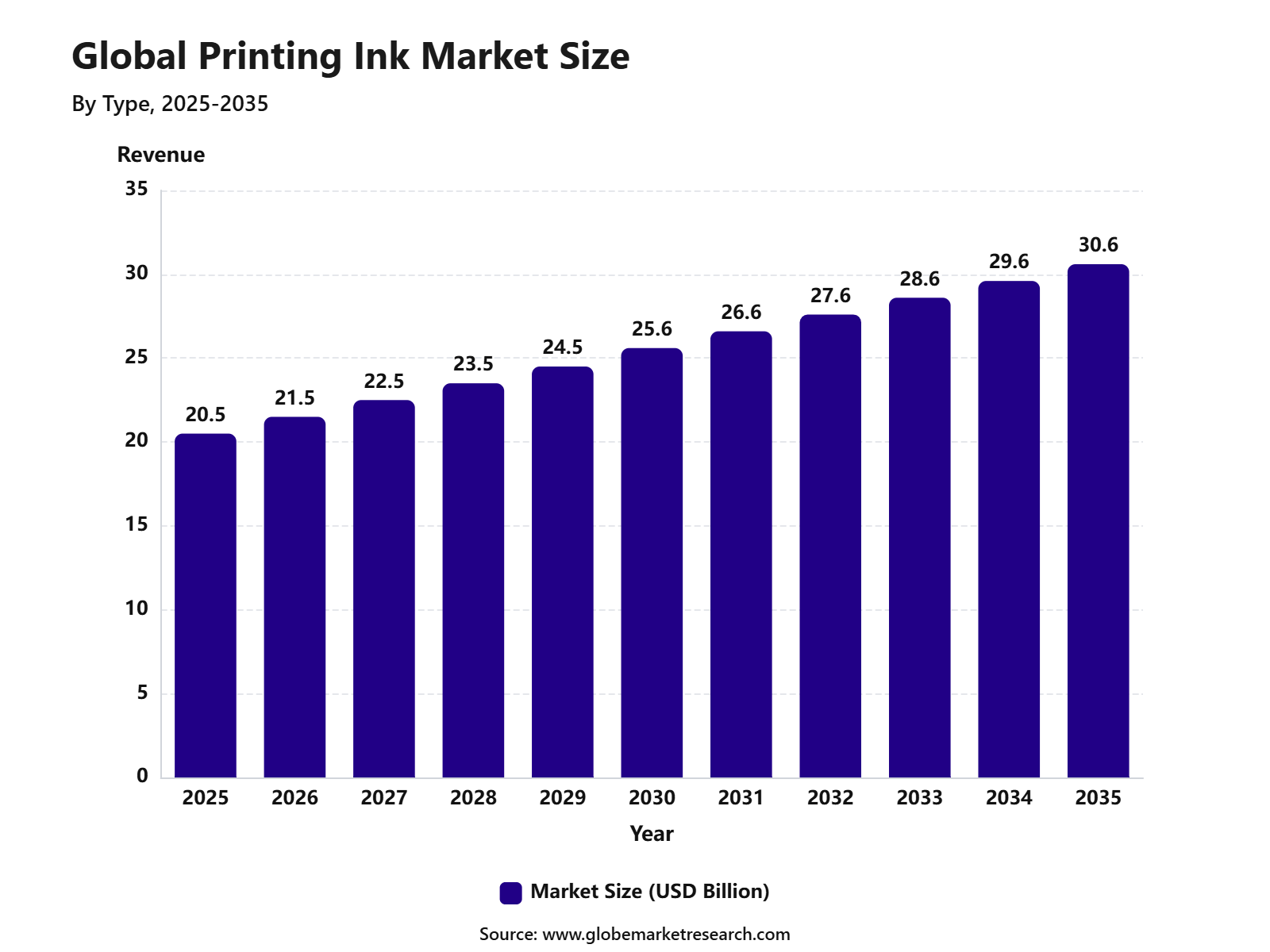

Revenue, 2025

$ 20.5 Bn

Forecast, 2035

$ 30.6 Bn

CAGR, 2025-2035

4.1%

Report Coverage

Global

Market Size and Forecast

The Global Printing Ink Market was valued at USD 20.5 billion in 2025 and is projected to reach USD 30.6 billion by 2035, growing at a CAGR of 4.1% from 2025 to 2035. The growth of the market can be attributed to rising demand from packaging, labels, publishing, commercial printing, and flexible packaging applications. Increasing use of printed packaging in food and beverages, consumer goods, e-commerce, and pharmaceuticals is also supporting steady market expansion.

