Strategic Market Snapshot

Key Parameter | Report Details |

|---|---|

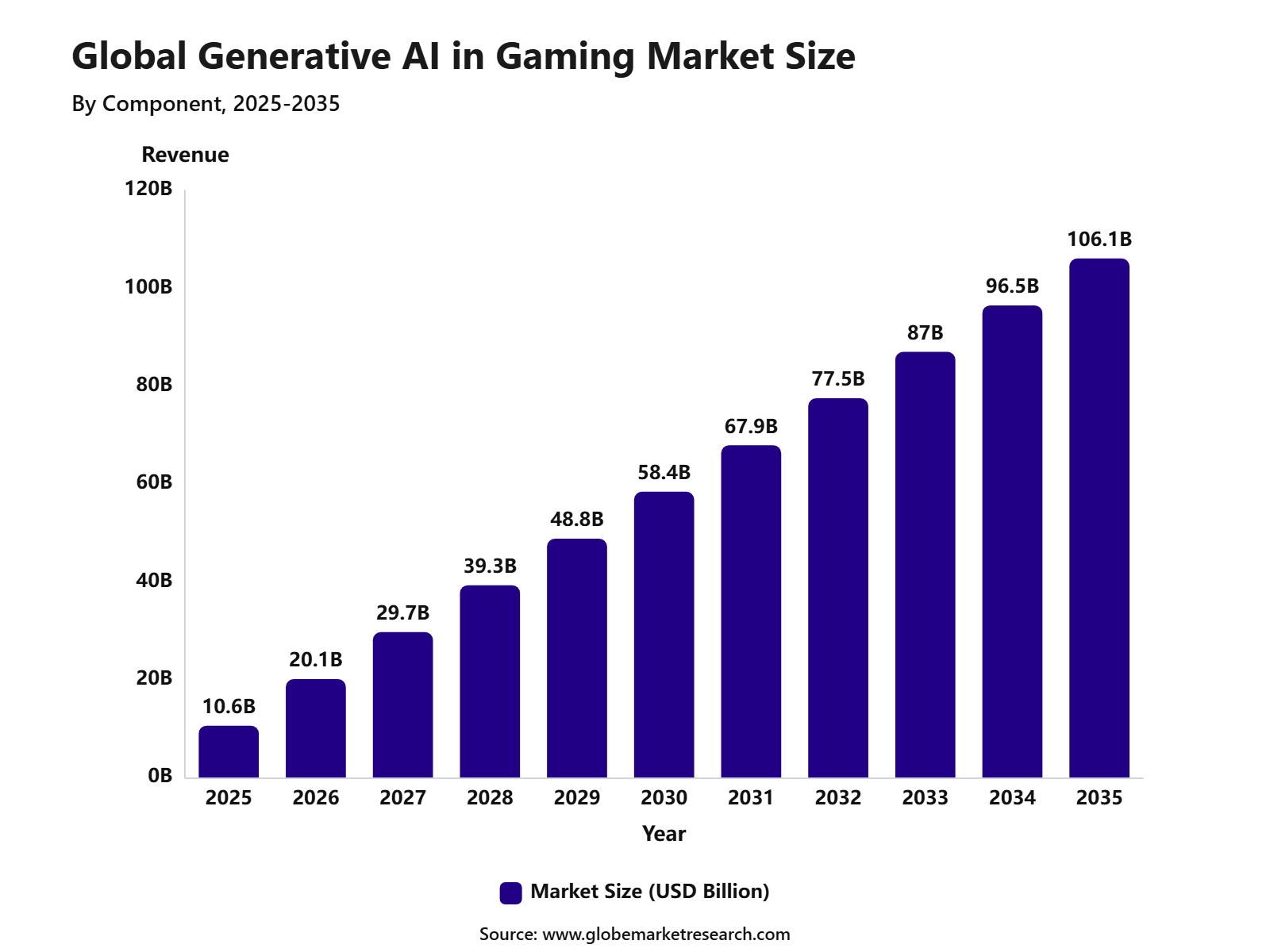

Market Revenue, 2025 | USD 10.6 Billion |

Projected Revenue, 2035 | USD 106.1 Billion |

CAGR, 2025-2035 | 25.9% |

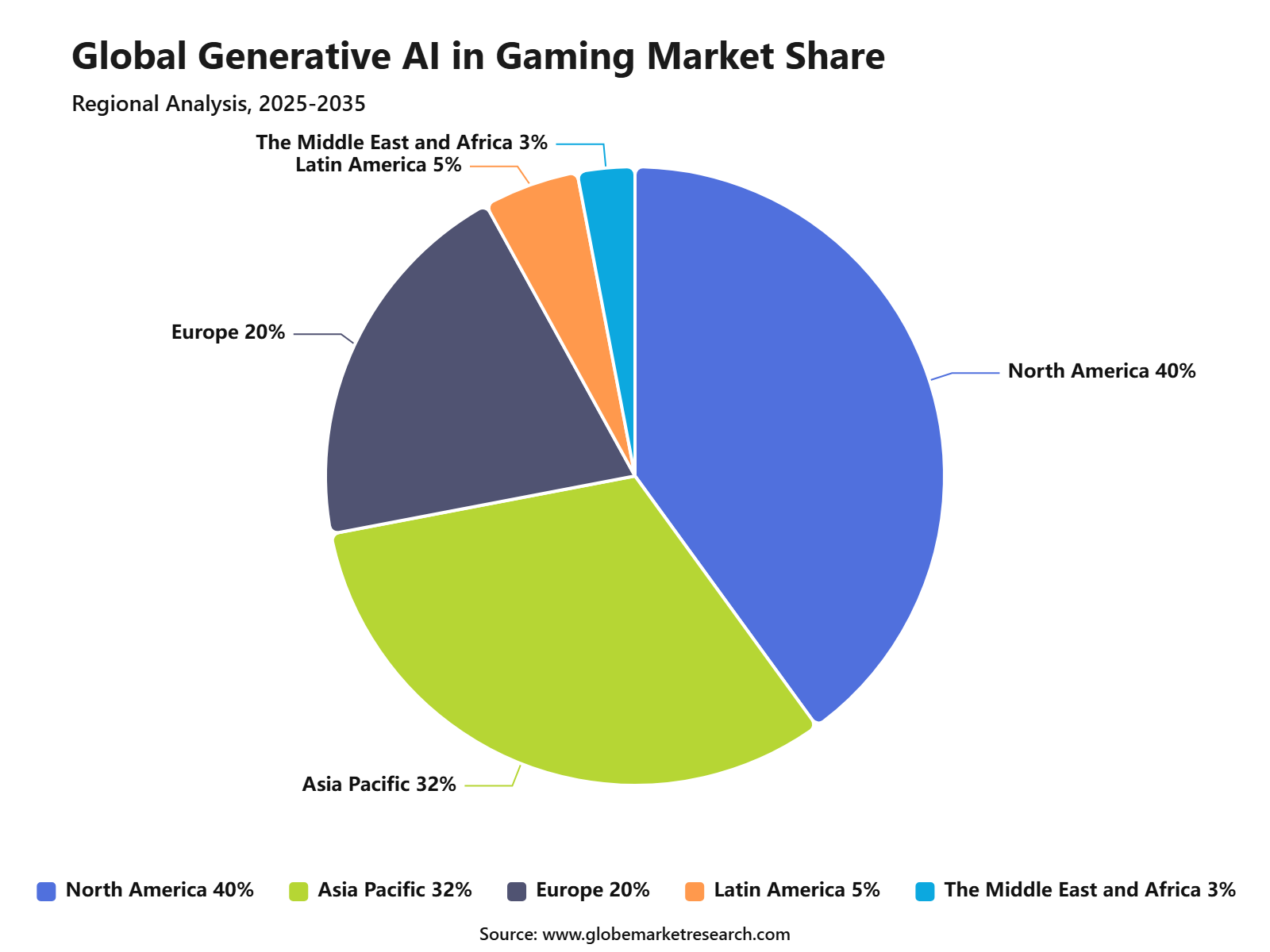

Largest Region | North America, 41.0% Share |

U.S. Market Revenue, 2025 | USD 3.5 Billion |

U.S. CAGR | 25.9% |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

Market Size and Growth Forecast

According to Globe Market Research, the global generative AI in gaming market was valued at USD 10.6 billion in 2025 and is projected to reach USD 106.1 billion by 2035, growing at a 25.9% CAGR. North America accounted for 41% share in 2025, supported by strong game studios, cloud infrastructure, AI model developers, and early adoption of AI-assisted production tools.

