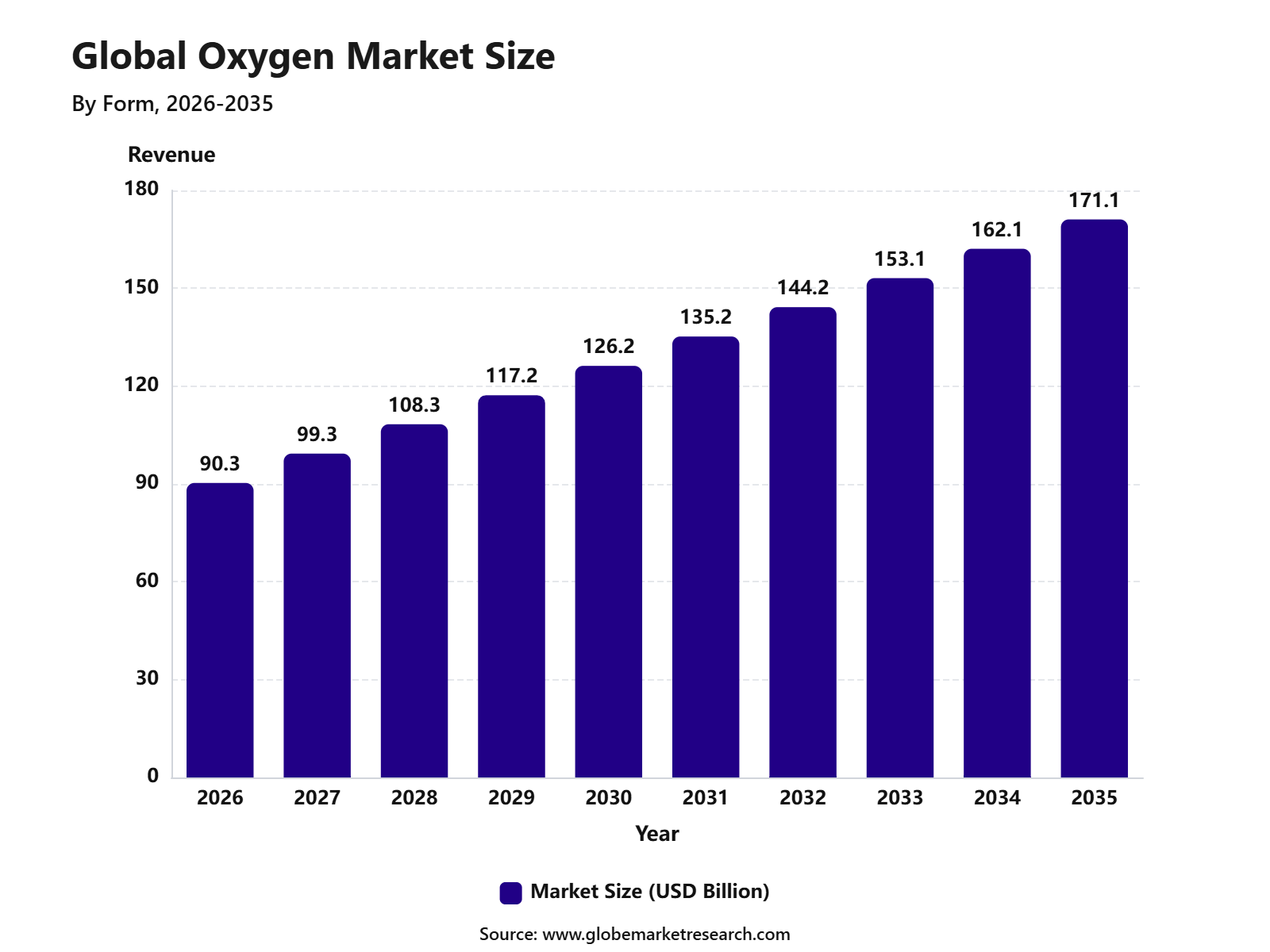

Revenue, 2026

$ 90.3 Bn

Forecast, 2035

$ 171.1 Bn

CAGR, 2025-2035

6.6%

Report Coverage

Global

Market Size and Forecast

The Global Oxygen Market was valued at USD 90.3 billion in 2025 and is projected to reach USD 171.1 billion by 2035, growing at a CAGR of 6.6% from 2025 to 2035. The growth of the market can be attributed to rising oxygen demand across healthcare, steel production, chemical processing, metal fabrication, wastewater treatment, and energy applications. Increasing use of medical oxygen in hospitals, emergency care, home healthcare , and respiratory disease treatment is also supporting steady market expansion.

