Market Size

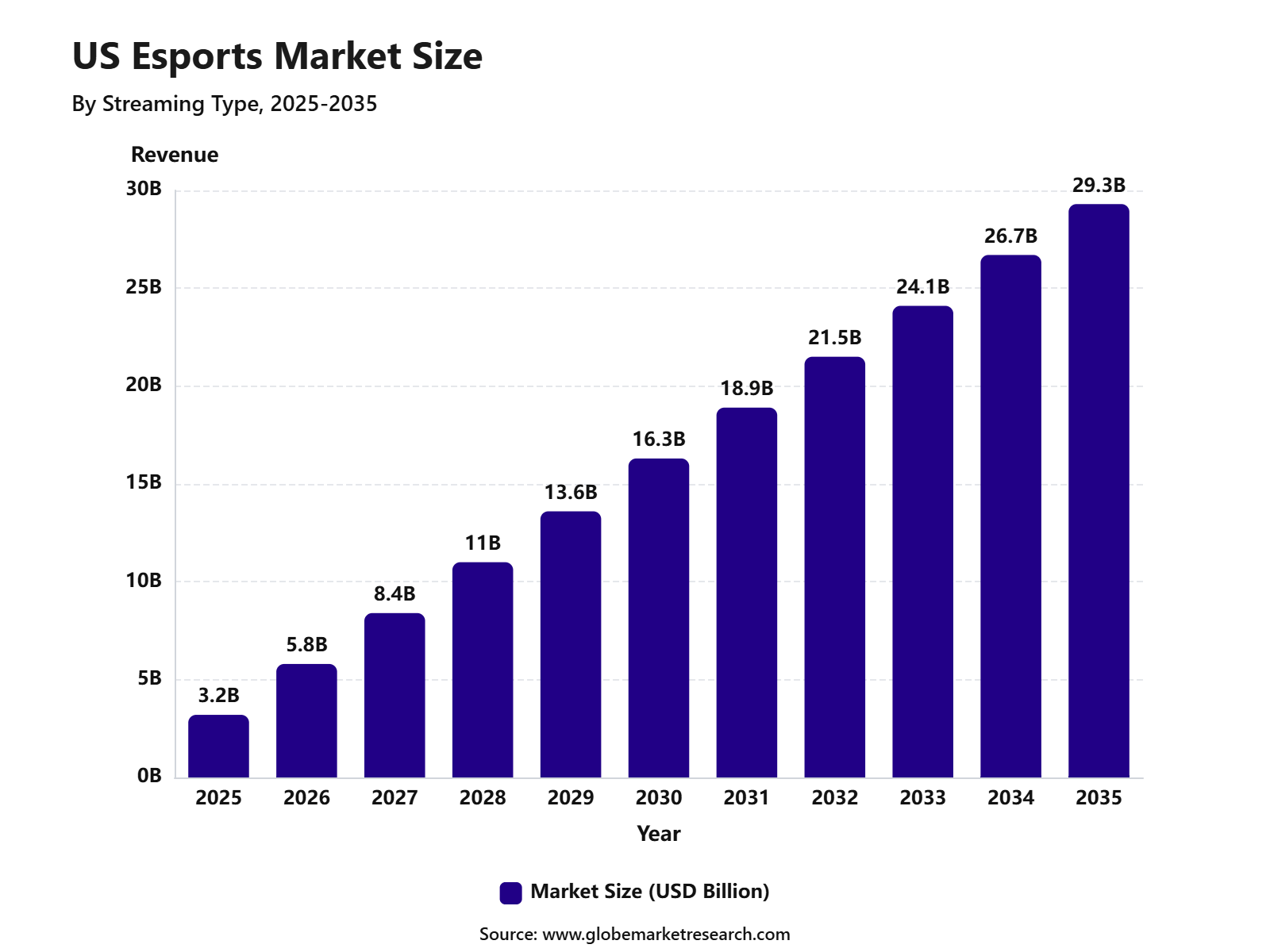

According to Globe Market Research, The U.S. Esports Market was valued at USD 3.2 billion in 2025 and is projected to reach USD 29.3 billion by 2035 , growing at a CAGR of 24.8% from 2025 to 2035. Growth is being supported by rising esports viewership, stronger brand sponsorships, live-streamed tournaments, game publisher participation, and the expansion of digital advertising across gaming platforms.

