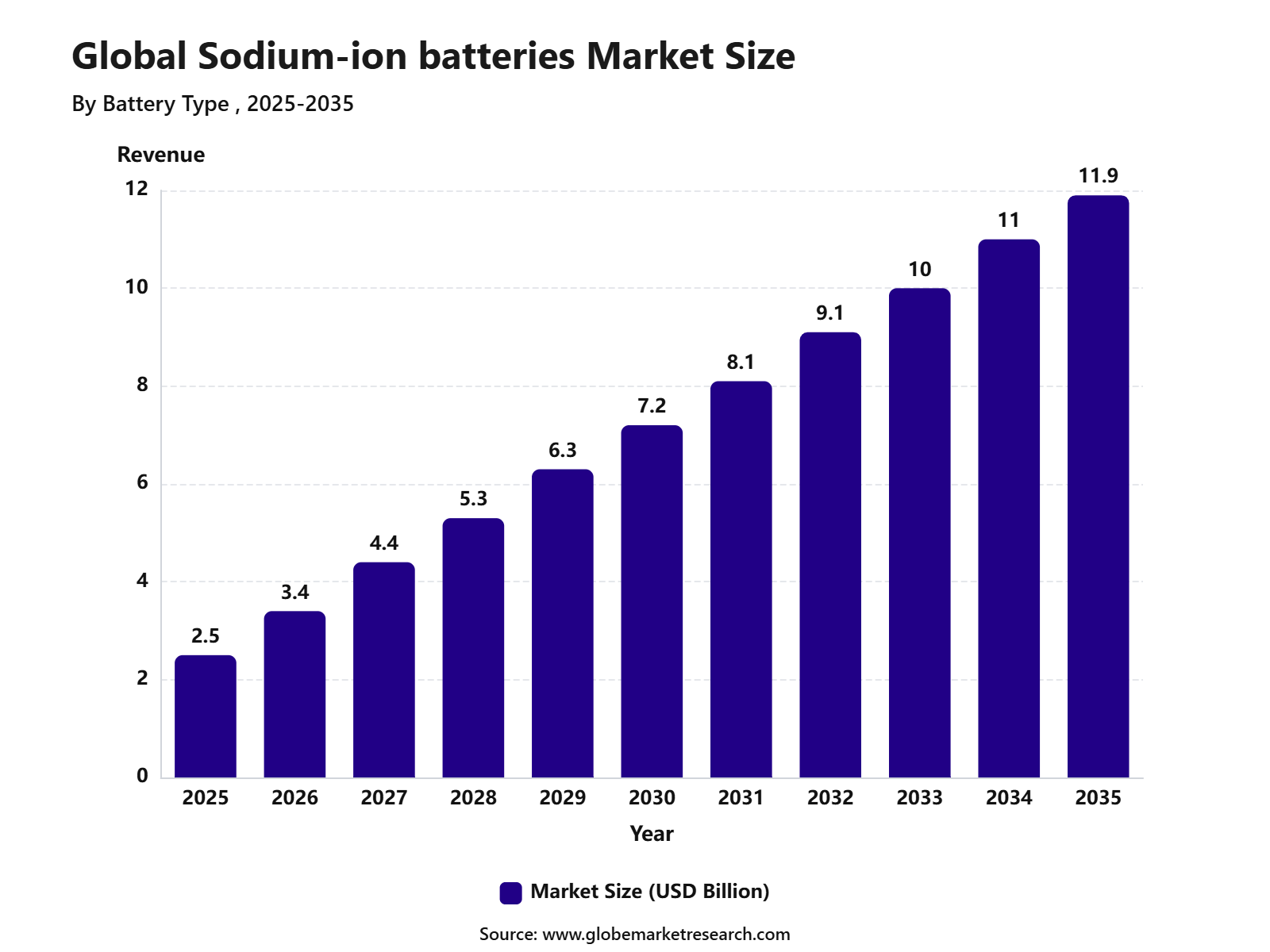

Revenue, 2025

$2.5 Bn

Forecast, 2035

$11.9 Bn

CAGR, 2025-2035

16.9%

Report Coverage

Global

Market Size and Forecast

The Global Sodium-ion Batteries Market reached USD 2.5 billion in 2025 and is expected to grow to USD 11.9 billion by 2035, registering a CAGR of 16.9% from 2025 to 2035. The growth of the market can be attributed to rising demand for low-cost, safe, and sustainable battery technologies for energy storage, electric mobility, renewable integration, and grid backup applications. Sodium-ion batteries are gaining attention as an alternative to lithium-ion batteries because sodium is more abundant, widely available, and less exposed to critical mineral supply constraints.

