Strategic Market Snapshot

Key Parameter | Report Details |

|---|---|

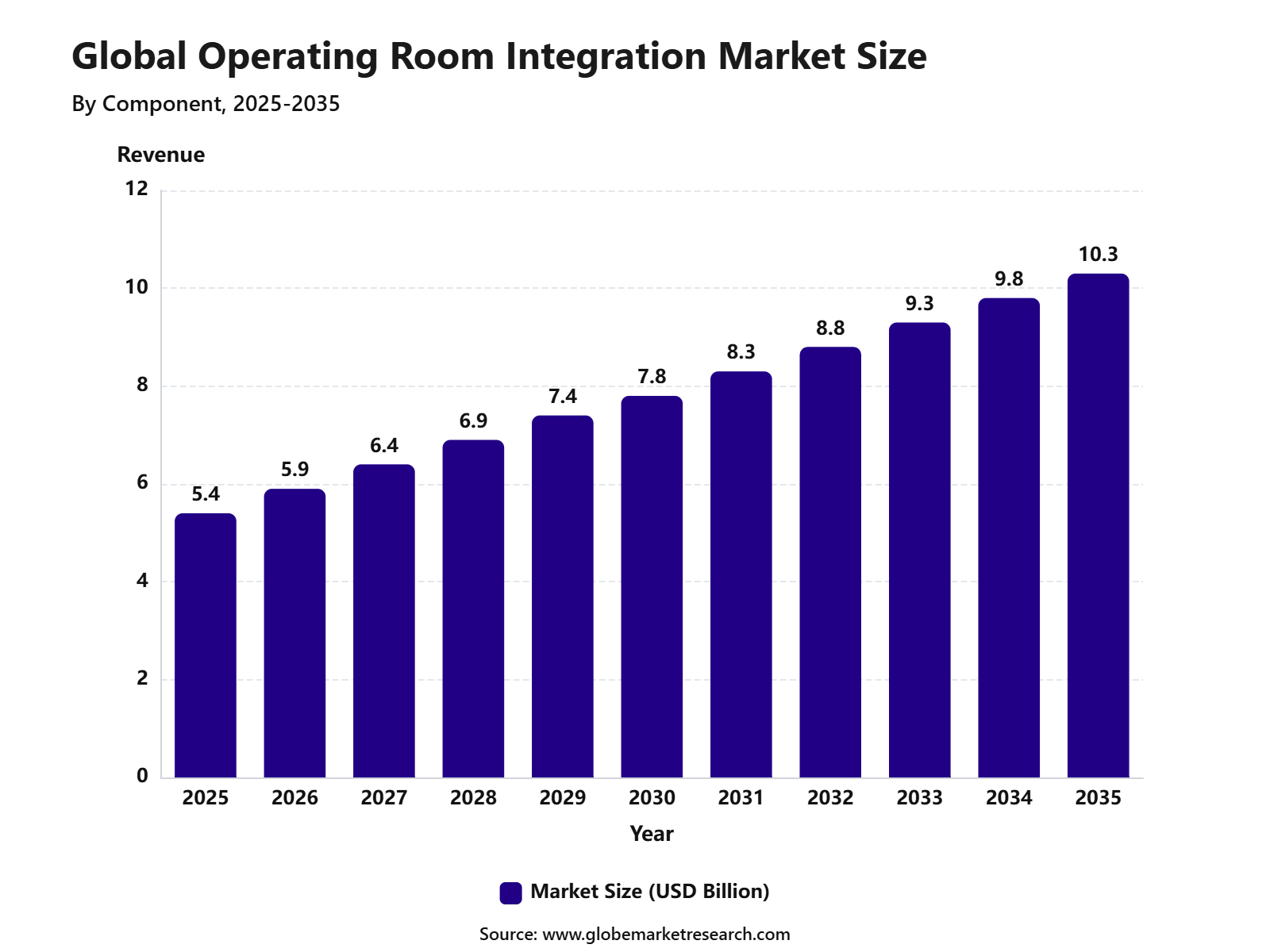

Market Revenue, 2025 | USD 5.4 Billion |

Projected Revenue, 2026 | USD 5.9 Billion |

Projected Revenue, 2035 | USD 10.3 Billion |

CAGR, 2025-2035 | 13.5% |

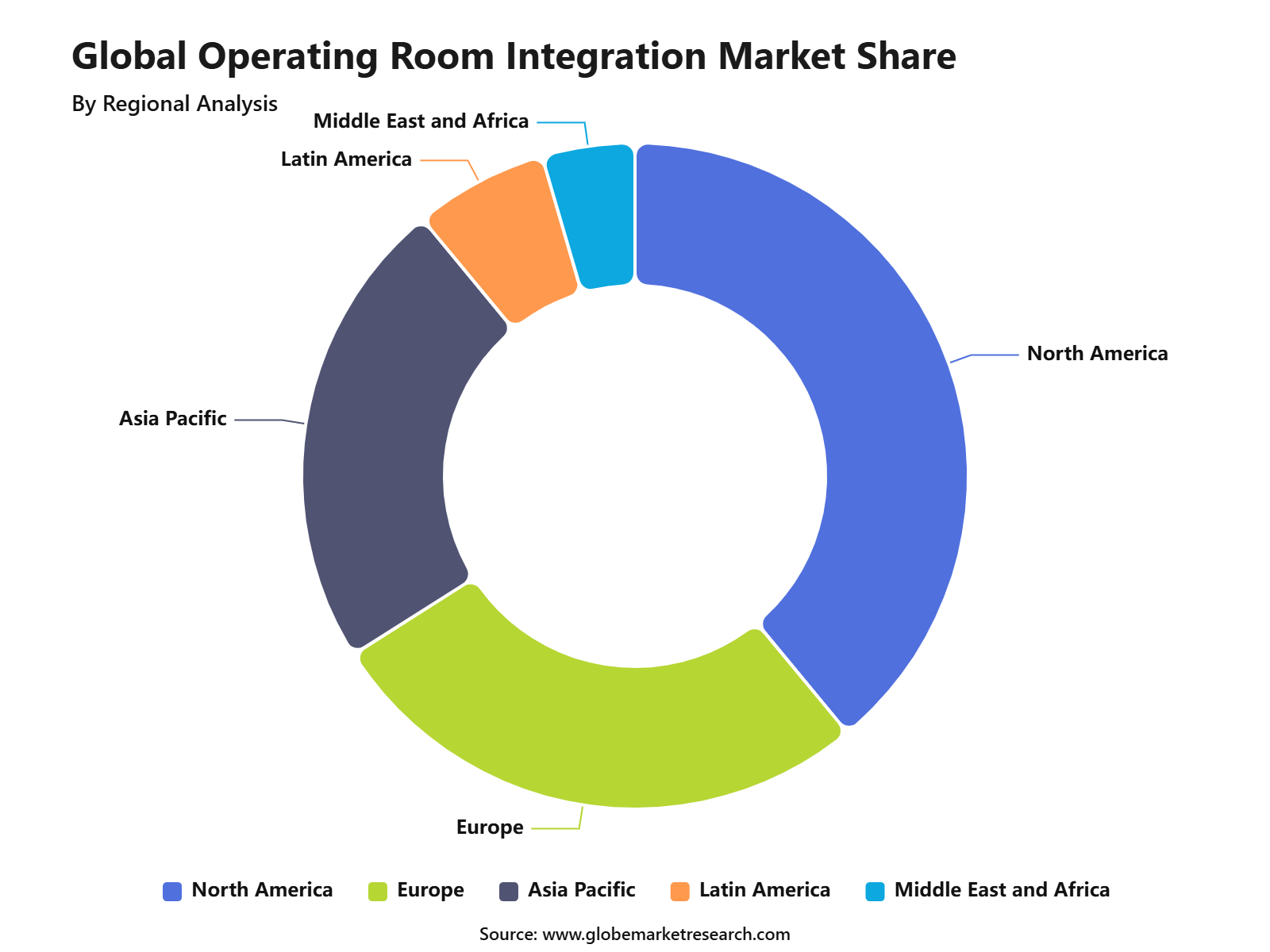

Largest Region | North America, 39.0% Share |

U.S. Market Revenue, 2025 | USD 3.4 Billion |

U.S. CAGR | 14.8% |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

Market Size and Growth Forecast

The global operating room integration market was valued at USD 5.4 billion in 2025 and is projected to reach USD 10.3 billion by 2035, growing at a 13.5% CAGR. The market is projected to reach USD 7.2 billion in 2026, while North America led with 39% share in 2025. Growth is being supported by digital operating rooms, connected surgical infrastructure, minimally invasive surgery, hybrid operating rooms, robotic surgery support, and real-time access to surgical data.

Operating room integration refers to connected systems that bring surgical devices, imaging platforms, displays, audio-video systems, documentation tools, lighting systems, cameras, and hospital networks into one coordinated surgical environment. These systems allow surgical teams to control and view critical information from a centralized platform, improving workflow, communication, documentation, and decision-making during procedures.

The U.S. market was valued at USD 3.4 billion in 2025 and is expected to expand at a 14.8% CAGR, supported by demand for hybrid operating rooms, robotic surgery support, real-time imaging integration, and connected surgical data platforms. In the U.S., there were 6,100 hospitals, 907,216 staffed beds, and 35.7 million hospital admissions, showing a large base of healthcare facilities that may require surgical infrastructure upgrades.

