Market Size and Growth Forecast

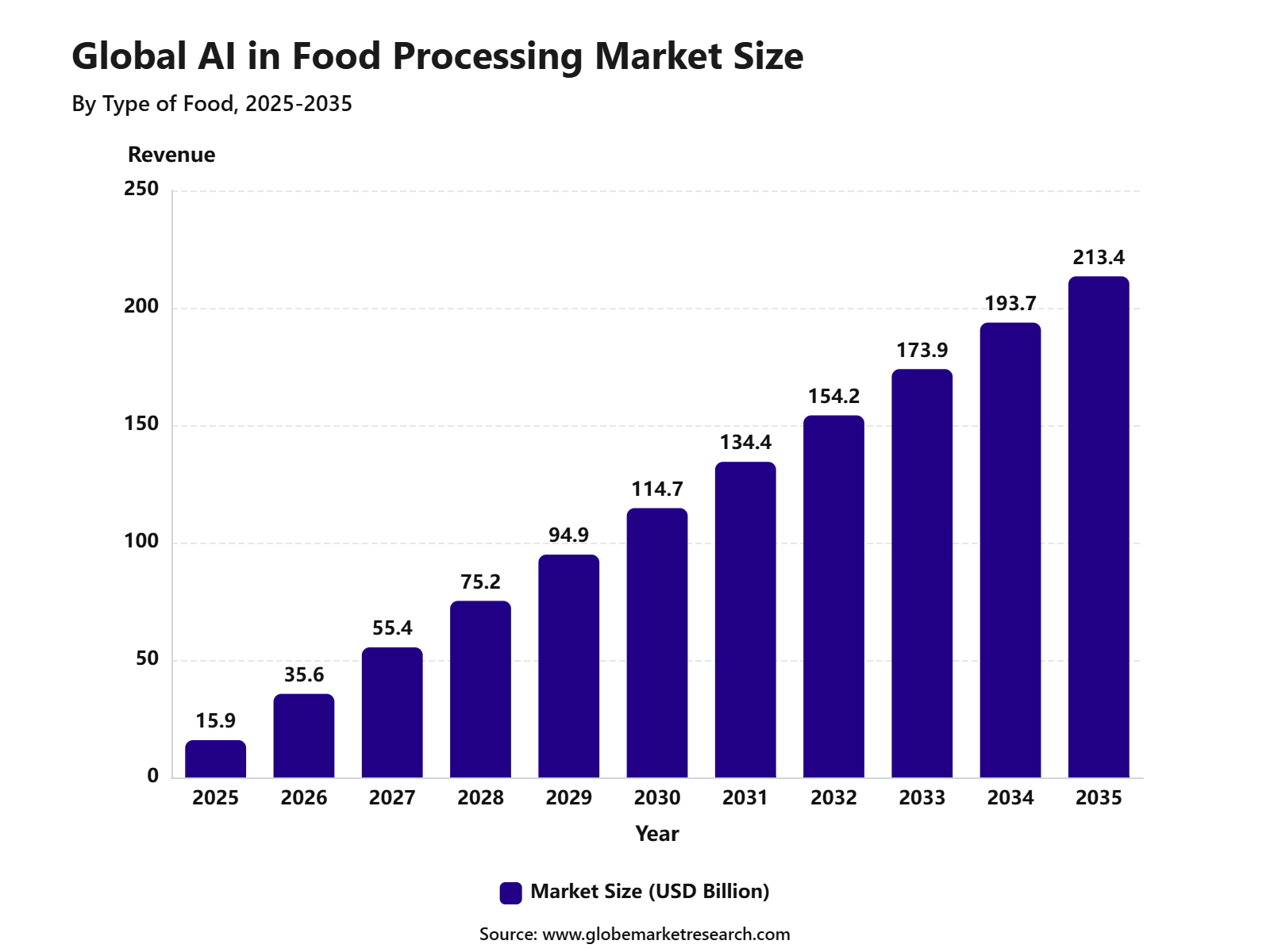

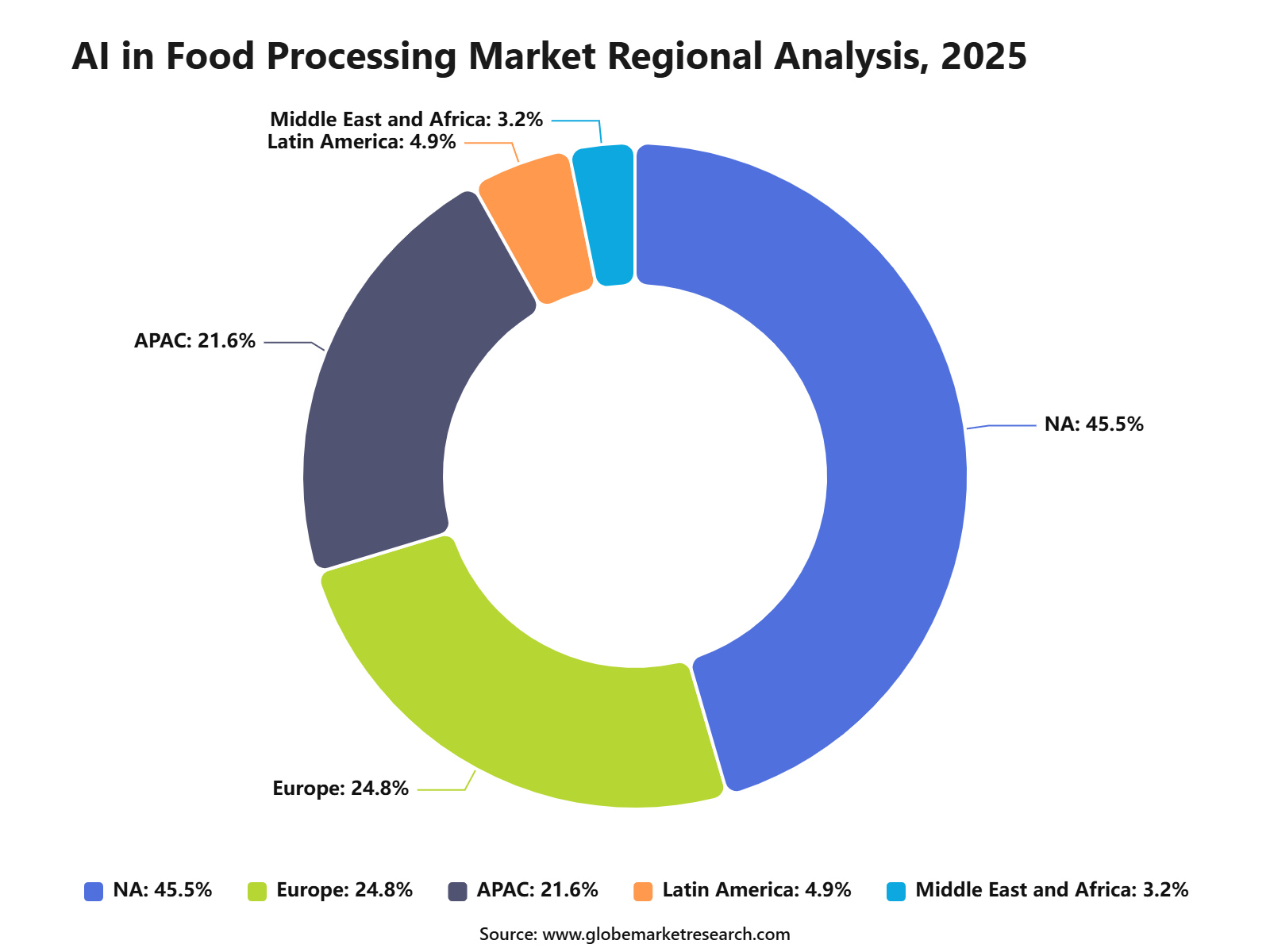

Based on data from Globe Market Research, the global AI in food processing market was valued at USD 15.9 billion in 2025 and is projected to reach USD 213.4 billion by 2035, growing at a 29.6% CAGR. North America held the largest regional share at 45.5% in 2025, supported by advanced food manufacturing systems, higher automation adoption, strong AI investment, and stricter food safety requirements.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 15.9 Billion |

Projected Revenue, 2035 | USD 213.4 Billion |

CAGR, 2025-2035 | 29.6% |

Largest Region | North America, 45.5% Share |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

AI in food processing includes the use of machine learning, computer vision, robotics, predictive analytics, smart sensors, and automation software across food production facilities. These systems are used for quality inspection, sorting, grading, contamination detection, predictive maintenance, recipe optimization, demand planning, packaging checks, and traceability.

The market is closely linked with smart factories, digital supply chains, automated packaging, food safety monitoring, and real-time production analytics. Growth is being supported by labor cost pressure, stricter quality standards, rising need to reduce food waste, and the shift from manual inspection to AI-enabled production decisions.

Why the AI in Food Processing Market Is Growing?

The growth of the AI in food processing market can be attributed to the rising need for faster inspection, consistent food quality, lower downtime, and stronger safety compliance. Food processors are adopting AI where measurable savings can be shown, such as fewer defects, reduced labeling errors, better batch consistency, and faster contamination detection.