Key Parameter | Report Details |

|---|---|

Current Revenue, 2025 | USD 3.2 Billion |

Projected Revenue, 2035 | USD 29.3 Billion |

CAGR, 2025 To 2035 | 24.8% |

Largest Region | United States |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

The U.S. has one of the strongest gaming audiences in the world, which creates a large base for esports participation and viewership. The Entertainment Software Association reported that 212.3 million Americans play video games every week , representing 67% of Americans aged 5 to 90 . This wide gaming base supports esports through live viewing, team fandom, creator-led content, competitive play, and digital communities.

Esports is also benefiting from the shift of advertising budgets toward digital video. IAB reported that U.S. digital video ad spending is projected to surpass USD 80 billion in 2026 , growing 11% year over year and accounting for more than 60% of total TV and video ad spend for the first time. This is important for esports because tournaments, livestreams, creator clips, and gaming content compete directly within digital video budgets.

Top Market Takeaway

Advertising and sponsorships led the revenue source segment with 45.3% share. Growth was supported by brand partnerships, tournament visibility, audience-based digital campaigns, in-stream ads, and event sponsorships.

PC gaming platforms held 43.6% share by platform. This was driven by professional esports formats, high-performance gameplay demand, keyboard-and-mouse precision, and strong use of PC-based competitive titles.

MOBA games accounted for around 30.7% share by game genre. The segment was supported by team-based competition, loyal fan communities, organized tournaments, and strong viewer engagement.

Live streaming captured more than 42.3% share by streaming type. Growth was driven by real-time match viewing, creator-led commentary, live chat, and interactive fan participation.

Smartphones held 50.5% share by device type. This was supported by mobile gaming growth, easy access to esports content, and rising participation among casual and competitive players.