Generative AI in gaming refers to AI tools and platforms used to create game assets, characters, dialogues, environments, animations, music, levels, storylines, and adaptive gameplay experiences. Unlike traditional scripted game AI, generative AI can create new content or variations dynamically, helping studios improve speed, creative output, testing, and player personalization.

The market is gaining attention because game development costs are rising, production timelines are becoming longer, and live-service games need frequent content updates. The wider gaming industry also provides a strong base for AI adoption, as global games revenue reached USD 201.6 billion in 2025, crossing the USD 200 billion level for the first time.

Why the Generative AI in Gaming Market Is Growing?

The growth of the generative AI in gaming market can be attributed to faster content creation, lower production cost pressure, and rising use of AI tools by game developers. AI is being used for concept art, character design, code assistance, dialogue generation, localization, testing, player support, and marketing content. Globe Market Research estimates that faster creation of game assets and design concepts adds a +3.2% impact, while rising use of AI tools by game developers adds +2.8%.

Developer adoption is moving from early testing into daily workflows. In 2026, 36% of game industry professionals reported using generative AI tools at work. The most common uses were research and brainstorming at 81%, code assistance at 47%, and prototyping at 35%, showing that AI is mainly being used to support production speed rather than fully replace creative teams. The commercial base is also strong. U.S. consumer spending on video games reached USD 60.7 billion in 2025, up 1.4% from 2024 and the second-highest annual level on record.

Software Remains the Leading Component

Software led the generative AI in gaming market with 67.4% share in 2025. This segment includes AI tools for asset generation, coding support, game testing, animation assistance, dialogue creation, level design, content moderation, and live operations. Software is leading because studios need flexible tools that can fit into existing development workflows. AI-based software can help teams generate early concepts, create asset variations, test gameplay ideas, write code snippets, and support localization.

This is especially useful for studios managing tight production schedules and frequent content updates. The value is strongest when AI improves speed while allowing artists, writers, designers, and engineers to retain creative control. The software opportunity is also supported by game engine integration. Unity’s 2026 game development report used survey input from 300 game developers and proprietary data from nearly 5 million developers using the Unity ecosystem in 2025, showing how engine-level workflows are becoming central to AI adoption.

Machine Learning Leads by Technology

Machine learning accounted for 34.8% share by technology in 2025. It supports player behavior analysis, procedural content generation, NPC behavior, game balancing, recommendation systems, automated testing, and content personalization. This segment is leading because modern games generate large volumes of player, performance, and engagement data.

Machine learning helps developers understand how players behave, where they drop off, which difficulty levels work best, and what content improves retention. This makes it useful not only for creative production but also for live-service operations, monetization planning, and player experience management. Deep learning, natural language processing, computer vision, reinforcement learning, and generative adversarial networks are also gaining relevance. These technologies support dialogue systems, visual asset creation, animation, game testing, dynamic environments, and AI-driven non-player characters.

Game Assets Are the Leading Content Type

Game assets held 31.6% share by content type in 2025. This includes characters, environments, textures, objects, sound effects, visual references, concept art, and animations. The segment is growing because modern games require large volumes of creative content across mobile, PC, console, cloud, and AR or VR platforms. Generative AI can help studios produce early-stage design options faster.

It can create multiple asset variations, support style exploration, reduce repetitive design tasks, and help small teams move from concept to prototype more quickly. However, quality control remains essential. Game assets must match technical standards, art direction, polygon limits, animation requirements, texture quality, engine compatibility, and brand identity. Tools that offer copyright-safe outputs, licensed training data, human review, and style consistency are likely to gain stronger studio trust.

Action Games Lead by Game Type

Action games accounted for 28.9% share in 2025. This segment is supported by demand for fast gameplay, dynamic environments, realistic character movement, combat scenarios, mission variety, and frequent content updates. These games often require large asset libraries and strong testing support. Generative AI can support enemy behavior design, level variation, animation support, mission planning, and gameplay testing.

