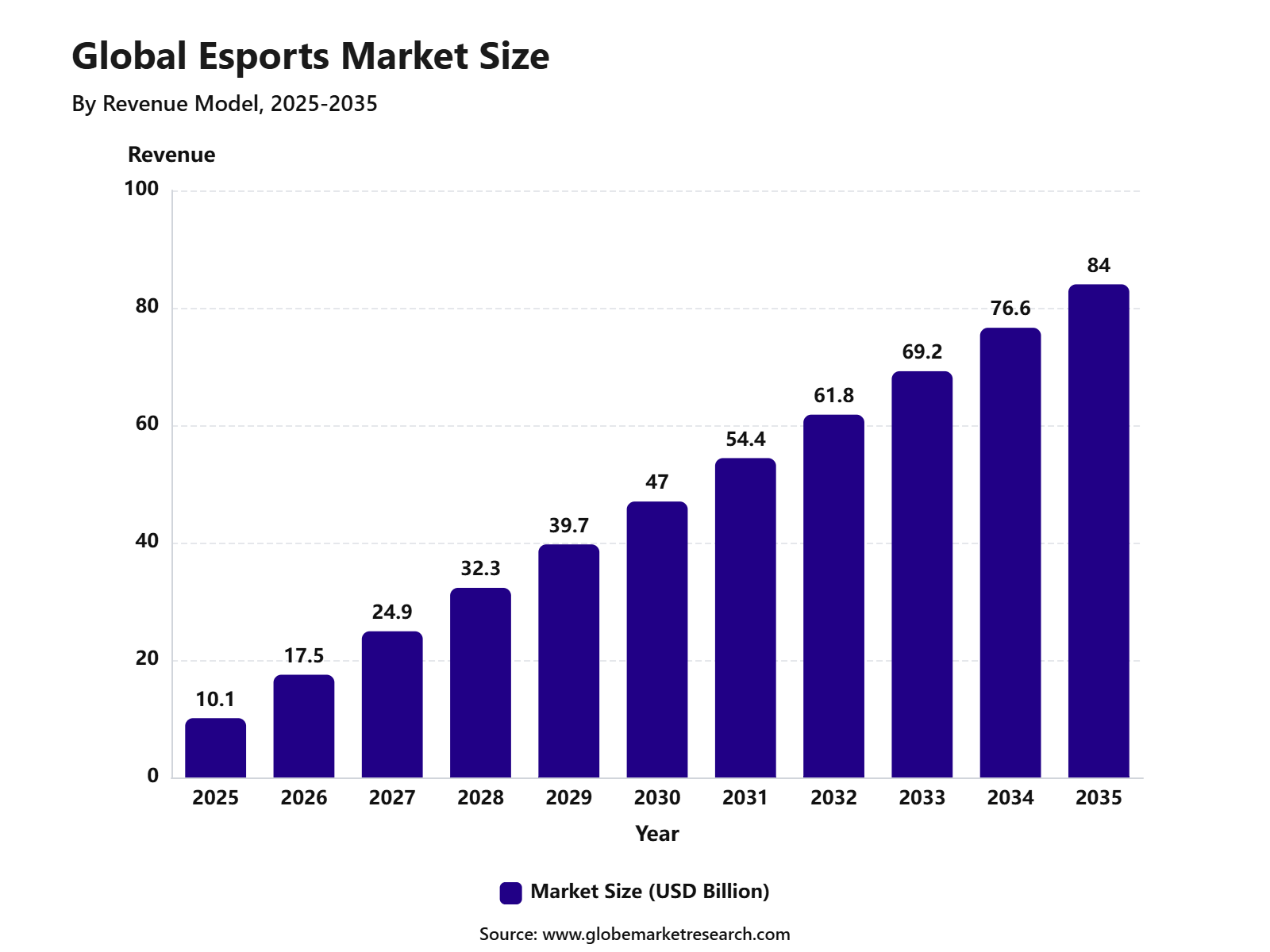

According to Globe Market Research, The Global Esports Market was valued at USD 10.1 billion in 2025 and is projected to reach USD 84.0 billion by 2035, growing at a CAGR of 23.6% during the forecast period. North America led the market with a 45.2% share in 2025, supported by strong gaming culture, high digital media consumption, large esports audiences, brand sponsorship activity, and the presence of major game publishers, tournament organizers, streaming platforms, and professional teams.

The U.S. Esports Market was valued at USD 3.2 billion in 2025 and is expected to grow at a CAGR of 24.8%, driven by rising esports viewership, growing sponsorship revenue, collegiate esports programs, and wider adoption of competitive gaming content across streaming and social media platforms. Esports refers to organized competitive video gaming where professional players, teams, and leagues compete across game titles such as multiplayer online battle arena games, first-person shooters, sports simulation games, strategy games, and battle royale formats.