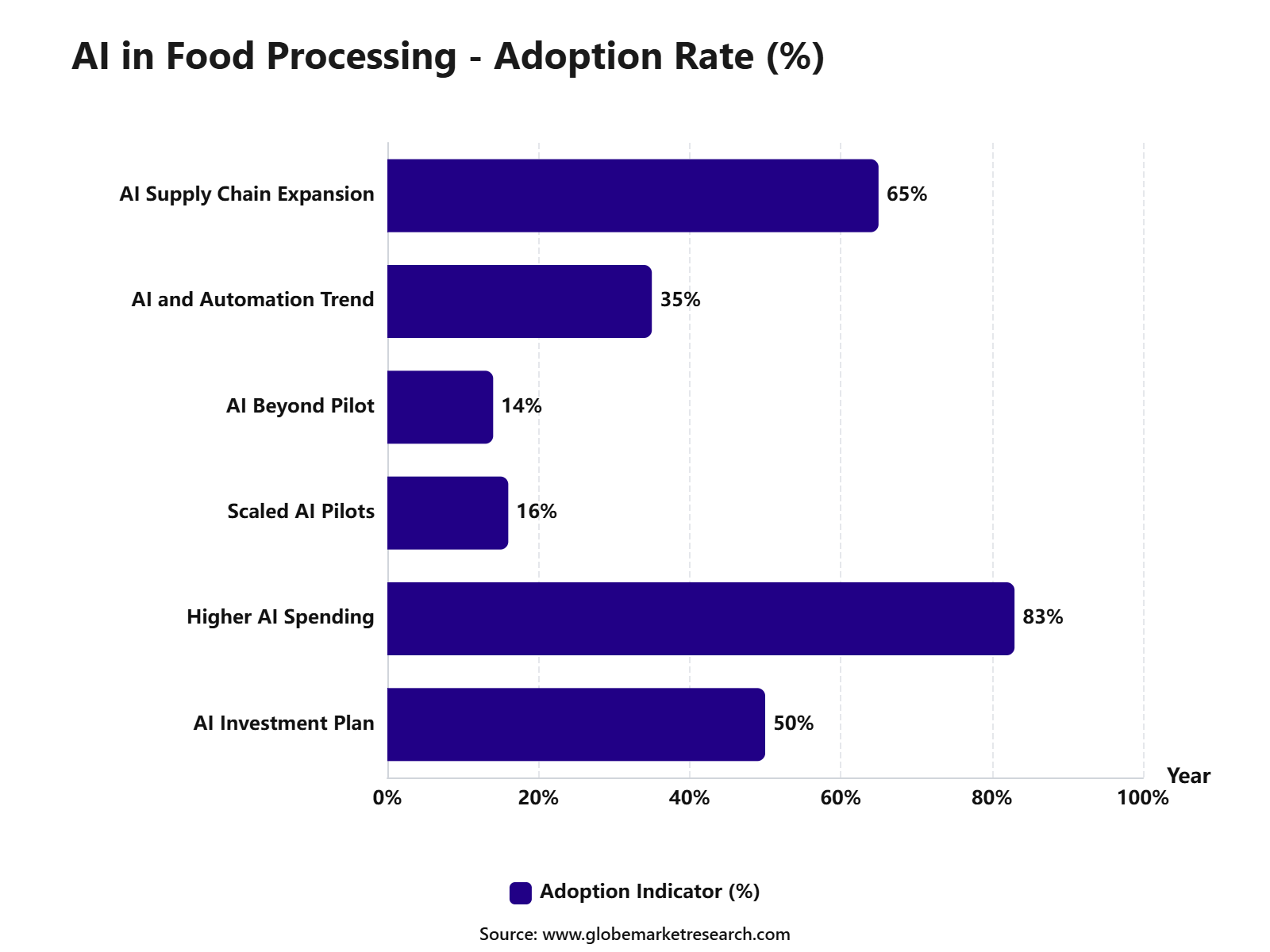

A 2025 food technology survey found that 50% of industry professionals planned to invest in AI, while 48% planned to invest in supply-chain tracking systems. This shows that AI adoption is moving from experimentation toward plant-level deployment in quality control, processing, traceability, and compliance. Automation pressure is also increasing. The International Federation of Robotics reported that U.S. industrial robot installations rose 11% year over year to 38,000 units in 2025, with strong growth coming from the food industry and other non-manufacturing sectors.

Food safety remains a strong driver. The CDC updated its food safety statistics in 2025, estimating that 48 million people in the U.S. get sick from foodborne illness each year, with 128,000 hospitalizations and 3,000 deaths. This public health burden supports stronger use of AI for inspection, monitoring, risk detection, and recall readiness.

Convenience Food and Snacks Lead by Food Type

Convenience food and snacks led the type of food segment with 33.5% share in 2025. This leadership is supported by high production volume, changing eating habits, demand for ready-to-eat foods, and the need for consistent quality across fast-moving packaged products.

AI is being used in this segment to improve recipe consistency, shelf-life prediction, automated sorting, packaging inspection, portion control, and demand forecasting. These tools are important because convenience food and snacks usually move through high-speed production lines where small quality issues can become large-scale losses.

The 2026 snacking environment also supports this segment. The latest State of Snacking report shows that snacking behavior is shaped by health, indulgence, convenience, social connection, and novelty. This creates demand for AI tools that can help manufacturers balance clean-label formulations, packaging efficiency, consistent taste, and rapid product innovation.

For food companies, this segment offers strong commercial value because snacks and convenience foods need frequent innovation, stable quality, and efficient production. AI can support faster reformulation, ingredient optimization, real-time line inspection, and better alignment between production planning and consumer demand.