It can also help developers create different maps, combat scenes, and character interactions faster than traditional manual workflows. The opportunity is strongest where AI supports replay value without reducing quality. Action games depend heavily on player trust, game feel, visual quality, and performance. For this reason, AI-generated content must be reviewed carefully before reaching players.

Mobile Games Remain the Leading Platform

Mobile games led the platform segment with 39.7% share in 2025. The segment is supported by large smartphone access, wide app store distribution, casual gaming behavior, frequent content updates, and strong demand for personalized in-game experiences. Mobile games are well suited for AI-supported personalization because they generate frequent user interaction data.

Developers can use generative AI to improve onboarding, recommend content, tune difficulty, generate ad creatives, create seasonal assets, and support live events. The wider gaming market also supports the platform opportunity. Newzoo reported that mobile outperformed earlier expectations in 2025, while Asia Pacific held 47% of global games revenue and North America held 27%. This supports the role of mobile-first and region-specific AI gaming tools.

Procedural Content Generation Is the Leading Application

Procedural content generation accounted for 35.2% share by application in 2025. This application is used to create levels, maps, quests, environments, missions, items, and gameplay variations at scale. It is becoming important because players expect larger worlds, fresh content, and personalized experiences. Generative AI can help developers produce varied game paths, dynamic missions, adaptive challenges, and replayable environments.

This is especially valuable for open-world games, RPGs, simulation games, live-service games, and cloud gaming platforms. The segment is also linked with production efficiency. Globe Market Research estimates that growth of procedural content generation adds a +2.2% impact, while AI-supported player engagement tools add +1.9%. These tools can support adaptive difficulty, AI NPCs, personalized quests, automated moderation, and real-time content updates.

