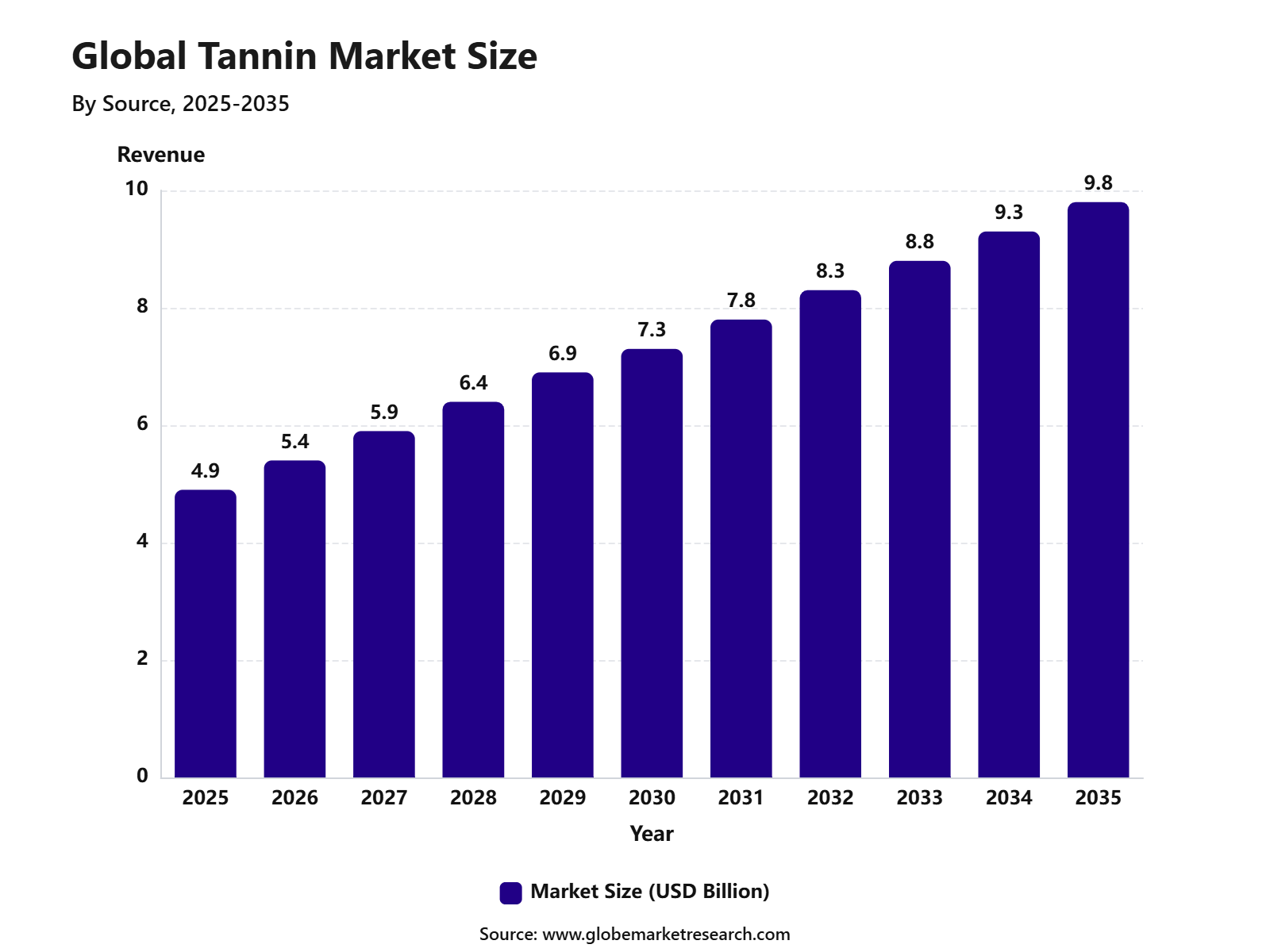

Revenue, 2025

$ 4.9 Bn

Forecast, 2035

$ 9.8 Bn

CAGR, 2025-2035

7.2%

Report Coverage

Global

Market Size and Forecast

The Global Tannin Market was valued at USD 4.9 billion in 2025 and is projected to reach USD 9.8 billion by 2035, growing at a CAGR of 7.2% from 2025 to 2035. The growth of the market can be attributed to rising demand for tannins in leather processing, wine production, wood adhesives, animal feed, pharmaceuticals, and natural antioxidant applications. Increasing preference for bio-based and plant-derived ingredients is also supporting wider use of tannins across industrial and consumer-focused sectors.

