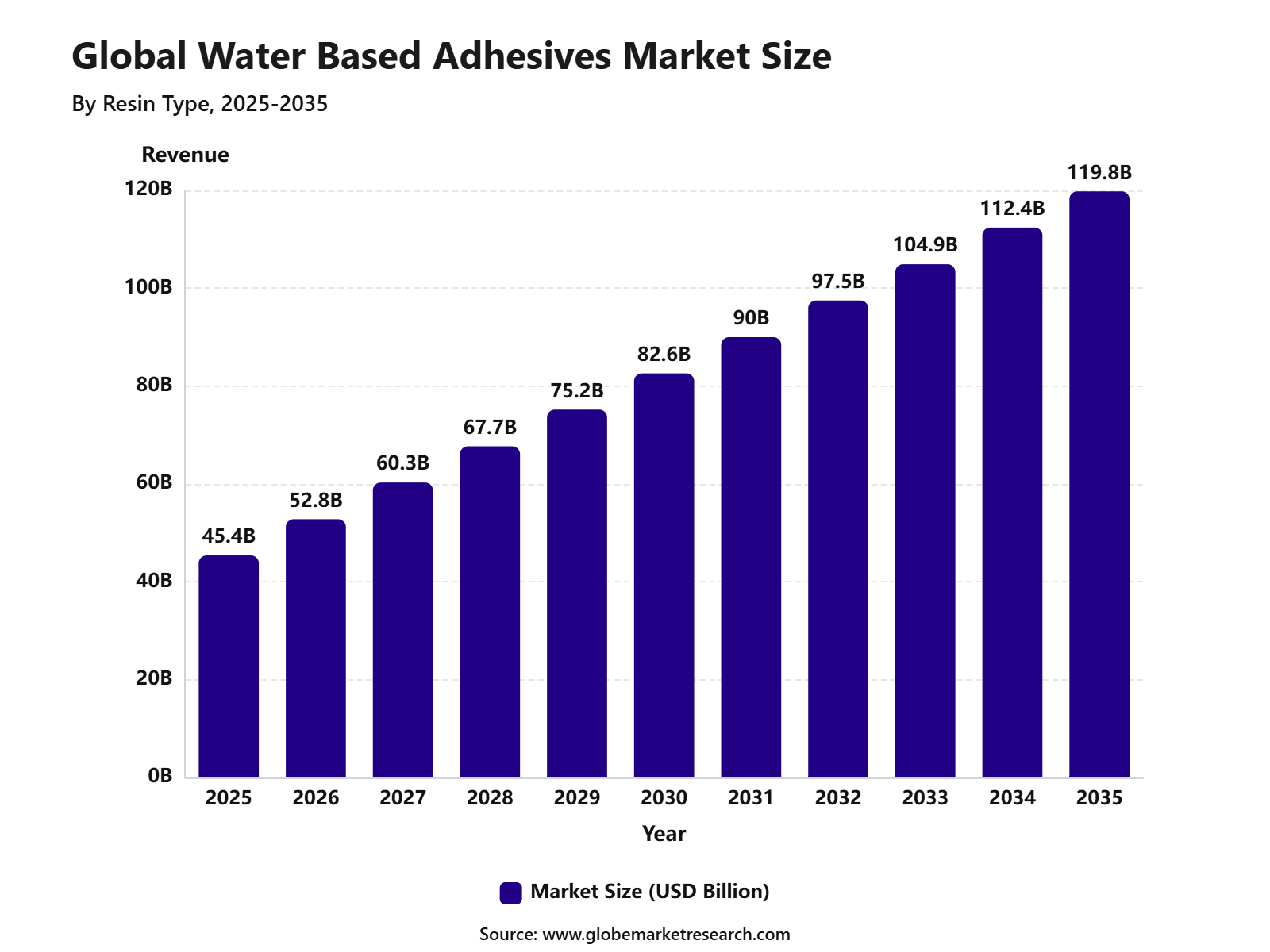

Revenue, 2025

$ 45.4 Bn

Forecast, 2035

$ 119.8 Bn

CAGR, 2025-2035

10.2%

Report Coverage

Global

Market Size and Forecast

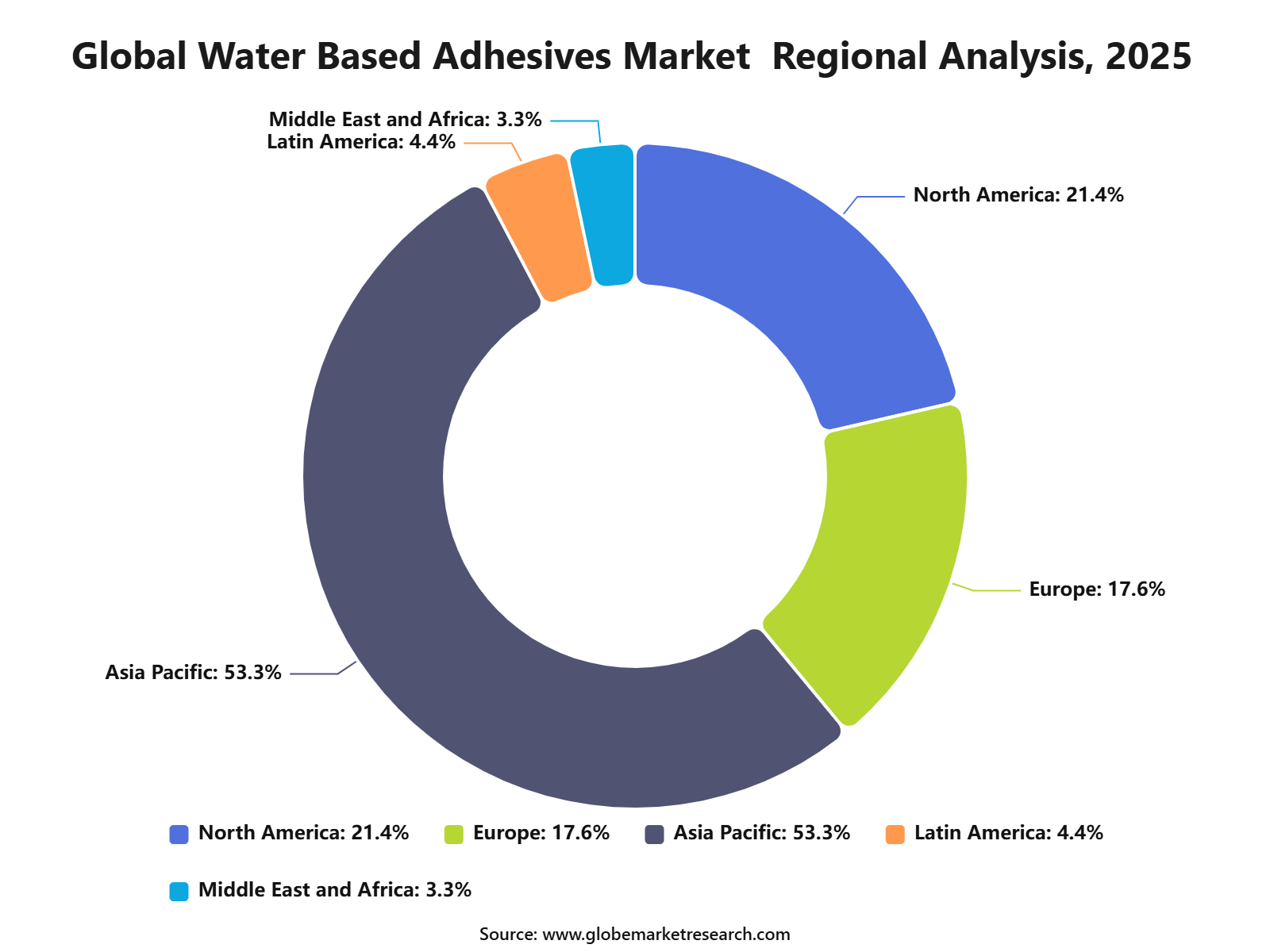

The Global Water Based Adhesives Market was worth USD 45.4 billion in 2025 and is expected to reach USD 119.8 billion by 2035, growing at a CAGR of 10.2% from 2025 to 2035. Asia Pacific held the largest regional share of 53.3% in 2025, supported by strong packaging production, expanding construction activity, rising furniture manufacturing, and growing demand for low-VOC adhesive solutions across China, India, Japan, South Korea, and Southeast Asia.

