Market Size and Growth Projections

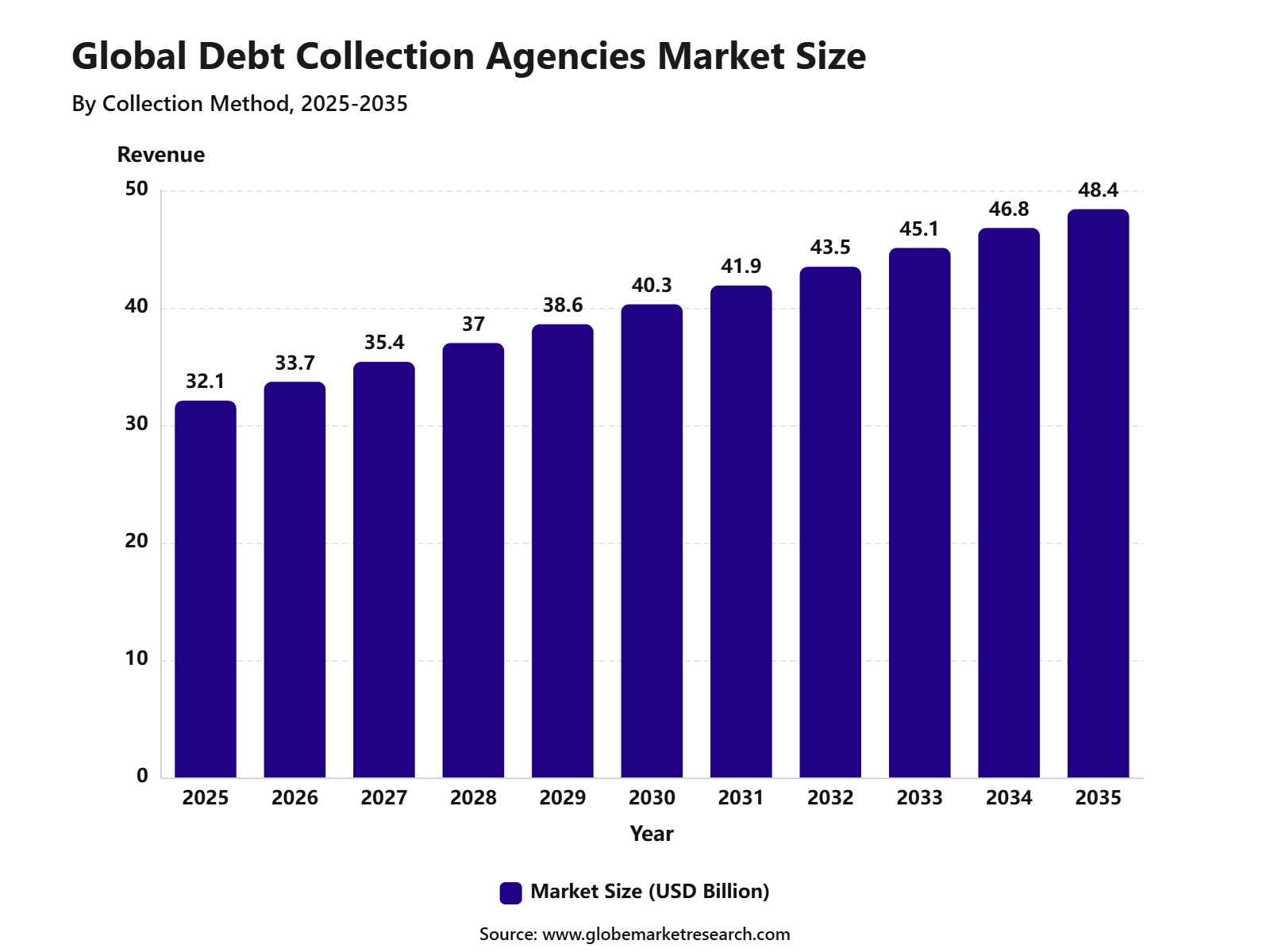

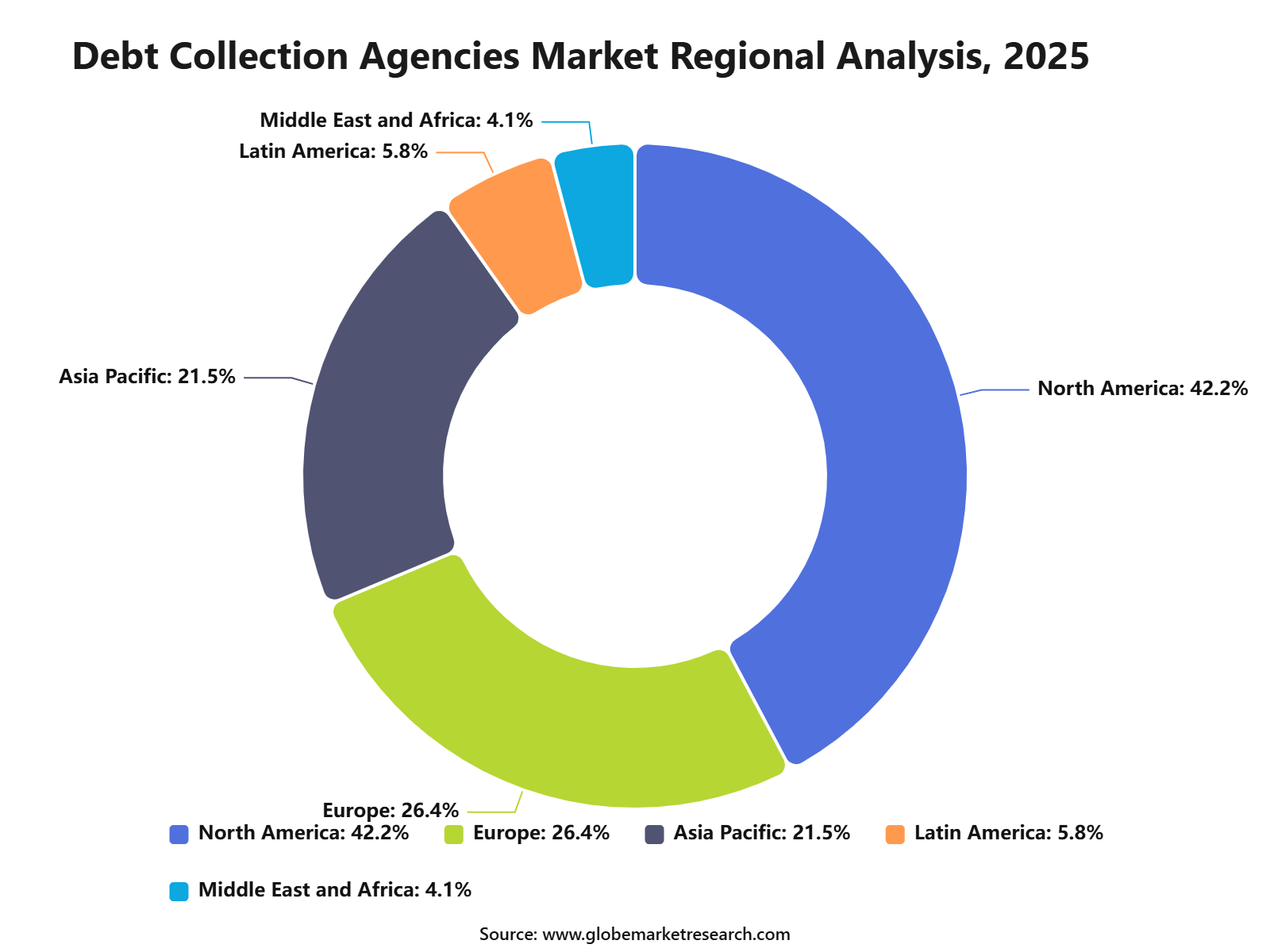

According to Globe Market Research, the global debt collection agencies market was valued at USD 32.1 billion in 2025 and is projected to reach USD 48.4 billion by 2035, growing at a 4.2% CAGR. North America led the market with 42.2% share in 2025, supported by high consumer borrowing, large financial services activity, and established third-party collection practices.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 32.1 Billion |

Projected Revenue, 2035 | USD 48.4 Billion |

CAGR, 2025-2035 | 4.2% |

Largest Region | North America, 42.2% Share |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

Debt collection agencies help banks, lenders, healthcare providers, telecom companies, utilities, retailers, and government bodies recover overdue payments. The market is being shaped by rising consumer debt, higher delinquency pressure, demand for outsourced recovery services, and stronger adoption of compliant digital collection platforms.

