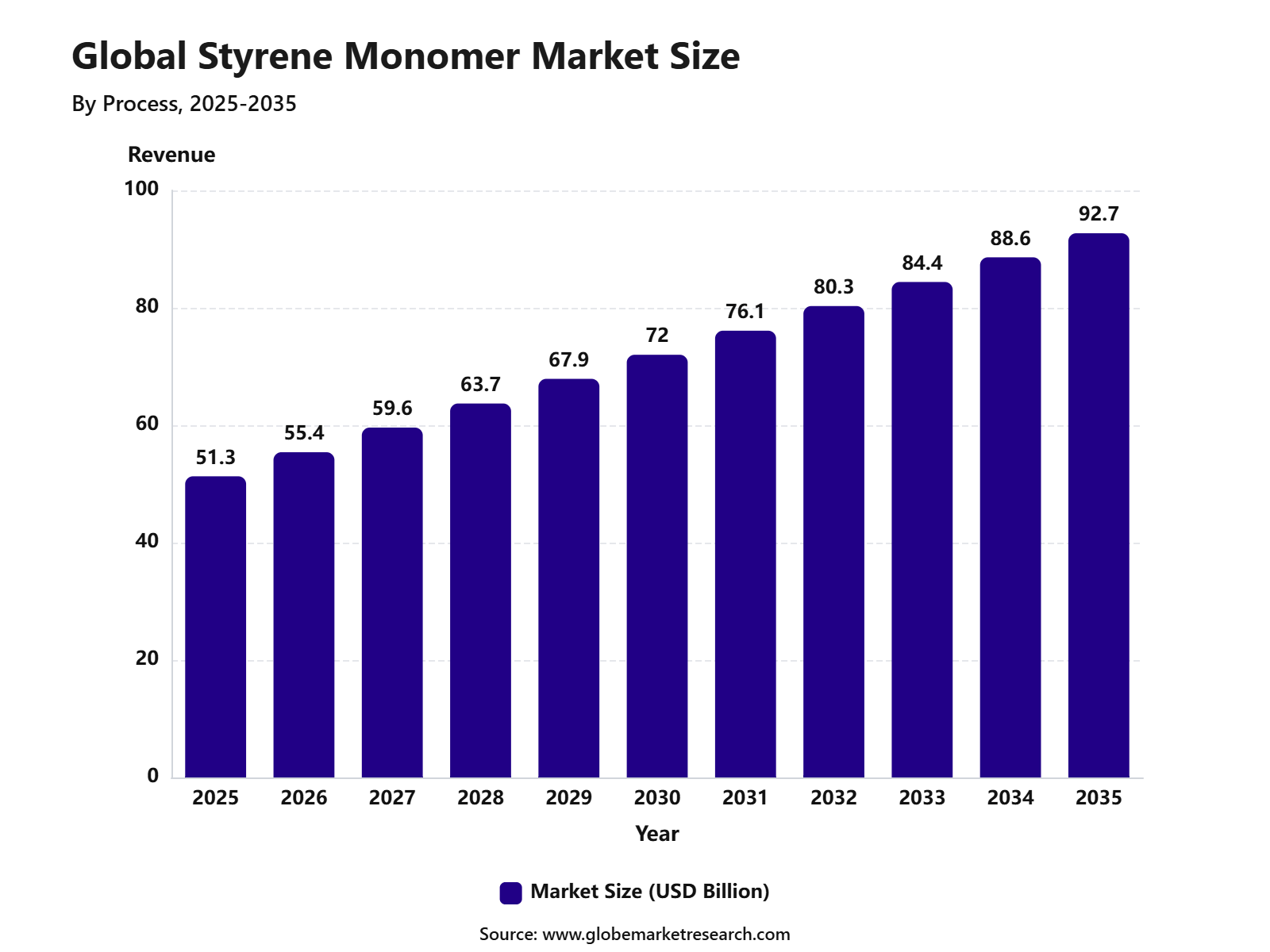

Revenue, 2025

$51.3 Bn

Forecast, 2035

$92.7 Bn

CAGR, 2025-2035

6.1%

Report Coverage

Global

Market Size and Forecast

The Global Styrene Monomer Market reached USD 51.3 billion in 2025 and is expected to grow to USD 92.7 billion by 2035, registering a CAGR of 6.1% from 2025 to 2035. The growth of the market can be attributed to rising demand for polystyrene, ABS, SAN, synthetic rubber, latex, and other styrene-based materials across packaging, automotive, construction, consumer goods, electronics, and industrial applications. Styrene monomer remains a key raw material in the petrochemical value chain due to its wide use in lightweight plastics, insulation materials, disposable packaging, appliances, and durable molded products.