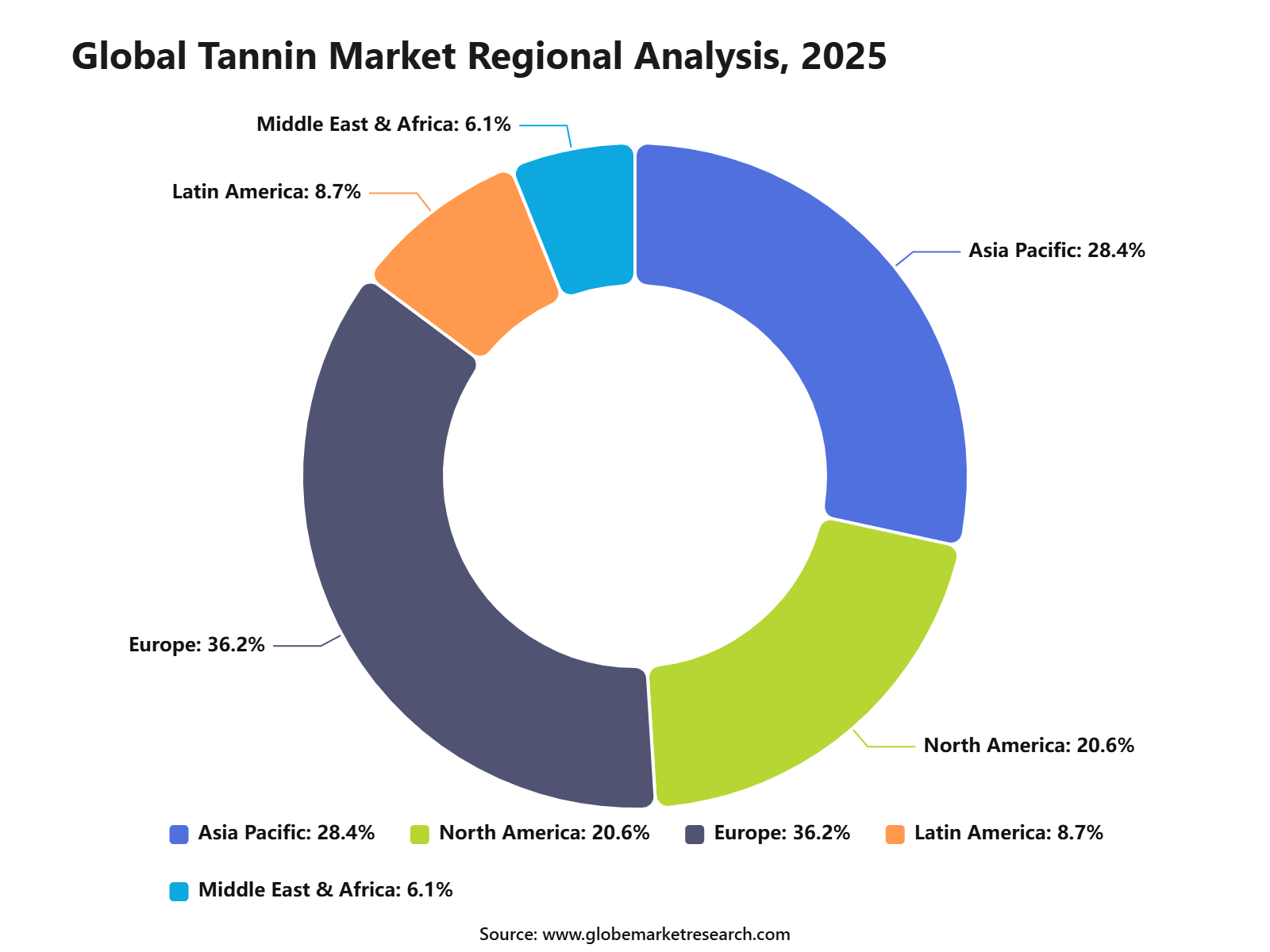

Europe held the largest regional share of 36.2% in 2025, valued at approximately USD 1.8 billion. The region’s leadership can be linked to strong demand from the wine, leather, food processing, and pharmaceutical industries, along with growing adoption of natural additives and sustainable raw materials. Countries such as Italy, France, Germany, and Spain continue to support market expansion through established wine production, advanced chemical processing, and rising use of plant-based functional ingredients.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Plant-based tannins led the source segment with 83.2% share, supported by their wide availability, natural origin, and strong use across leather processing, food applications, pharmaceuticals, and industrial formulations.