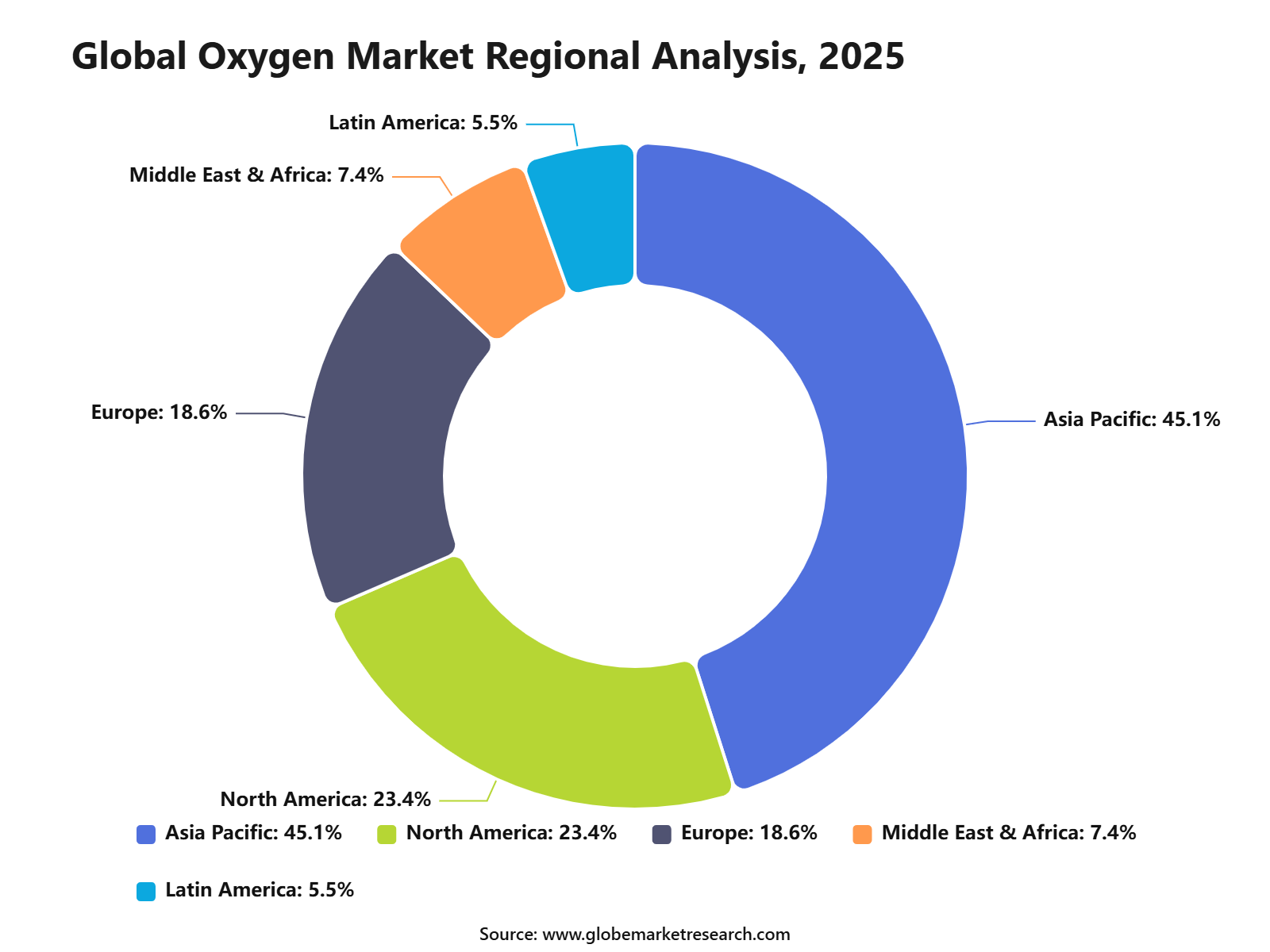

Asia Pacific held the largest regional share of 45.1% in 2025, valued at approximately USD 40.7 billion . The region’s dominance can be linked to strong industrial production, expanding healthcare infrastructure, high steel manufacturing output, and rising demand from chemical and electronics industries. Countries such as China, India, Japan, South Korea, and Southeast Asian economies continue to support market growth through large-scale industrial gas consumption, hospital oxygen demand, and investment in manufacturing capacity.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Gas form led the oxygen market with 88.1% share , supported by its wide use in industrial operations, healthcare delivery, metal processing, chemical production, and wastewater treatment.

Industrial oxygen accounted for 66.2% share by type, driven by strong demand from manufacturing, steelmaking, welding, cutting, refining, and other heavy industrial applications.