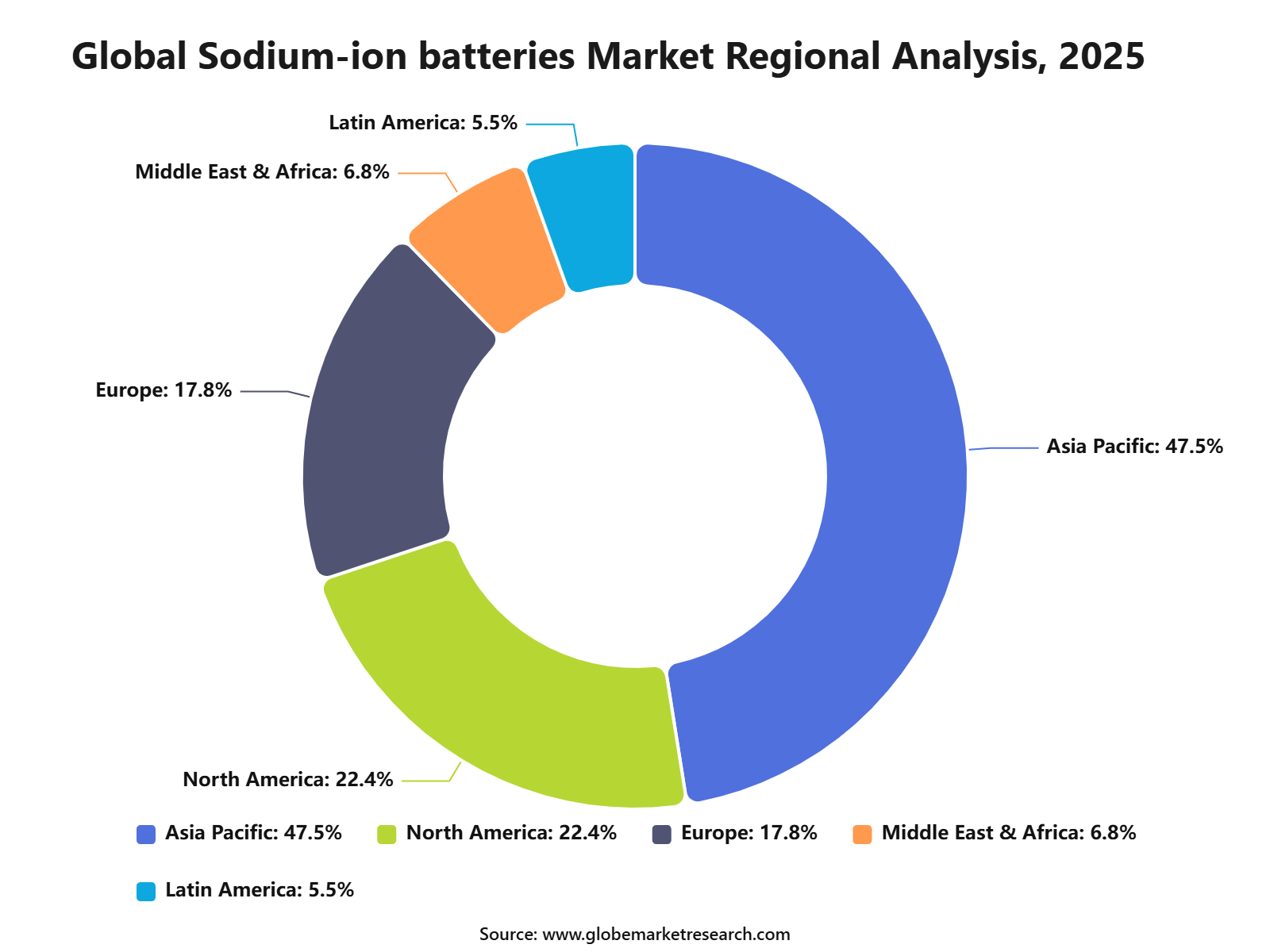

Asia Pacific held the largest regional share of 47.5% in 2025, supported by strong battery manufacturing capacity, growing renewable energy deployment, and rising investment in alternative battery chemistries across China, India, Japan, South Korea, and Southeast Asia. China is leading early commercialization due to its strong cell manufacturing base, large energy storage market, and active development of sodium-ion battery production lines. The region is expected to remain dominant as governments and manufacturers focus on reducing battery material dependency, lowering storage costs, and improving supply chain security.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Sodium-sulfur batteries led the battery type segment with 47.9% share, supported by their strong use in grid storage, renewable energy integration, and long-duration energy storage applications.