Quality Control and Safety Compliance Remain the Leading Application

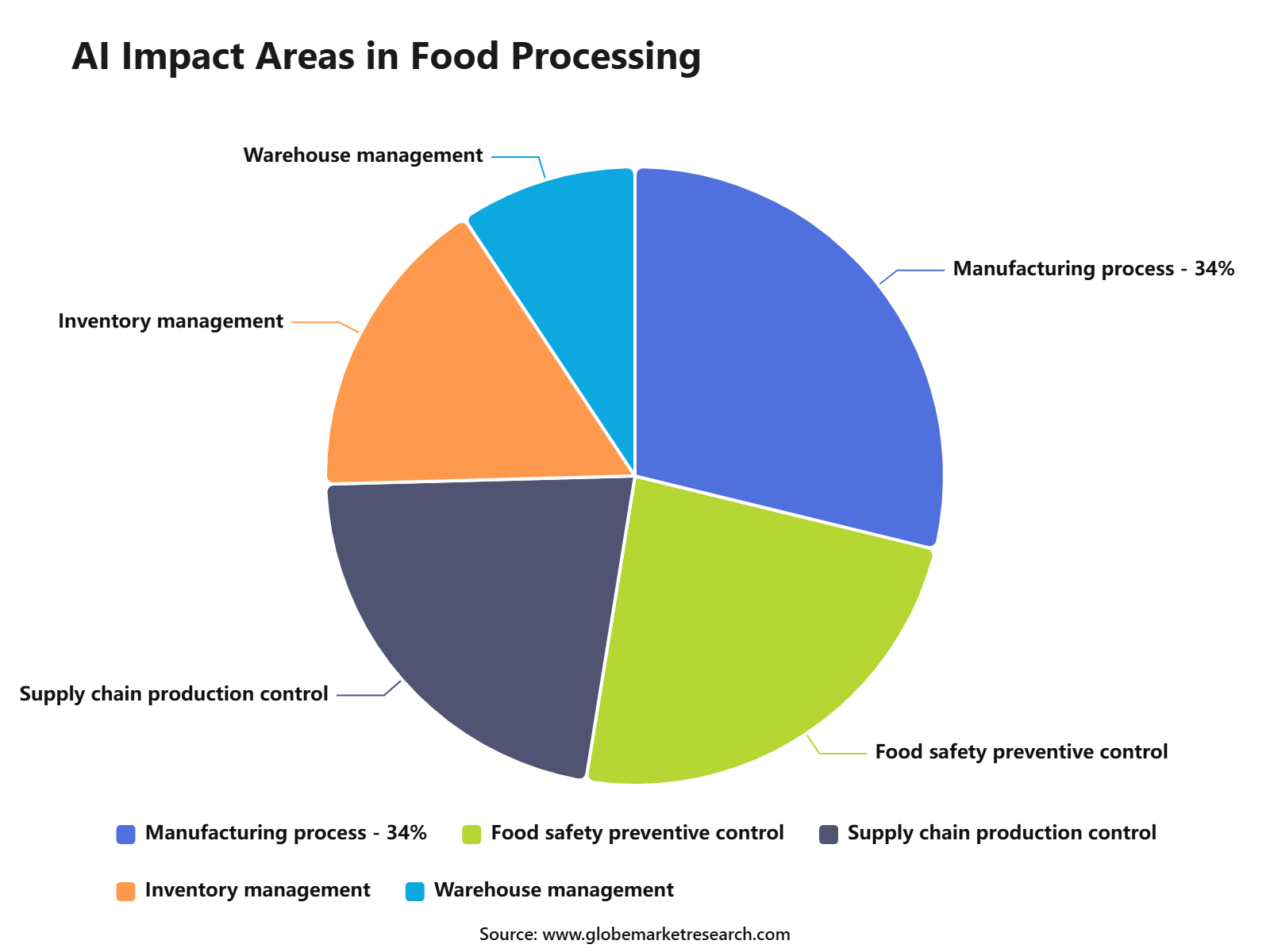

Quality control and safety compliance accounted for 35.9% share in 2025, making it the leading application segment. AI-based vision inspection, sensor analytics, and predictive quality systems are being used to detect product defects, color variation, shape changes, packaging errors, foreign materials, and contamination risks. This application is gaining importance because manual inspection can be slow, inconsistent, and difficult to scale in high-volume production.

AI systems can inspect products continuously and identify irregularities faster than traditional methods. This is especially useful in meat, poultry, bakery, dairy, snacks, beverages, grains, and frozen foods. Regulatory traceability is also increasing the need for digital compliance systems. The FDA Food Traceability Rule requires firms that manufacture, process, pack, or hold foods on the Food Traceability List to maintain Key Data Elements for Critical Tracking Events. This supports the use of AI and digital tools for batch tracking, anomaly detection, supplier risk analysis, and faster recall response.