The Water Based Adhesives Market includes adhesive formulations that use water as the main carrier instead of solvent-based systems. These adhesives are widely used in packaging, labels, tapes, paper bonding, woodworking, construction materials, textiles, footwear, automotive interiors, and consumer goods. The market is closely linked with sustainable packaging, regulatory compliance, industrial bonding, flexible materials, and safer workplace chemical practices.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market outlook remains strong as industries continue to shift toward eco-friendly, low-emission, and easy-to-apply adhesive products. Growth can be attributed to rising demand for flexible packaging, increasing use in furniture and building materials, and stricter restrictions on solvent-based chemicals. The expansion of e-commerce packaging, green construction, and advanced polymer-based adhesive formulations is expected to support long-term market growth.

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 45.4 Billion |

Forecast Revenue (2035) | USD 119.8 Billion |

CAGR (2025-2035) | 10.2% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Key Market Insights

Acrylic polymer emulsion led the resin type segment with 39.54% share, supported by strong bonding performance, flexibility, water resistance, and wide use across packaging, labels, construction, and consumer applications.

Tapes and labels accounted for 18.4% share by application, driven by rising demand for pressure-sensitive adhesives in packaging, logistics, retail labeling, and industrial product identification.

Building and construction held 47.9% share by end-use industry, supported by strong use of water based adhesives in flooring, insulation, panels, wall coverings, and interior finishing materials.