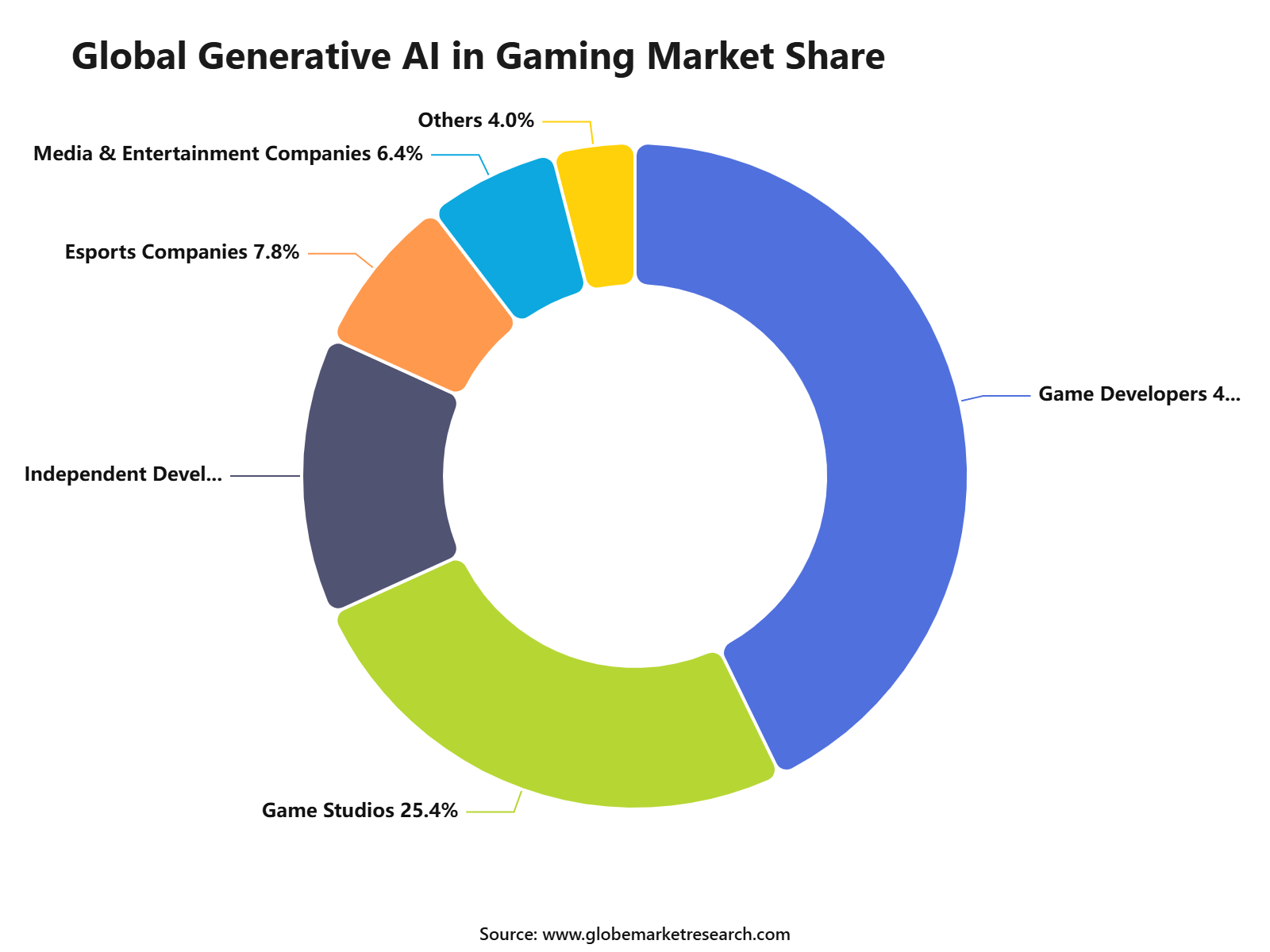

Game Developers Are the Leading End Users

Game developers held 42.8% share by end user in 2025. They are the main users of generative AI because they directly apply the tools across design, coding, asset creation, testing, localization, documentation, and content production. Developers are adopting AI because production cycles are becoming more complex.

Large games require many creative, technical, and quality assurance tasks, while smaller studios need tools that reduce workload and lower entry barriers. AI adoption will depend on trust and workflow fit. Developers are more likely to use tools that improve productivity without weakening creative ownership, intellectual property safety, technical quality, or team morale.

North America Leads the Market

North America held the leading regional position with 41% share in 2025. The region benefits from strong game studios, cloud computing platforms, AI model developers, gaming technology companies, and early use of AI-assisted production tools. The U.S. generative AI in gaming market was valued at approximately USD 3.5 billion in 2025 and is projected to expand at a 25.9% CAGR from 2025 to 2035.

Growth is supported by AI-based game asset creation, procedural content generation, character design, dialogue generation, testing automation, and player experience personalization. Asia Pacific is also an important opportunity area due to large gaming populations in China, Japan, South Korea, India, and Southeast Asia. The region has strong mobile gaming demand, anime-style content production, real-time translation needs, and a large base of independent developers using low-cost AI tools.

Risk Factors and Market Barriers

Copyright and intellectual property concerns are the largest restraint, with an estimated negative impact of -2.4%. Game assets include protected artwork, music, scripts, code, voice, characters, and designs, which makes ownership and licensing highly important. The U.S. Copyright Office has been reviewing AI and copyright issues, including AI-generated works and generative AI training.

For game companies, this creates practical questions around training data, commercial use rights, human authorship, and copyright protection for AI-assisted outputs. Creative resistance is another major barrier, with an estimated negative impact of -2.1%. Developers and gaming communities may reject AI-generated content if it is viewed as low-quality, unethical, or harmful to creative jobs. Inconsistent AI-generated content quality also carries a -1.8% impact because poor outputs can increase review and editing time.

Analyst Perspective

What the Data Is Telling Generative AI Gaming Companies?

From an analyst perspective, the data shows that generative AI in gaming is moving from experimental use to workflow-level adoption. A market value of USD 10.6 billion in 2025 and a projected value of USD 106.1 billion by 2035 indicate strong long-term demand, but growth will favor tools that improve productivity without creating copyright, quality, or trust issues.

The strongest signal is the leadership of software, game assets, mobile games, procedural content generation, and game developers. Software held 67.4% share, game assets held 31.6% share, mobile games captured 39.7% share, procedural content generation accounted for 35.2% share, and game developers held 42.8% share. This shows that adoption is strongest where AI supports production speed and content scale.

What Opportunities Are Emerging?

