Revenue, 2025

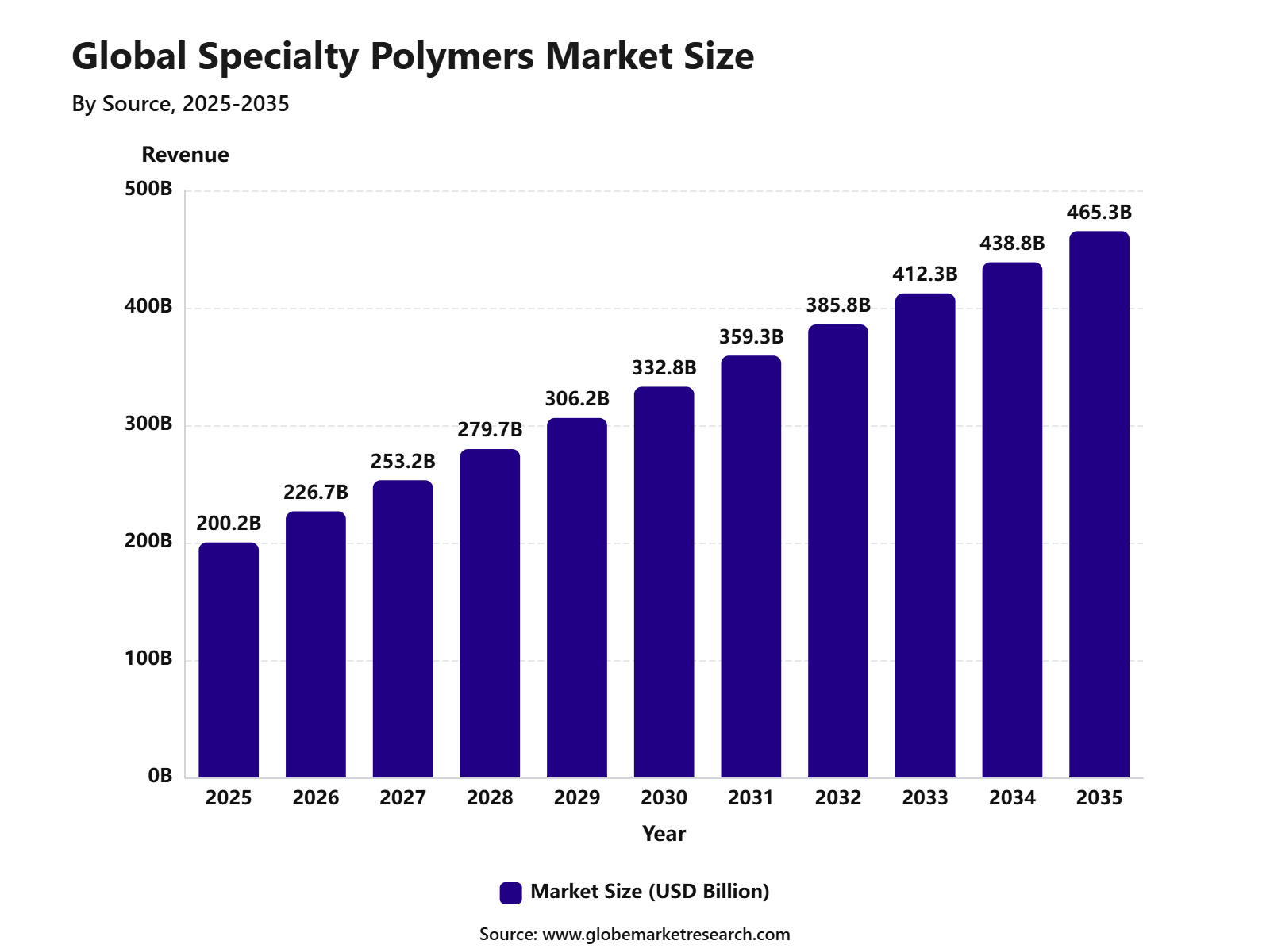

$ 200.2 Bn

Forecast, 2035

$ 465.3 Bn

CAGR, 2025-2035

8.8%

Report Coverage

Global

Market Size and Forecast

The Global Specialty Polymers Market was worth USD 200.2 billion in 2025 and is expected to reach USD 465.3 billion by 2035, growing at a CAGR of 8.8% from 2025 to 2035. Asia Pacific held the largest regional share of 43.4% in 2025, supported by strong plastics processing, expanding electronics manufacturing, rising automotive production, and growing demand for high-performance materials across China, India, Japan, South Korea, and Southeast Asia.