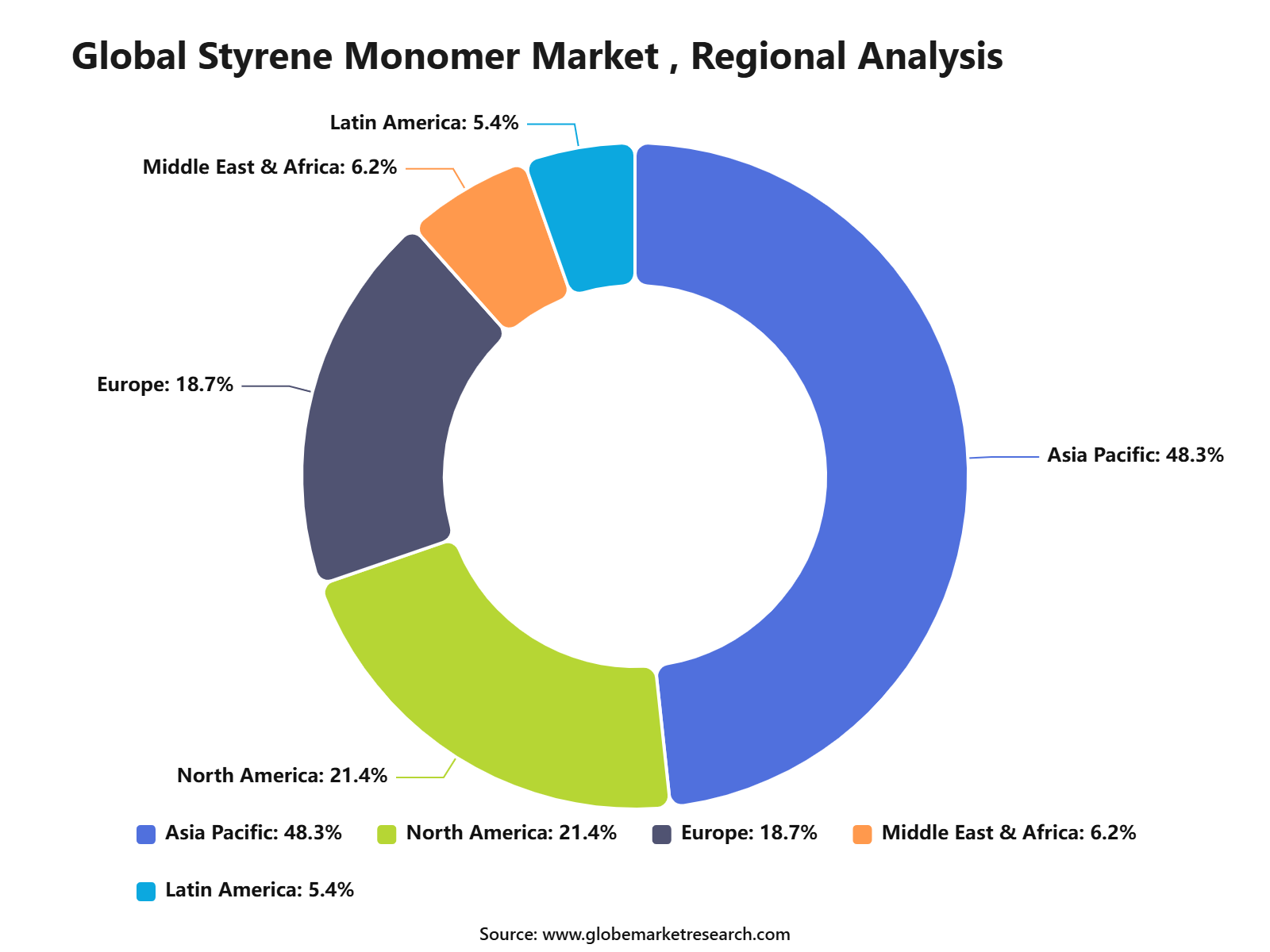

Asia Pacific held the largest regional share of 48.3% in 2025, supported by strong manufacturing activity, high plastic consumption, expanding automotive production, and growing demand from packaging and construction industries. China, India, Japan, South Korea, and Southeast Asian countries continue to support regional growth through large petrochemical capacity, strong downstream processing, and rising consumption of consumer and industrial plastic products. Market demand is also being supported by urbanization, e-commerce packaging growth, electronics production, and increasing use of styrene-based polymers in lightweight and cost-effective material applications.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Ethylbenzene dehydrogenation led the process segment with 90.2% share, supported by its established commercial use, high production efficiency, and wide adoption in large-scale styrene manufacturing.