The biggest opportunity is in AI-assisted production workflows. Studios need faster support for concept art, early prototypes, localization, code assistance, level ideas, character variation, and game testing.

NPC dialogue and adaptive gameplay are also emerging as high-value areas. These use cases can make game worlds more interactive, especially in RPG, simulation, open-world, and live-service games.

Small studios and independent developers may benefit strongly because generative AI can reduce early production barriers. Tools that help create playable prototypes, test game ideas, and support publishing workflows can gain wider adoption.

What Risks Should Companies Be Aware Of?

The main risk is copyright and ownership uncertainty. Studios need to know whether AI-generated assets, scripts, music, code, and character designs can be used commercially without legal exposure.

Creative backlash is another major risk. Many developers and players are concerned that AI may reduce originality, weaken artistic identity, or harm creative jobs. This means disclosure, human review, and responsible positioning will matter.

Quality risk should also be managed carefully. AI outputs may be inconsistent, technically unsuitable, or misaligned with art direction. If the review burden becomes too high, expected productivity gains may weaken.

What Decisions Should Clients Make Next?

Clients should first identify where AI can support production without replacing core creative judgment. Research, brainstorming, prototyping, localization, QA, and asset variation are practical starting points.

Second, studios should create clear AI governance rules. These should cover approved tools, data privacy, copyright checks, human review, disclosure standards, and final approval workflows.

Finally, clients should select vendors based on licensed data, game engine integration, output control, IP protection, security, and workflow compatibility. The best tools should improve production speed while protecting creative quality and commercial rights.

Recent Developments

In June 2026, NVIDIA released RTX Remix 1.5 with RTX IO compression, Smooth Normals, and RTX Remix Skills agents. The update supports AI-assisted modding and faster remastering of classic games.

In 2026, Unity continued to expand Unity AI with in-editor assistance, asset generation, workflow automation, AI Gateway support, and MCP Server integration for game developers. Unity’s MCP Server allows AI tools to access scene hierarchy, code, and project context, helping developers work inside the actual game engine environment.

In March 2025, Amazon Web Services highlighted generative AI-powered game development solutions at GDC 2025, including character and world design support and AI-driven game ad personalization. This indicates growing cloud provider interest in game development workflows.

In 2026, Roblox continued to strengthen its creator ecosystem, with AI tools increasingly positioned around faster content creation, coding support, and creator productivity. This supports the wider shift toward AI-enabled user-generated gaming platforms.

Competitive Landscape

The generative AI in gaming market is competitive, with established game engines, cloud providers, AI model developers, gaming studios, creative software companies, and specialist AI gaming startups competing for adoption. Key companies include NVIDIA Corporation, Unity Software Inc., Epic Games, Electronic Arts, Ubisoft, Roblox Corporation, Microsoft, Sony Interactive Entertainment, Tencent, NetEase, Amazon Web Services, Google, Meta Platforms, Adobe, Stability AI, OpenAI, Inworld AI, Scenario, Convai, Charisma.ai, Ludo.ai, Promethean AI, Latitude, Modulate, and Anything World.

Competition is expected to increase as AI tools become more embedded in game engines, content pipelines, testing platforms, dialogue systems, and live-service operations. Large platforms may benefit from existing developer ecosystems, while specialist startups may win in focused use cases such as NPC behavior, asset generation, moderation, and automated testing.

The strongest companies will be those that combine technical performance with creative trust. Buyers will look for licensed training data, commercial usage rights, strong integration, security, workflow controls, human review, and clear output quality. Market success will depend on more than model capability. Providers must understand game production pipelines, asset standards, engine requirements, localization, platform rules, player expectations, and legal risk. This will separate practical AI gaming tools from generic generative AI platforms.

Conclusion

The generative AI in gaming market is entering a strong growth phase as studios adopt AI for game assets, procedural content generation, character design, dialogue, testing, localization, and player personalization. Growth is being supported by high gaming revenue, rising production complexity, mobile gaming scale, and demand for faster content creation.

Future growth will be led by software platforms, machine learning tools, AI-assisted game assets, procedural content generation, mobile games, dynamic NPC systems, automated testing, and developer-focused workflows. The market outlook remains positive, but adoption will depend on copyright safety, creative acceptance, quality control, and responsible AI governance.