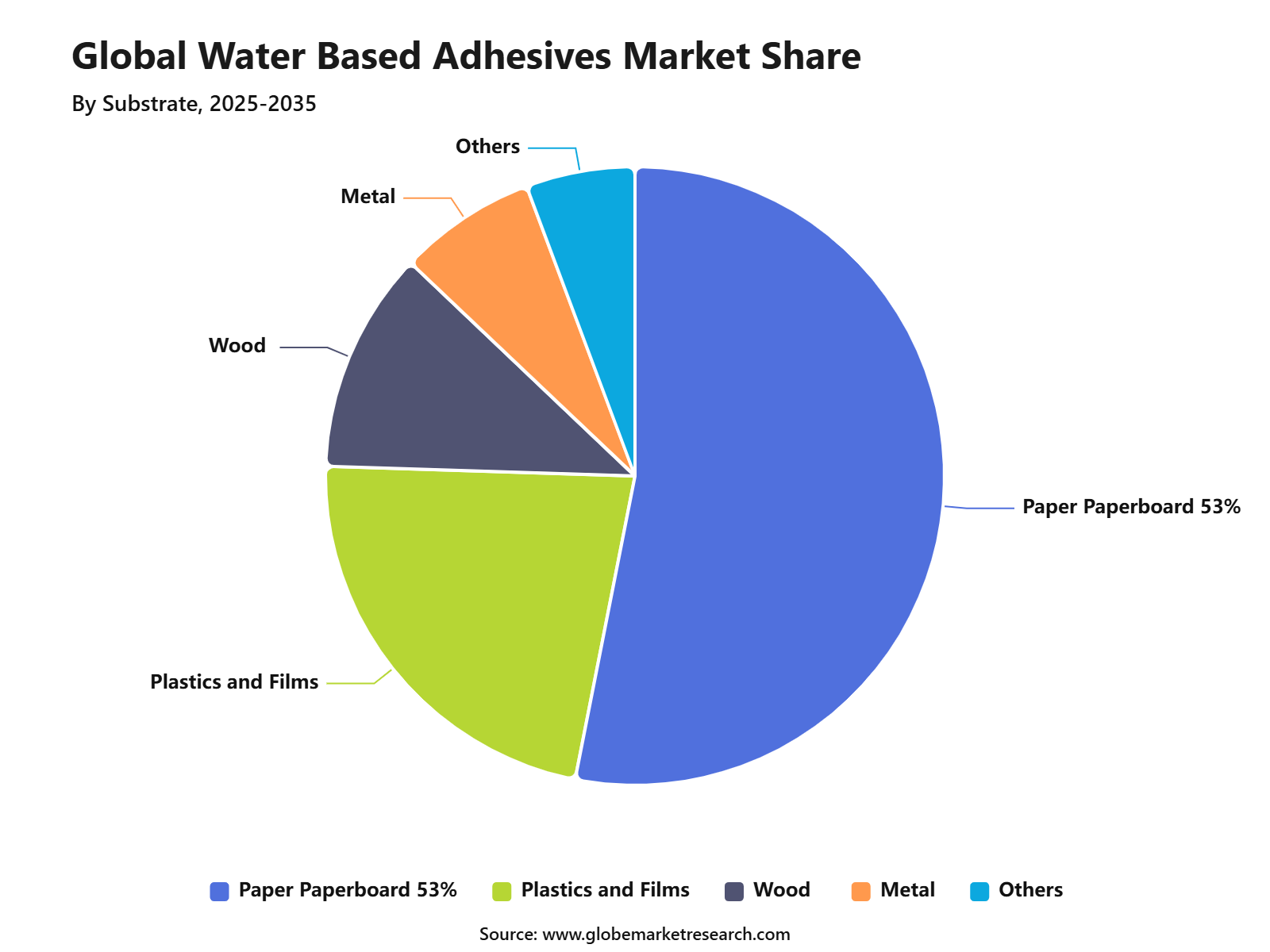

Paper and paperboard captured 53.1% share by substrate, driven by high adoption in packaging, cartons, labels, paper bags, and sustainable bonding applications.

Asia Pacific led the water based adhesives market with 53.3% share, supported by strong packaging demand, expanding construction activity, rising manufacturing output, and large adhesive consumption across China, India, Japan, and Southeast Asia.

Top Funding Highlights

Avery Dennison completed the acquisition of Meridian Adhesives Group’s U.S. flooring adhesives business for USD 390 million in October 2025. The business had projected 2025 revenue of about USD 110 million and operates four manufacturing facilities in the United States. This deal supports demand for specialty flooring adhesives and strengthens Avery Dennison’s position in high-value bonding and coating materials.

Sika announced the acquisition of Turkey-based Akkim Sealants & Adhesives in February 2026. Akkim had net sales of around CHF 220 million and provides adhesives and sealants with strong distribution access across Turkey and export markets. The acquisition will expand Sika’s production footprint and support long-term growth in distribution-focused adhesives and sealants.

Pidilite continued to invest in adhesive, sealant, construction chemical, and waterproofing categories in India. Its investor presentation noted more than INR 200 crore invested for capacity building, while CRISIL reported expected annual capex of around INR 650 crore to INR 760 crore over the medium term. This supports India’s growing demand for Fevicol-type white adhesives, industrial adhesives, sealants, waterproofing, and construction bonding products.

Investment View

The water-based adhesives market is attracting investment because buyers are shifting toward low-VOC, safer, and more sustainable bonding systems. Strong demand is visible in packaging, paper and paperboard, flooring, construction, labels, tapes, hygiene, furniture, and consumer goods. Investments in polymer dispersions are especially important because they improve supply security for acrylic, vinyl acetate, and polyurethane-based waterborne adhesive formulations.

Future investment is expected to remain strong in water-based pressure-sensitive adhesives, recyclable packaging adhesives, flooring adhesives, acrylic dispersions, VAE emulsions, and low-emission construction bonding systems. Companies with regional production, strong formulation capability, stable raw material access, and compliance-ready adhesive portfolios are likely to gain better customer preference.

By Resin Type

Acrylic polymer emulsion held 39.54% share in the Water Based Adhesives market, making it the leading resin type segment. Its dominance can be attributed to strong bonding performance, good aging resistance, flexibility, and suitability across packaging, labels, construction materials, and consumer goods applications.

The segment is supported by rising demand for low-VOC and waterborne adhesive solutions. Acrylic polymer emulsions are preferred because they provide stable adhesion, faster drying, and compatibility with different surfaces such as paper, board, plastics, films, and textiles.

Acrylic polymer emulsion is expected to remain a key resin type as manufacturers shift toward safer and more environmentally responsible adhesive systems. Its use is likely to expand further in tapes, labels, packaging, construction, and pressure-sensitive adhesive products.