Why the Operating Room Integration Market Is Growing?

The growth of the operating room integration market can be attributed to rising surgical procedure volumes, growing demand for workflow efficiency, and wider adoption of minimally invasive procedures. Rising surgical procedure volume has an estimated positive impact of +2.7%, while the need for surgical workflow efficiency adds +2.4%. These factors are increasing demand for operating rooms that support better coordination, faster access to imaging, and smoother team communication.

Operating rooms are among the most expensive hospital areas. Published surgical cost data show that one minute of operating room time costs around USD 36 to USD 37, meaning delays, turnover inefficiency, and manual coordination can create measurable financial pressure. Integrated OR systems help hospitals reduce manual steps, improve visibility, support faster documentation, and improve room utilization.

Minimally invasive surgery and robotic-assisted procedures are also supporting market demand. Intuitive Surgical reported that about 3.15 million da Vinci procedures were performed in 2025, up 18% from 2024, and the company expected worldwide da Vinci procedures to grow 13% to 15% in 2026. This supports stronger demand for video routing, imaging integration, device connectivity, and robotic surgery-ready operating rooms.

Software Leads the Component Segment

Software led the component segment with 55.6% share in 2025. The segment is supported by demand for centralized control platforms, surgical workflow management, real-time data access, imaging integration, audio-video routing, and surgical documentation systems. Hospitals are using software to connect multiple operating room devices and reduce fragmented workflows. The value of software is strongest when it improves operating room visibility. Surgical teams need quick access to live video, endoscopic feeds, radiology images, patient records, procedure notes, and equipment status.

Integration software helps bring these functions into one coordinated interface. Software adoption is also linked with hospital digitization. Integrated OR platforms can connect with electronic health records, PACS, anesthesia systems, surgical cameras, documentation systems, and hospital IT infrastructure. This helps hospitals reduce manual documentation errors and improve post-surgery reporting.

Documentation Management Systems Lead by Device Type

Documentation management systems accounted for 36.7% share by device type in 2025. Adoption is being driven by the need to record surgical data, reduce manual documentation errors, improve compliance, and support faster post-surgery reporting. These systems help hospitals capture procedure notes, timestamps, images, videos, and surgical details in a structured format.

Documentation is becoming more important because hospitals need reliable surgical records for quality review, reimbursement, medico-legal protection, training, and audit readiness. Integrated documentation systems reduce the burden on clinical staff and help make surgical records easier to retrieve and review. Surgical safety also strengthens the need for better documentation.