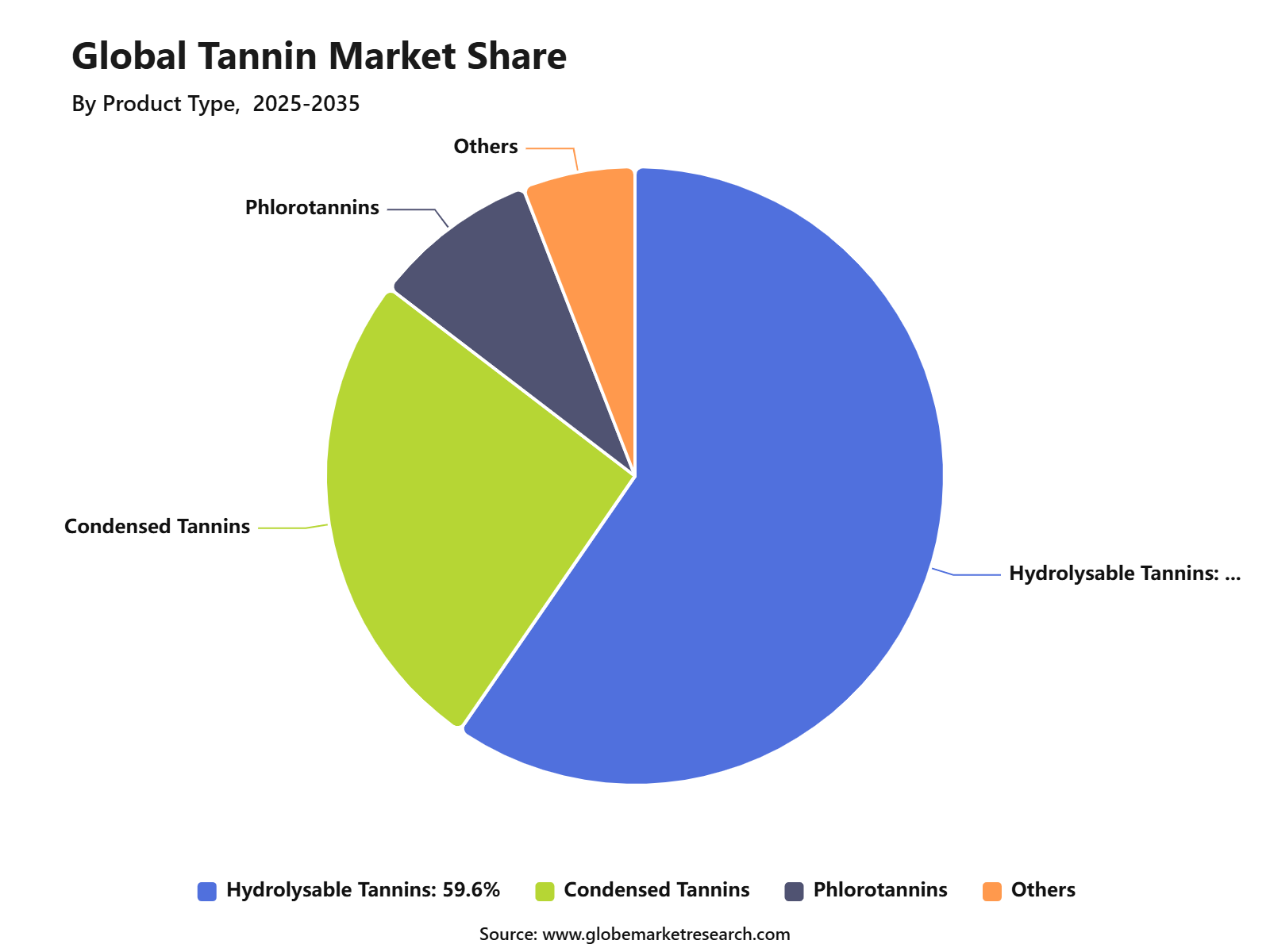

Hydrolysable tannins accounted for 59.6% share by product type, driven by their use in tanning, antioxidants, dyeing, adhesives, and specialty chemical applications.

The leather industry captured 67.6% share by application, supported by tannins’ strong role in leather tanning, preservation, texture improvement, and durability enhancement.

Europe held 36.2% share of the tannin market, supported by established leather processing activity, demand for natural ingredients, and strong use of plant-based tannins in industrial and specialty applications.

Go-to-Market and Sales Economics

The Tannin Market needs an application-led go-to-market strategy because tannins are used across leather tanning, wine processing, animal feed, food additives, wood adhesives, pharmaceuticals, cosmetics, and water treatment. Suppliers should position products by source and function, such as quebracho extract, wattle extract, chestnut extract, gallotannic acid, tara tannin, myrobalan extract, and food-grade tannic acid. For leather use, buyers focus on color tone, penetration, astringency, leather feel, and consistency. For wine and food use, buyers focus on purity, taste impact, regulatory status, and technical documentation.

Sales economics are strongest when suppliers sell standardized, application-specific grades rather than raw botanical extracts only. Leather remains an important demand base because vegetable tanning uses plant-derived tannins as a natural alternative to chrome-based tanning in selected leather applications. UNIDO’s Leather Panel states that the leather industry converts around 7.3 million tons of hides and skins each year that would otherwise go to landfill, showing the large industrial base linked to tanning inputs.

Risk Factors & Market Barriers

The main risk factor is raw material supply stability. Natural tannins depend on forest and agricultural sources such as quebracho wood, wattle bark, chestnut wood, tara pods, myrobalan fruit, sumac, gall nuts, and other plant materials. Supply can be affected by climate conditions, forestry rules, harvest cycles, transport costs, and sustainability requirements. This creates quality and cost risk for buyers that require stable color, tannin content, moisture level, and extraction performance.

