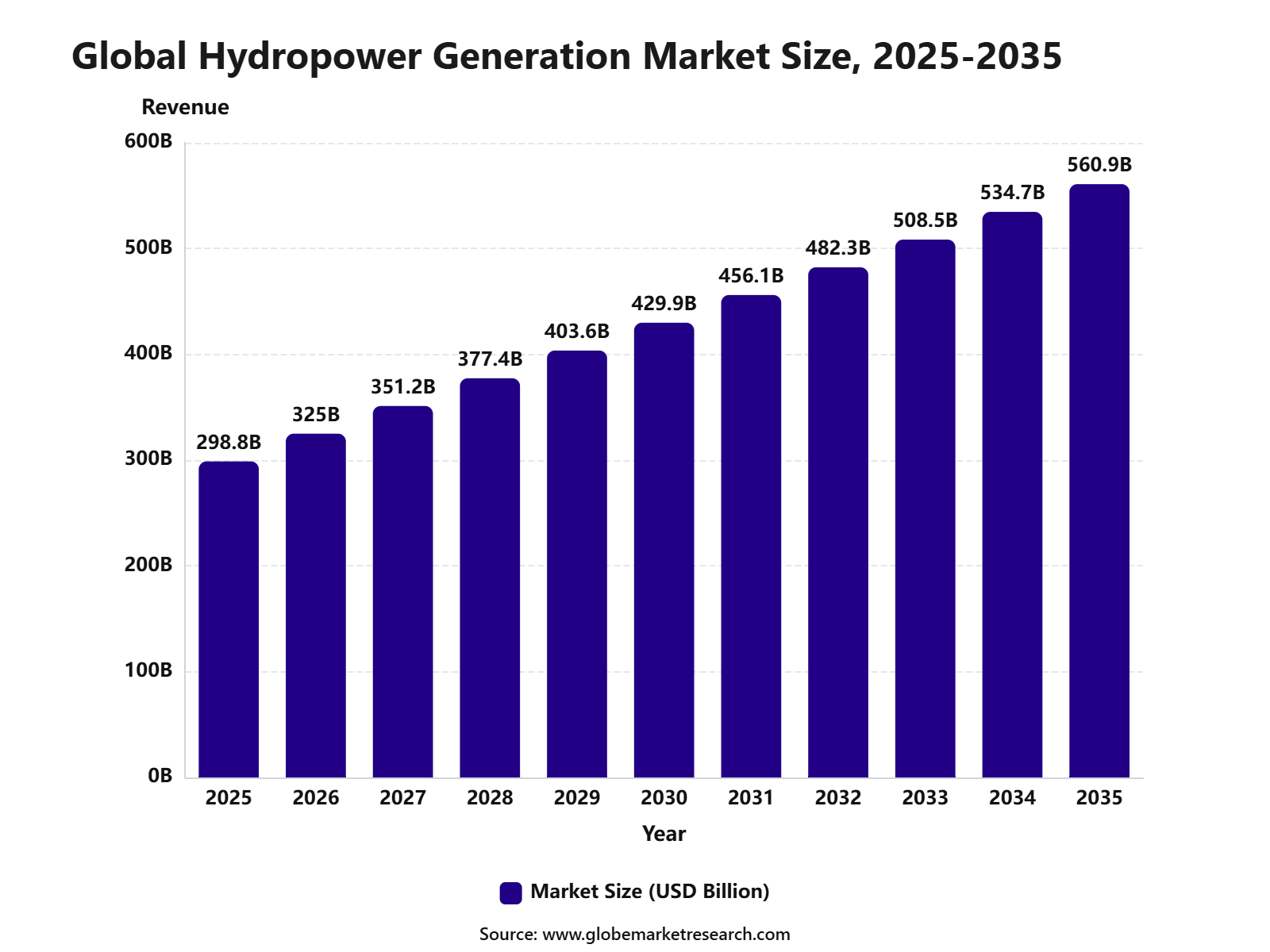

Revenue, 2025

$ 298.8 Bn

Forecast, 2035

$ 560.9 Bn

CAGR, 2025-2035

6.5%

Report Coverage

Global

Market Size and Forecast

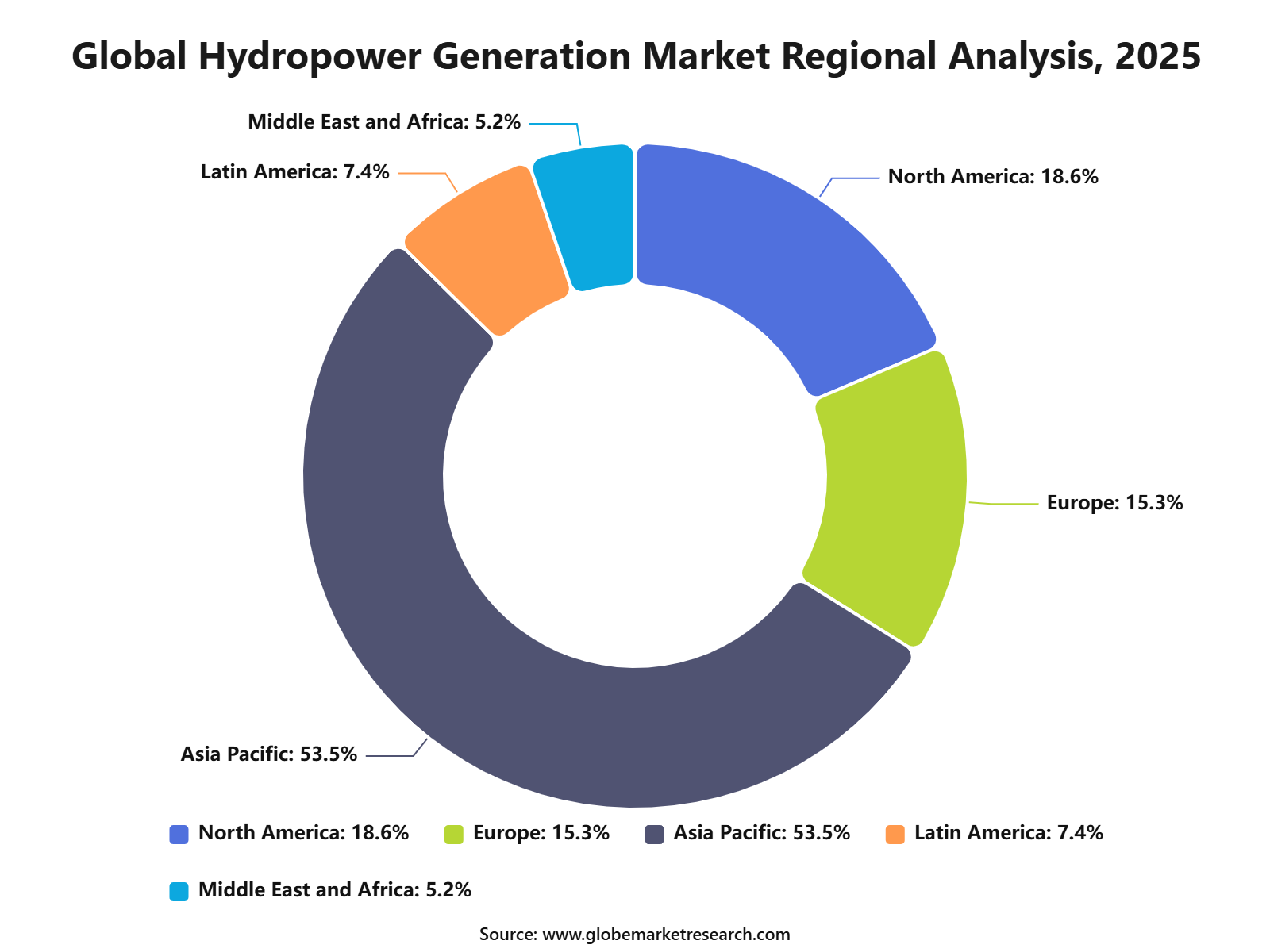

The Global Hydropower Generation Market was worth USD 298.8 billion in 2025 and is expected to reach USD 560.9 billion by 2035, growing at a CAGR of 6.5% from 2025 to 2035. Based on this growth rate, the market is estimated to reach around USD 325.0 billion in 2026. Asia Pacific held the largest regional share of 53.5% in 2025, valued at around USD 159.8 billion, supported by large hydropower capacity, rising electricity demand, river-based power projects, and grid infrastructure expansion.

The Hydropower Generation Market includes electricity produced from flowing or stored water through dams, reservoirs, run-of-river systems, pumped storage plants, and small hydropower projects. It is widely used for baseload power, grid balancing, renewable energy supply, irrigation-linked power systems, and energy storage support. The market is closely linked with clean electricity, water resource management, and long-term power infrastructure.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 298.8 Billion |

Projected Revenue, 2035 | USD 560.9 Billion |

CAGR (2025-2035) | 6.5% |

Largest Region | Asia Pacific: 53.5%, USD 159.8 Bn |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

The market outlook remains positive as countries continue investing in reliable renewable power and flexible grid capacity. Growth can be attributed to rising demand for low-carbon electricity, modernization of existing hydropower plants, and expansion of pumped storage systems. The growth of Asia Pacific energy demand, renewable integration, and large-scale infrastructure projects is expected to support long-term market demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Large hydropower plants led the plant type segment with 66.3% share, supported by their high electricity output, long operating life, grid stability benefits, and strong role in large-scale renewable power generation.