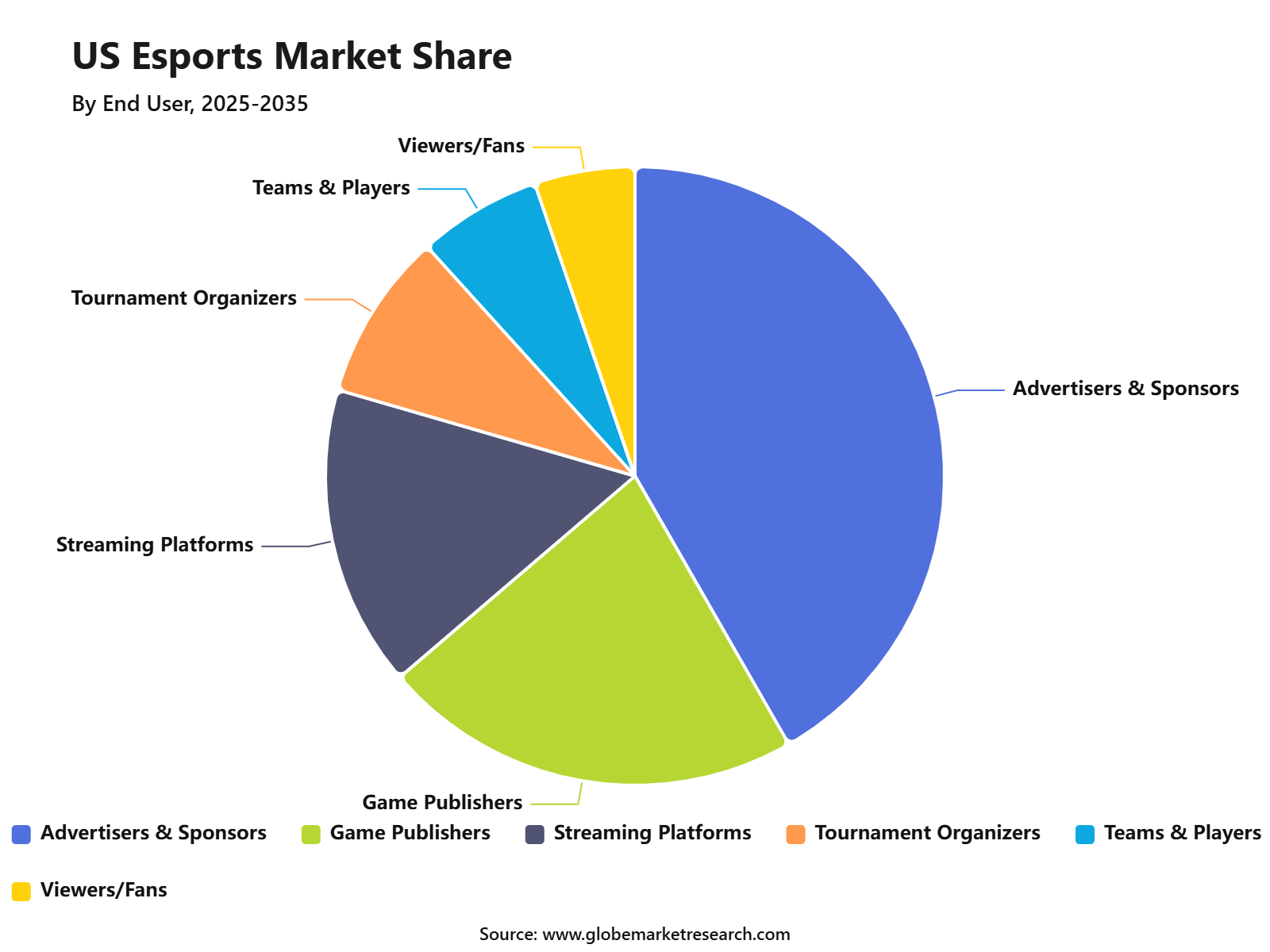

Advertisers and sponsors accounted for 41.3% share by end user. Demand was driven by targeted audience reach, brand visibility, tournament partnerships, and esports media campaigns.

Top Funding and Investment Trends

The U.S. esports market is moving from hype-led funding toward disciplined investment in teams, live events, college esports, gaming venues, creator-led media, publisher-backed leagues, and brand sponsorships. Investment is being supported by a large gaming base, as 212.3 million Americans play video games for at least one hour per week, while total U.S. video game consumer spending reached USD 60.7 billion in 2025.

The funding environment is selective, but the market remains attractive because esports sits inside a large gaming economy. The U.S. video game industry supports more than 250,000 jobs and generates USD 95.8 billion in total economic impact, creating a strong base for esports leagues, gaming content, live events, college programs, and gaming infrastructure.

Investment Area | Latest Signal | Market Impact |

|---|---|---|

Esports clubs | Esports Foundation selected 40 clubs for its USD 20 million 2026 Club Partner Program, including 100 Thieves, Cloud9, NRG, Sentinels, and Team Liquid. | Supports U.S. team branding, fan growth, content production, and global competition exposure. |

Gaming and esports media | GameSquare added a USD 2 million credit facility and divested its remaining FaZe Media stake while retaining 100% ownership of FaZe Esports. | Shows investor focus on leaner esports operations and profitable competitive assets. |

Publisher-led U.S. circuits | Garena launched a U.S. Free Fire competitive circuit for 2026 after the FFUSC brought USD 60,000 in cumulative prize money in 2025. | Opens fresh investment space in mobile esports, grassroots tournaments, and open qualifiers. |

Live esports events | FaZe Vegas will host the 2026 Call of Duty League Championship Weekend in Las Vegas. | Strengthens U.S. esports tourism, ticketing, venue revenue, and sponsor activation. |

Esports venues | Friendly Fire plans major Texas expansion, with at least five esports cafés planned in Austin, Dallas, Houston, and San Antonio. | Supports location-based gaming, franchise revenue, and community esports participation. |

College esports | ESA Foundation will continue its collegiate esports scholarship for the 2026 to 2027 academic year. | Builds the talent pipeline for players, coaches, broadcasters, and gaming professionals. |

By Revenue Source

Advertising and sponsorships led the revenue source segment with 45.3% share, supported by brand partnerships, tournament visibility, team sponsorships, creator campaigns, and audience-focused digital promotions. Esports gives advertisers access to young, engaged, and digitally active audiences through live tournaments, streaming platforms, in-game placements, and social media content.

This segment is also supported by the growth of live gaming content. Global live streaming viewership reached 36.4 billion hours watched in 2025, up 6% from 2024, which increased the value of sponsor exposure across tournaments, creator-led streams, and esports broadcasts.

By Platform

PC gaming platforms held 43.6% share, driven by professional esports tournaments, competitive game formats, high-performance gameplay needs, and strong adoption among serious players. PC platforms remain important because they support faster controls, advanced graphics, high refresh rates, and deeper customization, which are essential in competitive titles.

The segment also benefits from strong spending across PC, cloud, and non-console gaming formats. In March 2026, U.S. PC, cloud, and non-console VR content spending increased 28% year-on-year, showing continued demand for advanced gaming formats that support competitive play.

By Game Type

MOBA games accounted for around 30.7% share, supported by strong team-based competition, loyal fan communities, structured leagues, and high viewer engagement. These games are attractive for esports because they combine strategy, skill, teamwork, and long-term fan loyalty, making them suitable for both professional play and streaming audiences.