By Application

Tapes and labels accounted for 18.4% share in the Water Based Adhesives market, making it the leading application segment. The segment is supported by high adhesive demand from packaging, logistics, retail labeling, food packaging, e-commerce shipping, and industrial identification products.

Water based adhesives are widely used in tapes and labels because they offer clean bonding, easy coating, good tack, and lower solvent emissions. These properties make them suitable for pressure-sensitive labels, carton sealing tapes, masking tapes, and specialty labeling materials.

The segment is expected to grow steadily as packaging volumes increase across food, beverages, healthcare, personal care, and online retail. Demand is also supported by the shift toward recyclable packaging formats, where water based adhesive systems are preferred for paper and paperboard applications.

By End-Use Industry

Building and construction held 47.9% share in the Water Based Adhesives market, making it the leading end-use industry. This position is supported by strong use of these adhesives in flooring, wall coverings, insulation, panels, tiles, laminates, and interior finishing materials.

The segment benefits from rising construction activity, renovation projects, and demand for safer indoor materials. Water based adhesives are preferred in buildings because they reduce solvent exposure, support better indoor air quality, and meet stricter environmental and safety requirements.

Building and construction demand is expected to remain strong as developers and contractors adopt more sustainable materials. Growth is also supported by green building practices, urban infrastructure expansion, and the use of adhesive-based systems for lightweight and modular construction products.

By Substrate

Paper and paperboard accounted for 53.1% share in the Water Based Adhesives market, making it the leading substrate segment. Its dominance is linked to the wide use of water based adhesives in cartons, labels, corrugated boxes, paper bags, envelopes, and flexible paper packaging.

The segment is supported by strong compatibility between water based adhesive formulations and cellulose-based materials. These adhesives provide reliable bonding, quick drying, and efficient application on paper surfaces, which makes them suitable for high-speed packaging and converting operations.

Paper and paperboard are expected to remain the main substrate due to rising demand for recyclable and fiber-based packaging. As brands reduce plastic use and shift toward paper packaging, water based adhesives will continue to play an important role in bonding, sealing, and labeling applications.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Region

Asia Pacific held 53.3% share in the Water Based Adhesives market, making it the leading regional market. The region’s dominance is supported by large packaging production, strong construction activity, expanding manufacturing output, and rising demand from automotive, consumer goods, and healthcare sectors.

China, India, Japan, South Korea, and Southeast Asian countries are major contributors to regional demand. These countries have strong industrial bases, growing e-commerce activity, high paper packaging consumption, and rising investment in infrastructure and housing projects.

Asia Pacific is expected to maintain its strong position as manufacturers continue to adopt cost-efficient and low-emission adhesive technologies. Growth is also supported by expanding packaging supply chains, increasing domestic consumption, and stricter environmental focus across adhesives and coating applications.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Asia Pacific leads the Water Based Adhesives Market with 53.3% share in 2025, supported by packaging production, construction growth, furniture manufacturing, and industrial processing. China and India remain key contributors because of large-scale manufacturing and rising demand for low-emission adhesives.

North America and Europe remain important value markets due to strict VOC standards, sustainable packaging trends, and advanced construction materials. These regions are expected to support higher-value products with better performance, safety, and environmental positioning.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +3.6% | Asia Pacific, 53.3% share in 2025 | Leads volume demand. |

China packaging and manufacturing scale | +2.3% | China | Drives regional consumption. |

India construction and consumer goods growth | +1.8% | India | Supports future demand. |

North America low-VOC adhesive adoption | +1.3% | U.S. and Canada | Builds value demand. |

Europe sustainable packaging transition | +1.1% | Germany, France, UK, Italy | Supports premium products. |

Go-to-Market and Sales Economics

The go-to-market approach for the Water Based Adhesives Market should focus on low-VOC performance, packaging compatibility, fast application, bond strength and regulatory fit. These adhesives are widely used in tapes and labels, paper and packaging, woodworking, flooring, construction, hygiene products and consumer goods because water is used as the carrier instead of high-solvent systems. Current air-quality regulation is also supporting demand, as California’s consumer products program targets VOC emission reductions of 20 tons per day statewide and 8 tons per day in the South Coast by 2037.

