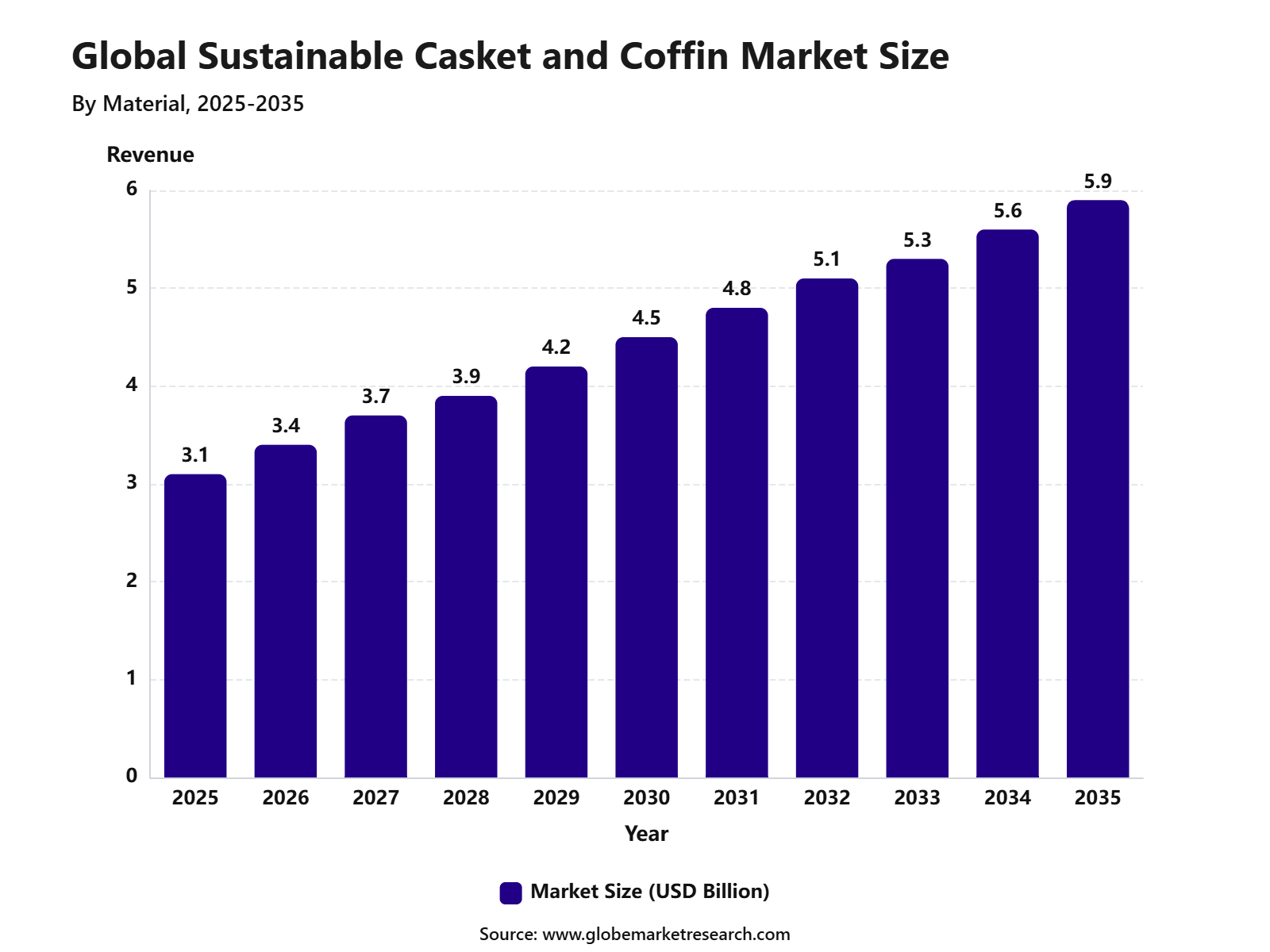

Revenue, 2025

$3.1 billion

Forecast, 2035

$5.9 billion

CAGR, 2025-2035

6.4%

Report Coverage

Global

Market Size and Forecast

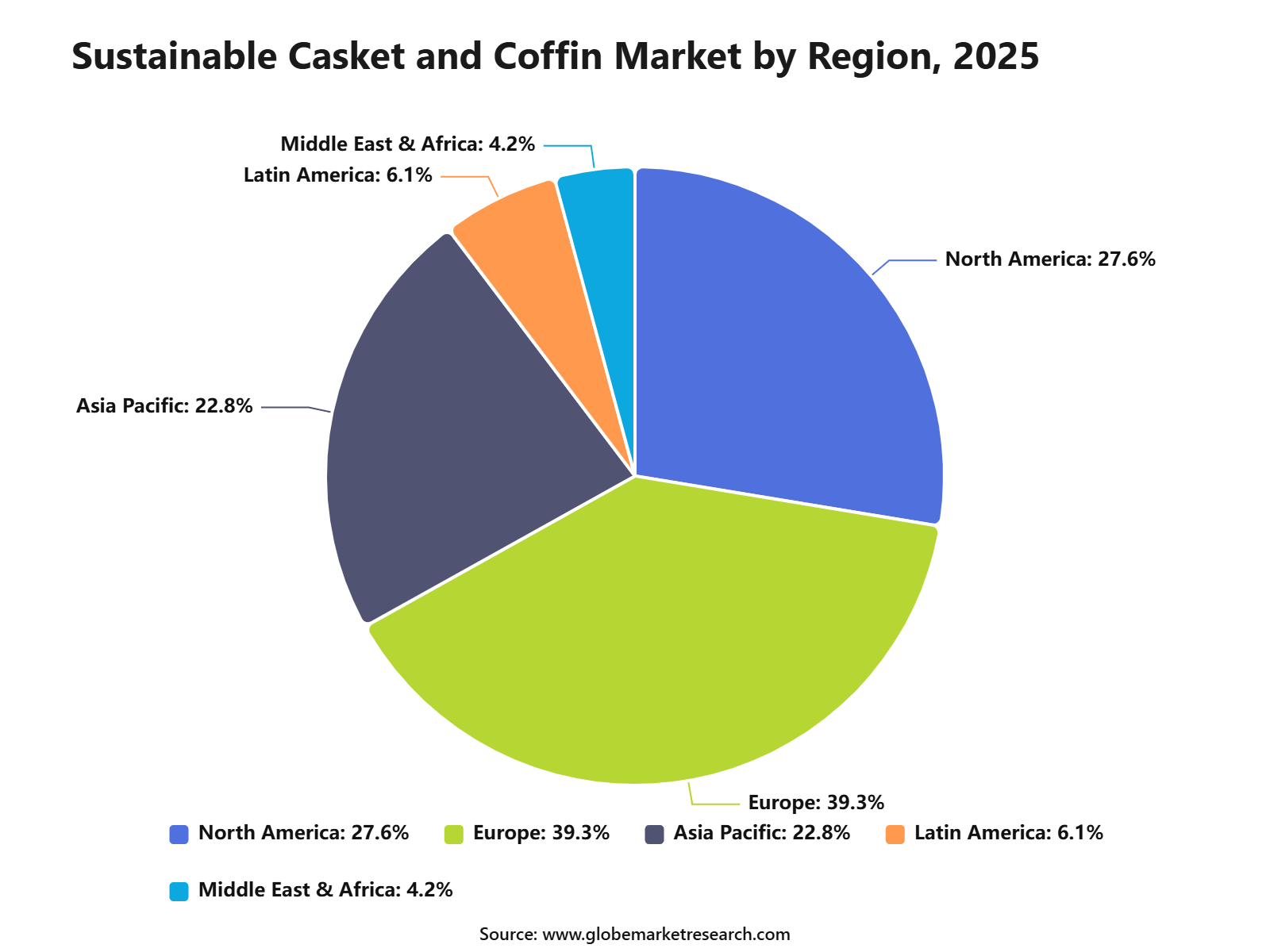

The Global Sustainable Casket and Coffin Market is estimated at USD 3.1 billion in 2025 and is forecast to generate USD 5.9 billion by 2035, growing at a CAGR of 6.4%. Europe held the largest regional share of 39.3% in 2025, supported by rising demand for eco-friendly funeral products, stronger environmental awareness, green burial practices, and wider acceptance of biodegradable materials across funeral services.

The Sustainable Casket and Coffin Market refers to burial products made from environmentally responsible, biodegradable, recyclable, or low-impact materials. These include bamboo, willow, cardboard, recycled wood, sustainably sourced timber, banana leaf, seagrass, and other natural materials. The market is closely linked with green cemeteries, natural burial services, carbon-conscious funeral planning, and changing consumer preferences toward simple and sustainable end-of-life choices.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market outlook remains positive as families and funeral service providers increasingly consider environmental impact, affordability, and ethical sourcing in burial decisions. Growth can be attributed to the expansion of green burial grounds, rising interest in personalized funeral products, and increasing availability of sustainable caskets through funeral homes and online channels. Wider use of certified wood, plastic-free designs, and biodegradable finishes is expected to support steady adoption across developed and emerging markets.