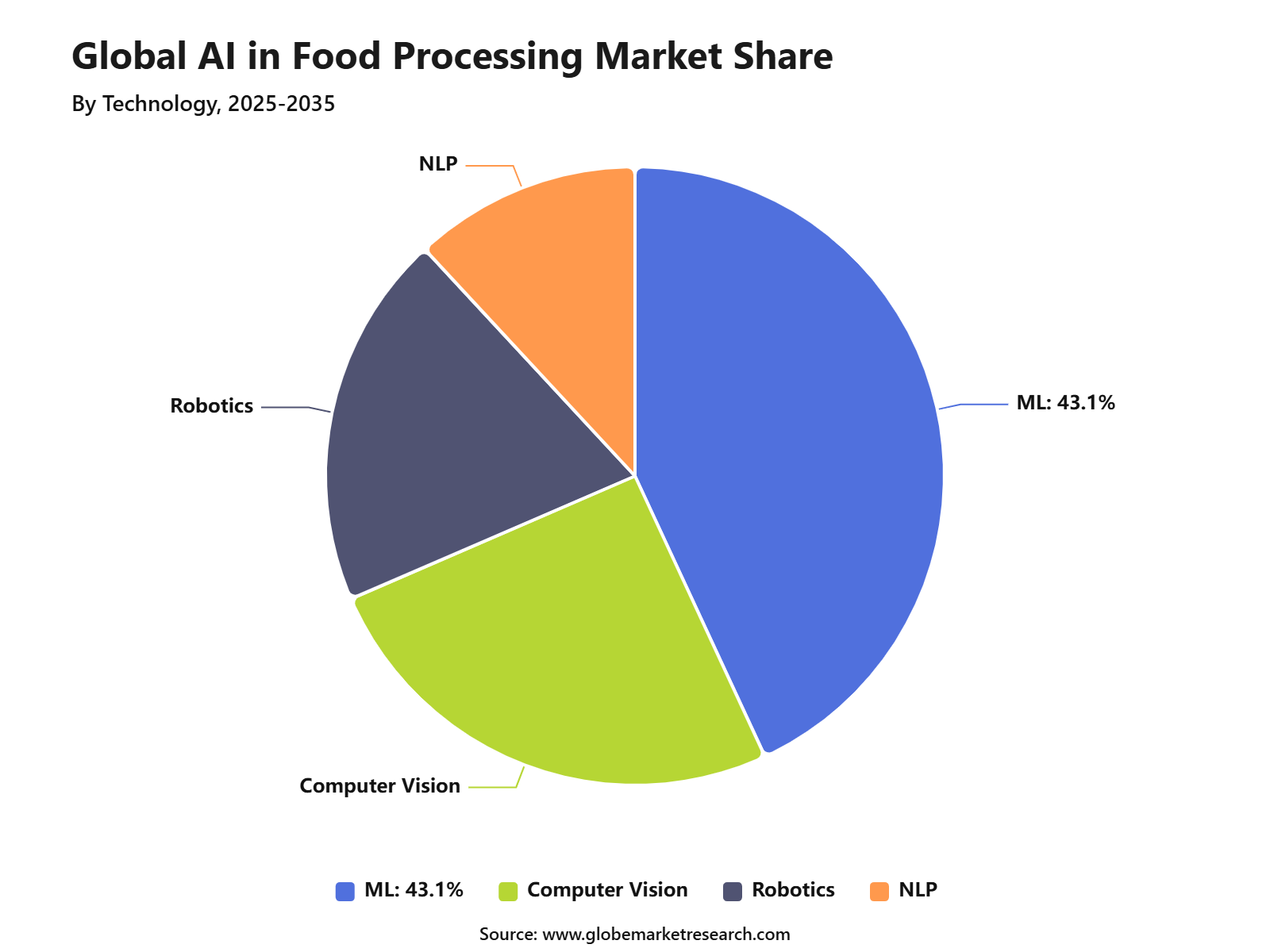

ML and Deep Learning Lead by Technology

Machine learning and deep learning held 43.1% share by technology in 2025. Their leadership is supported by strong use in defect detection, sorting, quality grading, predictive maintenance, process control, demand forecasting, and recipe optimization. These technologies are valuable because food processing creates large volumes of image, sensor, temperature, moisture, ingredient, and equipment data. Machine learning systems can identify patterns that are difficult for manual teams to track, especially in fast-moving and variable production environments.