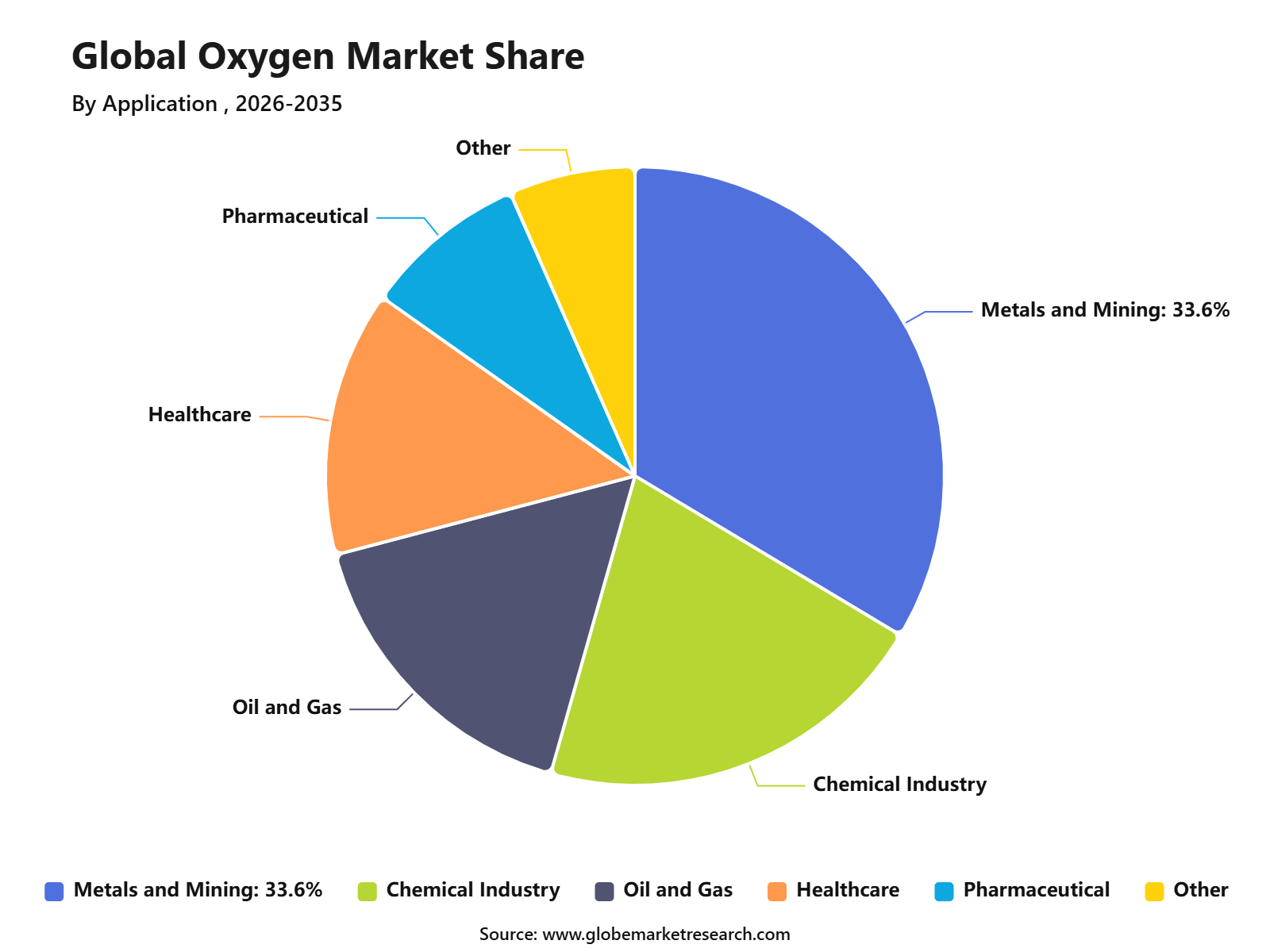

Metals and mining captured 33.6% share by application, supported by oxygen use in smelting, steel production, ore processing, combustion enhancement, and metal fabrication.

Asia Pacific led the oxygen market with 45.1% share, supported by strong industrial output, large steel production capacity, expanding healthcare infrastructure, and rising demand from manufacturing sectors.

Go-to-Market and Sales Economics

The Oxygen Market needs a dual go-to-market strategy because demand is divided between industrial oxygen and medical oxygen. Industrial suppliers should target steel plants, metal fabrication units, glass manufacturers, chemical producers, wastewater treatment plants, pulp and paper mills, mining companies, aerospace users, and welding operations. Medical oxygen suppliers should focus on hospitals, emergency care centers, homecare providers, ambulances, surgery centers, and oxygen therapy systems. The Lancet Global Health Commission reported in 2025 that 374 million people need medical oxygen each year, including 364 million for acute medical and surgical needs and 9 million for long-term oxygen needs, showing the scale of healthcare-linked demand.

Sales economics are strongest when suppliers offer reliable supply, storage, delivery systems, cylinder management, PSA plant installation, liquid oxygen tanks, pipeline supply, and service contracts. In industrial applications, long-term contracts with steel, chemicals, and fabrication customers can support stable offtake. In healthcare, reliability is more important than price alone because oxygen is an essential medicine and must be available without interruption. WHO states that oxygen produced by air liquefaction must contain not less than 99.5% oxygen , while PSA plants are specified at 93% ± 3% oxygen , which makes quality assurance central to supplier credibility.

Risk Factors & Market Barriers