Viewer data also supports the strength of MOBA esports. In 2025, League of Legends and Mobile Legends: Bang Bang each surpassed 400 million hours watched on YouTube Gaming, while Worlds 2025 peaked at 3.8 million concurrent viewers on the platform.

By Streaming Type

Live streaming captured more than 42.3% share, driven by real-time match viewing, creator-led commentary, watch parties, live chat, and interactive fan participation. Esports audiences prefer live formats because they provide instant reactions, community discussion, and shared viewing around major matches and tournaments.

The live streaming base continues to expand across major gaming platforms. YouTube Gaming reached a record 8.8 billion hours watched in 2025, representing 12% year-on-year growth and around 25% of hours watched across live-streaming gaming platforms.

By Device

Smartphones held 50.5% share, supported by mobile gaming growth, easy access, lower device barriers, and rising participation among casual and competitive players. Mobile devices help esports reach users who may not own gaming PCs or consoles, making competitive gaming more accessible across income groups, age groups, and smaller cities.

The wider U.S. gaming population also supports smartphone-led participation. ESA reported that 67% of Americans play video games for more than one hour per week in 2026, equal to 212.3 million weekly players. This creates a broad audience base for mobile esports, casual competitions, and app-based tournament formats.

By End User

Advertisers and sponsors accounted for 41.3% share, driven by strong demand for targeted audience reach, brand visibility, tournament partnerships, influencer collaborations, and digital campaign performance. Esports allows brands to connect with gaming communities through sponsored teams, branded tournaments, creator content, product placements, and live-stream integrations.

The segment is gaining strength as gaming becomes a mainstream entertainment channel. U.S. video game spending reached USD 60.7 billion in 2025, the second-highest annual total on record, while content spending reached USD 52.3 billion. This scale makes esports attractive for advertisers seeking measurable engagement within the broader gaming economy.

Emerging Trends

Creator-led esports viewing is rising: Esports viewing is becoming more creator-led, with fans watching matches through streamers, co-streamers, and commentators rather than only through official broadcasts. This trend is improving engagement because audiences often prefer familiar personalities, live reactions, and community-based viewing. Sponsored streams also gained strength in 2025, with YouTube Gaming sponsored streams reaching 4.5 million hours watched in Q4 2025.

Mobile esports is expanding access: Mobile esports is becoming more important because smartphones allow more users to participate without expensive hardware. This trend is especially relevant for younger players, casual gamers, and first-time competitive players. Smartphone-based esports also supports short-format tournaments, social gaming, and regional competitions.

Live streaming platforms are becoming core revenue channels: Streaming platforms are no longer only distribution channels. They are becoming monetization centers through advertising, subscriptions, sponsorships, fan donations, merchandise links, and creator partnerships. The rise of 36.4 billion live streaming hours watched in 2025 shows that esports revenue is increasingly tied to digital audience attention.

Esports is moving closer to mainstream sports marketing: Brands are using esports to reach audiences that are difficult to engage through traditional media. Sponsorship value is being supported by tournament visibility, team loyalty, creator influence, and real-time fan engagement. This is making esports more attractive for advertisers from technology, food and beverages, apparel, fintech, telecom, and entertainment.

Factors Affecting the Esports Market

Strong gaming participation supports audience growth: A large gaming population is the strongest base for the U.S. esports market. In 2026, 212.3 million Americans played video games weekly, and the player base was spread across age groups and genders. This supports esports viewership, amateur tournaments, mobile gaming, influencer content, and brand partnerships.

Consumer spending affects monetization: Esports depends on the broader gaming economy because spending on content, hardware, subscriptions, accessories, and in-game purchases supports the ecosystem. U.S. video game spending reached USD 60.7 billion in 2025, while subscription services recorded a 20% increase. This supports stronger monetization opportunities for competitive gaming platforms and event organizers.

Platform competition influences audience reach: Esports growth is shaped by where audiences watch content. Twitch, YouTube Gaming, and other platforms compete for creators, tournaments, and fan attention. YouTube Gaming reached 8.8 billion hours watched in 2025, showing that platform strategy, discoverability, and creator partnerships can strongly affect esports visibility.

Game title popularity affects tournament demand: Esports revenue is highly linked to the popularity of specific games. MOBA, FPS, battle royale, and sports simulation titles attract different audiences and sponsor categories. If a major game loses active players or competitive relevance, tournament viewership and sponsorship returns can be affected.