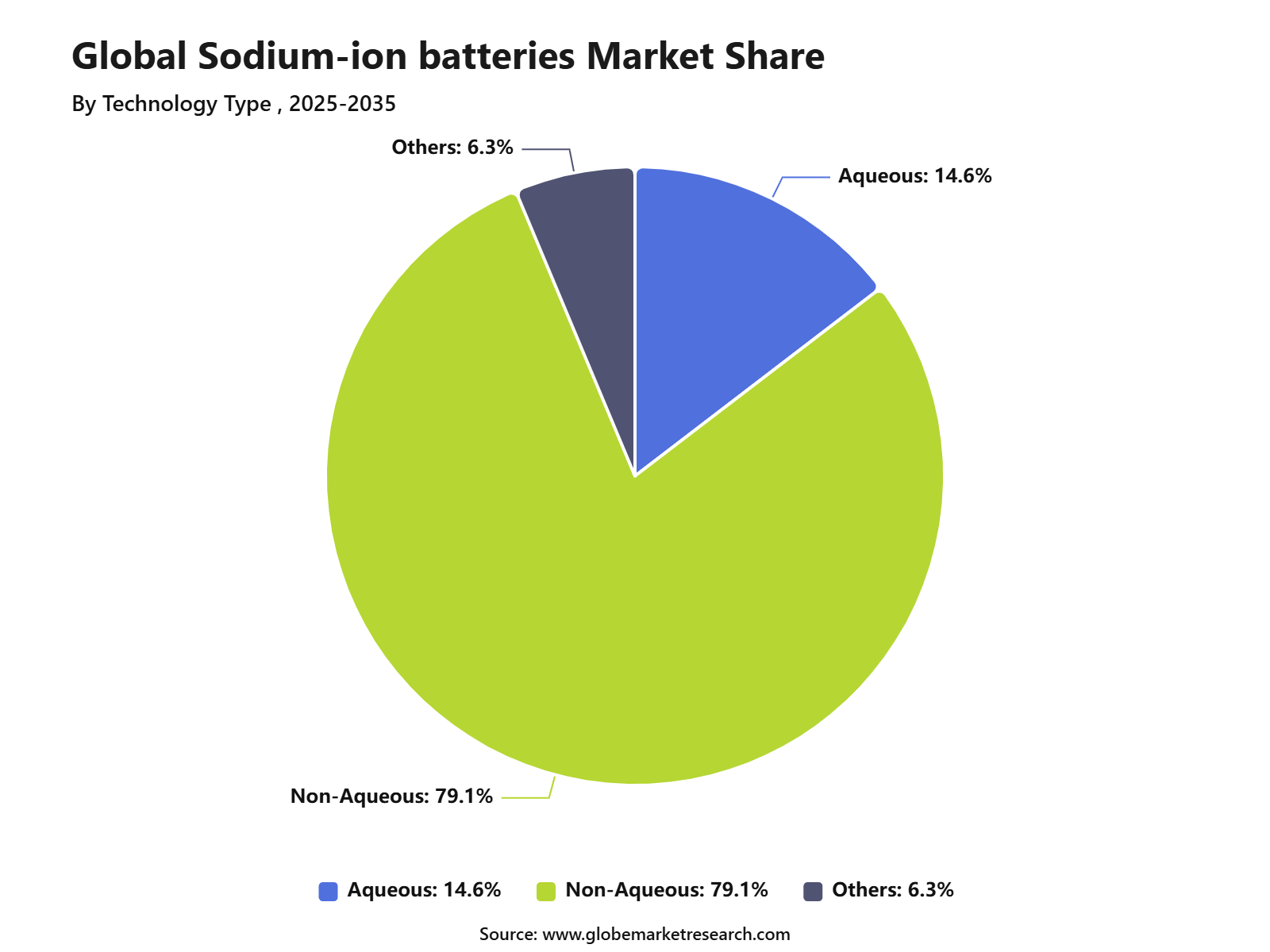

Non-aqueous technology accounted for 79.1% share, driven by higher energy density, better voltage stability, and wider suitability for advanced sodium-ion battery systems.