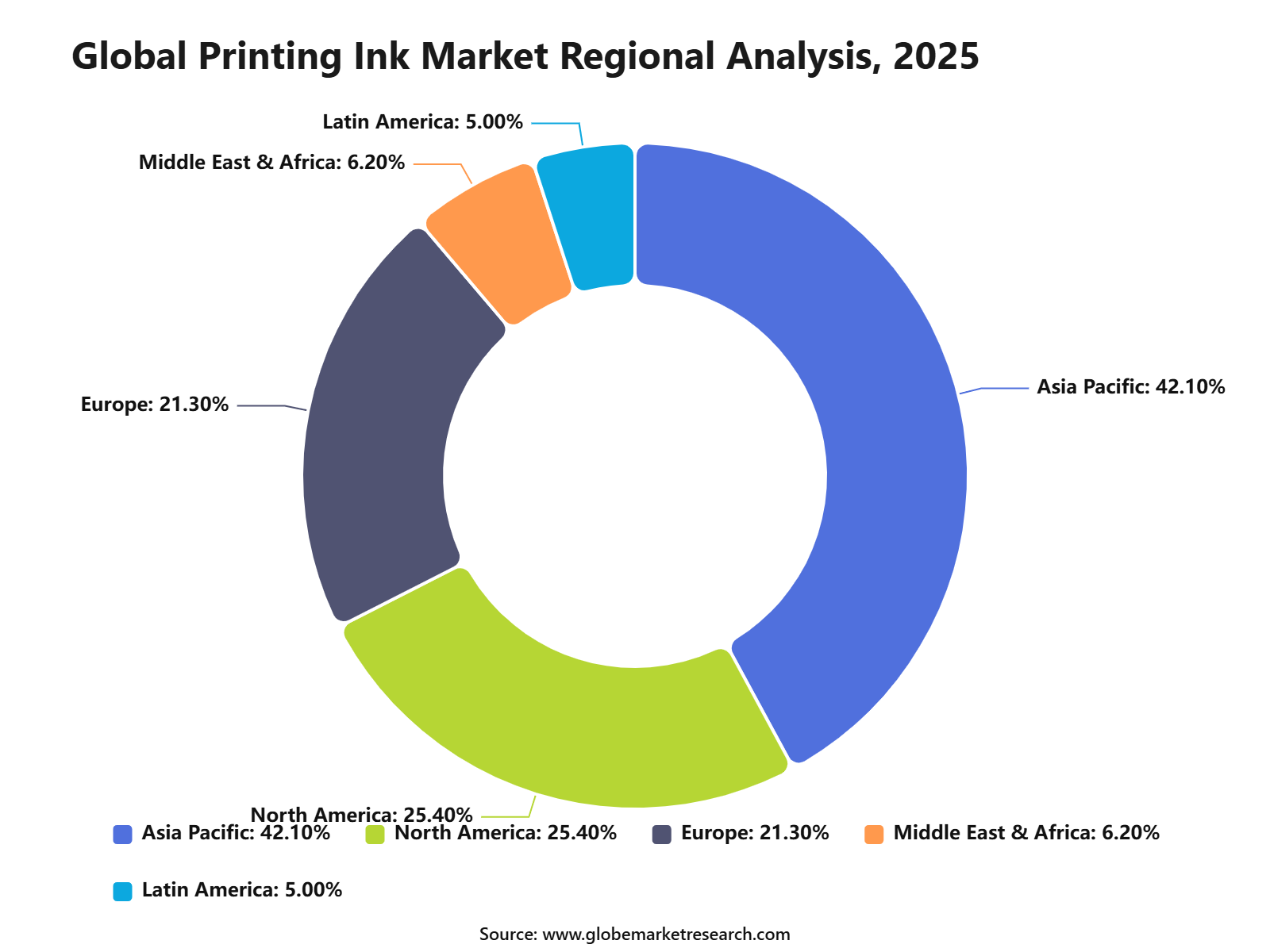

Asia Pacific held the largest regional share of 42.1% in 2025, valued at approximately USD 8.6 billion. The region’s dominance can be linked to strong packaging production, rapid industrialization, expanding consumer goods manufacturing, and rising demand for cost-effective printing solutions across China, India, Japan, South Korea, and Southeast Asian countries. Growth is further supported by increasing demand for flexible packaging, digital printing, and eco-friendly ink formulations.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Oil-based inks led the type segment with 40.70% share, supported by strong use in commercial printing, packaging, publishing, and industrial print applications.

Lithographic printing accounted for 32.95% share by process, driven by its high print quality, cost efficiency, and wide adoption across labels, cartons, books, and advertising materials.