Sales economics should be built around formulation support and high-volume customer retention. Packaging converters, label producers, carton makers, furniture manufacturers and construction product companies need adhesives that run smoothly on automated lines and meet drying-speed, tack, heat-resistance and food-contact requirements. H.B. Fuller reported USD 950 million in Q2 2026 net revenue, up 5.8% year over year, showing that large adhesive suppliers are benefiting from pricing execution, acquisitions and stronger customer demand in selected channels.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is spread across paper packaging, corrugated boxes, labels, tapes, bookbinding, woodworking, furniture, flooring, textiles, hygiene products and construction materials. Packaging is one of the most important revenue channels. AF&PA reported that U.S. packaging papers and specialty packaging shipments increased 12% in May 2026 compared with May 2025, while shipments were up 6% for the first five months of 2026.

Containerboard and paperboard applications also support steady adhesive demand. In 2025, U.S. containerboard production reached 36.1 million tons, and containerboard mills maintained a 91.9% operating rate despite lower capacity. This reflects the continued importance of fiber-based packaging, where water based adhesives are used for box closing, laminating, labeling and converting applications.

Construction and building materials create another revenue pool through flooring adhesives, wall coverings, panels, insulation, laminates and sealant-compatible systems. U.S. private residential construction spending reached USD 909.9 billion in April 2026, while public construction spending stood at USD 532.7 billion. These activity levels support demand for low-odor, indoor-use adhesives used in flooring, panels, interiors and repair applications.

Financial Impact

The financial impact of water based adhesives is mainly linked to lower solvent exposure, easier regulatory positioning and better fit with recyclable paper-based packaging. Producers that offer stable quality and efficient application performance can help customers reduce adhesive waste, improve machine uptime and lower rework. This supports premium pricing in packaging, labels, hygiene and construction uses where consistency is more important than only low unit cost.

Raw material movement remains a key margin factor. Vinyl acetate, a major input for several water based adhesive systems, was priced at USD 0.83/kg in North America and USD 1.06/kg in Europe in June 2026. Acrylic acid, used in acrylic adhesive chemistry, was priced at USD 1.58/kg in North America and USD 1.19/kg in Northeast Asia during the same period. This makes feedstock-linked pricing and regional sourcing important for margin protection.

Profitability is expected to be stronger for suppliers that sell engineered formulations rather than commodity glue alone. H.B. Fuller reported a 34.2% adjusted gross margin in Q2 2026, up 200 basis points year over year, supported mainly by pricing execution and restructuring savings. This shows that disciplined pricing, raw material control and product mix can protect earnings even when industrial demand remains uneven.

Drivers Impact Analysis

The Water Based Adhesives Market is driven by rising demand for low-VOC, safer, and environmentally friendly bonding solutions across packaging, construction, woodworking, paper, labels, textiles, and automotive applications. These adhesives are preferred because they reduce solvent emissions and support safer workplace conditions.

Asia Pacific remains the strongest demand region due to packaging growth, construction activity, furniture manufacturing, and consumer goods production. China, India, Japan, South Korea, and Southeast Asia support strong consumption through industrial production and rising use of sustainable adhesive technologies.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for low-VOC adhesives | +2.6% | Asia Pacific, Europe, North America | Drives cleaner adoption. |

Growth in packaging applications | +2.2% | China, India, Southeast Asia, U.S. | Supports volume demand. |

Expansion of construction and woodworking | +1.8% | Asia Pacific, Middle East, North America | Builds bonding demand. |

Shift from solvent-based adhesives | +1.5% | Europe, U.S., Japan, South Korea | Supports regulatory adoption. |

Demand from labels and tapes | +1.2% | Global consumer goods markets | Adds steady usage. |

Restraints Impact Analysis

The market faces restraints from performance limitations in high-moisture, high-temperature, and heavy-duty bonding conditions. Some water based adhesives may need longer drying time or stronger formulation support compared with solvent-based alternatives.