The Specialty Polymers Market includes advanced polymer materials designed to deliver superior heat resistance, chemical resistance, strength, flexibility, durability, and processing performance. These polymers are widely used in automotive components, electrical and electronics, medical devices, packaging, construction materials, coatings, adhesives, aerospace parts, and industrial applications. The market is closely linked with material innovation, lightweight engineering, advanced manufacturing, and performance-based product development.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market outlook remains strong as industries continue to replace conventional materials with lightweight, durable, and application-specific polymer solutions. Growth can be attributed to rising demand from electric vehicles, semiconductors, healthcare products, sustainable packaging, and high-performance industrial components. The expansion of recyclable polymers, bio-based formulations, and specialty engineering plastics is expected to support long-term market demand.

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 200.2 Billion |

Forecast Revenue (2035) | USD 465.3 Billion |

CAGR (2025-2035) | 8.8% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Key Market Insights

Synthetic specialty polymers led the source segment with 61.2% share, supported by controlled performance properties, consistent quality, and wide use across industrial, automotive, packaging, and electronic applications.

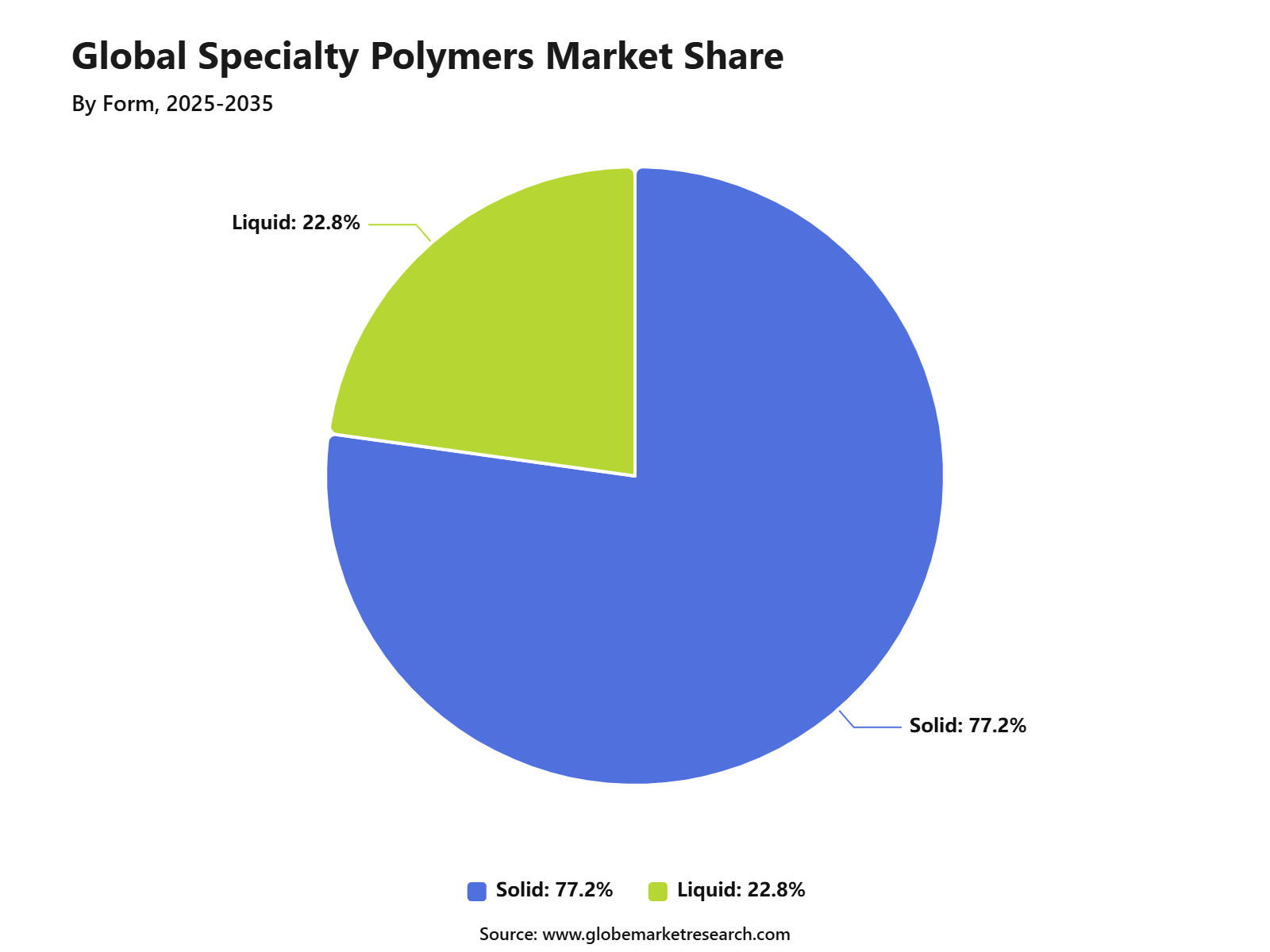

Solid form accounted for 77.2% share, driven by easier handling, better storage stability, and strong suitability for molded parts, films, coatings, elastomers, and engineered materials.

Specialty elastomers held 30.5% share by product type, supported by demand for flexible, durable, and high-performance materials used in seals, gaskets, tires, medical devices, and industrial components.

Transport captured 29.4% share by end use, driven by rising adoption of lightweight, heat-resistant, and impact-resistant polymers in automotive, aerospace, rail, and mobility applications.