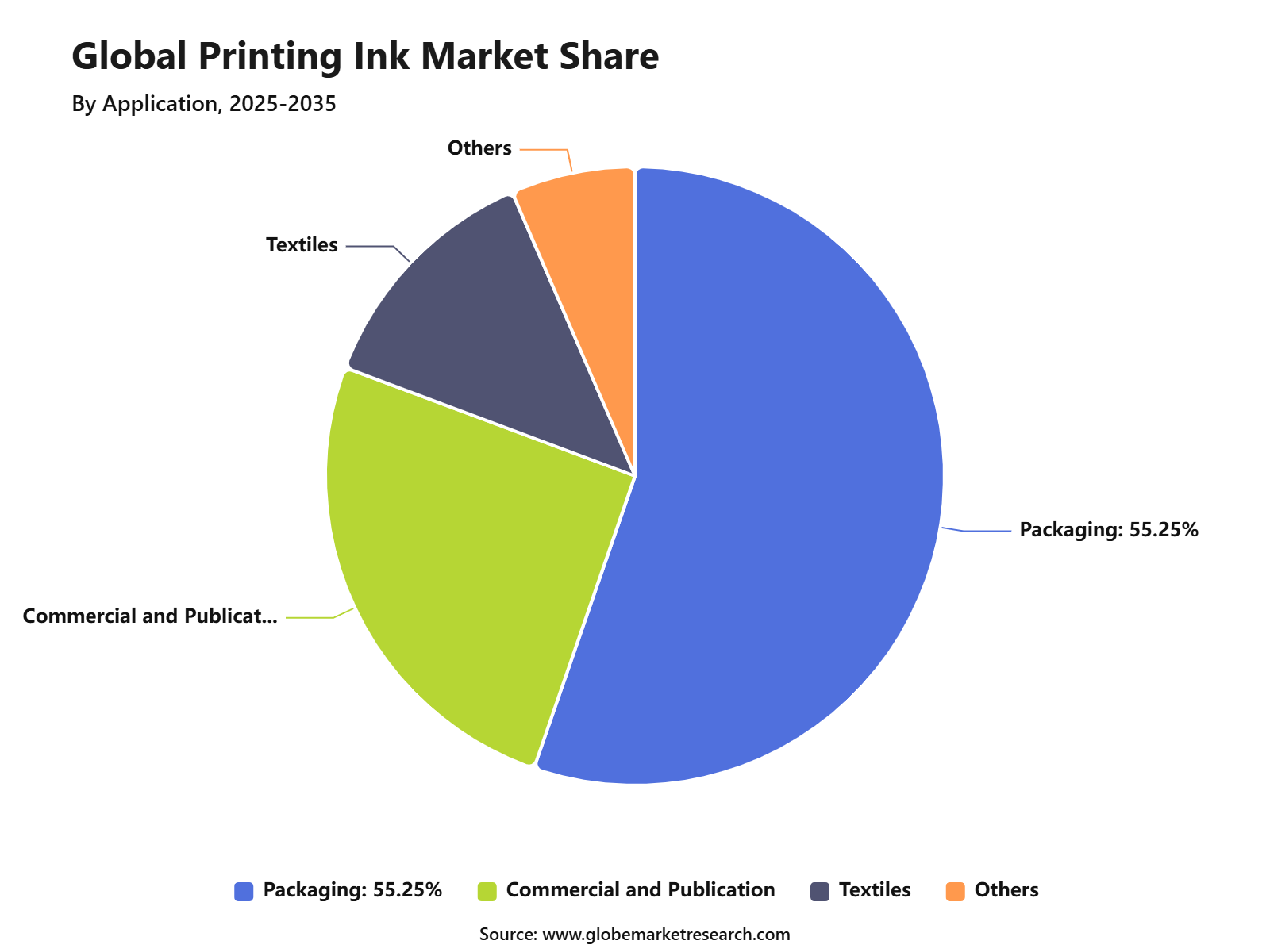

Packaging captured 55.25% share by application, supported by rising demand for printed labels, flexible packaging, cartons, food packaging, and consumer goods branding.

Asia Pacific led the global printing ink market with 42.1% share, supported by strong packaging production, expanding e-commerce, high manufacturing activity, and growing demand from food, beverage, and consumer goods industries.

Go-to-Market and Sales Economics

The Printing Ink Market needs an application-led go-to-market strategy because buyers choose inks based on substrate, print method, drying system, compliance needs, and final packaging use. Suppliers should position inks separately for flexible packaging, labels, folding cartons, corrugated boxes, commercial print, publishing, textiles, metal cans, plastic films, paperboard, and digital printing. Packaging remains the most stable demand base because food, beverages, pharmaceuticals, personal care, e-commerce, and consumer goods require printed labels, barcodes, branding, safety information, and traceability codes.

In the U.S., retail e-commerce sales reached USD 326.7 billion in Q1 2026, up 9.7% from Q1 2025, supporting demand for printed shipping packs, labels, cartons, and flexible packaging. Sales economics are strongest when ink suppliers sell technical value rather than only color or volume. Packaging buyers need inks with strong adhesion, low migration, fast curing, rub resistance, chemical resistance, print consistency, and food-contact suitability where required. Cost control is also important because the U.S. Producer Price Index for printing ink manufacturing reached 202.829 in May 2026, up from 196.757 in April 2026, showing that input and manufacturing cost pressure remains active.