Cylindrical cells held 49.1% share by form factor, supported by scalable manufacturing, strong mechanical stability, and broad use in energy storage and mobility applications.

Stationary energy storage dominated the application segment with 73.1% share, driven by rising demand for grid balancing, backup power, renewable energy storage, and utility-scale storage systems.

Utilities accounted for 57.2% share by end-user industry, supported by increasing investment in energy storage infrastructure, renewable power integration, and grid reliability solutions.

Asia Pacific held 47.5% share of the sodium-ion batteries market, valued at around USD 1.1875 billion, supported by large-scale battery production, renewable energy expansion, and strong demand for cost-effective energy storage solutions.

Market Overview

The Sodium-ion Batteries Market is gaining attention as battery users seek safer, lower-cost, and less mineral-dependent energy storage solutions. Sodium-ion batteries use more abundant raw materials and avoid lithium, which makes them attractive for stationary energy storage, low-speed electric mobility, backup power, telecom systems, and grid applications. The International Energy Agency stated that sodium-ion batteries may cost around 30% less than lithium iron phosphate batteries and are expected to take a growing share of battery storage, although they are likely to account for less than 10% of EV batteries by 2030.

Market growth is also supported by the rapid expansion of battery storage and electric mobility. The IEA reported that 108 GW of new battery storage capacity was deployed worldwide in 2025, up 40% from 2024, while installed battery storage capacity became 11 times higher than in 2021. EV battery deployment also reached 1.2 TWh in 2025, increasing by almost 30% from 2024 and remaining more than 7 times higher than in 2020. Commercial progress is improving as well, with CATL reporting that its Naxtra sodium-ion battery reached an energy density of 175 Wh/kg, supports a driving range of up to 500 km, and can achieve over 10,000 cycles, showing that sodium-ion technology is moving from research toward practical energy storage and mobility use.

Customer Acquisition Strategy

The sodium-ion batteries market should target customers where cost stability, safety, cold-weather performance, and supply chain diversification matter more than maximum energy density. Key customer groups include grid-scale energy storage developers, renewable power operators, data center backup power users, telecom tower operators, microgrid developers, low-speed EV makers, two-wheeler producers, and cold-climate mobility fleets.

Customer acquisition should be built around pilot projects, performance guarantees, cell safety testing, bankable warranties, and long-term supply agreements. The opportunity is supported by strong battery demand, as EV battery deployment reached 1.2 TWh in 2025, up almost 30% from 2024, while average battery prices declined 8% in 2025. CATL also signed a 60 GWh sodium-ion battery supply deal for energy storage over three years in April 2026, showing that commercial adoption is moving from testing to large-volume supply.

Tariff Impact

In the U.S., Section 301 actions raised tariffs on battery parts for non-lithium-ion batteries to 25% in 2024, while lithium-ion non-EV batteries are scheduled to face a 25% tariff in 2026. For sodium-ion batteries, the actual impact will depend on product classification, country of origin, and whether the imported item is treated as a finished battery, battery pack, component, or input material. Higher duties may increase short-term landed costs for cell makers, pack assemblers, and energy storage integrators, especially where imported equipment, separators, current collectors, electrolytes, or China-linked cell supply are still used.

At the same time, tariffs may support domestic and regional production of sodium-ion cells, cathode materials, anodes, electrolytes, and battery packs across North America, Europe, and India. Sodium-ion batteries are attractive because they reduce dependence on lithium and may cost around 30% less than LFP batteries, although they are expected to account for less than 10% of EV batteries by 2030. The impact is important as global battery storage deployment reached 108 GW of new capacity in 2025, up 40% from 2024.

Battery Type Analysis

Sodium-sulfur batteries led the battery type segment with a 47.9% share in 2025. Growth was supported by their suitability for stationary storage, renewable power balancing, peak load management, and grid support applications. Their use is stronger in large-scale storage systems where battery weight is less important than storage duration, reliability, and operating stability.