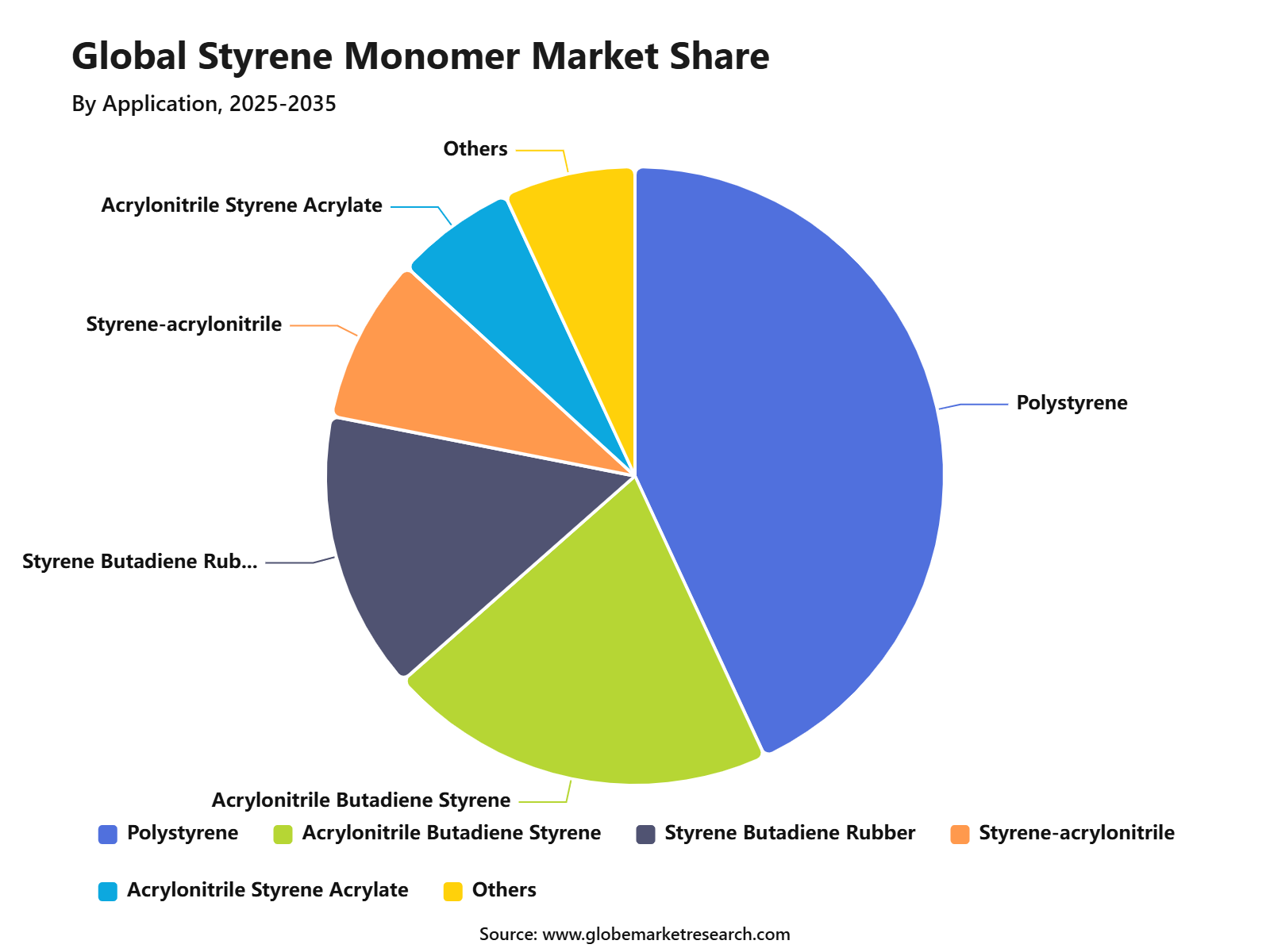

Polystyrene accounted for 43.1% share by application, driven by strong demand in packaging, consumer goods, insulation materials, disposable products, and industrial components.