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape is spread across flexible packaging inks, label inks, corrugated inks, folding carton inks, publication inks, commercial printing inks, digital inks, textile inks, metal decorating inks, UV inks, water-based inks, solvent-based inks, and specialty security inks. Packaging and labels are expected to remain the most reliable revenue areas because they are tied to food, beverages, healthcare, retail, logistics, and e-commerce. Digital inks also offer stronger value where short-run printing, customization, variable data, and fast design changes are required.

Trade data shows that printing inks remain a meaningful global traded product. In 2024, the leading importers of non-black printing ink under HS 321519 were the European Union at USD 602.38 million, the United States at USD 485.91 million, France at USD 353.26 million, Germany at USD 328.68 million, and Mexico at USD 212.39 million. For black printing ink under HS 321511, the United States imported USD 135.04 million in 2024, followed closely by the European Union at USD 134.44 million.

Financial Impact

The financial impact can be positive for ink companies that serve packaging, labels, food-safe applications, digital printing, and specialty industrial uses. Better margins can be created through low-migration inks, UV and EB-curable systems, water-based inks, high-performance pigments, technical service, and customer-specific formulations. Suppliers that support compliance documentation, press trials, color matching, and faster problem-solving are better positioned than sellers competing only on price.

Financial risk remains linked to raw material inflation, energy cost, freight, tariff exposure, regulatory reformulation, and slower demand in publication printing. EPA’s VOC and hazardous air pollutant rules, France’s mineral oil restrictions, and packaging recycling targets are increasing reformulation and documentation costs for ink suppliers. The strongest financial resilience is expected from companies that diversify into packaging and labels, reduce solvent exposure, improve supply security, and provide inks that meet both performance and compliance requirements.