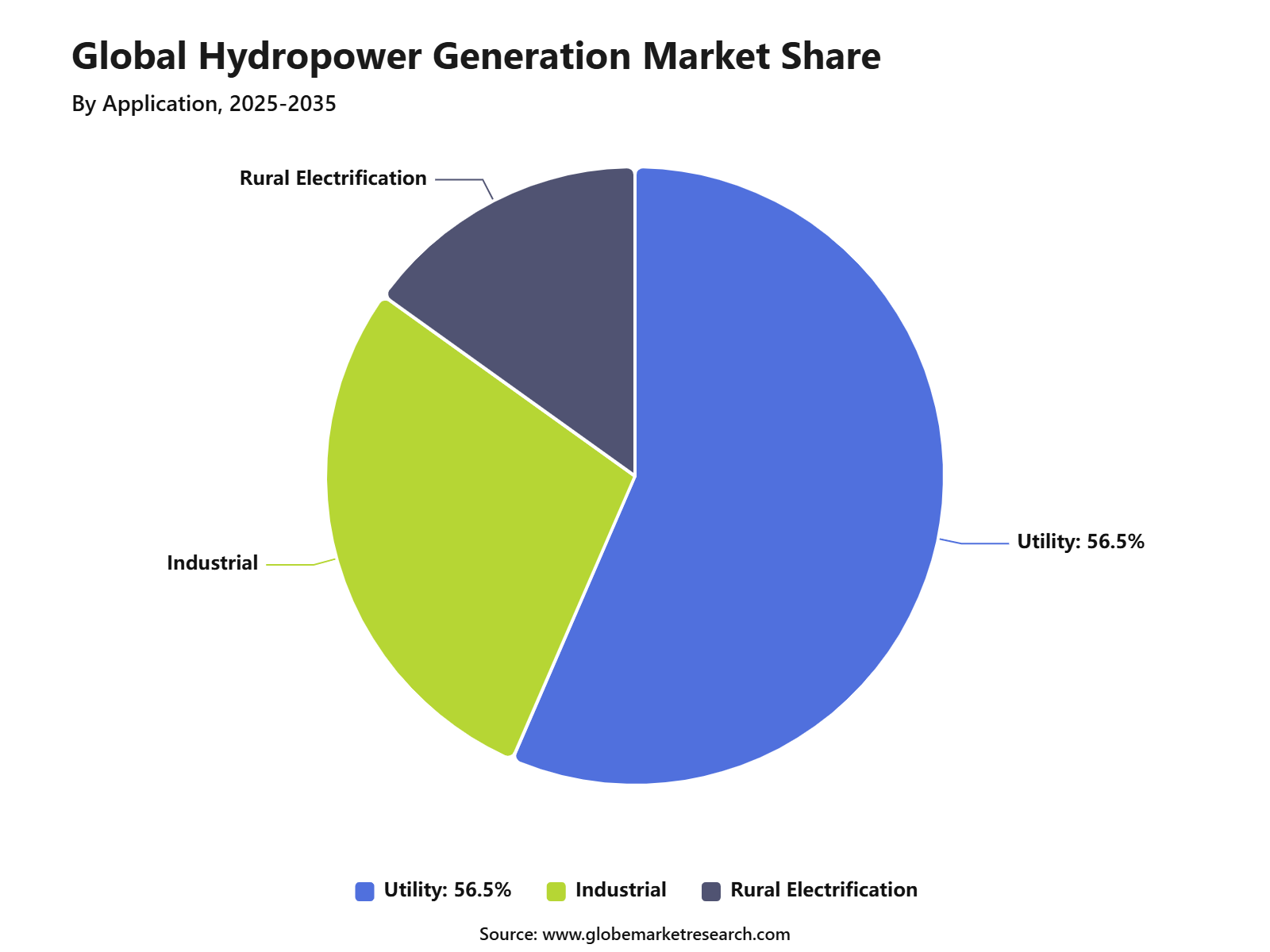

Utility applications accounted for 56.5% share, driven by rising demand for reliable electricity supply, baseload renewable generation, peak load management, and large grid-connected hydropower projects.

Asia Pacific led the hydropower generation market with 53.5% share, valued at USD 159.8 billion, supported by large river systems, expanding electricity demand, strong government investment, and major hydropower capacity across China, India, and Southeast Asia.

Top Funding and Investment

Top Investments

China started construction of the Yarlung Zangbo hydropower project in Tibet with an estimated investment of about 1.2 trillion yuan, around USD 167.8 billion. The project includes five cascade hydropower stations and is planned to supply electricity to other regions while also meeting local demand in Xizang.

Mozambique advanced the USD 6 billion Mphanda Nkuwa hydropower project with World Bank backing. The project is planned as a 1,500 MW hydroelectric plant and is described as southern Africa’s largest hydropower project in 50 years.

Tata Power and Druk Green Power signed commercial agreements for the 1,125 MW Dorjilung Hydroelectric Power Project in Bhutan. The project cost is estimated at ₹13,100 crore, with Tata Power committing ₹1,572 crore in equity investment and 80% of power planned for supply to India.

Tata Power announced an investment of ₹11,000 crore for the 1,800 MW Shirawta pumped hydro storage project in Pune, Maharashtra. The project is expected to be financed through a 70:30 debt-equity structure and construction work is planned to start in July 2026.

SJVN signed an MoU with the Government of Chhattisgarh and CSPGCL for the 1,800 MW Kotpali Pumped Storage Project. The project involves an investment of ₹9,500 crore, is expected to generate about 3,967 million units annually, and may create around 5,000 jobs during construction and development.

Top Funding

Khorlochhu Hydro Power Ltd signed a ₹4,829 crore term loan agreement with Power Finance Corporation. The company is developing the 600 MW Khorlochhu Hydropower Project in Bhutan, estimated to cost about ₹6,900 crore, with an additional ₹950 crore standby credit facility also provided.