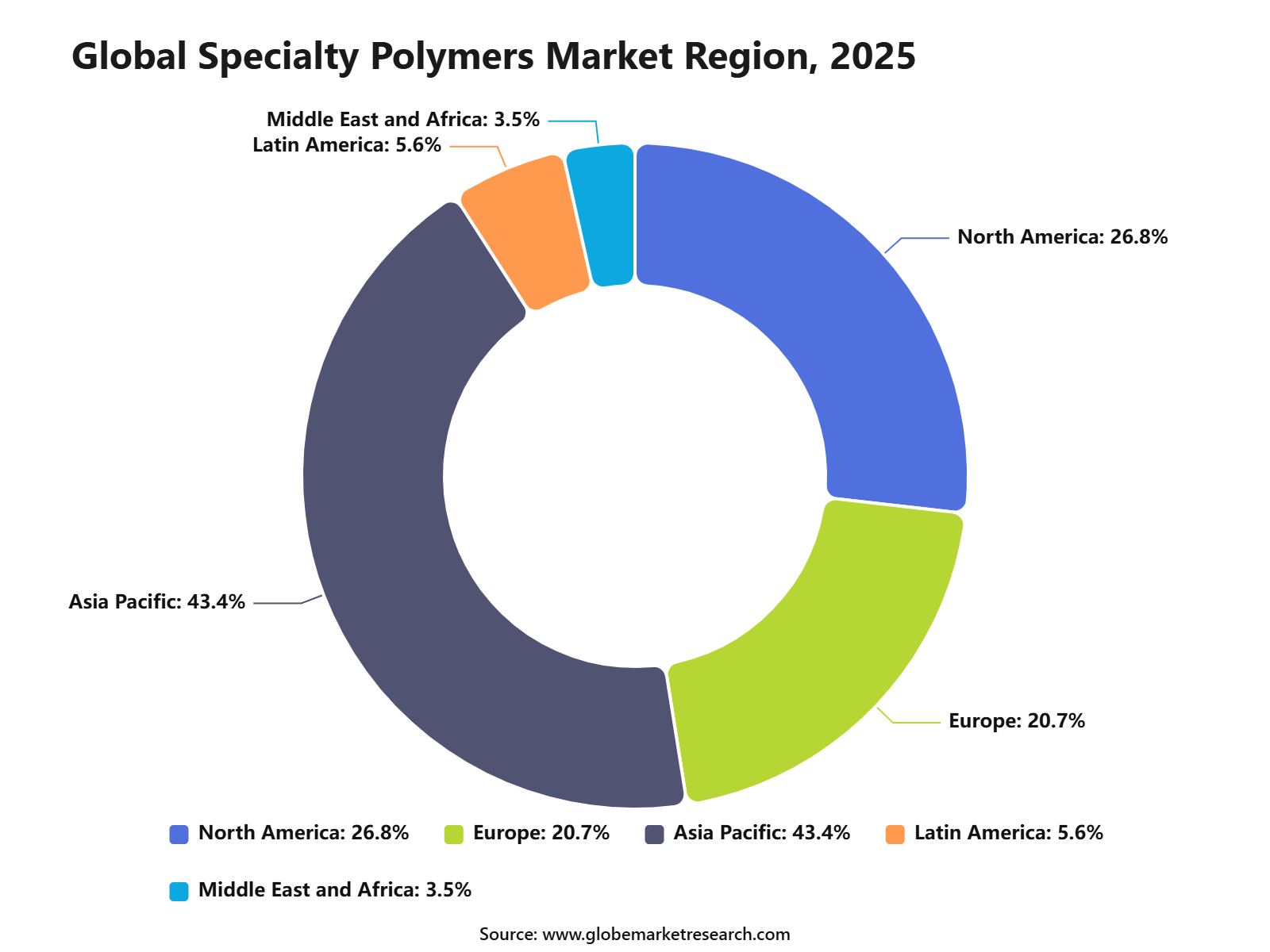

Asia Pacific led the specialty polymers market with 43.4% share, supported by strong manufacturing activity, expanding automotive production, rising electronics demand, and high polymer consumption across China, India, Japan, and Southeast Asia.

Top Funding and Investment Highlights

Arkema finalized the acquisition of a 54% stake in PI Advanced Materials in December 2023, based on a €728.0 million enterprise value. The deal strengthened Arkema’s high-performance polymer portfolio in polyimide films for advanced electronics, mobile devices, flexible screens, and electric mobility. PIAM held more than 30% global market share, with expected sales growth of around 13% per year.

Zeon revised its planned investment for a new cyclo olefin polymer plant from ¥70 billion to ¥78 billion in 2025. The funds are being arranged through internal resources and borrowings. The investment supports COP demand from optical films, medical applications, semiconductor use, and high-purity specialty plastic applications.

Solvay announced a €300.0 million investment at Tavaux, France, to expand Solef PVDF production capacity to 35 kilotons, making it the largest PVDF production site in Europe. The investment was aimed at electric vehicle batteries, where PVDF is used as a binder and separator coating in lithium-ion batteries.

DuPont completed a USD 250.0 million capital project at Circleville, Ohio, to expand production of Kapton polyimide film and Pyralux flexible circuit materials. These specialty polymer materials serve automotive, consumer electronics, telecommunications, specialized industrial, semiconductor, and defense applications.

SABIC opened a USD 170.0 million ULTEM resin manufacturing facility in Singapore in 2024. The plant is SABIC’s first advanced specialty chemical manufacturing facility in the region and supports high-performance thermoplastic demand from aerospace, healthcare, 5G, AI, and electric vehicle applications. It is also expected to increase global ULTEM specialty resin production by more than 50%.

By Source

Synthetic specialty polymers accounted for 61.2% share of the Specialty Polymers Market. This dominance can be attributed to their strong performance consistency, high durability, and ability to meet demanding industrial specifications across transport, electronics, healthcare, packaging, and construction applications.

The segment is widely preferred because synthetic polymers can be engineered with specific properties such as chemical resistance, heat stability, flexibility, lightweight strength, and electrical insulation. These advantages make them suitable for advanced applications where conventional polymers may not deliver the required performance.

Demand is also supported by the growing use of high-performance plastic materials in automotive components, electrical parts, medical devices, and industrial equipment. As manufacturers focus on lightweight design and longer product life, synthetic specialty polymers are expected to remain the preferred source category.

By Form

Solid specialty polymers held 77.2% share of the Specialty Polymers Market. The segment leads due to broad usage in pellets, granules, sheets, films, molded parts, and engineered components across major end-use industries.