Type Analysis

Oil-based inks led the Global Printing Ink Market with 40.70% share, supported by their strong use in commercial printing, packaging, labels, publications, and industrial print applications. These inks are preferred because they offer good adhesion, strong color output, smooth print performance, and suitability for high-volume printing operations. The growth of this segment can be attributed to continued demand from packaging converters, publishers, label printers, and commercial printing companies.

Oil-based inks remain important because they perform well on paperboard, coated paper, labels, cartons, and several packaging substrates. However, the segment is also being shaped by environmental rules, volatile organic compound concerns, and raw material price movements linked to petrochemical inputs. This is encouraging ink producers to improve formulations, reduce emissions, enhance drying performance, and develop more sustainable oil-based ink alternatives.

Process Analysis

Lithographic printing accounted for 32.95% share, making it the leading process segment in the Global Printing Ink Market. The process is widely used for packaging, books, brochures, magazines, catalogs, labels, cartons, and commercial print materials because it provides high-quality output and cost efficiency for medium and large print runs. The segment is supported by strong demand for sharp image reproduction, consistent color quality, and reliable print speed.

Lithographic printing remains important for brand owners and packaging companies that require detailed graphics, readable text, and premium visual appearance. Demand is expected to remain stable across packaging and commercial printing, even as digital printing adoption rises. Lithographic printing continues to be preferred where large-volume production, high print quality, and cost control are important for business operations.

Application Analysis

Packaging led the application segment with 55.25% share, supported by strong demand for printed labels, cartons, flexible packaging, corrugated boxes, food packaging, beverage packaging, pharmaceutical packaging, and consumer goods packaging. Printing inks are essential in packaging because they provide brand identity, product details, regulatory information, barcodes, warning labels, and consumer communication. The growth of this segment can be attributed to rising consumption of packaged food, personal care products, medicines, e-commerce parcels, and retail goods.

As brands compete for shelf visibility and consumer attention, high-quality printed packaging continues to play an important role in product differentiation. Packaging-related ink demand is also being shaped by sustainability and food safety requirements. Manufacturers are focusing on low-migration inks, recyclable packaging compatibility, water-based systems, energy-curable inks, and safer formulations that meet changing regulatory and brand requirements.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Analysis

Asia Pacific led the Global Printing Ink Market with 42.1% share, supported by strong packaging production, expanding manufacturing activity, rising consumer goods demand, and high use of printed labels and flexible packaging. China, India, Japan, South Korea, and Southeast Asian countries remain major contributors to regional ink consumption.

The growth of Asia Pacific is being driven by packaged food demand, e-commerce growth, pharmaceutical production, personal care product sales, and industrial manufacturing. The region also has a large base of printers, converters, packaging companies, and export-oriented manufacturers, which supports steady demand for printing inks.

Asia Pacific is expected to remain the leading regional market as packaging demand continues to rise across food, beverages, healthcare, electronics, and consumer goods. Future opportunities are likely to be seen in sustainable ink systems, flexible packaging inks, low-migration packaging inks, and high-performance inks for labels and cartons.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +1.5% | Asia Pacific, 42.1% share in 2025 | Leads volume demand. |

China and India packaging growth | +1.0% | China and India | Drives regional consumption. |

North America sustainable ink adoption | +0.7% | U.S. and Canada | Supports premium formulations. |

Europe regulation-led transition | +0.6% | Germany, UK, France, Italy | Drives low-VOC inks. |

Latin America and MEA gradual expansion | +0.4% | Brazil, Mexico, GCC, South Africa | Builds steady demand. |

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Packaging remains leading application | +1.0% | Global | Drives core demand. |

Lithographic printing demand | +0.8% | Asia Pacific, Europe, North America | Supports commercial use. |

Shift toward low-VOC inks | +0.7% | Europe, North America, Japan | Improves environmental compliance. |

Growth of digital and inkjet printing | +0.6% | Developed and urban markets | Supports customization. |

Demand for high-performance specialty inks | +0.5% | Labels, films, security printing | Improves product value |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Ink Manufacturers | +0.9% | Global | Expands product portfolios. |