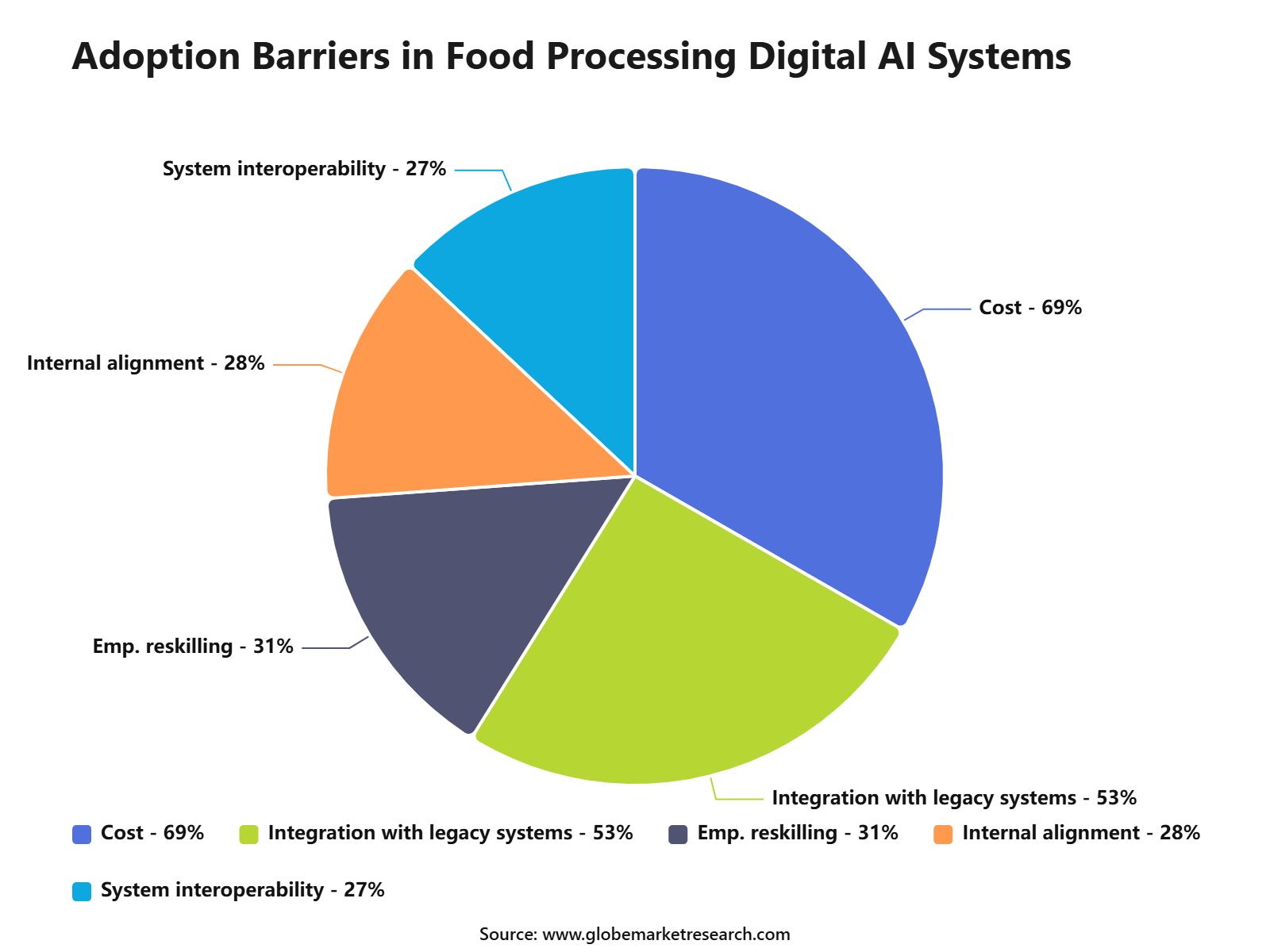

A 2025 review of AI in food manufacturing highlighted that adoption remains uneven because of heterogeneous datasets, limited system interoperability, and skill gaps between data scientists and food experts. It also identified supply chain, formulation and processing, consumer insights, nutrition and health, and workforce education as key areas for AI use in food manufacturing. Deep learning and computer vision are especially useful where product appearance matters. They can help detect size, shape, bruising, discoloration, foreign objects, seal defects, and labeling errors. These capabilities are becoming more important as manufacturers aim to improve yield, safety, and production consistency.

Software Holds the Largest Component Share

Software captured 50.5% share by component in 2025, supported by the growing use of AI platforms for monitoring, analytics, production planning, quality management, traceability, and predictive maintenance. Software works as the intelligence layer that connects machines, sensors, cameras, cloud systems, dashboards, and production teams. Food-specific AI software is becoming important because processors need systems that understand batch production, recipes, allergens, shelf life, sanitation, supplier records, packaging checks, and quality documentation.

General AI tools may not be enough unless they can be adapted to food safety and plant-level workflows. The wider AI environment also supports this segment. Stanford’s 2026 AI Index reported that U.S. private AI investment reached USD 285.9 billion in 2025, while the U.S. had 1,953 newly funded AI companies. This strong AI ecosystem supports faster development of computer vision, predictive analytics, automation software, and industrial AI tools. Software providers are expected to gain traction when they offer measurable outcomes. Food manufacturers are more likely to adopt tools that reduce inspection time, lower waste, improve equipment uptime, support compliance, and connect easily with existing plant systems.