CDC guidance notes that surgical site infections are among the most costly healthcare-associated infections, with an estimated annual cost of USD 3.3 billion, an added hospital stay of 9.7 days, and more than USD 20,000 in additional hospitalization cost per admission. Better documentation, communication, and workflow visibility can support safer perioperative processes.

General Surgery Holds the Largest Application Share

General surgery held the largest application share at 41% in 2025. The segment leads because general surgical procedures are performed in high volumes across hospitals and surgical centers. These procedures often need coordinated access to imaging, patient records, video systems, surgical equipment, and clinical communication tools. Operating room integration is useful in laparoscopic, abdominal, gastrointestinal, emergency, and routine surgical procedures.

Integrated displays and video routing can help surgeons and support teams view the same information at the right time, reducing delays caused by equipment switching or scattered data access. The general surgery segment is also supported by robotic and minimally invasive procedures. As more procedures shift toward image-guided and video-assisted methods, hospitals need operating rooms that can handle multiple data sources, high-definition video, and device connectivity.

Hospitals Remain the Leading End User

Hospitals dominated the market with 65.4% share in 2025. Their leadership is supported by higher surgical volumes, larger digital infrastructure budgets, advanced imaging systems, and the need to improve operating room efficiency and patient safety. Large hospitals and multi-specialty facilities are investing in integrated ORs to improve productivity, coordination, and room utilization.

Hospitals remain the natural buyers for operating room integration because they manage complex procedures and multiple surgical specialties. Operating room directors, surgeons, biomedical engineering teams, IT departments, and hospital administrators all influence the buying decision. The large U.S. hospital base further supports the market opportunity. The American Hospital Association reported 5,121 community hospitals, 1,797 rural community hospitals, and 3,324 urban community hospitals in its 2026 hospital statistics. This creates a wide addressable base for OR upgrades, especially where hospitals are modernizing surgical suites and digital infrastructure.

On-Premise Deployment Leads Due to Data Control

On-premise deployment held 59.6% share in 2025. Hospitals continue to prefer on-premise systems because operating room data is sensitive and must be protected under strict privacy, safety, and compliance requirements. These systems support direct control over hardware, software updates, device connectivity, and internal hospital networks. Operating rooms require high uptime. During surgery, teams need uninterrupted access to images, videos, patient records, room controls, and device feeds.

On-premise systems can offer stronger local reliability, which is important in critical surgical environments. Cloud and hybrid deployment will continue to grow as hospitals adopt analytics, remote collaboration, surgical video storage, and multi-site performance review. However, cybersecurity and patient data protection will remain central to deployment decisions. FDA guidance on medical device cybersecurity also reinforces the need to include cybersecurity considerations in connected medical device and software submissions.