Packaging Companies | +0.8% | Asia Pacific, Europe, North America | Drives ink demand. |

Chemical and Pigment Suppliers | +0.7% | Global | Strengthens raw material supply. |

Private Equity Firms | +0.5% | Asia Pacific, Europe, North America | Supports capacity scaling. |

Sustainable Materials Investors | +0.5% | Europe, North America, Japan | Supports low-VOC innovation. |

Segment Covered in the Report

By Type

Solvent-Based

UV

UV-LED

Others

By Process

Lithographic Printing

Flexographic Printing

Gravure Printing

Digital Printing

Others

By Application

Commercial and Publication

Textiles

Others

By Region

Asia Pacific

North America

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand from packaging printing | +1.1% | Asia Pacific, North America, Europe | Drives ink consumption. |

Growth in flexible packaging | +0.9% | Asia Pacific, Europe, North America | Supports high-volume use. |

Expansion of food and beverage packaging | +0.8% | Global | Increases label and carton printing. |

Growth in e-commerce packaging | +0.6% | China, India, U.S., Europe | Boosts printed packaging demand. |

Rising demand for brand and product labeling | +0.5% | Global | Supports specialty inks. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Volatile raw material prices | -0.7% | Global | Pressures production margins. |

Environmental regulations on solvent-based inks | -0.6% | Europe, North America, Asia Pacific | Raises compliance cost. |

Decline in publication printing | -0.5% | North America, Europe | Reduces traditional ink use. |

High cost of eco-friendly inks | -0.4% | Emerging markets | Slows sustainable adoption. |

Supply chain pressure for pigments and resins | -0.4% | Global | Affects ink availability. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in water-based inks | +0.9% | Europe, North America, Asia Pacific | Supports cleaner printing. |

Expansion of UV-curable inks | +0.8% | Developed and industrial markets | Improves print durability. |

Rising demand for sustainable packaging inks | +0.7% | Europe, U.S., Japan, India | Builds long-term demand. |

Digital printing ink adoption | +0.6% | North America, Europe, Asia Pacific | Supports short-run printing. |

Growth in labels and flexible films | +0.5% | Global | Expands application scope. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Balancing cost and sustainability | -0.6% | Global | Affects formulation choices. |

Maintaining color consistency | -0.5% | Packaging and commercial printing | Requires quality control. |

Migration safety in food packaging | -0.4% | U.S., Europe, Asia Pacific | Raises testing needs. |

Competition from low-cost suppliers | -0.4% | Asia Pacific, Latin America | Pressures pricing. |

Technology shift from conventional printing | -0.3% | Developed markets | Changes demand mix. |

Recent Developments

In February 2026, Sun Chemical announced an investment of about USD 10.0 million at its Newport, Delaware facility to expand quinacridone pigment production. Quinacridone pigments are used in high-performance color applications, including printing inks, coatings, plastics, and specialty materials. The investment is focused on improving production reliability, plant safety, supply continuity, and manufacturing performance. Sun Chemical also stated that the wider DIC Group has more than USD 7.0 billion in combined annual sales and over 21,000 employees, which supports its global production and customer service network.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 20.5 Billion |

Forecast Revenue (2035) | USD 30.6 Billion |

CAGR (2025-2035) | 4.1% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Type (Solvent-Based, Water-Based, Oil-Based, UV, UV-LED, Others), By Process (Lithographic Printing, Flexographic Printing, Gravure Printing, Digital Printing, Others), By Application (Packaging, Commercial and Publication, Textiles, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | DIC Corporation, Flint Group, hubergroup, Sakata INX Corporation, Siegwerk Druckfarben AG & Co. KGaA, ALTANA, Dainichiseika Color & Chemicals Mfg. Co., Ltd., DuPont, Epple Druckfarben AG, INX International Ink Co. |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Environment Analysis

The Printing Ink Market is competitive, technically mature, and closely linked with packaging, publishing, commercial printing, labels, textiles, and industrial printing. The competitive environment is led by companies that offer broad ink portfolios across flexographic, gravure, offset, digital, screen, UV, LED-UV, water-based, and solvent-based technologies. Demand is increasingly influenced by packaging growth, food-safe ink requirements, sustainability targets, low-VOC formulations, and the shift toward recyclable and mono-material packaging.