The European Investment Bank approved financing of up to €400 million for Energie AG Oberösterreich’s hydropower expansion in Austria. This included €320 million for the Ebensee pumped storage power plant and support for the planned Roitham/Traunfall run-of-river hydropower plant.

The World Bank approved a USD 350 million IDA grant for Malawi’s 358.5 MW Mpatamanga Hydropower Storage Project. The funding is intended to support a major infrastructure project designed to strengthen Malawi’s power supply and economic development.

Top Acquisitions

ENGIE Brasil acquired the Cachoeira Caldeirão and Santo Antônio do Jari hydropower plants in Brazil. What it acquired was a combined 612 MW hydro portfolio, including a 219 MW plant and a 393 MW plant. The implied enterprise value for 100% of the assets was R$2.9 billion.

Thunder Consortium, led by Aboitiz Renewables with Sumitomo Corporation and J-POWER, acquired the 797 MW Caliraya-Botocan-Kalayaan hydropower complex in the Philippines. What it acquired was a hydro and pumped storage asset base serving the Luzon grid, including the Kalayaan pumped-storage units.

By Plant Type

Large hydropower plants accounted for 66.3% share of the Hydropower Generation Market. This leading position is supported by their ability to generate high-volume electricity for national grids, industrial demand centers, and large utility networks.

The segment is widely preferred because large hydropower plants provide stable power output, long operating life, and low operating emissions once installed. These plants are also used for grid balancing, water storage, flood control, and irrigation support in many regions.

Demand for large hydropower plants is expected to remain strong as countries focus on reliable renewable power and long-term energy security. Their role in baseload electricity supply and large-scale clean power generation will continue to support segment growth.

By Application

Utility applications held 56.5% share of the Hydropower Generation Market. This dominance is driven by the large use of hydropower in centralized electricity generation, public grid supply, and national renewable energy planning.

Utilities rely on hydropower because it can provide dependable electricity and help balance variable renewable sources such as solar and wind. Hydropower plants can also support peak-load demand, frequency control, and grid stability when power systems face changing consumption patterns.

The segment is expected to remain the largest application area as electricity demand continues to rise across residential, commercial, and industrial users. Utility-scale hydropower will remain important for countries seeking lower-emission power, energy storage support, and dependable grid operations.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Region

Asia Pacific accounted for 53.5% share of the Hydropower Generation Market, reaching USD 159.8 billion. The region’s leadership is supported by large river systems, strong electricity demand, and continued investment in renewable power infrastructure.

China, India, Japan, Vietnam, Laos, Indonesia, and other regional economies are key contributors to hydropower development. The region benefits from large installed hydropower capacity, rising industrial electricity needs, and government focus on clean energy expansion.

Asia Pacific is expected to maintain its leading position as energy demand, grid expansion, and renewable power targets continue to increase. Large hydropower projects, pumped storage systems, and modernization of existing plants will continue to support regional market growth.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Asia Pacific leads the Hydropower Generation Market with 53.5% share in 2025, valued at around USD 159.9 billion, supported by large electricity demand, extensive river systems, major installed hydropower capacity, and continued investment in pumped storage and renewable grid balancing. China and India remain major regional growth engines.

North America remains important because of large legacy hydropower assets, modernization projects, grid reliability needs, and pumped storage opportunities. Europe supports value growth through hydro refurbishment, climate resilience upgrades, energy security planning, and flexible renewable integration.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +2.5% | Asia Pacific, 53.5% share in 2025 | Leads global value demand. |

China pumped storage and hydro scale | +1.6% | China | Drives regional capacity growth. |

India hydropower and grid demand | +1.2% | India | Supports future expansion. |

North America modernization demand | +0.8% | U.S. and Canada | Adds asset upgrade value. |

Europe hydro refurbishment and flexibility | +0.7% | Norway, France, Italy, Austria | Supports stable growth. |

Go-To-Market and Sales Economics

Hydropower generation is commercialized through utility concessions, IPP auctions, EPC contracts, turbine OEM packages, refurbishment programs, and long-term power purchase agreements. The route-to-market is shifting toward firm renewable power and storage services because global hydropower capacity reached 1,469 GW in 2025 after 28 GW of new additions.