Leading Segment Share Summary

Soft wooden caskets and coffins led the material segment with 48.8% share. Their strong position was supported by biodegradability, natural appearance, lower environmental impact, and growing preference for eco-friendly burial products.

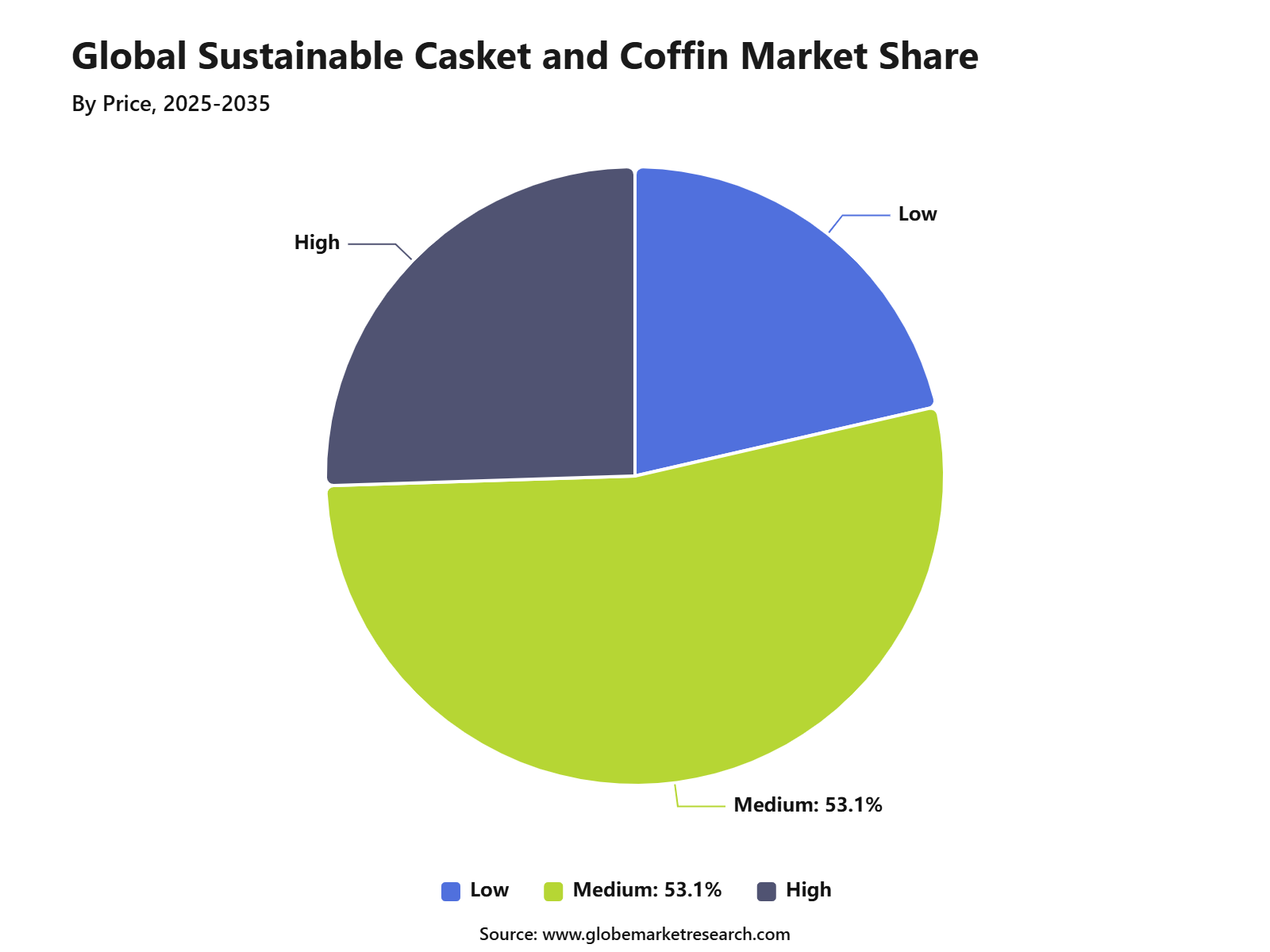

Medium-priced caskets and coffins accounted for 53.1% share. This segment gained traction as consumers preferred affordable, durable, and sustainable options without choosing premium-priced alternatives.