Demand risk is also linked to leather and wine cycles. Global wine consumption fell 2.7% in 2025 to 208 million hectolitres, the lowest level since 1957, while wine exports fell 4.7% in volume to 94.8 million hectolitres. Since oenological tannins are used in wine structure, stabilization, mouthfeel, and color management, weak wine consumption can limit near-term demand from wineries, especially in regions facing inventory pressure.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape for tannins is spread across leather tanning, wine processing, animal feed, food additives, natural dyes, pharmaceuticals, cosmetics, wood adhesives, water treatment, and industrial chemicals. Leather remains a large industrial application because vegetable tannins help convert hides into durable leather and support chrome-free or reduced-chrome leather positioning. FAO noted in its latest meat market review that global meat production was projected to rise in 2025, with strong demand for bovine meat supporting international trade flows, which indirectly supports hide availability for leather value chains.

Trade data confirms that tannins and vegetable tanning extracts remain active specialty products. In 2024, top importers of HS 320190 products included India at USD 61.3 million and 23.5 million kg, Italy at USD 12.7 million and 3.3 million kg, the European Union at USD 10.1 million and 3.0 million kg, the United States at USD 9.7 million and 1.2 million kg, and Japan at USD 8.8 million and 693,703 kg. This shows that demand is concentrated in countries with leather processing, specialty chemical use, wine, and industrial formulation activity.

Financial Impact

The financial impact can be positive for suppliers that control plant sourcing, extraction quality, product standardization, and regulatory documentation. Higher-value opportunities are expected in food-grade tannic acid, wine tannins, feed additives, pharmaceutical grades, and technical leather chemicals where purity and performance are more important than bulk price. Export-oriented suppliers can also benefit from strong demand in India, Europe, the United States, Japan, and other industrial markets.