The main risk factor is high operating cost because oxygen production is energy-intensive. Cryogenic air separation, compression, liquefaction, storage, and transport require continuous power and strong plant reliability. When electricity, fuel, or logistics costs rise, oxygen producers face margin pressure, especially in bulk industrial supply contracts where price escalation may be limited. The latest U.S. oxygen PPI data shows that prices remain elevated versus long-term index history, which confirms that cost control is still a central issue for producers and buyers.

Another barrier is supply-chain reliability. Medical and industrial oxygen both require dependable production, storage, and distribution, but shortages can occur when demand surges or when transport networks are weak. WHO states that fewer than half of health facilities in low- and middle-income countries have uninterrupted access to medical oxygen. This creates both a market barrier and a public health gap, especially in rural hospitals, emergency care, neonatal care, surgery, and respiratory treatment.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape for oxygen is spread across steelmaking, chemicals, refining, welding, cutting, glass, pulp and paper, wastewater treatment, aquaculture, healthcare, home respiratory care, emergency medicine, semiconductors, aerospace, and clean energy applications. Steel remains a core industrial revenue base because basic oxygen furnace steelmaking uses large oxygen volumes to convert molten iron into steel. Britannica notes that oxygen consumption in basic oxygen steelmaking is about 110 cubic metres per ton of steel , while large converters can use oxygen flow rates above 800 cubic metres per minute .

High-purity oxygen is also becoming more important in semiconductor and advanced manufacturing supply chains. In April 2026, Air Liquide announced a EUR 200 million , or about USD 236 million , investment in Japan to build and operate two new industrial gas production units in Hiroshima. These units are expected to supply ultra-high-purity nitrogen, oxygen, and argon for next-generation AI chip production by the end of 2028. This shows that oxygen revenue is expanding beyond heavy industry into high-value electronics and advanced manufacturing applications.