The segment also benefited from rising demand for non-lithium battery chemistries that use more abundant raw materials. Sodium and sulfur are widely available, which supports interest in sodium-sulfur batteries for cost-sensitive and large energy storage projects. However, traditional sodium-sulfur batteries require high operating temperatures, so safety, insulation, and system design remain important for wider adoption.

Technology Type Analysis

Non-aqueous technology held the leading position with a 79.1% share in 2025. Growth was supported by its ability to provide higher voltage, better energy density, and stronger electrochemical performance compared with many aqueous systems. This made non-aqueous batteries more suitable for applications that require compact energy storage, longer operating life, and improved power delivery.

The segment’s dominance was also supported by its use across advanced rechargeable battery systems. Non-aqueous electrolytes are commonly used where energy performance and cell stability are key requirements. As battery developers continue improving electrolyte safety, thermal performance, and cycle life, non-aqueous technology is expected to remain important across stationary storage and mobility-linked battery applications.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFForm Factor Analysis

Cylindrical cells accounted for a 49.1% share in 2025. Growth was supported by mature production processes, high mechanical strength, scalable manufacturing, and strong use in electric mobility, power tools, consumer electronics, and modular battery packs. Their standard shape also supports automated production and easier quality control.

The segment gained further support from the need for reliable and repeatable battery formats. Cylindrical cells are preferred in many applications because they offer structural stability and efficient thermal behavior when arranged properly in packs. These advantages make them suitable for high-volume manufacturing where safety, consistency, and cost control are important.

Application Analysis

Stationary energy storage led the application segment with a 73.1% share in 2025. Growth was driven by rising renewable energy integration, grid balancing needs, backup power demand, and utility-scale storage deployment. Battery systems are increasingly being used to store solar and wind power and release it when electricity demand is higher.

The segment also benefited from growing investment in grid flexibility. Stationary batteries help utilities manage frequency response, peak shaving, renewable curtailment, and power reliability. As electricity systems add more variable renewable power, stationary energy storage is becoming a core part of modern grid infrastructure.

End-User Industry Analysis

Utilities dominated the end-user industry segment with a 57.2% share in 2025. Growth was supported by rising grid modernization needs, renewable power integration, energy storage mandates, and demand for reliable power supply. Utilities use battery storage to improve grid stability, reduce renewable energy waste, and support electricity delivery during peak demand periods.

The segment is also gaining strength as power systems shift toward cleaner and more flexible generation. Battery storage allows utilities to manage short-term supply gaps, improve resilience, and reduce pressure on transmission networks. This makes utilities the largest and most important end-user group for sodium-based and stationary battery storage systems.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape is expected to develop first across stationary energy storage, renewable energy integration, telecom backup, industrial storage, data centers, microgrids, and short-range electric mobility. These applications are suitable because they value safety, cost stability, raw material availability, and operating performance more than maximum driving range. CATL signed a three-year agreement to supply 60 GWh of sodium-ion batteries to Beijing HyperStrong for energy storage systems, showing that large commercial offtake is beginning to appear in the sector.

Electric mobility still offers opportunity, but sodium-ion batteries are likely to enter through selected use cases first. These include small EVs, city vehicles, two-wheelers, low-speed vehicles, and hybrid battery packs designed to reduce cold-weather range loss. IEA noted that sodium-ion batteries can retain around 90% of nominal capacity at temperatures as low as minus 40°C, which gives them a clear advantage in cold regions. This makes the technology commercially relevant for markets where winter performance and safety are important purchasing factors.

Financial Impact

The financial impact can be positive for suppliers that combine low-cost materials with reliable manufacturing and strong customer validation. Sodium-ion batteries reduce exposure to lithium and graphite price volatility, which can improve procurement stability for energy storage developers and fleet operators. However, financial returns may remain uneven until production scale improves, supply chains mature, and customer qualification cycles shorten. Companies with integrated cell design, stable material supply, and regional assembly capacity are likely to achieve better economics than suppliers selling early-stage cells without system support.

The strongest financial upside is expected where sodium-ion batteries reduce total system cost instead of competing only on cell energy density. Stationary storage, data center backup, cold-climate storage, and grid-balancing applications can benefit because space and weight are less restrictive than in passenger EVs. IEA reported that EV battery deployment could reach almost 3 TWh by 2030 under stated policy and current policy scenarios, showing the scale of battery demand that alternative chemistries may support over time. For sodium-ion producers, the key financial priority will be moving from pilot supply to bankable, warranty-backed commercial contracts.