Solid forms are preferred because they offer easier handling, storage, transport, and processing. They can be used in injection molding, extrusion, compression molding, and other high-volume manufacturing processes, making them suitable for commercial-scale production.

The strong share of solid specialty polymers is also supported by their use in transport parts, electronics housings, industrial machinery, packaging films, and medical components. Their stable physical structure and process flexibility make them a key material form in specialty polymer applications.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Product Type

Specialty elastomers captured 30.5% share of the Specialty Polymers Market. Their leadership is driven by high elasticity, flexibility, sealing performance, and resistance to heat, chemicals, oils, and mechanical stress.

These materials are widely used in automotive seals, gaskets, hoses, vibration control parts, medical devices, footwear, industrial equipment, and electrical applications. Their ability to maintain performance under harsh operating conditions makes them valuable in safety-critical and durability-focused uses.

The segment is gaining further support from the transport and industrial sectors, where lightweight and high-performance rubber-like materials are required. Specialty elastomers are expected to remain important as manufacturers replace traditional materials with advanced polymers that improve efficiency and product reliability.

By End Use

The transport segment held 29.4% share of the Specialty Polymers Market. Growth in this segment is supported by rising use of lightweight, durable, and fuel-efficient materials in automotive, aerospace, rail, marine, and electric mobility applications.

Specialty polymers are used in interior parts, exterior components, under-the-hood systems, battery housings, seals, connectors, cables, coatings, and structural applications. These materials help reduce vehicle weight while improving heat resistance, impact strength, safety, and design flexibility.

The shift toward electric vehicles and advanced mobility systems is also strengthening demand. Specialty polymers support thermal management, electrical insulation, noise reduction, and component miniaturization, making them essential for modern transport manufacturing.

By Region

Asia Pacific accounted for 43.4% share of the Specialty Polymers Market, making it the leading regional market. This dominance is supported by strong manufacturing activity, expanding automotive production, growing electronics output, and rising demand from packaging, healthcare, construction, and industrial sectors.

Countries such as China, India, Japan, South Korea, and Southeast Asian economies are major consumers of specialty polymers. The region benefits from large-scale production capacity, cost-efficient manufacturing, strong export activity, and increasing use of engineered polymer materials in high-growth industries.

Asia Pacific is expected to maintain its leading position as industrial investment, electric vehicle production, electronics manufacturing, and infrastructure development continue to expand. The growing need for lightweight, high-performance, and application-specific materials will further support regional demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFGo-to-Market and Sales Economics

The go-to-market approach for the Specialty Polymers Market should focus on application-specific performance, technical validation and long-term supply agreements. Demand is strongest where polymers must deliver heat resistance, chemical resistance, flexibility, lightweighting, durability or regulatory suitability. In the U.S., plastic resin output is expected to rise 0.7% in 2026, while specialty chemical output is expected to soften slightly by 0.3%, showing that demand is selective rather than broad-based.

Sales economics should be built around high-value end-use industries such as automotive, electronics, healthcare, industrial equipment, packaging, construction, renewable energy and 3D printing. In May 2026, U.S. sales and captive use of major plastic resins reached 8.3 billion pounds, while year-to-date sales and captive use reached 43.4 billion pounds, up 3.9% from the same period in 2025. This supports recurring polymer demand, but suppliers need pricing discipline because monthly sales were weaker than both the prior month and the prior year.

The strongest sales model is technical account selling, where suppliers work directly with OEMs, compounders and converters during material qualification. Specialty polymers are often approved into specific parts, devices or formulations, which increases switching costs after validation. This gives producers an advantage when they offer grade customization, testing support, regional warehousing, regulatory files and faster customer troubleshooting.

Risk Factors & Market Barriers

The main barriers are high raw material cost, long qualification timelines, regulatory pressure, and substitution risk from lower-cost engineering plastics. FRED reported the U.S. plastics material and resin manufacturing producer price index at 377.676 in May 2026, compared with 303.509 in January 2026, showing strong cost movement.

Regulatory risk is important for fluoropolymers and other advanced polymer chains linked with PFAS chemistry. EPA states that TSCA PFAS submissions are due by October 13, 2026 for most manufacturers, while small businesses reporting only imported articles have until April 13, 2027. This increases documentation and compliance pressure.