Sales economics are strongest when assets earn revenue from electricity generation, capacity payments, ancillary services, and pumped-storage arbitrage. Pumped storage surpassed 200 GW worldwide in 2025, with 11.7 GW added during the year and 243 GW already under construction, showing that long-duration storage is becoming a key hydro value pool.

OEMs and service providers gain from turbines, generators, controls, digital systems, gates, and modernization work. ANDRITZ recorded Q1 2026 Hydropower order intake of EUR 1,876.8 million, up 229.9%, driven by pumped storage projects, including the 3,000 MW Saidongar project in India.

Risk Factors & Market Barriers

The main barriers are long permitting, large civil works, land acquisition, environmental approvals, sediment management, fish passage, and community acceptance. IHA’s 2026 outlook shows a 1,127 GW global project pipeline, but only 28 GW was commissioned in 2025, indicating that development conversion remains slow.

Hydrology is the most important operating risk. EIA expects U.S. hydropower generation to rise 5% to 259 BkWh in 2026, but still remain 1.8% below the 10-year average because snow drought and early snowmelt have reduced spring and summer water availability in western states.

Grid connection and storage market design also affect investment. IEA reported that more than 2,500 GW of generation, storage, and large-load projects are stuck in connection queues worldwide, while annual grid investment must rise about 50% from today’s USD 400 billion by 2030.

Revenue Potential Analysis

Revenue Landscape Across

Revenue is spread across conventional dams, run-of-river plants, pumped storage, modernization, asset operation, grid balancing, and capacity services. China remains the largest development base, accounting for more than 40% of 2025 global capacity additions, with more than 300 GW under construction, including 218 GW of pumped storage.

South and Central Asia are becoming a stronger revenue landscape as pumped storage expands. India’s CEA roadmap projects all-India storage requirements of 17 GW in 2026-27, 62 GW in 2029-30, and 161 GW by 2034-35, creating demand for PSP development, engineering, turbines, and grid services.

North America remains a stable modernization and generation market. EIA expects U.S. hydropower to represent 6% of electricity generation in 2026, while the Northwest and Rockies region is forecast to produce 125 BkWh, up 17% from 2025 despite water-supply uncertainty.

Financial Impact

Hydropower improves financial performance by providing low-carbon energy, dispatchable capacity, inertia, black-start capability, and storage-backed flexibility. IHA’s 2026 outlook states that rising electricity demand from electrification, industry, artificial intelligence, and data centers is accelerating demand for firm renewable power, which strengthens hydro revenue quality.

Financial returns depend on reservoir inflows, merchant power prices, ancillary-service rules, capex control, and equipment life. Pumped storage can earn from peak shifting and grid support, but projects require long construction cycles. India’s roadmap notes off-stream closed-loop PSP gestation is generally 3.5 to 4 years.

The strongest financial impact is expected from modernization, uprating, pumped storage, hybrid hydro-solar systems, long-duration storage, and capacity-market revenues. ANDRITZ’s Q1 2026 backlog reached EUR 12,367.4 million, while Hydropower revenue rose 8.4%, showing that project execution and services can translate hydro demand into industrial earnings.

Drivers Impact Analysis

The Hydropower Generation Market is driven by rising electricity demand, renewable energy targets, grid stability needs, pumped storage projects, and modernization of aging hydro assets. Hydropower remains important because it provides reliable renewable electricity, long asset life, and flexible power support for grids with more solar and wind capacity.