Cloud Deployment Is Gaining Strong Adoption

Cloud deployment accounted for 59.9% share in 2025, supported by scalable computing, remote access, centralized data storage, and easier integration across multiple food processing facilities. Cloud platforms allow companies to manage AI models, quality records, production analytics, and supplier data without depending only on local systems. Cloud-based AI is useful for multi-site food manufacturers.

A company can compare production performance across plants, monitor quality trends, standardize workflows, and manage compliance data from one connected platform. This is important for large processors with distributed manufacturing networks. Flexera’s 2026 State of the Cloud report found that generative AI became the third most widely used public cloud service, reaching 58% usage, while wasted cloud spend rose to 29% due to growing complexity from AI and new cloud services.

This shows that cloud AI adoption is rising, but cost governance is becoming more important. For food processors, cloud adoption should be balanced with cybersecurity, data governance, production uptime, and cost control. Hybrid models may be preferred where real-time inspection must happen at the edge, while cloud systems can be used for analytics, dashboards, model training, and reporting.

Food Manufacturers Are the Leading End Users

Food manufacturers held 63.8% share by end user in 2025. This leadership is driven by direct needs for automation, quality consistency, production efficiency, waste reduction, food safety, and regulatory compliance. AI is most valuable at the manufacturing stage because it can be applied directly to processing lines, packaging systems, inspection points, and plant-level planning.

The user base is large and operationally complex. USDA ERS reported that food and beverage processing establishments employed 1.7 million workers and represented a major share of U.S. manufacturing employment. BLS also reported in 2026 that food and beverage manufacturing is projected to add the most jobs among manufacturing industries over 2024 to 2034, reaching more than 2.2 million workers by 2034.

AI can support these manufacturers by helping workers monitor lines, detect process deviations, reduce manual quality checks, forecast demand, and manage maintenance. It should be viewed as a productivity support tool rather than only a labor replacement tool. Adoption will be strongest where AI solves clear production problems. These include visual inspection, allergen control, foreign object detection, temperature monitoring, recipe optimization, equipment failure prediction, shelf-life forecasting, and automated documentation.

North America Leads the AI in Food Processing Market

North America led the regional segment with 45.5% share in 2025. The region benefits from advanced food manufacturing infrastructure, strong AI investment, mature cloud adoption, and strict food safety standards. The U.S. remains a major driver because of its strong technology ecosystem, large food manufacturing base, and active regulatory focus on food safety and traceability. AI tools are being adopted across inspection, sorting, packaging, forecasting, quality control, and supply-chain monitoring.

Food safety regulation adds to regional demand. The FDA traceability framework supports faster identification of product movement across the supply chain, while CDC foodborne illness statistics show the continued need for stronger prevention and faster response systems. Asia Pacific is also expected to grow strongly as food manufacturers modernize plants, expand packaged food capacity, and adopt automation. India, China, Japan, South Korea, and Southeast Asia are likely to remain important markets due to rising food demand, labor pressure, and increasing investment in digital manufacturing.

Key Opportunities

The strongest opportunity is in food safety, quality control, and traceability. AI can help detect contamination risks, identify foreign materials, monitor hygiene conditions, and flag abnormal production data before products reach consumers. This directly supports food safety and brand protection.

Predictive maintenance is another major opportunity. Food plants operate under strict production schedules, and equipment failure can cause downtime, spoilage, and delayed deliveries. AI can analyze vibration, temperature, motor behavior, and production data to predict failure before breakdowns occur.

Waste reduction is also a high-value opportunity. AI can improve demand forecasting, inventory rotation, shelf-life prediction, and production planning. This is especially important for ultra-fresh foods, bakery products, meat, dairy, prepared meals, and fruits and vegetables.

Robotics and adaptive automation are becoming more attractive because food products vary in size, shape, texture, and placement. AI-enabled robots can support meal assembly, packing, sorting, and handling where fixed automation is less effective.

Analyst Perspective

What the Data Is Telling AI in Food Processing Companies?

From an analyst perspective, the data shows that AI in food processing is moving from experimental technology to a practical plant-level efficiency tool. A market value of USD 15.9 billion in 2025 and a projected value of USD 213.4 billion by 2035 indicate strong long-term demand, but adoption will favor solutions that can prove measurable savings and operational reliability.

The strongest signal is that quality control, software, cloud deployment, and food manufacturers are leading demand. Quality control and safety compliance held 35.9% share, software captured 50.5% share, cloud deployment accounted for 59.9% share, and food manufacturers held 63.8% share. This shows that companies are prioritizing AI where it directly improves safety, inspection, compliance, and production performance.

What Opportunities Are Emerging?

The biggest opportunity is in AI-enabled quality inspection and food safety monitoring. Foodborne illness, allergens, contamination risk, and labeling errors continue to create operational and reputational pressure for food companies.

Waste reduction is another strong opportunity. AI can help processors forecast demand, optimize production, reduce surplus, and improve redistribution decisions. This is important in fresh, chilled, bakery, dairy, meat, and prepared food categories.