The latest U.S. credit data shows why recovery services remain important. Based on data from Federal Reserve Bank of New York, U.S. household debt reached USD 18.8 trillion in Q1 2026, while credit card balances stood at USD 1.25 trillion and auto loan balances reached USD 1.69 trillion. Around 4.8% of outstanding debt was in some stage of delinquency, and 5.0% of consumers had a third-party collection account on their credit report.

Why the Debt Collection Agencies Market Is Growing

The growth of the debt collection agencies market can be attributed to rising consumer credit use, loan defaults, unpaid invoices, healthcare receivables, telecom dues, utility bills, and financial service delinquencies. As lenders and service providers face higher overdue account volumes, specialized recovery partners are being used to improve collection efficiency and reduce internal operating costs.

Credit conditions also support demand for professional recovery services. U.S. bankruptcy filings increased 11.5% in the year ending June 30, 2025, reaching 542,529 filings, compared with 486,613 in the prior year. This indicates that more households and businesses are under financial stress, which can increase demand for settlement, restructuring, legal recovery, and receivables management services.

At the same time, agencies must operate carefully because debt collection is a sensitive consumer-facing service. The strongest demand is expected for companies that combine recovery performance with fair communication, audit-ready documentation, digital payment options, and complaint reduction.

Bad Debt Remains the Leading Debt Type

Bad debt led the debt type segment with 65.9% share, supported by rising overdue consumer loans, credit card balances, unpaid medical bills, personal loans, and defaulted financial accounts. This segment remains important because banks, lenders, healthcare providers, telecom operators, and retailers depend on agencies to recover unpaid balances and reduce financial losses.

The growth of bad debt collection is also linked to higher credit exposure across households and businesses. When borrowers face pressure from interest costs, inflation, job uncertainty, or repayment fatigue, overdue accounts can rise across unsecured and installment credit products.

For agencies, bad debt creates revenue opportunity, but recoverability risk must be managed. Older accounts, disputed balances, poorly documented loans, bankrupt borrowers, deceased accounts, and accounts outside legal recovery limits can reduce collection success and increase compliance risk.

Third-Party Agencies Are Gaining Importance

Third-party agencies accounted for 53.6% share by agency type. These agencies are hired by creditors when internal collection teams are unable to recover balances efficiently or when lenders prefer to outsource complex recovery work to specialists. The segment is supported by the need for trained collectors, legal knowledge, compliance controls, large-scale account handling, and technology-enabled recovery workflows.

Third-party agencies are especially useful for banks, fintech lenders, telecom companies, healthcare providers, utilities, and retailers that want to protect internal resources. However, outsourcing must be managed carefully. Creditors remain exposed to reputation risk when agency communication is aggressive, unclear, or non-compliant. This is why vendor selection, complaint monitoring, call controls, data quality, and regulatory audits are becoming more important.

Traditional Collection Still Leads, but Digital Collection Is Rising

Traditional collection held 48.5% share by collection method, supported by continued use of phone calls, letters, notices, field follow-ups, and direct negotiation. This method remains useful for older accounts, complex disputes, legal recovery cases, and borrowers who respond better to human contact. Digital debt collection is gaining momentum because borrowers increasingly prefer self-service repayment tools, SMS reminders, emails, digital payment links, chat-based support, and online portals.

These tools can reduce manual effort, improve repayment convenience, and support better documentation. The shift is not only about automation. The future model is likely to be hybrid, where digital tools manage reminders, payments, segmentation, and routine communication, while human agents handle disputes, hardship cases, legal issues, and sensitive borrower interactions.