Technology Adoption Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Non-aqueous sodium-ion technology | +3.8% | Asia Pacific, Europe, North America | Enhances battery stability. |

Sodium-sulfur battery systems | +3.5% | Utilities and grid storage users | Supports large-scale storage. |

Advanced cathode materials | +3.1% | China, Japan, South Korea, U.S. | Improves energy output. |

Battery management systems | +2.7% | Global | Improves safety and life. |

Scalable cell manufacturing | +2.5% | Asia Pacific, Europe, North America | Supports commercial rollout. |

Investment Opportunity Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Stationary storage battery production | +4.0% | Asia Pacific, Europe, North America | Offers strong growth. |

Sodium-ion cell manufacturing | +3.6% | China, India, Japan, South Korea | Builds supply capacity. |

Utility-scale storage projects | +3.4% | Global | Supports grid reliability. |

Advanced material development | +2.9% | Asia Pacific, Europe, U.S. | Improves battery performance. |

Battery recycling and lifecycle services |

Regional Analysis

Asia Pacific led the Sodium-ion Batteries Market with 47.5% share, contributing around USD 1.1875 billion in 2025. The region benefits from strong battery manufacturing capacity, large renewable energy deployment, rising grid storage demand, and strong participation from China, Japan, South Korea, and India. The growth of Asia Pacific is also supported by expanding supply chains for battery materials, cell manufacturing, and energy storage system integration. The region is expected to remain the leading market as sodium-ion battery commercialization improves and demand rises across utilities, renewable energy developers, data centers, and industrial users.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFSegment covered in the Report

By Battery Type

Sodium-Sulfur Batteries

Sodium-Salt Batteries

Sodium-Air Batteries

Others

By Technology Type

Aqueous

Non-Aqueous

Others)

By Form Factor

Cylindrical Cells

Prismatic Cells

Pouch Cells

By Application

Stationary Energy Storage

Transportation

Industrial Backup Power

Consumer Electronics

Others

By End-User Industry

Utilities

Automotive

Industrial

Consumer Electronics

Telecommunications

Others

By Region

Asia Pacific

North America

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for low-cost battery chemistry | +4.4% | Asia Pacific, Europe, North America | Reduces battery cost pressure. |

Growing need for stationary energy storage | +4.0% | China, India, Europe, U.S. | Drives grid storage adoption. |

Lower dependence on lithium and cobalt | +3.6% | Global | Improves raw material security. |

Expansion of renewable energy integration | +3.2% | Asia Pacific, Europe, Middle East | Supports clean energy storage. |

Increasing investment in battery manufacturing | +2.9% | China, India, Japan, South Korea | Strengthens production capacity. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Lower energy density than lithium-ion batteries | -2.3% | EV and portable electronics markets | Limits premium adoption. |

Early-stage commercial scale-up | -2.0% | Global | Slows mass deployment. |

Limited supply chain maturity | -1.7% | North America, Europe, emerging Asia | Restricts production growth. |

Performance limitations in high-end EVs | -1.5% | Automotive markets | Reduces advanced vehicle use. |

Lack of standardization | -1.2% | Global | Delays customer acceptance. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in grid-scale energy storage | +4.2% | Asia Pacific, Europe, North America | Creates strong demand. |

Adoption in low-speed electric vehicles | +3.5% | China, India, Southeast Asia | Supports affordable mobility. |

Expansion in telecom and backup power | +3.1% | Global | Builds steady demand. |

Development of non-aqueous battery technology | +2.8% | Asia Pacific, Europe, U.S. | Improves battery performance. |

Recycling and safer battery chemistry | +2.5% | Europe, North America, Japan | Supports sustainable adoption. |

Recent Developments

April 2026: CATL signed a major three-year agreement to supply 60 GWh of sodium-ion batteries to Beijing Hyper Strong Technology for energy storage systems. This development shows that sodium-ion batteries are moving from pilot-scale testing toward commercial energy storage deployment.