Financial risk remains linked to raw botanical supply, forest regulation, freight, tariffs, exchange rates, and competition from chrome tanning agents, synthetic tannins, and other specialty chemicals. Europe’s 2026 move to exclude leather, hides, and skins from its anti-deforestation law may reduce some compliance pressure for leather importers, but sustainability scrutiny remains high because leather and tanning chemicals are still judged by traceability, waste, effluent, and environmental impact. The strongest financial resilience is expected from tannin suppliers that offer certified sourcing, consistent active content, multi-application grades, and customer-specific technical support.

Source Analysis

Plant-based tannins led the Tannin Market with 83.2% share, supported by their wide availability across bark, wood, leaves, fruits, pods, and other botanical sources. These tannins are commonly extracted from acacia, chestnut, quebracho, oak, tara, gallnut, and other tannin-rich plants. The growth of this segment can be attributed to rising demand for natural, renewable, and plant-derived ingredients across leather, food and beverage, pharmaceuticals, wood adhesives, and industrial applications.

Plant tannins are preferred because they provide binding, astringent, antioxidant, and preservation-related properties. Plant-based tannins are expected to remain dominant as industries continue to shift toward bio-based inputs and lower-impact processing materials. Their strong use in vegetable tanning, natural additives, and specialty formulations will continue to support demand across mature and emerging applications.

Product Type Analysis

Hydrolysable tannins accounted for 59.6% share of the Tannin Market, making them the leading product type. These tannins are valued for their chemical reactivity, light color properties, and use in applications that require specific performance characteristics. The segment is supported by demand from leather processing, food and beverage clarification, pharmaceutical formulations, nutraceutical from leather processing, food and beverage clarification products, and specialty industrial uses.

Hydrolysable tannins are commonly associated with sources such as gallnut, tara, chestnut, and other plant materials rich in gallic or ellagic acid derivatives. Hydrolysable tannins are expected to maintain strong demand because they offer functional advantages in applications where color stability, purity, and controlled reactivity are important. Their use in premium leather, natural extracts, and health-focused products is likely to support future growth.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFApplication Analysis

The leather industry led the Tannin Market with 67.6% share, supported by the long-standing use of tannins in vegetable tanning. Tannins help bind with collagen in hides and skins, improving leather stability, durability, texture, and resistance to decomposition. The growth of this segment can be attributed to demand for high-quality leather products used in footwear, furniture, automotive interiors, fashion accessories, saddlery, and luxury goods.

Vegetable-tanned leather is valued for its natural finish, firm structure, aging character, and lower dependence on synthetic tanning inputs. The leather industry is expected to remain the largest application area as producers continue to use tannins for specialty and premium leather processing. Demand will be supported by interest in natural tanning agents, sustainable leather production, and high-value leather goods.

Regional Analysis

Europe held 36.2% share of the Tannin Market, supported by strong demand from leather goods, wine processing, food and beverage applications, pharmaceuticals, and specialty chemicals. The region has a long history of vegetable tanning and a strong base of premium leather, fashion, footwear, furniture, and luxury product manufacturing. The growth of Europe can be linked to increasing preference for natural ingredients, sustainable processing, and high-quality leather production.

Tannins are also used in wine clarification, food applications, wood adhesives, and health-related formulations, which supports diversified demand across the region. Europe is expected to remain a leading regional market due to its strong focus on quality, traceability, environmental standards, and natural material use. Future demand is likely to remain strong for plant-based tannins, hydrolysable tannins, vegtable tanning agents, and specialty tannin extracts.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Europe market leadership | +2.1% | Europe, 36.2% share in 2025 | Leads premium demand. |

Asia Pacific leather processing demand | +1.7% | China, India, Japan, Southeast Asia | Drives volume growth. |

North America natural ingredient adoption | +1.2% | U.S. and Canada | Supports food and health use. |

Latin America plant source availability | +0.9% | Brazil, Argentina, Chile | Strengthens raw supply. |

Middle East and Africa emerging adoption | +0.6% | GCC, South Africa | Shows gradual demand. |

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Plant-based tannin adoption | +1.8% | Europe, North America, Asia Pacific | Supports natural sourcing. |

Hydrolysable tannins gaining traction | +1.5% | Europe and developed markets | Drives premium applications. |