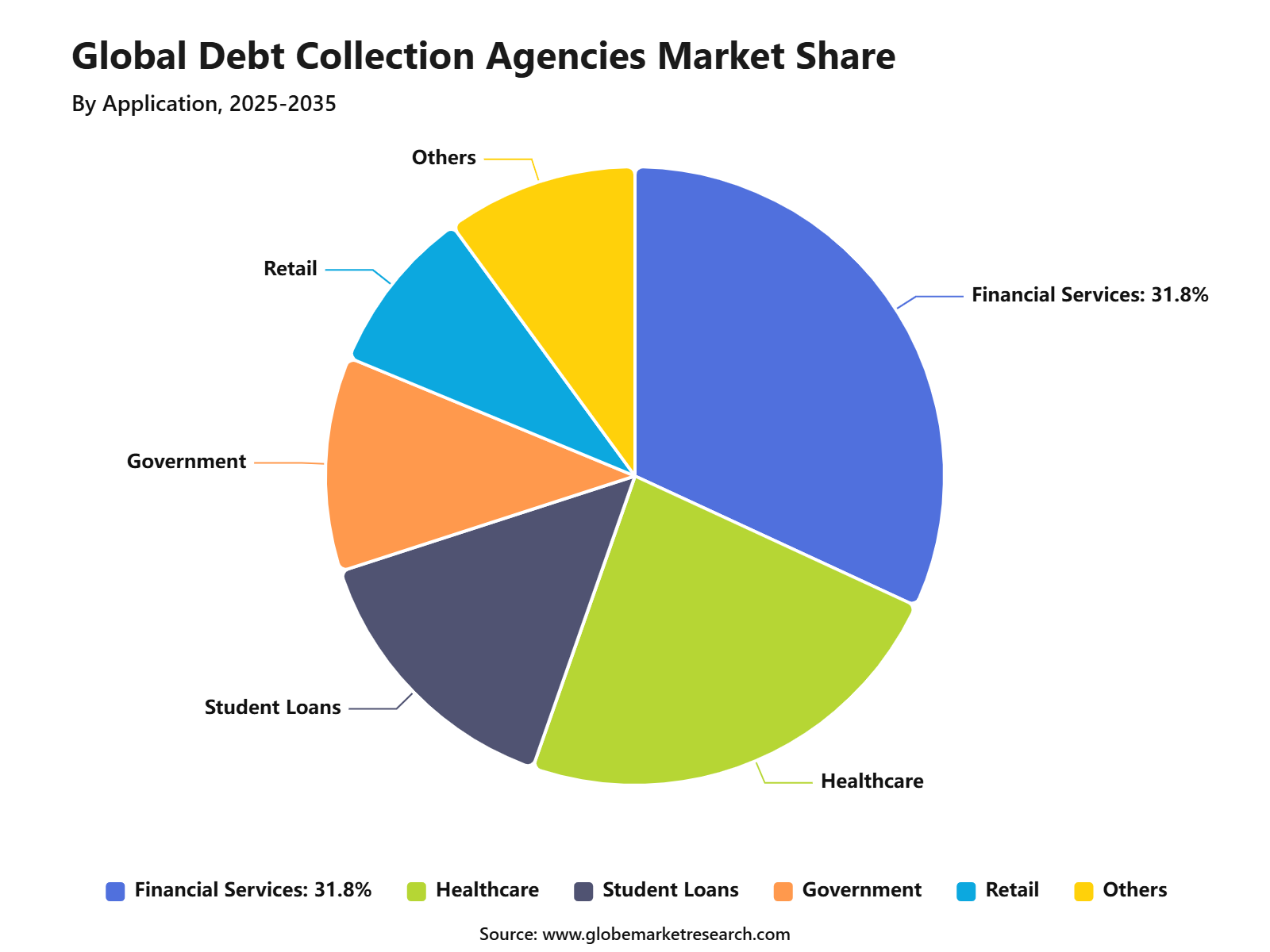

Financial Services Lead the Application Segment

Financial services captured 31.8% share by application, driven by credit card debt, personal loans, auto loans, mortgages, fintech lending, and other consumer credit products. Banks, credit card issuers, non-bank lenders, mortgage providers, and auto finance companies generate large volumes of overdue accounts that require structured recovery support. The financial services segment is being supported by high borrowing levels.

In Q1 2026, U.S. credit card balances stood at USD 1.25 trillion, while student loan balances were USD 1.66 trillion and mortgage balances reached USD 13.19 trillion. These large credit pools create ongoing demand for early-stage recovery, late-stage collection, restructuring, and account resolution services. For lenders, debt collection agencies are becoming part of broader risk management. Recovery quality, consumer treatment, dispute resolution, data security, and regulatory compliance are now as important as collection volume.

North America Leads

North America led the market with 42.2% share in 2025, supported by high consumer credit usage, mature financial services, strict recovery regulations, and strong demand for third-party collection services. The region has a large base of banks, card issuers, healthcare providers, telecom firms, utilities, and retail lenders that require collection support.