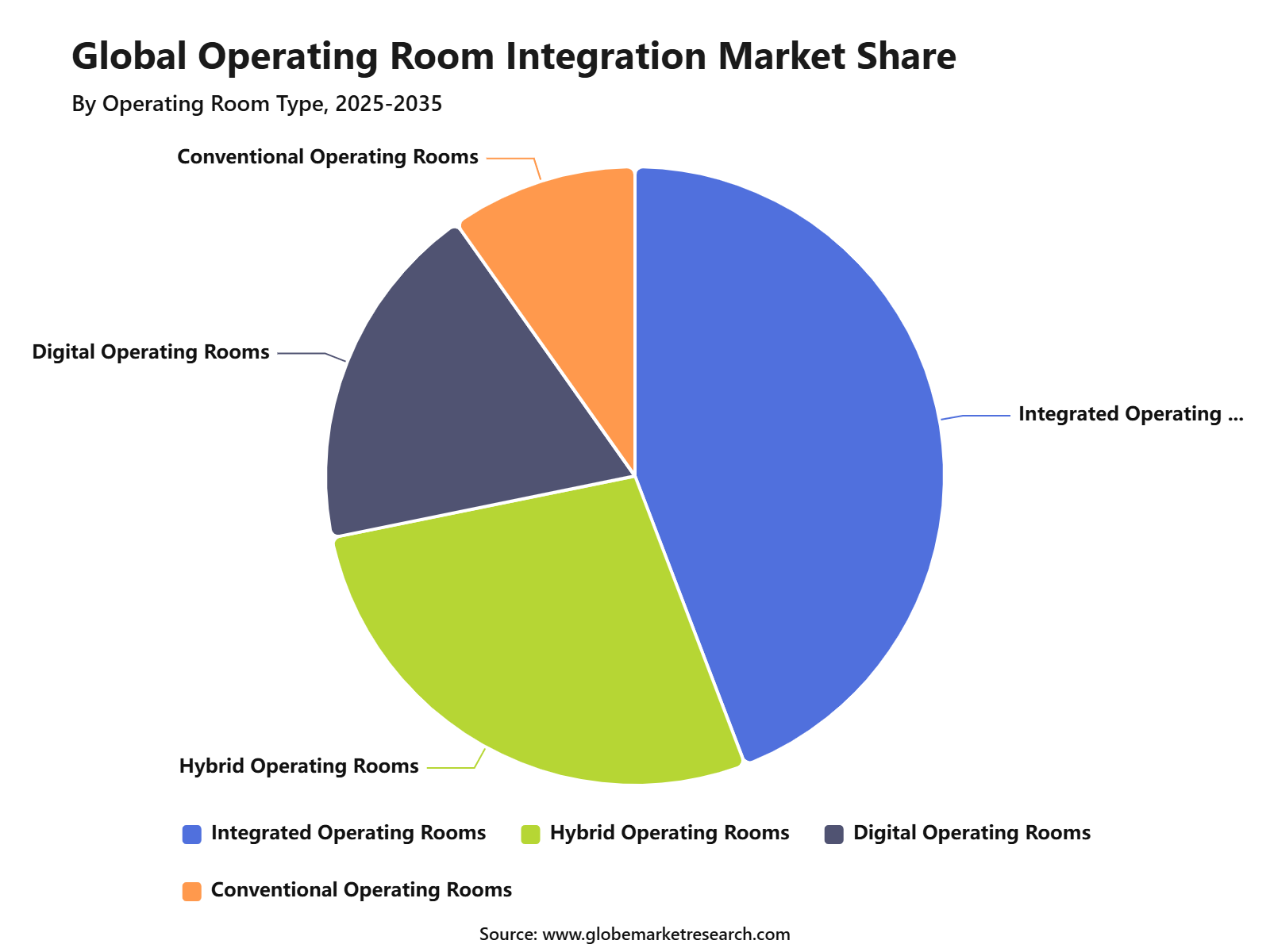

Integrated Operating Rooms Lead by Operating Room Type

Integrated operating rooms accounted for 44.2% share in 2025. Growth is being supported by the need to connect surgical devices, imaging systems, displays, lighting, cameras, documentation tools, and communication systems into one coordinated structure. These rooms are designed to reduce clutter, improve visibility, and support centralized control. Integrated operating rooms are especially useful for minimally invasive surgery, image-guided surgery, robotic-assisted procedures, and multi-specialty workflows.

They help surgical teams work with several sources of clinical and visual information without unnecessary movement or manual switching. Hybrid operating rooms are also gaining demand in cardiac, vascular, neuro, and trauma centers. The growth of hybrid operating rooms has an estimated positive impact of +2.0%, as hospitals invest in integrated imaging, surgical displays, device control, and multidisciplinary procedure support.

Image and Video Integration Leads by Technology

Image and video integration led the technology segment with 36.7% share in 2025. Demand is increasing because surgeons need high-quality visualization, multi-source video routing, procedure recording, and fast access to diagnostic images during surgery. This technology helps teams display live surgical video, endoscopic images, radiology scans, patient data, and procedural content on centralized screens. Modern surgical procedures depend heavily on visualization. High-definition displays, 4K imaging, endoscopy feeds, robotic surgery systems, surgical cameras, and diagnostic images must work together without disrupting workflow.