Packaging held 28.3% share by end use, supported by rising demand for lightweight, durable, and cost-effective plastic packaging materials.

Asia Pacific led the styrene monomer market with 48.3% share, supported by strong manufacturing activity, high polymer consumption, expanding packaging demand, and large-scale chemical production capacity.

Styrene Monomer Market Overview

Styrene monomer is a key petrochemical raw material used to produce polystyrene, expandable polystyrene, ABS, SAN, styrene-butadiene rubber, latex, and unsaturated polyester resins. Demand is mainly supported by packaging, building insulation, automotive components, consumer appliances, electronics, synthetic rubber, and industrial molded products.

The market remains closely linked to the wider plastics and petrochemical value chain, where demand is supported by the continued need for lightweight, durable, and cost-efficient materials. Global plastics production increased by 4.1% in 2024 and rose by 16.3% compared with 2018, showing a strong long-term consumption base for styrene-based polymers.

The market is also supported by steady demand for chemical feedstocks, especially in Asia, where packaging, construction, electronics, automotive, and consumer goods manufacturing remain strong. The International Energy Agency reported that chemical feedstocks accounted for around 70% of volumetric oil demand growth in 2024, while petrochemical feedstock demand increased by more than 12% over the previous five years. Trade data also shows active global styrene movement, with India importing about USD 1.31 billion of styrene in 2024, while the United States, Saudi Arabia, and the Netherlands were among the leading exporters.

Go-to-Market and Sales Economics Strategy

The styrene monomer market should be positioned around long-term contracts with polystyrene, ABS, SBR, resins, packaging, automotive, electronics, and construction customers. Sales economics are strongly linked to feedstock pass-through clauses because benzene, ethylene, crude oil, and naphtha costs can move faster than downstream demand. In June 2026, styrene prices were reported at about USD 0.88 per kg in North America, USD 1.39 per kg in Europe, and USD 1.29 per kg in Northeast Asia, with Northeast Asia down 7.2%, showing that sellers need flexible pricing instead of fixed-margin selling.

A stronger go-to-market model should focus on regional supply security, customer credit quality, and value-added technical service for polymer producers. North America has a cost advantage where ethylene was about USD 0.70 per kg in May 2026, compared with USD 1.50 per kg in Europe and USD 0.94 per kg in Northeast Asia, supporting better export economics for U.S. based producers when freight and tariffs are manageable.

Revenue Potential Analysis

Revenue Landscape Across

Based on data from reuters, The revenue landscape remains strongest across polystyrene, ABS, styrene-butadiene rubber, unsaturated polyester resins, packaging, construction materials, automotive parts, electronics, and appliances. Asia Pacific remains the key revenue center because it combines large polymer processing capacity, electronics manufacturing, automotive production, and packaging consumption.

Trade data confirms the importance of export-oriented supply chains. In 2024, the leading styrene exporters were the United States at about USD 1.70 billion, Saudi Arabia at about USD 1.43 billion, and the Netherlands at about USD 1.39 billion, followed by Singapore and Taiwan. This shows that revenue growth will be shaped not only by domestic consumption, but also by access to reliable shipping routes, tariff exposure, buyer contracts, and regional feedstock cost advantages.

Financial Impact

The financial impact is expected to remain positive over the long term, but earnings may be uneven across regions. North American producers are better placed when crude-linked feedstocks rise because U.S. plastics production is largely supported by natural gas and related feedstocks, while Asia and Europe remain more exposed to naphtha and imported crude. During the 2026 Middle East disruption, Reuters reported that North America remained the most cost-advantaged region, while Asia and Europe faced higher input costs and tighter margins.

Profitability will depend on pass-through pricing, plant integration, operating rates, and the ability to serve high-value resin customers instead of only commodity-grade buyers. Europe highlights the downside risk, as production volumes increased only 0.4% in 2024 after a 7.6% contraction in 2023, while sector turnover fell 13% and the region’s global market share declined to 12%. For styrene monomer suppliers, the strongest financial returns are expected from integrated producers with benzene and ethylene access, diversified export channels, and contracts linked to feedstock movement.

Process Analysis

Ethylbenzene dehydrogenation led the Styrene Monomer Market with 90.2% share, supported by its strong commercial use in large-scale styrene production. This process is widely preferred because ethylbenzene can be converted into styrene through catalytic dehydrogenation under high-temperature operating conditions.

The dominance of this process can be attributed to its established technology base, large production capacity, and strong integration with petrochemical value chains. Producers continue to prefer ethylbenzene dehydrogenation because it supports consistent output, scalable operations, and reliable feedstock conversion for downstream styrene applications.