Technical barriers also affect adoption because specialty polymers require precise processing, moisture control, compounding stability, mold design, and temperature management. If end users lack processing knowledge, defects can occur through warpage, poor flow, weak bonding, or surface issues. Suppliers must therefore support trials, tool design, testing, and production training.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is spread across engineering plastics, thermoplastic elastomers, fluoropolymers, polyamides, polyimides, high-performance films, medical polymers, barrier materials, wire and cable insulation, automotive compounds and electronics-grade materials. Electric mobility is a strong demand channel because specialty polymers are used in battery housings, insulation, connectors, thermal management, lightweight parts and sealing systems. Global electric car sales are expected to reach 23 million units in 2026, equal to 28% of total car sales.

Electronics and semiconductor applications are another major revenue pool. Specialty polymers are used in chip packaging, connectors, films, photoresist-related materials, high-purity handling systems, displays and insulating components. Global semiconductor sales reached USD 298.5 billion in Q1 2026, rising 25% from Q4 2025, which supports demand for high-performance materials used in advanced electronics manufacturing.

Healthcare, sports, batteries, 3D printing and advanced fluorospecialties are also creating premium revenue opportunities. Arkema reported that several innovation-focused markets, including batteries, sports, 3D printing, healthcare and new-generation fluorospecialties, delivered around 20% year-over-year sales growth in Q3 2025. This shows that specialty polymer growth is being led by targeted applications where performance value is higher than basic material cost.

Financial Impact

The financial impact of specialty polymers is mainly linked to premium pricing, qualification barriers and customer-specific formulations. Arkema reported €1,251 million EBITDA in 2025 with a 13.8% EBITDA margin, despite weak demand in the U.S. and Europe. This indicates that specialty material producers can protect earnings when portfolios are supported by higher-value applications and disciplined cost control.

Margin pressure remains a key risk because lower selling prices, raw material movements and weak industrial demand can reduce profitability. Covestro’s Performance Materials segment reported €6.1 billion in 2025 sales, down 12.1%, while EBITDA fell to €375 million. This shows that even large polymer suppliers remain exposed to price pressure when demand is weak and capacity utilization is uneven.

The strongest financial upside will be captured by suppliers that move beyond commodity resin supply into engineered grades, application testing and integrated customer support. Covestro’s Solutions & Specialties segment reported €681 million EBITDA in 2025, which remained higher than its Performance Materials earnings. This supports the view that differentiated specialty polymer portfolios can deliver better earnings stability than volume-led polymer businesses.

Drivers Impact Analysis

The Specialty Polymers Market is driven by rising demand for high-performance materials used in automotive, electronics, healthcare, packaging, construction, aerospace, and industrial applications. These polymers offer benefits such as heat resistance, chemical stability, lightweight strength, flexibility, durability, and improved design freedom.

Asia Pacific supports strong growth because of large manufacturing activity, electronics production, automotive output, and expanding industrial polymer processing. China, India, Japan, South Korea, and Southeast Asia remain important demand centers for engineering plastics, elastomers, fluoropolymers, and specialty resins.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for high-performance materials | +2.3% | Asia Pacific, North America, Europe | Drives core adoption. |

Growth in automotive lightweighting | +2.0% | China, India, Japan, Europe, U.S. | Supports polymer substitution. |

Expansion of electronics manufacturing | +1.8% | Asia Pacific, U.S., Europe | Builds technical demand. |

Increasing healthcare and medical use | +1.5% | North America, Europe, Japan, China | Adds premium applications. |

Demand for durable packaging materials | +1.2% | Global consumer markets | Supports steady volume. |

Restraints Impact Analysis

The market faces restraints from high production cost, raw material price volatility, and complex processing requirements. Specialty polymers often need advanced feedstocks, controlled manufacturing, and strict quality standards, making them more expensive than commodity plastics. Environmental pressure on plastic materials is also increasing. Producers must improve recyclability, reduce emissions, and comply with safety rules, especially in applications linked to packaging, electronics, automotive, and healthcare products.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High material and processing cost | -1.2% | Global end users | Limits mass adoption. |