Robotics, predictive maintenance, and traceability platforms are also emerging as strong growth areas. These solutions help companies improve uptime, reduce manual work, support compliance, and create better plant-level visibility.

What Risks Should Companies Be Aware Of?

The main risk is poor data readiness. If plant data is incomplete, inconsistent, or disconnected, AI systems may not produce reliable results. This can weaken confidence and delay wider deployment.

Integration cost is another major risk. Many food factories have legacy equipment and fragmented software systems, which can make AI projects more expensive and slower than expected. Smaller processors may find upfront investment harder to justify.

Trust and safety are also important barriers. AI tools used in food production must be explainable, tested, and monitored because wrong decisions can affect product safety, quality, compliance, and brand reputation.

What Decisions Should Clients Make Next?

Clients should first identify the highest-value use case. Quality inspection, allergen control, foreign object detection, predictive maintenance, traceability, and waste reduction are better starting points than broad AI transformation projects.

Second, companies should assess data readiness before large-scale deployment. They should review sensors, cameras, machine connectivity, batch records, ERP integration, quality documentation, and workforce skills.

Finally, clients should select AI providers based on food-sector experience, integration capability, explainability, measurable ROI, and support for regulatory workflows. The best solutions should improve production decisions without removing human oversight where safety is critical.

Latest Recent Developments

Market News

In April 2026, Findability Sciences launched LactaAI, an industrial intelligence platform built for dairy and whey processing plants. The platform supports real-time process intelligence across milk reception, evaporation, drying, packaging, and utilities, helping processors improve yield, energy use, and faster plant-level decision-making.

In April 2026, Chef Robotics announced that its AI-enabled food production robots had completed 100 million servings in customer production facilities. This update is important for the AI in food processing market because real-world food handling data is becoming a key advantage for robotic meal assembly, ingredient handling, and high-volume prepared food production.

In 2026, Sesotec showcased AI-based inspection systems and software for food safety at Interpack 2026. The company highlighted intelligent inspection systems for foreign body management, process safety, and efficiency across the food production chain.

Funding

In June 2026, Protein Industries Canada funded a project to build an AI platform for more efficient fermentation using agricultural byproducts. The project received C$607,000 toward a C$1.4 million initiative, showing public-sector support for AI-led food processing and ingredient innovation.

In March 2025, Chef Robotics raised USD 43.1 million in combined equity and debt financing to scale AI-enabled robotic deployments for food manufacturing. The round supported automated meal assembly, ingredient handling, and flexible robotics for high-volume food production lines.

In February 2025, MOA Foodtech secured EUR 14.8 million in European Innovation Council support for AI-powered biomass fermentation. The funding includes grant and equity commitment support to convert agri-food byproducts into high-value functional ingredients.

Mergers and Acquisitions

In January 2025, JBT completed the settlement of its voluntary takeover of Marel and began operating as JBT Marel Corporation. The combination created a larger food and beverage processing technology platform with stronger exposure to automation, software, and advanced processing systems.

In December 2025, Fortifi completed the acquisition of Provisur Technologies. The acquisition expanded Fortifi’s food processing automation, robotics, and software capabilities, especially across protein processing applications.

In May 2025, Insort, Qcify, and TriVision joined forces under the eivis group to advance intelligent food processing solutions. The consolidation brings together chemical imaging, AI-powered quality control, and vision-based inspection for food sorting, packaging inspection, and process optimization.

Competitive Landscape

The AI in food processing market includes automation companies, industrial software providers, robotics firms, sorting equipment specialists, machine vision providers, and food processing technology companies. Key players include ABB Ltd., Rockwell Automation, Siemens AG, Honeywell International Inc., KUKA AG, Key Technology Inc., TOMRA Systems ASA, Marel, Bühler Group, GREEFA, JBT Corporation, GEA Group AG, Sesotec GmbH, and Raytec Vision SpA.

Competition is expected to increase as food manufacturers invest in machine vision, predictive analytics, robotic handling, cloud platforms, and traceability systems. Larger providers may benefit from established equipment relationships, while specialist firms may win in focused use cases such as sorting, grading, allergen detection, and shelf-life prediction.

The strongest companies will be those that combine food processing knowledge with reliable AI performance. Buyers will look for proven inspection accuracy, easy integration, plant-level support, strong cybersecurity, and clear financial impact. Market success will depend on more than technology capability. Vendors must understand sanitation, batch control, food safety rules, packaging workflows, ingredient variability, and production line constraints. This will separate practical AI providers from generic AI software vendors.

Conclusion

The AI in food processing market is entering a high-growth phase as manufacturers focus on quality control, food safety, waste reduction, automation, traceability, and production efficiency. Growth is being supported by machine learning, computer vision, robotics, cloud deployment, and rising demand for smarter food manufacturing systems.

Future growth will be led by AI-enabled inspection, predictive maintenance, robotic sorting, food safety compliance tools, cloud-based production analytics, and demand forecasting systems. Food manufacturers that invest in data readiness, workforce training, and practical use cases will be better positioned to scale AI successfully.