Brand safety and regulation remain important: Esports involves younger audiences, online chat, in-game purchases, creator content, and live communities. This makes brand safety, age-appropriate advertising, moderation, privacy, and responsible monetization important for sponsors and platforms. Strong governance is needed to protect audience trust and long-term brand investment.

Top Use Cases

Brand sponsorship and advertising: Esports is widely used by brands for digital advertising, jersey sponsorships, tournament naming rights, creator campaigns, and product placements. The format is useful because it provides targeted reach and direct engagement with gaming audiences.

Tournament and league monetization: Tournament organizers use esports to generate revenue through sponsorships, ticketing, media rights, live streaming, merchandise, and premium digital content. Major events also support local fan communities and help build long-term game loyalty.

Live streaming and creator partnerships: Streaming is one of the most important use cases in esports. Creators provide commentary, reactions, analysis, and community interaction, which helps expand viewership beyond official broadcasts.

Team branding and fan engagement: Esports teams use digital channels to build fan communities, sell merchandise, promote sponsors, and create year-round content. This helps teams remain visible even outside major tournament periods.

Mobile esports participation: Smartphone-based esports supports casual competitions, short tournaments, campus events, and regional gaming communities. It also helps expand esports access among users who may not have high-cost gaming hardware.

College and youth esports programs: Schools, colleges, and community organizations are using esports for student engagement, teamwork, digital skills, and organized competition. This use case is helping esports move from entertainment into structured education and community programs.

Competitive Landscape

The U.S. esports market is competitive, with game publishers, streaming platforms, tournament organizers, professional teams, sponsors, media companies, and technology providers all playing important roles. Companies are focusing on live event formats, digital fan engagement, sponsorship packages, franchise leagues, content monetization, and cross-platform gaming.

The market is expected to benefit from stronger media rights opportunities, brand partnerships, mobile esports formats, creator-led tournaments, college esports growth, and live event expansion across major U.S. cities.

Key Market Segments

By Revenue Source

Advertising & Sponsorships

Media Rights

Merchandise & Tickets

Publisher Fees

Others

By Platform

PC Gaming Platforms

Console Gaming Platforms

Mobile & Tablet Platforms

Others

By Game Genre

MOBA Games

First-Person Shooter Games

Battle Royale Games

Sports Simulation Games

Fighting Games

Others

By Streaming Type

Live Streaming

On-Demand Streaming

Hybrid Streaming

By Device Type

Smartphones

PC

Console

Others

By End User

Advertisers & Sponsors

Game Publishers

Streaming Platforms

Tournament Organizers

Teams & Players

Viewers/Fans

Conclusion

The U.S. Esports Market is moving from a niche gaming category into a wider digital sports and entertainment economy. Growth is being supported by a large gaming population, rising digital video advertising, live streaming, sponsorship demand, and organized competition across professional and college levels.

The strongest opportunities are expected for companies that can combine audience engagement, reliable tournament formats, brand-safe sponsorship models, strong content production, and interactive fan experiences. As gaming continues to shape digital entertainment, esports is expected to become a more important commercial channel in the U.S. media and sports landscape.

People Also Ask

What is the U.S. esports market?

The U.S. esports market includes competitive video gaming, tournaments, teams, live streaming, sponsorships, advertising, ticketing, merchandise, and digital fan engagement. It is supported by the country’s large gaming population and strong digital entertainment spending.

Which segment leads the esports market by revenue source?

Advertising and sponsorships lead the revenue source segment with 45.3% share. Growth is supported by brand partnerships, tournament visibility, creator-led campaigns, and high engagement among gaming audiences.

Why are PC gaming platforms important in esports?

PC gaming platforms are important because many professional esports titles require high performance, fast response time, advanced controls, and reliable tournament infrastructure. This is why PC platforms held 43.6% share.

Why are MOBA games popular in esports?

MOBA games are popular because they offer team-based strategy, strong fan loyalty, regular tournament formats, and high replay value. The segment accounted for around 30.7% share.

Why is live streaming important for esports?

Live streaming is important because esports audiences prefer real-time match viewing, live chat, creator commentary, and interactive fan participation. Live streaming captured more than 42.3% share.

Why are smartphones growing in esports?

Smartphones are growing because they make esports more accessible. Players can join competitive gaming without expensive hardware, which supports mobile tournaments, casual esports, and wider audience growth.

Who are the main buyers in the esports market?

Advertisers and sponsors are major buyers, accounting for 41.3% share. They use esports for brand visibility, targeted marketing, tournament partnerships, influencer campaigns, and digital audience engagement.