Use in wine clarification and stabilization | +1.2% | Europe, North America, Latin America | Supports beverage quality. |

Sustainable leather tanning solutions | +1.1% | Europe, Asia Pacific | Improves eco-positioning. |

Tannin-based bioadhesive innovation | +0.9% | Europe, North America | Builds industrial value. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Ingredient Manufacturers | +1.5% | Global | Expands tannin supply. |

Leather Chemical Producers | +1.3% | Europe, Asia Pacific, Latin America | Supports tanning demand. |

Food and Beverage Companies | +1.1% | Europe, North America, Asia Pacific | Drives natural additive use. |

Pharmaceutical and Nutraceutical Investors | +1.0% | Europe, U.S., Japan | Supports health applications. |

Sustainable Materials Investors | +0.9% | Europe, North America | Funds bio-based innovation. |

Segment Covered in the Report

By Source

Plant

Brown Algae

By Product Type

Hydrolysable Tannins

Condensed Tannins

Phlorotannins

Others

By Application

Pharmaceutical and Nutraceutical

Leather Industry

Wood Industry

Others

By Region

Asia Pacific

North America

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand from leather processing | +1.9% | Europe, Asia Pacific, Latin America | Drives core usage. |

Growth in wine and beverage applications | +1.5% | Europe, North America, Asia Pacific | Supports premium demand. |

Increasing use in pharmaceuticals and nutraceuticals | +1.3% | Europe, U.S., Japan, China | Expands health applications. |

Demand for natural plant-based ingredients | +1.1% | Europe, North America | Supports clean-label adoption. |

Growth in wood adhesive and industrial uses | +0.9% | Europe, Asia Pacific | Broadens application base. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Raw material supply fluctuations | -0.9% | Europe, Asia Pacific, Latin America | Affects production stability. |

High extraction and processing cost | -0.8% | Global producers | Pressures margins. |

Quality variation in plant sources | -0.7% | Global | Impacts product consistency. |

Competition from synthetic alternatives | -0.6% | Industrial applications | Limits replacement speed. |

Regulatory checks for food and pharma use | -0.5% | Europe, North America, Asia Pacific | Raises compliance needs. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Expansion of hydrolysable tannins | +1.7% | Europe, North America, Asia Pacific | Supports high-value use. |

Growth in natural food preservatives | +1.4% | Europe, U.S., Japan, India | Opens food applications. |

Rising demand in nutraceutical formulations | +1.2% | Developed and urban markets | Builds health demand. |

Bio-based wood adhesive development | +1.0% | Europe, North America | Supports sustainable materials. |

Increasing use in animal feed additives | +0.9% | Europe, Asia Pacific, Latin America | Expands agricultural demand. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining stable tannin concentration | -0.8% | Global | Affects formulation quality. |

Dependence on plant-based feedstock | -0.7% | Europe, Asia Pacific, Latin America | Creates supply risk. |

Limited standardization across grades | -0.6% | Global | Slows buyer adoption. |

Environmental pressure on extraction processes | -0.5% | Europe, North America | Increases operating controls. |

Price pressure in leather applications | -0.5% | Asia Pacific and Latin America | Reduces margin flexibility. |

Recent Developments

In May 2026, According to IntechOpen review highlighted tannin supplementation as a potential tool for reducing methane formation in ruminants. The review stated that methane formation can represent a 2% to 12% loss of ingested energy in animals, while tannin use may help reduce methane and ammonia production by affecting rumen microbes. The study also noted that an ideal dietary tannin range of 2 to 3 g per 100 g of dry matter is recommended for goats, sheep, and cattle, while effectiveness is higher in diets with more than 60% roughage.