Financial Impact

The financial impact can be positive for oxygen suppliers with efficient air separation plants, low energy cost, strong logistics, high cylinder utilization, and long-term customer contracts. Bulk oxygen supply to steel, refining, chemicals, glass, and hospitals can support stable revenue when contracts include take-or-pay terms, energy pass-through clauses, and service agreements. On-site generation can also improve customer retention because the supplier may provide equipment, maintenance, purity monitoring, and technical service over a longer period.

Financial risk remains linked to electricity prices, plant downtime, cylinder losses, transport cost, safety incidents, and compliance spending. Medical oxygen suppliers also face additional costs from CGMP compliance, labeling, traceability, quality testing, and container closure controls. The strongest financial resilience is expected from companies that serve both industrial and medical buyers, operate regional production networks, invest in on-site systems, and provide reliable quality documentation for regulated customers.

Form Analysis

Gas led the Oxygen Market with 88.1% share , supported by its wide use across metals, mining, healthcare, chemicals , wastewater treatment , glass production, pulp and paper, and industrial combustion. Gaseous oxygen is preferred in many operations because it can be supplied through pipelines, cylinders, and on-site generation systems.

The growth of this segment can be attributed to strong demand from continuous industrial processes that require a steady oxygen supply. Steel plants, mining facilities, refineries, hospitals, and chemical units depend on gaseous oxygen for oxidation, combustion support, enrichment, and process efficiency.

Gaseous oxygen is expected to remain the leading form because it offers operational flexibility and reliable supply for both large and small users. Demand will remain strong where industries need high-purity oxygen for production, treatment, safety, and critical care applications.

Type Analysis

Industrial oxygen accounted for 66.2% share , making it the leading type segment in the Oxygen Market. The segment is supported by strong use in steelmaking, metal cutting, welding, mining, chemical processing, glass manufacturing, wastewater treatment, and energy-related applications.

The growth of industrial oxygen is being driven by rising manufacturing activity and the need for efficient combustion and oxidation processes. In metal production, oxygen helps improve furnace efficiency, increase output, and support cleaner and more controlled processing.

Industrial oxygen demand is expected to remain steady as heavy industries continue to invest in capacity expansion, productivity improvement, and process optimization. The segment is also likely to benefit from on-site oxygen generation systems, which help large users reduce transport dependency and improve supply reliability.

Application Analysis

Metals and mining led the application segment with 33.6% share , supported by the strong use of oxygen in steelmaking, smelting, refining, mineral processing, and metal cutting. Oxygen is widely used in basic oxygen furnaces, blast furnace enrichment, non-ferrous metal processing, and mining-related oxidation processes.

The segment’s growth can be linked to the continued demand for steel, aluminum, copper, and other metals used in construction, automotive, energy, machinery, and infrastructure. Oxygen improves process temperature, reaction speed, and fuel efficiency, which makes it an important input in metal production.

Metals and mining are expected to remain a major demand center for oxygen due to large production volumes and continuous operating requirements. Future demand will be supported by industrial expansion in Asia Pacific, modernization of steel plants, and the need to improve energy efficiency in metal processing.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Analysis

Asia Pacific led the Oxygen Market with 45.1% share , supported by strong manufacturing activity, large steel production capacity, expanding mining operations, and rising healthcare demand. China, India, Japan, South Korea, and Southeast Asian countries remain major contributors due to their large industrial base and growing infrastructure needs.

The region’s dominance can be attributed to high demand from steelmaking, chemicals, electronics, healthcare, wastewater treatment, and energy-intensive industries. Rapid urbanization and industrial expansion continue to support oxygen consumption across both bulk industrial gases and medical oxygen applications.

Asia Pacific is expected to remain the leading regional market as industrial production and healthcare infrastructure continue to expand. Demand is likely to remain strong for gaseous oxygen, industrial oxygen, on-site generation systems, and oxygen supply solutions for metals and mining applications.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +2.0% | Asia Pacific, 45.1% share in 2025 | Leads industrial demand. |

China and India manufacturing growth | +1.4% | China and India | Drives oxygen consumption. |

North America healthcare and industrial demand | +1.0% | U.S. and Canada | Supports stable growth. |

Europe environmental and industrial applications | +0.8% | Germany, UK, France, Italy | Drives advanced usage. |