Integration helps improve situational awareness and team communication. AI-enabled surgical video analysis is also emerging. A 2026 surgical AI paper notes that minimally invasive procedures and endoscopic video create an opportunity to observe, measure, and improve intraoperative quality through AI-supported recognition of anatomy, instruments, workflow, actions, adverse events, and critical moments.

North America Leads the Market

North America held the largest regional share at 39% in 2025. The region leads due to advanced hospital infrastructure, high adoption of digital surgery platforms, strong healthcare spending, and wider use of minimally invasive and robotic-assisted procedures. The U.S. is the key regional growth engine. Demand is being supported by hospital modernization, surgical workflow automation, robotic surgery support, hybrid OR demand, and connected imaging systems.

The presence of large health systems and advanced surgical centers supports faster adoption of integrated OR platforms. Europe is expected to grow through hospital digitization, surgical training demand, and robotic surgery adoption, while Asia Pacific is gaining momentum through new hospitals, private healthcare investment, and surgical infrastructure upgrades. Hospital modernization in emerging economies has an estimated positive impact of +1.8%, especially in India, China, Southeast Asia, the Middle East, and Latin America.

Revenue Potential and Financial Impact

Revenue potential is strongest across software platforms, documentation systems, image and video integration, hybrid OR upgrades, robotic surgery integration, AI-enabled workflow tools, and cloud-based surgical data management. Software held 55.6% share, while image and video integration held 36.7% share, showing where hospitals are prioritizing investment. The financial impact is linked with operating room efficiency. Since OR time has been estimated at around USD 36 to USD 37 per minute, even small improvements in turnover time, case coordination, and documentation workflow can create meaningful savings for hospitals.

The market is also supported by hospital spending on surgical instruments, computing infrastructure, and diagnostic imaging equipment. Globe Market Research notes that hospitals spent more than USD 10 billion on surgical and medical instruments in 2024, nearly USD 4.5 billion on computing infrastructure and data processing, and about USD 1.4 billion on diagnostic imaging equipment. This shows that OR integration fits naturally into wider hospital modernization spending.

Risk Factors and Market Barriers

High installation and infrastructure cost is the largest restraint, with an estimated negative impact of -2.0%. Hospitals must invest in displays, control systems, video routers, cameras, software, cabling, networking, documentation tools, cybersecurity layers, and device interfaces. This can delay adoption in smaller hospitals and budget-constrained facilities.

Complex integration with legacy hospital systems carries an estimated negative impact of -1.7%. Many hospitals still use older imaging systems, fragmented documentation tools, separate medical devices, and isolated OR equipment. Integration becomes harder when systems must connect with EHR, PACS, anesthesia systems, endoscopy platforms, and hospital IT networks.

Cybersecurity remains a major concern. Connected operating rooms increase the number of networked devices, endpoints, and clinical data flows. Verizon’s 2026 DBIR found that 31% of breaches now start with software vulnerabilities, showing why hospitals must treat connected OR systems as both clinical infrastructure and cybersecurity infrastructure.

Analyst Perspective

What the Data Is Telling Operating Room Integration Companies?

From an analyst perspective, the data shows that operating room integration is moving from a technology upgrade to a surgical efficiency and safety priority. A market value of USD 5.4 billion in 2025 and projected value of USD 10.3 billion by 2035 indicate steady demand, but growth will favor vendors that can prove workflow improvement, secure integration, and measurable hospital value.

The strongest signal is the leadership of software, documentation management systems, general surgery, hospitals, on-premise deployment, integrated operating rooms, and image and video integration. Software held 55.6% share, hospitals captured 65.4% share, on-premise deployment held 59.6% share, and image and video integration led with 36.7% share. This shows that hospitals are prioritizing secure, centralized, and practical operating room control.

What Opportunities Are Emerging?

The biggest opportunity is in integrated OR platforms that connect surgical imaging, documentation, device control, audio-video routing, and workflow software. Hospitals want fewer disconnected systems and stronger visibility during procedures.