Asia Pacific leads the market due to large river systems, high electricity demand, strong public infrastructure investment, and major installed hydropower capacity. China, India, Japan, Vietnam, Indonesia, and other regional markets continue to support growth through new projects, upgrades, and pumped storage development.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising renewable electricity demand | +1.9% | Asia Pacific, Europe, North America | Drives core hydropower growth. |

Growth in pumped storage projects | +1.6% | China, India, Japan, Europe | Supports grid flexibility. |

Modernization of aging hydro plants | +1.3% | Developed and mature hydro markets | Improves output and efficiency. |

Need for grid balancing with solar and wind | +1.1% | Renewable-heavy power systems | Adds flexible power value. |

Long operating life of hydropower assets | +0.9% | Global utility markets | Supports long-term investment. |

Restraints Impact Analysis

The market faces restraints from high capital cost, long permitting timelines, environmental concerns, and land acquisition challenges. Large hydropower projects require major civil works, reservoir planning, transmission links, and long construction periods.

Another restraint is climate-related water flow uncertainty. Droughts, changing rainfall patterns, seasonal variability, and river flow changes can affect hydropower output, project economics, and long-term generation reliability.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High upfront project cost | -0.9% | Global hydropower developers | Slows new project investment. |

Long approval and construction timelines | -0.8% | Large hydro projects | Delays capacity addition. |

Environmental and social concerns | -0.7% | River basin regions | Raises project opposition. |

Climate-related water flow risk | -0.6% | Drought-prone markets | Affects generation reliability. |

Land acquisition and resettlement issues | -0.5% | Emerging hydropower markets | Increases execution complexity. |

Opportunities Impact Analysis

Opportunities are strong in pumped storage hydropower, small hydropower, plant refurbishment, turbine upgrades, digital hydro operations, and hybrid renewable systems. These areas benefit from demand for clean, flexible, and dispatchable electricity.

Higher-value opportunities are emerging in grid-scale energy storage using pumped hydro, floating solar on reservoirs, sediment management, smart monitoring, and cross-border hydropower trade. Companies that improve efficiency, safety, and environmental performance can capture stronger long-term value.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Pumped storage hydropower expansion | +1.8% | Asia Pacific, Europe, North America | Builds grid storage value. |

Hydro plant refurbishment | +1.4% | Mature hydro markets | Increases generation output. |

Small and mini hydropower projects | +1.1% | Rural and mountainous regions | Supports distributed power. |

Floating solar-hydro hybrid systems | +0.9% | Reservoir-rich markets | Improves asset utilization. |

Digital monitoring and automation | +0.7% | Utility-owned hydro assets | Improves reliability and maintenance. |

Challenges Impact Analysis

The main challenge is balancing power generation benefits with environmental protection and community impact. Hydropower projects must manage river ecosystems, fish movement, sediment flow, water use, and local livelihood concerns.

Another challenge is maintaining generation reliability under changing climate conditions. Hydropower operators need better forecasting, reservoir management, and flexible operating strategies to handle uneven rainfall and seasonal water availability.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Managing environmental impact | -0.8% | Large river basin projects | Affects project approvals. |

Handling water availability changes | -0.7% | Climate-sensitive regions | Impacts output stability. |

Sedimentation in reservoirs | -0.6% | Older and large hydro assets | Reduces storage and efficiency. |

Ensuring dam safety and maintenance | -0.5% | Mature hydropower fleets | Raises operating responsibility. |

Balancing multi-use water needs | -0.4% | Agriculture, urban, and power systems | Increases planning complexity. |

Segment Covered in the Report

By Plant Type

Large Hydropower Plant

Small Hydropower Plant

Pumped Storage Hydropower

By Application

Utility

Industrial

Rural Electrification

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward pumped storage, hydro modernization, digital dam monitoring, turbine efficiency upgrades, small hydropower, and hybrid renewable projects. Hydropower is increasingly viewed as a stabilizing resource for grids with high solar and wind penetration.

