/Wdc in Q4 2025 in the U.S., down 1% year over year, so inverter suppliers must protect value through software, service, and reliability.

Drivers Impact Analysis

The Single Phase String Inverters Market is driven by rising residential solar installations, small commercial rooftop solar systems, grid-connected solar adoption, net metering programs, and demand for efficient power conversion. Single phase string inverters are widely used in homes and small buildings because they are cost-effective, compact, and easier to install.

North America leads the market due to strong rooftop solar adoption, household energy cost concerns, supportive clean energy policies, and demand for grid-connected residential solar systems. The U.S. remains the main regional contributor because of its large residential solar base and growing interest in energy independence.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in residential rooftop solar | +1.2% | North America, Europe, Asia Pacific | Drives core inverter demand. |

Rising electricity cost concerns | +1.0% | U.S., Canada, Europe, Australia | Supports solar adoption. |

Expansion of grid-connected solar systems | +0.8% | Developed solar markets | Builds steady demand. |

Demand for compact and efficient inverters | +0.6% | Residential and small commercial users | Improves product adoption. |

Supportive clean energy policies | +0.5% | North America and Europe | Encourages installations. |

Restraints Impact Analysis

The market faces restraints from lower growth in mature rooftop solar regions, pricing pressure, grid connection delays, and competition from microinverters and hybrid inverters. Customers are also comparing inverter options based on monitoring, safety, battery compatibility, and long-term service support.

Another restraint is dependence on solar installation activity. If residential solar demand slows because of financing costs, policy changes, or utility rules, single phase string inverter demand can also weaken.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Pricing pressure from low-cost suppliers | -0.6% | Global inverter markets | Pressures margins. |

Competition from microinverters | -0.5% | North America and Europe | Affects residential share. |

Grid connection and permitting delays | -0.4% | U.S., Canada, Europe | Slows installation timelines. |

Policy and net metering uncertainty | -0.4% | Residential solar markets | Affects buyer confidence. |

Limited battery integration in basic models | -0.3% | Premium solar households | Reduces upgrade appeal. |

Opportunities Impact Analysis

Opportunities are strong in residential rooftop solar, small commercial solar, smart inverters, grid-support functions, solar monitoring systems, and battery-ready inverter platforms. These areas benefit from rising demand for efficient energy management and better solar system visibility.

Higher-value opportunities are also emerging in hybrid-ready systems, digital monitoring, remote diagnostics, safety shutdown features, and inverter replacement demand. Companies that combine reliability, warranty support, and easy installation can capture stronger long-term value.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Residential solar inverter replacement | +1.0% | North America, Europe, Australia | Builds recurring demand. |

Smart inverter adoption | +0.9% | Grid-connected solar markets | Improves grid support. |

Battery-ready inverter platforms | +0.7% | Premium residential users | Supports future upgrades. |

Small commercial rooftop solar | +0.6% | U.S., Canada, Europe, India | Adds installation demand. |

Remote monitoring and diagnostics | +0.5% | Developed solar markets | Improves service value. |

Challenges Impact Analysis

The main challenge is maintaining competitiveness in a price-sensitive market. Single phase string inverter suppliers must offer reliability, efficiency, digital features, safety compliance, and after-sales service without raising costs too much.

Another challenge is adapting to changing grid standards. Utilities and regulators are increasing requirements for voltage control, frequency response, remote shutdown, and grid communication, which requires continuous product upgrades.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining price competitiveness | -0.5% | Global inverter suppliers | Affects profitability. |

Meeting changing grid codes | -0.4% | North America, Europe, Australia | Raises compliance needs. |

Managing warranty and service cost | -0.4% | Residential solar markets | Impacts long-term margins. |

Competing with hybrid inverter systems | -0.3% | Battery-ready solar markets | Affects product positioning. |

Ensuring long-term reliability | -0.3% | Rooftop solar users | Protects brand trust. |

Segment Covered in the Report

By Connectivity

On-Grid

Off-Grid

By Power Rating

Below 1 kW

1 kW to 3 kW

3 kW to 5 kW

Above 5 kW

By Application

Residential

Commercial

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward smart single phase inverters, compact designs, higher efficiency, app-based monitoring, grid-support features, and battery-compatible systems. Residential customers now expect better visibility into solar output, fault alerts, and energy savings.