In 2026, According to Green Chemistry assessed industrial-scale tannin production from Norway spruce bark for leather applications. The study estimated a minimum selling price of €2.1 per kg for spruce bark tannin and reported a global warming potential of 4.5 kg CO₂-eq per kg of tannin product. This development is important because bark is an underused biomass stream, and its conversion into tannin powder can support more sustainable leather tanning.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 4.9 Billion |

Forecast Revenue (2035) | USD 9.8 Billion |

CAGR (2025-2035) | 7.2% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Source (Plant, Brown Algae), By Product Type (Hydrolysable Tannins, Condensed Tannins, Phlorotannins, Others), By Application (Food and Beverage, Pharmaceutical and Nutraceutical, Leather Industry, Wood Industry, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Ajinomoto Co., Inc., Silvateam Group, Laffort Holding, TANAC, Ulrich Holding GmbH, Esseco Group Srl, Tanin d.d. Sevnica, Tannin Corporation, NTE Company and Other Key Players |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Environment Analysis

The Tannin Market is shaped by demand from leather tanning, food and beverage, wine processing, animal nutrition, wood adhesives, water treatment, pharmaceuticals, and nutraceutical applications. Competition is led by companies that can secure reliable plant-based raw materials, maintain extraction quality, and supply consistent tannin grades for industrial and food-related uses. The market is strongly linked with natural ingredients, bio-based chemistry, clean-label processing, and the shift toward lower-impact materials.

Leather remains one of the most established application areas for tannins. Vegetable tannins from chestnut, quebracho, tara, mimosa, myrobalan, and wattle are used in tanning and retanning processes to improve leather body, feel, fullness, and appearance. Companies with strong sourcing networks and technical service for tanneries hold a stronger competitive position because leather performance depends on extract type, penetration, color tone, and process control.

The wine and beverage segment is another important competitive area. Oenological tannins are used to support clarification, color stability, antioxidant protection, mouthfeel, and aging performance in wine production. Suppliers that provide specialized tannins for fermentation, aging, finishing, and oxidation control are better positioned in wineries and beverage processing applications.

Implementation Complexity & Technology Readiness

Tannin Technology / Application | Implementation Complexity | Technology Readiness | Market Position |

|---|---|---|---|

Vegetable tannins for leather | Moderate | High | Well-established in premium leather tanning. |

Hydrolysable tannins | Moderate | High | Used across food, wine, pharma, and specialty chemicals. |

Condensed tannins | Moderate | High | Widely used for binding and polyphenol activity. |

Oenological tannins | Moderate | High | Mature use in wine processing. |

Tannic acid | Moderate to High | High | Used where purity and quality are critical. |

Tannin-based animal nutrition products | Moderate | Moderate to High | Rising use in plant-derived feed additives. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Södra Skogsägarna

Ajinomoto Co., Inc.

Silvateam Group

Laffort Holding

TANAC

Ulrich Holding GmbH

Esseco Group Srl

Tanin d.d. Sevnica

Tannin Corporation

NTE Company Pty Ltd

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Oxygen Market to Exceed USD 171.1 Billion by 2035

Global Oxygen Market Size, Share Analysis By Form (Gas, Liquid, Solid), By Type (Industrial, Medical), By Application (Metals and Mining, Chemical Industry, Oil and Gas, Healthcare, Pharmaceutical, Other Applications), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Printing Ink Market to Hit USD 30.6 Billion by 2035

Global Printing Ink Market Size, Go-to-Market Strategy Analysis By Type (Solvent-Based, Water-Based, Oil-Based, UV, UV-LED, Others), By Process (Lithographic Printing, Flexographic Printing, Gravure Printing, Digital Printing, Others), By Application (Packaging, Commercial and Publication, Textiles, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Methanol Market to Exceed USD 64.1 Billion by 2035

Global Methanol Market Size By Feedstock (Natural Gas, Coal, Biomass and Renewables), By Derivative (Formaldehyde, Acetic Acid, MTBE, DME, Gasoline Blending, Biodiesel, MTO/MTP, Solvent, Others), By Sub-derivatives (Gasoline additives, Olefins, UF/PF resins, VAM, Polyacetals, MDI, PTA, Acetate Esters, Acetic anhydride, Fuels, Others), By Application (Construction, Automotive, Electronics, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Xylose Market to hit USD 7.0 Billion by 2035

Global Xylose Market Size By Type (D-Xylose, L-Xylose, DL-Xylose), By Form (Powder, Liquid, Granules), By Source (Wood, Corncobs, Sugarcane Bagasse, Others), By Application (Food and Beverage, Cosmetics and Personal Care, Animal Feed, Pharmaceuticals, Biofuel Industry, Others) , By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035