The U.S. remains the most important local market because it has large credit card, auto loan, mortgage, student loan, healthcare, telecom, and utility receivable pools. The New York Fed reported that about 124,000 consumers had a bankruptcy notation added to their credit reports in Q1 2026, while about 59,000 individuals had new foreclosures on their credit reports.

Europe is expected to remain highly compliance-led, while Asia Pacific is being supported by credit expansion, digital lending, and fintech growth. Local success will depend on licensing rules, borrower protection laws, repayment behavior, digital payment adoption, and lender outsourcing preferences.

Compliance Is the Main Operating Priority

Debt collection is highly regulated because it directly affects consumers under financial stress. The Fair Debt Collection Practices Act is intended to eliminate abusive debt collection practices and protect collectors that follow the law from being unfairly disadvantaged. Call-frequency compliance is especially important in the U.S. Under the CFPB Debt Collection Rule, collectors are presumed to violate the law if they place more than seven calls within seven days about a particular debt or call within seven days after a phone conversation about that debt.

Complaint management is also becoming central. The CFPB received approximately 387,400 debt collection complaints in 2025, and around 304,700, or 79%, were sent to companies for review and response. This shows that documentation, response quality, dispute handling, and consumer communication practices are now critical operating measures.

Technology Adoption Is Improving Recovery Efficiency

AI and predictive analytics are becoming important in debt collection because they can help agencies score accounts, segment borrowers, prioritize outreach, identify hardship cases, and improve repayment probability. The linked report identifies AI and predictive analytics as a technology adoption factor with +0.9% estimated CAGR impact.

Digital payment portals are another important technology area. They allow consumers to pay securely, set up repayment plans, confirm balances, and access account information without always speaking to an agent. This can improve repayment speed and reduce friction.

CRM platforms, automated messaging systems, case management tools, and data security solutions are also becoming essential. Agencies that can combine technology with compliant human oversight are expected to perform better than agencies that rely only on high-volume calling.

Analyst Perspective

What the Data Is Telling Debt Collection Companies?

From an analyst perspective, the data shows that debt collection is shifting from a volume-based business to a compliance-led recovery model. The market is growing steadily, but not aggressively, with a 4.2% CAGR through 2035. This means agencies will need efficiency, trust, and technology adoption to improve profitability rather than relying only on market expansion. The strongest signal is that demand is being supported by consumer credit pressure.

U.S. household debt stood at USD 18.8 trillion in Q1 2026, while 4.8% of debt was delinquent. This creates a large recovery need, but agencies must balance collection activity with borrower affordability and legal requirements. For clients, the message is clear. Debt collection partners should not be selected only on recovery promises. They should be evaluated on compliance strength, complaint performance, digital capability, documentation quality, and ability to protect brand reputation.

What Opportunities Are Emerging?

The first major opportunity is digital debt collection. Digital portals, automated reminders, online repayment plans, SMS updates, and payment links can improve convenience for borrowers and reduce manual workload for agencies. The report identifies growth in digital debt collection as an opportunity with +1.0% estimated CAGR impact.

The second opportunity is AI-based recovery analytics. Agencies can use data models to prioritize accounts, identify repayment probability, segment borrowers, and improve agent productivity. This is especially useful for banks, fintech lenders, telecom firms, and utilities managing high account volumes.

Healthcare collections and fintech lending are also emerging opportunity areas. Healthcare providers need careful receivables recovery, while fintech lenders need fast, digital-first workflows. Agencies that can handle these sectors with compliant, consumer-friendly communication may gain stronger client demand.

What Risks Should Companies Be Aware Of?

The first risk is regulatory exposure. Debt collection rules are strict, and complaints can damage both agency reputation and client trust. The CFPB’s 2025 complaint data shows that debt collection remains one of the most sensitive financial service areas.

The second risk is poor borrower experience. Aggressive communication, unclear balance validation, limited hardship options, and weak dispute handling can increase complaints and reduce repayment willingness. In a regulated market, poor treatment can become both a legal and commercial problem.

The third risk is lower recovery quality in stressed accounts. Rising bankruptcy filings, higher delinquencies, and borrower affordability pressure can increase collection demand, but they can also reduce successful recovery rates. This makes portfolio scoring and account documentation more important.

What Decisions Should Clients Make Next?