The growth of the market can be attributed to rising online gaming participation, increasing live-streaming audiences, growing brand investments, and stronger monetization through sponsorships, media rights, ticketing, merchandise, and in-game engagement. The market outlook remains strong as esports continues to expand across professional leagues, college tournaments, mobile gaming, influencer-led content, and digital fan communities. Demand is expected to rise for esports platforms, event management solutions, team analytics, gaming hardware, live production tools, and fan engagement technologies.

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 10.1 Bn |

Forecast Revenue (2035) | USD 84.0 Bn |

CAGR (2025-2035) | 23.6% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Top Market Takeaways

Sponsorship remained the leading revenue model in the esports market, accounting for 43.6% share. This position was supported by rising brand partnerships, team sponsorship agreements, tournament naming rights, and the strong media visibility offered by competitive gaming events.

PC-based esports held the largest platform share at 49.3%. Its leadership was driven by high-performance gaming systems, established professional tournament formats, and strong adoption among competitive and professional players.

MOBA games led the market by game type with 35.4% share. Their strong performance was supported by large global fan communities, team-based gameplay, structured leagues, and frequent international tournaments.

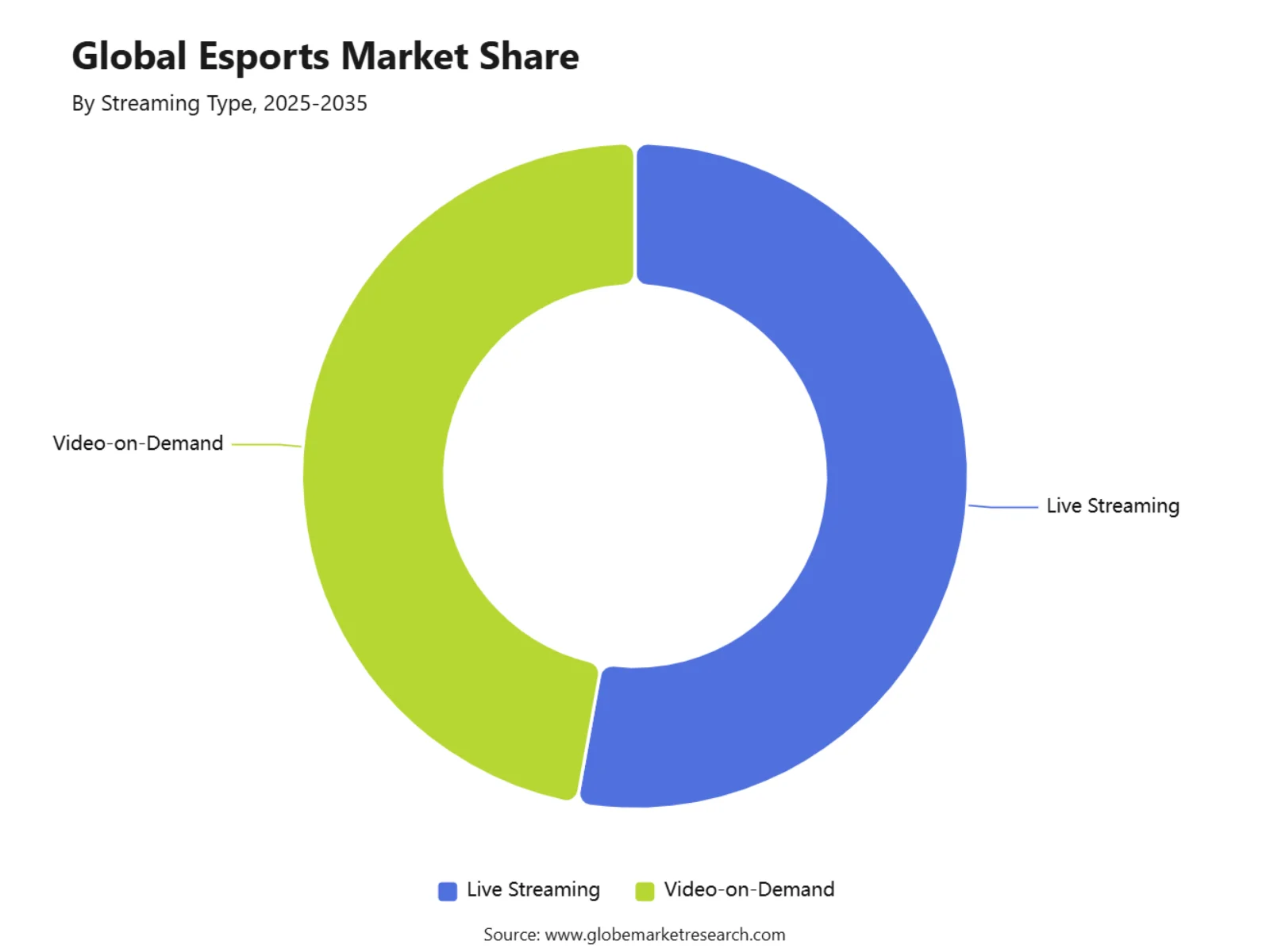

Live streaming accounted for 52.8% share, making it the dominant viewing format. Growth was supported by real-time fan engagement, influencer-led content, interactive chat features, and expanding esports broadcast audiences.

Casual viewers represented the largest audience group with 39.4% share. This segment expanded due to easy access to streaming platforms, mobile viewing, social media exposure, and the growing appeal of esports as mainstream digital entertainment.

Advertisers and sponsors held 42.3% share by end user. Their strong participation was driven by the need to reach young, digital-first audiences through gaming content, esports teams, tournament broadcasts, and creator-led campaigns.

North America led the esports market with 45.2% share. The region benefited from a large gaming population, strong PC and mobile gaming adoption, established tournament infrastructure, and high brand spending on esports partnerships.

The U.S. esports market was valued at USD 2.6 billion and is projected to grow at a 22.8% CAGR. Growth is being supported by rising esports viewership, expanding sponsorship activity, professional league development, and increased monetization through streaming and digital media.

Esports Market Share Statistics

By Revenue Model: Sponsorship led the esports market with a 43.6% share, supported by strong brand partnerships, team sponsorships, tournament naming rights, and digital media visibility. Brands are using esports sponsorships to reach young, digital-first audiences through teams, players, livestreams, and major gaming events.

By Platform: PC-based esports held the leading platform share of 49.3%, driven by high-performance gaming systems, professional tournament formats, and strong adoption among competitive players. PC remains important in esports because it supports advanced graphics, faster response times, and established competitive titles.