Raw material cost volatility also affects market stability. Inputs such as acrylics, polyvinyl acetate, polyurethane dispersions, and additives can face price movement, which pressures manufacturer margins and customer pricing.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Performance limits in harsh conditions | -1.3% | Industrial and construction markets | Restricts application fit. |

Longer drying and curing time | -1.1% | Packaging, woodworking, assembly | Affects production speed. |

Raw material price volatility | -1.0% | Global producers | Pressures margins. |

Competition from hot-melt adhesives | -0.8% | Packaging and labeling markets | Limits share gain. |

Storage sensitivity and shelf-life issues | -0.6% | Humid and variable climates | Raises handling needs. |

Opportunities Impact Analysis

Opportunities are strong in flexible packaging, paper packaging, e-commerce labels, construction panels, furniture, hygiene products, and automotive interiors. These applications need reliable bonding while meeting sustainability and safety requirements.

Higher-value opportunities are also emerging in acrylic emulsion adhesives, polyurethane dispersion adhesives, and bio-based adhesive formulations. Producers that improve water resistance, bonding speed, and substrate compatibility can capture stronger margins.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Sustainable packaging growth | +2.5% | Asia Pacific, Europe, North America | Builds strong demand. |

Bio-based adhesive development | +2.0% | Europe, North America, Japan | Supports green innovation. |

Polyurethane dispersion adhesives | +1.8% | Automotive, textile, construction | Adds premium value. |

E-commerce label and tape demand | +1.5% | Global retail logistics | Expands usage volume. |

Furniture and wood bonding growth | +1.3% | Asia Pacific, Europe, North America | Supports industrial demand. |

Challenges Impact Analysis

The main challenge is improving performance while keeping adhesives cost-competitive. Customers want water based adhesives that offer strong bonding, quick drying, moisture resistance, and durability without adding major production cost.

Another challenge is adapting formulations for different substrates. Paper, plastic films, wood, textiles, metal, and composites need different adhesive properties, so manufacturers must invest in technical service and application-specific product development.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Achieving faster bonding speed | -1.1% | Packaging and assembly lines | Affects productivity. |

Improving moisture resistance | -1.0% | Construction, packaging, woodworking | Raises formulation needs. |

Meeting substrate-specific requirements | -0.9% | Global end users | Increases customization. |

Maintaining price competitiveness | -0.8% | Emerging and mass markets | Limits premium pricing. |

Managing formulation stability | -0.6% | Global adhesive producers | Affects product quality. |

Segment Covered in the Report

By Resin Type

Acrylic Polymer Emulsion

Polyvinyl Acetate

Vinyl Acetate Ethylene Emulsion

Styrene Butadiene Latex

Polyurethane Dispersion

Others

By Application

Tapes and Labels

Paper and Packaging

Woodworking

Building and Construction

Automotive

Others

By End-Use Industry

Building and Construction

Packaging

Automotive

Healthcare

Consumer Goods

Others

By Substrate

Paper and Paperboard

Plastics and Films

Wood

Metal

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward acrylic polymer emulsion, polyvinyl acetate, and polyurethane dispersion-based adhesives. These technologies are gaining preference because they support lower emissions, better safety, and wider use across packaging, wood, paper, and construction applications. Packaging remains a major trend area because brands and converters are shifting toward recyclable and low-emission bonding materials. Water based adhesives are also gaining traction in labels, tapes, cartons, flexible packaging, and paperboard applications.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Acrylic emulsion adhesives gain demand | +2.3% | Asia Pacific, Europe, North America | Leads formulation growth. |

Packaging remains key application | +2.1% | Global consumer markets | Drives volume usage. |

Polyvinyl acetate use expands | +1.7% | Woodworking, paper, construction | Supports stable demand. |

Low-emission bonding gains preference | +1.5% | Europe, U.S., Japan, South Korea | Supports compliance needs. |

Pressure-sensitive adhesives grow | +1.2% | Labels, tapes, hygiene products | Adds recurring demand. |

Investor Type Impact Matrix

Investors should focus on water based adhesive producers with strong formulation capability, reliable raw material access, and exposure to packaging, construction, woodworking, and labels. These end-use areas provide diversified demand and reduce dependence on one application. Strategic investors can also target bio-based adhesives, recyclable packaging solutions, and high-performance emulsion technologies. Companies that combine environmental compliance with strong bonding performance are better positioned for long-term growth.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Water Based Adhesive Producers | +2.2% | Global | Expands product capacity. |