Offline channels held the largest distribution share at 87.9%. Funeral homes, local distributors, and direct consultation services remained important due to the sensitive and personal nature of purchasing decisions.

Europe led the sustainable casket and coffin market with 39.3% share. Growth was supported by strong environmental awareness, green burial practices, and rising demand for sustainable funeral products.

Go-to-Market and Sales Strategy

The go-to-market strategy for the sustainable casket and coffin market should be built around funeral homes, green cemeteries, natural burial grounds, online funeral product platforms, hospice networks, and end-of-life planning advisors. Demand is being supported by families that want simple, lower-impact, and values-based funeral choices. NFDA reported that 61.4% of consumers were interested in exploring green funeral options in 2025, up from 55.7% in 2021, which shows rising consumer acceptance of eco-conscious funeral products.

Sales economics are shaped by material selection, handmade production, certification, logistics, storage, and funeral home partnerships. Sustainable caskets made from bamboo, willow, wicker, seagrass, cardboard, unfinished pine, softwood, or mycelium can be positioned as practical alternatives to metal, hardwood, and chemically finished products. Green Burial Council states that green burial containers should be biodegradable and may include caskets, shrouds, urns, or pouches made from 100% biodegradable materials.

Revenue Potential Analysis

Revenue potential is strongest in natural burial, direct burial, green funeral packages, cremation alternative containers, and online pre-planning sales. The product is no longer limited to traditional burial because cremation families also need simple alternative containers for direct cremation. NFDA projected the U.S. cremation rate at 63.4% in 2025, compared with a burial rate of 31.6%, which makes cremation-compatible sustainable containers an important sales route.

Higher revenue can be created through certified biodegradable caskets, locally sourced wooden coffins, flat-pack designs, personalized natural finishes, and bundled services with green cemeteries. The product value increases when sustainability claims are backed by clear material details, non-toxic adhesives, no metal parts, low-emission production, and local sourcing. GBC notes that certified products should use plant-derived, natural, animal, or unfired earthen materials, and that finishes, adhesives, and dyes should not release toxic byproducts into the ground.

Revenue Landscape Across

The revenue landscape is spread across funeral homes, cemetery operators, direct-to-consumer sales, green burial specialists, hospice care referrals, religious communities, and estate planning services. Funeral homes remain important because families often make purchase decisions at the time of need, while online channels are useful for pre-planning and lower-cost product comparison.

The FTC Funeral Rule also supports third-party selling because funeral providers cannot refuse a casket or urn bought online, from a local store, or from another supplier. Revenue is also supported by the wider shift toward simpler funeral formats. NFDA reported that the national median cost of a funeral with viewing and burial was USD 8,300 in 2023, while the median cost of a funeral with cremation was USD 6,280.

Financial Impact

The financial impact of sustainable caskets and coffins is positive when suppliers can control material cost, reduce shipping weight, and build repeat relationships with funeral homes. Cardboard, wicker, bamboo, pine, and other lightweight materials can reduce handling and freight pressure compared with heavy hardwood or metal products. Flat-pack and locally manufactured designs can also improve storage efficiency for funeral homes with limited showroom or warehouse space.

At the buyer level, sustainable caskets can reduce total funeral spending when they are used with direct burial, natural burial, or cremation services. The FTC states that no state or local law requires the use of a casket for cremation, and funeral homes offering cremation must inform consumers that alternative containers are available. This creates a clear financial opening for lower-cost, biodegradable, and cremation-ready containers.

By Material

Soft wooden held the leading material share of 48.8%, supported by its wide use in sustainable caskets and coffins. The material is preferred because it is lighter, easier to shape, and more suitable for natural finishes compared to many heavy hardwood alternatives.

The growth of soft wooden products can also be linked to rising interest in biodegradable and responsibly sourced funeral products. As European circular economy policies encourage lower material waste and better resource use, soft wooden options are gaining stronger acceptance among families, funeral homes, and eco-conscious buyers.

By Price

The medium price segment accounted for the highest share of 53.1%, as buyers often seek a balance between affordability, dignity, and product quality. In funeral-related purchases, families usually prefer products that look reliable and respectful without moving into highly premium price ranges.