Asia Pacific remains the largest value region because of its strong installed base, rising electricity demand, and continued hydropower investment. Europe and North America support value growth through refurbishment, pumped storage, grid reliability projects, and environmental upgrades.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Pumped storage becomes more important | +1.7% | Asia Pacific, Europe, North America | Supports renewable integration. |

Hydro asset modernization rises | +1.3% | Mature hydropower markets | Improves plant performance. |

Digital dam safety systems expand | +1.0% | Utility and public infrastructure markets | Reduces operational risk. |

Small hydropower gains selective demand | +0.8% | Rural and remote regions | Adds local renewable supply. |

Hybrid hydro-solar projects increase | +0.7% | Reservoir-rich markets | Improves clean power output. |

Investor Type Impact Matrix

Investors should focus on hydropower companies with strong project execution, grid access, dam safety capability, long-term power contracts, and exposure to pumped storage or modernization projects. Water availability, permitting strength, asset condition, and environmental management are key success factors.

Strategic investors can also target pumped storage developers, turbine manufacturers, dam safety technology providers, hydro engineering firms, digital monitoring platforms, and renewable hybrid project developers. Companies that improve flexibility, safety, and generation efficiency are better positioned for long-term growth.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Hydropower Project Developers | +1.4% | Global | Expands renewable power capacity. |

Pumped Storage Developers | +1.2% | Asia Pacific, Europe, North America | Supports grid flexibility. |

Turbine and Generator Manufacturers | +1.0% | Hydropower infrastructure markets | Builds modernization value. |

Dam Safety and Digital Monitoring Firms | +0.8% | Mature and large hydro fleets | Reduces operational risk. |

Strategic Renewable Infrastructure Investors | +0.7% | Global power markets | Funds long-life energy assets. |

Recent Developments

June 2026: Statkraft submitted a licence application for a new Mår power plant in Rjukan, Norway, while its 2025 report confirmed major hydropower upgrade applications and rehabilitation completions.

June 2026: China Three Gorges highlighted Three Gorges Dam expansion and reservoir operation updates, supporting Yangtze economic belt infrastructure, navigation, water regulation and continued hydropower-linked operations across its flagship project base.

March 2026: ANDRITZ received Tata Power’s order for the 1,000 MW Bhivpuri pumped-storage plant in Maharashtra, supplying reversible pump turbines, motor-generators and electromechanical equipment under a low three-digit million-euro contract.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

GE Vernova

Siemens Energy

ANDRITZ Hydro

Voith Hydro

China Three Gorges Corporation

ENERGO-PRO

Toshiba Energy Systems

Bharat Heavy Electricals Limited

Turbine Generator Maintenance Inc.

ABB Ltd.

Statkraft

Mitsubishi Power

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Energy and Power

Small Wind Turbine Market to Hit USD 17.9 Billion by 2035

Small Wind Turbine Market Size, Share, Analysis By Axis Type (Horizontal Axis Wind Turbines and Vertical Axis Wind Turbines), By Capacity Rating (0 To 5 KW, 6 To 20 KW, and 21-100 KW), By Connectivity (Off-Grid, On-Grid, and Hybrid), By Installation Location (Rooftop/Building-Integrated and Freestanding Tower), By Application (Residential, Commercial, and Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Power Generation Market to Hit USD 2,539.5 Billion by 2035

Power Generation Market Size, Share, Analysis By Type (Conventional/Non-Renewable (Nuclear and Fossil Fuels), Non-Conventional/Renewable (Solar, Wind, Hydro, and Others)), By End-User (Residential, Commercial, Industrial, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Single Phase String Inverters Market to Hit USD 5.1 Billion by 2035

Single Phase String Inverters Market Size, Share, Analysis By Connectivity (On-Grid, Off-Grid), By Power Rating (Below 1 kW, 1 kW to 3 kW, 3 kW to 5 kW, Above 5 kW), By Application (Residential, Commercial), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Fuel Cells Market to Hit USD 70.2 Billion by 2035

Hydrogen Fuel Cells Market Size, Share, Analysis By Type (Air-Cooled Type, Water-Cooled Type), By Application (Stationary, Transport, Portable), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035