Application Analysis

Polystyrene accounted for 43.1% share of the Styrene Monomer Market, making it the leading application segment. Styrene monomer is a key raw material used to produce polystyrene, which is used in rigid and foam-based products across packaging, consumer goods, insulation, foodservice products, and protective materials.

The segment is supported by polystyrene’s light weight, moldability, cost efficiency, and suitability for packaging and disposable product applications. Demand is expected to remain linked with food packaging, electronics packaging, appliance parts, insulation boards, and consumer product manufacturing.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFEnd Use Analysis

Packaging held 28.3% share of the Styrene Monomer Market, supported by strong demand for polystyrene-based packaging formats. Styrene-based materials are used in food containers, trays, foam packaging, protective packaging, cups, lids, and insulation-based packaging products.

The growth of this segment is driven by demand for lightweight, protective, and cost-efficient packaging. However, regulatory pressure on plastic waste and single-use packaging is encouraging manufacturers to improve recyclability, reduce material use, and develop more sustainable packaging alternatives.

Regional Analysis

Asia Pacific led the Styrene Monomer Market with 48.3% share, supported by strong manufacturing activity, high plastics consumption, and large downstream demand from packaging, consumer goods, automotive, electronics, and construction industries. China, India, Japan, South Korea, and Southeast Asian countries remain major contributors to regional styrene consumption.

The region’s dominance can be linked to its large petrochemical production base and strong demand for polystyrene, ABS, and synthetic rubber. Asia Pacific is expected to remain the leading market as packaged goods consumption, electronics production, vehicle manufacturing, and construction-related material demand continue to support styrene monomer use.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFInvestment Opportunity Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Polystyrene and EPS production | +1.5% | Asia Pacific, Europe, Middle East | Offers volume growth. |

ABS resin manufacturing | +1.2% | Asia Pacific, North America, Europe | Supports high-value demand. |

Packaging-grade styrenic materials | +1.1% | China, India, Southeast Asia | Expands application growth. |

Cleaner production technologies | +0.8% | Europe, U.S., Japan, China | Improves compliance value. |

Recycling and circular styrene solutions | +0.7% | Europe, North America, developed Asia | Builds long-term opportunity. |

Technology Adoption Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Ethylbenzene dehydrogenation process | +1.5% | Global production facilities | Supports large-scale output. |

Process efficiency improvements | +1.0% | Asia Pacific, Europe, North America | Reduces production cost. |

Emission control technologies | +0.8% | Europe, U.S., Japan, China | Improves regulatory fit. |

Advanced catalyst systems | +0.7% | Major styrene producers | Enhances production yield. |

Chemical recycling technologies | +0.6% | Europe, North America, Japan | Supports circular plastics. |

Demand Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Demand from packaging industry | +1.6% | Asia Pacific, Europe, North America | Drives leading application. |

Demand from construction insulation | +1.2% | Europe, China, North America | Supports EPS consumption. |

Demand from automotive plastics | +1.0% | China, Japan, Germany, U.S. | Expands ABS usage. |

Demand from consumer appliances | +0.9% | Asia Pacific, Latin America | Supports resin growth. |

Demand from electronics and electrical goods | +0.8% | China, South Korea, Japan, India | Improves specialty use. |

Segment covered in the Report

By Process

Ethylbenzene Dehydrogenation

Propylene Oxide Styrene Monomer

By Application

Polystyrene

Acrylonitrile Butadiene Styrene

Acrylonitrile Styrene Acrylate

Styrene-acrylonitrile

Styrene Butadiene Rubber

Others

By End Use

Packaging

Electronics

Healthcare

Household

Automotive

Construction

Others

By Region

Asia Pacific

North America

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for polystyrene | +1.7% | Asia Pacific, North America, Europe | Drives core consumption. |

Growth in packaging applications | +1.4% | China, India, Southeast Asia, Europe | Supports high-volume demand. |

Expansion of consumer goods manufacturing | +1.2% | Asia Pacific, Latin America | Increases styrene usage. |

Growth in construction insulation materials | +1.0% | Europe, North America, China | Supports EPS demand. |

Increasing automotive component production | +0.9% | China, Japan, Germany, U.S. | Boosts ABS and composites. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Volatile benzene and ethylene prices | -0.9% | Global | Pressures margins. |

Environmental and health regulations | -0.8% | Europe, North America, developed Asia | Raises compliance cost. |