This segment benefits from practical buying behavior, especially during planned or urgent funeral arrangements. Medium-priced products are widely accepted because they offer better design, finish, and material value than entry-level options while remaining easier to purchase than expensive customized products.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Distribution Channel

Offline channels dominated the market with an 87.9% share, mainly because casket and coffin purchases are highly sensitive and trust-driven. Customers often prefer direct consultation, physical inspection, immediate guidance, and personal support from funeral service providers before making a final decision.

Even though online buying is rising across Europe, offline channels remain important for products that require emotional assurance, correct sizing, material verification, and timely delivery. Physical stores and funeral homes continue to hold a strong role because families value clear communication and dependable service during difficult situations.

By Region

Europe led the regional market with a 39.3% share, supported by stronger awareness of sustainable materials, established funeral service networks, and rising demand for natural end-of-life products. The region has shown steady movement toward circular practices, responsible sourcing, and environmentally lower-impact choices.

The regional advantage is also supported by consumer familiarity with certified wood products and growing interest in green burial options. With sustainability becoming a stronger part of purchase decisions, Europe remains a key market for soft wooden, biodegradable, and ethically sourced casket and coffin products.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRisk Factors and Market Barriers

The main risks include limited consumer awareness, uneven availability of green cemeteries, certification gaps, product damage during shipping, and uncertain buyer trust in sustainability claims. Many families still make funeral decisions under emotional pressure, which can reduce comparison shopping and limit awareness of sustainable options. Product education must therefore be simple, respectful, and clear at the point of sale.

Market barriers are also created by cemetery rules, funeral home preferences, and inconsistent definitions of “green” or “natural.” Green Burial Council notes that certified hybrid cemeteries do not require vaults and must allow eco-friendly biodegradable containers such as shrouds and softwood caskets, but not every cemetery operates under these standards. This means product suppliers must verify cemetery acceptance before promoting specific casket or coffin formats.

Regulatory and Compliance Risks

Regulatory risk is linked to funeral pricing disclosure, third-party casket acceptance, cremation container rules, burial ground requirements, and environmental marketing claims. Under the FTC Funeral Rule, funeral providers must give consumers casket price information before showing caskets and must allow families to provide a casket or urn bought elsewhere without charging an extra handling fee.

Green claim compliance is also important because terms such as sustainable, biodegradable, natural, non-toxic, and eco-friendly must be supported by evidence. The FTC Green Guides are designed to help marketers avoid environmental claims that mislead consumers, including guidance on how claims are interpreted, substantiated, and qualified. Sustainable casket companies should therefore avoid broad claims unless material composition, biodegradability, coatings, adhesives, sourcing, and disposal conditions are clearly documented.

Market Adoption Barriers

Adoption barriers are mainly related to tradition, low awareness, emotional buying behavior, and limited product visibility in funeral homes. Many families still depend on funeral directors for guidance, so the product must be easy for funeral professionals to explain. Adoption can improve when suppliers provide product samples, certification documents, clear price sheets, cemetery compatibility information, and simple family-facing education material.

Another adoption barrier is the lack of standardization across natural burial sites and funeral service providers. Some buyers may question whether a product is truly biodegradable, locally sourced, or free from harmful finishes. To overcome this, companies should use third-party certification where possible, disclose material origins, provide decomposition-related information, and train channel partners on compliant sustainability messaging.

Segment Covered in the Report

By Material

Soft Wooden

Cardboard

Wicker

Others

By Price

Low

Medium

High

By Distribution Channel

Online

Offline

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for eco-friendly funeral products | +1.6% | North America, Europe, Australia | Drives green adoption. |

Growing awareness of sustainable burial practices | +1.3% | Developed markets | Supports consumer shift. |

Increasing preference for biodegradable materials | +1.1% | Europe, North America, Asia Pacific | Reduces environmental impact. |

Expansion of green funeral homes | +0.9% | U.S., UK, Germany, Australia | Improves product access. |

Rising demand for personalized funeral products | +0.8% | Global | Supports premium sales. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Limited awareness in emerging markets | -0.8% | Asia Pacific, Latin America, Africa | Slows adoption. |

Higher cost than conventional options | -0.7% | Price-sensitive markets | Limits mass demand. |

Cultural preference for traditional coffins | -0.6% | Asia Pacific, Middle East, Africa | Restricts switching. |

Limited supplier availability | -0.5% | Rural and smaller markets | Affects accessibility. |