Middle East and Africa infrastructure expansion | +0.6% | GCC, South Africa, Egypt | Builds future demand. |

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Industrial oxygen demand growth | +1.6% | Asia Pacific, North America, Europe | Leads market consumption. |

Gas-form oxygen dominance | +1.3% | Global | Supports broad usage. |

Medical oxygen system upgrades | +1.1% | Global healthcare markets | Improves supply reliability. |

Oxygen enrichment in industrial processes | +0.9% | Steel, chemicals, wastewater treatment | Improves process efficiency. |

Digital monitoring of gas supply systems | +0.7% | Developed markets | Enhances operational control. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Industrial Gas Producers | +1.5% | Global | Expands oxygen capacity. |

Healthcare Infrastructure Investors | +1.2% | Asia Pacific, Africa, Latin America | Supports medical supply. |

Steel and Metallurgy Companies | +1.1% | Asia Pacific, Europe, North America | Drives bulk oxygen use. |

Private Equity Firms | +0.8% | Asia Pacific, Europe, North America | Supports asset scaling. |

Clean Energy and Hydrogen Investors | +0.7% | Europe, China, India, Middle East | Creates by-product opportunity. |

Segment Covered in the Report

By Form

Gas

Liquid

Solid

By Type

Industrial

Medical

By Application

Metals and Mining

Chemical Industry

Oil and Gas

Healthcare

Pharmaceutical

Other

By Region

Asia Pacific

North America

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand from metals and mining | +1.7% | Asia Pacific, North America, Latin America | Drives industrial usage. |

Growth in healthcare oxygen demand | +1.4% | Global | Supports medical supply needs. |

Expansion of chemical manufacturing | +1.1% | China, India, U.S., Europe | Increases process demand. |

Use in wastewater treatment and environmental applications | +0.9% | Europe, North America, Asia Pacific | Supports treatment efficiency. |

Growth in welding, cutting, and fabrication | +0.8% | Asia Pacific, Middle East, North America | Expands industrial consumption. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High energy cost in oxygen production | -0.9% | Global | Pressures operating margins. |

Storage and transportation complexity | -0.8% | Emerging and remote markets | Limits supply reach. |

Safety risks in handling oxygen | -0.6% | Global industrial users | Raises compliance needs. |

Price pressure from bulk buyers | -0.5% | Industrial markets | Reduces margin flexibility. |

Infrastructure gaps in medical oxygen supply | -0.5% | Africa, Latin America, rural Asia | Slows access expansion. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

On-site oxygen generation systems | +1.5% | Hospitals, steel plants, industrial sites | Reduces supply dependency. |

Expansion of medical oxygen infrastructure | +1.3% | Asia Pacific, Africa, Latin America | Builds healthcare access. |

Growth in green hydrogen and electrolysis projects | +1.1% | Europe, China, India, Middle East | Creates oxygen by-product value. |

Rising use in steel decarbonization | +1.0% | China, India, Europe, U.S. | Supports cleaner steelmaking. |

Industrial gas pipeline and bulk supply expansion | +0.8% | Asia Pacific, North America, GCC | Improves supply efficiency. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining uninterrupted supply | -0.8% | Healthcare and heavy industries | Requires reliable logistics. |

Energy-intensive air separation process | -0.7% | Global producers | Increases production cost. |

Cylinder availability and distribution issues | -0.6% | Emerging markets | Affects medical access. |

Compliance with purity and safety standards | -0.5% | Healthcare and industrial sectors | Raises quality requirements. |

Demand volatility from cyclical industries | -0.5% | Metals, mining, manufacturing | Impacts revenue stability. |

Recent Developments

January 2026, Linde’s new air separation unit in Brownsville, Texas was expected to start up in the first quarter of 2026. The facility is designed to deliver liquid oxygen, nitrogen, and argon for space operations, while also improving merchant industrial gas capacity across Texas. This development is important because liquid oxygen is a critical oxidizer for launch systems, and space activity is becoming a stronger demand source for industrial gas suppliers.