Packaging Material Companies | +1.9% | Asia Pacific, Europe, North America | Drives adhesive demand. |

Construction Chemical Companies | +1.5% | Asia Pacific, Middle East, North America | Supports building use. |

Specialty Polymer Suppliers | +1.3% | Global adhesive value chains | Strengthens formulation supply. |

Sustainability-Focused Investors | +1.1% | Europe, North America, Asia Pacific | Funds cleaner adhesives. |

Recent Developments

In April 2026, Henkel expanded its paper coatings portfolio with water based barrier and heat seal coatings for paper packaging. The solutions are designed to improve recyclability, heat sealing, food-contact suitability, and protection against water, grease, oils, and humidity. This development is important because packaging converters are shifting from plastic laminates toward recyclable paper-based formats.

In March 2026, H.B. Fuller announced a global price adjustment across all product lines. The company stated that a minimum 10% price increase would take effect from April, 2026, with higher increases in selected technologies and regions. This indicates continued cost pressure from raw materials, logistics, and supply continuity across the adhesive industry.

In June 2026, WACKER announced price increases of up to 15% for resins, dispersions, and dispersible polymer powders sourced from Europe and the U.S. These materials are key inputs for water based adhesives, sealants, coatings, construction chemicals, and paper applications. The move shows that polymer dispersion costs remain a major factor for adhesive formulators.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Henkel AG & Co. KGaA

3M Company

BASF SE

Sika AG

Dow Inc.

H.B. Fuller Company

Ashland Inc.

Kraton Corporation

Wacker Chemie AG

DIC Corporation

Arkema S.A.

Avery Dennison Corporation

Pidilite Industries Limited

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Carbon Capture Chemicals Market Size to Reach USD 78.0 Billion by 2035

Carbon Capture Chemicals Market By Chemical Type (Amines, Carbonates, Ammonia-based Solvents, Ionic Liquids, Solid Sorbent Chemicals, Others), By Absorption Type (Chemical Absorption, Physical Absorption), By End-Use Industry (Oil and Gas, Power Generation, Chemical and Petrochemical, Cement, Iron and Steel, Others), By Application (Post-combustion Capture, Pre-combustion Capture, Industrial Gas Separation, Direct Air Capture, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Bio-based Chemicals Market Size to Hit USD 296.7 Bn by 2035

Bio-based Chemicals Market By Product Category (Platform Chemicals, Polymers for Plastics, Paints, Coatings, Inks and Dyes, Surfactants, Cosmetics and Personal Care Products, Adhesives, Man-made Fibers, Others), By Application (Industrial, Agricultural, Pharmaceutical, Others), By Source (Plant-based, Animal-based, Microbial-based, Waste-based), By End Use (Chemical Manufacturing, Agriculture, Food and Beverage, Personal Care, Pharmaceuticals, Automotive), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Processing Chemicals Market Size to Hit USD 14.6 Billion by 2035

Hydrogen Processing Chemicals Market By Chemical Type (Catalysts, Adsorbents, Solvents, Corrosion Inhibitors, Scavengers, Others), By Function (Reforming Chemicals, Purification Chemicals, Hydroprocessing Chemicals, Gas Treatment Chemicals, Corrosion Control Chemicals, Others), By Process (Steam Methane Reforming, Hydrocracking, Hydrotreating, Pressure Swing Adsorption, Water-Gas Shift Reaction, Others), By End Use (Refineries, Ammonia Production, Methanol Production, Petrochemicals, Clean Hydrogen Plants, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Electrolyte Chemicals Market to Cross USD 49.4 Billion by 2035

Electrolyte Chemicals Market By Battery Type (Lithium-ion Electrolytes, Lead-acid Electrolytes, Flow Battery Electrolytes, Others), By Electrolyte Form (Liquid Electrolytes, Gel, Solid-State Electrolytes), By Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, Industrial and Motive Batteries, Others), By Product Type (Lithium-Based Electrolytes, Sulfide-Based Electrolytes, Polymer-Based Electrolytes, Oxide-Based Electrolytes, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035