Replacement demand is also becoming more important as older rooftop solar systems reach inverter replacement age. North America remains the value leader, while Europe and Asia Pacific continue to grow through rooftop solar programs, energy security goals, and household clean energy adoption.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Smart inverter features expand | +1.0% | North America, Europe, Asia Pacific | Supports product upgrades. |

App-based monitoring gains demand | +0.8% | Residential solar users | Improves user experience. |

Battery compatibility becomes important | +0.7% | U.S., Canada, Europe, Australia | Supports energy storage adoption. |

Compact inverter designs improve | +0.5% | Residential rooftops | Eases installation. |

Replacement market grows steadily | +0.5% | Mature solar markets | Adds recurring revenue. |

Investor Type Impact Matrix

Investors should focus on companies with reliable inverter technology, smart monitoring capability, strong installer partnerships, safety compliance, and after-sales service networks. Product reliability, warranty strength, and compatibility with solar-plus-storage systems are key success factors.

Strategic investors can also target inverter manufacturers, solar monitoring software firms, residential solar service providers, component suppliers, and distributed energy platforms. Companies that improve inverter efficiency, serviceability, and grid compatibility are better positioned for long-term growth.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Single Phase String Inverter Manufacturers | +0.9% | Global | Expands rooftop solar supply. |

Smart Inverter Technology Providers | +0.7% | North America, Europe, Asia Pacific | Supports digital energy control. |

Solar Monitoring Software Companies | +0.6% | Residential solar markets | Improves service value. |

Residential Solar Service Providers | +0.5% | North America and Europe | Builds replacement demand. |

Strategic Distributed Energy Investors | +0.4% | Global rooftop solar markets | Funds product and service expansion. |

Recent Developments

June 2026: Enphase launched IQ9N microinverters with GaN technology for U.S. residential solar, expanding its next-generation inverter portfolio after beginning IQ9 commercial microinverter shipments in the United States.

June 2026: Sungrow launched PowerHarbor residential energy storage, supporting up to 1.6x PV-to-battery charging and using PID ZERO technology to protect PV output and improve long-term home energy performance.

January 2026: SolarEdge started shipping U.S.-manufactured residential solar and storage inverters, while first U.S.-made Single SKU residential inverter products were exported to Italy, France and the Netherlands in late 2025.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

APsystems

Canadian Solar

Enphase Energy

Fronius International

Huawei Technologies

INVT Solar

NingBo Deye Inverter Technology

SolarEdge Technologies

Sungrow

UTL Solar

SMA Solar Technology

GoodWe

Other Key Players

Frequently Asked Questions

Related Reports

More in Energy and Power

Small Wind Turbine Market to Hit USD 17.9 Billion by 2035

Small Wind Turbine Market Size, Share, Analysis By Axis Type (Horizontal Axis Wind Turbines and Vertical Axis Wind Turbines), By Capacity Rating (0 To 5 KW, 6 To 20 KW, and 21-100 KW), By Connectivity (Off-Grid, On-Grid, and Hybrid), By Installation Location (Rooftop/Building-Integrated and Freestanding Tower), By Application (Residential, Commercial, and Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydropower Generation Market to Hit USD 560.9 Billion by 2035

Hydropower Generation Market Size, Share, Analysis By Plant Type (Large Hydropower Plant, Small Hydropower Plant, Pumped Storage Hydropower), By Application (Utility, Industrial, Rural Electrification), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Power Generation Market to Hit USD 2,539.5 Billion by 2035

Power Generation Market Size, Share, Analysis By Type (Conventional/Non-Renewable (Nuclear and Fossil Fuels), Non-Conventional/Renewable (Solar, Wind, Hydro, and Others)), By End-User (Residential, Commercial, Industrial, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Fuel Cells Market to Hit USD 70.2 Billion by 2035

Hydrogen Fuel Cells Market Size, Share, Analysis By Type (Air-Cooled Type, Water-Cooled Type), By Application (Stationary, Transport, Portable), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035