Raw material price volatility | -1.0% | Asia Pacific, Europe, North America | Pressures margins. |

Recycling and disposal concerns | -0.9% | Europe, North America, developed Asia | Raises sustainability pressure. |

Strict regulatory requirements | -0.8% | Healthcare, food contact, electronics | Increases compliance cost. |

Competition from commodity polymers | -0.7% | Price-sensitive markets | Reduces substitution speed. |

Opportunities Impact Analysis

Opportunities are strong in electric vehicles, electronics, medical devices, advanced packaging, renewable energy, aerospace, and high-performance industrial components. Specialty polymers can replace metals, glass, rubber, and commodity plastics in applications where performance and weight reduction are important.

Higher-value opportunities are also emerging in bio-based polymers, recyclable specialty grades, and flame-retardant materials. Companies that provide customized polymer solutions for demanding end-use industries can capture stronger margins and long-term customer relationships.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Electric vehicle polymer demand | +2.2% | Asia Pacific, Europe, North America | Builds future growth. |

Medical-grade specialty polymers | +1.9% | U.S., Europe, Japan, China | Supports premium demand. |

High-performance electronics materials | +1.7% | Taiwan, South Korea, China, Japan | Adds technical value. |

Bio-based specialty polymer development | +1.4% | Europe, North America, Japan | Supports sustainability shift. |

Aerospace and industrial composites | +1.2% | U.S., Europe, Asia Pacific | Expands advanced use. |

Challenges Impact Analysis

The main challenge is balancing performance, cost, and sustainability. Customers need specialty polymers that deliver strength, heat resistance, barrier performance, or chemical stability, but they also want lower environmental impact and better recyclability. Another challenge is meeting industry-specific qualification standards. Automotive, healthcare, electronics, and aerospace customers require strict testing, documentation, and long approval cycles before using new polymer grades in commercial products.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Balancing performance and sustainability | -1.1% | Global polymer users | Affects material selection. |

Long customer qualification cycles | -0.9% | Automotive, healthcare, electronics | Slows product adoption. |

Technical processing complexity | -0.8% | Global manufacturers | Raises production burden. |

Maintaining consistent material quality | -0.7% | Advanced applications | Protects buyer trust. |

Meeting recyclability expectations | -0.6% | Europe, North America, Asia Pacific | Requires product redesign. |

Segment Covered in the Report

By Source

Synthetic

Natural

Semisynthetic

By Product Type

Specialty Elastomers

Specialty Thermoplastics

Specialty Thermosets

Biodegradable Polymers

Liquid Crystal Polymers

Others

By Form

Solid

Liquid

By End Use

Transport

Medical and Healthcare

Textile

Electrical and Electronics

Cosmetics and Personal Care

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward engineering plastics, elastomers, fluoropolymers, high-temperature polymers, and specialty resins. These materials are gaining importance as industries shift toward lighter, safer, and more durable products. Automotive, electronics, and healthcare remain major trend areas because they require materials with tighter performance standards. Asia Pacific continues to shape volume demand, while North America and Europe support premium-grade innovation and sustainability-led product development.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Engineering plastics gain wider use | +2.1% | Asia Pacific, Europe, North America | Leads value demand. |

High-temperature polymers expand | +1.8% | Electronics, aerospace, automotive | Supports advanced design. |

Specialty elastomers gain adoption | +1.5% | Automotive, healthcare, industrial sectors | Adds flexible performance. |

Fluoropolymer demand remains strong | +1.3% | Electronics, chemical processing, energy | Supports resistant materials. |

Recyclable specialty grades increase | +1.1% | Europe, North America, Asia Pacific | Supports circular materials. |

Investor Type Impact Matrix

Investors should focus on specialty polymer producers with strong technical capability, reliable feedstock access, customer-specific formulation expertise, and exposure to automotive, electronics, healthcare, and packaging applications. These areas provide both volume demand and higher-value opportunities.