By Game Type: MOBA games led the esports market with a 35.4% share, supported by large fan communities, structured team-based competition, and frequent global tournaments. These games attract strong viewer engagement because they combine strategy, teamwork, player skill, and long-term league formats.

By Streaming Type: Live streaming accounted for 52.8% share, driven by real-time viewer engagement, creator-led content, and rising esports broadcast audiences. Platforms focused on live gaming content have made tournaments more accessible, allowing fans to follow matches, interact with streamers, and watch professional players in real time.

By Audience Type: Casual viewers represented the leading audience segment with a 39.4% share, supported by wider access to streaming platforms and growing interest in esports as entertainment. Many viewers follow esports through highlights, influencer streams, short-form clips, and major tournament finals rather than only through professional league schedules.

By End User: Advertisers and sponsors accounted for 42.3% share, driven by strong demand for youth-focused digital marketing and gaming audience reach. Esports offers brands a direct channel to engage audiences through sponsorship placements, branded tournaments, in-stream advertising, team partnerships, and creator collaborations.

By Region: North America led the esports market with a 45.2% share, supported by large gaming populations, strong tournament ecosystems, established esports organizations, and high brand spending on digital entertainment. The region benefits from advanced streaming infrastructure, professional leagues, college esports programs, and strong commercial partnerships.

U.S. Esports Market: The U.S. esports market was valued at USD 2.6 billion and is projected to grow at a 22.8% CAGR, supported by strong sponsorship activity, rising viewership, and wider adoption of competitive gaming across PC, console, and mobile platforms. Growth is also supported by esports arenas, collegiate competitions, gaming creators, and brand campaigns targeting young digital audiences.

Competitive Landscape Assessment

The Esports Market is a fast-growing digital entertainment market built around competitive video gaming, live streaming, professional teams, publisher-led leagues, global tournaments, sponsorships, media rights, ticketing, in-game items, merchandise, and creator-led fan engagement. The market is shaped by game publishers, tournament organizers, esports teams, streaming platforms, sponsors, hardware brands, telecom operators, and event production companies. Competitive strength is closely linked with audience reach, game popularity, tournament quality, team performance, sponsor value, and digital community engagement.

The competitive landscape is different from traditional sports because game publishers control the intellectual property behind each title. Publishers such as Riot Games, Valve, Tencent, Activision Blizzard, Electronic Arts, Epic Games, Ubisoft, Krafton, and Moonton play a central role in league structure, tournament rules, broadcast rights, game updates, and competitive ecosystems. This gives publishers strong control over the commercial direction of esports titles.