February 2026: CATL and Changan launched the world’s first mass-production sodium-ion passenger vehicle. CATL’s Naxtra sodium-ion battery offers up to 175 Wh/kg energy density, supports a driving range of more than 400 km, and maintains over 90% capacity retention at minus 40°C..

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 2.5 Billion |

Forecast Revenue (2035) | USD 11.9 Billion |

CAGR (2025-2035) | 16.9% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Battery Type (Sodium-Sulfur Batteries, Sodium-Salt Batteries, Sodium-Air Batteries, Others), By Technology Type (Aqueous, Non-Aqueous, Others), By Form Factor (Cylindrical Cells, Prismatic Cells, Pouch Cells), By Application (Stationary Energy Storage, Transportation, Industrial Backup Power, Consumer Electronics, Others), By End-User Industry (Utilities, Automotive, Industrial, Consumer Electronics, Telecommunications, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Aquion Energy, Faradion Limited, HiNa Battery Technology Co., Ltd, Ben'an Energy Technology (Shanghai) Co., Ltd, AMTE Power plc, Natron Energy, Inc., Tiamat Energy, Jiangsu Zhongna Energy Technology Co., Ltd., Contemporary Amperex Technology Co. Limited (CATL), Li-FUN Technology Corporation Limited, BLUETTI Power Inc., Indigenous Energy Storage Technologies Pvt. Ltd. (Indi Energy), Altris AB, NEI Corporation, Blackstone Technology GmbH |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Aquion Energy

Faradion Limited

HiNa Battery Technology Co., Ltd

Ben'an Energy Technology (Shanghai) Co., Ltd

AMTE Power plc

Natron Energy, Inc.

Tiamat Energy

Jiangsu Zhongna Energy Technology Co., Ltd.

Contemporary Amperex Technology Co. Limited (CATL)

Li-FUN Technology Corporation Limited

BLUETTI Power Inc.

Indigenous Energy Storage Technologies Pvt. Ltd. (Indi Energy)

Altris AB

NEI Corporation

Blackstone Technology GmbH

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Carbon Capture Chemicals Market Size to Reach USD 78.0 Billion by 2035

Carbon Capture Chemicals Market By Chemical Type (Amines, Carbonates, Ammonia-based Solvents, Ionic Liquids, Solid Sorbent Chemicals, Others), By Absorption Type (Chemical Absorption, Physical Absorption), By End-Use Industry (Oil and Gas, Power Generation, Chemical and Petrochemical, Cement, Iron and Steel, Others), By Application (Post-combustion Capture, Pre-combustion Capture, Industrial Gas Separation, Direct Air Capture, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Bio-based Chemicals Market Size to Hit USD 296.7 Bn by 2035

Bio-based Chemicals Market By Product Category (Platform Chemicals, Polymers for Plastics, Paints, Coatings, Inks and Dyes, Surfactants, Cosmetics and Personal Care Products, Adhesives, Man-made Fibers, Others), By Application (Industrial, Agricultural, Pharmaceutical, Others), By Source (Plant-based, Animal-based, Microbial-based, Waste-based), By End Use (Chemical Manufacturing, Agriculture, Food and Beverage, Personal Care, Pharmaceuticals, Automotive), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Processing Chemicals Market Size to Hit USD 14.6 Billion by 2035

Hydrogen Processing Chemicals Market By Chemical Type (Catalysts, Adsorbents, Solvents, Corrosion Inhibitors, Scavengers, Others), By Function (Reforming Chemicals, Purification Chemicals, Hydroprocessing Chemicals, Gas Treatment Chemicals, Corrosion Control Chemicals, Others), By Process (Steam Methane Reforming, Hydrocracking, Hydrotreating, Pressure Swing Adsorption, Water-Gas Shift Reaction, Others), By End Use (Refineries, Ammonia Production, Methanol Production, Petrochemicals, Clean Hydrogen Plants, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Electrolyte Chemicals Market to Cross USD 49.4 Billion by 2035

Electrolyte Chemicals Market By Battery Type (Lithium-ion Electrolytes, Lead-acid Electrolytes, Flow Battery Electrolytes, Others), By Electrolyte Form (Liquid Electrolytes, Gel, Solid-State Electrolytes), By Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, Industrial and Motive Batteries, Others), By Product Type (Lithium-Based Electrolytes, Sulfide-Based Electrolytes, Polymer-Based Electrolytes, Oxide-Based Electrolytes, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035