Strategic investors can also target companies developing bio-based polymers, recyclable grades, high-performance elastomers, and polymers for EVs and electronics. Businesses that combine performance, compliance, and sustainability are better positioned for long-term growth.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Specialty Polymer Manufacturers | +2.0% | Global | Expands product capacity. |

Engineering Plastic Producers | +1.7% | Asia Pacific, Europe, North America | Drives technical demand. |

Automotive and EV Material Suppliers | +1.5% | China, Europe, U.S., Japan | Supports lightweighting. |

Healthcare Polymer Suppliers | +1.2% | U.S., Europe, Japan, China | Builds premium usage. |

Private Equity and Strategic Investors | +1.0% | Global specialty material markets | Supports capacity scaling. |

Recent Developments

In January 2026, Arkema started its new Rilsan Clear transparent polyamide unit in Singapore. The project involved an investment of around US$20 million and tripled Arkema’s global production capacity for Rilsan Clear transparent polyamide. This strengthens supply for high-performance applications in eyewear, consumer goods, sports equipment, electronics, and lightweight industrial parts.

In May 2026, Syensqo reported €530 million in Specialty Polymers net sales for Q1 2026. Sales declined year over year, but demand was supported by higher volumes in automotive, healthcare, and industrial and chemicals end markets. This shows that specialty polymers are still supported by critical applications, even when pricing and product mix remain under pressure.

In June 2026, Evonik opened an Anion Exchange Membrane application technology center in Shanghai. The center will test DURAION high-performance membranes under real operating conditions. This is important for specialty polymers because membrane materials are gaining demand in hydrogen, energy conversion, gas separation, and advanced electrochemical systems.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Arkema

BASF SE

Evonik Industries AG

Covestro AG

Solvay SA

Dow Inc.

DuPont de Nemours, Inc.

SABIC

Celanese Corporation

Eastman Chemical Company

Mitsubishi Chemical Group Corporation

Toray Industries, Inc.

Kuraray Co., Ltd.

LG Chem

Wacker Chemie AG

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Carbon Capture Chemicals Market Size to Reach USD 78.0 Billion by 2035

Carbon Capture Chemicals Market By Chemical Type (Amines, Carbonates, Ammonia-based Solvents, Ionic Liquids, Solid Sorbent Chemicals, Others), By Absorption Type (Chemical Absorption, Physical Absorption), By End-Use Industry (Oil and Gas, Power Generation, Chemical and Petrochemical, Cement, Iron and Steel, Others), By Application (Post-combustion Capture, Pre-combustion Capture, Industrial Gas Separation, Direct Air Capture, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Bio-based Chemicals Market Size to Hit USD 296.7 Bn by 2035

Bio-based Chemicals Market By Product Category (Platform Chemicals, Polymers for Plastics, Paints, Coatings, Inks and Dyes, Surfactants, Cosmetics and Personal Care Products, Adhesives, Man-made Fibers, Others), By Application (Industrial, Agricultural, Pharmaceutical, Others), By Source (Plant-based, Animal-based, Microbial-based, Waste-based), By End Use (Chemical Manufacturing, Agriculture, Food and Beverage, Personal Care, Pharmaceuticals, Automotive), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Processing Chemicals Market Size to Hit USD 14.6 Billion by 2035

Hydrogen Processing Chemicals Market By Chemical Type (Catalysts, Adsorbents, Solvents, Corrosion Inhibitors, Scavengers, Others), By Function (Reforming Chemicals, Purification Chemicals, Hydroprocessing Chemicals, Gas Treatment Chemicals, Corrosion Control Chemicals, Others), By Process (Steam Methane Reforming, Hydrocracking, Hydrotreating, Pressure Swing Adsorption, Water-Gas Shift Reaction, Others), By End Use (Refineries, Ammonia Production, Methanol Production, Petrochemicals, Clean Hydrogen Plants, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Electrolyte Chemicals Market to Cross USD 49.4 Billion by 2035

Electrolyte Chemicals Market By Battery Type (Lithium-ion Electrolytes, Lead-acid Electrolytes, Flow Battery Electrolytes, Others), By Electrolyte Form (Liquid Electrolytes, Gel, Solid-State Electrolytes), By Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, Industrial and Motive Batteries, Others), By Product Type (Lithium-Based Electrolytes, Sulfide-Based Electrolytes, Polymer-Based Electrolytes, Oxide-Based Electrolytes, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035