Competition is strongest in packaging inks because food, beverage, personal care, pharmaceutical, and e-commerce packaging require high print quality, regulatory compliance, strong adhesion, and reliable supply. Large suppliers compete through global production networks, color management systems, technical service teams, and customer support for converters and brand owners. Regional suppliers compete through price flexibility, faster delivery, and customized formulations for local substrates and printing conditions.

Implementation Complexity & Technology Readiness

Ink Technology | Implementation Complexity | Technology Readiness | Market Position |

|---|---|---|---|

Solvent-based inks | Moderate | High | Widely used, but affected by VOC controls. |

Water-based inks | Moderate | High | Strong fit for lower-emission printing applications. |

UV-curable inks | Moderate to High | High | Used where fast curing and durable print are required. |

LED-UV inks | High | Moderate to High | Rising adoption, but press compatibility is important. |

Offset inks | Low to Moderate | High | Mature and widely used across printing applications. |

Technology Readiness Assessment

Printing ink technology is highly mature across offset, gravure, flexographic, and solvent-based platforms. These technologies have long operating histories, well-established supplier networks, and deep process knowledge among printers and converters. Their continued relevance is supported by large installed press bases and broad use in packaging and commercial printing. Water-based ink technology is also mature and continues to improve through better resin systems, pigment dispersion, drying performance, and substrate adhesion.

The technology is well positioned in paper packaging, corrugated packaging, and selected flexible packaging formats. Its readiness is supported by lower emission concerns and stronger alignment with sustainability goals. UV and LED-UV ink systems are technologically ready, but their adoption is more dependent on press investment and curing infrastructure. LED-UV is gaining attention because it can support faster curing and energy-efficient operations when used with suitable equipment. These technologies are expected to remain important in labels, high-quality packaging, and premium commercial print.

Bio-based and low-migration ink systems are moving from niche use toward wider adoption. Their readiness is improving as food packaging safety, recyclable packaging, and lower-carbon materials become higher priorities for brands. However, formulation cost, raw material availability, certification, and performance validation remain important adoption barriers.

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

DIC Corporation

Flint Group

hubergroup

Sakata INX Corporation

Siegwerk Druckfarben AG & Co. KGaA

ALTANA

ALTANA

DuPont

Epple Druckfarben AG

INX International Ink Co.

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Oxygen Market to Exceed USD 171.1 Billion by 2035

Global Oxygen Market Size, Share Analysis By Form (Gas, Liquid, Solid), By Type (Industrial, Medical), By Application (Metals and Mining, Chemical Industry, Oil and Gas, Healthcare, Pharmaceutical, Other Applications), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Tannin Market to Hit USD 9.8 Billion by 2035

Global Tannin Market Size, Share and Go-to-Market Strategy Analysis By Source (Plant, Brown Algae), By Product Type (Hydrolysable Tannins, Condensed Tannins, Phlorotannins, Others), By Application (Food and Beverage, Pharmaceutical and Nutraceutical, Leather Industry, Wood Industry, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Methanol Market to Exceed USD 64.1 Billion by 2035

Global Methanol Market Size By Feedstock (Natural Gas, Coal, Biomass and Renewables), By Derivative (Formaldehyde, Acetic Acid, MTBE, DME, Gasoline Blending, Biodiesel, MTO/MTP, Solvent, Others), By Sub-derivatives (Gasoline additives, Olefins, UF/PF resins, VAM, Polyacetals, MDI, PTA, Acetate Esters, Acetic anhydride, Fuels, Others), By Application (Construction, Automotive, Electronics, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Xylose Market to hit USD 7.0 Billion by 2035

Global Xylose Market Size By Type (D-Xylose, L-Xylose, DL-Xylose), By Form (Powder, Liquid, Granules), By Source (Wood, Corncobs, Sugarcane Bagasse, Others), By Application (Food and Beverage, Cosmetics and Personal Care, Animal Feed, Pharmaceuticals, Biofuel Industry, Others) , By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035