Clients should first define the collection model they need. Early-stage accounts may require customer-friendly reminders and digital payment tools, while late-stage accounts may require negotiation, legal review, settlement planning, or specialist recovery support.

Second, clients should select agencies based on compliance and recovery quality. Important measures include complaint rate, validation accuracy, right-party contact controls, call frequency compliance, dispute response time, audit readiness, and data security standards.

Third, clients should invest in digital recovery infrastructure. Self-service payment portals, hardship workflows, automated reminders, CRM integration, and AI-based segmentation can improve recovery performance while reducing manual effort. The best results are expected when digital tools are combined with trained human support for complex cases.

Competitive Landscape

The debt collection agencies market includes debt recovery firms, debt buyers, third-party agencies, legal recovery providers, and digital collection platforms. Key companies include Encore Capital Group, PRA Group, Intrum AB, EOS Group, Credit Collection Services, IC System, Resurgent Capital Services, Northland Group, Convergent Outsourcing, Transworld Systems, CBE Group, Midland Credit Management, Apex Asset Management, and Account Control Technology.

Competition is increasing as clients demand stronger compliance, digital capability, better reporting, and lower complaint exposure. Agencies with advanced analytics, secure data systems, trained recovery teams, and industry-specific workflows are likely to gain stronger client preference. The strongest players are expected to be those that can recover debt while protecting consumer rights and client reputation. In this market, trust, documentation, and regulatory discipline are becoming as important as collection performance.

Latest Recent Developments

Market News

In 2026, Encore Capital Group reported strong U.S. receivables purchasing conditions, with global portfolio purchases of USD 363 million in Q1 2026 and record collections of USD 718 million. The update indicates that large debt purchasers are benefiting from higher charged-off consumer receivables and stronger digital recovery execution.

In 2026, Intrum continued its transition toward a capital-light operating model supported by operational technology, digital channels, and AI-driven collection tools. The company reported that it delivered SEK 92 billion to clients across 20 European markets in 2025, reflecting the role of large credit management firms in outsourced receivables recovery.

In 2026, CredResolve raised its focus on AI-powered collections infrastructure, combining voice bots, digital channels, field agent networks, and legal automation. The company said it was managing more than USD 6 billion in monthly assets across more than 40 lenders and 10 Indian states, showing rising demand for full-stack digital recovery models.

Funding

In 2026, CredResolve raised Pre-Series A funding led by Merak Ventures, with participation from Unleash Capital Partners and CDM Capital. The capital will be used to expand operations to 15 Indian states, strengthen multilingual AI and voice capabilities, and build a self-serve platform for lenders.

In 2025, DPDzero raised USD 7 million in Series A funding led by GMO Venture Partners, with participation from SMBC Asia Rising Fund, Blume Ventures, India Quotient, Sinarmas Group, and others. The funding will support a multilingual AI collection agent and a professional field collection network.

In 2025, Murphy raised USD 15 million in pre-seed and seed funding led by Northzone, with participation from ElevenLabs, Lakestar, Seedcamp, and existing investors. The company is building autonomous multilingual AI agents for debt recovery across banking, BNPL, utilities, healthcare, and telecom use cases.

Mergers and Acquisitions

In 2026, doValue completed the acquisition of coeo Group GmbH. coeo specializes in managing non-bank originated receivables using artificial intelligence, and the acquisition supports doValue’s diversification into new clients, geographies, and digital recovery models.

In 2025, TrueAccord acquired Sentry Credit, a Washington-based debt collection agency. The deal expanded TrueAccord’s client portfolio and added first-party collection and litigation services to its digital-first collection model.

In 2025, Aldaron Partners and True Wind Capital acquired DCM Services, an estate and specialty account recovery provider. The acquisition is expected to support growth in financial services, healthcare, automotive, retail, telecommunications, and utilities receivables recovery.

Conclusion

The debt collection agencies market is entering a more regulated and technology-driven phase. Growth is supported by rising consumer credit usage, bad debt volumes, financial service delinquencies, healthcare receivables, and demand for outsourced recovery services. Future growth will be led by digital debt collection, AI-based borrower segmentation, payment portals, compliant omnichannel communication, and third-party recovery services. However, agencies must manage strict regulations, consumer privacy concerns, complaint risk, and lower recoverability in stressed accounts.