Plastic waste and recycling pressure | -0.7% | Europe, North America, Asia Pacific | Limits conventional plastic use. |

Competition from alternative materials | -0.6% | Packaging and construction sectors | Reduces substitution potential. |

Cyclical demand from end-use industries | -0.5% | Global | Affects production planning. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in expandable polystyrene demand | +1.5% | Asia Pacific, Europe, Middle East | Supports insulation and packaging. |

Expansion of ABS resin applications | +1.2% | Automotive, electronics, appliances | Improves value demand. |

Rising demand from food packaging | +1.1% | Asia Pacific, North America, Europe | Expands application base. |

Capacity expansion in Asia Pacific | +1.0% | China, India, South Korea | Strengthens regional supply. |

Development of recyclable styrenic materials | +0.8% | Europe, U.S., Japan | Supports sustainable growth. |

Recent Developments

February 2026, the European Commission imposed anti-dumping duties on ABS imports from South Korea and Taiwan, with duties ranging from 5.2% to 7.5% for Korea and 10.9% to 21.7% for Taiwan. ABS is a major styrenic resin, so this trade action is expected to affect downstream styrene monomer demand, pricing, and sourcing strategies in Europe.

January 2026, Shell Chemicals updated its styrene monomer offering with a stronger focus on bio-based, circular, and lower-carbon solutions. This reflects rising customer demand for sustainable feedstock options in packaging, automotive, consumer goods, and construction applications.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 51.3 Billion |

Forecast Revenue (2035) | USD 92.7 Billion |

CAGR (2025-2035) | 6.1% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Process (Ethylbenzene Dehydrogenation, Propylene Oxide Styrene Monomer), By Application (Polystyrene, Acrylonitrile Butadiene Styrene, Acrylonitrile Styrene Acrylate, Styrene-acrylonitrile, Styrene Butadiene Rubber, Others), By End Use (Packaging, Electronics, Healthcare, Household, Automotive, Construction, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | SABIC, INEOS, Shell plc, KR Chemicals, Qingdao Haiwan Group Co., Ltd., Denka Company Limited, Chevron Phillips Chemical Company LLC, KH Chemicals, LOTTE Chemical Corporation, Repsol, Hanwha TotalEnergies Petrochemical Co., Ltd., Americas Styrenics LLC, Westlake Corporation, Equate Petrochemical Company, The Kuwait Styrene Company, Other Key Players |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

SABIC

INEOS

Shell plc

KR Chemicals

Qingdao Haiwan Group Co., Ltd.

Denka Company Limited

Chevron Phillips Chemical Company LLC

KH Chemicals

LOTTE Chemical Corporation

Repsol

Hanwha TotalEnergies Petrochemical Co., Ltd.

Americas Styrenics LLC

Westlake Corporation

Equate Petrochemical Company

The Kuwait Styrene Company

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Oxygen Market to Exceed USD 171.1 Billion by 2035

Global Oxygen Market Size, Share Analysis By Form (Gas, Liquid, Solid), By Type (Industrial, Medical), By Application (Metals and Mining, Chemical Industry, Oil and Gas, Healthcare, Pharmaceutical, Other Applications), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Tannin Market to Hit USD 9.8 Billion by 2035

Global Tannin Market Size, Share and Go-to-Market Strategy Analysis By Source (Plant, Brown Algae), By Product Type (Hydrolysable Tannins, Condensed Tannins, Phlorotannins, Others), By Application (Food and Beverage, Pharmaceutical and Nutraceutical, Leather Industry, Wood Industry, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Printing Ink Market to Hit USD 30.6 Billion by 2035

Global Printing Ink Market Size, Go-to-Market Strategy Analysis By Type (Solvent-Based, Water-Based, Oil-Based, UV, UV-LED, Others), By Process (Lithographic Printing, Flexographic Printing, Gravure Printing, Digital Printing, Others), By Application (Packaging, Commercial and Publication, Textiles, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Methanol Market to Exceed USD 64.1 Billion by 2035

Global Methanol Market Size By Feedstock (Natural Gas, Coal, Biomass and Renewables), By Derivative (Formaldehyde, Acetic Acid, MTBE, DME, Gasoline Blending, Biodiesel, MTO/MTP, Solvent, Others), By Sub-derivatives (Gasoline additives, Olefins, UF/PF resins, VAM, Polyacetals, MDI, PTA, Acetate Esters, Acetic anhydride, Fuels, Others), By Application (Construction, Automotive, Electronics, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035