AI-enabled surgical decision support and surgical video analytics are also emerging. These tools can help hospitals review procedure quality, identify workflow gaps, support training, and improve surgical performance over time.

Hybrid operating rooms, robotic surgery integration, and remote surgical education are also strong opportunities. These areas require high-quality imaging, stable connectivity, advanced displays, procedure recording, and reliable system uptime.

What Risks Should Companies Be Aware of?

The main risk is high upfront cost. Operating room integration requires hardware, software, installation, training, cybersecurity, and ongoing support, which can delay adoption in smaller hospitals and emerging markets.

Interoperability is another major risk. Hospitals often use devices and systems from different vendors, and weak compatibility can slow implementation. Interoperability between multiple device brands has an estimated negative impact of -1.8%.

Cybersecurity and uptime risks must also be managed carefully. Operating rooms cannot tolerate system failures during procedures, and connected OR platforms must protect patient data, surgical video, device access, and hospital networks.

What Decisions Should Clients Make Next?

Clients should first decide which OR workflows need integration most urgently. Imaging access, video routing, documentation, robotic surgery support, hybrid OR capability, and surgical workflow control should be prioritized based on case volume and clinical need.

Second, hospitals should assess current infrastructure before purchase. EHR connectivity, PACS integration, medical device compatibility, network strength, cybersecurity readiness, and biomedical engineering support must be reviewed before implementation.

Finally, clients should select vendors based on interoperability, uptime support, cybersecurity controls, clinical usability, training quality, and measurable return on investment. The best systems should reduce operational friction without adding complexity for surgical teams.

Recent Developments

In April 2026, Getinge AB highlighted integrated operating room systems that bring devices, data, and workflows into one connected structure, reducing manual coordination and supporting more efficient surgical teams.

In August 2025, Stryker advanced its operating room integration platform with a focus on connecting surgical imaging, room cameras, displays, and compatible surgical devices through a simplified interface for better workflow control.

In April 2026, ALVO Medical continued to promote intelligent operating room integration, with focus on modular OR design, integrated displays, telemedicine support, and surgical robotics readiness.

In February 2026, Richard Wolf GmbH promoted smart networking solutions for operating rooms, supporting communication between surgical systems and clinical teams through its RIWOlink approach.

In June 2026, Ditec Medical advanced its ORisTIC digital operating room roadmap, focusing on intelligent operating rooms, AI, virtual reality, international expansion, and stronger digital surgical theatre capabilities.

Competitive Landscape

The operating room integration market is competitive, with companies focusing on integrated surgical platforms, medical imaging connectivity, audio-video routing, documentation systems, surgical displays, hybrid OR infrastructure, and digital surgical workflow tools. Key companies include:

Stryker

Getinge AB

Brainlab AG

Barco

Drägerwerk AG & Co. KGaA

Steris Plc.

KARL STORZ SE & CO. KG

Olympus

Caresyntax

Arthrex, Inc.

ALVO Medical

Skytron, LLC

Merivaara

Richard Wolf GmbH

Ditec Medical

Competition is expected to increase as hospitals demand more connected, secure, and workflow-focused surgical environments. Companies with strong interoperability, cybersecurity, clinical training, and end-to-end integration capability are likely to gain stronger hospital trust. The strongest providers will be those that can connect clinical needs with technical reliability. In this market, hospitals will not buy integration only for technology appeal. They will buy systems that improve surgical coordination, reduce delays, protect data, and support safer operating room workflows.

Conclusion

The operating room integration market is entering a stronger digital growth phase as hospitals invest in connected surgical suites, image and video integration, documentation systems, hybrid operating rooms, robotic surgery support, and AI-enabled surgical workflows. Growth is being supported by rising surgical complexity, high OR costs, hospital modernization, and the need for better clinical coordination.

Future growth will be led by software platforms, documentation management systems, image and video integration, integrated operating rooms, hybrid ORs, AI-enabled surgical decision support, and secure on-premise or hybrid deployment models. The market outlook remains positive, but adoption will depend on cost control, interoperability, cybersecurity, training, and measurable return on investment.