March 2026, INOX Air Products was reported to be planning a USD 1 billion initial public offering in Mumbai. The company operates nearly 50 locations across India, produces more than 4,200 tonnes per day of liquid gases, and serves over 1,800 customers across 18 industries. This is important for the oxygen market because India’s industrial and medical gas demand is expanding across steel, chemicals, pharmaceuticals, textiles, electronics, and healthcare.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 90.3 Billion |

Forecast Revenue (2035) | USD 171.1 Billion |

CAGR (2025-2035) | 6.6% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Form (Gas, Liquid, Solid), By Type (Industrial, Medical), By Application (Metals and Mining, Chemical Industry, Oil and Gas, Healthcare, Pharmaceutical, Other Applications) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Linde PLC, Air Liquide, Air Products and Chemicals, Inc., NIPPON SANSO HOLDINGS CORPORATION, Messer SE & Co. KGaA, AIR WATER INC., INOX-Air Products Inc., Hangzhou Oxygen Group Co., Ltd., Gulf Cryo, Yingde Gas Shanghai |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Environment Analysis

The Oxygen Market is a mature and essential industrial gas market, supported by demand from healthcare, metals and mining, chemicals, oil and gas, pharmaceuticals, water treatment, food processing, glass, pulp and paper, semiconductors, and aerospace. Competition is led by companies that can provide reliable oxygen supply through bulk liquid oxygen, compressed gas cylinders, on-site oxygen generation systems, pipeline supply, and medical oxygen services. The market is strongly influenced by supply reliability, purity standards, plant availability, distribution reach, and safety compliance.

The competitive landscape is concentrated among large industrial gas companies, regional gas suppliers, and specialized oxygen system providers. Large suppliers hold an advantage because they operate air separation units, cryogenic storage networks, bulk tanker fleets, cylinder filling stations, and healthcare gas service teams. Regional suppliers remain important in cylinder distribution, hospital supply, welding and cutting applications, and small industrial customer service.

Implementation Complexity & Technology Readiness

Oxygen Technology / Application | Implementation Complexity | Technology Readiness | Market Position |

|---|---|---|---|

Cryogenic air separation units | Very High | High | Core route for large-scale oxygen supply. |

Bulk liquid oxygen supply | High | High | Strong fit for hospitals and large users. |

Compressed oxygen cylinders | Low to Moderate | High | Widely used for flexible distribution. |

On-site PSA oxygen plants | High | High | Supports local oxygen generation. |

VPSA and VSA oxygen systems | High | Moderate to High | Suitable for larger on-site industrial needs. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Linde PLC

Air Liquide

Air Products and Chemicals, Inc.

NIPPON SANSO HOLDINGS CORPORATION

Messer SE & Co. KGaA

AIR WATER INC.

INOX-Air Products Inc.

Hangzhou Oxygen Group Co., Ltd.

Gulf Cryo

Yingde Gas Shanghai

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Ethylene Market Size to Hit USD 306.4 Billion by 2035

Global Ethylene Market Size, Share Analysis By Feedstock (Naphtha, Ethane, Propane, Butane, Others), By Derivative (Polyethylene, Ethylene Oxide, Ethylene Dichloride, Ethylbenzene, Others), By Application (Packaging, Construction, Automotive, Consumer Goods, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Semiconductor Chemicals Market Size to Exceed USD 75.6 Bn by 2035

Global Semiconductor Chemicals Market Size, Share Analysis By Chemical Type (Acid and Base Chemicals, High-Performance Polymers, Adhesives, Solvents, Others), By Purity Level (4N, 5N, 6N and Above), By End Use (Integrated Circuits, Printed Circuit Boards, Discrete Semiconductors, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Tannin Market to Hit USD 9.8 Billion by 2035

Global Tannin Market Size, Share and Go-to-Market Strategy Analysis By Source (Plant, Brown Algae), By Product Type (Hydrolysable Tannins, Condensed Tannins, Phlorotannins, Others), By Application (Food and Beverage, Pharmaceutical and Nutraceutical, Leather Industry, Wood Industry, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Printing Ink Market to Hit USD 30.6 Billion by 2035

Global Printing Ink Market Size, Go-to-Market Strategy Analysis By Type (Solvent-Based, Water-Based, Oil-Based, UV, UV-LED, Others), By Process (Lithographic Printing, Flexographic Printing, Gravure Printing, Digital Printing, Others), By Application (Packaging, Commercial and Publication, Textiles, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035