Implementation Complexity & Technology Readiness

Esports Area | Implementation Complexity | Technology Readiness | Market Position |

|---|---|---|---|

Publisher-led leagues | High | High | Strongest for controlled league operations. |

Third-party tournaments | Moderate to High | High | Widely used across major esports titles. |

Multi-title esports events | Very High | Moderate to High | Strong audience and sponsor appeal. |

Live streaming platforms | High | High | Core esports distribution layer. |

Esports team operations | High | High | Mature, but profitability depends on revenue mix. |

Mobile esports | Moderate | High | Strong adoption in mobile-first markets. |

Competitive Landscape by Revenue Stream

Revenue Stream | Competitive Intensity | Key Buying Factors | Competitive Position |

|---|---|---|---|

Sponsorship and brand partnerships | Very High | Audience fit, engagement quality, team reach, event scale, brand safety | Largest strategic revenue area. |

Media and streaming rights | High | Viewership, platform reach, exclusivity, content quality, regional audience | Strong for top-tier titles and events. |

Publisher revenue sharing | High | Team participation, fan purchases, digital items, league structure | Important for recurring team income. |

Prize pools | High | Tournament scale, title popularity, sponsor funding, event prestige | Supports player motivation and visibility. |

Ticketing and live events | Moderate to High | Venue experience, location, fan base, match importance, festival value | Strong in major live events. |

Key Market Segments

By Revenue Model

Sponsorship

Advertising

Media Rights

Merchandise & Tickets

Publisher Fees

Others

By Platform

PC-Based Esports

Mobile & Tablet Esports

Console-Based Esports

By Game Type

MOBA

FPS

Battle Royale

Sports Simulation

Real-Time Strategy

Fighting Games

Others

By Streaming Type

Live Streaming

Video-on-Demand

By Audience Type

Casual Viewers

Esports Enthusiasts

Professional Players

Amateur Players

By End User

Game Publishers

Tournament Organizers

Esports Teams

Streaming Platforms

Advertisers & Sponsors

Fans

By Region

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Recent Developments

January 2026, Riot Games confirmed that Worlds 2026 will run from October 15 to November 14, with stages across Los Angeles, Allen in Texas, and the Grand Final at Barclays Center in Brooklyn, New York. This supports event revenue, ticketing, sponsorship, broadcast inventory, and city-level esports tourism.

February 2026, RTS completed the acquisition of the Evolution Championship Series, known as Evo, one of the most established fighting game tournaments. The move strengthens Saudi-backed involvement in fighting game esports and gives Evo a larger international expansion platform. Financial terms were not disclosed.

March 2026, The Esports Foundation launched the 2026 Club Partner Program, a USD 20 million initiative. Each selected club can receive funding of up to USD 1 million, along with strategic support and international exposure. This is important because team economics remain one of the biggest challenges in esports, especially for organizations dependent on sponsorship and prize winnings.

People Also Ask

How big is the esports market?

The global esports market was valued at USD 10.1 billion in 2025 and is projected to reach USD 84.0 billion by 2035. The market is expected to grow at a CAGR of 23.6% during the forecast period. The U.S. market was valued at USD 3.2 billion in 2025 and is projected to reach USD 29.3 billion by 2035.

What is esports?

Esports means competitive video gaming played by individuals or teams in organized formats. It includes professional tournaments, leagues, online competitions, live events, and streaming broadcasts. Popular esports games include League of Legends, Counter-Strike, Valorant, Dota 2, Fortnite, PUBG Mobile, Mobile Legends, EA Sports FC, and Street Fighter.

Why is esports so popular?

Esports is popular because it combines gaming, competition, entertainment, community, and live streaming. Fans can watch professional players, learn strategies, follow teams, and interact with creators in real time. Its popularity is also supported by free-to-play games, mobile access, and global online platforms.

What is driving the esports market?

The esports market is driven by sponsorships, streaming platforms, mobile gaming, digital advertising, tournament prize pools, and publisher investment. Brands are using esports to reach young audiences who spend more time on gaming and online video platforms. Growth is also supported by regional leagues and international tournaments.

Which segment dominates the esports market?

Sponsorship dominates the market by revenue stream with a 43.6% share. PC leads by platform with a 49.3% share, while MOBA games lead by genre with a 35.4% share. Live events lead by format with a 47.2% share.

What are the top esports games?

Top esports games include League of Legends, Counter-Strike 2, Valorant, Dota 2, Fortnite, PUBG Mobile, Mobile Legends: Bang Bang, EA Sports FC, Rocket League, Apex Legends, Call of Duty, and Street Fighter. The top games vary by region because PC esports, console esports, and mobile esports have different audience strengths.