Certification and material compliance issues | -0.4% | Europe, North America | Raises production burden. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in natural burial services | +1.5% | North America, Europe, Australia | Supports green funerals. |

Expansion of bamboo and wicker coffins | +1.2% | Asia Pacific, Europe, North America | Builds material diversity. |

Demand for low-carbon funeral products | +1.0% | Developed markets | Strengthens eco positioning. |

Online funeral product sales | +0.8% | North America, Europe, urban Asia | Improves customer reach. |

Partnerships with funeral service providers | +0.7% | Global | Expands distribution. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining material durability | -0.7% | Global manufacturers | Affects product trust. |

Balancing sustainability and affordability | -0.6% | Global | Limits broad adoption. |

Supply consistency for natural materials | -0.5% | Asia Pacific, Europe, North America | Impacts production stability. |

Funeral industry resistance to change | -0.5% | Traditional service markets | Slows market entry. |

Educating consumers during sensitive purchases | -0.4% | Global | Requires careful marketing. |

Recent Developments

May 2026: Earth Funeral opened a large human composting facility in Elkridge, Maryland, supporting eco-friendly deathcare services that reduce reliance on conventional burial materials, including metal caskets, concrete vaults, and chemical-heavy practices. The facility is nearly 37,000 square feet and is described by the company as the first East Coast soil transformation facility.

March 2026: Scottish Government brought hydrolysis regulations into force from March 2026, allowing businesses to begin the approval process to offer water cremation as a sustainable alternative to burial and flame cremation. This is relevant to coffin demand because hydrolysis can reduce the use of single-use coffin materials in some service models.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 3.1 billion |

Forecast Revenue (2035) | USD 5.9 billion |

CAGR (2025-2035) | 6.4% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Material (Soft Wooden, Cardboard, Wicker, Others), By Price (Low, Medium, High), By Distribution Channel (Online, Offline) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific -China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Starmark, Chistann, Carnation Caskets, Loop Living Cocoon, Cardboard Coffin Company, Titan Casket, The Old Pine Box, Natural Woven Products Ltd., Caring Coffins, Green Coffins Ireland Ltd., Batesville, Matthews International Corporation, and Thacker Caskets, Inc. and Other Key Players |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Starmark

Chistann

Carnation Caskets

Loop Living Cocoon

Cardboard Coffin Company

Titan Casket

The Old Pine Box

Natural Woven Products Ltd.

Caring Coffins

Green Coffins Ireland Ltd.

Batesville

Matthews International Corporation

Thacker Caskets, Inc.

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Consumer Goods

Sports Sponsorship Market to hit USD 215.8 billion by 2035

Global Sports Sponsorship Market Size, Go-to-Market Strategy Analysis By Sponsorship Type (Team/Club, Athlete, Events, Venue, Others), By Sports Category (Football, Cricket, E-sports, Others), By Event Type (International, League, Domestic), By Application (Competition Sponsorship, Training Sponsorship, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Subscription Box Market to hit USD 225.2 billion by 2035

Global Subscription Box Market Size, Go-to-Market Strategy Analysis By Type (Replenishment Subscription, Curation Subscription, Access Subscription), By Price Range (Budget-friendly, Mid-range, Premium/Luxury), By Application (Beauty and Personal Care, Food and Beverages, Fashion and Apparel, Pet Products, Health and Fitness, Kids and Baby Products, Books and Entertainment, Home Goods, Tech and Gadgets, Arts and Crafts, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Pet Toys Market to hit USD 35.6 billion by 2035

Global Pet Toys Market Size, Share Analysis By Product Type (Plush, Rope, Balls, Others), By Pet Type (Dogs, Cats, Others), By Distribution Channel (Offline, Online), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Black Hair Care Market to hit 17.1 Bn by 2035

Global Black Hair Care Market By Product Type (Shampoo, Conditioner, Hair Dye, Hair Oils, Hair Serums, Others.), By Application (Household, Commercial Use, Salons, Beauty Parlors, Professional Hair Care Services), By Distribution Channel (Offline Stores, Online Platforms, Supermarkets and Hypermarkets, Specialty Beauty Stores, Retail Stores, Pharmacies, Direct-to-Consumer Channels), By End User (Women, Men, Kids, Professional Stylists, Salons), By Hair Concern (Dryness and Moisture Retention, Scalp Health, Breakage Repair, Curl Definition, Frizz Control, Protective Styling, Hair Growth Support, Chemical-Free Hair Care), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035